Digital Transformation (DX) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

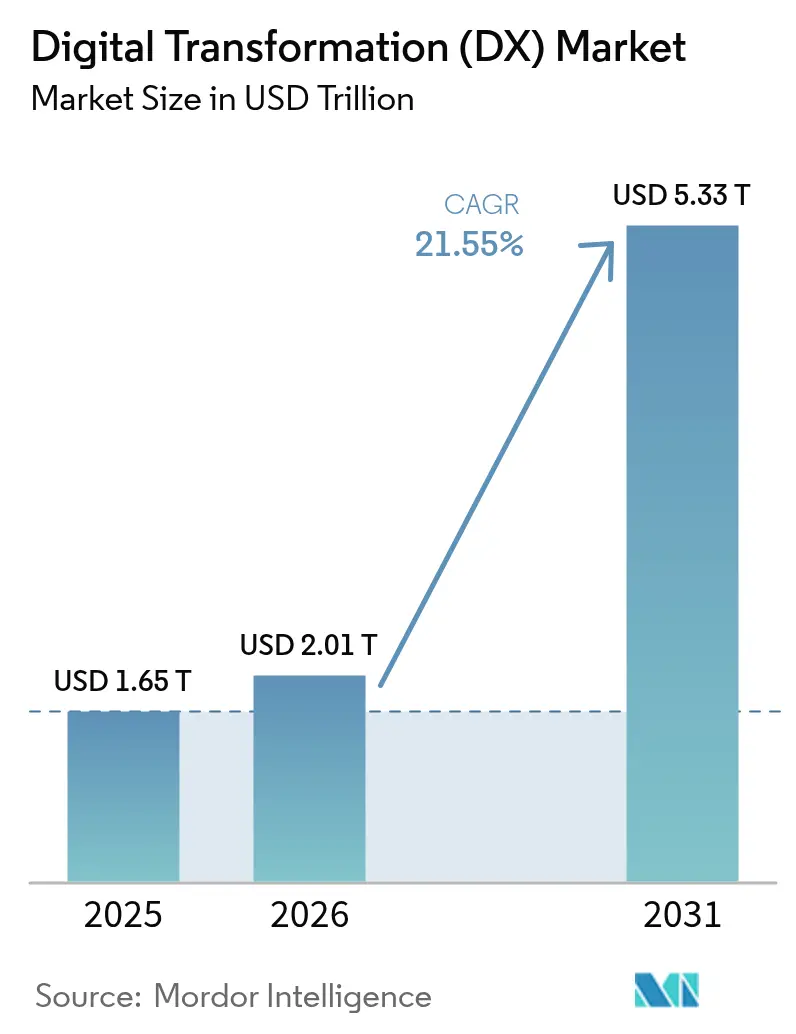

| Market Size (2026) | USD 2.01 Trillion |

| Market Size (2031) | USD 5.33 Trillion |

| Growth Rate (2026 - 2031) | 21.55% CAGR |

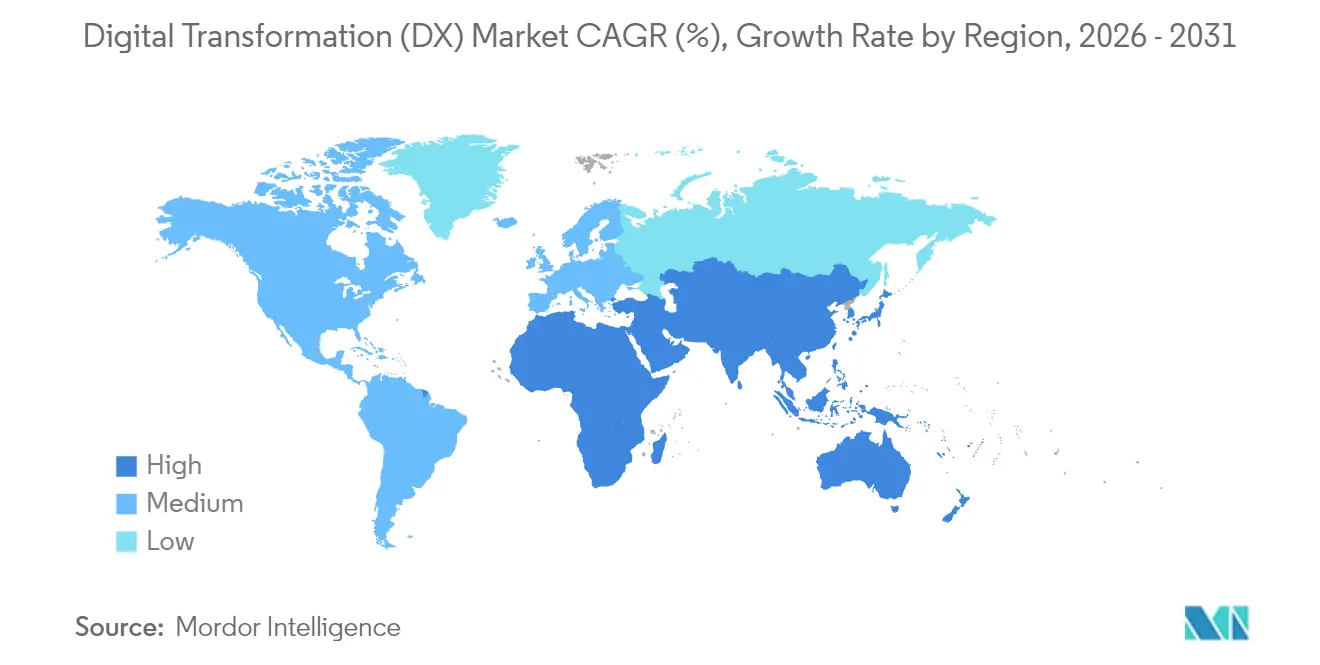

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Transformation (DX) Market Analysis by Mordor Intelligence

The digital transformation market size is expected to grow from USD 1.65 trillion in 2025 to USD 2.01 trillion in 2026 and is forecast to reach USD 5.33 trillion by 2031 at 21.55% CAGR over 2026-2031. Strong growth stems from enterprise AI adoption, cloud-first spending priorities, and regulatory mandates that compel organizations to digitize operations. Sovereign-AI policies push companies to localize computing, while 5G networks open real-time use cases in manufacturing and healthcare. Low-code platforms extend application development beyond IT departments, and ESG reporting rules accelerate data-driven compliance investments. Incremental modernization strategies gain favor as enterprises balance innovation goals with legacy-system cost pressures. Competitive intensity remains moderate because businesses pursue multi-vendor cloud and AI strategies to avoid lock-in, yet hyperscale-provider capital expenditure is redefining scale economics in the digital transformation market.

Key Report Takeaways

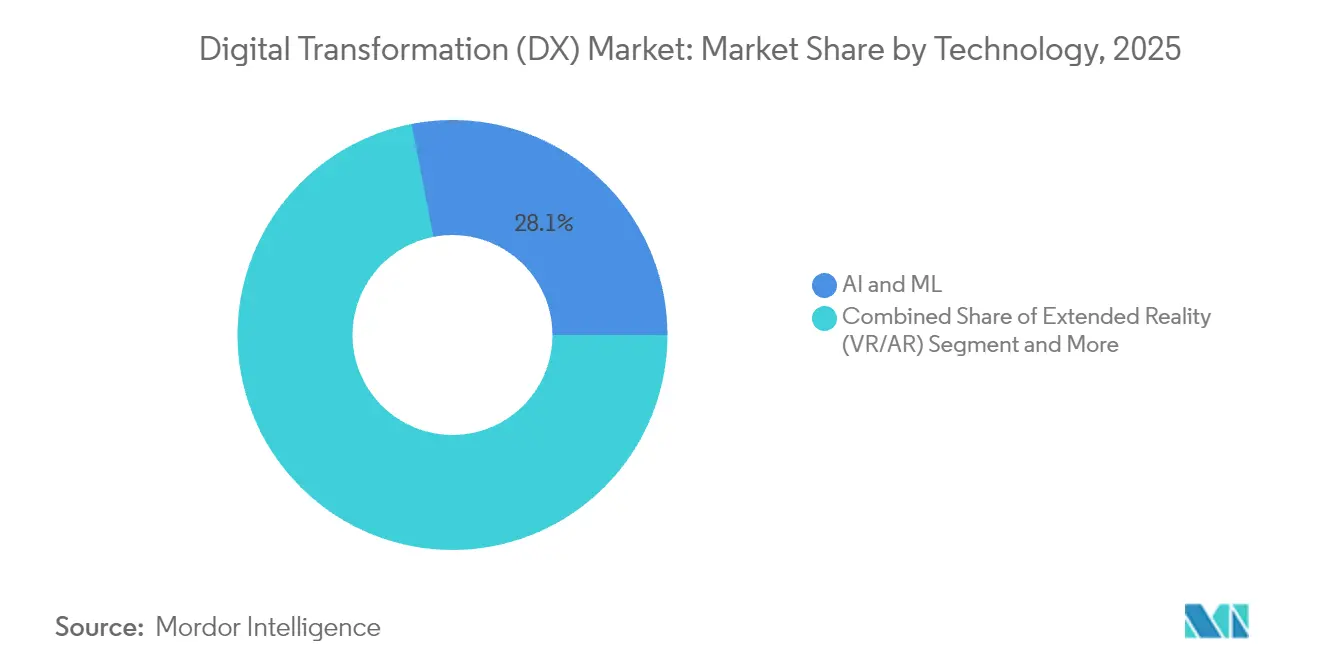

- By technology, AI and ML held 28.05% of digital transformation market share in 2025; these solutions are forecast to grow at 23.9% CAGR through 2031.

- By deployment model, cloud-based implementations commanded 62.65% share of the digital transformation market size in 2025, and are expanding at 22.1% CAGR to 2031.

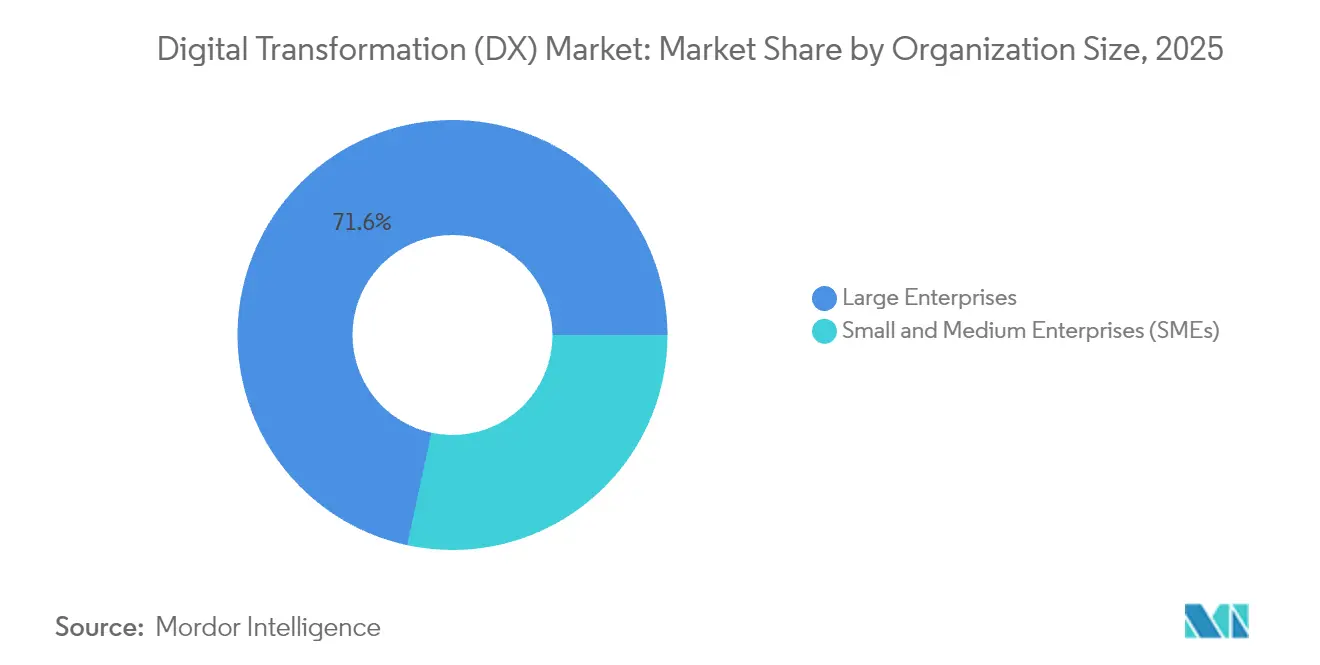

- By organization size, large enterprises captured 71.62% of digital transformation market share in 2025, while still delivering 22.7% CAGR through 2031.

- By industry vertical, healthcare is the fastest-growing segment at 21.6% CAGR, whereas BFSI retained the largest revenue contribution at 23.42% in 2025.

- By geography, North America led with 31.95% share in 2025; Asia-Pacific is the fastest-growing region at 22.0% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Transformation (DX) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first enterprise IT spending boom | +4.2% | Global, with North America and EU leading | Medium term (2-4 years) |

| Rising AI/ML integration across business functions | +5.8% | Global, with Asia-Pacific and North America core | Short term (≤ 2 years) |

| 5G-enabled real-time data use-cases | +3.1% | Asia-Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Mandatory ESG reporting digitisation | +2.4% | EU leading, expanding to North America and Asia-Pacific | Long term (≥ 4 years) |

| Digital-sovereignty public-sector funding waves | +3.7% | EU and Asia-Pacific core, selective North America adoption | Long term (≥ 4 years) |

| Low-code / no-code platforms democratising DX | +2.1% | Global, with enterprise adoption in North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-first enterprise IT spending boom

Organizations are reallocating budgets from on-premise hardware toward cloud-native platforms that support AI workloads and hybrid work models. For example, Amazon Web Services resolved more than 1 million internal developer questions with its AI assistant Amazon Q, saving 450,000 hours of manual effort. [1]Swami Sivasubramanian, “Amazon Q Boosts Developer Productivity,” About Amazon, aboutamazon.comCloud economics shorten procurement cycles and shift spending from capital to operating budgets, allowing faster experimentation. Strategic deals, such as Microsoft’s partnership with Coca-Cola, show how generative-AI services ride atop scalable cloud foundations. As enterprises view cloud infrastructure as essential, vendors expand regional data centers to comply with sovereign-data rules.

Rising AI/ML integration across business functions

AI moves from pilots to production at scale. Goldman Sachs rolled out AI assistants across multiple departments, and UnitedHealth Group manages more than 1,000 AI use cases that automate claims and clinical decisions. Defense, industrial, and retail leaders replicate the pattern, embedding generative models in design, maintenance, and customer-experience workflows. Workforce upskilling and data-governance frameworks mature in tandem, making AI a core competency rather than an experimental add-on.

5G-enabled real-time data use-cases

Low-latency 5G connectivity unlocks applications that were impractical on 4G networks. Mercedes-Benz deploys private 5G to support predictive maintenance on assembly lines. Remote patient monitoring and telemedicine rely on high-definition video streams delivered over 5G links, expanding healthcare access in rural regions. Mining, agriculture, and logistics operators roll out 5G IoT sensors that feed real-time analytics engines, improving safety and asset utilization.

Mandatory ESG reporting digitisation

The EU’s Corporate Sustainability Due Diligence Directive requires Scope 3 emissions tracking, prompting companies to adopt blockchain-enabled traceability and AI analytics. Renault’s XCEED platform, built with IBM, processes 500 compliance transactions per second.[2]Ginni Rometty, “Renault and IBM Launch XCEED,” IBM Newsroom, ibm.com Investor scrutiny on sustainability disclosures escalates, turning ESG digitisation into a board-level imperative rather than a tick-box exercise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy technical-debt lock-ins | -3.8% | Global, with higher impact in North America and EU | Medium term (2-4 years) |

| Cyber-talent scarcity and wage inflation | -2.9% | Global, with acute shortage in North America and Asia-Pacific | Short term (≤ 2 years) |

| Digital-identity regulatory fragmentation | -1.6% | EU leading, expanding to global markets | Long term (≥ 4 years) |

| Scope-3 data-quality gaps for ESG audits | -1.2% | Global, with stricter requirements in EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy technical-debt lock-ins

Enterprises still devote up to 80% of IT budgets to maintain decades-old systems, reducing funds for innovation. ServiceNow found that aging applications cost USD 40,000 annually per system and drain 17 employee hours weekly.[3]Bill McDermott, “Legacy Systems Cost Time and Money,” ServiceNow Press, servicenow.com Government agencies illustrate the problem, spending the majority of their USD 100 billion IT outlay on legacy assets. The resulting technical debt inflates cybersecurity risk because outdated software lacks modern controls.

Cyber-talent scarcity and wage inflation

A global shortfall of 3.4 million cybersecurity specialists drives salaries to USD 138,500–585,000 for senior roles in the United States. Similar shortages in Singapore push analyst salaries above USD 121,500. Small businesses struggle to staff security programs, forcing reliance on managed service providers, while large enterprises deploy AI-driven security automation to mitigate human-resource gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: AI and ML spearhead enterprise adoption

AI and ML claimed 28.05% of digital transformation market share in 2025, and the segment is expected to grow at 23.9% CAGR, reinforcing that data-driven automation is a strategic differentiator. This portion of the digital transformation market size is fueled by enterprises scaling chatbots, recommendation engines, and predictive-maintenance models. Production deployments at Goldman Sachs and Lockheed Martin exemplify the shift from pilots to mission-critical systems. Extended-Reality tools deliver 275% training-retention gains for industrial employees, while blockchain solutions such as Walmart’s food-traceability network cut provenance checks from 7 days to 2.2 seconds.

A parallel wave of edge-computing clusters processes data near sensors to avoid cloud-latency penalties. Industrial robotics synchronized with digital twins allow continuous process optimization in automotive and electronics plants. Additive-manufacturing lines use real-time prints of tooling components to shrink downtime. Together these technologies deepen the digital transformation market penetration across heavy industries.

By Deployment Model: cloud dominance accelerates

Cloud solutions owned 62.65% of digital transformation market share in 2025 and will expand at 22.1% CAGR through 2031. This share of the digital transformation market size correlates with hyperscalers’ multi-billion-dollar data-center builds. AWS’s Project Rainier clusters Trainium 2 chips into the world’s most powerful AI training computer. Microsoft’s USD 80 billion infrastructure spend underscores escalating investment cycles. Enterprises retain on-premises nodes for regulated workloads, yet hybrid architectures flourish; Oracle’s pact with Google Cloud allows bidirectional low-latency links with no egress fees.

Cloud economics also attract small businesses that lack capital budgets for servers. Pay-as-you-go models align costs with usage, and regional availability zones satisfy data-residency regulations. Over time, platform lock-in concerns lead many firms to distribute microservices across multiple clouds, creating demand for cross-plane orchestration tools.

By Organization Size: large enterprises drive adoption

Large organizations held 71.62% of digital transformation market share in 2025 and still register 22.7% CAGR. Unilever’s “operations metaverse” digitally mirrors its global factories and supply chain, enabling continuous optimization. These resources allow parallel digital-transformation workstreams in finance, HR, manufacturing, and marketing. They also foster multi-vendor procurement strategies, reducing dependence on single platforms and spurring competitive pricing.

Small and medium enterprises catch up through low-code systems and cloud SaaS that obviate upfront hardware outlays. Yet cybersecurity staffing gaps and legacy data silos slow their progress. Collective purchasing consortiums and managed services emerge to address cost and skills hurdles for the SME cohort.

By Industry Vertical: healthcare races ahead

Healthcare is growing fastest at 21.6% CAGR as digital health-record mandates and telemedicine adoption widen. Partners HealthCare saved USD 10 million and cut readmissions 44% by integrating IoT devices with AI analytics. Pharmaceutical firms deploy machine learning for target identification and trial-data cleansing, shortening drug-discovery timelines. Medical-device makers integrate sensors for continuous patient monitoring, while hospitals employ AI chatbots to triage inquiries.

BFSI remains the largest revenue contributor at 23.42% share in 2025, upgrading core banking, fraud analytics, and digital-wallet ecosystems. Manufacturing leans on digital twins and predictive-maintenance AI to cut downtime. Retail chains harness computer-vision and edge-compute for shelf monitoring and personalized offers. Energy utilities connect smart meters to IoT platforms that balance grid loads, and government agencies roll out national digital-ID services.

Geography Analysis

North America secured 31.95% of digital transformation market share in 2025, anchored by deep venture capital pools and proximity to hyperscale-cloud headquarters. Texas alone hosts a USD 500 billion data-center expansion featuring NVIDIA supercomputers, plus Texas Instruments’ USD 30 billion chip plant that adds thousands of tech jobs. Federal and state agencies adopt AI assistants like “Humphrey” to automate administrative tasks, further boosting demand. Cross-border initiatives under USMCA support manufacturing digitisation throughout Canada and Mexico.

Asia-Pacific delivers the fastest growth at 22.0% CAGR due to extensive government infrastructure programs and mobile-first consumer behavior. Digital wallets account for nearly 70% of e-commerce checkouts, highlighting the region’s leapfrog adoption curves. India, Japan, and South Korea each articulate national AI strategies, while Australia’s Queensland earmarked AUD 1.2 billion (USD 800 million) for sovereign-cloud services. Combined, these moves expand the addressable digital transformation market.

Europe emphasizes digital sovereignty under eIDAS 2.0, mandating universal acceptance of European Digital Identity Wallets by 2027. Germany’s EuroStack program predicts EUR 300 billion investment to localize compute stacks by 2035. Schleswig-Holstein’s migration away from proprietary software shows practical implementation of sovereignty ideals. South America and the Middle East and Africa trail the leading regions but experience rising foreign investment in fiber backbones, cloud regions, and 5G rollouts, unlocking new service opportunities.

Mordor Intelligence provides coverage of the digital transformation (dx) market across other key regional markets, including Asia, Europe, North America, Africa, Middle East, and Latin America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Thailand, Spain, Canada, and Nigeria incorporating local coverage and market participation, as required.

Regulatory Landscape

Digital transformation programs are increasingly shaped by purpose-built national frameworks and supranational rulebooks that govern cloud, AI, identity, and critical-infrastructure modernization. Vietnam ratified a Law on Digital Transformation in December 2025, with an effective date of July 1, 2026. The law creates a basis for digital government and the digital economy alongside national technical standards, which increases compliance requirements for interoperability, data handling, and public-sector digitization. In the EU, the AI Act regulatory framework adds governance and transparency obligations, with transparency rules scheduled for implementation in August 2026, and the European Commission advanced a Digital Omnibus proposal (COM(2025)837) aimed at simplifying and aligning compliance across major digital regulations.

Public-sector oversight and infrastructure-enablement measures also influence DX execution models and procurement. Portugal issued Decree-Law No. 85/2026 in April 2026 to establish the State Simplification and Technology Network, including prior authorization for government IT projects exceeding EUR 2 million, reinforcing centralized control over large digital programs. In the United States, a July 2025 directive to accelerate federal permitting for high-voltage transmission and AI-integrated data center infrastructure supports compute-heavy modernization. Spectrum and broadband policy actions, including the release of 800 MHz of spectrum for commercial mobile services under Public Law 119-21, also affect 5G-enabled real-time data use cases that enterprises incorporate into DX roadmaps.

Value Chain Analysis

The DX value chain spans infrastructure and platforms (hyperscale and sovereign cloud regions, networks including 5G, edge compute, and data centers), core software layers (AI/ML tooling, data platforms, cybersecurity, low-code/no-code, and integration middleware), and downstream delivery (systems integrators, managed services, and vertical solution providers) that operationalize transformation programs across BFSI, healthcare, manufacturing, and government. Demand is shaped by multi-vendor cloud and AI strategies and by regulated workload requirements that keep hybrid and on-premises nodes relevant, while large enterprises continue to run complex modernization programs with multi-year portfolios across applications, data, and operating models.

Upstream constraints increasingly sit in the physical and operational supply chain for AI and cloud infrastructure rather than in software availability. Through Q1 2026, shortages were reported across multiple infrastructure inputs such as power components, optics, thermal infrastructure, helium, and substrate materials, with lead times reaching as long as 128 weeks. These gaps can delay data center and network build-outs and shift DX sequencing toward modernization, data readiness, and security hardening. Service providers and enterprises respond by redesigning architectures for resilience, including more distributed edge-to-cloud patterns, and by increasing reliance on platform ecosystems and managed services to offset cyber-talent scarcity and rising operational complexity.

Competitive Landscape

Competition remains moderate because no single vendor exceeds one-third of total revenue, yet hyperscalers wield scale advantages. Microsoft links its USD 80 billion capex plan with co-innovation agreements at Coca-Cola, Siemens, and BlackRock. AWS counters through Project Rainier and a USD 230 million accelerator fund for AI startups that funnel workloads onto its services. Google Cloud lures senior executives from rivals to expand its AI business unit and champions open-source security tooling.

Specialist AI vendors and low-code providers attack niches the giants overlook. OutSystems, Mendix, and Retool enable domain experts to build apps with minimal coding, a shift that could reduce enterprise reliance on large-vendor professional-service teams. Intellectual property filings in generative AI accelerate as firms race to claim defensive moats. Meanwhile, multi-cloud orchestration startups compete to harmonize workloads across AWS, Azure, Google, and Oracle infrastructure.

Regulated industries complicate competitive dynamics by demanding in-country hosting, which encourages regional cloud alliances and sovereign-stack offerings. Consequently, market leaders augment portfolios with compliance toolkits and local partnerships, exemplified by Oracle’s collaboration with Google Cloud to meet data-residency rules in financial services.

Digital Transformation (DX) Industry Leaders

Accenture PLC

Google LLC (alphabet Inc.)

Siemens AG

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Agentic AI and autonomous operations create a clear whitespace where enterprises look for packaged approaches that combine cloud platforms, governance, and implementation capacity to move from pilots to production at scale. Accenture and Google Cloud expanded their partnership in April 2026 with the Gemini Enterprise Acceleration Program, reflecting demand for specialized AI agents that can run within enterprise controls. IBM and Google Cloud also announced a new Google Cloud Practice in June 2026 to modernize core systems and scale AI delivery. Together, these moves indicate a shift in buying criteria toward reusable architectures, controllable agent frameworks, and cross-vendor delivery models that reduce integration friction and shorten time-to-value across functions such as customer experience, finance, and IT operations.

Telecom and digital infrastructure modernization is another opportunity zone because it connects AI workloads and edge use cases to enterprise digitization through standardized architectures and new capacity investments. TM Forum members launched an AI-native Open Digital Architecture roadmap for autonomous telecoms in June 2026, and e& aligned with TM Forum on a blueprint for autonomous networks, supporting vendor-agnostic implementation and interoperability. On the capacity side, KT Corporation announced in July 2026 an 18 trillion KRW three-year plan to become an AI-centric platform company, including 5 trillion KRW earmarked for 1 GW of AI data center capacity and 1 trillion KRW for submarine cable expansion. This reinforces demand for DX offerings tied to compute, connectivity, and data gravity across regions.

Recent Industry Developments

- July 2026: Accenture launched Accenture Edge, a business unit focused on bringing agentic AI solutions to mid-market companies in collaboration with Google Cloud. The move packages transformation delivery with hyperscaler tooling to shorten deployment cycles and broaden agentic AI adoption beyond large-enterprise early adopters.

- June 2025: AWS launched Project Rainier, clustering Trainium 2 chips into a large-scale AI training system positioned as a major step-up in AI compute capability. This expansion strengthens hyperscaler-led infrastructure economics that underpin cloud-first modernization and enterprise AI production deployments.

- November 2024: AWS formed the Generative AI Partner Innovation Alliance to scale its Generative AI Innovation Center through an expanded partner ecosystem. The initiative increased delivery capacity for enterprise AI programs by formalizing partner-led solution development, integration, and deployment support.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the digital transformation market is defined as enterprise and public-sector spending on technologies and related services that modernize processes, customer experiences, and IT operations through cloud, data, and automation-led change.

Scope exclusions: Consumer-only gadgets and standalone telecom network buildouts are excluded unless they are purchased as part of an enterprise digital transformation program.

Segmentation Overview

- By Technology

- AI and ML

- Extended Reality (VR/AR)

- Internet of Things (IoT)

- Industrial Robotics

- Blockchain

- Digital Twin

- Additive Manufacturing / Industrial 3-D Printing

- Edge Computing

- Others

- By Deployment Model

- Cloud

- On-Premise

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Industry Vertical

- BFSI

- Healthcare and Life-Sciences

- Manufacturing and Industrial

- Retail and E-commerce

- Energy and Utilities

- Automotive and Transportation

- Government and Public Sector

- Others (Media, Education, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, map the value chain, and collect the baseline signals needed for a clean model build. We relied on public sources such as the US Census Bureau and Bureau of Economic Analysis for business investment context, the International Telecommunication Union for connectivity indicators, the OECD for digital economy metrics, and the World Bank for macro variables used in normalization.

To translate this into market sizing inputs, we also reviewed company filings and investor presentations to understand revenue mixes, partner ecosystems, and typical deal patterns across software, services, and infrastructure that enable transformation. Patent databases were checked to sense where activity is accelerating in AI, automation, and industrial digitization, and an import-export shipment-level database was used selectively to sanity check hardware-related demand where it ties to enterprise projects. These desk sources are illustrative, and many other public datasets and disclosures were also referenced to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on validating what is actually being bought under digital transformation budgets, how spending is split across cloud, security, data, and automation, and how pricing and renewal behavior is evolving. We spoke with a mix of solution providers, system integrators, and buyer-side IT and business leaders across APAC, EMEA, and the Americas, and the discussions were used to confirm adoption timing, replacement cycles, and the share of projects that are transformation-driven versus routine IT upgrades.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 45% |

| Mid tier: 45% | Functional/Unit leaders: 31% | EMEA: 37% |

| Smaller Players: 19% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where overall ICT and digital spend pools are reconstructed by region, and then filtered using adoption and penetration signals tied to transformation programs across industries. The model is then cross-checked using selective bottom-up approximations such as sampled vendor revenue mixes, channel feedback on deal volumes, and average contract value ranges multiplied by a reasonable count of active programs, and any major gaps are adjusted with documented assumptions.

Key inputs used in the model include cloud adoption intensity and migration pace, cybersecurity spend linked to modernization projects, enterprise AI and analytics rollout rates, the share of workloads moving to edge and IoT in industrial settings, and services intensity (implementation and managed services) as a share of total program value. Where country-level data is uneven, we use proxy indicators like digital readiness, enterprise IT spend per employee, and regional industry mix, which are then reconciled through interview feedback. For forecasting, scenario analysis is used with a base case anchored to expected cloud and AI budget growth, and the scenarios are tuned using primary feedback on project deferrals, pricing changes, and regulatory-driven digitization timelines.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals such as regional IT spending direction, reported backlog and bookings commentary, and changes in digital skills hiring and program pipelines. We run variance checks at region and major technology level, and outliers are re-tested by revisiting assumptions, re-checking source context, and re-contacting experts when a shift cannot be explained by visible market events.

Before sign-off, the model and narrative go through multi-step analyst review so that unit logic, currency conversions, and time alignment are consistent. The report is refreshed annually, and interim updates are made when material events occur, such as major policy changes, large macro shocks, or clear technology step-changes. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Digital Transformation Market Size Compared With Other Published Estimates

Published estimates for digital transformation often differ because the market boundary can shift depending on whether adjacent IT spend is counted, how cloud and services are bundled, and which year is treated as the starting point. Differences also show up when firms use different currency timing, inflation handling, and assumptions on how fast AI-led programs move from pilots into scaled deployments.

The table points to a spread that is mainly driven by scope and counting rules, especially around what is treated as transformation spend versus routine IT operations. Some studies lean on aggressive scenarios for enterprise AI and include broader categories like general IT services, while others keep a narrower technology-only view and may not fully validate the services intensity that buyers report in real programs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.01 T (2026) | |

| Global Research Publisher A | USD 1.30 T (2025) | Uses a 2025 base and a narrower interpretation that can undercount transformation-linked services and multi-technology programs, which compresses the value versus a scope that follows full program spend. |

| Industry Research Portal B | USD 1.49 T (2025) | Often applies faster growth assumptions for broad technology buckets and may blend general ICT categories, which can shift totals depending on how much non-transformation IT spend is captured. |

The table shows that a large part of the difference comes from base-year choice and what gets treated as program-driven spend, and in Mordor Intelligence's model the total is built by counting transformation budgets only when they map to defined technology and service activities tied to modernization programs. With that clarity, users can trace the number back to practical drivers like cloud migration pace, services intensity, and regional adoption timing, and the steps can be repeated as conditions change.

Key Questions Answered in the Report

What is the current size of the digital transformation market?

The digital transformation market stands at USD 2.01 trillion in 2026.

How fast will the digital transformation market grow?

It is forecast to rise at a 21.55% CAGR, reaching USD 5.33 trillion by 2031.

Which technology segment leads the digital transformation market?

AI and ML technologies dominate with 28.05% share and a 23.9% CAGR outlook.

Which deployment model is most popular?

Cloud implementations command 62.65% of current spending and are expanding at 22.1% CAGR.

Which region shows the highest growth potential?

Asia-Pacific is projected to expand at 22.0% CAGR due to large-scale digital infrastructure programs.

What is the main challenge to digital transformation?

Legacy technical debt absorbs up to 80% of IT budgets, slowing modernization efforts and adding security risks.

Page last updated on: