Polyclonal Antibodies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

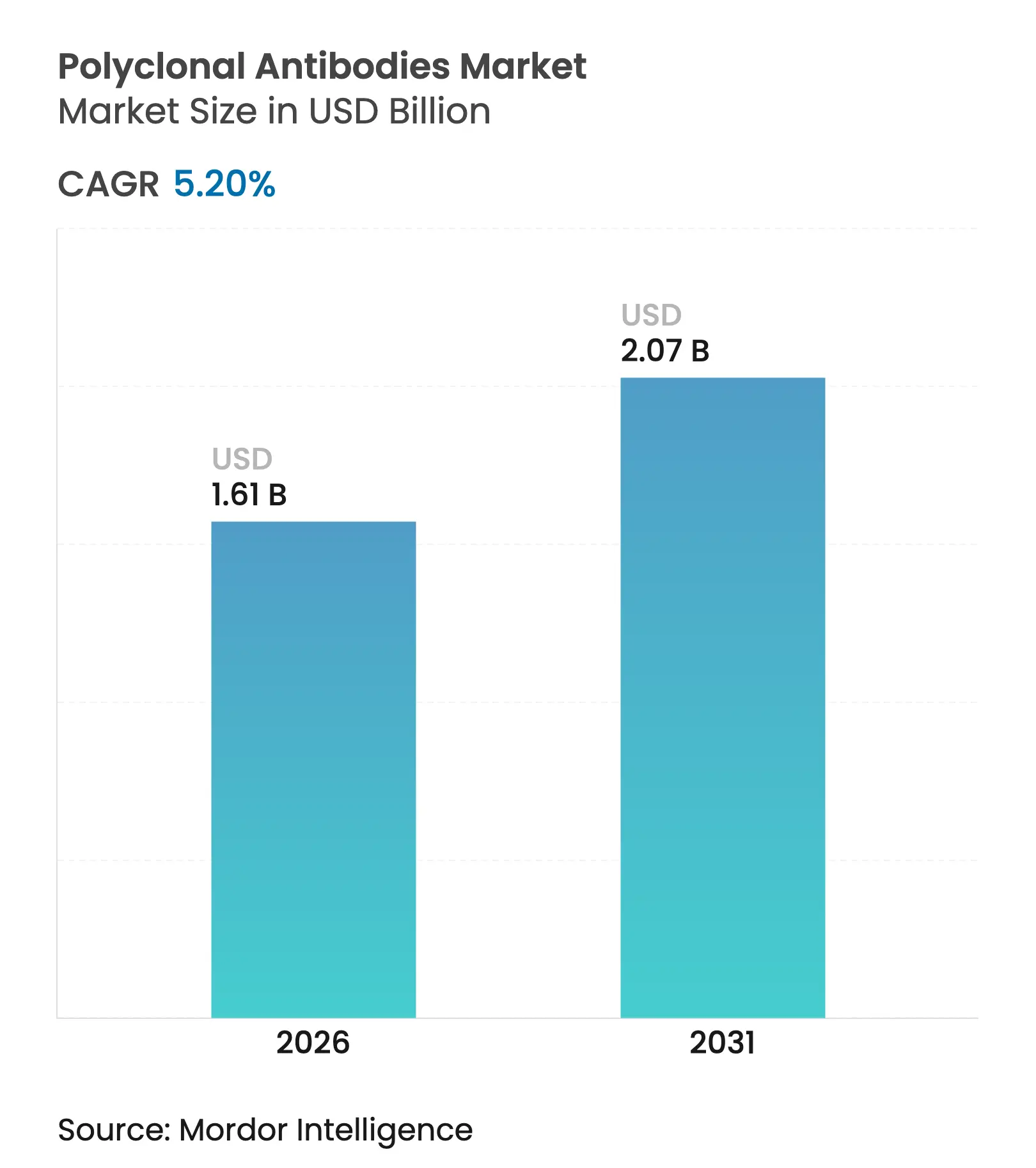

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 5.20 % CAGR |

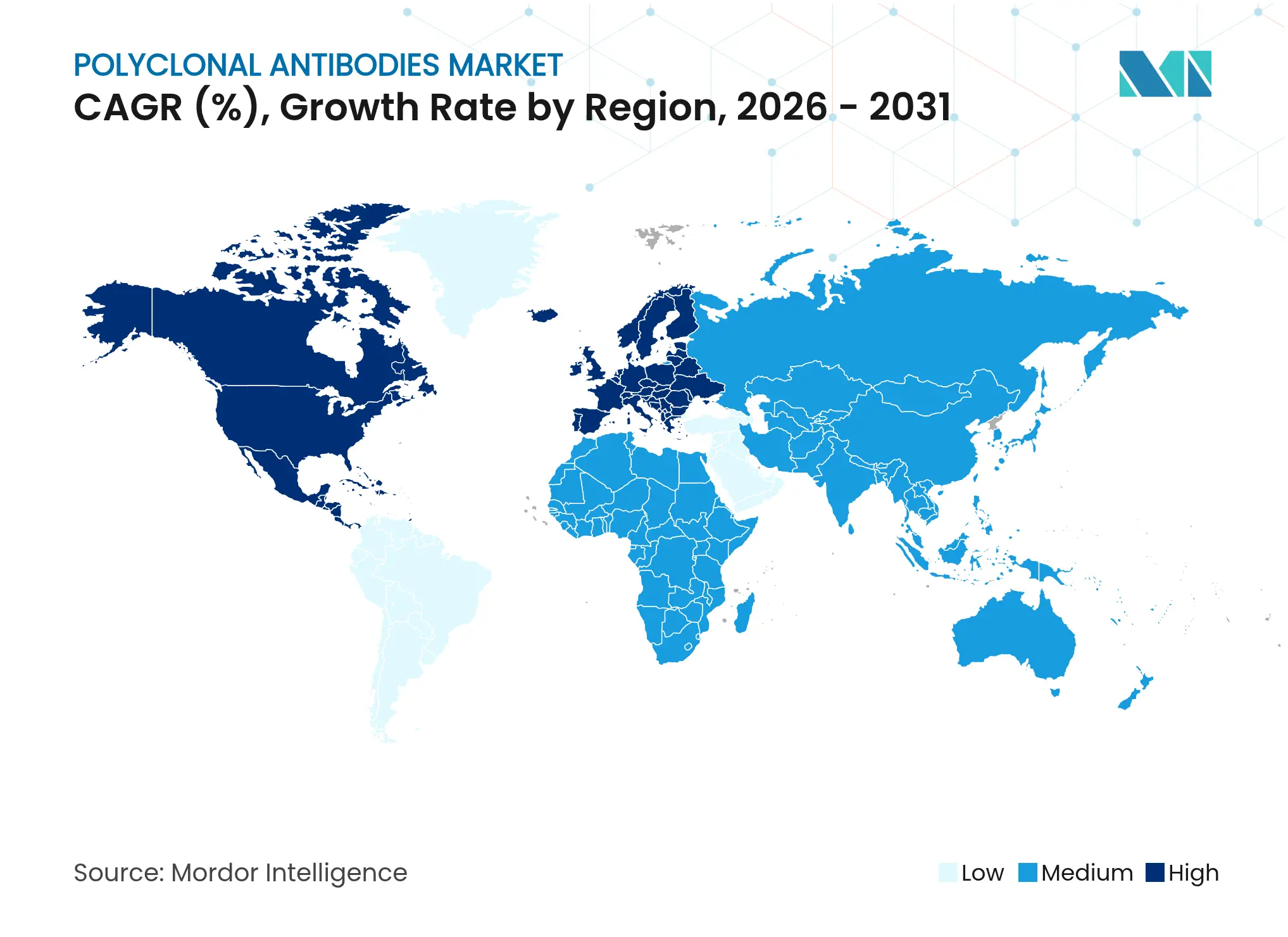

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Polyclonal Antibodies Market Analysis by Mordor Intelligence

The polyclonal antibodies market size is expected to grow from USD 1.53 billion in 2025 to USD 1.61 billion in 2026 and is forecast to reach USD 2.07 billion by 2031 at 5.2% CAGR over 2026-2031. Growth continues despite competitive pressure from monoclonal and recombinant formats because laboratories rely on the broad epitope recognition of polyclonal antibodies for sensitive immunodiagnostic assays. Hospital demand strengthens as point-of-care testing expands, while biopharmaceutical producers use polyclonals for in-process quality control. Artificial-intelligence tools that predict immunogenic epitopes shorten development timelines and lower production risk, making custom polyclonal projects more attractive to research institutions. Geographic expansion remains uneven: North America holds the largest spending base, but Asia-Pacific delivers the fastest incremental revenue as local regulators encourage domestic antibody manufacturing capacity.

Key Report Takeaways

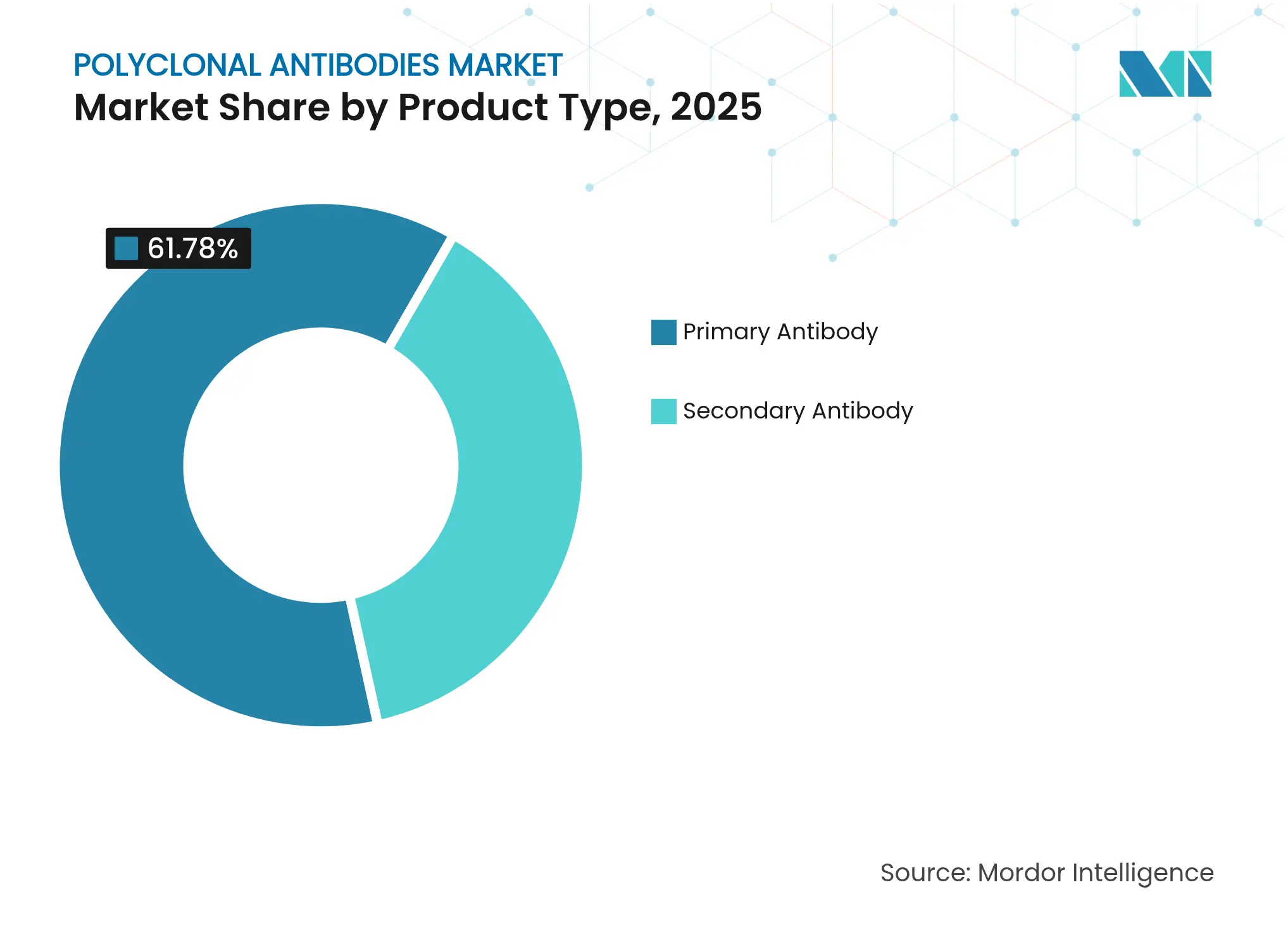

- By product type, primary antibodies led with a 61.78% revenue share in 2025; secondary antibodies are projected to grow at a 6.02% CAGR through 2031.

- By source, rabbit antibodies captured 42.85% of the polyclonal antibodies market share in 2025, while goat antibodies are expected to expand at a 5.95% CAGR to 2031.

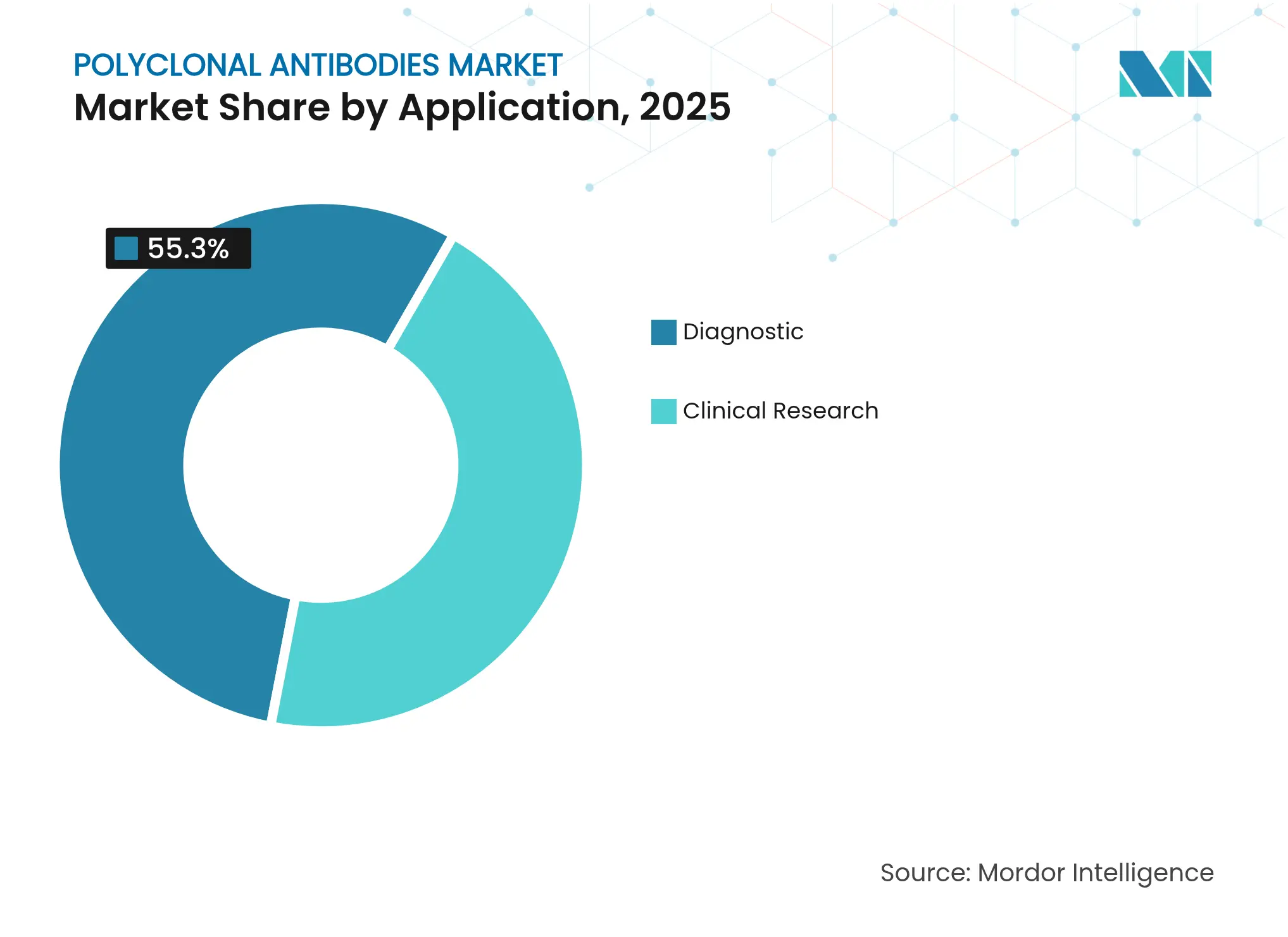

- By application, diagnostic testing accounted for 55.30% of the polyclonal antibodies market size in 2025; clinical research is forecast to advance at a 6.55% CAGR between 2026-2031.

- By end user, biopharmaceutical industries held 38.05% share of the polyclonal antibodies market in 2025, whereas hospitals represent the fastest-growing segment at a 6.18% CAGR.

- By geography, North America contributed 43.95% of 2025 revenue; Asia-Pacific is set to post a 6.88% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyclonal Antibodies Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of infectious & chronic diseases

Rising prevalence of infectious & chronic diseases

| +1.2% | Global, highest effect in APAC & MEA | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, highest effect in APAC & MEA

|

Impact Timeline

:

Medium term (2-4 years)

|

Broader use in diagnostics & biopharma production

Broader use in diagnostics & biopharma production

| +0.9% | North America & Europe, expanding in APAC | Short term (≤ 2 years) | |||

Expansion of proteomics & genomics workflows

Expansion of proteomics & genomics workflows

| +0.8% | United States, Germany, China | Long term (≥ 4 years) | |||

Increased immunotherapy R&D budgets

Increased immunotherapy R&D budgets

| +0.7% | North America & Europe, emerging Asia-Pacific | Medium term (2-4 years) | |||

Sustainable IgY production platforms

Sustainable IgY production platforms

| +0.5% | Europe & Japan | Long term (≥ 4 years) | |||

AI-enabled epitope prediction

AI-enabled epitope prediction

| +0.4% | United States, EU, China, Israel | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising prevalence of infectious & chronic diseases

A growing caseload of viral outbreaks and complex non-communicable disorders maintains steady demand for polyclonal reagents in diagnostics and therapy. During the COVID-19 pandemic, glyco-humanized polyclonal antibody XAV-19 accelerated patient recovery while neutralizing multiple variants, demonstrating the value of broad epitope coverage for agile pathogen response [1]B. Lorin et al., “Efficacy of Glyco-Humanized Polyclonal Antibody XAV-19 Against SARS-CoV-2 Variants,” Frontiers in Immunology, frontiersin.org. The same rationale extends to oncology, where heterogeneous tumor antigens challenge single-epitope therapeutics.

Broader use in diagnostics & biopharma production

Immunohistochemistry, flow cytometry and titer-monitoring workflows increasingly specify polyclonal antibodies because their multi-epitope binding raises assay sensitivity and reduces false-negatives, critical for regulatory batch release testing. Protein-A chromatography innovations now detect antibody titers seven times more sensitively than earlier columns, enhancing in-process control for vaccine and therapeutic protein facilities.

Expansion of proteomics & genomics workflows

Completion of 93% of the predicted human proteome catalyzes demand for reagents that can detect isoforms and post-translationally modified proteins. Polyclonal antibodies’ ability to bind multiple epitopes on the same protein enables comprehensive characterization, especially when integrated with mass-spectrometry-coupled immunoenrichment protocols [2]C. Deutsch et al., “Progress Toward a Complete Human Proteome,” MDPI Proteomes, mdpi.com.

Increased immunotherapy R&D budgets

Global spending on antibody-based drugs continues to climb toward USD 479 billion by 2028, and part of that budget now funds recombinant polyclonal approaches tailored for multi-target engagement. Preclinical studies of hepatitis B candidates showed higher binding potency than plasma-derived comparators, validating polyclonal strategies in highly variable viral landscapes.

Sustainable IgY production platforms

European research groups demonstrate that IgY antibodies harvested from egg yolk reduce animal use while offering comparable affinity. Clinical trials reported successful eradication of refractory H. pylori infections without adverse reactions, supporting regulatory momentum toward welfare-compliant production.

AI-enabled epitope prediction

Machine-learning models trained on structural immunology datasets shorten design cycles for custom polyclonal projects and improve hit rates by scoring epitope immunogenicity in silico prior to animal immunization. Early adopters report double-digit reductions in development time and material cost, a key advantage for labs operating under compressed grant timelines.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited availability of high-quality batches

Limited availability of high-quality batches

| -0.8% | Global, hitting emerging markets hardest | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

Global, hitting emerging markets hardest

|

Impact Timeline

:

Short term (≤ 2 years)

|

Intensifying competition from monoclonal & recombinant

formats

Intensifying competition from monoclonal & recombinant

formats

| -1.1% | United States, EU, Japan | Medium term (2-4 years) | |||

Batch-to-batch variability raising reproducibility risk

Batch-to-batch variability raising reproducibility risk

| -0.6% | Global labs & manufacturing sites | Short term (≤ 2 years) | |||

Stricter animal-welfare regulations raising cost

Stricter animal-welfare regulations raising cost

| -0.4% | EU & North America, spreading worldwide | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited availability of high-quality batches

Independent benchmarking shows that a sizable fraction of commercial antibodies lacks required specificity, leading to costly repeat experiments. Industry leaders continue to retire underperforming catalog items, yet smaller suppliers still struggle to meet consensus validation guidelines.

Intensifying competition from monoclonal & recombinant formats

More than 100 monoclonal therapeutics have secured FDA approval, creating established regulatory pathways and heightening buyer expectations for consistency. Recombinant platforms now deliver monoclonal-like uniformity with polyclonal-level diversity, drawing development budgets away from traditional serum-derived products.

Segment Analysis

By Product Type: Secondary antibody innovation broadens utility

Primary antibodies accounted for 61.78% of 2025 revenue, underlining their foundational role in antigen detection across life-science workflows. Secondary antibodies, though smaller today, are on track for a 6.02% CAGR as multiplexed imaging and high-throughput ELISA platforms proliferate. Conjugation advances enable dual reporter tagging, permitting fluorescence and enzymatic readouts from a single assay cycle. Enhanced specificity filters—such as species-adsorbed preparations—limit background noise, protecting experimental reproducibility. These developments support consistent revenue expansion and reinforce the broader polyclonal antibodies market growth narrative.

Secondary antibody vendors now bundle exhaustive validation datasets with each lot, a practice once limited to premium monoclonal providers. Automated purification lines and in-line endotoxin removal cut turnaround times and widen appeal among diagnostics manufacturers scaling for mass-market test kits. Over the forecast horizon, secondary reagents will likely outpace primaries in incremental dollar contribution, even while primaries retain volume leadership.

Note: Segment shares of all individual segments available upon report purchase

By Source: Goat and IgY platforms gain momentum

Rabbit serum remains the leading animal source, capturing 42.85% of shipments in 2025 thanks to high-affinity immune responses and mature purification protocols. Goat antibodies, however, will record a sector-leading 5.95% CAGR as researchers seek cross-species reactivity and lower immunogenicity profiles for preclinical use. Chick-origin IgY products move from niche to mainstream as European guidelines favor non-invasive collection methods. Egg-yolk harvesting yields kilogram-scale batches without terminal bleeds, aligning with tightening welfare legislation and driving incremental demand. Suppliers investing in IgY capacity may secure early contract wins with vaccine developers wanting sustainable inputs, contributing to the long-term competitiveness of the polyclonal antibodies market.

Cost dynamics also shift: goat facilities in low-labor-cost geographies now achieve unit economics comparable to large-scale rabbit establishments, encouraging portfolio diversification. Meanwhile, recombinant expression of polyclonal repertoires in CHO cells offers a future avenue for completely animal-free production.

By Application: Diagnostics retain size leadership; research accelerates

Diagnostics absorbed 55.30% of 2025 spending as histopathology, infectious-disease screening and companion diagnostics rely on broad epitope coverage to flag low-abundance targets. Clinical research, while smaller, is expanding at 6.55% annually on the back of proteomics grants and biomarker-driven drug-discovery programs. The polyclonal antibodies market size for clinical research is projected to rise in line with single-cell analyses, which demand reagents capable of recognizing splice variants and post-translational modifications simultaneously. Multiplex immunoassay kits embedding polyclonal capture antibodies shorten workflow times, an attractive feature for translational medicine units facing tight patient sample windows.

Regulators increasingly mandate orthogonal validation of biomarker assays. Laboratories combine polyclonal and monoclonal pairs to cross-verify presence and abundance, cementing the continued relevance of polyclonal formats even within precision-medicine settings. Over the forecast horizon, research funding volatility represents the principal risk, but growing public-private consortia mitigate sharp downturns.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals emerge as fastest-growing buyers

Biopharmaceutical manufacturers held 38.05% of 2025 demand, leveraging polyclonal reagents for host-cell protein monitoring and product-identity confirmation. Hospitals, however, will post a 6.18% CAGR as decentralized testing initiatives proliferate. Rapid antigen panels that detect multiple pathogen strains with a single strip rely on polyclonal capture layers for broad coverage, ideal for emergency departments and rural clinics. Academic and government laboratories retain consistent order flow, underpinning baseline stability for suppliers even during cyclical downturns in pharma capital expenditure.

High-throughput clinical chemistry analyzers now integrate polyclonal-based modules that automate calibration and control checks, reducing technician intervention and reinforcing hospital procurement trends. Over time, digital pathology adoption may create additional pull, as AI algorithms benefit from staining protocols that highlight a wide spectrum of cellular targets.

Geography Analysis

North America generated 43.95% of 2025 revenue and remains the epicenter of advanced antibody R&D. The FDA’s roadmap to modernize biologics testing—by removing certain animal-test requirements—lowers compliance barriers for innovative production technologies, sustaining investment momentum. Venture funding continues to favor startups developing recombinant polyclonal platforms, reflecting a robust commercialization pipeline.

Europe provides a complementary demand base shaped by stringent welfare regulations. The European Parliament’s resolution to phase out animal-derived antibodies galvanizes producers to adopt recombinant and IgY solutions earlier than peers on other continents. This regulatory stance strengthens local supply chains built around sustainable sourcing, positioning European manufacturers to export validated, welfare-compliant products worldwide.

Asia-Pacific delivers the fastest expansion at a 6.88% CAGR through 2031. Government incentives to localize biologics production in China, South Korea and India spur capacity additions across serum-purification and fill-finish operations. Domestic players secure priority access to public-health procurement tenders, challenging traditional Western exporters. Concurrently, multinational corporates invest in regional manufacturing hubs—Samsung Biologics’ USD 1.46 billion facility being emblematic—to serve global supply networks while capturing tariff advantages. The polyclonal antibodies market benefits from this dual-track strategy: rising in-region spend plus new export flows.

Competitive Landscape

Market Concentration

The polyclonal antibodies market features moderate fragmentation: no single firm controls more than one-tenth of global revenue, yet the top five companies collectively approach half of all sales. Established brands such as Thermo Fisher Scientific, Merck KGaA and Abcam defend share through validated catalog breadth, automated purification systems and stringent batch-release analytics. New entrants differentiate with AI-guided antigen selection and animal-free production, shortening lead times for custom projects and winning niche contracts in personalized medicine.

Mergers and licensing deals accelerate pipeline breadth. Sino Biological expanded its recombinant antibody library after opening a 20,000 m² bioprocessing center capable of 10,000 unique clones per year, bolstering its positioning in the growing Asia-Pacific customer base [3]Sino Biological, “Grand Opening of Recombinant Antibody Center,” sinobiological.com. In North America, GigaGen’s BARDA-funded recombinant polyclonal program illustrates public-sector confidence in multi-epitope therapeutics. Academic-industry collaborations, such as the University of Zurich’s multiplex animal-reduction protocol, push validation speed while aligning with welfare expectations, a competitive advantage in EU tenders.

Pricing remains firm because high-quality polyclonal production involves specialized animal facilities, skilled immunologists and extensive QC. However, recombinant expression could begin to cap prices by 2028 if yields reach parity with serum-derived methods. Suppliers investing early in automation and recombinant vectors are best placed to defend margins and expand volume simultaneously.

Polyclonal Antibodies Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Carter Keller confirmed a USD 135.2 million BARDA contract to advance recombinant polyclonal antibody therapies against botulinum neurotoxins and an undisclosed biothreat.

- October 2023: Creative Diagnostics launched Anti-Small Molecule Label Antibodies, including Anti-FAM polyclonal formulations, to enable next-generation nucleic-acid lateral-flow immunoassays.

- February 2023: Roche introduced the ATRX Rabbit Polyclonal Antibody to aid mutation detection in brain-cancer diagnostics.

Table of Contents for Polyclonal Antibodies Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Global Prevalence Of Infectious & Chronic Diseases

- 4.2.2Expanding Use In Diagnostics & Biopharma Production

- 4.2.3Growing Proteomics And Genomics Workflows

- 4.2.4Rising R&D Investment In Immunotherapy

- 4.2.5Emergence Of Sustainable Igy Platforms

- 4.2.6Ai-Driven Epitope Prediction For Custom Pabs

- 4.3Market Restraints

- 4.3.1Limited Availability Of High-Quality Pabs

- 4.3.2Intensifying Competition From Monoclonal And Recombinant Antibody Formats

- 4.3.3Batch-To-Batch Variability Impacting Reproducibility

- 4.3.4Tightening Animal-Welfare Regulations Increasing Cost

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts

- 5.1By Product Type

- 5.1.1Primary Antibody

- 5.1.2Secondary Antibody

- 5.2By Source

- 5.2.1Rabbit

- 5.2.2Mouse

- 5.2.3Goat

- 5.2.4Horse

- 5.2.5Other Animals

- 5.3By Application

- 5.3.1Diagnostic

- 5.3.2Clinical Research

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Academic & Research Centers

- 5.4.3Biopharmaceutical Industries

- 5.4.4Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Abcam plc

- 6.3.2Thermo Fisher Scientific Inc.

- 6.3.3Merck KGaA (MilliporeSigma)

- 6.3.4Bio-Rad Laboratories Inc.

- 6.3.5Agilent Technologies Inc.

- 6.3.6GenScript Biotech Corp.

- 6.3.7Creative Diagnostics

- 6.3.8Proteintech Group

- 6.3.9GeneTex Inc.

- 6.3.10Boster Biological Technology

- 6.3.11Rockland Immunochemicals Inc.

- 6.3.12Santa Cruz Biotechnology Inc.

- 6.3.13Sigma-Aldrich Corp.

- 6.3.14Abnova Corp.

- 6.3.15Lonza Group Ltd.

- 6.3.16Sino Biological Inc.

- 6.3.17Novus Biologicals (Bio-Techne)

- 6.3.18Gallus Immunotech

- 6.3.19Emergent BioSolutions Inc.

- 6.3.20ImmunoPrecise Antibodies Ltd.

- 6.3.21SAB Biotherapeutics Inc.

- 6.3.22PerkinElmer Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Polyclonal Antibodies Market Report Scope

As per the scope of the report, the polyclonal antibody market comprises a group of antibodies that represent the body's normal immunological response to an antigen. These are a collection of immunoglobulin molecules that react to a certain antigen and isolate different epitopes from that antigen. The polyclonal antibody market is segmented by product type (primary antibody and secondary antibody), source type( rabbit, mouse, goat, horse, and other animals), application (diagnostic and clinical research), end-user (hospitals, academics, biopharmaceutical industries, biotechnology industries, and diagnostic centers), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above segments.