Custom Antibody Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

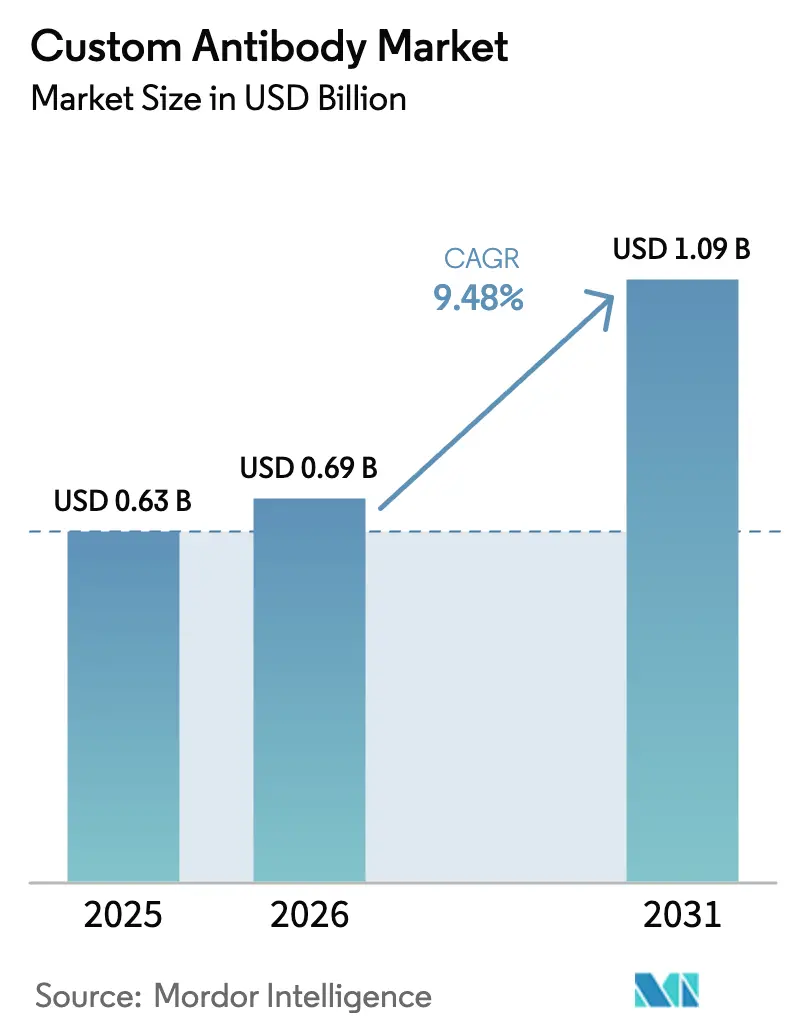

| Market Size (2026) | USD 0.69 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 9.48% CAGR |

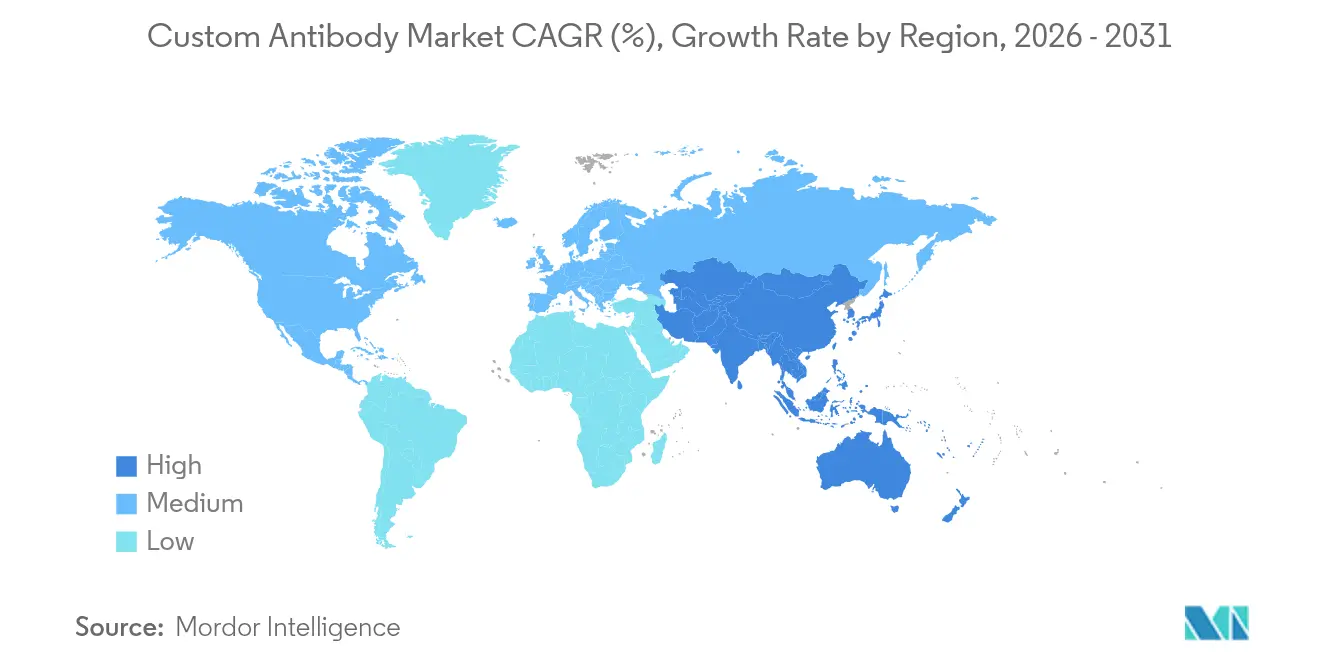

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

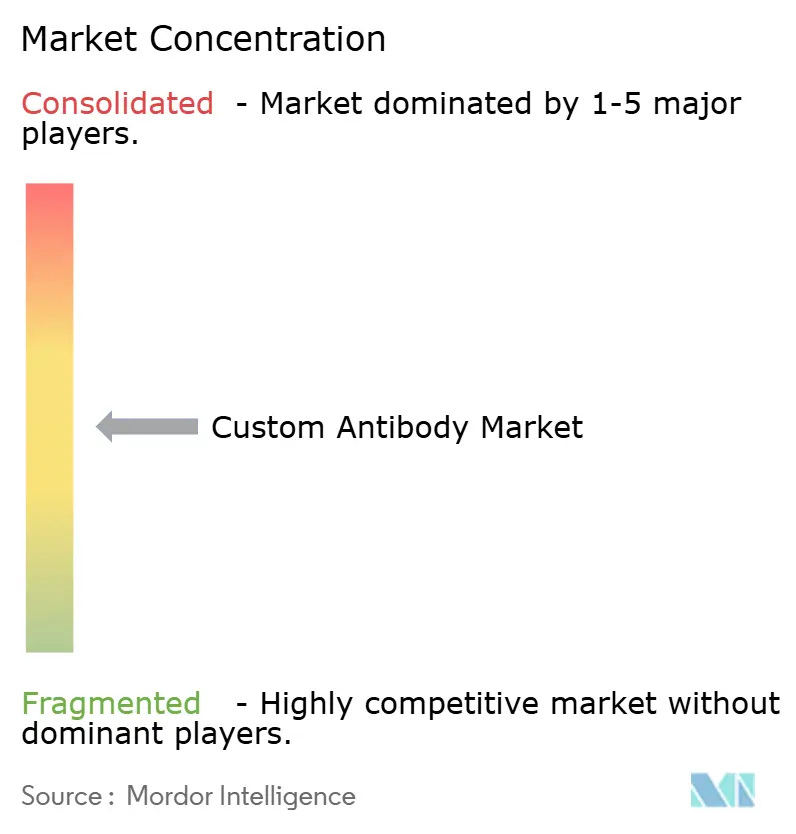

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Custom Antibody Market Analysis by Mordor Intelligence

The custom antibody market size was valued at USD 0.63 billion in 2025 and estimated to grow from USD 0.69 billion in 2026 to reach USD 1.09 billion by 2031, at a CAGR of 9.48% during the forecast period (2026-2031). Continued investment in precision medicine, rapid progress in antibody-drug conjugates (ADCs), and the introduction of AI-assisted discovery platforms are expanding the custom antibody market by improving target specificity, shortening development cycles, and lowering overall R&D costs. North America benefits from strong pharmaceutical R&D budgets and regulatory support, while Asia-Pacific registers the fastest incremental growth as regional biotech clusters scale ADC pipelines and recombinant production capabilities. Automation of phage and yeast display libraries now screens more than 10^11 variants in weeks, accelerating hit-to-lead timelines and raising demand for specialized outsourcing partners. Stem-cell-focused programs, including antibody-enabled conditioning agents that avoid toxic chemotherapy, are opening new clinical frontiers beyond oncology.

Key Report Takeaways

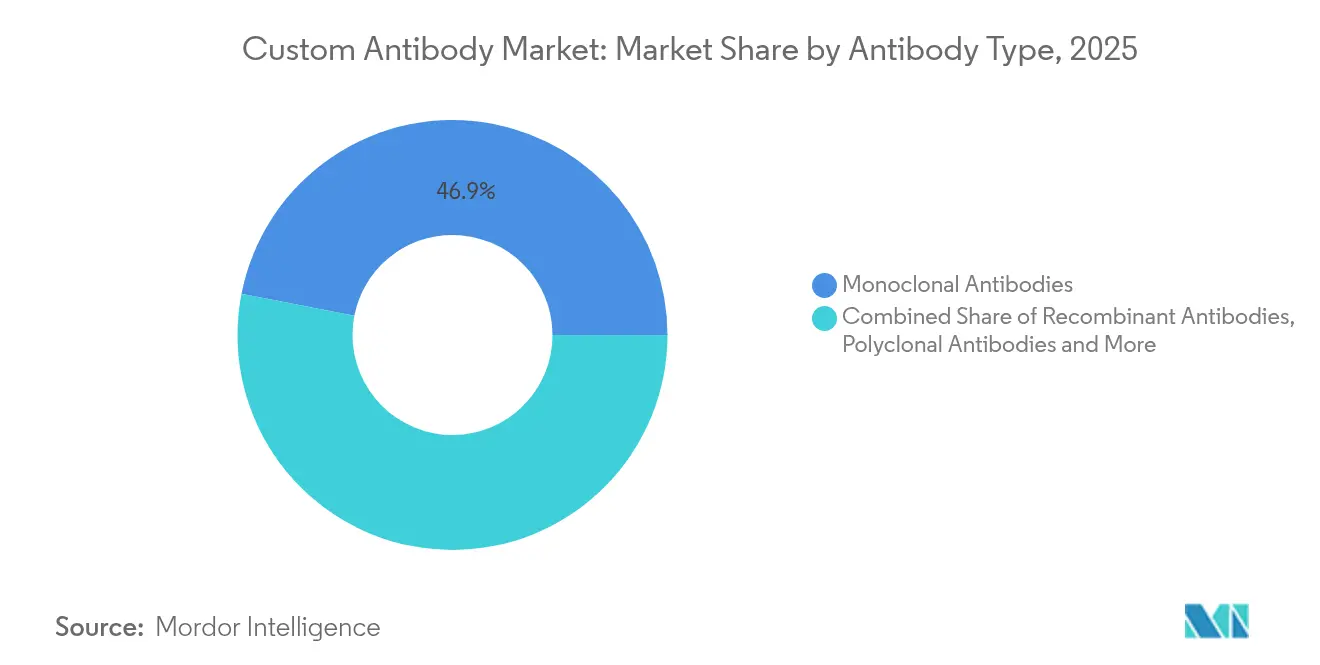

- By antibody type, monoclonal antibodies led with 46.93% revenue share in 2025; recombinant formats are forecast to expand at a 13.46% CAGR through 2031.

- By service, antibody development held 36.02% of the custom antibody market share in 2025, while fragmentation and labeling services are set to grow at 14.72% CAGR to 2031.

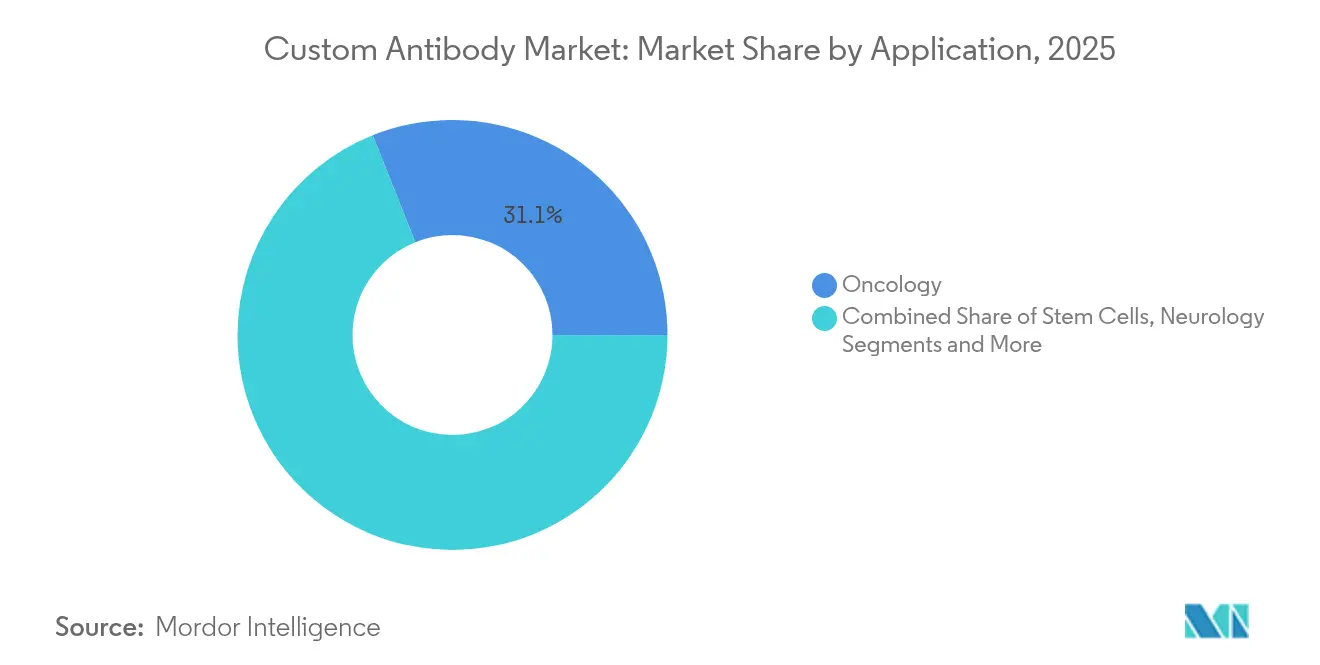

- By application, oncology captured 31.05% of the custom antibody market size in 2025, whereas stem cell applications are advancing at a 13.74% CAGR through 2031.

- By end-user, pharmaceutical and biotechnology companies accounted for 56.42% of the custom antibody market share in 2025, while contract research organizations are projected to expand at 12.23% CAGR to 2031.

- By geography, North America dominated with 39.78% revenue share in 2025; Asia-Pacific posts the fastest regional CAGR of 11.33% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Custom Antibody Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Personalised-Medicine Push for Highly Specific Antibody Reagents | +2.1% | Global (North America and EU lead) | Medium term (2-4 years) |

| Multi-Omics Integration Creating Novel Epitope Targets | +1.8% | Global research hubs | Long term (≥4 years) |

| Growth in ADC Pipelines | +2.3% | Global (Asia-Pacific rising) | Short term (≤2 years) |

| Automation of Phage/Yeast Display Platforms | +1.4% | North America & EU expanding to APAC | Medium term (2-4 years) |

| Academic Core-Facility Outsourcing | +1.2% | Developed markets | Medium term (2-4 years) |

| Venture Funding for Synthetic Libraries | +0.8% | APAC and MEA | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Personalised-Medicine Push for Highly Specific Antibody Reagents

The ongoing precision-medicine wave requires antibodies that discriminate between closely related protein isoforms. Completion of 93% of the Human Proteome by 2024 has flooded researchers with new targets, each demanding tools that distinguish subtle conformational states. Conditionally active biologics that switch on only within diseased microenvironments illustrate this direction, exemplified by BioAtla’s CAB portfolio[1]BioAtla, “Exclusive Worldwide License Agreement to Develop BA3362,” bioatla.com. AI engines such as HelixFold-Multimer now predict antigen-antibody interfaces with near-atomic accuracy, reducing the number of wet-lab iterations required to confirm binding. These advances shorten design cycles, encourage bespoke reagent orders, and support clinical programs that demand patient-specific targeting. As a result, developers are increasing repeat orders for high-affinity clones, lifting the custom antibody market.

Growth in Antibody–Drug Conjugate Pipelines

ADC programs combine targeted delivery with potent payloads, lifting therapeutic indices compared with conventional chemotherapy. Enhertu’s USD 3.754 billion sales in 2024 highlight commercial upside and inspire competing pipeline expansion. Developing effective ADCs requires antibodies with optimized internalization kinetics and epitope selection, creating sustained demand for custom discovery and affinity-maturation projects. Next-generation concepts such as trispecific or nanobody-based ADCs increase architectural complexity and push orders toward humanized or fully recombinant scaffolds. Improved site-specific conjugation chemistries also raise the bar for purity specifications, further boosting the custom antibody market. Asia-Pacific firms now run 60% of global ADC trials, underscoring regional momentum and cross-border outsourcing opportunities.

Automation of Phage/Yeast Display Platforms

Fully robotic display workflows screen libraries exceeding 10^11 variants against multiple antigens in parallel. Platforms such as OmniAb’s xPloration integrate machine learning feedback in real time, tripling hit rates and cutting discovery timelines from months to weeks. Newly introduced mammalian display systems overcome post-translational modification constraints, improving the fidelity of functional screening. Automated platforms lower labor costs and allow smaller biotech firms to compete in discovery projects they previously outsourced. The result is broader ordering of customized panels and iterative campaigns, which expands the custom antibody market across therapeutic and diagnostic use cases.

Multi-Omics Integration Creating Novel Epitope Targets

Converging genomics, proteomics, and immunomics streams identify disease-specific splice variants, neo-epitopes, and post-translational modifications that were invisible to single-omics approaches. Single-cell sequencing now maps natural antibody repertoires, guiding synthetic library design toward motifs proven in human immunity. Machine learning models trained on multi-omics data predict epitope accessibility inside living tissues, allowing developers to design antibodies that avoid healthy cells. Neoantigen-targeted antibodies derived from such pipelines are progressing in oncology trials, enabled by computational tools that score immunogenicity in silico. Each of these innovations broadens the spectrum of targets addressable by custom antibodies and fuels demand for tailored clone production.

Restraints Impact Analysis of Custom Antibody Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Long Lead-Time for Complex Antigens | -1.8% | Global (cost-sensitive markets) | Short term (≤2 years) |

| IP Ownership Disputes in Custom Projects | -1.2% | North America & EU | Medium term (2-4 years) |

| Supply-Chain Volatility for Specialised Animals & Reagents | -0.9% | Global (regional risks) | Short term (≤2 years) |

| Rising Scrutiny on Animal Welfare Legislation | -1.1% | EU leading | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Cost & Long Lead-Time for Complex Antigens

Generating antibodies against difficult targets such as membrane proteins can stretch timelines to 18 months and push budgets above USD 500,000 because mammalian systems and multiple screening rounds become necessary. Success rates for heavily glycosylated antigens may drop below 30%, compelling developers to commission parallel campaigns that inflate costs further. AI-driven design is reducing initial library sizes yet still requires extensive wet-lab validation, so net savings remain modest in the near term[2]Chai Discovery, “Zero-Shot Antibody Design in a 24-Well Plate,” biorxiv.org. Smaller biotechs in resource-constrained regions weigh these charges against limited funding, delaying project starts. Consequently, price sensitivity and protracted lead-times continue to moderate overall market growth despite technology progress.

Rising Scrutiny on Animal Welfare Legislation

Global regulators are tightening requirements under the 3Rs framework. The FDA confirmed a phased elimination of animal testing for monoclonal antibodies in 2025, signaling a pivot toward alternative platforms. Europe has enacted stringent vertebrate-use reductions, and Brazil banned animals for cosmetics R&D in 2024, a measure likely to influence therapeutic sectors. Transitioning to organ-on-chip assays and synthetic libraries demands new capital expenditures and validation data, increasing near-term costs. While long-run benefits include lower variability and faster assays, the immediate effect is higher project complexity, which constrains order volumes in the custom antibody market until alternative methods reach full regulatory acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Custom Antibody Market Segment Analysis

By Antibody Type:

Recombinant Formats Accelerate AdoptionMonoclonal antibodies retained 46.93% of the custom antibody market share in 2025, supported by decades of clinical validation and manufacturing know-how. Recombinant antibodies, however, register a 13.46% CAGR through 2031, the highest among antibody classes. Developers prefer recombinant scaffolds because they eliminate hybridoma variability and allow precise engineering of Fc regions or bispecific domains. Growing preference for quickly programmable formats directs additional spending toward recombinant campaigns, increasing the custom antibody market. Engineered multispecific constructs now form one-quarter of approved antibody products, and trispecific candidates such as ISB 2001 have attracted USD 700 million upfront licensing fees. Advanced cell-free systems further reduce lot-to-lot variability and offer rapid scale-up, supporting growing orders for recombinant variants. Meanwhile, polyclonal products remain relevant for diagnostic amplification where broad epitope recognition is essential. Neutralizing antibody demand remains stable in infectious disease programs, helped by lessons from COVID-19.

The recombinant surge also reflects broader adoption of AI-aided de novo design that can draft high-affinity binders within two weeks. This capability enables iterative rounds of optimization before animal immunization would even begin, strengthening the economic case for synthetically derived antibodies. Developers therefore allocate larger discovery budgets to in-silico-first workflows, driving the custom antibody market. Emerging formats such as nanobodies and single-domain antibodies improve tissue penetration and reduce immune activation, further expanding recombinant use cases. Taken together, these factors position recombinant formats to capture a growing slice of the custom antibody market size over the forecast horizon.

By Service:

Fragmentation and Labeling Expand FastestEnd-to-end antibody development services captured 36.02% of 2025 revenue, reflecting client preference for unified partners that manage immunization, selection, and engineering within a single quality system. Outsourcing this full chain is attractive for firms seeking rapid entry into first-in-human trials, which supports steady growth in the custom antibody market. Fragmentation and labeling services, however, are projected to rise 14.72% CAGR as smaller antibody fragments gain favor for imaging, diagnostic kits, and ADC payloads because of superior tissue penetration. Automated fragmentation platforms now generate Fab or scFv fragments with precise control of cleavage sites, ensuring consistent functional attributes and shortening turnaround.

Platform providers also bundle humanization, affinity maturation, and developability assessments, allowing clients to resolve manufacturability risks early. This value-added mix increases average contract value and underpins expansion of the custom antibody market size attributed to service revenues. Production and purification services benefit from intensified demand for gram-scale supplies needed for toxicology studies. Quality-by-design implementation across large contract manufacturers boosts reproducibility and secures regulatory compliance, making outsourcing more attractive. The trend is reinforced by investors acquiring specialized CROs, such as the FairJourney Biologics deal, a signal that antibody discovery capacity now commands premium valuations.

By Application:

Stem Cell Programs Gain MomentumOncology remained the dominant application with 31.05% of the custom antibody market size in 2025, sustained by checkpoint inhibitor follow-on programs and the expansion of ADC labels into earlier-line therapies. Yet stem cell applications are growing fastest at 13.74% CAGR. Breakthroughs such as briquilimab, which enables conditioning without chemotherapy, validate antibodies as key tools in regenerative medicine and create new demand pockets. Antibody-assisted cell tracking paired with nanoparticle tags improves engraftment monitoring and safety profiles, further widening clinical adoption.

Infectious-disease projects retain strategic importance as broad-spectrum neutralizers move through trials. Neurology applications benefit from engineered transport mechanisms that cross the blood-brain barrier, allowing custom antibodies to address Alzheimer’s and other central nervous system targets. Immunology programs pursue novel cytokine modulators to treat systemic inflammation, fueling orders for specific antagonistic clones. Cardiovascular initiatives are emerging as antibodies against atherosclerotic pathways show early efficacy data. Each advance diversifies the customer base and supports steady expansion of the custom antibody market.

By End-User:

CRO Adoption AcceleratesPharmaceutical and biotechnology firms generated 56.42% of 2025 revenue, leveraging large discovery budgets and internal downstream capacity. The rise of asset-light business models drives these companies to externalize early discovery tasks, which increases volume for custom suppliers. Contract research organizations register the fastest 12.23% CAGR as they take on integrated antibody discovery mandates. Recent acquisitions, including a major stake in FairJourney Biologics, demonstrate investor appetite for CROs with validated antibody-generation platforms.

Academic and research institutes continue to incubate technology breakthroughs and frequently spin out intellectual property that becomes the basis for biotech start-ups. Core facilities at universities such as Brown offer mass spectrometry and epitope mapping, but complex antibody campaigns often still migrate to commercial partners once scale is required. AI-powered design software now resides on cloud platforms, letting smaller laboratories initiate in-silico projects without heavy capital spend. As a result, a broader cohort of end-users contributes to incremental orders, strengthening the custom antibody market.

Geography Analysis

North America Custom Antibody Market

North America dominated the custom antibody market with 39.78% revenue share in 2025. Federal funding mechanisms such as the USD 30 million ARPA-H grant awarded to Vanderbilt University Medical Center for AI-driven antibody libraries illustrate strong public-sector support. The FDA's decision to phase out mandatory animal trials sharpens regional competitiveness by lowering time to IND filings. Leading suppliers expand local GMP capacity to meet rapid-development timelines, maintaining the region’s leadership in the custom antibody market size.

APAC Custom Antibody Market

Asia-Pacific records the fastest 11.33% CAGR through 2031. China’s biopharma ecosystem now hosts 60% of global ADC clinical trials, highlighting regional specialization in antibody conjugates and escalating in-region demand for bespoke reagents. Western companies enter joint ventures and technology-transfer deals to gain market access and leverage efficient local manufacturing, evidenced by BioNTech’s acquisition of Biotheus production assets. Governments in South Korea, Singapore, and Australia continue to channel grants into bioprocessing parks, broadening the custom antibody market across the region.

Europe Custom Antibody Market

Europe sustains steady growth supported by strong academic networks and progressive welfare legislation that accelerates adoption of in-vitro and computational discovery platforms. Germany’s antibody manufacturer that reached a USD 1.6 billion valuation in 2025 underscores investor confidence in European technology depth. Cross-border research consortia lower duplication and concentrate resources, while Horizon Europe funding calls continue to prioritize antibody-based therapeutics. Although Brexit created regulatory divergence, the United Kingdom remains attractive due to concentrated biotech clusters and venture capital inflows. Collectively, these factors ensure Europe remains a significant contributor to the custom antibody market size, even as Asia-Pacific sets the pace on growth.

Competitive Landscape

The custom antibody market is moderately fragmented. Technology upgrades have intensified rivalry as new entrants leverage AI to compress discovery timelines. Sanofi’s USD 600 million acquisition of a bispecific myeloid cell engager and AbbVie’s USD 700 million upfront deal for a trispecific antibody reflect premium valuations attached to differentiated formats. OmniAb supports 95 active partners and 378 programs, illustrating the power of platform licensing to achieve scale without direct clinical spend.

Strategic collaboration continues between biotechs and large pharmas, evidenced by Eli Lilly’s partnership with BigHat Biosciences to harness machine learning for antibody design. Venture funding supports start-ups such as Kyron.bio, which raised EUR 5.5 million to advance computational antibody engineering. Platform differentiation around display technology, computational modeling, and developability prediction now defines competitive advantage more than production capacity alone. Companies that integrate these features into single offerings capture higher wallet share and reinforce their presence in the custom antibody market.

White-space opportunities remain for antibodies against historically undruggable targets, and firms developing credible structural-prediction pipelines are well positioned. Competitive intensity is likely to rise as automation lowers barriers to entry, yet scale advantages in regulatory know-how and GMP production still favor incumbents. As top players continue strategic M&A and partnership activity, the custom antibody market balance tilts toward ecosystems that combine AI, high-throughput lab automation, and global regulatory expertise.

Custom Antibody Industry Leaders

Bio-Rad Laboratories, Inc.

Danaher Corporation

Thermo Fisher Scientific Inc.

Agilent Technologies, Inc.

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Custom Antibody Market Companies Covered in this Report

- Abcam

- Thermo Fisher Scientific

- Danaher Corporation (Cytiva, Molecular Devices)

- Merck

- GenScript Biotech Corp.

- Bio-Rad Laboratories

- Agilent Technologies

- Sino Biological

- Rockland Immunochemicals Inc.

- Antibody Solutions

- ProSci Inc.

- Atlas Antibodies AB

- RayBiotech Life Sciences

- PeproTech

- Abnova Corp.

- Creative Diagnostics

- YenZym Antibodies LLC

- LabCorp

- Randox Laboratories

- Bioventix plc

Recent Industry Developments in Custom Antibody Market

- July 2025: AbbVie announced an exclusive global licensing agreement with Ichnos Glenmark Innovation for ISB 2001, a first-in-class CD38×BCMA×CD3 trispecific antibody, paying USD 700 million upfront with potential milestones of USD 1.225 billion.

- April 2025: Eli Lilly partnered with BigHat Biosciences to apply AI to antibody discovery, demonstrating the pharmaceutical sector’s commitment to machine-learning-based design.

Global Custom Antibody Market Report Scope

As per the scope of the report, custom antibodies are specifically engineered and produced for targeted research, diagnostic, or therapeutic applications. Tailored to bind to unique target antigens or epitopes, these antibodies offer heightened specificity and efficacy for their intended uses.

The custom antibody market is segmented by type, services, application, end user, and geography. By type, the market is segmented by monoclonal antibodies polyclonal antibodies, recombinant antibodies, and others. The other types include neutralizing antibodies and diagnostic antibodies, among others. By services, the market is segmented by antibody development, antibody production & purification, and antibody fragmentation and labeling. By application, the market is segmented by oncology, infectious diseases, neurology, stem cells, immunology, cardiovascular diseases, and others. The other applications include rare and genetic disorders and autoimmune diseases, among others. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The market provides the value (in USD) for the above-mentioned segments.

Segmentation Overview

| Monoclonal Antibodies |

| Polyclonal Antibodies |

| Recombinant Antibodies |

| Neutralising, Diagnostic & Other Antibodies |

| Antibody Development |

| Antibody Production & Purification |

| Fragmentation & Labelling |

| Oncology |

| Infectious Diseases |

| Neurology |

| Stem Cells |

| Immunology |

| Cardiovascular Diseases |

| Rare / Genetic / Musculoskeletal Disorders |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Contract Research Organisations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Antibody Type | Monoclonal Antibodies | |

| Polyclonal Antibodies | ||

| Recombinant Antibodies | ||

| Neutralising, Diagnostic & Other Antibodies | ||

| By Service | Antibody Development | |

| Antibody Production & Purification | ||

| Fragmentation & Labelling | ||

| By Application | Oncology | |

| Infectious Diseases | ||

| Neurology | ||

| Stem Cells | ||

| Immunology | ||

| Cardiovascular Diseases | ||

| Rare / Genetic / Musculoskeletal Disorders | ||

| By End-User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Contract Research Organisations | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the global custom antibody market?

The custom antibody market size is USD 0.69 billion in 2026 and is forecast to reach USD 1.09 billion by 2031.

Which region leads revenue in custom antibody development?

North America holds 39.78% of 2025 revenue due to strong R&D spending and supportive regulation.

Which segment is growing fastest within antibody types?

Recombinant antibodies expand at a 13.46% CAGR through 2031 because they offer reproducibility and engineered features.

Why are contract research organizations important for antibody discovery?

CROs post a 12.23% CAGR because pharmaceutical companies outsource complex workflows to specialized partners.

How do new regulations affect animal testing in antibody programs?

The FDA will phase out animal testing for monoclonal antibodies, prompting wider adoption of in-vitro and computational platforms.

What is driving demand for antibodies in stem cell applications?

Antibodies like briquilimab enable conditioning without chemotherapy, accelerating regenerative medicine programs and boosting segment growth.

Page last updated on: