Malaysia Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

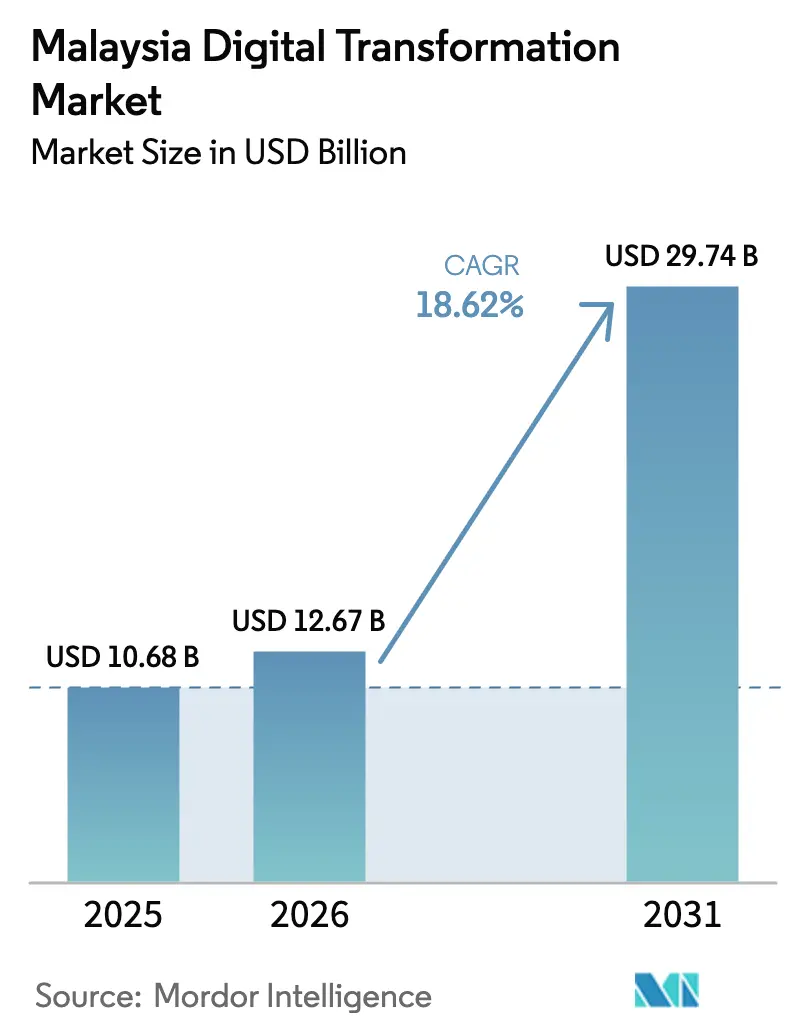

| Base Year Market Size (2025) | USD 10.68 Billion |

| Market Size (2026) | USD 12.67 Billion |

| Market Size (2031) | USD 29.74 Billion |

| Growth Rate (2026 - 2031) | 18.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Digital Transformation Market Analysis by Mordor Intelligence

The Malaysia digital transformation market size was valued at USD 10.68 billion in 2025 and estimated to grow from USD 12.67 billion in 2026 to reach USD 29.74 billion by 2031, at a CAGR of 18.62% during the forecast period (2026-2031). This sustained trajectory reflects the government’s blueprint for a digital-first economy that targets a 25.5% GDP contribution by 2025, backed by hyperscale investments from AWS, Microsoft, and Google that already exceed USD 5 billion.[1]Malaysia Digital Economy Corporation, “Digital Investment Statistics 2024,” mdec.my Rapid 5G coverage, now at 82.4% of the population, reduces latency for cloud and edge workloads, while SME-focused grants under the Malaysia Digital program spur mass adoption of enterprise-grade software. Large enterprises account for most current spending, yet aggressive digital incentives for smaller firms are broadening the addressable base faster than in any prior technology cycle. Competitive intensity remains moderate as global hyperscalers own the infrastructure layer, leaving implementation and localization to domestic integrators that understand data-sovereignty and Sharia compliance requirements.

Key Report Takeaways

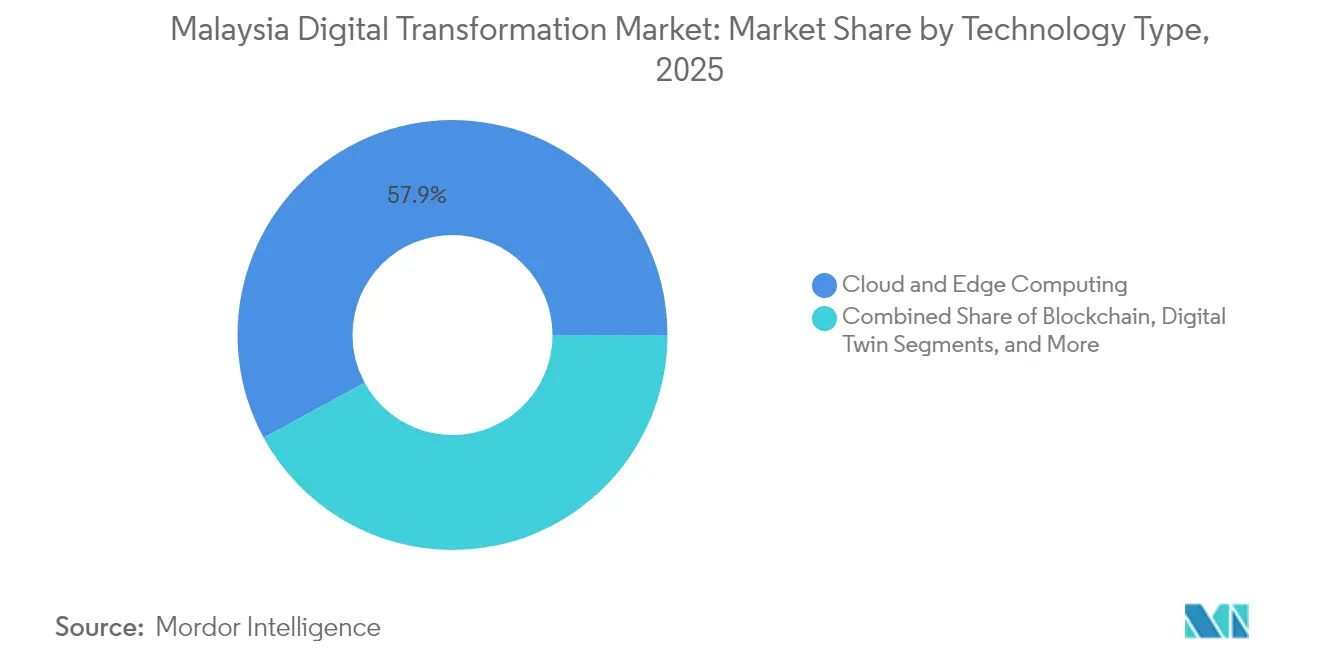

- By technology type, Cloud and Edge Computing led with 57.93% of Malaysia digital transformation market share in 2025, while Generative-AI Platforms are forecast to expand at a 19.12% CAGR through 2031.

- By deployment mode, cloud solutions captured 70.02% of Malaysia digital transformation market size in 2025 and are advancing at a 19.74% CAGR on the back of government cloud-first policies.

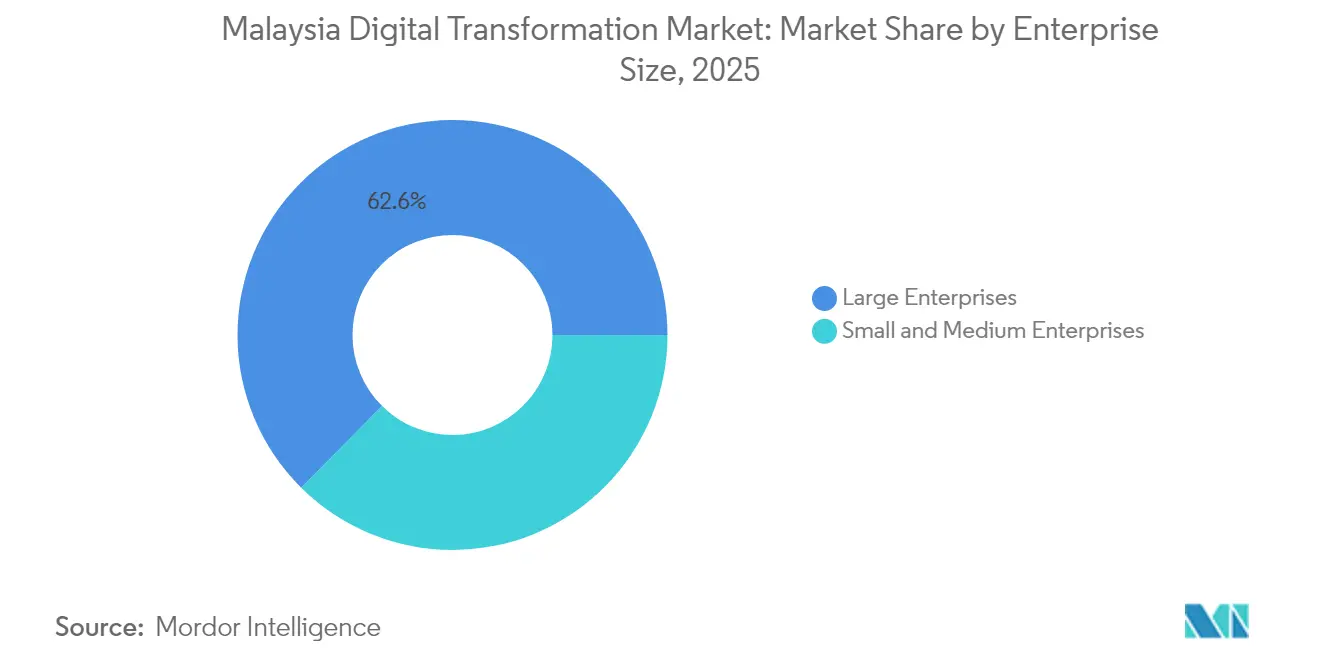

- By enterprise size, large enterprises held 62.58% revenue share in 2025 in the Malaysia digital transformation market; SMEs record the fastest growth at a 19.56% CAGR to 2031, buoyed by grants that fund up to 80% of digital spend.

- By end-user industry, manufacturing commanded 27.61% of Malaysia digital transformation market share in 2025, whereas healthcare is set to post the highest 18.95% CAGR through 2031 as telemedicine scales nationwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market participation spans countries and regions, making Malaysia competition one layer within a larger international field. In its global digital transformation (dx) industry statistics, Mordor Intelligence maps that multi-region structure.

Malaysia Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digital-economy blueprint targeting 25.5% of GDP by 2025 | +4.2% | National, with concentration in Klang Valley and Johor | Medium term (2-4 years) |

| Hyperscale cloud and data-centre FDI surge (AWS, Microsoft, Google) | +3.8% | National, with primary hubs in Selangor and Cyberjaya | Long term (≥ 4 years) |

| Expansion of 5G/mobile broadband driving ubiquitous connectivity | +3.1% | National, with urban-first rollout strategy | Short term (≤ 2 years) |

| SME digital-enablement grants under "Malaysia Digital" initiative | +2.9% | National, with focus on rural and semi-urban areas | Medium term (2-4 years) |

| Johor-Singapore SEZ catalysing cross-border digital trade flows | +1.7% | Regional, concentrated in Johor and cross-border corridors | Long term (≥ 4 years) |

| Islamic-fintech compliance platforms accelerating BFSI digitisation | +1.4% | National, with global Islamic finance market implications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Digital-Economy Blueprint Drives Systematic Transformation

Malaysia’s RM 163.6 billion digital blueprint marks a shift from siloed initiatives toward economy-wide digital integration, aligning policy, funding, and regulatory oversight under a single framework. Clear targets accelerate enterprise adoption because firms can map their technology roadmaps to measurable national milestones. The National AI Office, launched in 2024 with RM 500 million, synchronizes cross-ministry projects and prioritizes Bahasa Malaysia language models, thereby anchoring local providers in public-sector contracts.[2]National AI Office, “AI Malaysia Framework,” ai.gov.my MyDigital ID, already live across 150 agencies, illustrates how unified identity rails reduce duplication and create platform effects for private-sector onboarding. Data-sovereignty clauses, meanwhile, favor domestically hosted clouds, giving homegrown integrators a structural edge even as hyperscalers dominate hardware.

Hyperscale Infrastructure Investment Reshapes Market Dynamics

Google’s USD 2 billion region, Microsoft’s USD 1 billion Azure expansion, and ByteDance’s USD 2.2 billion data center in Johor collectively lower compute latency by up to 50 milliseconds versus Singapore routes, enabling time-sensitive workloads such as digital-twin simulation and streaming analytics. Spillover benefits reach local managed-service providers that supply staffing, migration, and compliance services. The concentration of facilities in Selangor and Cyberjaya forms a “technology corridor” that attracts multinational shared-service centers. Preferential data-flow agreements negotiated under the Johor-Singapore SEZ further extend Malaysia’s catchment across ASEAN, positioning Malaysia's digital transformation market as a regional processing hub.

5G Ubiquity Accelerates Enterprise IoT and Edge Computing

Wholesale 5G under Digital Nasional Berhad now covers 82.4% of Malaysians and introduces a second-network option via U Mobile, dropping enterprise bandwidth costs by 30% compared with 2023 rates. Manufacturers such as Proton report 25% efficiency gains from 5G-enabled digital twins that feed real-time analytics into predictive-maintenance systems.[3]Proton Holdings, “Smart Factory Initiative,” proton.com Cyberjaya’s autonomous-vehicle zone showcases 1-millisecond edge processing, while rural connectivity under the JENDELA program supports precision agriculture pilots that double crop-yield forecasts. Diverse use cases accelerate revenue pools across devices, platforms, and services, reinforcing the virtuous cycle of network upgrades.

SME Digital Grants Create Mass-Market Adoption

The DigitalSME matching grant reimburses up to 80% of qualifying costs on cloud ERP, CRM, and e-commerce rollouts for firms under RM 50 million in revenue, removing the historic capital barrier to modernization. More than 50,000 SMEs onboarded digital tools during 2024, creating a long-tail customer base for integrators and SaaS vendors. The grant conditions favor integrated suites over point solutions, nudging buyers toward comprehensive digital ecosystems. Domestic providers win a significant share because SMEs value localized support and Malay-language interfaces. As adoption broadens, network effects emerge, for example, e-invoicing tools automatically link to banks and tax authorities, multiplying overall productivity benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security skills shortage and wage inflation | -2.8% | National, with acute shortages in Klang Valley and Cyberjaya technology corridors | Short term (≤ 2 years) |

| Data-privacy compliance challenges around PDPA and cross-border flows | -1.9% | National, with cross-border implications for Johor-Singapore SEZ and multinational operations | Medium term (2-4 years) |

| High electricity tariffs and power-capacity limits for data-centres | -1.2% | National, with particular impact on Selangor and Johor hyperscale facilities | Long term (≥ 4 years) |

| Scarcity of Bahasa-Malay AI training datasets for local-language NLP | -0.8% | National, affecting government and SME AI adoption in local language applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Talent Shortage Constrains Enterprise Adoption

Roughly 15,000 cybersecurity roles remained unfilled in 2024, pushing wages up 25% and forcing SMEs to postpone cloud migrations or operate with heightened risk exposures. Although government scholarship programs funnel new graduates into entry-level security operations centers, advanced cloud-security architecture skills still require seasoned experts. Multinationals backfill shortages through Singapore and India talent pools, inflating project budgets and elongating go-live timelines. The mismatch between rapid technology rollout and slower human-capital development creates a drag on near-term revenue realization, particularly for compliance-sensitive sectors such as BFSI and healthcare.

Data-Privacy Compliance Creates Cross-Border Friction

Ambiguities around Personal Data Protection Act amendments have led enterprises to over-invest in local data centers, adding 15-20% to infrastructure outlays versus globally distributed architectures.[4]Personal Data Protection Department, “PDPA Implementation Guide,” pdp.gov.my Financial and healthcare firms must often maintain dual systems, one for Malaysian citizens and another for foreign clients, raising integration complexity. The Johor-Singapore SEZ’s digital-trade framework should eventually harmonize standards, but interim uncertainty defers large, multi-year transformation deals. Vendors that can certify Sharia compliance alongside PDPA adherence hold a competitive edge in winning cross-border Islamic-fintech projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Cloud Infrastructure Dominates While AI Platforms Surge

Cloud and Edge Computing generated 57.93% of Malaysia's digital transformation market revenue in 2025 as government cloud-first mandates aligned with USD 5 billion hyperscale capacity additions. Generative-AI Platforms, although nascent, are scaling at a 19.12% CAGR, thanks to National AI Office subsidies that prioritize Bahasa Malaysia language models. Advanced analytics, IoT, and extended-reality applications deepen cloud workloads, while industrial robotics and digital twins enhance shop-floor efficiency. Gartner-style demand curves show late-cycle technologies, blockchain, and additive manufacturing, finding footholds in Islamic finance record-keeping and aerospace prototyping, respectively.

The Malaysia digital transformation market benefits from vendors bundling AI acceleration and cybersecurity hardening, improving time-to-value for risk-averse buyers. Proton’s 40% throughput gain from collaborative robots demonstrates how AI, edge, and robotics converge. Healthcare providers deploy AI-assisted diagnostics that shrink radiology backlogs, affirming demand for specialized medical-language models. Domestic software firms secure public-sector tenders by embedding data-localization switches, a regulatory advantage that cushions them against global-vendor price competition.

By Deployment Mode: Cloud Dominance Accelerates Hybrid Adoption

Cloud accounted for 70.02% of Malaysia digital transformation market size in 2025 and is on track for a 19.74% CAGR through 2031, propelled by transparent cost-of-ownership benefits and certified data-center regions that satisfy PDPA rules. Hybrid architectures now capture incremental workloads where data sovereignty or low-latency edge processing is critical, especially in Islamic banking and utilities. On-premises environments persist for latency-sensitive SCADA systems but increasingly connect via secure gateways to cloud analytics engines, forming a continuum rather than a binary choice.

The Malaysia digital transformation market registers heightened demand for managed security services that wrap around hybrid stacks, mitigating the skills bottleneck. Telekom Malaysia’s recent cloud-services acquisition added 2,000 enterprise clients, evidencing synergies between network operators and managed-service portfolios. As hyperscalers launch sovereign-cloud options inside Malaysia, the hybrid share may compress post-2028, but near-term growth remains driven by organizations balancing regulatory caution with scalability imperatives.

By Enterprise Size: SME Acceleration Challenges Large-Enterprise Dominance

Large enterprises held 62.58% of spending in 2025, yet SMEs post the headline 19.56% CAGR, demonstrating the equalizing effect of cloud and grant-funded adoption. Multinational manufacturers deploy mature stacks, digital twins, AI analytics and robotics, while SMEs typically start with SaaS ERP and e-commerce. The Malaysia digital transformation market attracts ecosystem players offering verticalized, plug-and-play bundles geared toward fast-track SME onboarding.

Programmatic grants create artificial demand peaks, but sustained transformation will rely on recurring subscription economics and demonstrated ROI. SMEs favor domestic vendors for on-site support and localized interfaces, generating annuity revenue streams for smaller integrators. Meanwhile, large enterprises are renegotiating multi-cloud contracts for better GPU availability to train proprietary models, reflecting a pivot from generic cloud lift-and-shift toward differentiated AI capability.

By End-User Industry: Manufacturing Leadership Meets Healthcare Innovation

Manufacturing delivered 27.61% of 2025 revenue, reflecting entrenched Industry 4.0 roadmaps that leverage robotics, IoT, and advanced analytics. Healthcare is forecast to grow at a 18.95% CAGR, underpinned by telemedicine reimbursement frameworks and AI-enabled diagnostics endorsed by the Ministry of Health. The Malaysia digital transformation industry, therefore, balances brownfield modernization in factories with greenfield digital-health platforms in clinics and hospitals.

Islamic banking digitization accelerates BFSI adoption of blockchain-derived smart contracts tuned for Sharia compliance. Oil, gas and utilities deploy digital-twin models for predictive maintenance, validated by Petronas’ grid-optimization pilot that achieved 15% energy-efficiency gains. Retail and e-commerce invest in omnichannel AI personalization, whereas government smart-city programs standardize urban data layers that become ready-made platforms for private innovation.

Geography Analysis

Klang Valley captures roughly 59.20% of the Malaysia digital transformation market because hyperscale zones in Selangor cluster near government procurement centers in Putrajaya. Cyberjaya’s smart-city sandbox, complete with autonomous-vehicle lanes and 5G street furniture, serves as a national demonstration site that fast-tracks commercial proofs of concept. Johor’s proximity to Singapore, paired with SEZ incentives, channels regional data-processing workloads into newly built data centers, allowing enterprises to arbitrage cost differentials while maintaining millisecond proximity to Singapore financial markets.

Penang emerges as a northern hub leveraging its electronics heritage; here, contract manufacturers overlay IoT sensors onto existing lines, then funnel data into centralized analytics housed in Selangor clouds for global supply-chain synchronization. Sabah and Sarawak, historically underserved, benefit from state-backed 5G rollouts under JENDELA, enabling precision agriculture pilots and remote diagnostics that broaden the Malaysia digital transformation market footprint beyond urban cores.

State-level policy variations diversify demand: Selangor extends tax rebates for cloud CAPEX, Johor subsidizes AI training datasets relevant to cross-border commerce, while Penang co-funds robotics labs in vocational colleges. This multipolar geography mitigates single-city concentration risk and positions Malaysia as a resilient digital gateway for the broader ASEAN region.

Coverage of the digital transformation (dx) market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Middle East, Latin America, and Asia, alongside detailed country-level intelligence for Thailand, China, Israel, Mexico, France, and Oman, each shaped by local operating conditions.

Competitive Landscape

The Malaysia digital transformation market sits at a medium concentration level where hyperscalers dominate IaaS and PaaS layers, but domestic integrators remain indispensable for last-mile customization. Microsoft, AWS and Google routinely partner with local firms such as Fusionex and GHL Systems rather than compete head-to-head, reflecting regulatory preferences for joint go-to-market models. Telekom Malaysia’s acquisition of NetByte underscores telco momentum in enterprise cloud, integrating connectivity, hosting, and managed security under one roof.

Strategic moves pivot toward ecosystem building rather than isolated product launches. Microsoft’s USD 500 million expansion bundles AI research chairs at local universities, seeding talent pipelines that subsequently benefit its Azure adoption. Google Cloud’s second availability zone focuses on compliance certifications that remove residual PDPA objections, widening its addressable base in BFSI. Local champions differentiate via domain expertise: Silverlake Axis for Islamic core banking, Fusionex for Bahasa Malaysia AI, and GHL Systems for e-payments.

M&A and joint ventures are set to intensify as integrators seek scale to absorb rising cybersecurity wage bills. Foreign vendors will continue to localize via equity stakes or long-term contracts, given ownership caps in strategic sectors. Over the forecast horizon, competitive advantage will rest on bundled offerings that address AI, cybersecurity and compliance in a single service-level agreement, shortening procurement cycles for risk-averse buyers.

Malaysia Digital Transformation Industry Leaders

Microsoft Corporation

Google LLC

Telefonaktiebolaget LM Ericsson

International Business Machines Corporation

NTT DATA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft unveiled a sovereign-cloud blueprint co-developed with MDEC to align Azure regions with PDPA localization clauses, including zero-knowledge encryption options for public-sector workloads.

- November 2024: Google Cloud partnered with Petronas to pilot generative-AI models that optimize downstream supply chains, targeting 10% cost reductions in refinery operations.

- September 2024: ByteDance confirmed its USD 2.2 billion Johor data center, cementing Malaysia’s status as TikTok’s SEA content hub.

- August 2024: Microsoft doubled its Malaysia region capacity with an additional USD 500 million, adding dedicated GPUs for enterprise AI workloads.

Malaysia Digital Transformation Market Report Scope

Digital transformation leverages digital technologies such as artificial intelligence and machine learning, extended reality (XR) for industrial applications, IoT, among others to create new business processes or modify existing ones, reshape organizational culture, and enhance customer experiences.

Malaysia digital transformation market is segmented by type (analytics, artificial intelligence, and machine learning, extended reality (XR), Iot, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, and others [digital twin, mobility, and connectivity]), end-user industry (manufacturing, oil, gas and utilities, retail & e-commerce, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector and others), the market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Analytics, Artificial Intelligence and Machine Learning |

| Extended Reality (XR) |

| Internet of Things (IoT) |

| Industrial Robotics |

| Blockchain |

| Additive Manufacturing / 3-D Printing |

| Cyber-security |

| Cloud and Edge Computing |

| Digital Twin |

| Mobility and Connectivity |

| On-premises |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and e-Commerce |

| Transportation and Logistics |

| Healthcare |

| Banking, Financial Services and Insurance (BFSI) |

| Telecom and Information Technology |

| Government and Public Sector |

| Other End-User Industries |

| By Technology Type | Analytics, Artificial Intelligence and Machine Learning |

| Extended Reality (XR) | |

| Internet of Things (IoT) | |

| Industrial Robotics | |

| Blockchain | |

| Additive Manufacturing / 3-D Printing | |

| Cyber-security | |

| Cloud and Edge Computing | |

| Digital Twin | |

| Mobility and Connectivity | |

| By Deployment Mode | On-premises |

| Cloud | |

| Hybrid | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-User Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and e-Commerce | |

| Transportation and Logistics | |

| Healthcare | |

| Banking, Financial Services and Insurance (BFSI) | |

| Telecom and Information Technology | |

| Government and Public Sector | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Malaysia digital transformation market?

The market is valued at USD 12.67 billion in 2026, with a forecast USD 29.74 billion by 2031.

How fast will spending grow on generative-AI platforms?

Generative-AI platforms are projected to expand at a 19.12% CAGR through 2031, the fastest among all technology segments.

Which deployment model holds the largest share?

Cloud deployment led with 70.02% revenue share in 2025 and is growing at a 19.74% CAGR as organizations migrate from on-premises setups.

Why are SMEs accelerating their digital adoption?

SME acceleration stems from government grants that reimburse up to 80% of digital costs, making enterprise-grade tools financially viable.

Which end-user industry is forecast to grow the fastest?

Healthcare is expected to expand at a 18.95% CAGR through 2031, driven by telemedicine and AI-powered diagnostics mandates

Page last updated on: