Oman Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

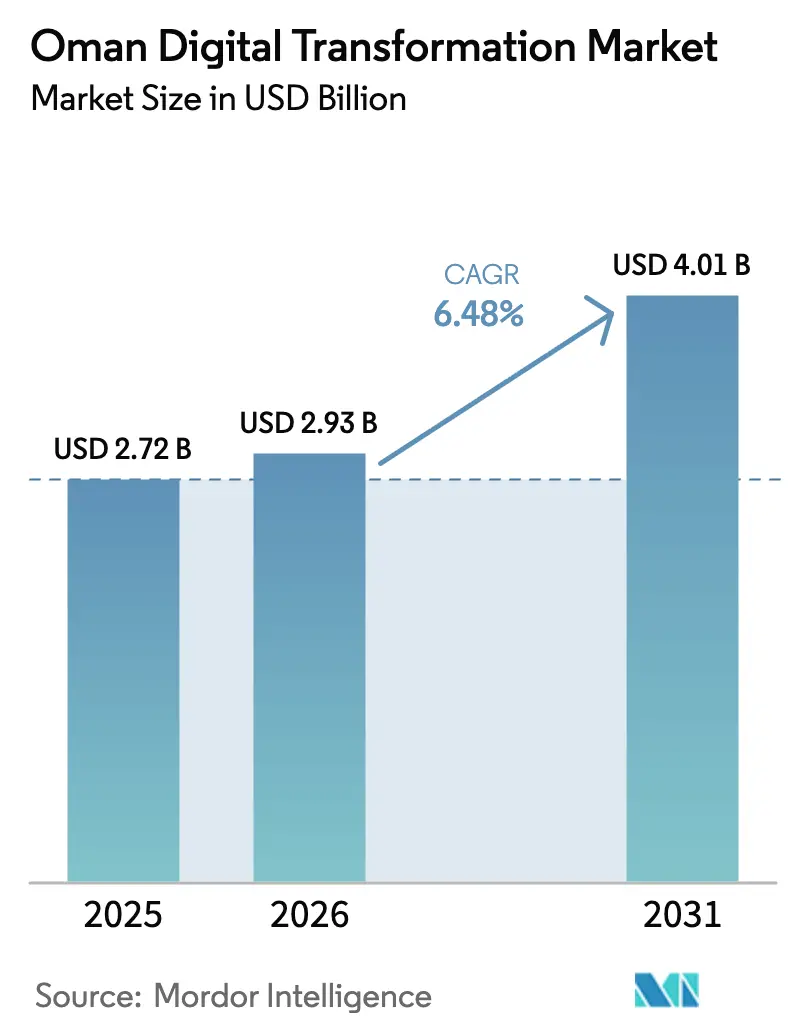

| Base Year Market Size (2025) | USD 2.72 Billion |

| Market Size (2026) | USD 2.93 Billion |

| Market Size (2031) | USD 4.01 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Digital Transformation Market Analysis by Mordor Intelligence

The Oman digital transformation market size is projected to expand from USD 2.72 billion in 2025 and USD 2.93 billion in 2026 to USD 4.01 billion by 2031, registering a CAGR of 6.48% between 2026 to 2031. Policymakers are channeling Vision 2040 funds toward service automation rather than show-piece smart cities, creating steady, policy-led demand across public services and regulated industries. Government mandates on data residency, a national 5G build-out that already covers 91% of the population, and rising cloud capacity from hyperscalers are accelerating infrastructure modernisation. Oil-price volatility and talent shortages temper the growth trajectory, yet sustained public-private partnerships continue to unlock targeted opportunities, especially in tourism, manufacturing and logistics. Competitive dynamics remain moderate, with global cloud vendors racing to localise footprints while Omantel, Ooredoo and Vodafone Oman reposition as full-stack service partners.

Key Report Takeaways

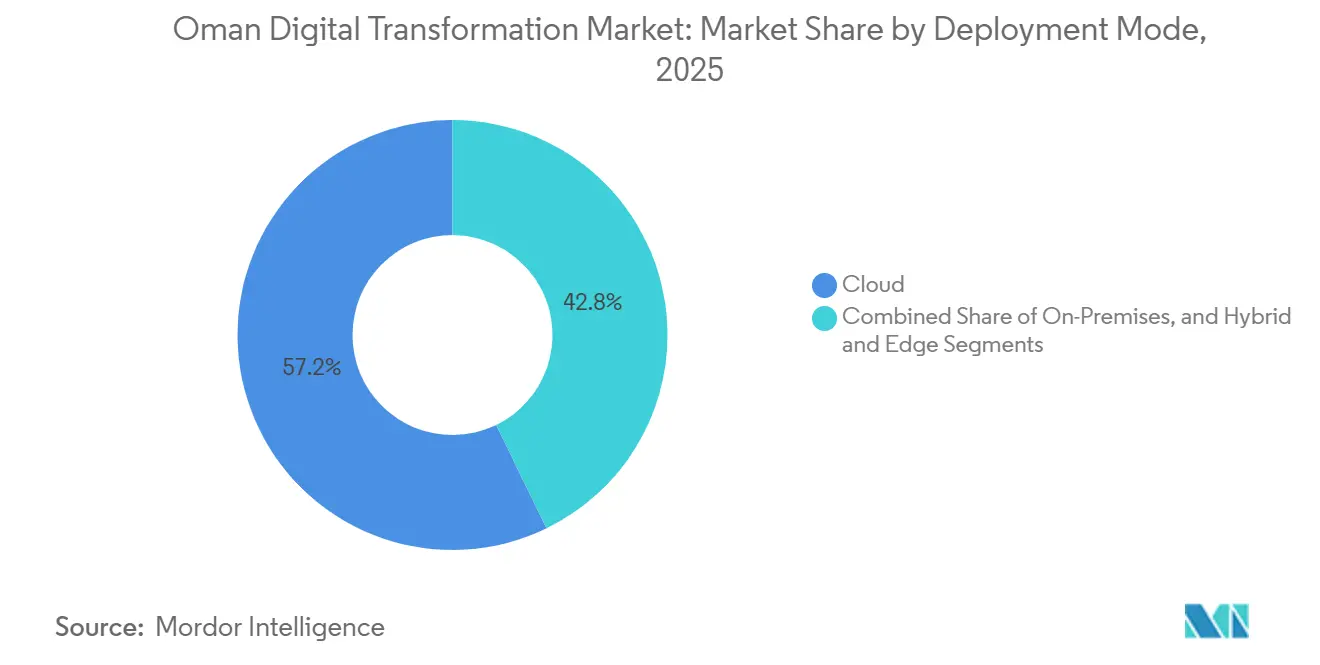

- By deployment, cloud deployment led with 57.21% of the Oman digital transformation market share in 2025, while hybrid and edge architectures are advancing at an 8.19% CAGR through 2031.

- By technology, internet of things accounted for 26.73% of technology spending in 2025, whereas cloud and edge computing is forecast to expand at a 9.07% CAGR, the fastest among all technology types.

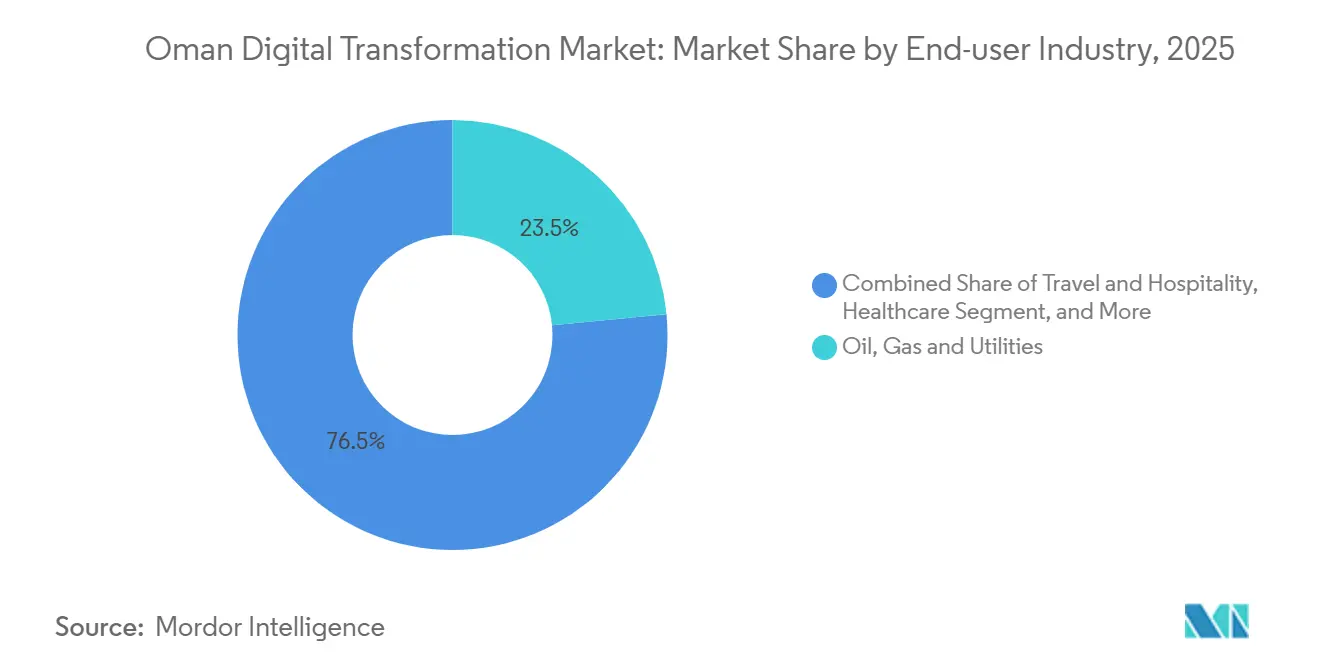

- By end-user, oil, gas and utilities held 23.46% of end-user spending in 2025, yet travel and hospitality is projected to grow at an 8.31% CAGR to 2031.

- By enterprize size, large enterprises commanded 67.59% share of the Oman digital transformation market size in 2025, but small and medium enterprises are pacing ahead at a 7.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Oman representing one among them. The global report on digital transformation (dx) market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Oman Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2040, Government Digital Policies and PPP Initiatives | +1.8% | National (Muscat, Salalah, Duqm, Sohar) | Long term (≥ 4 years) |

| National 5G Roll-out Accelerating IoT Uptake | +1.5% | National, urban centres leading | Medium term (2-4 years) |

| Sovereign Data-Residency Mandate Fueling Local Cloud Hubs | +1.2% | Muscat, Ibri, Barka | Medium term (2-4 years) |

| Ongoing Events and Tourism Driving Automation | +0.9% | Muscat, Salalah, Nizwa, Jebel Akhdar | Short term (≤ 2 years) |

| Manufacturing 4.0 Investments in Free Zones | +0.6% | Sohar, Duqm, Rusayl | Medium term (2-4 years) |

| Carbon-Neutral Port Operations Requiring Smart Logistics | +0.4% | Duqm, Salalah, Sohar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2040, Government Digital Policies and PPP Initiatives

Vision 2040 raises the ICT contribution target from 2% of GDP in 2021 to 10% by 2040, compelling ministries to digitise workflows and pursue public-private delivery models. The Government Digital Transformation Programme allocates OMR 170 million (USD 442 million) across more than 50 institutions to automate 80% of public services by 2025.[1]Zakasoa A. Randriamiadana, “Oman launches transformative AI and digital technologies programme to boost economy,” Digital Watch Observatory, dig.watch Strategic partnerships with AWS, Google Cloud and Microsoft diversify technology stacks and reduce lock-in risk while upholding Ministerial Decision 1152/2/19/2024-20 on data sovereignty. A national open-data platform, an AI research centre and a Fourth Industrial Revolution hub provide long-term institutional scaffolding. Oman and the United Arab Emirates are the only GCC members to improve simultaneously in the UN eGovernment Development Index and the E-Participation Index, confirming that incremental, policy-driven transformation is gaining traction.

National 5G Roll-out Accelerating IoT Uptake

The three mobile operators operate 5,893 5G sites, achieving 91% coverage and median download speeds of 259.94 Mbps, which ranks Oman eighteenth worldwide. Omantel, Ooredoo and Vodafone Oman have each invested in standalone 5G cores, enabling ultra-low-latency applications such as remote drilling, autonomous port vehicles and 5G fixed wireless access for underserved industrial zones. Subscriptions for 5G FWA surged six-fold between 2021 and 2024, demonstrating enterprise appetite for high-bandwidth connectivity in areas where fibre is impractical. Sohar Port, Salalah Port and Petroleum Development Oman are using the network for digital twins, predictive maintenance and condition monitoring. The national coverage buffer positions the Oman digital transformation market for sustained IoT-led innovation across logistics, healthcare and utilities.

Sovereign Data-Residency Mandate Fueling Local Cloud Hubs

Ministerial Decision 1152/2/19/2024-20 obliges public entities and critical-infrastructure operators to store citizen data onshore. In response, Oman Data Park doubled capacity to 20 MW, Oracle opened a secondary dedicated region in Ibri and SAP launched a private-cloud data centre hosting OQ Group’s ERP stack.[2]Oracle Corporation, “Oracle Cloud Infrastructure Regions,” oracle.com The Personal Data Protection Law introduces fines for unauthorised cross-border transfers and mandates 72-hour breach reporting, aligning compliance requirements with ISO 27001. Localisation lowers latency and satisfies central-bank and defence requirements but also reshapes vendor economics by favouring onshore, multi-tenant infrastructure over offshore hyperscale models. As agencies migrate core systems, a growing ecosystem of local integrators and multinational partners is emerging to meet sovereignty, disaster-recovery and performance needs.

Ongoing Events and Tourism Driving Automation

OMRAN’s smart-tourism hackathons, VR heritage tours in Muscat and AR exhibitions at the Osaka 2025 World Expo showcase how immersive technologies create revenue multipliers for hospitality operators. The accessible-tourism segment, valued globally at USD 76 billion in 2024, is particularly attractive because travellers with mobility needs often journey with companions, boosting average spend. Municipalities are piloting IoT-based crowd management, smart lighting and dynamic pricing in tourist hotspots, while telco 5G private networks ensure coverage in remote ecological areas such as Jebel Akhdar. These initiatives directly support the Vision 2040 target of 11.7 million annual visitors by 2030 and push the Oman digital transformation market toward experience-oriented use cases that complement traditional service automation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy Dependence on Oil and Gas Revenues | −0.9% | National, budget exposure | Short term (≤ 2 years) |

| Digital Skills Gap and Reliance on Expats | −0.7% | Muscat, Salalah, Sohar | Medium term (2-4 years) |

| Fragmented SME Tech-Adoption Culture | −0.4% | Muscat, Salalah, Nizwa | Medium term (2-4 years) |

| Cyber-Talent Flight to Neighboring GCC Markets | −0.3% | UAE, Saudi Arabia, Qatar pull | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heavy Dependence on Oil and Gas Revenues

Hydrocarbon exports provide 60% of government income, so dips in Brent prices translate quickly into delayed IT tenders and reallocated budgets. Although the OMR 170 million (USD 442 million) transformation fund is substantial, it equates to less than 1% of annual public expenditure, making it vulnerable during downturns. Private-sector oil and gas spending offers partial insulation, yet even integrated players such as Petroleum Development Oman must curb discretionary projects when parent-company cash flows tighten. Boom-bust cycles deter vendors from maintaining large local teams, adding cost to knowledge transfer and elongating project timelines.[3]Telecom Review Middle East, “Innovation in Action: Oman's Bold Steps in Digital Government Transformation,” telecomreview.com

Digital Skills Gap and Reliance on Expats

Only 1,880 professionals completed Makeen programmes by 2025 against a 10,000-person target, leaving acute shortages in data science, cybersecurity and cloud engineering. Hadatha cybersecurity centres at three universities address entry-level skills, but mid-career talent often departs for 30-50% higher salaries in the UAE or Saudi Arabia. Enterprises thus rely on expatriates who command premium pay and seldom commit to long-term localisation of expertise. This churn raises costs, complicates vendor-client communication and constrains the creation of indigenous intellectual property, limiting the competitive differentiation of Omani solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Strategies Dominate Sovereignty-First Transformation

Cloud deployment held 57.21% Oman digital transformation market share in 2025. The preference for public cloud reflects early partnerships with Microsoft Azure, Oracle Cloud Infrastructure and AWS, yet data-sovereignty rules require many agencies to embrace hybrid configurations. Hybrid and edge architectures are growing at an 8.19% CAGR, outpacing the overall Oman digital transformation market. Omantel’s Otech platform unifies Oman Data Park and Tedom into a single commercial layer, allowing ministries to retain sensitive datasets onshore while leveraging offshore regions for testing or analytics. Oracle’s Muscat-Ibri dual-region model satisfies disaster-recovery rules and positions the vendor for banking and defence workloads that demand geographic separation.

Edge computing closes latency gaps in oil fields, ports and remote industrial estates. Petroleum Development Oman uses wellhead edge nodes to filter sensor data, which trims bandwidth costs by 60%. Sohar Port’s edge analytics cut truck turnaround by 25%, while Duqm and Salalah ports plan similar deployments. Although on-premises environments persist in defence and critical infrastructure, the long-term trajectory points to a hybrid equilibrium where public cloud is reserved for variable workloads, on-premises resources host classified systems and edge devices process mission-critical data in real time. This balanced topology matches both fiscal realities and legal constraints, ensuring that the Oman digital transformation market continues to expand without breaching sovereignty rules.

By Technology Type: Cloud and Edge Infrastructure Outpaces IoT Saturation

Internet of Things represented 26.73% of spending in 2025, a testament to mature deployments across hydrocarbons, utilities and logistics. However, incremental growth has slowed as leading verticals near device saturation. In contrast, cloud and edge computing is accelerating at a 9.07% CAGR, reinforcing its status as the most dynamic segment of the Oman digital transformation market. Hyperscalers and local data-centre operators are racing to provision in-country capacity that meets residency mandates, while ministries modernise legacy stacks with containerised, cloud-native workloads.

Artificial intelligence adoption is moving from pilot to production stages, bolstered by a national AI lab and Arabic language models that preserve cultural context. Extended reality applications in tourism, education and maintenance are gaining budgeted pilot projects, underpinned by the high-bandwidth, low-latency advantages of the 5G network. Industrial robotics, blockchain proofs-of-concept, digital twins and additive manufacturing have each secured footholds in manufacturing and logistics clusters, illustrating the Oman digital transformation market’s gradual pivot from connectivity to advanced automation capabilities.

By End-User Industry: Energy Sector Leads Digital Adoption

Oil, gas, and utilities accounted for 23.42% of Oman digital transformation market share in 2025, underscored by Petroleum Development Oman’s IBM Maximo project that digitized asset workflows across 60,000 items and slashed paper usage by 70,000 sheets annually. Predictive-maintenance algorithms, digital twins, and real-time asset dashboards now permeate upstream, midstream, and downstream environments, creating demonstrable cost savings. Travel and hospitality emerges as the quickest-growing vertical at an 11.61% CAGR, buoyed by Omran Group’s strong profitability and flagship tourism projects like the Club Med resort and New City Salalah waterfront.

Healthcare digitization accelerates under the Health Vision 2050 roadmap, with blockchain pilots securing patient data and telehealth initiatives tackling rural-access gaps. Banking and financial services reorganize payment rails; the Central Bank’s 24/7 real-time gross settlement and mobile-payment clearing processed more than 5 million transactions in 2023, paving the way for QR-code ubiquity. Manufacturing benefits from free-zone Industry 4.0 incentives, and government agencies leverage the USD 442 million e-services modernization pool, ensuring that each vertical reinforces aggregate momentum across the Oman digital transformation market.

By Organization Size: SME Growth Outpaces Enterprise Adoption

Large enterprises captured 67.55% of 2025 spend thanks to entrenched IT budgets, in-house expertise, and complex multi-year roadmaps. Nonetheless, small and medium enterprises are expected to grow at a 11.86% CAGR through 2031, reflecting regulatory simplification, dedicated credit lines, and tailored insurance products. The Future Fund directs 7% of its war chest toward SME digital upgrades, while the Capital Market Authority standardizes coverage for cyber and operational risks, easing lender concerns.

Survey data confirms that SMEs face skills gaps and financing constraints; however, Tasees’ pre-incubation program provided coaching on marketing, operations, and finance to 31 entrepreneurs drawn from 120 applicants, illustrating bottom-up ecosystem vitality. Phaze Ventures’ USD 30 million fund injects much-needed early-stage risk capital, anchored by sovereign and corporate LPs. These catalysts collectively expand the Oman digital transformation market’s breadth as smaller firms adopt cloud accounting, e-commerce storefronts, and low-code workflow tools.

Geography Analysis

Muscat-centric initiatives command the largest share of the Oman digital transformation market share, reflecting the concentration of ministries, banks and data-center capacity in the capital. The twin Oracle Cloud regions in Muscat and Ibri, along with Oman Data Park’s 20 MW facility, anchor sovereign workloads close to regulators and headquarters, lowering latency for core banking and defense applications. Muscat Municipality’s automation of 267 services and virtual-reality heritage tours demonstrates how service digitalization and experiential technology reinforce each other in the city-state hub. Together, these programs showcase how the Muscat corridor functions as the primary laboratory for policy pilots that later scale nationwide. As a result, Muscat remains the proving ground for enterprise workloads that will continue to guide investment decisions across the wider Oman digital transformation market.

Salalah, the southern logistics and tourism gateway, is leveraging port automation and 5G fixed-wireless access to shorten container dwell times and to enrich visitor experiences during the Khareef season. Salalah Port’s smart-logistics roadmap includes IoT yard-management systems and digital-twin simulations that improve berth productivity, reinforcing the port’s competitive position on the East-West trade lane. In parallel, OMRAN’s augmented-reality heritage projects are expanding the addressable base of accessible tourism, positioning the governorate to capture a larger slice of the Oman digital transformation market size tied to experiential travel. The coupling of freight efficiency and immersive attractions highlights how regional priorities shape distinct technology stacks.

Duqm and Sohar form the industrial flank of the Oman digital transformation market, each pursuing Manufacturing 4.0 and smart-port blueprints tailored to free-zone incentives. Duqm Special Economic Zone rolled out automated gate control, CCTV analytics and an integrated terminal-operating system, creating a data spine for petrochemical and green-hydrogen investors. Sohar Industrial City adopted edge-enabled digital-twin modelling that reduced truck turnaround by 25% and paved the way for additive-manufacturing pilots in metals and cables. These projects confirm that coastal logistics corridors outside the capital are now absorbing industrial workloads once exclusive to Muscat, distributing demand more evenly across the Oman digital transformation market. Collectively, the four regional clusters, Muscat, Salalah, Duqm and Sohar, form a diversified geography that balances sovereign-data mandates with growth opportunities in tourism, logistics and heavy industry.

Mordor Intelligence provides coverage of the digital transformation (dx) market across other key regional markets, including Asia, Europe, and North America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United Arab Emirates, Spain, China, United States, Canada, and Thailand incorporating local coverage and market participation, as required.

Competitive Landscape

Global hyperscalers, notably Microsoft, Oracle and Amazon Web Services, are expanding sovereign capacity in country to comply with Ministerial Decision 1152/2/19/2024-20, but none match Oracle’s dual-region architecture that became operational in October 2025. Local telecom operators are responding by up-skilling and re-branding: Omantel’s February 2026 launch of the Otech platform merged Oman Data Park and Tedom into a single, full-stack services arm that bundles cloud, cybersecurity and managed services under one invoice. Ooredoo and Vodafone Oman upgraded to standalone 5G cores in 2024, enabling ultra-reliable low-latency connectivity for ports and oil fields and positioning both telcos as edge-computing enablers . This head-to-head underscores a strategic realignment in which connectivity incumbents hedge against commoditised bandwidth by climbing the value stack.

Regional integrators such as Gulf Business Machines Oman and National Technology Group exploit their multi-vendor heritage to bridge legacy mainframes with containerised microservices during phased cloud migrations. Gulf Business Machines Oman, the sole IBM distributor, offers ISO 27001 consulting and tier-1 multivendor support, securing maintenance contracts that lock in annuity revenue even as customers modernise.[4]IBM PartnerPlus Directory, “Gulf Business Machines (Oman) Co. L.L.C.,” ibm.com National Technology Group targets SMEs with subscription-based ERP and e-commerce bundles that address localisation gaps in Arabic interfaces and Omani tax compliance. At the same time, international consultancies like Accenture, PwC and Deloitte bundle change-management and cybersecurity audits into enterprise-wide contracts, increasing switching costs for large clients and raising the entry bar for pure-play software firms.

White-space opportunities persist in edge-analytics devices for remote oil wells, low-code SaaS for the 130,359 registered SMEs and accessible-tourism platforms that combine multilingual chatbots with AR content. Start-ups that align with data-residency rules and ISO 27001 standards gain a regulatory moat against offshore vendors lacking in-country assets. Meanwhile, the combined share of the five largest providers is estimated at roughly 55%, leaving meaningful headroom for specialised challengers and justifying a concentration score of 6 for the Oman digital transformation market.

Oman Digital Transformation Industry Leaders

Google LLC (Alphabet Inc.)

IBM Corporation

Microsoft Corporation

Hewlett Packard Enterprise Company

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Omantel launched the Otech platform, bringing Oman Data Park and Tedom under one brand to deliver integrated cloud, cybersecurity and managed services.

- October 2025: Oracle commissioned a secondary Oracle Cloud Infrastructure Dedicated Region in Ibri, establishing a dual-region architecture for sovereign workloads.

- July 2025: Sultan Qaboos University opened a Hadatha Cybersecurity Centre, followed by centres at University of Technology and Applied Sciences and Middle East College in October 2025.

- May 2025: The Ministry of Health introduced the Shifa telemedicine app, connecting more than 200 facilities for virtual consultations and prescription refills.

Oman Digital Transformation Market Report Scope

The digital transformation market is defined based on the revenues generated from technologies such as AI and ML, extended reality (VR and AR), IoT, industrial robotics, blockchain, 3D printing, cyber security, and edge computing, among others, that are being used in various end-user industries across Oman. The analysis is mainly based on the market insights that are captured through secondary research and the primaries. The market also covers the key factors impacting the growth of the market in terms of drivers and restraints.

The Oman Digital Transformation Market Report is Segmented by Deployment Mode (On-Premises, Cloud, Hybrid and Edge), Technology Type (Artificial Intelligence and Machine Learning, Extended Reality, Internet of Things, Industrial Robotics, Blockchain, Digital Twin, Additive Manufacturing, Cybersecurity, Cloud and Edge Computing, Other Technology Types), End-user Industry (Oil, Gas and Utilities, Travel and Hospitality, Healthcare, Banking, Financial Services, and Insurance, Manufacturing and Construction, Government and Defence, Other End-User Industries), Enterprise Size (Large Enterprises, Small and Medium Enterprises), and Geography (Oman). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premises |

| Cloud |

| Hybrid and Edge |

| Artificial Intelligence and Machine Learning |

| Extended Reality (VR and AR) |

| Internet of Things (IoT) |

| Industrial Robotics |

| Blockchain |

| Digital Twin |

| Additive Manufacturing |

| Cybersecurity |

| Cloud and Edge Computing |

| Other Technology Types |

| Oil, Gas and Utilities |

| Travel and Hospitality |

| Healthcare |

| Banking, Financial Services, and Insurance (BFSI) |

| Manufacturing and Construction |

| Government and Defence |

| Other End-User Industries (Environment, Transportation, Media and Entertainment) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Deployment Mode | On-Premises |

| Cloud | |

| Hybrid and Edge | |

| By Technology Type | Artificial Intelligence and Machine Learning |

| Extended Reality (VR and AR) | |

| Internet of Things (IoT) | |

| Industrial Robotics | |

| Blockchain | |

| Digital Twin | |

| Additive Manufacturing | |

| Cybersecurity | |

| Cloud and Edge Computing | |

| Other Technology Types | |

| By End-user Industry | Oil, Gas and Utilities |

| Travel and Hospitality | |

| Healthcare | |

| Banking, Financial Services, and Insurance (BFSI) | |

| Manufacturing and Construction | |

| Government and Defence | |

| Other End-User Industries (Environment, Transportation, Media and Entertainment) | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) |

Key Questions Answered in the Report

What is the projected value of the Oman digital transformation market by 2031?

The market is forecast to reach USD 4.01 billion by 2031, growing at a 6.48% CAGR.

Which deployment model is expanding fastest across Oman?

Hybrid and edge architectures lead, advancing at an 8.19% CAGR as agencies balance cloud scalability with data-residency mandates.

Which sector is expected to register the highest growth rate?

Travel and hospitality is set to grow at an 8.31% CAGR, driven by smart-tourism and immersive visitor experiences.

How are SMEs influencing market dynamics?

Government incentives and SaaS pricing models enable SMEs to adopt digital tools at a 7.26% CAGR, narrowing the gap with large enterprises.

What impact do data-residency laws have on cloud adoption?

Sovereign data mandates are catalysing local data-centre investment, leading to hybrid architectures that locate sensitive workloads onshore while using global regions for less critical functions.

Which technology type is overtaking IoT in growth momentum?

Cloud and edge computing infrastructure is the fastest-growing segment, rising at a 9.07% CAGR through 2031.

Page last updated on: