Next-Generation Antibody Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

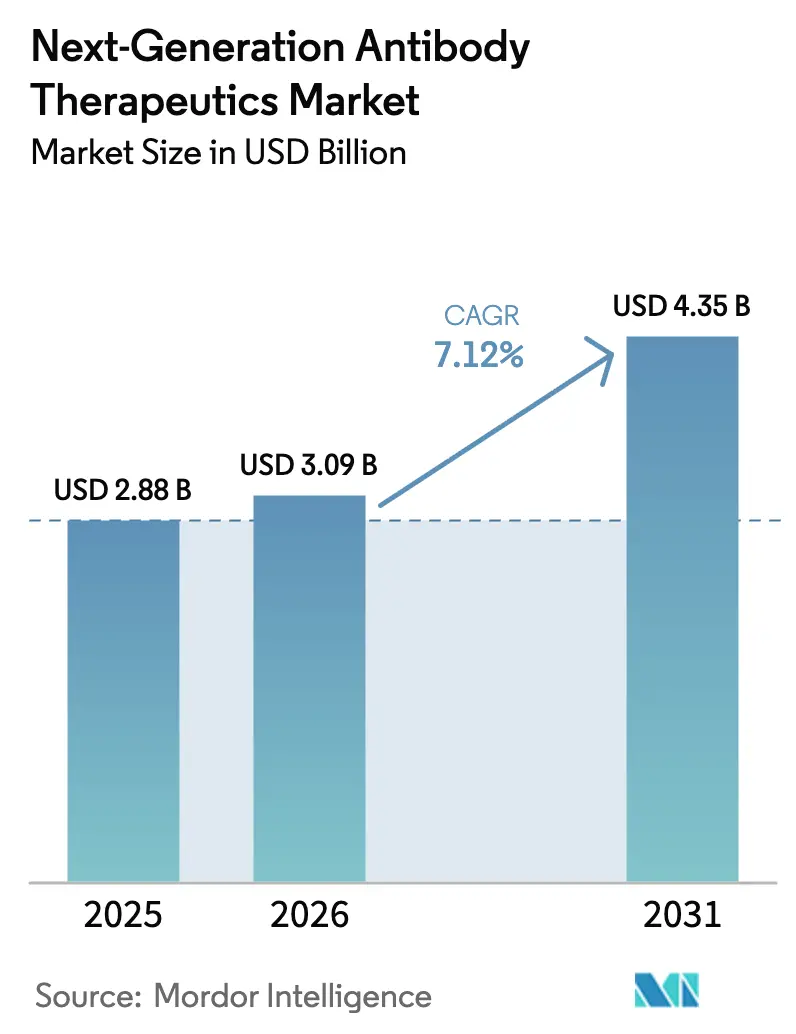

| Market Size (2026) | USD 3.09 Billion |

| Market Size (2031) | USD 4.35 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

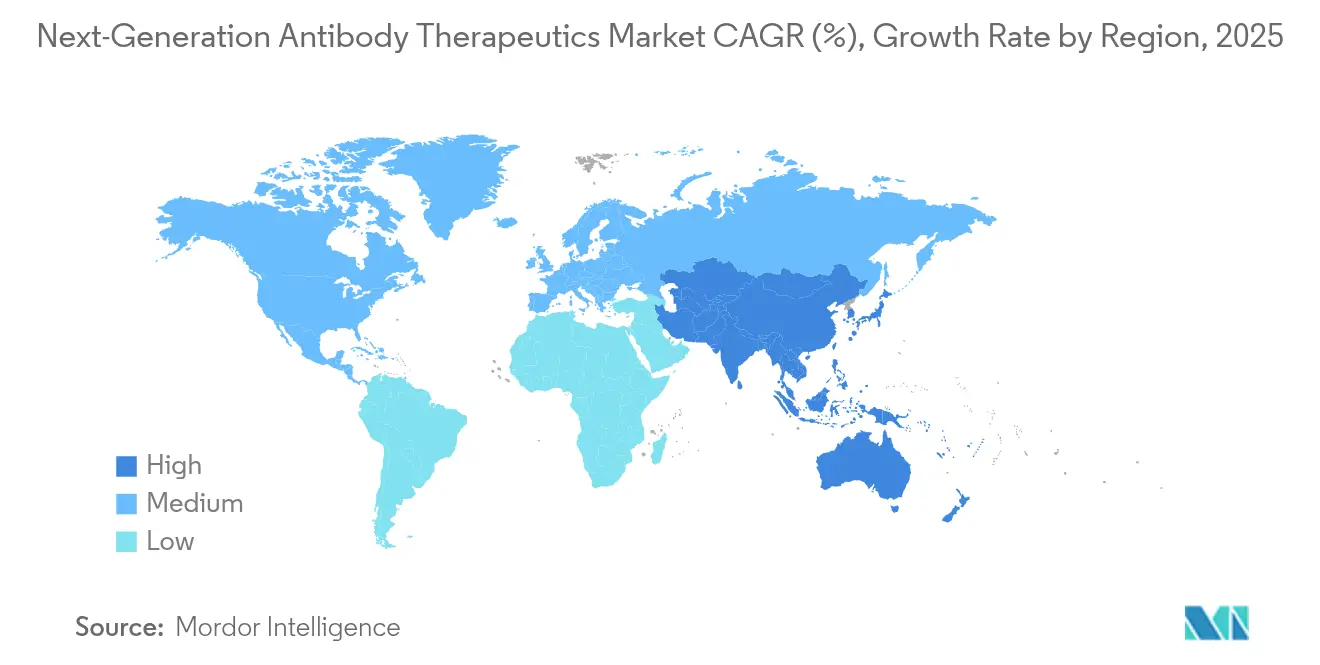

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Next-Generation Antibody Therapeutics Market Analysis by Mordor Intelligence

The next-generation antibody therapeutics market size in 2026 is estimated at USD 3.09 billion, growing from 2025 value of USD 2.88 billion with 2031 projections showing USD 4.35 billion, growing at 7.12% CAGR over 2026-2031. This solid mid‐single-digit trajectory signals the growing clinical and commercial influence of advanced antibody formats that deliver targeted cytotoxicity, dual-pathway immune modulation, and longer half-life dosing[1]U.S. Food & Drug Administration, “Modernizing the Development of Monoclonal Antibody Products,” fda.gov. Rapid clinical validation in solid tumors, steady gains in autoimmune applications, and increasingly supportive regulatory frameworks combine to accelerate adoption. Integration of artificial-intelligence-guided design shortens discovery cycles, while innovative formulation science propels a shift from intravenous to subcutaneous delivery in chronic regimens. These developments collectively reinforce the next-generation antibody therapeutics market as a high-value growth engine within biopharmaceuticals. North America maintains leadership on the strength of mature reimbursement systems and an extensive clinical-trial network, yet manufacturing expansions in Asia Pacific and supportive EU policies ensure sustained global competition through 2030.

Key Report Takeaways

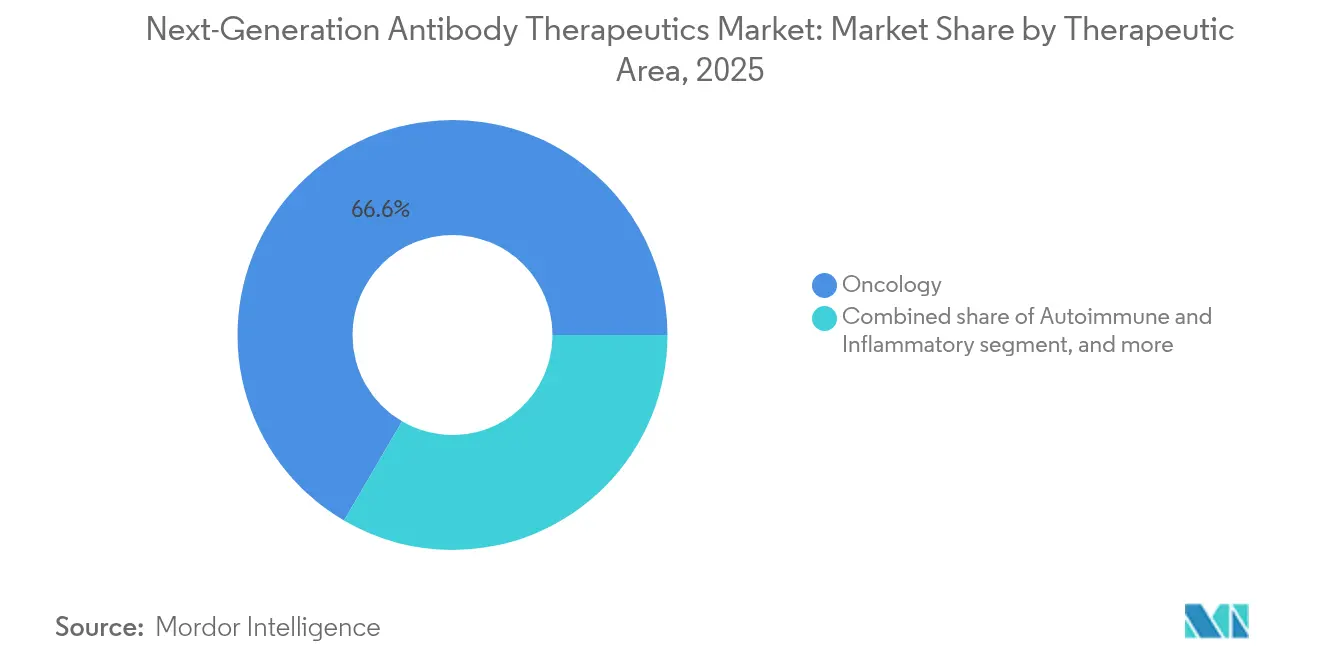

- By therapeutic area, oncology captured 66.58% of next-generation antibody therapeutics market share in 2025; non-oncology segments are forecast to grow at a 9.38% CAGR between 2026 and 2031.

- By technology, ADCs held 43.52% of the 2025 revenue pool, while bispecific and multispecific formats are advancing at an 10.92% CAGR over the forecast period.

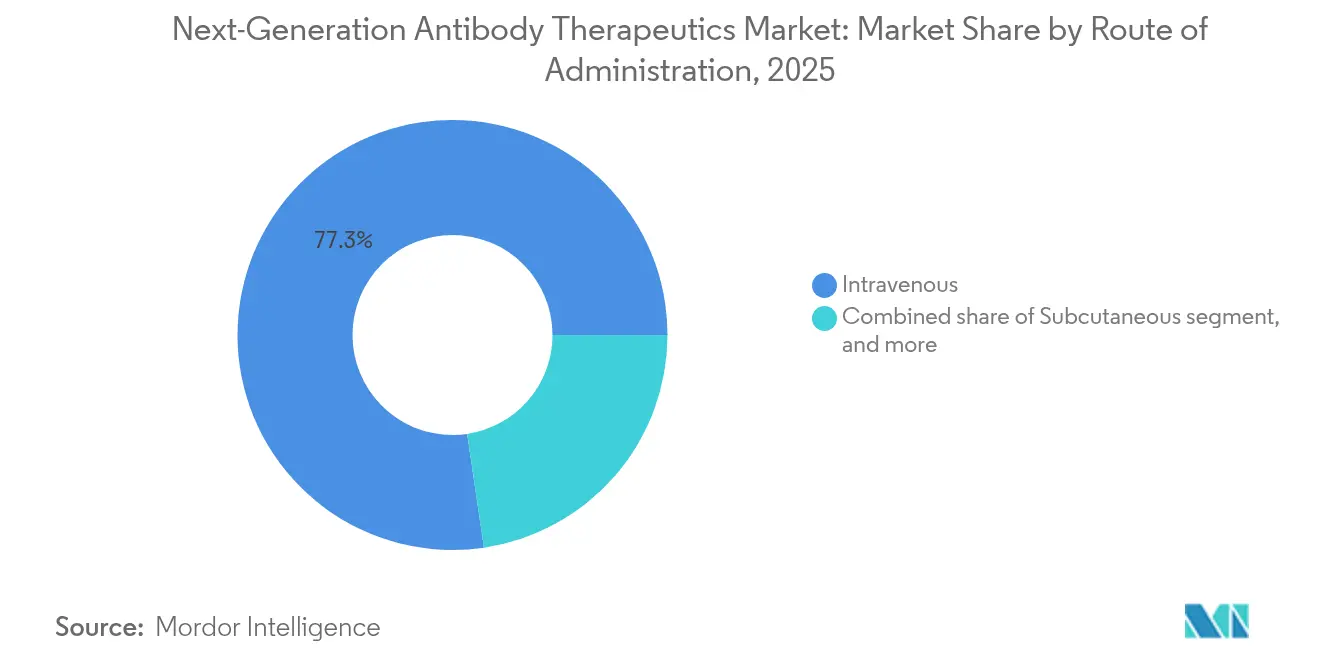

- By route of administration, subcutaneous formulations are expanding at 8.76% CAGR, challenging an intravenous base of 77.34% market share in 2025.

- By distribution channel, specialty clinics and cancer centers are growing at 8.84% CAGR but still trail hospital pharmacies’ 58.27% share in 2025.

- Regionally, Asia Pacific is the fastest mover at a 10.08% CAGR, underpinned by large-scale biomanufacturing investments such as AstraZeneca’s USD 1.5 billion ADC facility in Singapore.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Next-Generation Antibody Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global cancer incidence & unmet need in solid tumors | +1.8% | Global | Long term (≥ 4 years) |

| Growing prevalence of autoimmune disorders worldwide | +1.2% | Global | Long term (≥ 4 years) |

| Rapid advancements in antibody-engineering technologies (ADCs, bispecifics, Fc-engineering) | +0.9% | Global | Medium term (2–4 years) |

| Increasing venture-capital & big-pharma investments in next-gen antibody pipelines | +0.8% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Expansion of biomanufacturing capacity & specialized CDMO capabilities | +0.6% | North America, Asia-Pacific | Medium term (2–4 years) |

| Favorable regulatory designations (BTD, PRIME, RMAT) accelerating approvals | +0.5% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Cancer Incidence & Unmet Need in Solid Tumors

Escalating global cancer incidence intensifies the call for targeted therapeutics. More than 600 ADC candidates are in active trials for solid tumors, with breast and lung indications leading enrollment. Recent regulatory nods for HER2-low breast-cancer ADCs in 2024–2025 have energized development programs for gastric and ovarian malignancies, strengthening the clinical case for the next-generation antibody therapeutics market. Community oncology practices are adopting these agents earlier in treatment algorithms, driving a redistribution of infusion resources and accelerating patient access through 2030.

Growing Prevalence of Autoimmune Disorders Worldwide

Autoimmune diseases are emerging as the fastest-expanding opportunity segment. Bispecific constructs that can dampen multiple inflammatory pathways while sparing broad immunosuppression display high response durability in Phase 2 trials for rheumatoid arthritis and inflammatory bowel disease. Self-administrable subcutaneous formulations reduce clinic visits, supporting chronic disease management and broadening the commercial horizon for the next-generation antibody therapeutics market.

Rapid Advancements in Antibody-Engineering Technologies

Novel glycoengineering, site-specific conjugation, and Fc-domain alteration enable superior potency and safety profiles. Beyond classical cytotoxic payloads, developers are integrating radioisotopes and immunomodulators, widening indications and improving therapeutic windows. AI-guided epitope selection and in-silico developability screening accelerate lead optimization, reinforcing the technology edge.

Increasing Venture Capital & Big-Pharma Investments

More than USD 50 billion has flowed into platform acquisitions and co-development deals since 2024. Pfizer, Roche, and Eli Lilly each expanded their portfolios with multi-asset next-generation antibody programs, signalling sustained capital support for pipeline scale-up.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory & analytical requirements for novel antibody formats | −1.5% | North America, Europe | Short term (≤ 2 years) |

| High development & manufacturing costs for complex biologics | −1.2% | Global | Long term (≥ 4 years) |

| Safety and off-target toxicity concerns with potent antibody constructs | −0.8% | Global | Medium term (2–4 years) |

| Pricing pressures & biosimilar competition post-patent expiry | −0.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory & Analytical Requirements

Novel formats such as bispecifics and ADCs require extensive characterization of critical quality attributes. The FDA’s focus on interstitial lung disease risks in ADCs mandates additional pulmonary monitoring, delaying pivotal studies fda.gov. While the 2025 elimination of mandatory animal testing cuts some timelines, it simultaneously necessitates sophisticated in-vitro and computational assays, challenging resource-constrained developers.

High Development & Manufacturing Costs

ADC production can be 1.5-2× costlier than conventional monoclonals due to linker chemistry, high-potency payload handling, and complex analytical release. Scarcity of GMP payload manufacturing and constrained fill-finish capacity sustain elevated cost-of-goods, pushing launch prices toward the high end and inviting payer scrutiny.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Area: Oncology Dominance Faces Diversification

Oncology retained 66.58% of the next-generation antibody therapeutics market in 2025, reflecting the transformative effect of ADCs and bispecific T-cell engagers in refractory tumors. Recent approvals for HER2-low breast cancer and small-cell lung cancer entrench these modalities in first-line regimens. Novel targets such as Claudin-18.2 and c-Met broaden the patient base, sustaining oncology’s revenue lead.

Non-oncology indications are forecast to log a 9.38% CAGR, anchored by autoimmune and respiratory infectious-disease programs. Precision immune modulation via bispecific constructs offers prolonged remission without systemic toxicity, a compelling proposition for disorders requiring lifelong management.

By Technology: ADCs Lead While Bispecifics Accelerate

ADCs generated 43.52% of 2025 revenue. Homogeneous conjugation techniques and radio-payload innovation are extending applicability into hematology and solid-tumor niches. The next-generation antibody therapeutics market size tied to ADCs is set to expand as radioimmunoconjugates gain traction in difficult-to-resect tumors.

Bispecific and multispecific antibodies advance at an 10.92% CAGR, validated by approvals such as tarlatamab for small-cell lung cancer. Modular platforms ease construction of dual-specific binders, accelerating pipeline diversity. Fc-engineered IgGs enhance antibody-dependent cellular cytotoxicity, offering differentiated competitive positioning.

By Route of Administration: Intravenous Dominance Shifting to Subcutaneous

Intravenous treatment held 77.34% of 2025 administrations, but subcutaneous delivery grows rapidly at 8.76% CAGR. High-concentration formulations supported by hyaluronidase facilitate 5-10 mL injections, increasing at-home dosing. The next-generation antibody therapeutics market size attributable to subcutaneous formats will climb as wearable on-body injectors gain regulatory clearance.

Localized routes remain niche yet strategic in ocular, orthopedic, and intratumoral settings. These methods maximize local drug levels, limiting systemic exposure and enabling dose-sparing in toxicity-sensitive populations.

By Distribution Channel: Hospital Pharmacies Dominate Amid Specialty-Center Growth

Hospital pharmacies accounted for 58.27% of 2025 product flow, a reflection of infusion-centric usage and side-effect monitoring needs. However, specialty oncology centers and ambulatory clinics show 8.84% CAGR, propelled by subcutaneous options and payer incentives for site-of-care shifts. Cloud-integrated pharmacovigilance systems support safe outpatient dosing.

Retail and e-pharmacies supply maintenance doses for stable patients, hinting at future diversification of distribution pathways within the next-generation antibody therapeutics market.

Geography Analysis

North America commanded 47.56% of 2025 revenue, driven by high cancer prevalence, favorable reimbursement, and a rich concentration of biotech innovation. The U.S. leads on expedited pathways and advanced manufacturing tax credits that mitigate capital outlay for new plants. The 2025 regulatory shift away from animal testing is expected to shave months off pre-clinical timelines, sustaining the regional lead fda.gov.

Asia Pacific delivers the fastest growth at 10.08% CAGR. China’s high-profile biotech subsidies and Singapore’s best-in-class manufacturing incentives draw multinationals to establish regional supply hubs, anchoring the next-generation antibody therapeutics market there. Japan and South Korea leverage mature regulatory frameworks to speed conditional approvals for life-saving biologics. Expanded patient access programs and rising middle-class healthcare spending further boost uptake.

Europe maintains strong scientific infrastructure and reimbursement systems yet contends with rigorous price-value assessments. Recent EMA procedural reforms shorten clock-stop period for priority medicines, encouraging earlier filings. National health systems prioritize therapies with robust survival benefits, compelling developers to generate real-world evidence packages at launch. Germany, France, and the Nordics demonstrate the highest per-capita usage of next-generation antibody therapeutics.

Competitive Landscape

Industry concentration is moderate. Roche, AstraZeneca, and Pfizer sit atop revenue rankings, combining deep-pipeline breadth with in-house manufacturing. Roche’s Genentech campus integrates discovery through fill-finish, enabling rapid scale-up. AstraZeneca’s Singapore ADC plant delivers vertical integration and supply resilience[2]GeneOnline, “AstraZeneca to Invest USD 1.5 Billion in Singapore ADC Facility,” geneonline.com . Pfizer’s in-house radio-payload line underscores its technology diversification.

Strategic partnerships proliferate. Eli Lilly collaborates with BigHat Biosciences for AI-optimized antibodies, speeding affinity maturation cycles[3]Patsnap Synapse, “Eli Lilly and BigHat Biosciences Announce Collaboration,” synapse.patsnap.com. Roche teams with Oxford Biotherapeutics on next-wave conjugation chemistry, while Novartis’ purchase of Anthos Therapeutics secures abelacimab, a cardiovascular monoclonal antibody with blockbuster aspirations.

Specialized CDMOs such as Lonza and Samsung Biologics invest heavily in high-potency payload suites and aseptic fill-finish. Control of linker IP and payload supply positions these vendors as pivotal gatekeepers for small innovators seeking rapid clinical supply.

White-space opportunity remains in neurological and fibrotic indications, where blood-brain barrier crossing and deep-tissue penetration pose challenges. Advances in fragment-based delivery and receptor-mediated transcytosis could unlock these domains, creating fresh competitive fronts for the next-generation antibody therapeutics market.

Next-Generation Antibody Therapeutics Industry Leaders

AstraZeneca Plc.

Bristol-Myers Squibb Company

F. Hoffmann-La Roche Ltd.

Pfizer, Inc.

Seagen Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AstraZeneca received EU approval for DATROWAY, an ADC for breast cancer, broadening its oncology franchise.

- May 2025: GSK’s Blenrep (belantamab mafodotin) re-entered the UK market for relapsed/refractory multiple myeloma.

- April 2025: Eli Lilly partnered with BigHat Biosciences to use the Milliner AI platform for optimizing antibody attributes.

- April 2025: Synthetic Design Lab closed a USD 20 million seed round to progress its SYNTHBODY ADC platform.

- March 2025: Novartis acquired Anthos Therapeutics for up to USD 3.08 billion, adding the monoclonal antibody abelacimab to its cardiovascular portfolio.

Global Next-Generation Antibody Therapeutics Market Report Scope

As per the scope of the report, next-generation antibody therapies include a new improvised therapeutic antibody based on the modification of the conventional immunoglobulin (Ig) format to create novel drugs for the treatment of various diseases. Next-generation antibodies have been clinically developed to be more specific and often more potent than traditional monoclonal antibodies. The next-generation antibody therapeutics market is segmented by therapeutic area (oncology and autoimmunity or inflammation), technology (antibody-drug conjugates, bispecific antibodies, fc-engineered antibodies, and others), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Oncology |

| Autoimmune & Inflammatory |

| Other Therapeutic Areas |

| Antibody-Drug Conjugates (ADCs) |

| Bispecific & Multispecific Antibodies |

| Fc-Engineered & Glyco-Engineered IgGs |

| Antibody Fragments & Antibody-Like Proteins |

| Engineered Full-Length mAbs (IgG4, IgG1? Variants) |

| Biosimilar Next-Gen Antibody Products |

| Intravenous |

| Subcutaneous |

| Localized Administration (Intratumoral, Intravitreal) |

| Hospital Pharmacies |

| Specialty Clinics & Cancer Centers |

| Retail & Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapeutic Area | Oncology | |

| Autoimmune & Inflammatory | ||

| Other Therapeutic Areas | ||

| By Technology | Antibody-Drug Conjugates (ADCs) | |

| Bispecific & Multispecific Antibodies | ||

| Fc-Engineered & Glyco-Engineered IgGs | ||

| Antibody Fragments & Antibody-Like Proteins | ||

| Engineered Full-Length mAbs (IgG4, IgG1? Variants) | ||

| Biosimilar Next-Gen Antibody Products | ||

| By Route of Administration | Intravenous | |

| Subcutaneous | ||

| Localized Administration (Intratumoral, Intravitreal) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Clinics & Cancer Centers | ||

| Retail & Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast size of the next-generation antibody therapeutics market by 2031?

The next-generation antibody therapeutics market size is projected at USD 4.35 billion by 2031.

Which technology currently dominates the market?

Antibody-drug conjugates account for 43.52% of 2025 revenue and remain the leading technology segment.

Why are subcutaneous formulations gaining popularity?

Subcutaneous dosing supports at-home administration, reduces infusion-center burden, and is growing at a 8.76% CAGR.

Which region offers the highest growth potential?

Asia Pacific leads with a 10.08% CAGR, bolstered by large-scale biomanufacturing investments and expanding clinical-trial activity.

How do regulatory reforms affect development timelines?

The FDA’s 2025 removal of mandatory animal testing is expected to shorten U.S. pre-clinical phases, accelerating first-in-human entry.

What primary challenge constrains wider adoption?

Elevated manufacturing complexity and cost keep launch prices high, inviting payer scrutiny and potentially limiting access.

Page last updated on: