United States Digital Transformation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

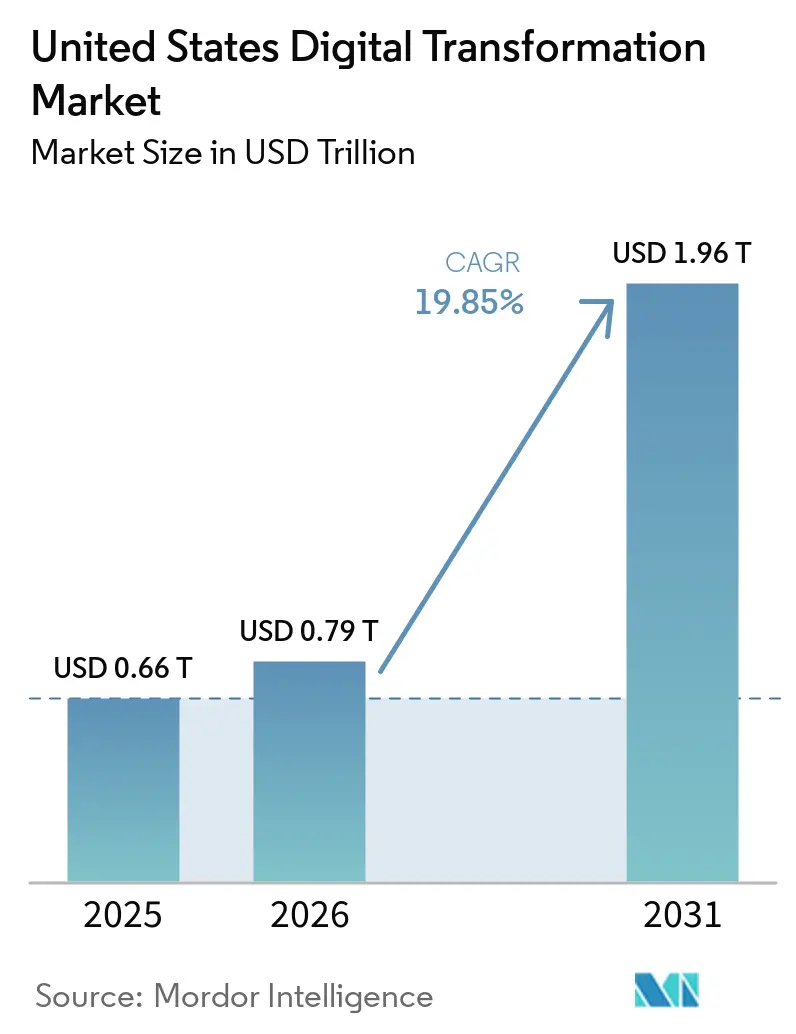

| Base Year Market Size (2025) | USD 0.66 Trillion |

| Market Size (2026) | USD 0.79 Trillion |

| Market Size (2031) | USD 1.96 Trillion |

| Growth Rate (2026 - 2031) | 19.85% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Digital Transformation Market Analysis by Mordor Intelligence

The United States digital transformation market size was valued at USD 0.66 trillion in 2025 and estimated to grow from USD 0.79 trillion in 2026 to reach USD 1.96 trillion by 2031, at a CAGR of 19.85% during the forecast period (2026-2031). Accelerated cloud migration under the FedRAMP 20x program is shortening federal authorization timelines, thereby signaling stronger demand for cloud-ready solutions.[1]General Services Administration, “GSA announces FedRAMP 20x,” gsa.gov Generative AI adoption has jumped from 55% to 78% of firms in one year, elevating analytics investment priorities and opening new growth avenues in personalized customer experiences. Southern states are outpacing national GDP growth, creating fresh regional hubs for technology spending. Healthcare’s push toward digital front-door models and CMS-backed interoperability mandates is channeling fresh capital into patient-facing platforms. Meanwhile, enterprises are grappling with USD 2.41 trillion in annual technical-debt costs that delay integration roadmaps.

Key Report Takeaways

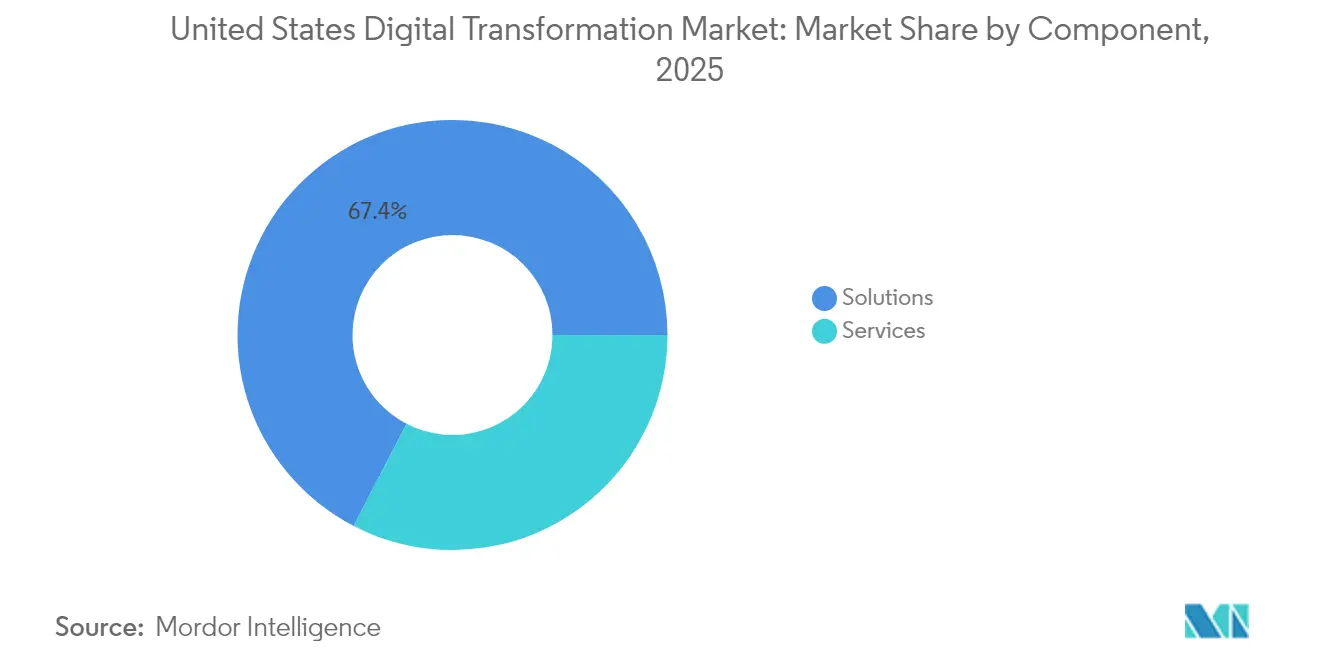

- By component, solutions held 67.40% of the United States digital transformation market share in 2025, while services are forecast to expand at a 20.74% CAGR through 2031.

- By deployment mode, on-premise systems accounted for 50.12% of the United States digital transformation market size in 2025; cloud deployment is advancing at a 20.35% CAGR to 2031.

- By enterprise size, large enterprises commanded 69.20% share of the United States digital transformation market size in 2025, whereas SMEs post the fastest 20.62% CAGR.

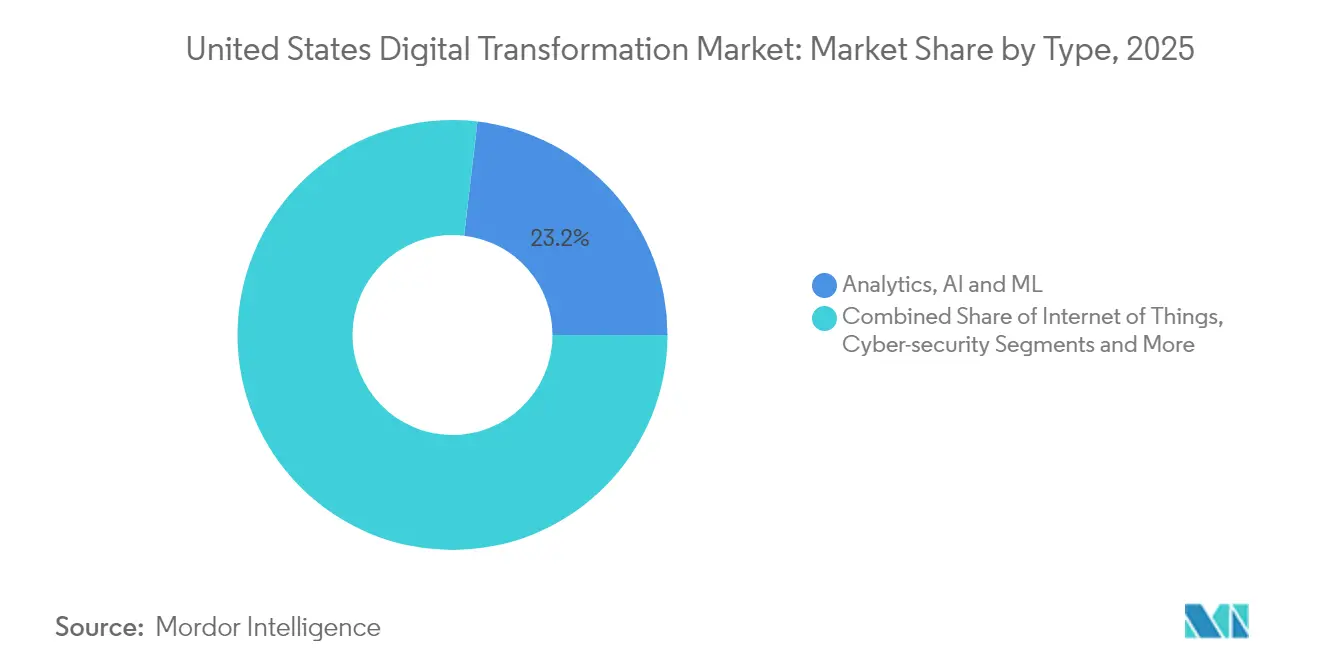

- By technology type, analytics, AI & ML led with 23.15% revenue share in 2025; extended reality is projected to grow at a 25.25% CAGR.

- By end-user industry, BFSI held 20.85% of United States digital transformation market share in 2025; healthcare & life sciences is set to rise at a 21.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's digital transformation (dx) market share coverage captures this comparative structure.

United States Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Cloud-Smart & FedRAMP programs | +3.2% | Northeast and West federal hubs | Medium term (2-4 years) |

| Generative-AI adoption for hyper-personalized CX | +6.5% | West and Northeast early adopters | Short term (≤ 2 years) |

| CMS-funded “digital front door” in healthcare | +2.8% | South and Midwest hospital systems | Medium term (2-4 years) |

| IoT & digital-twin uptake from reshoring wave | +4.1% | Midwest and South manufacturing hubs | Long term (≥ 4 years) |

| ESG data-platform investments under SEC rules | +1.9% | National financial centers | Medium term (2-4 years) |

| 5G SA roll-outs enabling edge computing | +1.8% | Urban cores nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Federal Cloud-Smart & FedRAMP Programs

FedRAMP 20x removes agency-sponsorship for low-impact workloads and automates security reviews, enabling federal cloud migrations to finish 60% faster. Civilian IT outlays allocate USD 74 billion for modernization in 2025, with USD 12.7 billion ring-fenced for cybersecurity. Vendors that pre-certify solutions under the codified FedRAMP Authorization Act gain preferred-supplier status, driving spillover demand across state and local agencies.

Generative-AI Adoption for Hyper-Personalized CX

Seventy-eight percent of U.S. firms now embed generative AI, producing a 3.7× ROI as Fortune 500 groups scale OpenAI-powered chat and design tools. By end-2025, 25% of enterprises plan agent-based deployments that automate frontline tasks. Sector-specific large-language models in healthcare, finance, and retail sustain compliance while boosting service quality.

CMS-Backed “Digital Front Door” Funding in Healthcare

CMS interoperability rules plus Accountable-Care expansion place 53.4% of Medicare patients in coordinated-care models.[2]Centers for Medicare & Medicaid Services, “2025-01-16 MLNC,” cms.gov Hospital-at-Home pilots report lower mortality and lower post-discharge spending, prompting 358 hospitals across 39 states to adopt remote-care platforms. Technology providers that secure HL7 FHIR-compliant data flows win new EHR-integration contracts.

IoT & Digital-Twin Uptake from U.S. Reshoring Wave

Sixty-six percent of manufacturers have drafted reshoring plans and expect USD 4.7 trillion in investments through 2025. Digital twins optimize predictive-maintenance cycles, while 5G-edge convergence supports latency-critical quality-assurance loops. Executives also link reshoring to environmental sustainability objectives, aligning technology roadmaps with ESG scorecards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-level privacy patchwork | -2.1% | California plus other strict states | Medium term (2-4 years) |

| Legacy mainframe lock-in at tier-1 banks | -1.9% | Northeast financial centers | Long term (≥ 4 years) |

| Cloud-security talent shortage | -1.4% | National | Short term (≤ 2 years) |

| Pandemic-era technical debt | -2.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

State-Level Privacy Patchwork (CPRA etc.)

Nineteen states have enacted comprehensive privacy statutes, and enforcement teams in California, Texas, and Virginia elevate compliance risk. Compliance spending rises 30-50% for multi-state businesses, with SMEs bearing higher proportional costs in the absence of a single federal framework.

Legacy Mainframe Lock-in across Tier-1 Banks

More than 60% of bank IT budgets still fund “run-the-bank” workloads, limiting capital for innovation. Migration to cloud-native cores requires phased de-risking strategies—simplifying processes, refactoring code, and layering APIs—while maintaining regulatory resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Solutions in Growth Race

Solutions accounted for a dominant 67.40% of the United States digital transformation market share in 2025, underpinned by enterprise investments in cloud, cybersecurity, and analytics platforms. The services arena, however, is forecast to post a 20.74% CAGR as firms turn to consultancies for integration, AI model tuning, and managed operations. A widening data-science skills gap—cited by 53% of IT leaders—reinforces demand for external expertise.

Demand for continuous optimization is reshaping services portfolios from one-time installs to outcome-based contracts. Providers bundle change-management and AI-governance advisories that accelerate time-to-value. As digital maturity grows, the United States digital transformation market size for services is expected to close the revenue gap with solutions by 2031.

By Deployment Mode: Cloud Adoption Accelerates Despite On-Premise Dominance

On-premise platforms retained 50.12% of the United States digital transformation market size in 2025, reflecting strict data-sovereignty rules in BFSI and healthcare. Cloud solutions, climbing at a 20.35% CAGR, benefit from FedRAMP streamlining and hybrid-cloud blueprints. Oracle-Google interconnects let firms run OCI databases alongside Google Analytics without cross-cloud fees.

Hybrid architectures combine on-premise control with elastic public-cloud compute, mitigating latency and compliance concerns while supporting AI workloads. By 2031, equilibrium between deployment models is plausible as cloud security hardens and mission-critical workloads gradually exit legacy stacks.

By Enterprise Size: SMEs Closing the Digital Divide

Large corporations captured 69.20% of the United States digital transformation market share in 2025, thanks to deeper budgets and dedicated innovation teams. Yet SMEs expand at a rapid 20.62% CAGR as pay-as-you-go cloud and industry-specific SaaS lower entry costs. CMS-aligned healthcare clouds, for instance, are on track for 70% adoption by mid-decade.

SMEs use targeted pilots—customer service bots, workflow automation—to generate quick returns before scaling. Vendor ecosystems now offer turnkey blueprints and financing bundles that lighten change-management burdens. This trend narrows the digital maturity gap, though skills shortages and compliance complexity still temper SME velocity.

By Type: Extended Reality Emerges as Growth Leader

Analytics, AI & ML tools held 23.15% of revenue in 2025, anchoring insight-driven operating models. Generative-AI platforms such as Kore.ai’s GALE now supply low-code toolkits that democratize advanced model deployment.

Extended reality’s 25.25% CAGR reflects new 5G-enabled industrial and clinical use cases. Surgeons rehearse procedures in immersive simulators, and factory technicians rely on AR overlays for real-time guidance. Cybersecurity spending keeps pace as healthcare alone logged 809 breach incidents in 2023, intensifying demand for zero-trust frameworks. Edge computing rounds out the stack with low-latency processing for connected devices.

By End-User Industry: Healthcare Accelerates Digital Adoption

BFSI-led spending with a 20.85% share of the United States digital transformation market in 2025, channeling funds into core-bank modernization, embedded finance, and fraud analytics. Fintech challengers force incumbents to compress release cycles and elevate mobile-banking UX.

Healthcare & life sciences is projected to climb at a 21.78% CAGR, propelled by CMS incentives and AI-first diagnostics. NVIDIA’s March 2025 release of turnkey healthcare microservices showcases the vendor's focus on domain-specific AI stacks. Manufacturing follows closely as reshoring and smart-factory agendas expand IoT footprints. Government departments leverage FedRAMP-cleared clouds to digitize citizen services.

Geography Analysis

The Northeast remains a nucleus for finance and biotech transformation, with New York and Boston sustaining heavy AI and analytics outlays. Seventy-seven percent of regional health executives list AI as a top investment vector. Slower population growth moderates consumer-driven projects, yet corporate demand keeps digital budgets intact.

Southern states exhibit the fastest economic momentum, with a 4.3% GDP rise from 2020-2024 and 78% of post-pandemic job creation.Texas and Florida attract hyperscalers and start-ups through tax incentives and lower living costs. Consumer-spending growth of 7.4% underpins high adoption of mobile commerce and streaming platforms. Infrastructure gaps in rural pockets and digital skills shortages remain policy priorities.

The Midwest balances manufacturing heritage with cautious optimism: 71% of middle-market leaders hold a positive firm-level outlook, yet only 40% are bullish on the wider economy. Reindustrialization agendas stimulate IoT, AI, and predictive-maintenance deployments. The West anchors national innovation, but semiconductor plants face aging-workforce issues as 55% of employees exceed 45 years . Silicon Valley’s AI breakthroughs diffuse nationwide, sustaining the technology flywheel for the United States digital transformation market.

Analysis of the digital transformation (dx) market by Mordor Intelligence spans multiple other regional evaluations across Africa, Middle East, and Latin America, supported by country-level insights for Colombia, Canada, Nigeria, Qatar, Japan, and India, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The market is semi-consolidated. Amazon Web Services controls 32% of U.S. cloud IaaS, trailed by Microsoft Azure at 23% and Google Cloud at 10%. Hyperscalers intensify partnering to penetrate regulated sectors; Oracle’s multi-cloud deals let customers co-locate OCI databases on AWS or Google for latency and license advantages.

IBM, ServiceNow, and Salesforce pursue vertical-solution depth, layering AI and low-code capabilities to win domain footprints. System integrators such as Accenture extend reach through design-studio acquisitions that speed digital-product rollout—e.g., the January 2024 Work & Co purchase.

Specialist AI vendors gain share in niches like conversational commerce, forcing incumbents to accelerate roadmap cycles or acquire to plug feature gaps. Pricing innovation—commitment-based cloud credits, outcome-linked services—emerges as a weapon in enterprise renewals. Ecosystem strategies now include co-innovation sandboxes where customers test multi-vendor stacks before production cutover.

United States Digital Transformation Industry Leaders

Google LLC (Alphabet Inc.)

IBM Corporation

Microsoft Corporation

Oracle Corporation

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Aramco signed USD 90 billion of MoUs with U.S. tech leaders, pairing AWS cloud adoption with NVIDIA AI infrastructure and Qualcomm 5G to digitize upstream operations.

- May 2025: SolarWinds launched SolarWinds AI, embedding privacy-by-design controls to help IT teams streamline multi-cloud observability.

- April 2025: Cloud Software Group committed USD 1.65 billion to Microsoft Azure and co-developed Citrix-enhanced AI workspace tools.

- April 2025: Informatica extended Master Data Management to Google BigQuery, quickening trusted-data pipelines for generative-AI workloads.

United States Digital Transformation Market Report Scope

Digital transformation is the process of incorporating digital technologies such as analytics, artificial intelligence, machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, and others (digital Twin, mobility, and connectivity) in various end-user industries.

The US digital transformation market is segmented by type (analytics, artificial intelligence, and machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, and others [digital Twin, mobility, and connectivity]) and end-user industry [manufacturing, oil, gas and utilities, retail and e-commerce, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, and other end-user industries (education, media & entertainment, environment etc)]. The market sizes and forecasts are provided in terms of value in USD for all the above-mentioned segments.

| Solutions |

| Services |

| On-premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Mid-sized Enterprises (SMEs) |

| Analytics, AI and ML |

| Internet of Things (IoT) |

| Cyber-security |

| Cloud and Edge Computing |

| Extended Reality (XR) |

| Blockchain |

| Industrial Robotics |

| Additive Manufacturing / 3-D Printing |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and E-commerce |

| Transportation and Logistics |

| Oil, Gas and Utilities |

| Telecom and IT Services |

| Government and Public Sector |

| Others |

| Northeast |

| Midwest |

| South |

| West |

| By Component | Solutions |

| Services | |

| By Deployment Mode | On-premise |

| Cloud | |

| Hybrid | |

| By Enterprise Size | Large Enterprises |

| Small and Mid-sized Enterprises (SMEs) | |

| By Type | Analytics, AI and ML |

| Internet of Things (IoT) | |

| Cyber-security | |

| Cloud and Edge Computing | |

| Extended Reality (XR) | |

| Blockchain | |

| Industrial Robotics | |

| Additive Manufacturing / 3-D Printing | |

| By End-User Industry | BFSI |

| Healthcare and Life Sciences | |

| Manufacturing | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Oil, Gas and Utilities | |

| Telecom and IT Services | |

| Government and Public Sector | |

| Others | |

| By Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current value of the United States digital transformation market?

The market is valued at USD 0.79 trillion in 2026 and is forecast to reach USD 1.96 trillion by 2031

Which segment is growing fastest within the United States digital transformation market?

Extended reality technologies post the highest 2026-2031 CAGR at 25.25%, driven by 5G-enabled industrial and healthcare use cases.

How are federal initiatives influencing adoption?

FedRAMP 20x accelerates cloud approvals, cutting authorization time by 60% and spurring uptake among agencies and their suppliers.

Why are SMEs gaining momentum?

Consumption-based cloud pricing, industry-specific SaaS, and turnkey change-management services allow SMEs to pursue targeted digital projects and grow at a 20.62% CAGR.

What regulatory challenges may slow progress?

A patchwork of 19 state privacy laws elevates compliance costs by up to 50%, particularly for firms operating across multiple jurisdictions.

Which regions are attracting the most new investments?

Southern states lead due to 4.3% GDP growth and a 10% jump in job creation since 2020, attracting both technology companies and skilled talent.

Page last updated on: