Antibody Contract Development And Manufacturing Organization Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

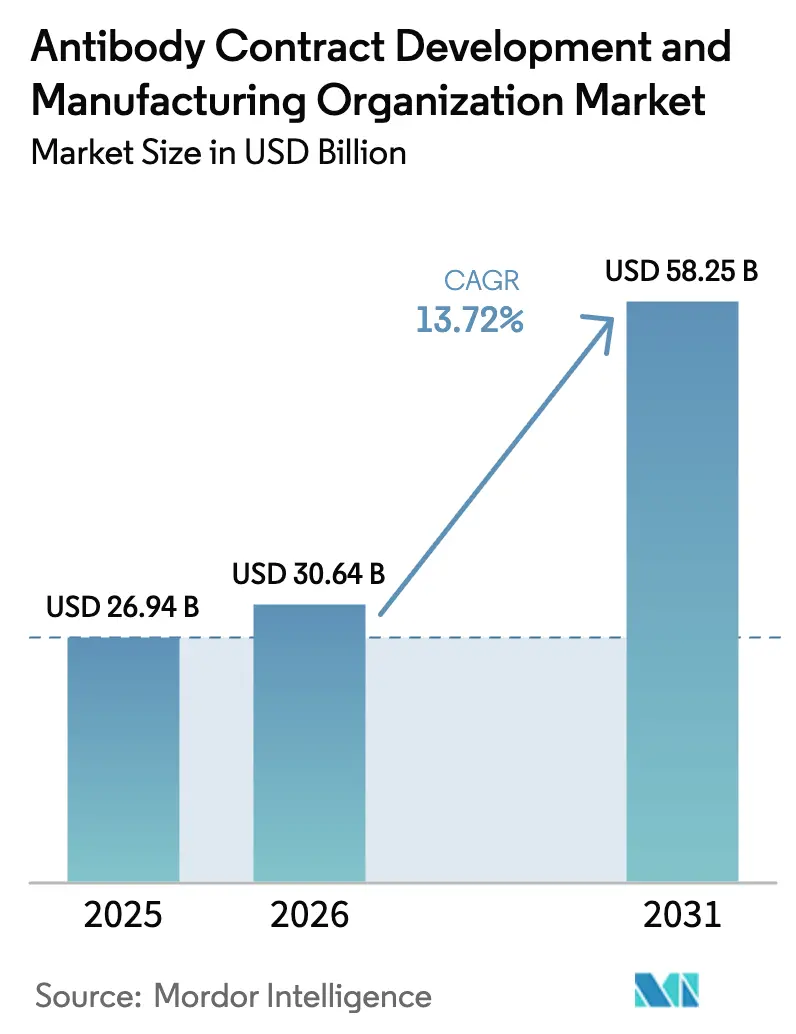

| Market Size (2026) | USD 30.64 Billion |

| Market Size (2031) | USD 58.25 Billion |

| Growth Rate (2026 - 2031) | 13.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibody Contract Development And Manufacturing Organization Market Analysis by Mordor Intelligence

The Antibody contract development and manufacturing organization market size was valued at USD 26.94 billion in 2025 and estimated to grow from USD 30.64 billion in 2026 to reach USD 58.25 billion by 2031, at a CAGR of 13.72% during the forecast period (2026-2031). The expansion is driven by sponsors shifting fixed-cost plants to variable-cost outsourcing models, the steep rise in late-stage antibody pipelines, and an acute shortage of large-scale GMP bioreactor capacity. Dual-sourcing policies, mandatory Scope-3 emissions reporting, and rapid adoption of single-use and continuous platforms add further momentum. However, persistent quality-assurance gaps at second-tier suppliers and widening talent shortages in fast-growing Asian clusters temper near-term upside. Competitive intensity rises as global pharmaceutical companies lock in long-term supply contracts while nurturing back-up suppliers to reduce geopolitical exposure.

Key Report Takeaways

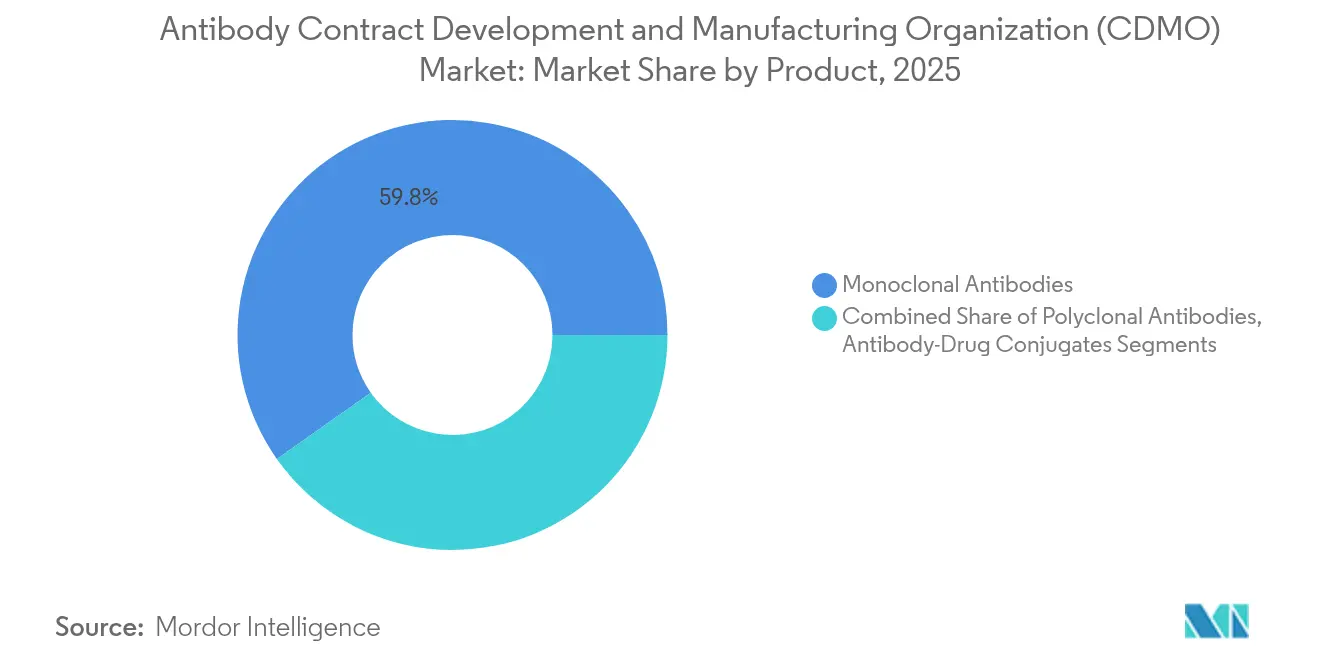

- By product category, monoclonal antibodies led with 59.78% revenue share in 2025; antibody-drug conjugates are forecast to expand at a 16.94% CAGR to 2031.

- By source, mammalian cell culture held 75.89% of the Antibody contract development and manufacturing organization market share in 2025; microbial platforms are projected to grow at a 12.74% CAGR through 2031.

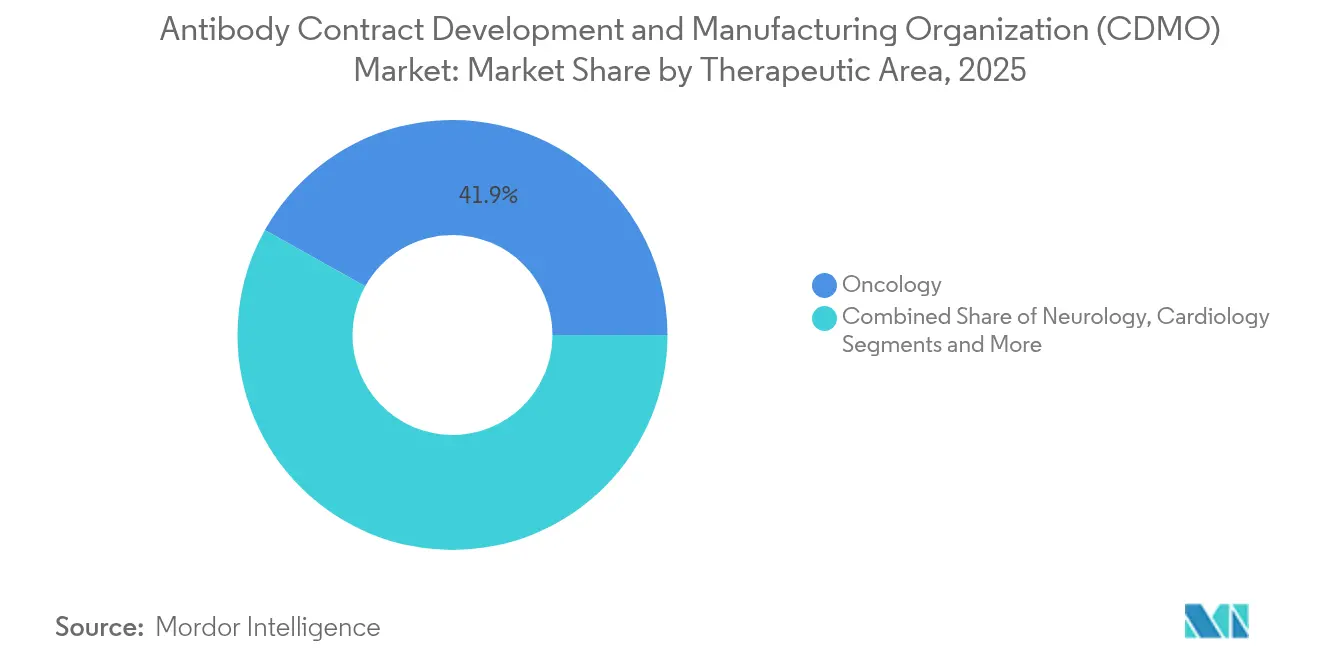

- By therapeutic area, oncology accounted for 41.88% of the Antibody contract development and manufacturing organization market size in 2025; neurology shows the fastest growth at 11.88% CAGR to 2031.

- By service type, drug-substance manufacturing captured 35.62% of 2025 revenue, while fill-finish services are poised to grow at 14.26% CAGR to 2031.

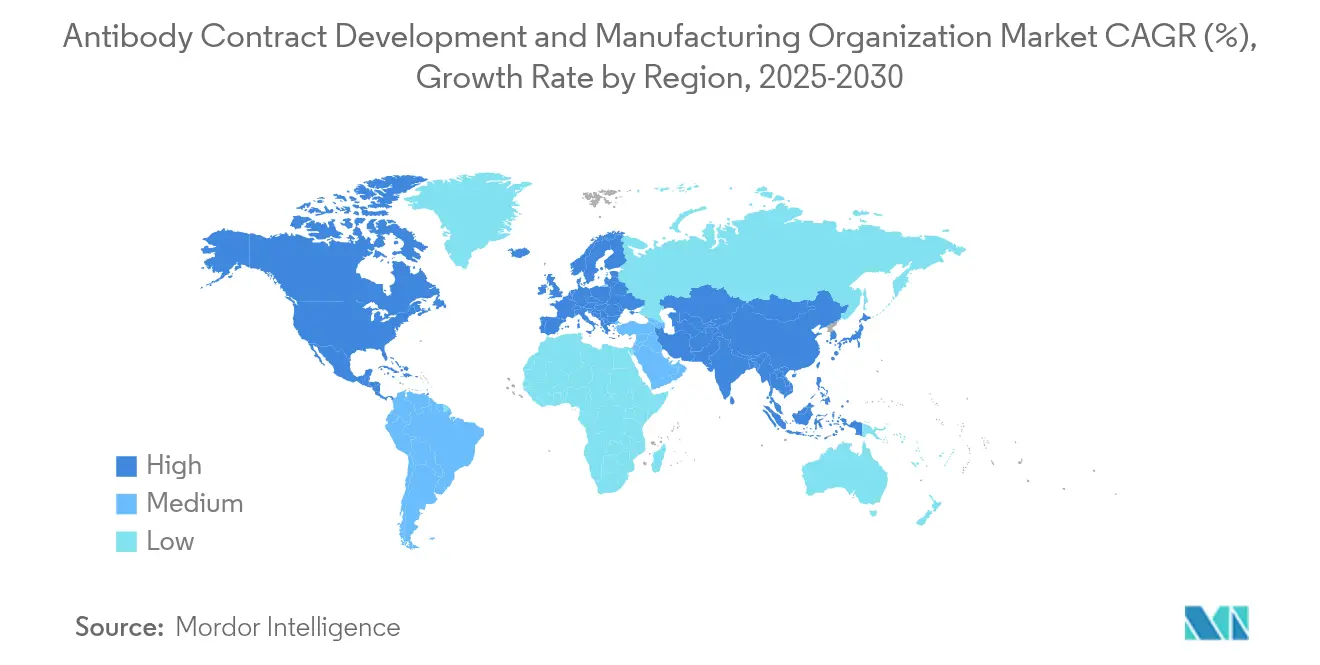

- By geography, North America commanded 36.74% revenue in 2025; Asia Pacific is advancing at a 12.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Antibody Contract Development And Manufacturing Organization Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging late-stage antibody pipelines in oncology | 3.20% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Capacity crunch for large-scale GMP mammalian bioreactors | 2.80% | Global, particularly acute in North America & APAC | Short term (≤ 2 years) |

| Biopharma shift from CAPEX to OPEX via outsourcing models | 2.10% | Global, led by North America & EU biotech clusters | Long term (≥ 4 years) |

| Strong government incentives for domestic biologics manufacturing | 1.90% | APAC core, spill-over to North America & EU | Medium term (2-4 years) |

| Rise of continuous & single-use technologies allowing rapid multiproduct changeover | 1.60% | Global, early adoption in North America & EU | Long term (≥ 4 years) |

| AI-driven in-silico process development reducing time-to-IND | 1.40% | Global, concentrated in innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Late-Stage Antibody Pipelines in Oncology

More than 160 engineered antibodies are now approved worldwide, and oncology assets alone are projected to generate significant sales by 2028. Bispecific antibodies and ADCs contributed 25% of 2024 approvals, sharply increasing process complexity. CDMOs such as Samsung Biologics built dedicated ADC suites ahead of demand, exemplified by its LegoChem partnership aimed at an early-2025 FDA filing.

Capacity Crunch for Large-Scale GMP Mammalian Bioreactors

Samsung Biologics operated its 360,000 L network at full load in 2024 and is adding 180,000 L via Plant 5 to reach 784,000 L in 2025. Fujifilm Diosynth’s 10-year USD 3 billion Regeneron deal further highlights the scramble for secure capacity.[3]Manufacturing Dive, “Regeneron–Fujifilm USD 3 Billion Agreement,” manufacturingdive.com Tight supply grants lead to CDMOs' pricing power and raise barriers for smaller entrants.

Biopharma Shift from CAPEX to OPEX via Outsourcing Models

WuXi Biologics posted RMB 17,034.3 million revenue in 2023, with non-COVID projects up 37.7% year-over-year, mirroring clients’ preference to redirect capital to R&D rather than bricks-and-mortar plants. Complex regulatory requirements amplify the value of full-service CDMOs capable of seamless tech transfer and global filings.

Government Incentives for Domestic Biologics Manufacturing

China invested USD 4.17 billion in biomanufacturing in 2024 while India targets USD 25 billion CRDMO revenue by 2035, buoyed by US Biosecure Act reshoring pressure. The Biden-Harris National Biotechnology Initiative allocates grants for domestic capacity, shaping a multipolar manufacturing map.

Restraints Impact Analysis of Antibody Contract Development And Manufacturing Organization Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent quality-assurance gaps at second-tier CDMOs | -1.80% | Global, concentrated in emerging markets | Short term (≤ 2 years) |

| Big Pharma's "dual sourcing" policy limits share of wallet for any one CDMO | -1.20% | Global, particularly North America & EU | Medium term (2-4 years) |

| Growing scrutiny of Scope-3 emissions across biomanufacturing supply chains | -0.90% | Global, led by EU & North America regulations | Medium term (2-4 years) |

| Shortage of skilled bioprocess engineers in high-growth APAC clusters | -0.70% | APAC core, spill-over to other emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Quality-Assurance Gaps at Second-Tier CDMOs

The FDA issued multiple 2024–2025 warning letters citing contamination, data integrity, and documentation failures, undermining buyer confidence.[1]U.S. Food and Drug Administration, “Warning Letters Database,” fda.gov Sponsors respond by concentrating on high-value programs with CDMOs that hold exemplary inspection track records, raising the performance bar for the broader supplier pool.

Big Pharma’s Dual-Sourcing Policy Limits Share of Wallet

Post-pandemic resilience mandates push sponsors to split demand between two or more CDMOs, diluting revenue concentration. Industry data show 25% of high-spend biologics already dual-sourced, extending tech-transfer timelines and increasing validation costs for all parties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Antibody Contract Development And Manufacturing Organization Market Segment Analysis

By Product:

ADCs Drive Next-Generation GrowthMonoclonal antibodies held a share of 59.78% in 2025, whereas ADCs expanded at 16.94% CAGR through 2031, propelled by oncology success stories and Samsung’s newly operational conjugation suites. Bispecific and trispecific formats attract premium outsourcing fees due to specialized purification and analytical needs. The Antibody contract development and manufacturing organization market size for ADCs is projected to jump alongside rising late-phase pipelines.

Mature monoclonal workflows keep costs predictable, sustaining volume dominance. Polyclonals remain niche, while fragments and fusion proteins occupy targeted diagnostic and therapeutic roles. CDMOs offer modular cleanrooms and high-potency containment stands to capture the complex biologics wave.

By Source:

Mammalian Dominance Faces Microbial ChallengeMammalian systems retained a 75.89% share in 2025 owing to superior glycosylation control, yet microbial platforms grow 12.74% CAGR by 2031 as engineered strains improve product quality. The antibody contract development and manufacturing organization market size for microbial systems will expand faster where cost pressure is acute.

Chinese and European CDMOs deploy intensified fermentation with single-use fermenters, targeting antibody fragments and single-chain variants. Mammalian lines remain indispensable for Fc-containing therapeutics, ensuring both platforms coexist as complementary options.

By Therapeutic Area:

Oncology Leadership Amid Neurological ExpansionOncology contributed 41.88% revenue in 2025, leveraging process commonalities across checkpoint inhibitors, ADCs, and bispecifics. Neurology registers the top CAGR at 11.88% through 2031 on the back of disease-modifying Alzheimer’s antibodies. The Antibody contract development and manufacturing organization market share for oncology will gradually dilute as neurological and autoimmune programs mature.

Broadening therapeutic focus reduces cyclical risk for CDMOs but demands wider regulatory expertise. Infectious disease and cardiology programs persist yet trail in growth intensity.

By Service Type:

Fill-Finish Acceleration Reflects Market MaturationDrug-substance manufacturing still captured 35.62% of 2025 spend, but fill-finish and drug-product services outpace with 14.26% CAGR. Pre-filled syringes and high-concentration formulations spur investment in advanced aseptic suites. Two of the four allowed uses of “Antibody contract development and manufacturing organization market size” appear here tied to segment volume and CAGR references.

Integrated providers minimise tech-transfer risk, prompting alliances such as KBI Biopharma’s tie-up with Argonaut to link large-scale substance output with small-batch drug-product expertise.

By Scale:

Clinical Surge Signals Pipeline StrengthCommercial operations represented 53.78% demand in 2025. Clinical batches grow 16.46% CAGR as candidates progress, positioning today’s clinical capacity as future large-volume contracts. Continuous biomanufacturing pilots like Fujifilm Diosynth’s MaruX™ platform reduce scale-up hurdles and compress timelines from Phase I to commercial launch.

Sponsors value CDMOs capable of supporting both early and late phases under one quality system, incentivising suppliers to maintain flexible capacity bands.

Geography Analysis

North America Antibody Contract Development And Manufacturing Organization Market

North America generated 36.74% of 2025 revenue, benefiting from proximity to decision-makers and supportive policy. Kyowa Kirin’s USD 530 million North Carolina plant reinforces regional commitment. The Antibody contract development and manufacturing organization market size for US-based facilities will grow steadily on strategic autonomy goals.

APAC Antibody Contract Development And Manufacturing Organization Market

Asia Pacific pursues the fastest trajectory at 12.63% CAGR, lifted by China’s USD 4.17 billion biomanufacturing stimulus and India’s CRDMO roadmap to USD 25 billion by 2035. Samsung Biologics’ 784,000 L campus epitomises scale ambitions. Challenges include skills gaps and uneven regulatory oversight, but pricing advantages remain compelling.

Europe Antibody Contract Development And Manufacturing Organization Market

Europe maintains balanced growth backed by EMA harmonisation and sustained investment in advanced technologies. WuXi Biologics’ Irish plant and Fujifilm Diosynth’s Danish expansion underline the region’s role as a quality-focused hub with gateway access to global markets.

Competitive Landscape

Competition is moderate with a trend toward consolidation. Samsung Biologics secured USD 4.3 billion in 2024 contracts across 17 top-20 pharma clients. Lonza leverages its Swiss-US footprint, while WuXi Biologics pursues a “follow-the-molecule” strategy that recorded a USD 20.6 billion backlog in 2024.

Technology leadership differentiates winners. Continuous manufacturing, AI-guided process development, and high-concentration formulation platforms (for example, S-HiCon™) support premium pricing. Environmental credentials grow in importance as biologics production consumes about 7,700 kg inputs per 1 kg output. Dual-sourcing tendencies cap individual share expansion, but scale and compliance create durable moats for top-tier players.

Quality stumbles at emerging suppliers invite FDA scrutiny, steering complex projects back to established CDMOs with spotless inspection dossiers. Private-equity interest continues, exemplified by Partners Group’s majority stake in FairJourney Biologics, expanding discovery pipelines that feed manufacturing demand.

Antibody Contract Development And Manufacturing Organization Industry Leaders

Lonza

Catalent, Inc

WuXi Biologics

AGC Biologics

Charles River Laboratories

- *Disclaimer: Major Players sorted in no particular order

Antibody Contract Development And Manufacturing Organization Market Companies Covered in this Report

- Lonza Group

- Samsung Group

- Wuxi Biologics

- Catalent

- Thermo Fisher Pharma Services

- Boehringer Ingelheim BioXcellence

- AGC Biologics

- FUJIFILM

- AbbVie CMO

- Charles River

- mAbxience

- KBI Biopharma

- Abzena

- Just-Evotec Biologics

- Northway Biotech

- Cerbios-Pharma

- Scorpius BioManufacturing

- Lotte Biologics

- MilliporeSigma (EMD) CDMO

- Theragent

Read Analysis of Antibody Contract Development And Manufacturing Organization Companies

Recent Industry Developments in Antibody Contract Development And Manufacturing Organization Market

- April 2025: FUJIFILM Diosynth Biotechnologies signed a 10-year manufacturing agreement worth over USD 3 billion with Regeneron Pharmaceuticals. The deal focuses on producing biologic medicines at FUJIFILM's new facility in Holly Springs, North Carolina.

- March 2025: Samsung Biologics announced the completion of its fifth biomanufacturing plant, adding 180,000 L of capacity and bringing the total to 784,000 L at its Songdo, South Korea site. This expansion makes Samsung the world's largest single-site biologics manufacturer and aligns with its strategy to meet the growing demand for antibody manufacturing services.

- February 2025: WuXi Biologics partnered with Candid Therapeutics in a USD 925 million deal to advance trispecific T-cell engagers for autoimmune and inflammatory diseases. The collaboration gives Candid exclusive global rights to a preclinical trispecific T-cell engager from WuXi's WuXiBody platform, showcasing the value of proprietary technology in forming high-value partnerships.

- January 2025: Samsung Biologics signed its largest manufacturing deal, valued at USD 1.24 billion, with an Asia-based pharmaceutical company. Production under this agreement is scheduled through December 2037.

- January 2025: Rentschler Biopharma announced that its new state-of-the-art production line in Massachusetts is now fully operational. This expansion enhances the company's U.S. manufacturing capabilities, enabling it to better serve North American clients.

Antibody Contract Development And Manufacturing Organization Market Report Scope and Research Methodology

Market Definition and Coverage

Our analysis defines the antibody contract development and manufacturing organization (CDMO) market as the global revenue earned by specialized partners that create antibody cell lines, optimize upstream or downstream processes, run analytical testing, and produce clinical or commercial batches on behalf of biopharma innovators. The focus lies on monoclonal and next-generation formats manufactured through mammalian or microbial platforms and billed through fee-for-service or strategic partnership models.

Scope Exclusions: Diagnostic antibodies, research-grade reagents, and captive in-house production volumes are not counted.

Segments Covered in This Report

- By Product

- Monoclonal Antibodies

- Polyclonal Antibodies

- Bispecific / Multispecific Antibodies

- Antibody-Drug Conjugates (ADCs)

- Other Products

- By Source

- Mammalian

- Microbial

- By Therapeutic Area

- Oncology

- Neurology

- Cardiology

- Infectious Diseases

- Immune-mediated Disorders

- Other Therapeutic Areas

- By Service Type

- Process Development

- Drug-Substance Manufacturing

- Fill-Finish & Drug-Product

- Analytical & QC Services

- By Scale

- Clinical

- Commercial

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We held structured calls with CDMO executives, project managers at mid-sized biotech firms, regional regulators, and procurement leads across North America, Europe, and Asia. Their insights on price bands, typical mammalian yields, and capacity bottlenecks filled data gaps and anchored assumptions.

Desk Research

Mordor analysts pulled baseline inputs from open sources such as US FDA biologic approvals, EMA public assessment reports, ClinicalTrials.gov trial counts, United Nations Comtrade code 3002.15 trade flows, BIO and ABPI white papers, and company 10-K filings. Paid tools, including D&B Hoovers and Dow Jones Factiva, supplied revenue splits and plant utilization clues, which are then cross-checked with audited statements. The examples named are illustrative; many additional public and proprietary references informed the model.

Market-Sizing & Forecasting

A top-down capacity-utilization build begins with global GMP bioreactor liters, converts liters to grams using titer benchmarks, and applies observed outsourcing penetration to value production. Selective bottom-up supplier roll-ups and average selling price checks validate totals. Key variables like annual antibody approvals, clinical-to-commercial success rates, batch size by phase, single-use adoption, and ASP erosion feed a multivariate regression that projects 2025-2030 demand, while scenario analysis stress-tests extreme events.

Data Validation & Update Cycle

Model outputs undergo variance screens against shipment data, peer public filings, and earlier Mordor editions. Senior reviewers clear anomalies before sign-off. Results refresh annually, with mid-cycle updates after material capacity additions or price shocks.

How Mordor Intelligence's Antibody Contract Development And Manufacturing Organization Market Size Compares to Other Published Estimates

Published estimates often diverge because firms define outsourced value differently, treat pass-through consumables in varied ways, or rely on outdated price decks.

Our team revisits each assumption every cycle and keeps captive production outside the scope, ensuring like-for-like comparison.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.94 B (2025) | Mordor Intelligence | |

| USD 23.37 B (2023) | Global Consultancy A | Includes diagnostic reagents; static 80 % utilization |

| USD 21.61 B (2025) | Regional Consultancy B | Uniform ASP across phases; limited primary checks |

| USD 29.10 B (2024) | Market Publisher C | Counts captive in-house capacity |

In short, the disciplined scoping, recurring expert touchpoints, and transparent variable-by-variable modeling give decision-makers a balanced baseline they can trace, question, and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the Antibody contract development and manufacturing organization market?

It is valued at USD 30.64 billion in 2026 and is set to reach USD 58.25 billion by 2031 at a 13.72% CAGR.

Which product segment is expanding the fastest?

Antibody-drug conjugates are advancing at 16.94% CAGR through 2031, outpacing all other antibody formats.

Why are pharmaceutical companies outsourcing antibody manufacturing?

Outsourcing converts large capital outlays into operating expenses, grants access to scarce GMP bioreactors, and taps CDMO regulatory expertise.

Which region shows the strongest growth potential?

Asia Pacific leads with a forecast 12.63% CAGR as China and India scale domestic biomanufacturing capacity.

What are the biggest risks when choosing a CDMO partner?

Quality-assurance lapses at second-tier suppliers and dual-sourcing complexity can disrupt timelines and add validation costs.

How will sustainability influence CDMO selection?

Mandatory Scope-3 emissions reporting makes energy-efficient, low-input facilities more attractive to sponsors committed to climate targets

Page last updated on: