Algae Based Animal Feed Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

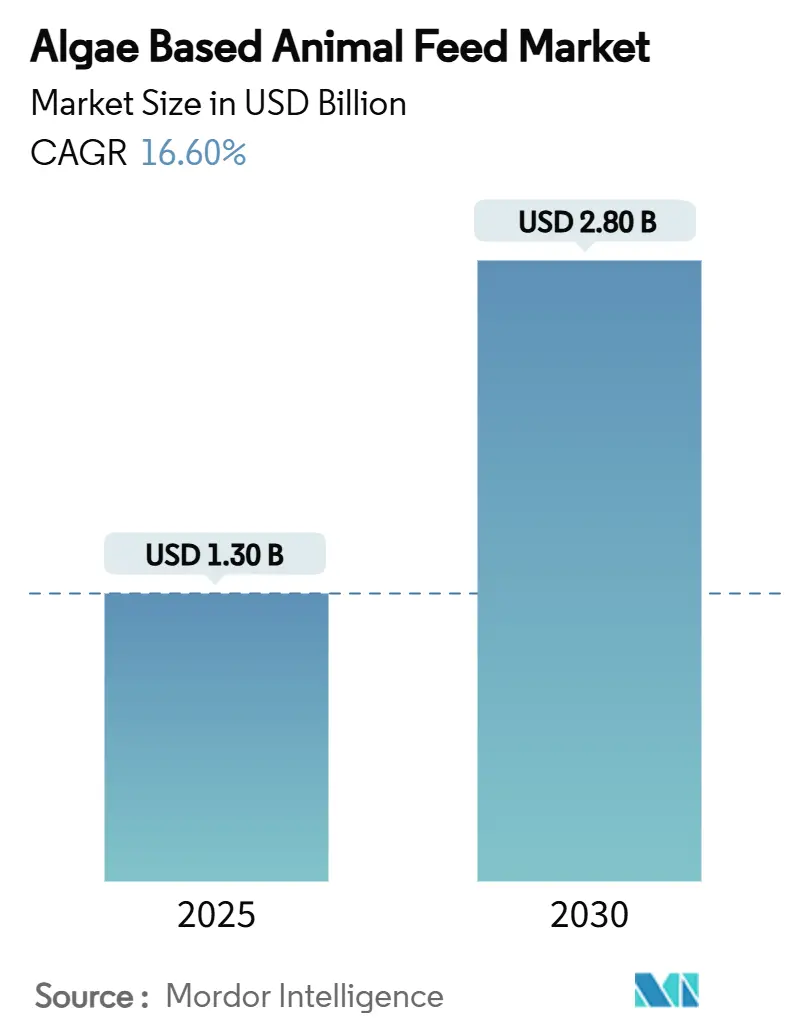

| Market Size (2025) | USD 1.30 Billion |

| Market Size (2030) | USD 2.80 Billion |

| Growth Rate (2025 - 2030) | 16.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algae Based Animal Feed Market Analysis by Mordor Intelligence

The algae-based animal feed market size was USD 1.3 billion in 2025 and is forecast to expand at a 16.6% CAGR to reach USD 2.8 billion in 2030. Rising demand for sustainable protein sources, regulatory pressure to curb fish-meal dependence and livestock methane, and expanding functional food premiums are accelerating adoption across livestock systems. Aquaculture maintains the highest consumption share as salmon farmers replace wild-caught fish oil with algae-derived omega-3. Rapid technological gains in photobioreactors and heterotrophic fermentation are narrowing production cost gaps, while industrial carbon-capture projects push new cost-efficient supply models. Mid-sized producers partner with multinational feed companies to secure off-take agreements, ensuring ingredient quality and supply stability.

Key Report Takeaways

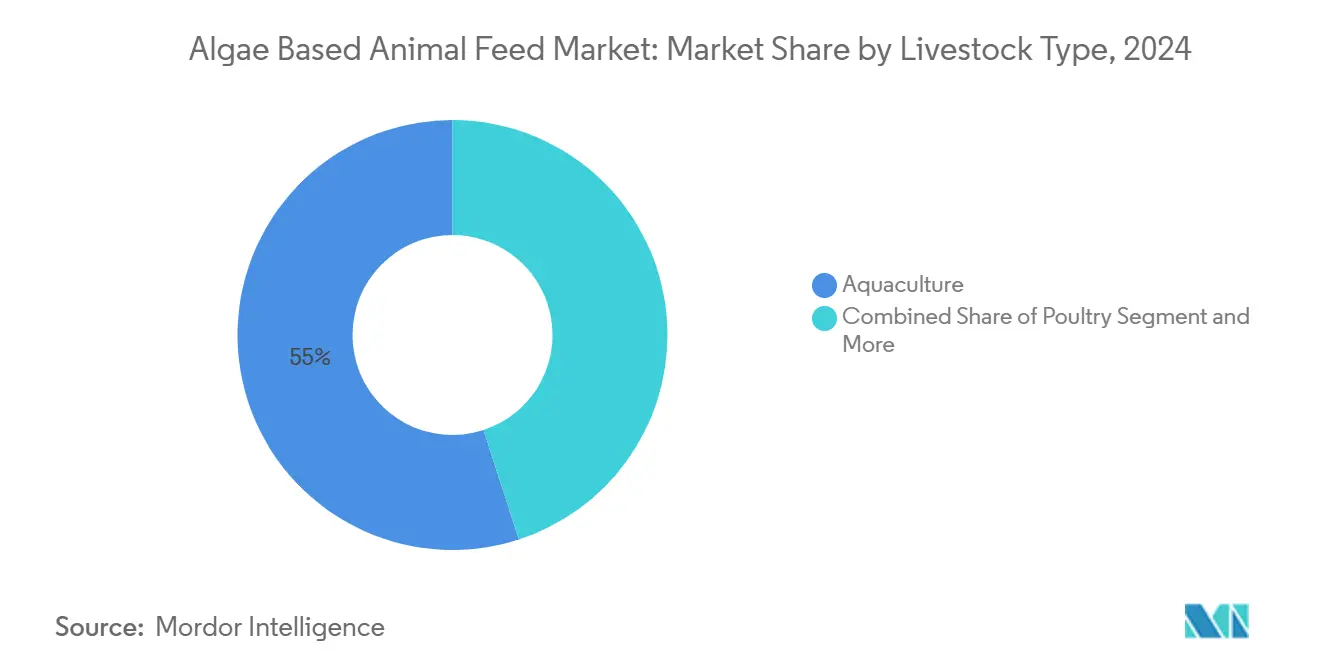

- By livestock type, aquaculture held a 55.0% share of the algae-based animal feed market size in 2024, while poultry is projected to post the fastest 21.4% CAGR to 2030.

- By algae species, spirulina led with 42.0% of the algae-based animal feed market share in 2024, schizochytrium is forecast to grow at 24.0% CAGR through 2030.

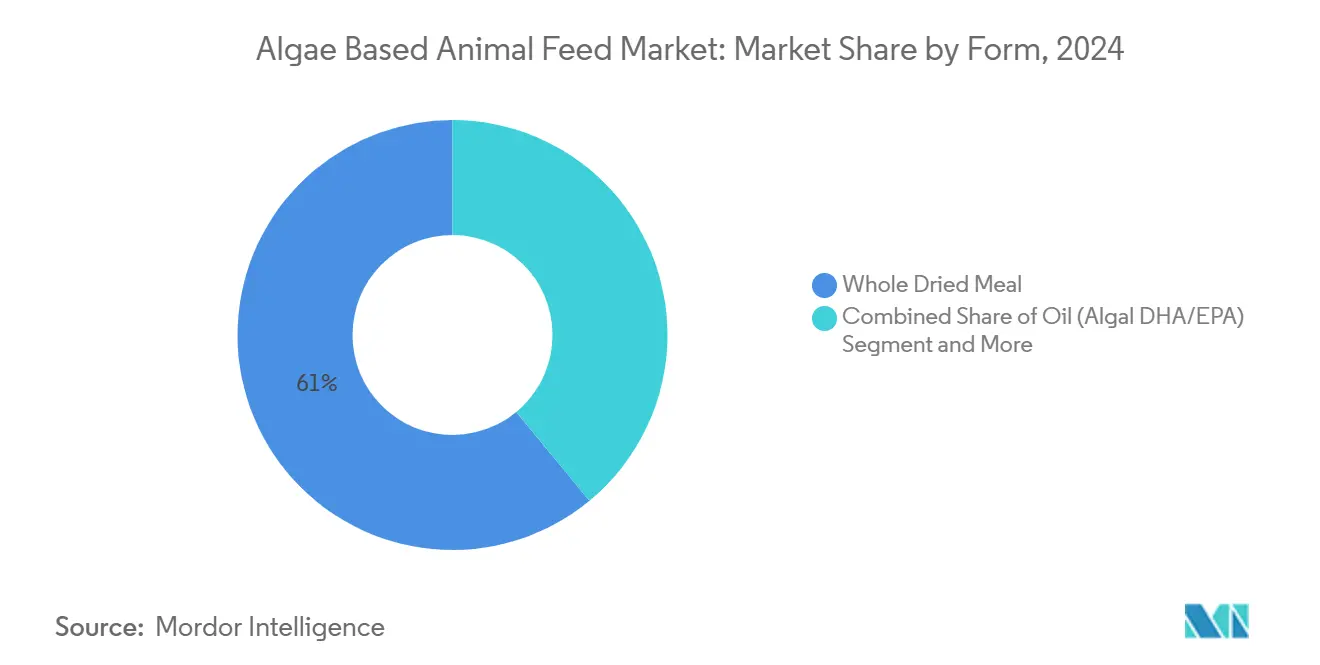

- By form, whole dried meal accounted for 61.0% share of the market size in 2024, and algal oil is advancing at a 26.5% CAGR through 2030.

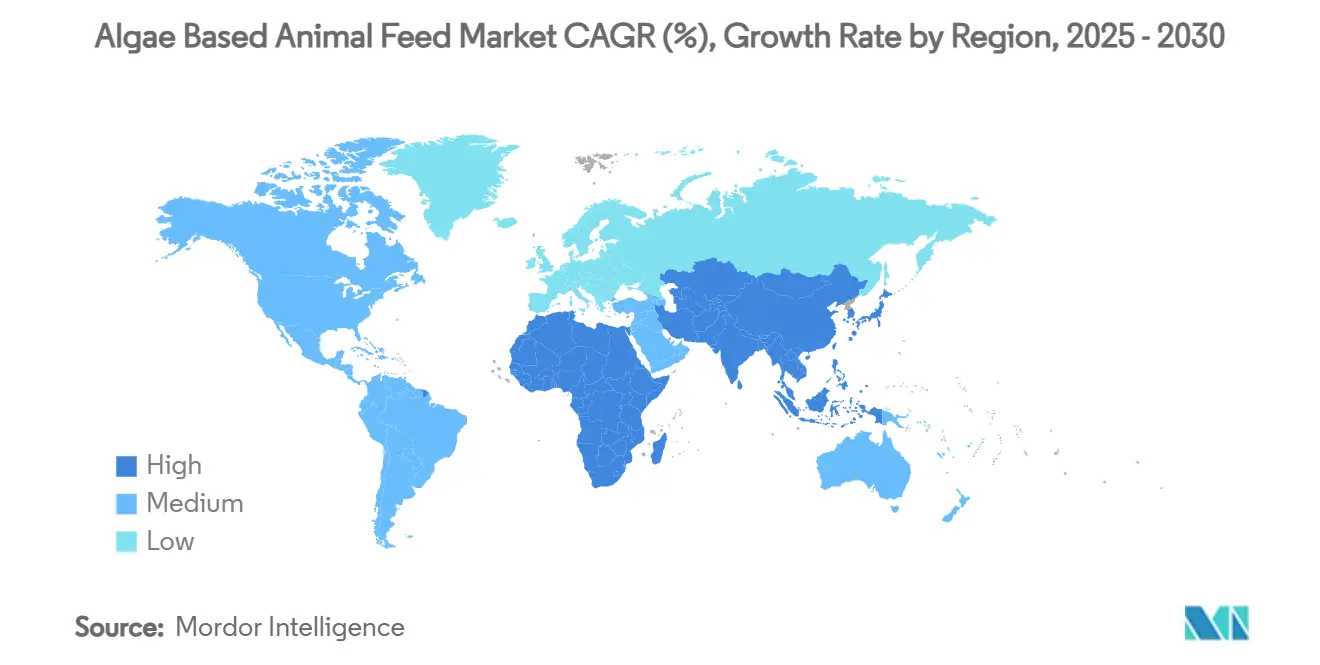

- By geography, Europe captured 35.4% of global revenue in 2024, and Asia-Pacific is projected to expand at a 19.4% CAGR to 2030.

Global Algae Based Animal Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable replacement for fish-meal and fish-oil in aquafeed | +4.2% | Asia-Pacific and Europe | Medium term (2-4 years) |

| Functional food premiums from omega-3 enriched meat, milk, and eggs | +3.1% | North America and Europe | Short term (≤2 years) |

| Regulatory pressure to cut livestock methane and antibiotic use | +2.8% | Europe and North America, expanding in Asia-Pacific | Long term (≥4 years) |

| Industrial CO₂- and wastewater-integrated algae cultivation lowers input costs | +2.3% | China and Netherlands lead | Medium term (2-4 years) |

| On-site modular photobioreactors at aquaculture farms slash logistics | +1.9% | Coastal regions, Norway and Chile | Medium term (2-4 years) |

| Scope-3 net-zero commitments forcing ingredient substitution deals | +2.2% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Sustainable replacement for fish-meal and fish-oil in aquafeed

Global fish-meal supply has plateaued while wild stocks face catch limits. Algae proteins mirror fish-meal amino acids, and algae oils supply long-chain omega-3 without marine harvest pressure. Cargill’s Latitude feeds improved salmon feed conversion significantly and reduced reliance on wild fish oil.[1]Cargill, “Latitude Algae Oil Improves Salmon Performance,” cargill.com EU quota curbs under the Common Fisheries Policy have accelerated algae adoption, and Veramaris’ Nebraska plant produces 15,000 metric tons of algal oil annually for direct fish-oil substitution. Feed manufacturers increasingly position algae-based animal feed market offerings as verified sustainable inputs that unlock premium branding for seafood exporters.

Functional food premiums from omega-3 enriched meat, milk, and eggs

Consumers routinely pay 25-40% more for omega-3 enhanced eggs and 15-20% more for DHA-rich poultry meat. Alltech’s All-G-Rich meal raises egg omega-3 content threefold, supporting retailer premium lines in Europe and the United States. Similar benefits now extend to dairy herds, where algal supplementation increases milk omega-3 while maintaining yield. These premiums create a margin pool that offsets current cost differentials, expanding the algae-based animal feed market across poultry and dairy value chains.

Regulatory pressure to cut livestock methane and antibiotic use

In addition to premium pricing for omega-3-enriched products, regulatory initiatives such as the EU Farm to Fork Strategy aim to cut livestock emissions by 50% by 2030. Spirulina inclusion at 2-3% reduces enteric methane by up to 18% in cattle, and policymakers consider feed-credits akin to renewable energy certificates. California already awards USD 200 per metric-ton CO₂-equivalent reductions, making algae feeds cash-positive for compliant dairies. New Zealand’s proposed 2025 pricing on farm emissions will increase demand across its ruminant sector. These policies strengthen long-run adoption curves for the algae-based animal feed market.

Industrial CO₂- and wastewater-integrated algae cultivation lowers input costs

Co-locating algae farms with industrial emitters slashes carbon capture costs and recycles process water. Calysseo’s FeedKind plant in Chongqing diverts factory CO₂ to produce 20,000 metric tons of single-cell protein at sub-USD 2.50 kg cost. Projects in the Netherlands and Portugal link breweries and cement plants to photobioreactors, yielding dual revenue from carbon abatement and feed sales. Integrated models narrow the algae-to-fish-meal cost gap and accelerate new capacity in the algae-based animal feed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost versus soybean meal and corn gluten | -3.8% | Price-sensitive markets globally | Long term (≥4 years) |

| Limited large-scale production capacity | -2.1% | Asia-Pacific most affected | Medium term (2-4 years) |

| Palatability Issues at Inclusion Rates Above 10% | -1.4% | Poultry and swine worldwide | Short term (≤2 years) |

| Regulatory uncertainty around novel feed ingredients | -1.7% | Emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost versus soybean meal and corn gluten

Average algae biomass ranges from USD 2.83 per kg to USD 315 per kg, while fish-meal hovers at USD 1.36-1.64 per kg and soybean meal near USD 0.50 per kg. Although technological gains have cut costs by 40% in recent facilities, price gaps remain material in bulk rations. Functional food premiums and carbon credits help bridge the difference, yet broad parity may not emerge before 2029, slowing mass-market uptake of the algae-based animal feed market.

Palatability Issues at Inclusion Rates Above 10%

In poultry and swine diets, inclusion rates above 10% sometimes cut intake due to pigment and odor profiles.[2]MDPI, “Palatability of Microalgae in Animal Feed,” mdpi.comOngoing strain selection and extraction processes reduce off-flavors in seaweed-based products. However, palatability continues to be a significant challenge for manufacturers. This limitation on dosage affects potential revenue growth, and the industry must overcome these taste barriers to achieve broader market acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Livestock Type: Aquaculture dominance, poultry fastest rise

Aquaculture captured 55.0% of the algae-based animal feed market size in 2024, on demand for fish-oil alternatives in salmon, shrimp, and trout feeds. Segment growth is forecast at 18.2% CAGR for 2025-2030 as more producers switch to algae oils with verified EPA-DHA levels. Poultry trails at 16.0% share yet accelerates at 21.4% CAGR on the back of omega-3 enriched egg and meat premiums.

Swine adoption builds gradually as integrators test 8% inclusion for gut health and odor mitigation. Ruminant demand expands more slowly, limited by palatability above 3% inclusion despite methane mitigation benefits. The pet category remains niche, but premium positioning and humanization trends reward algae-based functional claims, lifting its volume by double digits annually.

By Algae Species: Spirulina leadership faces schizochytrium surge

Spirulina retained 42.0% of the algae-based animal feed market share in 2024 because of established open-pond capacity and broad nutritional acceptance. Schizochytrium is forecast to post a 24.0% CAGR, propelled by heterotrophic fermentation that delivers 50% DHA oil independent of sunlight or climate variance.

Chlorella services immune-boosting and pigmentation niches, while Nannochloropsis and Haematococcus gain traction for aquaculture coloration. Growth outlook shows the algae-based animal feed market transitioning from single-species dominance toward species-specialist portfolios serving differentiated livestock outcomes.

By Form: Whole dried meal tops, algal oil accelerates

Whole dried meal held a 61.0% share in 2025 due to cost-effective spray-drying and handling simplicity. Algal oil, however, will record a 26.5% CAGR through 2030 as salmon farmers, pet-food formulators, and human supplement co-manufacturers demand high-purity omega-3.

Extracts such as astaxanthin attain premium pricing, yet volumes remain small. Supercritical CO₂ extraction now achieves 95% oil purity for direct fish-oil substitution by European salmon growers, validating high-value off-take. The algae-based animal feed market size for algal oil may exceed USD 700 million by 2030.

Geography Analysis

Europe generated 35.4% of global value in 2025, supported by the EU4Algae roadmap and more than 20 algae species approved as novel feed ingredients. Norway’s salmon sector consumes most European output, with BioMar and Skretting incorporating algae oil across premium lines. Germany hosts Veramaris’ large-scale facility and clusters public-private R&D alliances that refine photobioreactor efficiency. Consumer appetite for eco-labels sustains premium pricing, enabling positive margins despite higher production costs.

Asia-Pacific is the fastest expanding region with a 19.4% CAGR to 2030. Global seaweed production is concentrated in East and Southeast Asian countries, which have practiced commercial seaweed farming for over five decades.[3]World Bank, “Seaweed Aquaculture for Food Security,” worldbank.orgChina drives capacity through the FeedKind plant and multiple spirulina farms in Inner Mongolia and Hainan. Vietnam and Indonesia adopt algae oil in shrimp broodstock diets to meet US and EU procurement standards. India’s poultry integrators experiment with algae inclusion to tap functional egg demand in urban centers. Regional governments encourage carbon-capture-linked algae cultivation through tax breaks, supporting capital formation and positioning Asia-Pacific as a long-term cost leader in the algae-based animal feed market.

North America held a 28.2% share in 2025 on the strength of technological innovation and premium aquaculture. The United States anchors high-purity DHA production for salmon feed exports and supplies functional food manufacturers. Canada fosters pilot programs within Atlantic salmon and trout farms and co-funds algae R&D targeting cold-water species. Mexico constitutes an emerging frontier where integrated poultry firms explore algae proteins to improve meat nutrient density and differentiate export offerings.

Competitive Landscape

The market indicates a moderately concentrated environment. Competition centers on technological edge rather than price, as companies race to boost biomass productivity, oil purity, and functional-compound yields. Cargill leverages joint ventures with Veramaris to secure algae oil for its Latitude feed line and partners with Norwegian farmers for cage-side demonstrations.

Corbion’s full acquisition of AlgaPrime DHA streamlines decision-making and financing for expansion. Alltech’s Nordic acquisition extends functional DHA products into the salmon and trout markets. BioMar collaborates with Calysseo, integrating single-cell proteins into shrimp formulas.

Smaller innovators focus on modular photobioreactors, species specialization, and carbon-capture integration. Successful entrants differentiate through verified life-cycle carbon reductions, palatability solutions, and multi-stream biorefineries that monetize pigments and nutraceuticals. The algae-based animal feed market, therefore, rewards vertical integrations and cross-industry partnerships that de-risk scale-up.

Algae Based Animal Feed Industry Leaders

Cargill, Incorporated

ADM

Alltech

Corbion

BioMar Group (Schouw & Co)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Cellana announced a merger with PhytoSmart to create an integrated algae cultivation and processing platform, combining Hawaiian production facilities with European distribution networks.

- February 2022: BioMar increased the use of microalgae as an ingredient in fish feed production, following its extensive research and development studies on algae-based ingredients.

Global Algae Based Animal Feed Market Report Scope

| Aquaculture |

| Poultry |

| Swine |

| Ruminant |

| Pets |

| Spirulina |

| Chlorella |

| Schizochytrium/DHA-rich Algae |

| Others |

| Whole Dried Meal |

| Oil (Algal DHA/EPA) |

| Extracts/Pigments |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Chile | |

| Rest of South America | |

| Europe | Norway |

| Germany | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Livestock Type | Aquaculture | |

| Poultry | ||

| Swine | ||

| Ruminant | ||

| Pets | ||

| By Algae Species | Spirulina | |

| Chlorella | ||

| Schizochytrium/DHA-rich Algae | ||

| Others | ||

| By Form | Whole Dried Meal | |

| Oil (Algal DHA/EPA) | ||

| Extracts/Pigments | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Chile | ||

| Rest of South America | ||

| Europe | Norway | |

| Germany | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the algae based animal feed market in 2025?

The sector generated USD 1.3 billion in 2025 and is projected to grow rapidly to 2030.

Which livestock segment uses the most algae feed?

Aquaculture leads with 55.0% share, mainly from salmon and shrimp operations seeking sustainable omega-3 sources.

What is driving algae feed expansion in Asia-Pacific?

Rapid aquaculture growth in China and Vietnam, supportive industrial carbon-capture projects and cost-competitive production capacity boost regional demand.

Which algae species is growing fastest?

Schizochytrium is forecast to register a 24.0% CAGR through 2030 thanks to high DHA content achieved via heterotrophic fermentation.

Page last updated on: