Angola Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

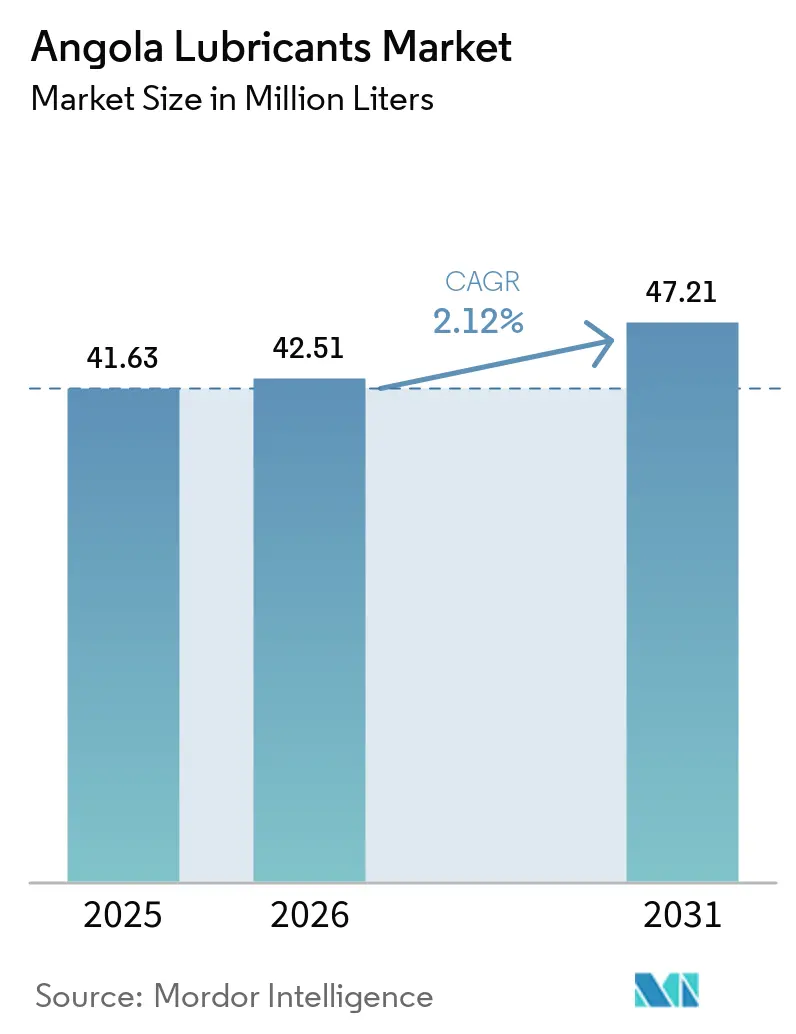

| Base Year Market Size (2025) | 41.63 Million liters |

| Market Volume (2026) | 42.51 Million liters |

| Market Volume (2031) | 47.21 Million liters |

| Growth Rate (2026 - 2031) | 2.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Angola Lubricants Market Analysis by Mordor Intelligence

The Angola Lubricants Market size is projected to expand from 41.63 Million liters in 2025 and 42.51 Million liters in 2026 to 47.21 Million liters by 2031, registering a CAGR of 2.12% between 2026 to 2031. Robust mining and construction activities, new downstream investments, and logistics improvements are driving demand, despite the country's continued reliance on imports for 80% of its lubricant needs. Automotive engine oil remains the leading segment, as commercial vehicle fleets and aging passenger cars significantly outnumber early-stage electric vehicles (EVs). Demand from heavy equipment, power generation, and marine sectors sustains high lubricant consumption, while the establishment of new local blending plants, such as Etu Energias’ 20,000 tons per year facility, is expected to reduce lead times and foreign exchange dependency. The enforcement of Executive Decree 31/21, which aligns local quality standards with API and ACEA norms, is prompting smaller blenders to upgrade operations or exit the market. This regulation is also driving the adoption of premium synthetic and bio-based formulations that align with mining clients’ environmental, social, and governance (ESG) objectives. Additionally, the September 2025 start-up of the Cabinda refinery and the rehabilitation of the Lobito Corridor rail network are anticipated to lower feedstock and freight costs, enhancing domestic value addition in the Angola lubricants market.

Key Report Takeaways

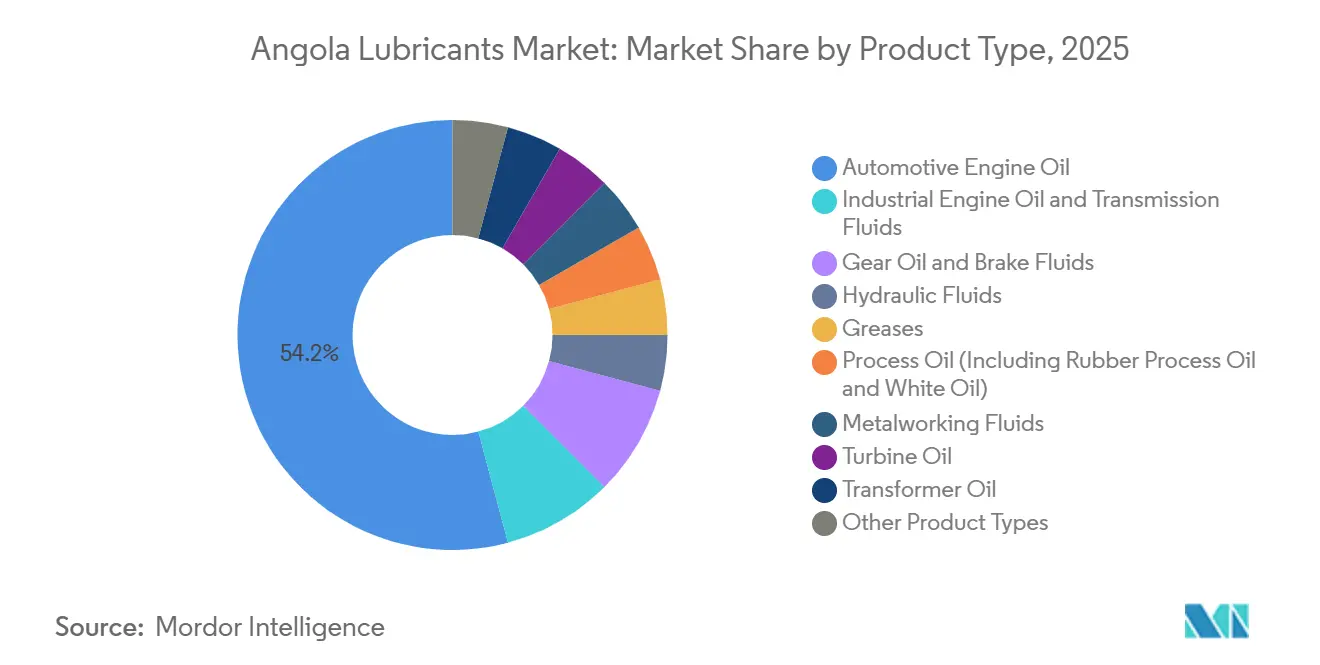

- By product type, automotive engine oil led with 54.15% Angola lubricants market share in 2025 and is projected to advance at a 2.41% CAGR through 2031.

- By base stock type, mineral oil-based lubricants accounted for 67.12% of the Angola lubricants market share in 2025, while bio-based lubricants are poised to grow fastest at a 2.55% CAGR through 2031.

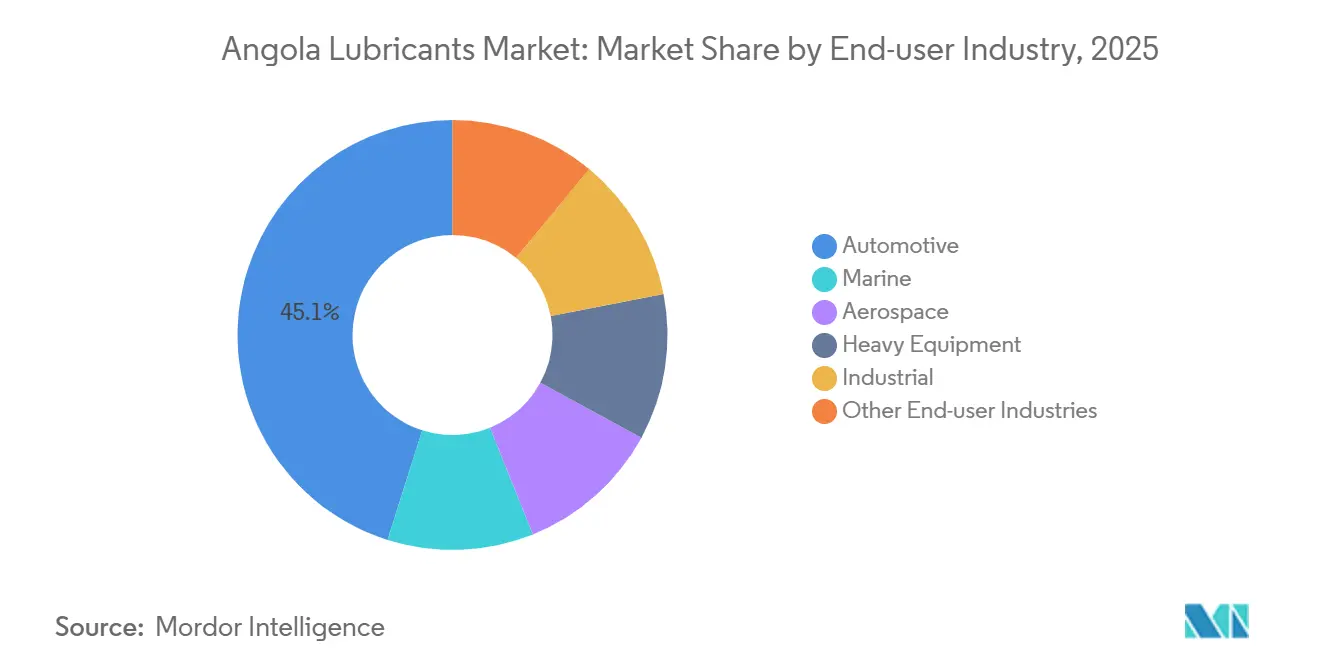

- By end-user industry, automotive held 45.12% of the Angola lubricants market share in 2025, while heavy equipment is set to grow at a 2.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Angola Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mining and construction projects | +0.8% | National, concentrated in Lunda Norte, Lunda Sul, Uíge | Medium term (2–4 years) |

| Industrial power-generation expansion | +0.4% | National, with key nodes in Luanda, Cabinda, Benguela | Long term (≥ 4 years) |

| Rebound in vehicle sales | +0.3% | National, primarily Luanda and provincial capitals | Short term (≤ 2 years) |

| Government "ProLub" local-blending incentives | +0.5% | National, targeting Luanda and Cabinda industrial zones | Medium term (2–4 years) |

| Port and rail logistics upgrades reducing supply cost | +0.3% | Lobito Corridor (Benguela), Namibe, with spillover to inland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Mining and Construction Projects

Diamond production reached 14 million carats in 2024, with the Luele mine alone aiming for 9 million carats by 2026. This growth drives the need for fleet renewals of equipment such as drills, haul trucks, and conveyors, which rely on heavy-duty engine oils, greases, and hydraulic fluids. The Tetelo underground copper mine, launched in October 2025, processes 4,000 tons of ore daily, positioning Angola within the electric vehicle (EV) supply chain and increasing demand for gear oils suitable for abrasive and high-temperature conditions. Additionally, large-scale motorway, bridge, and waterfront projects require continuous operation of excavators, cranes, and concrete pumps, raising lubricant consumption per unit of GDP beyond that of automotive-driven economies. OEM confidence is evident in Rokbak’s February 2026 appointment of Trevotech as the national dealer for RA30 and RA40 articulated haulers, combining equipment sales with captive lubricant contracts. As a result, the Angola lubricants market benefits from structural growth linked to capital-equipment replacement cycles in natural-resource extraction industries.

Industrial Power-Generation Expansion

Installed power generation capacity is projected to reach 9.9 GW by 2025. However, grid instability forces factories, hospitals, and telecom towers to rely on captive generators, which consume turbine and industrial engine oils at higher rates compared to grid-powered plants. The Soyo combined-cycle plant, operational in 2025, adds 750 MW of capacity and depends on premium turbine oils with oxidation stability exceeding 5,000 hours. The New Gas Consortium’s Quiluma and Maboqueiro fields are expected to support future petrochemical and process oil demand once gas production begins. Meanwhile, the Laúca hydroelectric dam, with a capacity of 2,070 MW, continues to require hydraulic fluids for gate mechanisms. These developments stabilize industrial output, pushing the Angola lubricants market toward consistent base-load consumption rather than seasonal variations.

Rebound in Vehicle Sales

National vehicle sales, which fell to 3,228 units in the first nine months of 2024, are showing signs of recovery, with 1,453 units sold in Q1 2025. Chinese brands are capturing the affordable segment of the market. Opaia Motors’ assembly plant, inaugurated in January 2026 with an annual capacity of 22,000 units, is expected to stabilize local supply and mitigate foreign exchange volatility[1]World Bank, “Angola Economic Update 2026,” worldbank.org. Each new passenger vehicle requires approximately 4–5 liters of engine oil during its first service, while heavy trucks consume 10–20 liters, amplifying lubricant demand even with modest sales growth. Additionally, commercial vehicle fleets, which operate under high mileage and shorter drain intervals, further contribute to the increasing demand for lubricants in Angola.

Government “ProLub” Local-Blending Incentives

At the March 2026 “Café com a Banca” forum, the oil minister highlighted that only one plant currently produces 17,600 tons per year (tpy) against a national demand exceeding 90,000 tpy. New government incentives aim to reduce import dependency to below 80% by 2029. Etu Energias has initiated construction of a USD 5 million facility with a capacity of 20,000 tpy across seven product lines, demonstrating policy progress. Local blending reduces shipping lead times by up to eight weeks during peak dry-season demand and allows for quicker adjustments to lubricants tailored for Angola’s tropical-savanna climate. These measures are transitioning the Angola lubricants market from heavy import reliance to a hybrid model incorporating local production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price pass-through volatility | -0.5% | National, with acute effects in Luanda and Cabinda | Short term (≤ 2 years) |

| Early-stage EV adoption in Luanda | -0.1% | Luanda metropolitan area, negligible elsewhere | Long term (≥ 4 years) |

| Enforcement of updated lubricant-quality decree raises compliance cost | -0.2% | National, concentrated among smaller blenders and importers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Pass-Through Volatility

Angola's benchmark oil price is expected to decrease from USD 78.5 per barrel in 2024 to USD 66.6 in 2025, with an average of USD 62.2 in 2026. This decline is likely to reduce fiscal revenues that finance infrastructure and mining projects. The 40% depreciation of the kwanza during 2023-2024 has caused new vehicle prices to rise by up to 75%, leading consumers to postpone purchases and extend oil-change intervals. Importers, tied to dollar-denominated supply contracts, are either increasing retail prices or cutting inventory levels, heightening the risk of stock shortages. Industrial demand for lubricants is more flexible; therefore, when capital budgets are reduced, lubricant volumes decrease more sharply than the increase in consumer usage driven by lower fuel costs.

Early-Stage EV Adoption in Luanda

From 2018 to 2023, only about 2,250 electric vehicles (EVs) were registered nationwide, representing less than 1% of the total vehicle fleet. Public charging infrastructure remains limited outside Luanda. Achieving the 2035 target of 1.485 million EVs would require an annual adoption growth rate of 80%, which is challenging given fiscal constraints. Current EV volumes have an insignificant impact on engine oil demand. However, long-term strategies by multinational companies may redirect research and development budgets toward EV-compatible fluids, potentially reducing investments in lubricants for internal combustion engines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automotive Engine Oil Dominates, Industrial Segments Diversify

Automotive engine oil represented 54.15% of the 2025 volume and is expected to grow at 2.41% through 2031, solidifying its role as a key component of the Angola lubricants market. Commercial vehicle fleets operating in mining and construction sectors utilize CK-4-grade diesel oils to endure challenging, high-dust environments, while passenger vehicles primarily use mid-tier mineral and semi-synthetic blends. Industrial engine oil demand remains robust due to the reliance on diesel and gas generators to address grid shortages in areas such as Luanda, Cabinda, and Benguela. Hydraulic fluids, gear oils, and greases are essential for mining and infrastructure projects, with lithium-complex greases preferred for their water-resistant properties. Metalworking fluids have seen increased demand, driven by projects like Algoa Cabinda Fabrication Services' delivery of Chevron’s South N’dola platform in May 2025, marking a resurgence in fabrication activities. Niche segments, including turbine, transformer, and compressor oils, benefit from maintenance cycles at the Soyo gas plant and Laúca dam, offering higher profit margins.

The transmission and gear oils are also expanding as mining fleets upgrade to automatic drivetrains requiring advanced fluids. Brake fluid demand is increasing due to the rising adoption of ABS-equipped vehicles, including low-cost Chinese imports. Specialty heat-transfer and compressor oils support the development of gas-processing infrastructure, while biodegradable hydraulic fluids are gaining popularity among multinational mining companies aiming for ISO 14001 compliance.

By Base Stock Type: Mineral Oils Lead, Bio-Based Formulations Gain Traction

Mineral oil-based lubricants accounted for 67.12% of the 2025 volume, reflecting the market's price sensitivity and the prevalence of older engines compatible with Group I formulations. The Cabinda refinery’s phase-one start-up in September 2025, with a capacity of 30,000 barrels per day, is expected to enhance Group I availability in northern regions, reducing freight costs for Luanda-based blenders. Synthetic oils, priced two to three times higher than mineral oils, are favored by high-uptime fleets aiming to extend drain intervals and minimize downtime. Semi-synthetic oils, offering a balance between cost and performance, are gaining popularity among logistics operators along the Lobito Corridor. Bio-based lubricants are projected to grow at the fastest rate, with a 2.55% CAGR through 2031. Etu Energias’ new plant will produce plant-ester blends that biodegrade by over 60% within 28 days, aligning with diamond mining companies’ ESG commitments and Angola’s 35% emission reduction target under its NDC. However, supply challenges persist due to the lack of domestic oilseed feedstock, though cost advantages improve when bio-based lubricants reduce cleanup expenses in environmentally sensitive areas.

By End-user Industry: Heavy Equipment Outpaces Automotive Despite Smaller Base

The automotive industry commanded 45.12% of the Angola lubricants market share in 2025. About 71% of the 3,228 vehicles sold during the first nine months of 2024 were passenger cars. However, commercial trucks consume significantly more oil, requiring 10-20 liters per oil change for mid-duty rigs and up to 50 liters for mine haul units. Consequently, fleets contribute a larger share of lubricant volume despite lower unit sales. Two-wheelers are gaining popularity in Luanda’s congested urban areas but have a minimal impact on lubricant demand, as each engine typically holds less than a liter of oil per service. Marine lubricant consumption remains stable, with offshore oil production declining from 1.10 million barrels per day (bpd) in 2024 to 1.08 million bpd in 2026, reducing drilling activity and the demand for cylinder, system, and trunk piston oils. Aerospace continues to be a niche segment, primarily serving TAAG and a few charter operators, with limited demand for turbine oil, hydraulic fluid, and grease.

Heavy equipment, including construction, mining, and agriculture, will lift the Angola lubricants market size fastest, advancing at a 2.79% CAGR through 2031 on the back of new mines, highways, and farm mechanization. Projects such as the Luele diamond expansion to 9 million carats in 2026, the Tetelo copper mine’s 300 tons per day concentrate output, and a USD 2.5 billion motorway program keep excavators, crushers, and haul trucks running long shifts that demand frequent changes of hydraulic fluids, gear oils, and heavy-duty diesel engine oils. Agriculture adds incremental growth as the PIDCR scheme deploys trucks, tractors, and harvesters across the Planalto provinces, lifting sales of universal tractor oils and agricultural transmission fluids. Industrial demand is steady rather than spectacular; the Soyo combined-cycle plant supports turbine-oil pull-through while metal-working needs track fabrication jobs, but overall output is capped by declining upstream production and a small manufacturing base.

Geography Analysis

Luanda represents the largest share of national demand, driven by its population of 8 million, over 3,900 service stations, and a high-density vehicle fleet. Cabinda’s offshore operations contribute to moderate lubricant consumption, supported by FPSOs, platform generators, and marine engines, despite its smaller population. Benguela, with Lobito port and the refurbished rail corridor connecting to the DRC-Zambia copper belt, is positioning itself as a logistics hub, increasing heavy-duty engine oil sales to trucking fleets. In Lunda Norte and Lunda Sul, demand is fueled by the Catoca and Luele diamond mines, which operate 24/7 haulage and processing facilities.

Namibe province benefits from iron ore and marble projects, while the Planalto region (Huambo, Bié, Huíla) experiences incremental growth due to agricultural mechanization under the PIDCR truck-distribution scheme[2]UNCTAD, “PIDCR logistics program briefing,” unctad.org. Quality standards enforcement is most stringent in Luanda and Cabinda, favoring established brands, while gray-market products remain prevalent in interior regions with less rigorous inspections. Regional warehousing near mining areas provides distributors with a competitive advantage, addressing challenges such as poor road connectivity and seasonal flooding. The Angola lubricants market requires a multi-node logistics approach to balance coastal demand with inland growth opportunities.

Competitive Landscape

BP, Shell, TotalEnergies, Chevron, and LUBÁFRICA collectively held approximately 75% of 2025 sales through branded networks and corporate contracts. Vivo Energy’s acquisition of PETRONAS’s ENGEN stake in May 2024 created a continent-wide lubricants leader with procurement and marketing efficiencies. Galp’s USD 777 million upstream divestment in 2023 allowed it to focus on defending downstream retail margins through its 49% stake in the Sonangalp joint venture. Local players like Etu Energias and LUBÁFRICA target heavy-equipment and industrial niches by leveraging proximity and offering technical services such as oil analysis and drain-interval optimization, reducing import lead times. Chinese suppliers, including SINOPEC, capitalize on EPC project ties to supply captive fleets, while gray-market traders operate in regions with sporadic enforcement of Executive Decree 31/21 inspections.

Technology is becoming a differentiator, with major players deploying fleet-management platforms and IoT-based oil-condition sensors to secure mining contracts. Sustainability is another key factor, as bio-based and biodegradable products from companies like Etu Energias appeal to multinational corporations with stringent ESG requirements. Market concentration remains moderate but is shifting toward vertical integration, with local blending facilities and branded retail networks gaining prominence, particularly as the Cabinda refinery’s base stock production lowers entry barriers.

Angola Lubricants Industry Leaders

BP p.l.c.

Shell plc

TotalEnergies

LUBÁFRICA

Chevron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Chevron Corporation's South N’dola Platform in Angola delivered its first oil. This development, achieved slightly over two years after construction began, is expected to enhance the availability of base oils, potentially impacting the lubricant market positively.

- November 2025: Etu Energias inaugurated a new service station within the Cuca Factory premises in Luanda, Angola, enhancing its downstream network. The station featured six fuel-filling points, domestic gas supply, solar-powered systems for sustainability, an on-site shop, and facilities for electric vehicle charging and tire calibration.

Angola Lubricants Market Report Scope

Lubricants are substances made from a combination of base oils and additives. These lubricants are used in various automotive applications such as engines, brakes, gears, and other parts. The base oil composition in the formulation of lubricants is primarily between 75-90%. Lubricants are used to reduce friction between surfaces in contact to minimize energy loss generated from friction.

The Angola lubricants market is segmented by product type, base stock type, and end-user industry. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, industrial, and other end-user industries. The automotive segment is further segmented into passenger vehicles, commercial vehicles, and two-wheelers. The heavy equipment segment is further segmented into construction, mining, and agriculture. The industrial segment is further segmented into power generation, metallurgy and metalworking, textiles, and oil and gas. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-user Industries |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the volume of the Angola lubricant market?

The Angola lubricant market stands at 42.51 million liters in 2026 and is forecast to reach 47.21 million liters by 2031.

Which product type dominated volume in 2025?

Automotive engine oil commanded 54.15% of the 2025 volume.

How fast are bio-based lubricants growing through 2031?

Bio-based formulations are on track for a 2.55% CAGR through 2031, the quickest among base stock types.

Which provinces are emerging growth hotspots?

Benguela, Lunda Norte, and Lunda Sul are expanding fastest thanks to the Lobito Corridor logistics upgrade and a mining boom.

Page last updated on: