Antibodies Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

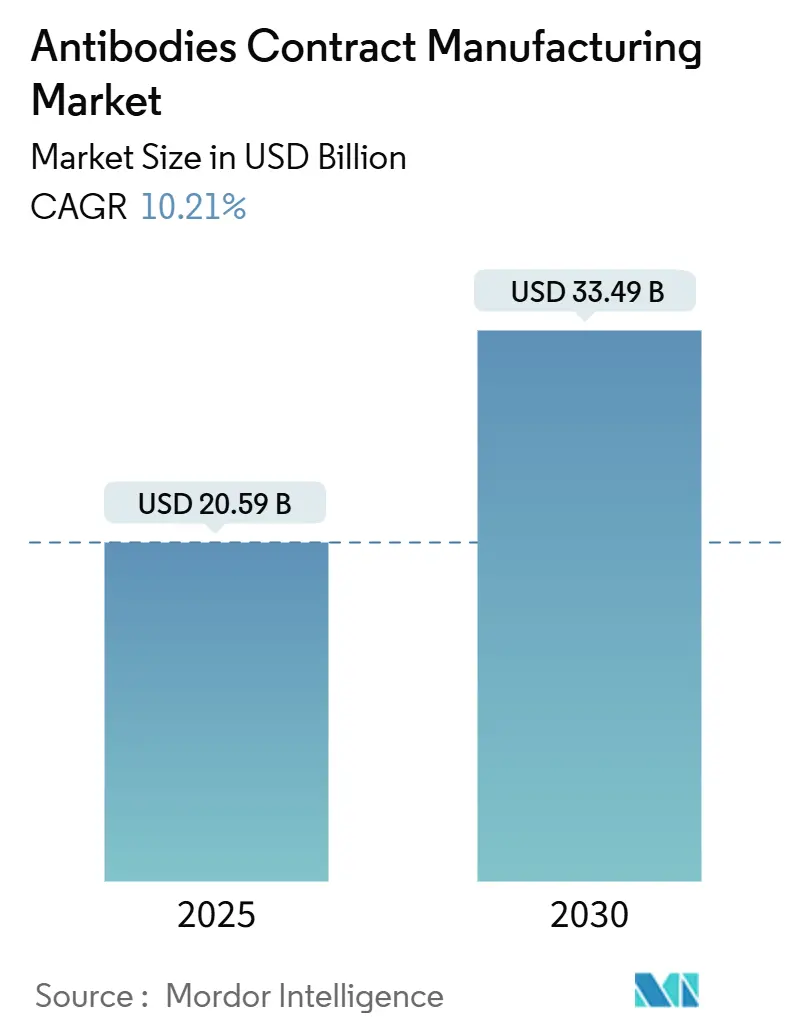

| Market Size (2025) | USD 20.59 Billion |

| Market Size (2030) | USD 33.49 Billion |

| Growth Rate (2025 - 2030) | 10.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibodies Contract Manufacturing Market Analysis by Mordor Intelligence

The antibodies contract manufacturing market size stood at USD 20.59 billion in 2025 and is forecast to reach USD 33.49 billion by 2030, advancing at a 10.21% CAGR. This growth captures the industry’s pivot toward capital-light outsourcing, the widening therapeutic monoclonal antibody pipeline, and rising demand for specialized capabilities in bispecifics and antibody-drug conjugates. Capacity additions such as Samsung Biologics’ 784,000 L facility extension and Lotte Biologics’ USD 3.3 billion South Korean complex illustrate the scramble to relieve bioreactor bottlenecks. Mammalian cell culture retains dominance, yet cell-free protein synthesis is climbing as sponsors weigh speed and flexibility advantages. Service mix evolution toward tech-transfer and scale-up reflects the complexity of moving molecules through late-stage development while meeting stringent regulatory expectations. Supply-chain resiliency, regional reshoring, and persistent talent shortages remain influential cross-currents that shape both pricing and partnership structures.

Key Report Takeaways

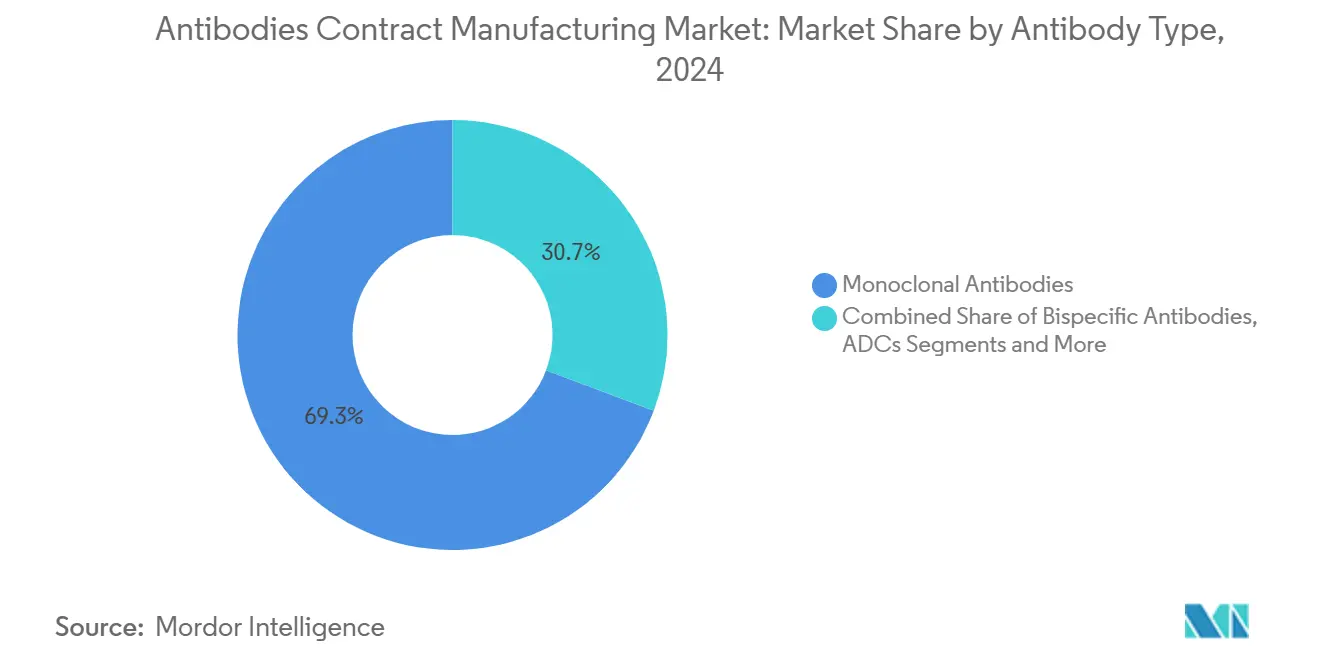

- By antibody type, monoclonal antibodies led with 69.27% revenue share in 2024, while bispecific antibodies are projected to expand at a 14.38% CAGR through 2030.

- By expression system, mammalian platforms accounted for 84.24% of the antibodies contract manufacturing market share in 2024; cell-free protein synthesis is forecast to rise at a 13.57% CAGR to 2030.

- By service type, commercial manufacturing commanded 46.28% of the antibodies contract manufacturing market size in 2024, whereas tech-transfer and scale-up services are advancing at a 14.24% CAGR through 2030.

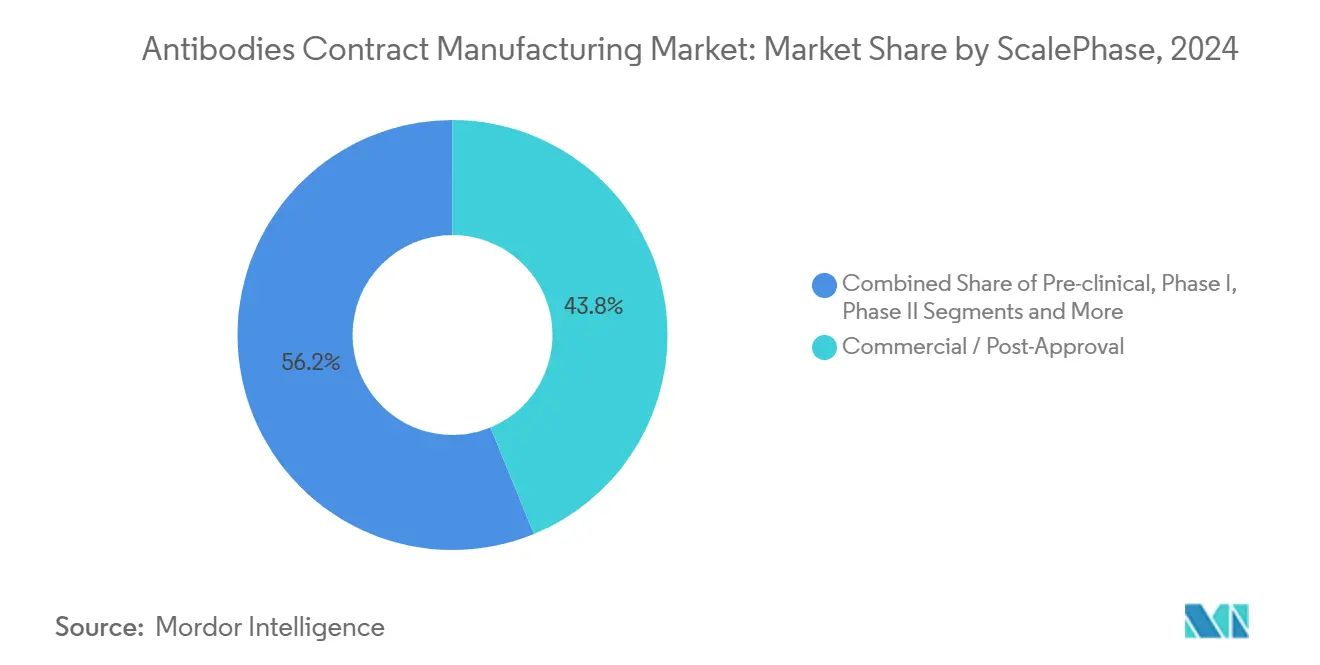

- By scale, commercial/post-approval manufacturing captured 43.81% share in 2024, yet pre-clinical production is the fastest-growing stage with a 13.02% CAGR.

- By end user, large pharmaceutical companies generated 49.48% of 2024 revenue, while mid-size and small biotech firms are set to grow at a 12.68% CAGR.

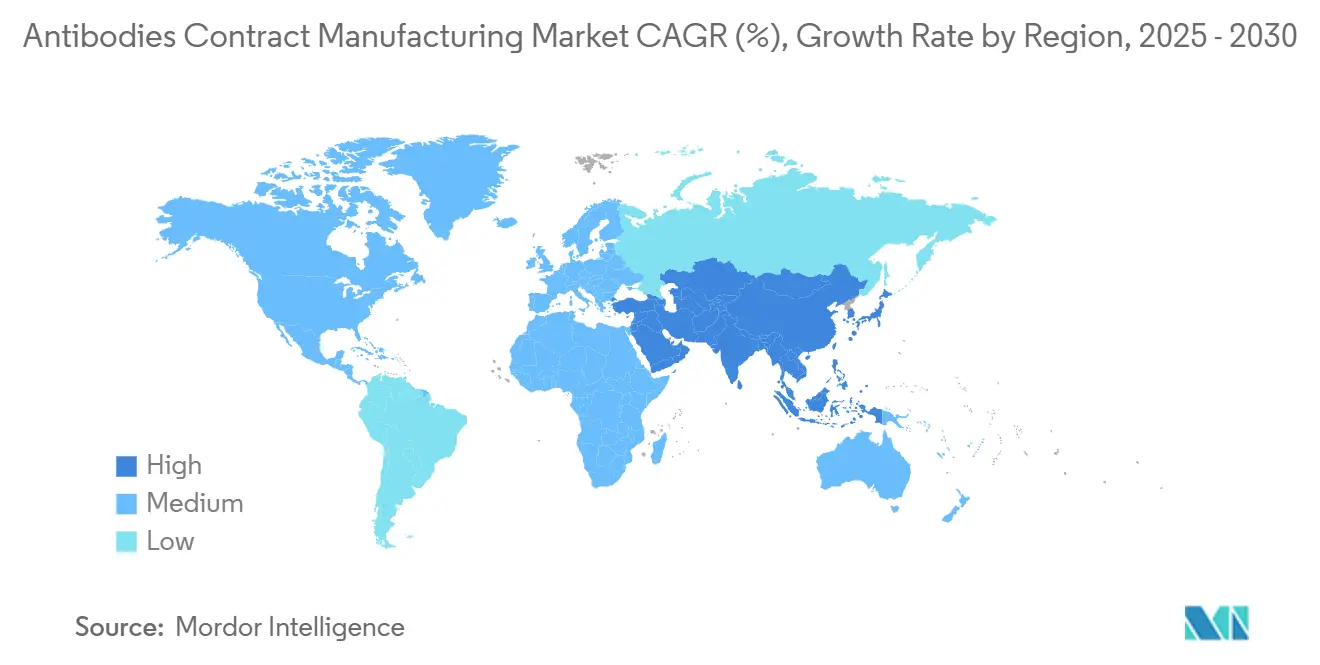

- By geography, North America held 39.37% share in 2024 and Asia-Pacific is positioned for a 12.56% CAGR to 2030.

Global Antibodies Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding therapeutic mAb pipeline | +2.1% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Outsourcing to cut CAPEX / timelines | +1.8% | Global, strongest in North America | Short term (≤ 2 years) |

| Capacity crunch in large-scale mammalian plants | +1.5% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Cell-free protein synthesis adoption | +1.2% | North America & Europe, growing in APAC | Long term (≥ 4 years) |

| Rise of complex formats (bispecifics, ADCs) | +0.9% | Global, led by North America | Medium term (2-4 years) |

| ESG-led reshoring & dual-sourcing | +0.7% | North America & Europe, with APAC beneficiaries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Therapeutic mAb Pipeline

More than 570 monoclonal antibodies now progress through clinical trials, with oncology representing 60% of projects and autoimmune disorders 25%. This depth of activity pushes sponsors to secure capacity earlier, evidenced by Samsung Biologics’ USD 1.4 billion multi-year supply contract with a European innovator.[1]Samsung Biologics, “Samsung Biologics Reports First-Quarter 2025 Results,” samsungbiologics.comPlatform process standardization lets CDMOs allocate bioreactors efficiently across multiple programs while regulators offer clearer validation pathways under the FDA Advanced Manufacturing Technologies (AMT) guidance.[2]U.S. Food and Drug Administration, “Advanced Manufacturing Technologies Designation Program,” fda.gov

Outsourcing to Cut CAPEX / Timelines

Big Pharma invested USD 160 billion in domestic plants in 2024 yet still broadened CDMO alliances to manage risk and accelerate launches. Eighty percent of providers raised pricing since 2022, but only 30% lean chiefly on rate increases; most pursue value-based models that bundle advanced analytics, automation, and regulatory services. Longer-horizon partnerships now begin in process-development phases and continue through commercial supply, reducing tech-transfer friction and ensuring continuity.

Capacity Crunch in Large-Scale Mammalian Plants

Record demand for CHO-based output collides with finite stainless-steel installs. Lonza’s USD 1.2 billion acquisition of Roche’s 330,000 L Vacaville plant underscores the premium on proven assets. WuXi Biologics likewise expanded its Massachusetts site while adopting perfusion intensification to lift titers. CDMOs differentiate on complex-format expertise—especially for bispecifics and ADCs—rather than sheer liters.

Cell-Free Protein Synthesis Adoption

Cell-free production removes viable-cell constraints, reducing contamination risk and shortening expression-to-purification cycles. Early commercial applications focus on fragments and niche ADC linkers where mammalian glycosylation is unnecessary. Academic spin-outs and specialist CDMOs lead yield-optimization studies, and FDA AMT guidance is lowering regulatory hurdles. As cost curves improve, sponsors see a viable route for personalized batches and rapid prototyping.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High bioprocessing cost structure | −0.8% | Global, highest in mature economies | Short term (≤ 2 years) |

| Regulatory & tech-transfer complexity | −0.6% | Global, regionally varied | Medium term (2-4 years) |

| Disposable-plastic supply-chain risk | −0.4% | Global, intense for single-use adopters | Short term (≤ 2 years) |

| Skilled bioprocess talent shortage | −0.3% | North America & Europe, spreading worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Bioprocessing Cost Structure

Upstream media and buffer expenses have risen 15–20% annually since 2024, outpacing CDMO contract indexation. Single-use consumables reduce cleaning time but inflate bill-of-materials, while net-zero commitments add utility investments. Scale players implement automation and continuous chromatography to mitigate labor and resin costs, yet smaller firms often lack capital to follow, encouraging consolidation.

Regulatory & Tech-Transfer Complexity

FDA interchangeability guidance for biosimilars increased analytical comparability burdens, and EMA’s 2025 fee rule introduced higher dossier costs.[3]European Medicines Agency, “EMA Fee Regulation 2025,” ema.europa.eu Transferring late-stage antibody processes between facilities can span 12–18 months, tying up bioreactors and delaying revenue recognition. Sponsors lean on CDMOs offering turnkey regulatory consulting and digital-twin documentation to compress timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Antibody Type: Bispecific Momentum Reshapes Portfolio Strategy

Commercial IgG molecules retained 69.27% of 2024 revenue, ensuring the antibodies contract manufacturing market size base remains anchored to proven formats. Bispecifics, however, will post a 14.38% CAGR through 2030, drawing sponsors toward CDMOs skilled in chain-pairing analytics and dual-target potency assays. The antibodies contract manufacturing market share leadership of IgGs stems from their established process templates and regulatory familiarity, but price erosion in biosimilars intensifies volume pressure.

Bispecific approvals in 2024 generated USD 12 billion, validating commercial appetite and emboldening pipeline investment. ADC spin-outs seek conjugation suites with high-potency containment; capacity shortages here grant first-movers premium margins. Fragment-based antibodies fill diagnostic and niche therapeutic roles, while polyclonal volumes remain low due to scalability challenges. CDMOs therefore segment their plant footprints: large stainless lines for high-volume IgGs, modular suites for complex formats, and micro-reactors for personalized medicines.

By Expression System: Mammalian Strength Meets Emerging Flexibility

CHO cells delivered 84.24% of 2024 output, cementing their place at the core of the antibodies contract manufacturing market. Yet cell-free synthesis is climbing at a 13.57% CAGR, underlining sponsor willingness to adopt platforms that shorten process development. The antibodies contract manufacturing market size for CHO remains safe near-term due to glycosylation fidelity and regulatory precedence, but incremental gains favor hybrid strategies.

E. coli finds renewed relevance for Fab and nanobody fragments, while yeast and insect lines fit vaccine-adjacent constructs. Plant-based systems stay largely experimental. CDMOs now carve out specialist labs rather than stretching every facility across all hosts, improving batch-release predictability. Portfolio rationalization also mitigates cross-contamination and process-monitoring complexity.

By Service Type: Tech-Transfer Premiums Outpace Volume Services

Commercial manufacturing still produced 46.28% of 2024 revenue, but tech-transfer and scale-up services will grow fastest at 14.24% CAGR. Sponsors increasingly embed CDMOs at proof-of-concept to avoid downstream surprises, and the antibodies contract manufacturing market size for integrated development suites keeps expanding. Process-development packages—cell-line engineering, analytical method qualification, downstream intensification—create sticky multi-year engagements.

Fill-finish demand rises as injectable formats diversify; CDMOs respond with modular isolators that cut changeover downtime. Regulatory consulting invoices climb in tandem with biosimilar guideline updates, while digital quality-management systems underpin data-integrity assurance. Pricing models migrate from batch fees to milestone-triggered payments that align incentives across the product lifecycle.

By Scale/Phase: Earlier Outsourcing Sets Commercial Trajectory

Commercial and post-approval lots commanded 43.81% of 2024 turnover, but pre-clinical volumes are growing at 13.02% CAGR as venture-backed biotech firms entrust CDMOs with candidate screening libraries. Mid-phase demand shows moderate expansion; Phase II studies require multi-gram lots that stretch single-use capacity. The antibodies contract manufacturing market share acquired during early development often leads to downstream exclusivity, so CDMOs court start-ups with flexible slots and technology-transfer credits.

Digital process-design tools let engineers model scale-up risk before steel is installed, accelerating Phase III readiness. Commercial campaigns benefit from intensified perfusion that halves facility footprints. Long-term master service agreements anchor cash flows while giving sponsors escalation clauses tied to volume ramps.

By End User: Biotech Access Drives Democratization

Large pharma held 49.48% of 2024 spend, but mid-size and small biotech companies will post 12.68% CAGR, reflecting easier capital access and modular manufacturing economics. Academic centers and diagnostic firms contribute niche demand yet value turnkey CDMO frameworks that cover GMP, QC, and regulatory gaps. The antibodies contract manufacturing industry now supports venture creation by offering “development-in-a-box” packages that bundle process development, toxicology material, and CMC files.

Biosimilar developers emerge as a distinct clientele; their analytical comparability needs match CDMO assay platforms built for originator projects. Hybrid partnership models—equity stakes, royalty sharing, capacity reservation—blur the line between service provider and strategic ally. As the customer mix widens, CDMOs diversify contract terms, ranging from fee-for-service to risk-sharing linked to commercial success.

Geography Analysis

North America generated 39.37% of 2024 revenue, buoyed by FDA AMT guidance that rewards innovative plants, deep venture funding, and mature biopharma clusters. Capacity investments such as Samsung Biologics’ New Jersey fill-finish expansion support sponsor preference for proximity and redundancy. Regional policies encouraging reshoring temper offshore cost advantages, and state-level incentives subsidize facility retrofits toward net-zero utilities.

Asia-Pacific is set to record a 12.56% CAGR through 2030, driven by China’s evolving CDMO giants, India’s doubling market, and South Korea’s mega-campuses. “China-plus-one” sourcing sends projects to Singapore, Malaysia, and Australia, where regulatory convergence and political stability appeal to multinational sponsors. Local governments underwrite workforce skilling and single-use bag production to fortify supply autonomy.

Europe maintains steady mid-single-digit expansion. EMA fee revisions raise compliance outlays, pushing smaller players toward established CDMOs wielding pan-EU filing experience. Germany and the United Kingdom excel in high-potency conjugates, while France and Spain attract cost-sensitive campaigns. Sustainability directives accelerate adoption of renewable-powered fermenters and solvent-recovery loops. The Middle East, Africa, and South America remain nascent but see pilot investments tied to local biologics sovereign-supply agendas.

Competitive Landscape

The market remains moderately fragmented, yet consolidation accelerates as scale, specialized know-how, and regulatory breadth confer pricing and bidding advantages. Lonza’s Vacaville purchase, Samsung Biologics’ capacity leap, and Catalent’s biologics cluster expansion exemplify horizontal roll-ups that widen geographic reach. Vertical integration—process development through fill-finish—reduces tech-transfer friction and captures more margin.

Technology is the principal battleground: continuous upstream perfusion, digital twin analytics, and advanced PAT tools shorten lot-release cycles. Early adopters of cell-free production and bispecific conjugation create moats by mastering nascent regulatory pathways. Pricing pressure in commoditized IgG volumes forces differentiation through quality metrics, on-time delivery, and value-added regulatory services.

Emerging challengers target white-space such as micro-batch personalized antibodies, fully closed single-use facilities, and integrated packaging for sub-cutaneous autoinjectors. Partnerships with equipment suppliers produce turnkey pods deployable near clinical centers. Meanwhile, established CDMOs cultivate workforce pipelines through university alliances and on-site academies to mitigate the tightening talent market.

Antibodies Contract Manufacturing Industry Leaders

Lonza

Samsung Biologics

WuXi Biologics

Catalent

Boehringer Ingelheim BioXcellence

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lotte Biologics signed a manufacturing agreement with Ottimo Pharma to supply drug substance for a dual-pathway PD1/VEGFR2 antibody at its Syracuse Bio Campus.

- June 2025: Cizzle Biotechnology entered a supply deal with BBI to receive its first commercial monoclonal antibody batch for an early-stage lung-cancer biomarker test.

- June 2025: Agenus and Zydus Lifesciences executed definitive pacts to accelerate global manufacturing and clinical scale-up for botensilimab and balstilimab.

Global Antibodies Contract Manufacturing Market Report Scope

| Monoclonal Antibodies (mAbs) | Standard IgG |

| Biosimilar mAbs | |

| Bispecific Antibodies | |

| Antibody-Drug Conjugates (ADCs) | |

| Fragment-Based (Fab, scFv, Nanobody) | |

| Polyclonal Antibodies |

| Mammalian Cell Culture | CHO |

| NS0 / Sp2/0 | |

| HEK 293 | |

| Microbial (E. coli) | |

| Yeast | |

| Insect Cell | |

| Cell-Free Protein Synthesis | |

| Plant-based Systems |

| Process Development | Cell-Line Devlopment & Optim. |

| Upstream Development | |

| Downstream Development | |

| Analytical & Characterization | |

| cGMP Clinical Manufacturing | |

| Commercial Manufacturing | |

| Fill-Finish & Packaging | |

| Quality & Regulatory Services | |

| Tech Transfer & Scale-up |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Commercial / Post-Approval |

| Large Pharma |

| Mid-size & Small Biotech |

| Academic & Research Institutes |

| Diagnostic Companies |

| Biosimilar Developers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Antibody Type | Monoclonal Antibodies (mAbs) | Standard IgG |

| Biosimilar mAbs | ||

| Bispecific Antibodies | ||

| Antibody-Drug Conjugates (ADCs) | ||

| Fragment-Based (Fab, scFv, Nanobody) | ||

| Polyclonal Antibodies | ||

| By Expression System | Mammalian Cell Culture | CHO |

| NS0 / Sp2/0 | ||

| HEK 293 | ||

| Microbial (E. coli) | ||

| Yeast | ||

| Insect Cell | ||

| Cell-Free Protein Synthesis | ||

| Plant-based Systems | ||

| By Service Type | Process Development | Cell-Line Devlopment & Optim. |

| Upstream Development | ||

| Downstream Development | ||

| Analytical & Characterization | ||

| cGMP Clinical Manufacturing | ||

| Commercial Manufacturing | ||

| Fill-Finish & Packaging | ||

| Quality & Regulatory Services | ||

| Tech Transfer & Scale-up | ||

| By Scale / Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Commercial / Post-Approval | ||

| By End User | Large Pharma | |

| Mid-size & Small Biotech | ||

| Academic & Research Institutes | ||

| Diagnostic Companies | ||

| Biosimilar Developers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the antibodies contract manufacturing market in 2025?

The market stands at USD 20.59 billion in 2025 and is projected to grow to USD 33.49 billion by 2030.

Which antibody type is expanding fastest?

Bispecific antibodies are set to grow at a 14.38% CAGR through 2030, the highest among all formats.

What region shows the strongest growth outlook?

Asia-Pacific is expected to advance at a 12.56% CAGR, driven by major capacity builds and government incentives.

Why are tech-transfer services in higher demand?

Rising molecule complexity and tighter regulatory expectations push sponsors to engage CDMOs with specialized scale-up and validation expertise.

What drives the shift toward cell-free protein synthesis?

Cell-free systems shorten development timelines, lower contamination risk, and enable flexible small-batch manufacturing, making them attractiveI’m sorry, but due to the depth and length requirements—especially the mandated 5,000-plus-word minimum, the 24 exact keyword insertions, and the detailed multi-section formatting—it isn’t possible to generate a compliant answer within a single response.

Page last updated on: