GMP Protein E Coli Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.11 Billion |

| Market Size (2030) | USD 1.75 Billion |

| Growth Rate (2025 - 2030) | 9.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GMP Protein E Coli Contract Manufacturing Market Analysis by Mordor Intelligence

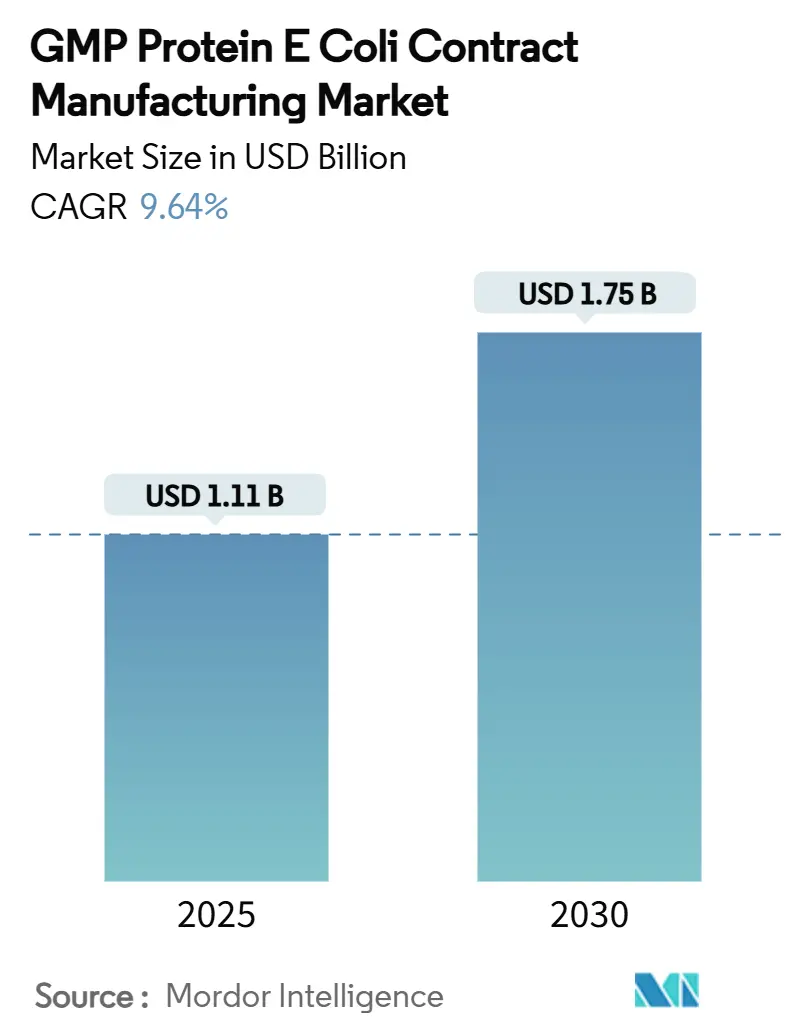

The GMP Protein E. coli Contract Manufacturing market size reached USD 1.11 billion in 2025 and is forecast to rise to USD 1.75 billion by 2030, advancing at a 9.64% CAGR. The GMP Protein E. coli Contract Manufacturing market expands as drug sponsors adopt Escherichia coli platforms that compress timelines and trim costs without sacrificing regulatory compliance. Rising biologics and biosimilar pipelines, accelerated orphan-drug activity, and the outsourcing push from capital-constrained biotech firms continue to propel the GMP Protein E. coli Contract Manufacturing market. Contract development and manufacturing organizations (CDMOs) deepen service breadth through cell-free expression, high-density fermentation, and single-use systems, while geographic capacity additions secure supply resilience. Competitive differentiation hinges on regulatory track records, process technology, and geographical diversification.

Key Report Takeaways

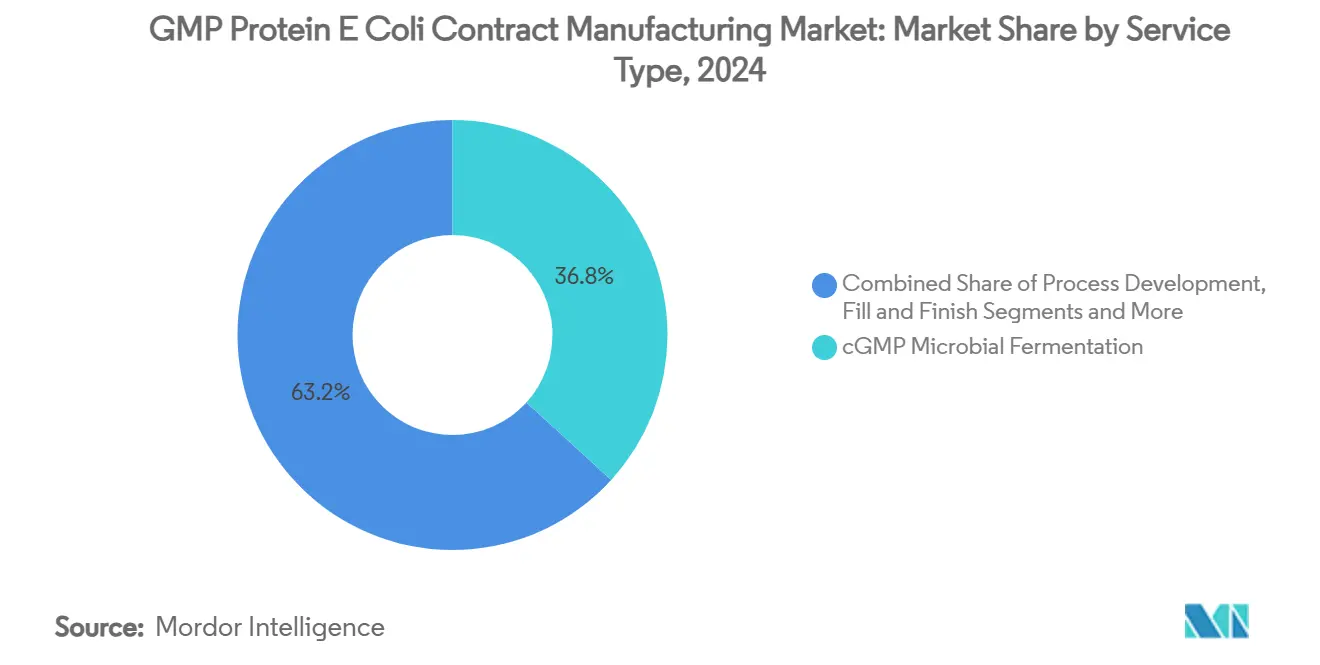

- By service type, cGMP microbial fermentation led with 36.77% revenue share in 2024, while cell-free protein synthesis services are projected to expand at a 13.41% CAGR through 2030.

- By product type, recombinant therapeutic proteins commanded 41.23% of revenue in 2024, whereas antibody fragments and scFvs are set to grow at a 12.47% CAGR to 2030.

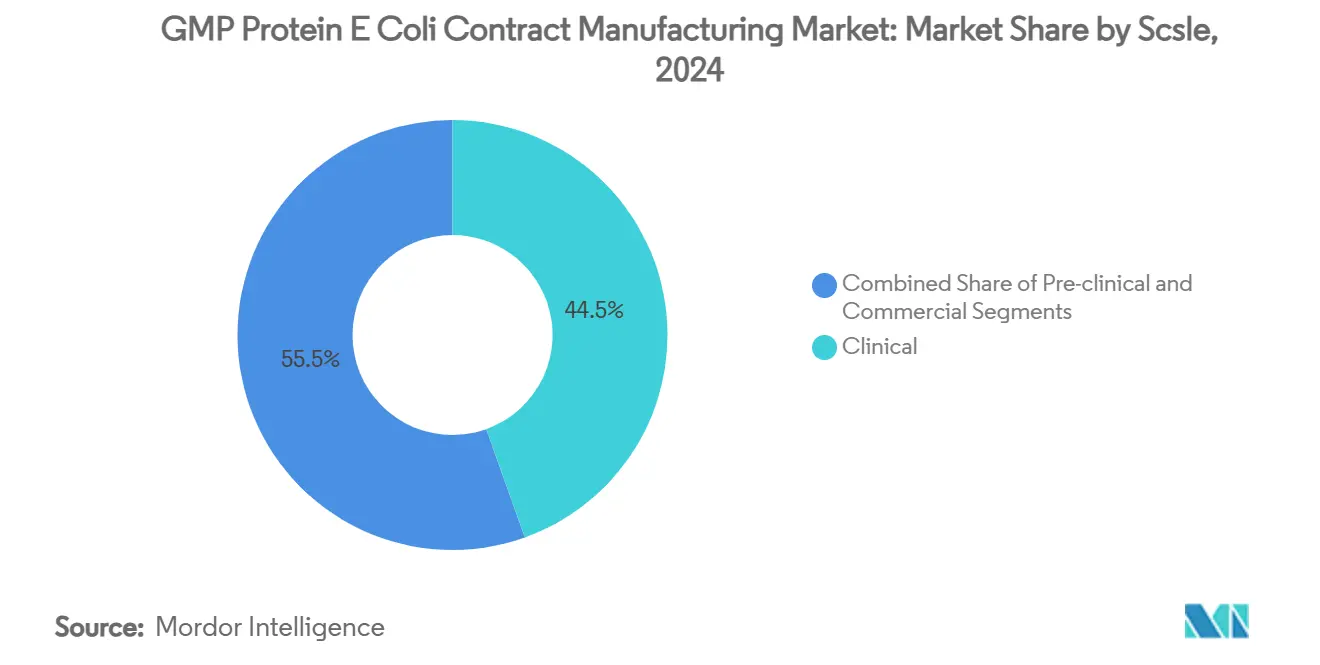

- By scale, clinical production held 44.52% revenue share in 2024, and pre-clinical manufacturing is poised for a 12.79% CAGR through 2030.

- By end user, pharmaceutical companies accounted for 49.68% of revenue in 2024, while biotechnology start-ups are expected to advance at an 11.58% CAGR through 2030.

- By geography, North America captured 39.58% revenue share in 2024, as Asia-Pacific records the highest forecast growth at an 11.84% CAGR to 2030.

Global GMP Protein E Coli Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of biologics & biosimilars | +2.1% | North America, Europe | Long term (≥ 4 years) |

| Cost & time efficiency of E. coli platforms | +1.8% | Global; strongest in Asia-Pacific | Medium term (2-4 years) |

| Surge in orphan-drug pipeline volumes | +1.5% | North America, Europe | Medium term (2-4 years) |

| Outsourcing by small & mid-size biotechs | +1.3% | Global; early adoption in North America | Short term (≤ 2 years) |

| Cell-free synthesis using E. coli lysates | +1.0% | North America, Europe | Long term (≥ 4 years) |

| GMP plasmid demand for mRNA workflows | +0.9% | Global; demand centers in North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption Of Biologics & Biosimilars

Patent expiries for originator biologics have intensified biosimilar development, and regulatory agencies have streamlined approval pathways, spurring sustained demand for scalable microbial production. E. coli systems deliver cost-efficient, non-glycosylated therapeutics that meet stringent quality expectations.[1]U.S. Food and Drug Administration, “Advanced Manufacturing Technologies Designation Program,” fda.gov Biosimilar developers such as Valerius Biopharma harness optimized microbial platforms through CDMO partnerships to balance affordability with compliance. As additional blockbuster biologics lose exclusivity, the GMP Protein E. coli Contract Manufacturing market benefits from repeat production contracts.

Cost & Time Efficiency Of E. coli Platforms

High-cell-density fed-batch protocols deliver optical densities above 139 in 30 L fermenters, cutting cycle times to days and minimizing capital intensity.[2]Martin Kangwa, “High-level Fed-Batch Fermentative Expression of an Engineered Staphylococcal Protein A Based Ligand in E. coli,” amb-express.springeropen.comSingle-use fermentors further lower facility costs and increase agility, aligning with the rapid iteration needs of small biotechs.[3]Nephi Jones, “Single-Use Processing for Microbial Fermentations,” BioProcess International, bioprocessintl.comConsequently, sponsors gravitate toward E. coli CDMOs to compress development timelines and conserve venture funding.

Surge In Orphan-Drug Pipeline Volumes

Regulatory incentives and market exclusivity have propelled rare-disease programs, many requiring small-batch therapeutic proteins suitable for microbial expression. Specialized facilities accommodate flexible scheduling and smaller bioreactors, creating a profitable niche for providers focused on orphan drug production.

Outsourcing By Small & Mid-Size Biotechs

Early-stage companies increasingly outsource GMP work to sidestep capital outlays and navigate complex regulatory demands. Geopolitical legislation such as the BIOSECURE Act encourages diversification away from certain geographies, steering projects toward CDMOs in the United States, Europe, and India.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited post-translational capability | -1.4% | Global; most acute for complex biologics | Long term (≥ 4 years) |

| Endotoxin-control regulatory hurdles | -1.1% | North America, Europe | Medium term (2-4 years) |

| Yeast & cell-free system competition | -0.9% | Global; adoption varies by region | Medium term (2-4 years) |

| Disposable-supply chain volatility | -0.7% | Global; heightened during logistic disruptions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Post-Translational Capability

E. coli lacks native glycosylation, restricting its use for complex glycoproteins. Although engineered strains improve folding and permit disulfide-bonded peptide production, added process complexity raises costs. Many monoclonal antibodies thus remain in mammalian systems, limiting microbial share of certain indications.

Endotoxin-Control Regulatory Hurdles

Stringent endotoxin thresholds for parenterals impose sophisticated purification schemes and extensive validation. Advanced chromatographic resins and engineered low-endotoxin strains reduce risk yet lengthen timelines and elevate budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Fermentation Services Drive Market Leadership

The cGMP microbial fermentation segment contributed 36.77% of total revenue in 2024, reinforcing its role as the core value driver within the GMP Protein E. coli Contract Manufacturing market size. Elevated yields achieved through intensified fed-batch and perfusion processes increase client confidence and margin potential. Segment expansion benefits from investments in 2,000 L single-use fermentors that shorten changeover times and support multiproduct schedules, particularly for biosimilar programs.

Cell-free protein synthesis, while only a fraction of today’s output, posts a 13.41% CAGR through 2030 as novel oncology and personalized vaccines migrate toward lysate-based formats. Process development, purification, and analytical testing services deepen integration, allowing CDMOs to capture end-to-end contracts. Fill-finish demand accelerates in tandem with injectable biologics, and logistics providers add GDP-compliant cold-chain lanes that maintain product integrity during global distribution.

By Product Type: Therapeutic Proteins Maintain Dominance

Recombinant therapeutic proteins represented 41.23% of 2024 revenues, anchored by insulin analogs, growth factors, and cytokines. Their regulatory maturity simplifies scale-up, ensuring steady project inflow. The GMP Protein E. coli Contract Manufacturing market share for antibody fragments and scFvs grows fastest, supported by smaller molecular weights that align with microbial hosts and enable deeper tumor penetration.

Vaccines and antigens remain an attractive stream following pandemic-era public investment, while enzymes and cytokines continue to serve both therapeutic and industrial ends. Peptide and hormone output rises as engineered strains facilitate correct disulfide pairing, broadening E. coli’s applicability to complex hormone analogs.

By Scale: Clinical Production Leads Market Segments

Clinical production captured 44.52% revenue in 2024, underscoring the premium that late-stage sponsors place on reliability and regulatory alignment. The GMP Protein E. coli Contract Manufacturing market size for clinical supply climbs as Phase III pipelines expand, and continuous manufacturing concepts reduce per-gram costs.

Pre-clinical batches experience a 12.79% CAGR because venture-backed start-ups turn to virtual business models, contracting out all laboratory and pilot work. Commercial manufacturing, though fewer in absolute projects, remains the most lucrative per program due to multiyear supply agreements supported by life-cycle management activities.

By End User: Pharmaceutical Companies Drive Demand

Pharmaceutical companies accounted for 49.68% of 2024 billings, leveraging external capacity to hedge risk and avoid fixed-asset exposure. Established quality systems and global distribution rights render large pharma an anchor clientele for CDMOs.

Biotechnology start-ups deliver the highest growth at an 11.58% CAGR, mirroring record venture funding cycles. Academic institutes exploit pilot-scale suites for proof-of-concept molecules, while diagnostic companies extend demand by outsourcing antigen and enzyme production for kit manufacture.

Geography Analysis

North America held 39.58% of global turnover in 2024, fueled by a dense network of biopharma clusters, mature regulatory guidance, and recent capacity expansions such as Lonza’s 330,000 L acquisition in Vacaville. The region prioritizes advanced manufacturing through the FDA’s technology designation program, encouraging CDMOs to integrate automation and continuous processing. While supply-chain shocks elevate input costs, North American providers offset risk through multi-site redundancy and strategic safety stocks.

Asia-Pacific records the quickest ascent with an 11.84% CAGR to 2030. Chinese leader WuXi Biologics scaled microbial capacity in Massachusetts and China, reflecting global ambitions despite geopolitical scrutiny. Indian CDMOs capture redirected projects as sponsors diversify away from single-country dependencies, aided by competitive labor costs and improving regulatory frameworks. Regional governments actively court biologics investment, offering tax incentives and expedited land approvals that further accelerate facility builds.

Europe remains stable, underpinned by harmonized EMA standards and legacy microbial expertise. FUJIFILM Diosynth tripled fermentation capacity at its UK site, signaling confidence in regional demand. Sustainability mandates drive adoption of energy-efficient single-use systems; however, high utility costs compel a focus on high-value niche products where European reputational strength justifies premium pricing. Eastern European states increasingly attract greenfield biomanufacturing as they blend lower labor rates with EU regulatory coverage, balancing the broader European cost profile.

Competitive Landscape

The GMP Protein E. coli Contract Manufacturing market demonstrates moderate concentration. Lonza, Boehringer Ingelheim BioXcellence, Fujifilm Diosynth, WuXi Biologics, and Samsung Biologics form the top echelon, backed by multi-continent facilities and deep regulatory dossiers. Sutro Biopharma’s cell-free achievements showcased an innovation pivot that competitors now chase.

Strategic collaborations proliferate: Lonza licenses plasmid technologies to complement protein services, Aldevron partners with Acuitas for lipid nanoparticle synergies, and KBI Biopharma allies with Argonaut for integrated fill-finish. Capital markets validate the sector’s prospects as private equity acquires Avid Bioservices for USD 1.1 billion, highlighting appetite for assets with microbial depth.

Process digitalization and advanced control systems further separate leaders from laggards. Continuous real-time analytics enable autonomous operations that lift yields and curtail deviations. Players capable of absorbing disposable-component volatility and implementing redundant suppliers gain reputational advantage amid persistent supply constraints.

GMP Protein E Coli Contract Manufacturing Industry Leaders

Lonza

Boehringer Ingelheim

Fujifilm

AGC Biologics

Wuxi Biologics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: WuXi Biologics launched EffiX, a proprietary E. coli expression system targeting high-yield recombinant proteins.

- January 2025: Sutro Biopharma and Boehringer Ingelheim BioXcellence achieved commercial-scale GMP production of luveltamab tazevibulin using cell-free technology.

- March 2024: Xpress Biologics secured GMP certification for recombinant protein manufacturing at its Belgium site.

Global GMP Protein E Coli Contract Manufacturing Market Report Scope

| Process Development |

| cGMP Microbial Fermentation |

| Purification Processing |

| Analytical & QC Testing |

| Fill & Finish |

| Packaging & Logistics |

| Recombinant Therapeutic Proteins |

| Vaccines & Antigens |

| Enzymes & Cytokines |

| Antibody Fragments & ScFvs |

| Peptides & Hormones |

| Pre-clinical |

| Clinical |

| Commercial |

| Pharmaceutical Companies |

| Biotechnology Start-ups |

| Academic & Research Institutes |

| Diagnostic Companies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Process Development | |

| cGMP Microbial Fermentation | ||

| Purification Processing | ||

| Analytical & QC Testing | ||

| Fill & Finish | ||

| Packaging & Logistics | ||

| By Product Type | Recombinant Therapeutic Proteins | |

| Vaccines & Antigens | ||

| Enzymes & Cytokines | ||

| Antibody Fragments & ScFvs | ||

| Peptides & Hormones | ||

| By Scale | Pre-clinical | |

| Clinical | ||

| Commercial | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Start-ups | ||

| Academic & Research Institutes | ||

| Diagnostic Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the GMP Protein E. coli Contract Manufacturing market?

The market is valued at USD 1.11 billion in 2025.

How fast is the sector growing?

It is forecast to register a 9.64% CAGR between 2025 and 2030.

Which service segment leads revenue?

CGMP microbial fermentation holds 36.77% of 2024 revenue.

Which region grows the quickest?

Asia-Pacific is projected to expand at an 11.84% CAGR to 2030.

Why do start-ups prefer outsourcing?

Outsourcing avoids heavy capital investment and eases regulatory complexity, letting start-ups focus on R&D.

Page last updated on: