Canada Digital Transformation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

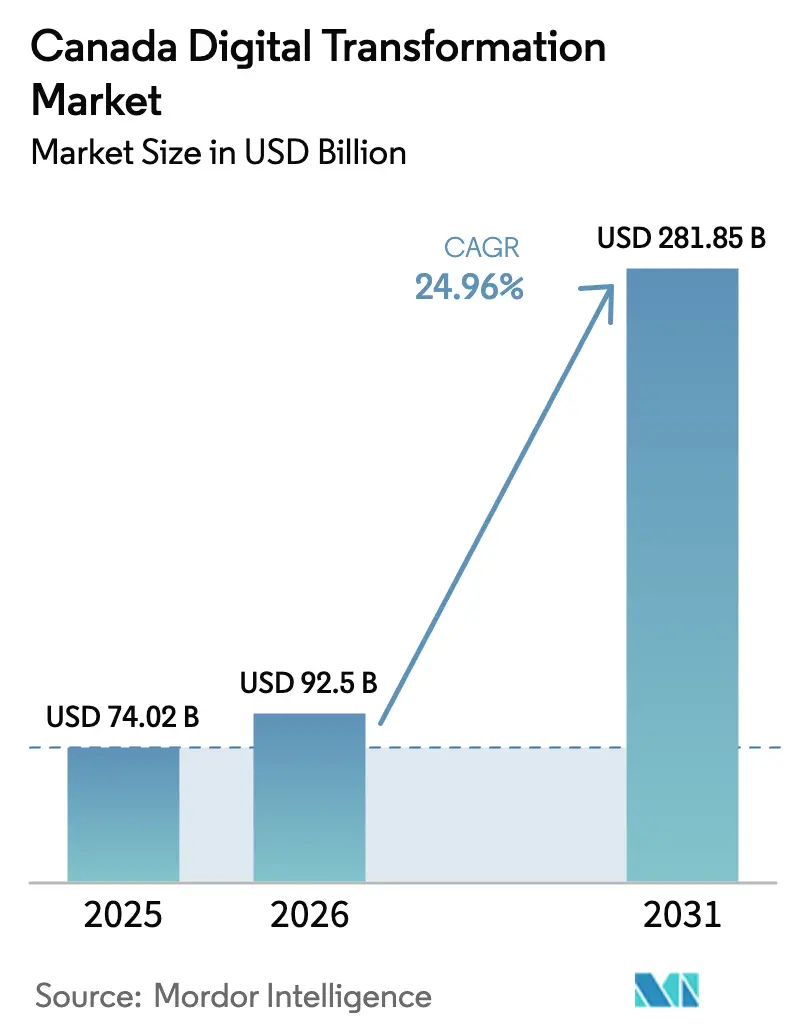

| Base Year Market Size (2025) | USD 74.02 Billion |

| Market Size (2026) | USD 92.5 Billion |

| Market Size (2031) | USD 281.85 Billion |

| Growth Rate (2026 - 2031) | 24.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Digital Transformation Market Analysis by Mordor Intelligence

The Canada digital transformation market size is expected to grow from USD 74.02 billion in 2025 to USD 92.5 billion in 2026 and is forecast to reach USD 281.85 billion by 2031 at 24.96% CAGR over 2026-2031. Growth is anchored by the federal USD 2 billion Sovereign AI Compute Strategy, provincial grant programs that lower adoption costs, and rapid cloud migration that aligns with 5G Stand-alone roll-outs. Ontario’s dense technology cluster continues to attract the largest share of investment, while Alberta is scaling power-efficient data-centre capacity that positions the province as an emerging compute hub. Momentum is further supported by open-banking deadlines that broaden API usage, and by government mandates requiring public-sector systems to meet higher service-delivery standards. Heightened cybersecurity risks and privacy legislation are tempering the pace, yet they are also stimulating demand for secure-by-design solutions, managed services, and compliance support across the Canada digital transformation market.

Key Report Takeaways

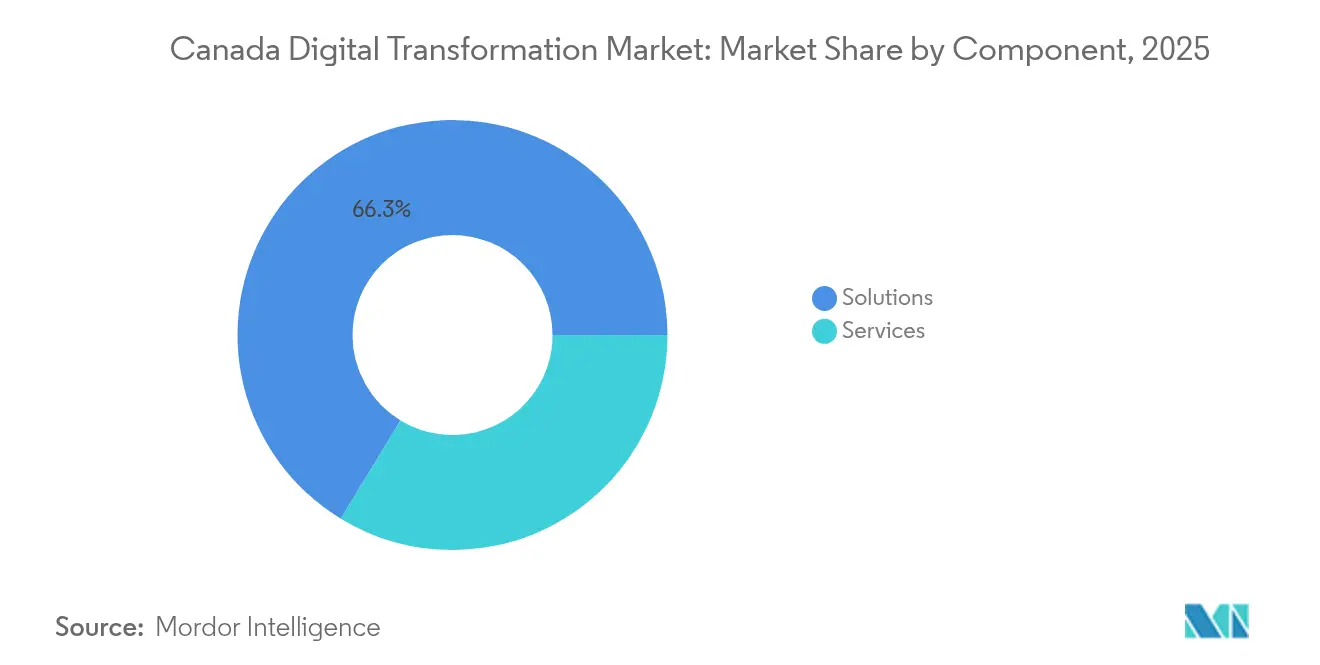

- By component, Solutions held 66.30% of Canada digital transformation market share in 2025; Services are projected to expand at a 28.9% CAGR through 2031.

- By deployment mode, Hosted/Cloud accounted for 51.10% of the Canada digital transformation market size in 2025 and is forecast to grow at 26.4% CAGR to 2031.

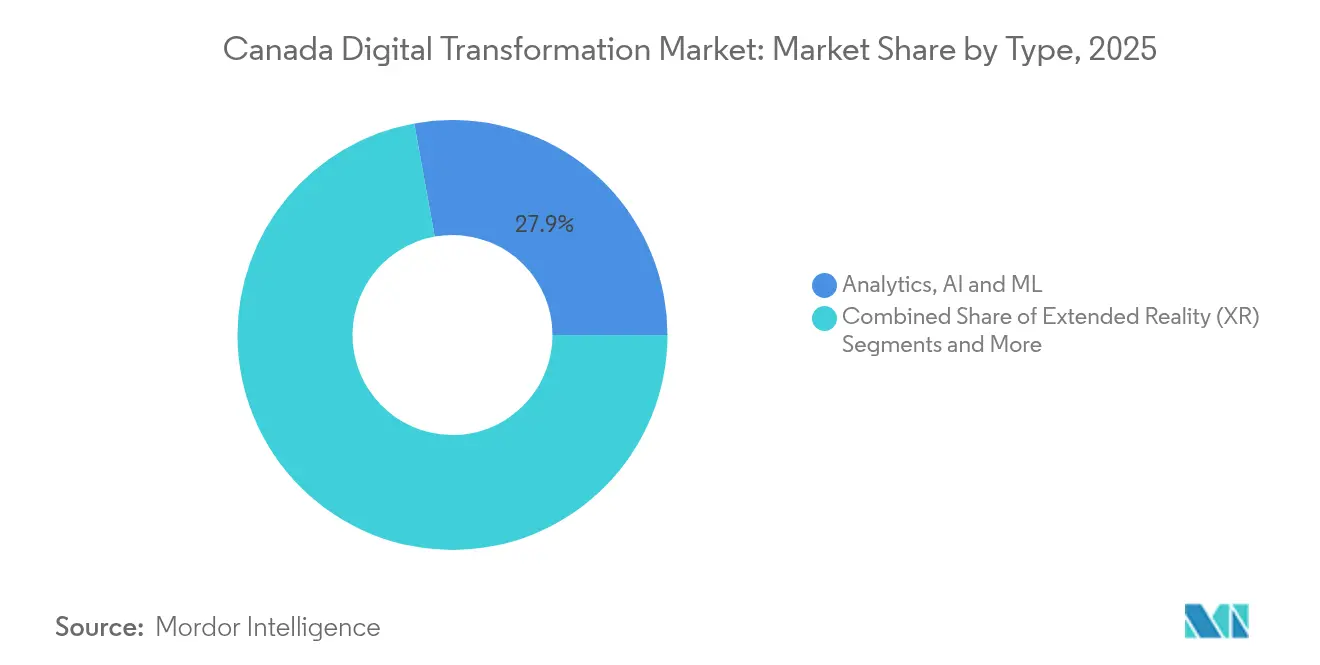

- By technology type, Analytics, AI & ML led with 27.85% revenue share in 2025, while Blockchain is expected to post a 31.2% CAGR through 2031.

- By enterprise size, Large Enterprises commanded 67.60% revenue in 2025, whereas SMEs are set to grow at a 28.7% CAGR over 2026-2031.

- By end-user industry, BFSI contributed 23.50% of 2025 revenue; Healthcare is poised for the fastest growth at a 27.8% CAGR.

- By province, Ontario captured 36.60% share in 2025, while Alberta is projected to lead growth with a 27.4% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple countries and regions, with Canada contributing to the overall trajectory. The outlook on worldwide digital transformation (dx) market reflects how these are expected to evolve collectively.

Canada Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal AI Compute Strategy Accelerates Cloud and AI Spending | +7.8% | National, with concentration in Ontario, Quebec, and Alberta | Medium term (2-4 years) |

| Ontario SME Digitization Grants Boosting SaaS Uptake | +3.2% | Ontario | Short term (≤ 2 years) |

| Cross-border Data-Flow pacts with US simplify Multi-cloud Adoption | +4.5% | National, with emphasis on border provinces | Medium term (2-4 years) |

| 5G Standalone Roll-outs Enable Edge Computing Use-cases in Remote Industries | +2.9% | Alberta, British Columbia, Northern Territories | Medium term (2-4 years) |

| Mandatory Open-Banking Timeline Drives API-first BFSI Projects | +3.6% | National, with concentration in Toronto, Montreal, Vancouver | Short term (≤ 2 years) |

| Quantum-ready Investments in Québec Super-Cluster stimulate Next-gen POCs | +1.8% | Quebec | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal AI Compute Strategy Accelerates Cloud and AI Spending

The 2024 announcement of a USD 2 billion federal program earmarks USD 1 billion for a national super-computing facility, USD 700 million for regional AI clusters, and USD 300 million in affordable compute credits that particularly benefit SMEs.[1]Government of Canada, “AI Strategy for the Federal Public Service 2025-2027,” canada.caThe plan narrows historic capacity gaps vis-à-vis other G7 nations and democratizes high-performance resources across sectors. Provinces are already coordinating site selection for new data-centre investments, and public-service agencies have embedded AI readiness into procurement criteria. As compute access equalizes, more enterprises are piloting generative-AI for logistics and customer-experience workloads, giving the Canada digital transformation market a broad-based demand uplift.

Ontario SME Digitization Grants Boost SaaS Uptake

Ontario reimburses up to CAD 150,000 (USD 109,000) per qualifying project. The grants complement federal vouchers for technology advice and have shortened payback periods on subscription software by covering advisory and integration costs. Adoption is highest among retail and professional-services SMEs that want to personalize customer engagement and standardize back-office workflows. Provincial economic-development agencies report stronger project pipelines in suburban and rural areas, indicating that digital benefits are diffusing beyond the Greater Toronto Area and broadening the addressable base of the Canada digital transformation market.

Cross-border Data-Flow Pacts Simplify Multi-cloud Adoption

Canada and the United States have harmonized key oversight rules on data residency and lawful-access requests. The alignment has reduced legal review cycles for cross-border workloads and cut compliance costs for regulated industries. National banks and insurers are expanding multi-cloud blueprints that combine hyperscale, sovereign cloud, and on-premises zones. Improved portability is also encouraging software vendors to run in-region instances, lowering latency for digital-experience platforms consumed inside the Canada digital transformation market.

5G Stand-alone Roll-outs Enable Edge-computing Use-cases

Commercial launch of 5G SA networks across Western Canada increases peak throughput and reduces end-to-end latency to sub-10 milliseconds. Mining, forestry, and utilities operators are now trialling machine-vision and autonomous-equipment controls that cannot tolerate back-haul delays.[2]Government Information Security, “Canada Warns Cyber Defenders to Buttress Edge Devices,” govinfosecurity.com Edge nodes located at mine sites or substations process sensor data locally, while regional clouds handle model training and analytics. The convergence of 5G and edge services is reshaping connectivity spending and expanding serviceable opportunities within the Canada digital transformation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Privacy Bill C-27 delays Cross-industry Data-Monetization Pilots | -3.5% | National | Medium term (2-4 years) |

| Scarcity of French-English Bilingual Tech Talent outside Urban Hubs | -2.2% | Quebec, New Brunswick | Short term (≤ 2 years) |

| Legacy Mainframe Footprint in Crown Corporations slows Cloud Migration | -1.8% | National, with concentration in federal and provincial government entities | Long term (≥ 4 years) |

| Fragmented Provincial Procurement Rules impede Scale-up for GovTech vendors | -1.4% | National, varying by province | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal Privacy Bill C-27 Delays Cross-industry Data Monetization

The prorogation of Parliament in January 2025 paused the Digital Charter Implementation Act, extending legal uncertainty over consent, algorithmic accountability, and penalty ceilings. Boards are therefore deferring tokenization and data-exchange platforms that rely on broader personal information usage rights. Healthcare networks and financial institutions, which hold rich datasets, have slowed external licensing negotiations until a clear compliance path emerges. While this restraint dampens near-term revenue creation, it is fostering interest in privacy-enhancing technologies and zero-knowledge frameworks that may ultimately raise solution complexity and revenue potential within the Canada digital transformation market.

Scarcity of French-English Bilingual Tech Talent Limits Growth

Unemployment in professional-science occupations sits below 4% across Canada, yet demand for bilingual AI engineers and cloud architects outstrips supply in Quebec and New Brunswick. Language requirements extend recruiting cycles and inflate salary premiums in regions looking to scale call-centre automation, e-government portals, and cloud migrations. Provincial up-skilling grants and STEM outreach programs are in place, but structural deficits persist and may constrain project timelines, especially for public-sector contracts. Vendors are countering by opening hybrid work hubs in smaller cities to broaden talent catchments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Strategic Importance

Services revenue is forecast to rise at a 28.9% CAGR, overtaking the growth of Solutions even as the latter keeps 66.30% of the 2025 spend. Advisory, implementation, and managed operations offerings are expanding as enterprises recognize that technology roll-outs demand process redesign, cyber-risk governance, and change-management support. The Canada digital transformation market size for consulting engagements linked to cloud migration has widened in banking, public services, and energy.

Solutions remain foundational, covering enterprise applications, platform-as-a-service, and advanced analytics suites. Continued investment in core software keeps vendor roadmaps aligned with sector-specific compliance features. However, integration complexity is driving co-sourcing models where solution providers bundle implementation services, reinforcing a virtuous cycle that channels additional spend toward the Services segment of the Canada digital transformation market.

By Deployment Mode: Cloud Dominance Accelerates

Hosted and cloud-native deployments held 51.10% revenue in 2025 and will grow at 26.4% CAGR through 2031. Shared Services Canada’s Public Cloud Operating Model sets a precedent for institutions to favour cloud unless mission risk dictates otherwise. Cost elasticity, security baselines, and access to AI accelerators all reinforce this migration, cementing cloud as the default architecture across the Canada digital transformation market.

On-premise and hybrid environments keep relevance where data sovereignty or latency dictates local control. Crown corporations running legacy mainframes adopt container gateways to bridge to public clouds, creating incremental opportunities in encryption, workload orchestration, and observability tooling. Spending linked to these hybrid topologies will temper the decline of pure on-premise revenue while sustaining demand for professional services tied to the optimization of the Canada digital transformation market size.

By Enterprise Size: SMEs Close the Digital Gap

Large enterprises generated 67.60% of 2025 spend, but SMEs will post a 28.7% CAGR as grant programs remove capital constraints. The Canada Digital Adoption Program and the AI Compute Access Fund provide subsidized hardware vouchers and advisory credits, fostering experimentation with e-commerce, ERP, and low-code automation among firms under 500 employees. These incentives broaden the customer funnel for SaaS providers competing in the Canada digital transformation market.

Corporates continue to outspend in absolute terms, focusing budgets on enterprise-wide data platforms and cybersecurity modernization. Yet rising SME agility is reshaping partner ecosystems; vendors segment offerings into tiered packages that de-risk adoption and accelerate time to value. Competitive intensity sharpens as hyperscalers court boutique consultancies that can aggregate SME demand at scale within the Canada digital transformation market.

By Type: Blockchain Disrupts Traditional Technology Hierarchy

Analytics, AI & ML generated 27.85% of 2025 revenue, leveraging Canada’s deep research talent pool and new sovereign compute capacity. Uptake spans fraud analytics, predictive maintenance, and conversational AI. Meanwhile, Blockchain will log a 31.2% CAGR to 2031, propelled by preparations for open banking and by pilot projects in supply-chain provenance tracking. Provincial regulators are collaborating with standards bodies to accelerate interoperability schemas through coalitions such as the IEEE Canada Blockchain Forum.

Other categories, including IoT, XR, and cybersecurity platforms, continue to register double-digit growth. Cross-stack synergies are emerging—blockchain ledgers secure IoT telemetry, while AI models optimize transaction sequencing, creating layered opportunities across the Canada digital transformation market size.

By End-user Industry: Healthcare Outpaces BFSI Leadership

BFSI held 23.50% revenue share in 2025, cemented by early adoption of digital channels and stringent compliance requirements. Banks and insurers are embedding AI-driven risk scoring and real-time payments, bolstered by sandbox partnerships with fintech scale-ups. Investments focus on microservices and event-streaming frameworks that underpin next-generation customer experiences.

Healthcare is the fastest mover with a 27.8% CAGR forecast. Workforce shortages and backlog pressures are prompting hospitals to digitize care-coordination processes and adopt virtual-consult platforms. Provincial health agencies allocate capital budgets to electronic health record modernization that demands high-assurance identity solutions and integration services. These dynamics significantly expand the addressable base of the Canada digital transformation market.

Geography Analysis

Ontario’s leadership in the Canada digital transformation market is underpinned by a comprehensive provincial innovation strategy that funds SME pilots, accelerates cybersecurity upgrades in the public sector, and incentivizes fintech-academia collaboration. The presence of top universities produces a steady talent pipeline, while diverse sector representation—from automotive to life sciences—creates resilient multi-industry demand. Cloud adoption, AI integration, and process automation initiatives form the three most frequent procurement themes across the province.

Alberta’s digital acceleration is structurally tied to energy economics and regulatory openness. Flexible power-purchase agreements enable data-centre operators to source low-carbon electricity directly from producers, balancing sustainability requirements with cost efficiency. The provincial strategic plan for 2025-2028 earmarks CAD 22.5 million (USD 16.3 million) for programs that link startups with industrial off-takers, compressing commercialization timelines for AI and IoT solutions that address resource-sector challenges. Quebec’s focus on French-language digital services shapes product design and customer-support models. Stricter privacy rules under Law 25 create higher diligence costs but also encourage adoption of privacy-enhancing tools. Montréal’s quantum-computing initiatives attract research grants and talent, while smaller cities emphasize bilingual digital-skills training to expand their share of the Canada digital transformation market. British Columbia channels grant funds toward test-bed programs that pair local suppliers with anchor customers, and the Atlantic provinces position AI as a catalyst for economic diversification, leveraging university-led clusters and federal connectivity projects.

Analysis of the digital transformation (dx) market by Mordor Intelligence spans multiple other regional evaluations across Latin America, Asia, and Europe, supported by country-level insights for United States, Brazil, Japan, United Kingdom, China, and United Arab Emirates, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The Canada digital transformation market exhibits moderate concentration: the five largest suppliers collectively account for about 35% of revenue, while a long tail of regional specialists tackles vertical or technology niches. Scale players emphasise platform ecosystems, embedding third-party APIs and low-code tooling to lock in developer communities. Market leaders deepen alliances: Bell Canada and ServiceNow signed a multi-year pact in 2025 to automate internal workflows and resell packaged solutions to enterprise clients.

Strategic whitespace centres on compliance technologies and trusted data services. Vendors leverage regulatory delays to position privacy-engineered solutions such as differential-privacy analytics. M&A activity is selective, targeting capabilities in cybersecurity orchestration and industry-specific SaaS. Mid-tier integrators pursue domain depth—public finance, utilities, or digital health—rather than scale, allowing them to differentiate on outcome metrics.

National cloud providers augment footprints with clean-energy data centres to meet emission targets and address sovereign-compute provisions. Meanwhile, edge-service start-ups bundle hardware, connectivity, and managed security for mining and agriculture, creating new competitive vectors. These shifts reinforce an outcomes-first positioning and intensify price-to-value scrutiny in procurement cycles across the Canada digital transformation market.

Canada Digital Transformation Industry Leaders

IBM Corporation

Telefonaktiebolaget LM Ericsson

Microsoft Corporation

Telus Corporation

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bell Canada entered a multi-year agreement with ServiceNow to embed the Now Platform across internal and customer-facing operations, aiming to reduce service resolution times through AI-driven workflow automation.

- April 2025: The federal government released the AI Strategy for the Public Service 2025-2027, setting governance rules and skills frameworks for responsible AI deployment in service delivery.

- March 2025: Ottawa launched an AI Compute Access Fund of up to CAD 300 million to subsidize SME access to high-performance infrastructure, complementing the wider CAD 2 billion Sovereign AI Compute Strategy.

- February 2025: British Columbia committed CAD 30 million to the Integrated Marketplace Initiative and increased its Interactive Digital Media Tax Credit to 25%, targeting stronger industry-academia product co-testing.

Canada Digital Transformation Market Report Scope

Digital transformation leverages digital technologies such as artificial intelligence and machine learning, extended reality (XR) for industrial applications, and IoT, among others, to create new business processes or modify existing ones, reshape organizational culture, and enhance customer experiences.

Canada's digital transformation market is segmented by type (analytics, artificial intelligence, and machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cyber security, cloud edge computing, and others (digital twin, mobility and connectivity), end-user industry (manufacturing, oil, gas, and utilities, retail & e-commerce, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, and Other End-user Industries (Education, Media & Entertainment, Environment etc)). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Solutions |

| Services |

| Hosted/Cloud |

| On-premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Analytics, AI and ML |

| Extended Reality (XR) |

| Internet of Things (IoT) |

| Industrial Robotics |

| Blockchain |

| Additive Manufacturing/3D Printing |

| Cybersecurity |

| Cloud Edge Computing |

| Others (Digital Twin, Mobility and Connectivity) |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Other Industries (Education, Media and Entertainment, Environment) |

| Ontario |

| Québec |

| British Columbia |

| Alberta |

| Atlantic Canada |

| Northern Territories |

| By Component | Solutions |

| Services | |

| By Deployment Mode | Hosted/Cloud |

| On-premise | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Type | Analytics, AI and ML |

| Extended Reality (XR) | |

| Internet of Things (IoT) | |

| Industrial Robotics | |

| Blockchain | |

| Additive Manufacturing/3D Printing | |

| Cybersecurity | |

| Cloud Edge Computing | |

| Others (Digital Twin, Mobility and Connectivity) | |

| By End-user Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Other Industries (Education, Media and Entertainment, Environment) | |

| By Region | Ontario |

| Québec | |

| British Columbia | |

| Alberta | |

| Atlantic Canada | |

| Northern Territories |

Key Questions Answered in the Report

How fast is the Canada digital transformation market expected to grow?

It is forecast to climb from USD 92.5 billion in 2026 to USD 281.85 billion in 2031, reflecting a 24.96% CAGR.

Which province leads the Canada digital transformation market?

Ontario holds the lead with a 36.60% share, supported by a dense technology ecosystem and targeted grant programs.

What component segment is expanding the quickest?

Services will advance at a 28.9% CAGR through 2031 as firms seek implementation, advisory, and managed-operations expertise.

Why is Alberta considered an emerging compute hub?

Alberta’s deregulated power market lowers energy costs for data-centres, supporting a provincial CAGR of 27.4% and attracting hyperscale investments.

How is privacy legislation influencing market dynamics?

The delay of Bill C-27 has slowed cross-industry data-monetization pilots, yet it heightens demand for privacy-enhancing technologies and compliance services.

Which technology type is projected to grow the most rapidly?

Blockchain leads with a 31.2% CAGR, driven by open-banking requirements and supply-chain provenance initiatives.

Page last updated on: