Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The KSA Digital Transformation Market Report is Segmented by Technology (Artificial Intelligence and Machine Learning, Internet of Things, Cloud and Edge Computing, and More), Deployment Mode (On-Premise, Public Cloud, and More), End-User Industry (Manufacturing, Oil Gas and Utilities, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

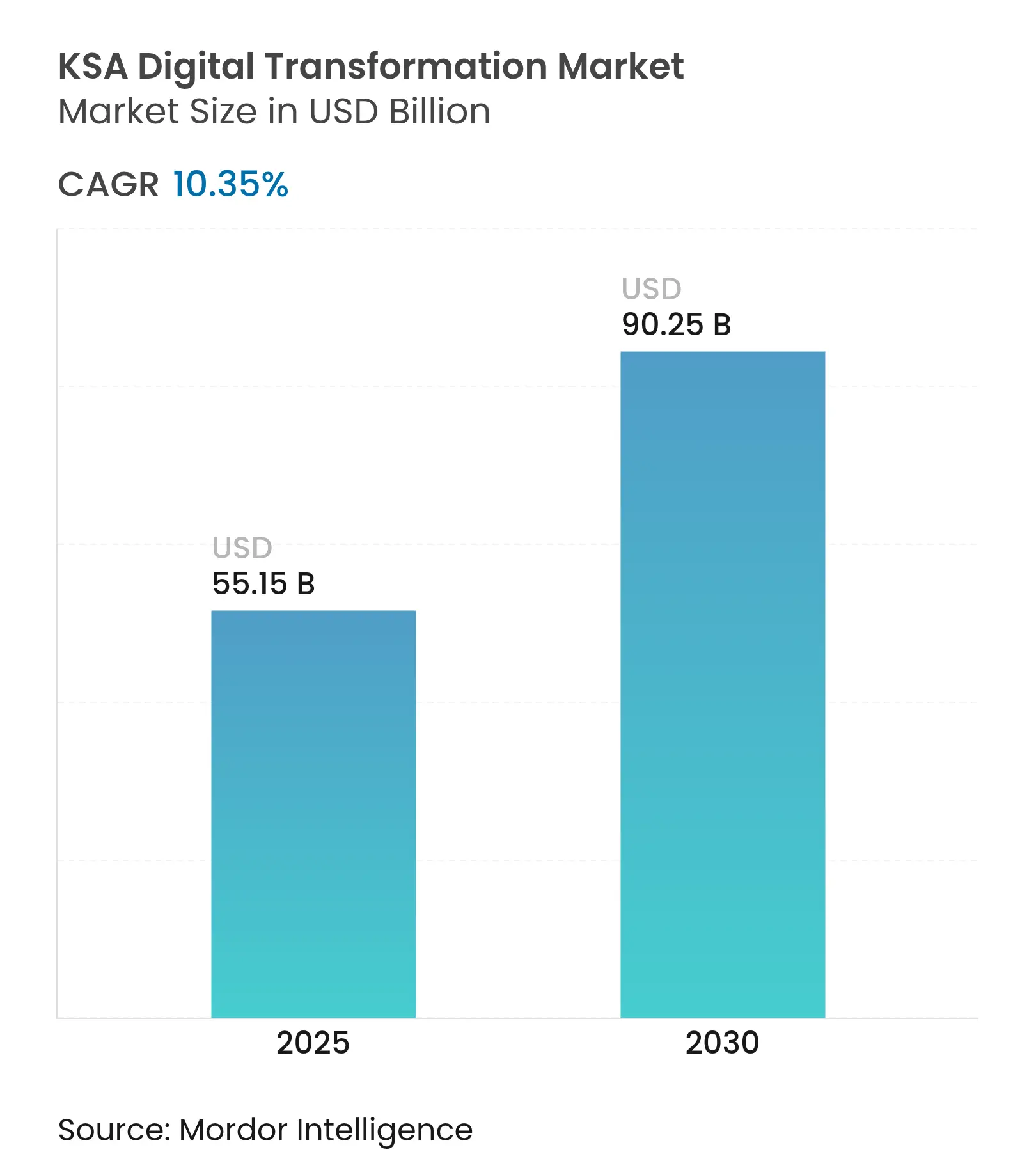

| Market Size (2025) | USD 55.15 Billion |

| Market Size (2030) | USD 90.25 Billion |

| Growth Rate (2025 - 2030) | 10.35 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The KSA digital transformation market size stood at USD 55.15 billion in 2025 and is forecast to reach USD 90.25 billion by 2030, advancing at a 10.35% CAGR. Mandated Vision 2030 programs, hyperscale cloud investments exceeding USD 21 billion, and 97% digitization of government services anchor current momentum. Demand escalates as Arabic-language AI models mature, 5G coverage spans 75 cities, and public-sector entities adopt unified digital platforms that already process more than 3 billion transactions yearly. Competitive activity intensifies through dedicated Saudi cloud regions from six global providers, while giga-projects such as NEOM embed digital twins, AI, and mixed reality at urban scale. Persistent growth drivers include rising cybersecurity spend mandated by Saudi Central Bank, rapid mobile-first adoption with 97% smartphone penetration, and strong government incentives for SME upskilling, together reinforcing a virtuous cycle of solution deployment across industries.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Vision 2030 public-sector digitization Vision 2030 public-sector digitization | +2.8% | Riyadh, Jeddah, Eastern Province | Medium term (2–4 years) | (~) % Impact on CAGR Forecast :+2.8% | Geographic Relevance :Riyadh, Jeddah, Eastern Province | Impact Timeline :Medium term (2–4 years) |

5G and hyperscale cloud expansion 5G and hyperscale cloud expansion | +2.1% | 75 cities nationwide | Short term (≤ 2 years) | |||

Big-data analytics and AI uptake Big-data analytics and AI uptake | +1.9% | Nationwide with hubs in Riyadh and NEOM | Medium term (2–4 years) | |||

Mobile devices and super-apps proliferation Mobile devices and super-apps proliferation | +1.4% | Urban centers nationwide | Short term (≤ 2 years) | |||

Arabic-language AI and NL demand Arabic-language AI and NL demand | +0.8% | National with MENA export potential | Long term (≥ 4 years) | |||

NEOM-driven digital-twin requirements NEOM-driven digital-twin requirements | +1.1% | Tabuk region and spillover projects | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Vision 2030 Public-Sector Digitization Programs

Nationwide digital government initiatives have produced SAR 23 million in operational savings and unified platforms serving 32 million users. The National Digital Transformation Strategy now embeds AI chatbots, blockchain pilots, and IoT integration within ministries. Saudi Central Bank’s cybersecurity mandates require financial institutions to achieve Maturity Level 4 by 2025, spurring demand for governance and compliance solutions.[1]National Cybersecurity Authority, “Cyber Resilience Fundamental Requirements,” rulebook.sama.gov.sa Regulatory sandboxes created by DGA, SAMA, and CST facilitate controlled pilots of emerging technologies, accelerating private-sector adoption. Collectively, these actions elevate the KSA digital transformation market as a benchmark for regional e-government excellence.

Expansion of 5G and Hyperscale Cloud Data Centers

Riyadh is expected to grow signficiantly in data-center capacity through 2027, driven by sustained hyperscale investment. STC extended 5G to 75 cities, achieving a 1,340% jump in 100G capacity and 43% lower power per gigabit. Microsoft, AWS, Google Cloud, and Alibaba Cloud have pledged more than USD 10 billion for local regions, aligning with data-sovereignty rules. Submarine cables linking Europe, Asia, and Africa turn the Kingdom into a digital gateway. These infrastructure gains secure low-latency environments vital for AI inference, IoT telemetry, and immersive experiences, further enlarging the KSA digital transformation market.

Surge in Big-Data Analytics and AI Adoption

SDAIA’s ALLaM model and SCAI’s SauTech speech engines outperform global benchmarks on Arabic tasks by 8–9%. The National Strategy for Data and AI allocates SAR 75 billion to train 20,000 specialists and foster 300 startups. SABIC’s predictive-maintenance models improve asset reliability, while Aramco’s Lighthouse facilities record 90% lower inspection times via AI-enabled drones. High-value use cases such as fraud analytics in banking and precision diagnostics in healthcare translate research advances into enterprise spending, reinforcing the KSA digital transformation market’s trajectory.

NEOM and Other Giga-Projects Driving Digital-Twin Demand

NEOM’s USD 5 billion partnership with DataVolt will create a 1.5 GW net-zero AI data-center campus.[2]NEOM, “Changing the Future of Technology & Digital,” neom.com Digital twins, AI-powered security, and mixed reality technologies underpin city operations managed by Tonomus. ENOWA’s smart grid blueprint uses IoT sensors for real-time load balancing. Construction workflows aligned to 90% prefabrication rely on cloud-based design coordination, amplifying solution demand within the KSA digital transformation market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Data-privacy and cybersecurity concerns Data-privacy and cybersecurity concerns | -1.2% | Financial and government sectors nationwide | Medium term (2–4 years) | (~) % Impact on CAGR Forecast :-1.2% | Geographic Relevance :Financial and government sectors nationwide | Impact Timeline :Medium term (2–4 years) |

Skilled-talent shortage Skilled-talent shortage | -1.6% | Riyadh and Eastern Province tech hubs | Medium term (2–4 years) | |||

Legacy-system integration in SOEs Legacy-system integration in SOEs | -0.9% | Traditional industries nationwide | Short term (≤ 2 years) | |||

Cultural AI-adoption resistance in SMEs Cultural AI-adoption resistance in SMEs | -0.7% | Traditional business centers with regional variation | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Data-Privacy and Cybersecurity Concerns

SAMA mandates board-level cybersecurity oversight and national CISOs for financial institutions. The National Cybersecurity Authority’s ECC-1:2018 standard and the Personal Data Protection Law impose strict compliance, driving uptake of managed security services. Attack volumes surpass 160,000 per day, prompting continuous investment in threat-detection platforms. SMEs feel budget pressure as 752,500 firms widen the attack surface. Heightened risk perception, while a restraint, simultaneously enlarges security spending inside the KSA digital transformation market.

Shortage of Skilled Digital Talent

Half of IT leaders cite talent scarcity as the top barrier, delaying project timelines. The Saudi Digital Academy aims to train 1.2–1.4 million public-sector employees, and Huawei’s Future Skills Centre targets 25,000 trainees. Microsoft’s Data Center Academy partnership with NITA addresses infrastructure roles. While active programs mitigate gaps, competition from UAE and Qatar persists, tempering the KSA digital transformation market’s pace of project execution.

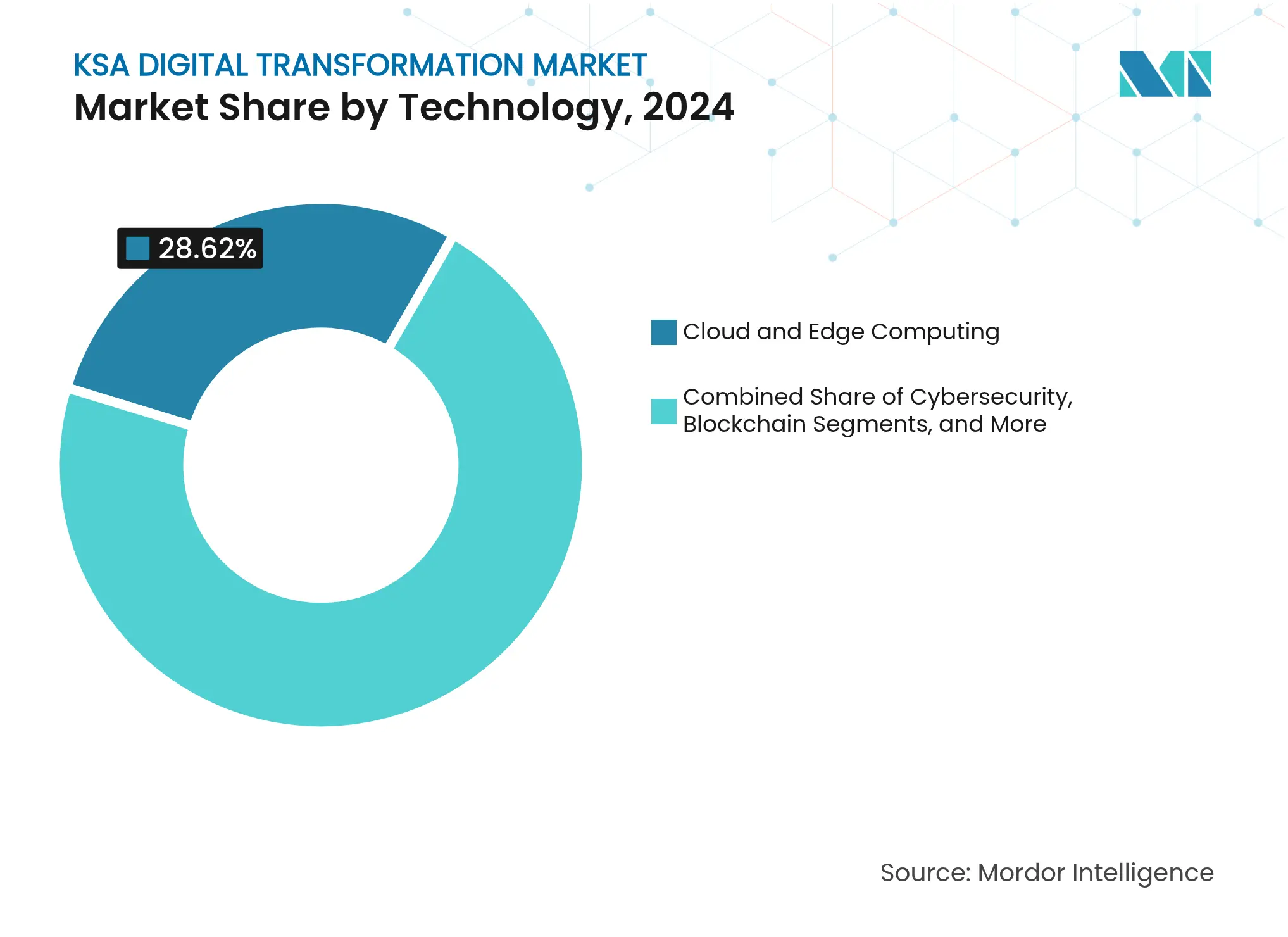

By Technology: Cloud Leadership and Blockchain Momentum

Cloud and Edge Computing accounted for 28.62% of the KSA digital transformation market in 2024. Dedicated Saudi regions from Microsoft, AWS, and Google Cloud, alongside center3’s 300 MW capacity, reinforce local data residency. The KSA digital transformation market size for cloud services is forecast to expand steadily as hyperscalers localize AI accelerators and data-lake solutions. AI and Machine Learning allocations benefit from SAR 75 billion national funding, with ALLaM and SauTech raising local relevance. IoT adoption accelerates as 82% of medium-to-large firms deploy sensors, generating data that funnels back into cloud analytics platforms.

Blockchain is projected to log a 10.62% CAGR by 2030, buoyed by SAMA’s cross-border payment pilots using Ripple and regulatory guidance on digital assets. VR/AR demand escalates through NEOM’s metaverse ambitions, with the Saudi market expected to reach USD 5.4 billion by 2030. Cybersecurity spend grows as governance mandates tighten, while additive manufacturing remains early-stage but aligns with localization aims in aerospace and automotive. Together, these trends maintain technology diversification within the KSA digital transformation market.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Mode: Hybrid Gains Traction

Public Cloud captured 46.51% share in 2024 as ministries consolidated workloads on DGA-approved platforms. The KSA digital transformation market size tied to public cloud benefits from rapid onboarding, standardized security, and pay-as-you-go economics. Financial institutions, however, balance agility with strict residency requirements.

Hybrid Cloud is advancing at a 10.87% CAGR to 2030 as banks, utilities, and manufacturers blend on-premises control with cloud analytics.[3]Digital Government Authority, “Digital Transformation Strategies Across Saudi Arabia,” dga.gov.sa Aramco and SABIC maintain sensitive operational datasets onsite but leverage Azure and AWS for machine-learning pipelines. The Saudi Cloud Computing Company’s joint venture with Alibaba Cloud showcases hybrid architecture under local licensing. On-premises footprints persist for critical infrastructure, yet cloud-ready modernizations signal gradual migration. Hybrid adoption accelerates the KSA digital transformation market as organizations future-proof compliance while unlocking innovation.

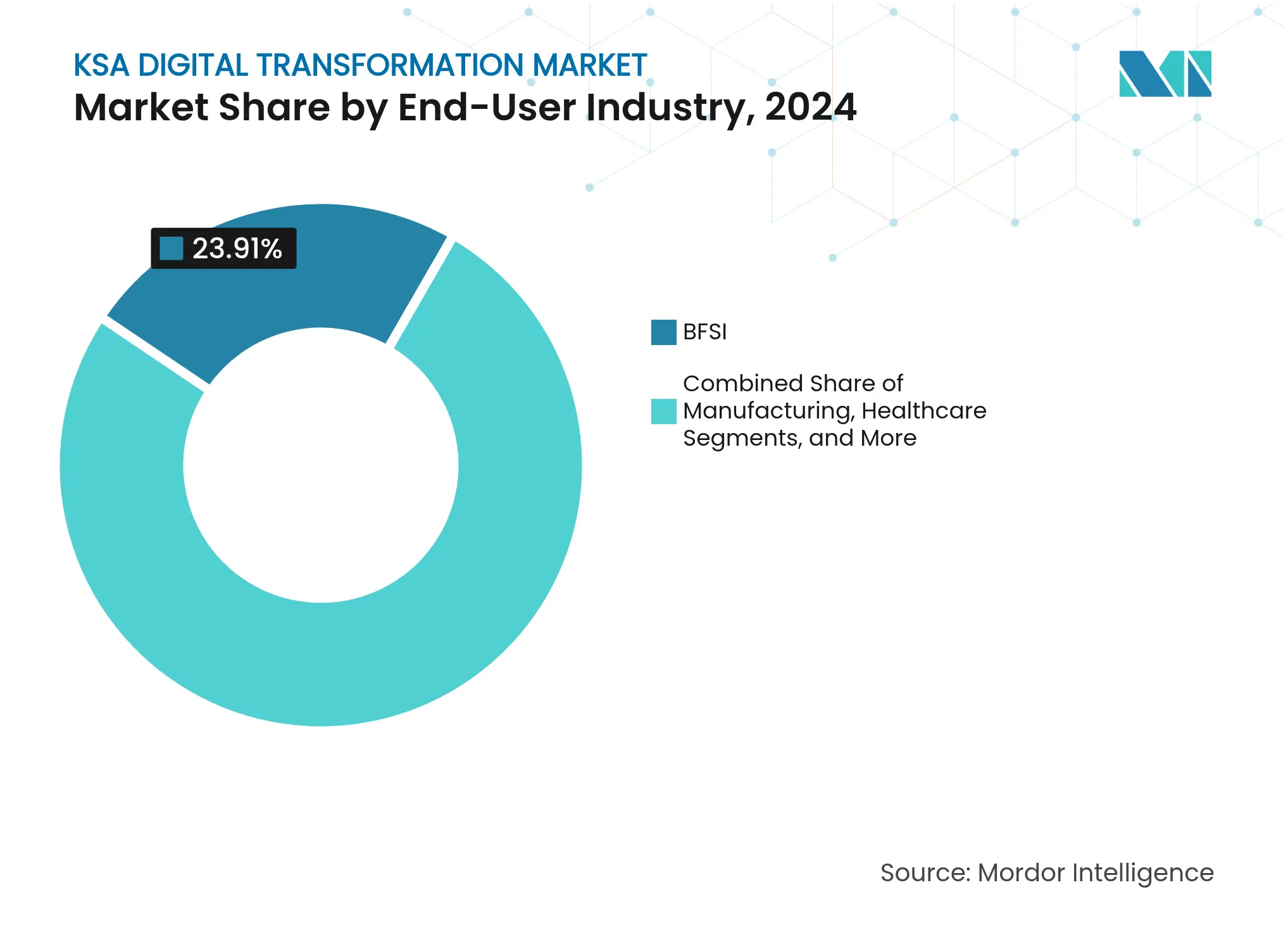

By End-User Industry: BFSI Dominance and Healthcare Surge

BFSI held 23.91% of the KSA digital transformation market share in 2024, propelled by SAMA’s digital banking mandates and cybersecurity frameworks. Open-banking pilots, Islamic fintech platforms, and automated compliance solutions boost spending. Oil, Gas, and Utilities contribute substantial demand via Aramco’s Lighthouse accolades and SABIC’s digital center.

Healthcare is projected to grow at 10.52% CAGR through 2030, fueled by Seha Virtual Hospital’s capacity to serve 400,000 patients annually. Sehhaty’s unified records and telehealth expansion target population-wide coverage. Investment exceeding USD 1.6 billion modernizes diagnostics, e-pharmacy, and remote monitoring. Manufacturing likewise benefits from Industry 4.0 centers, while government digital platforms reach 32 million citizens. Transportation pilots autonomous vehicles at KAUST’s Future Mobility Sandbox. Diversified adoption underlines broad opportunity across the KSA digital transformation market.

Note: Segment shares of all individual segments available upon report purchase

By Organization Size: Enterprise Scale and SME Momentum

Large enterprises commanded 61.31% of the KSA digital transformation market in 2024, leveraging capital resources and strategic alliances with global vendors. Aramco integrates AI for drone inspections that cut manual time by 90%, and NEOM allocates multibillion budgets for citywide automation. Such projects set benchmarks and transfer best practices downstream.

SMEs are forecast to record 11.24% CAGR, supported by 752,500 firms accessing cloud-based SaaS and government financing. The Saudi Digital Academy and regulatory sandboxes lower barriers while mobile-first solutions enable rapid consumer engagement. Challenges include limited cybersecurity budgets and cultural hesitation toward AI decisions, yet simplified tools and training begin to close gaps. SME agility injects dynamism into the KSA digital transformation market, particularly for localized apps and fintech services.

Riyadh anchors the KSA digital transformation market as the governmental, financial, and data-center nucleus. The Digital Government Authority orchestrates national rollouts from the capital, and DataVolt’s forthcoming facilities compound hyperscale presence. Dedicated cloud regions from Microsoft, AWS, and Google Cloud cluster near major business districts, ensuring low-latency access for ministries and enterprises. Financial institutions headquartered in Riyadh harness these assets to meet SAMA’s real-time compliance reporting.

The Eastern Province, led by Dammam and Khobar, channels industrial digitization. Aramco’s four Lighthouse facilities leverage IoT and AI for 30% lower maintenance costs, while Rockwell Automation’s Digital Center of Excellence demonstrates smart-manufacturing use cases. Pipeline monitoring, reservoir modeling, and petrochemical process optimization attract specialized software providers, amplifying regional share within the KSA digital transformation market.

The Western Region exploits Jeddah’s trade orientation and Red Sea connectivity. Carrier-neutral data hubs and submarine-cable landing stations maximize throughput between Europe, Asia, and Africa. King Abdullah Economic City hosts Lucid Motors and Ceer vehicle plants that integrate digital twins and robotic assembly lines. Tourism mega-projects along the Red Sea adopt immersive reality tech to enhance visitor engagement, drawing VR/AR vendors into the KSA digital transformation market’s ecosystem.

Northern Saudi Arabia’s Tabuk Region hosts NEOM, the singularly largest digital endeavor. Its mandate for autonomous logistics, renewable energy grids, and net-zero data centers converts the desert into a testbed for cognitive cities. Tonomus and DataVolt collaborations spawn AI factories powered by 100% renewables, illustrating the fusion of sustainability and digitalization. Spillover effects radiate to adjacent provinces through supply-chain contracts and workforce migration.

Regional disparities persist, though Vision 2030 targets balanced development. Fiber expansion to 576,000 remote homes and extended mobile coverage narrow digital divides. Economic zones in Qassim and Asir entice technology investors with tax incentives and R&D grants. Cross-regional standards maintained by DGA ensure interoperability, reinforcing unified progress throughout the KSA digital transformation market.

Market Concentration

Global hyperscalers occupy pivotal roles. Microsoft, AWS, Google Cloud, and Alibaba Cloud collectively committed more than USD 21 billion to localized regions, partnering with STC, Mobily, and Zain to satisfy data-sovereignty mandates. Local telecoms evolve into integrated solution providers, with STC attaining AWS Premier partnership and Zain completing cloud-based BSS/OSS overhaul in under three years.

Domestic champions leverage cultural expertise. SDAIA’s ALLaM model surpasses international peers in Arabic generation, and SCAI’s SauTech sets new benchmarks for dialect speech recognition. STC Pay’s unicorn valuation and Mobily’s IoT expansion into smart-city platforms highlight diversification beyond connectivity. White-space opportunities include compliance tech for SAMA’s cybersecurity rules and ZATCA’s e-invoicing, yielding fertile ground for niche vendors inside the KSA digital transformation market.

Strategic investments emphasize capability transfer. Huawei’s Future Skills Centre aims at 25,000 trainees, and SAP’s Khobar Innovation Hub co-creates industry blueprints with local partners. Joint ventures such as the Saudi Cloud Computing Company merge global IP with local licenses. National cybersecurity licensing elevates entry thresholds, favoring providers that can demonstrate operational maturity and sovereign compliance. Overall, collaboration often supersedes direct competition, accelerating maturity across the KSA digital transformation market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Digital transformation involves integrating technologies such as analytics, artificial intelligence, machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud, and edge computing, among others, across various end-user industry verticals.

The KSA digital transformation market is segmented by type (analytics, artificial intelligence and machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, and others (digital twin, mobility, and connectivity)) end-user industry (manufacturing, oil, gas and utilities, retail & e-commerce, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, and others (education, media & entertainment, environment, etc.)). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.