Ethiopia Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

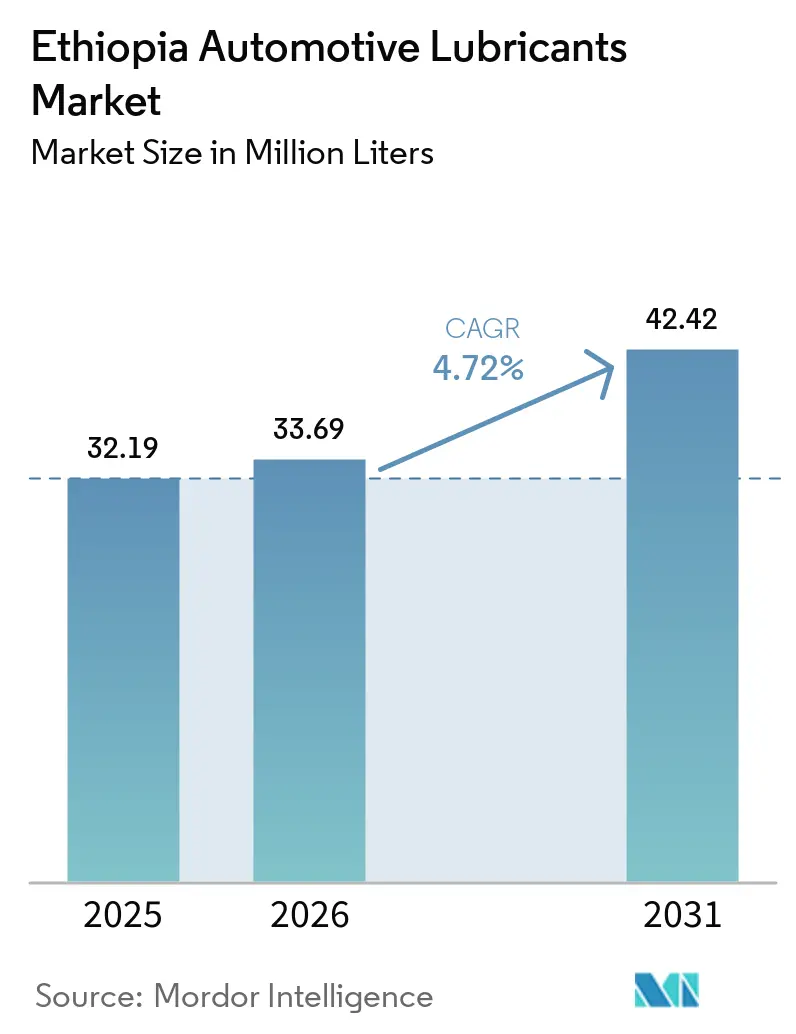

| Base Year Market Size (2025) | 32.19 Million liters |

| Market Volume (2026) | 33.69 Million liters |

| Market Volume (2031) | 42.42 Million liters |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

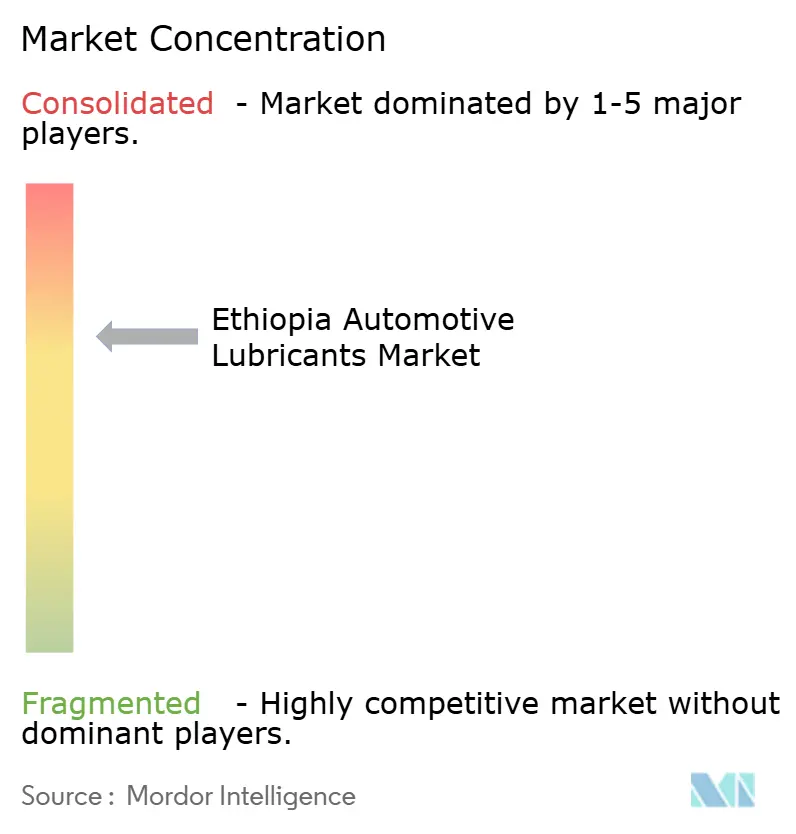

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethiopia Automotive Lubricants Market Analysis by Mordor Intelligence

The Ethiopia Automotive Lubricants Market size is expected to grow from 32.19 million liters in 2025 to 33.69 million liters in 2026 and is forecast to reach 42.42 million liters by 2031 at 4.72% CAGR over 2026-2031. Despite government efforts to hasten the shift to electric mobility by tightening bans on internal-combustion engine imports, demand remains robust. This resilience is largely attributed to an aging vehicle fleet, comprising predominantly older gasoline and diesel models. Infrastructure developments, like the Modjo–Hawassa Expressway and the Addis–Djibouti route, are boosting commercial freight activity. This uptick is subsequently driving up the consumption of heavy-duty diesel engine oils and extreme-pressure gear lubricants. National Oil Ethiopia boasts an extensive network of stations, and with TotalEnergies offering its oil-monitoring service, the industry sees heightened switching costs. This dynamic moderates competitive intensity, even in the face of counterfeit risks. While a scarcity of foreign exchange limits the influx of new vehicles, the "Let Ethiopia Produce" campaign is pushing industrial capacity utilization upward, benefiting local blending investments.

Key Report Takeaways

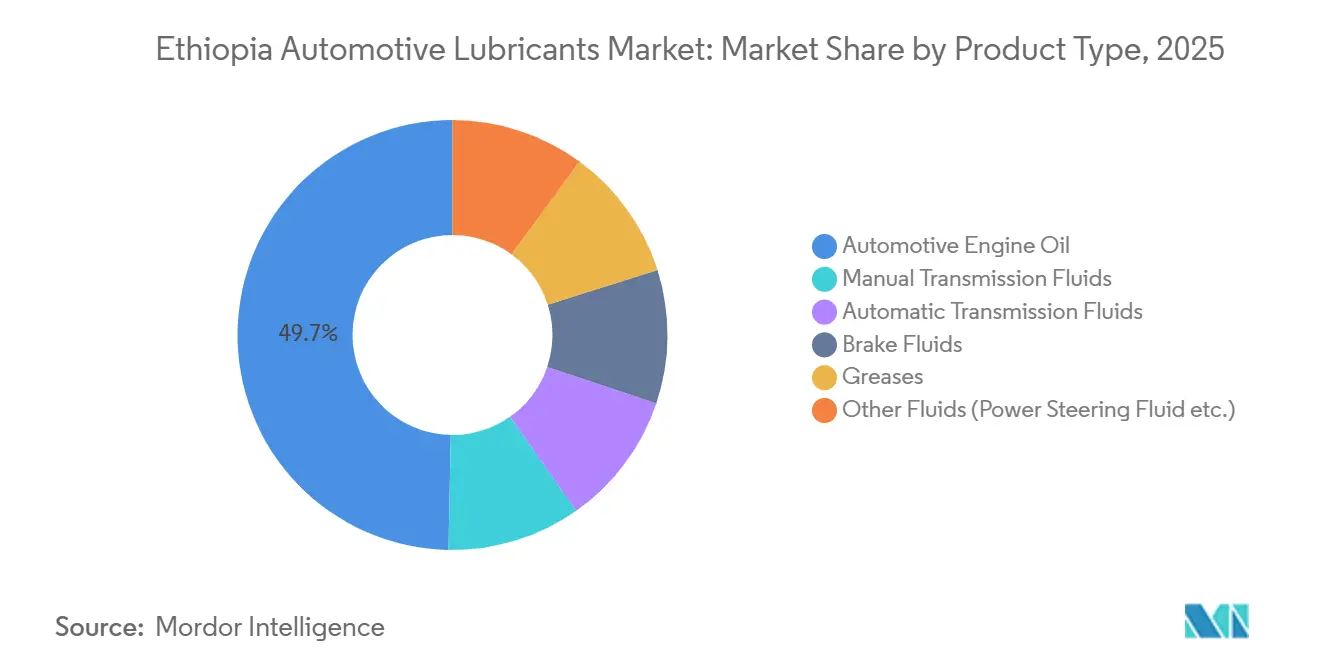

- Automotive engine oil commanded 49.71% of the Ethiopia automotive lubricants market share in 2025, while automatic transmission fluids are projected to expand at a 4.96% CAGR between 2026 and 2031.

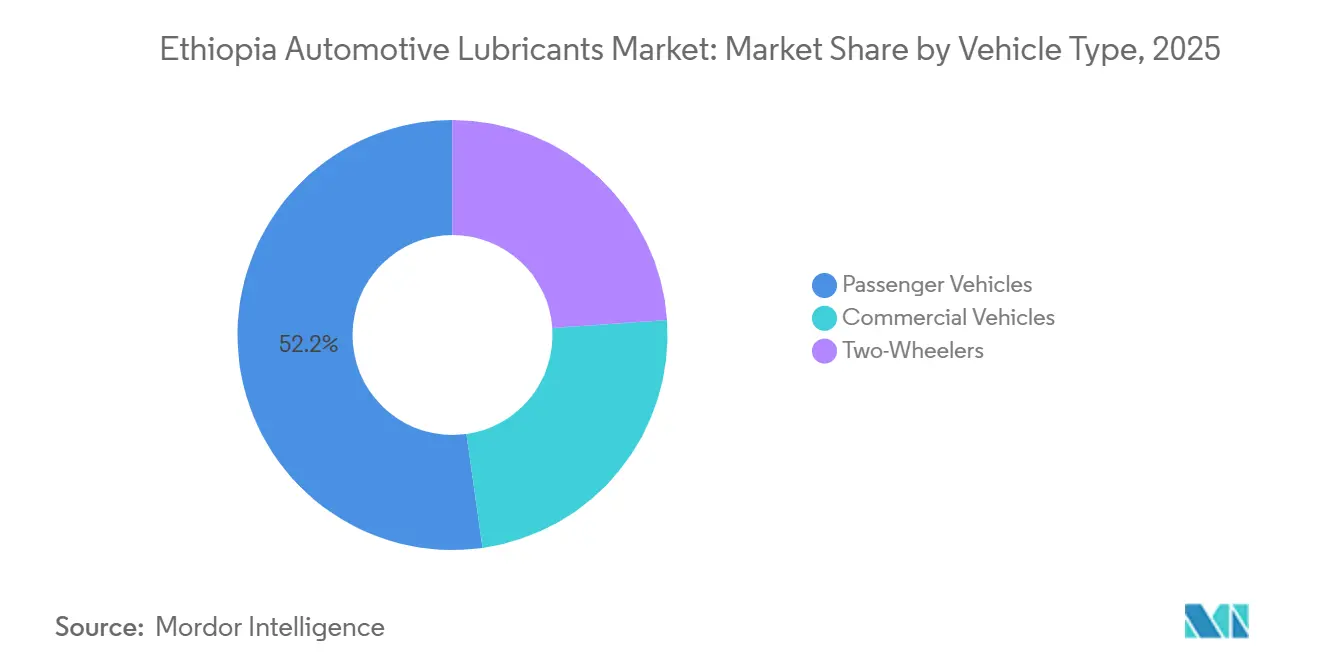

- Passenger vehicles accounted for 52.22% of volume in 2025, but commercial vehicles lead future growth with a 5.04% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ethiopia Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High average vehicle age and dominance of used imports | +1.20% | Addis Ababa and Oromia | Medium term (2-4 years) |

| Rapid expansion of infrastructure projects | +1.00% | National trunk corridors | Short term (≤ 2 years) |

| Growth in commercial vehicle fleet | +0.90% | Cross-border routes | Medium term (2-4 years) |

| Government-led industrialization push | +0.70% | National industrial parks | Long term (≥ 4 years) |

| Rising adoption of ride-hailing and two-wheelers | +0.50% | Major urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Average Vehicle Age And Dominance Of Used Imports Sustain Conventional Lubricant Demand

In Ethiopia, the majority of registered vehicles are second-hand, with many surpassing a decade in service. Older models from Toyota, Hyundai, and Isuzu, typically using American Petroleum Institute Service Level and Commercial Fleet 10W-30 and 15W-40 grades, necessitate more frequent oil changes. This trend shields the Ethiopian automotive lubricants market from an immediate shift towards electric vehicles. China's upcoming ban on "zero-mileage" exports is steering buyers towards even older imports, prolonging the lifespan of the fleet. National Oil Ethiopia is capitalizing on this trend, employing a nationwide used-oil analysis program to secure fleet contracts. Meanwhile, TotalEnergies is offering warranty-compliant fluids through diagnostics. This established maintenance routine ensures a steady demand for mineral and semi-synthetic engine oils, projected to continue through the forecast period.

Rapid Expansion of Infrastructure Projects Drives Commercial Lubricant Consumption

The nearing completion of a major expressway is set to significantly reduce freight transit times. This development is expected to increase truck mileage and, consequently, the turnover of heavy-duty diesel engine oil[1]World Bank Documents, “Horn of Africa Initiative Corridor Project,” worldbank.org. Concurrently, upgrades along the Addis–Djibouti corridor aim for improved road quality. While better road surfaces extend synthetic-oil drain intervals, they simultaneously boost overall demand due to rising freight volumes. With fuel-tanker fleets from National Oil Ethiopia, TotalEnergies, and Oil Libya comprising a substantial number of units, there is a robust institutional demand for gear oils and greases.

Growth In Commercial Vehicle Fleet Underpins Heavy-Duty Segment

As construction accelerates around the Grand Ethiopian Renaissance Dam and the local assembly of a dump-truck line gains momentum, commercial vehicle registrations are set to grow steadily during the forecast period. Diesel engines, requiring high-performance oils and transmission fluids, are driving a surge in demand for advanced additives. Furthermore, early export orders to Tanzania are positioning Ethiopia as a regional servicing hub, amplifying the demand for aftermarket lubricants.

Rising Adoption Of Ride-Hailing And Two-Wheelers Boosts Urban Turnover

In Addis Ababa, several app-based platforms are racking up significant daily mileage, leading to shortened oil drain intervals. Meanwhile, motorcycle delivery services, now legally operating under temporary permits, are expanding their reach to Hawassa and Bahir Dar, utilizing four-stroke oils. Dominating the informal transport sector, Bajaj Auto's three-wheelers c gear lubricants, driving steady sales of smaller packs through service stations[2]Bajaj Auto, “Bikes & 3-Wheelers Ethiopia,” bajajauto.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Forex controls restricting imports | -0.80% | National, acute at Port of Djibouti and dry ports (Modjo, Addis Ababa) | Short term (≤ 2 years) |

| Counterfeit and low-quality lubricants | -0.60% | National, concentrated in informal retail and unlicensed distributors | Medium term (2-4 years) |

| Limited synthetic availability | -0.50% | National, with acute gaps in commercial fleet and industrial segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Forex Controls Restricting Imports Constrain Supply And Elevate Costs

As foreign-exchange allocations tightened, vehicle-import spending experienced a significant decline over time. This sharp reduction directly curtailed fresh fleet additions and dampened derivative lubricant demand. Port handling at Djibouti is considerably more expensive compared to Mombasa, further inflating lubricant prices. Despite Ethiopia's legalizing private multimodal operators, their sparse entry has stifled competitive relief. While the Gode refinery promises a long-term solution, it does little to alleviate immediate shortages.

Counterfeit and low-quality lubricants erode brand trust and margins

Unlicensed dealers circulate illicitly repackaged and recycled oils, damaging engines and undermining authorized distributors. While Ethiopia’s adoption of the standard for viscosity grades sets benchmarks, it falls short on enforceable quality tests, creating significant loopholes. In response, National Oil Ethiopia implements laboratory testing and warranty programs, and TotalEnergies utilizes diagnostics to validate authenticity. Yet, until regulatory gaps are bridged, profit margins remain under pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automatic Transmission Fluids Outpace, Engine Oils Retain Scale

Automotive engine oil accounted for 49.71% of the Ethiopia automotive lubricants market share in 2025, reflecting the sizeable legacy parc requiring frequent changes. The Ethiopia automotive lubricants market size for automatic transmission fluids is projected to expand at a 4.96% CAGR between 2026-2031 As taxi fleets and newly assembled Shacman trucks adopt powershift gearboxes, demand for automatic transmission fluid is centered on specific formulations like DEXRON III and CAT TO-4. In response, National Oil Ethiopia is expanding its Texamatic portfolio. While greases and brake fluids have traditionally been niche, they are gaining significance. This shift is largely due to industrial parks installing high-speed equipment, which necessitates the use of calcium-sulfonate thickened greases known for their superior water resistance. Looking ahead, the anticipated surge in battery-electric vehicles is set to reduce the demand for engine oils. However, it will simultaneously spark a budding need for axle greases designed for electric vehicles and dielectric coolants. Notably, TotalEnergies and FUCHS are already ahead, boasting active research and development pipelines in these domains.

Viscosity emerges as a key differentiator in the market. While the crisp mornings of Addis favor multi-grade oils for passenger vehicles, the agricultural and quarrying sectors in the lowlands continue to rely on mineral blends. Suppliers of fully synthetic oils designed for advanced engine performance are witnessing a sluggish uptake, a trend expected to shift once newer Japanese hybrids gain traction. On the other hand, operators in the heavy-duty diesel segment are leaning towards synthetic-blend oils, prized for their extended drain intervals. This presents a lucrative opportunity for GP Lubricants Ethiopia, especially with their formulations approved by original equipment manufacturers. Given the ongoing threat of counterfeits, certified supply and guidance on drain intervals have emerged as crucial value propositions in Ethiopia's automotive lubricants landscape.

By Vehicle Type: Commercial Vehicles Deliver The Fastest Growth Curve

Passenger cars, taxis, and SUVs delivered 52.22% of volume in 2025, thanks to Addis Ababa holding half the national fleet. Nonetheless, the Ethiopia automotive lubricants market size for commercial vehicles is forecast to climb 5.04% per year through 2026 to 2031. Completion of the Modjo Hawassa Expressway and the Horn of Africa corridor has led to increased payload cycles for the cross-border truck fleet. These trucks, often heavily loaded, have consequently heightened the consumption of gear oils with high viscosity and performance standards. Meanwhile, with buses set for conversion to either liquefied natural gas or battery power, there's a noticeable shift in lubricant preferences towards long-life synthetic driveline fluids.

While two-wheelers and three-wheelers represent a smaller segment, they demonstrate a notable uptick in ride-hailing mileage. A typical motorcycle consumes engine oil at regular intervals, while tuk-tuks require gear oil after covering specific distances. This consistent consumption pattern ensures a steady demand for various oil pack sizes, primarily distributed through service stations. Looking ahead, anticipated regulatory relaxations on motorcycle passenger services are poised to further boost oil sales in urban areas.

Geography Analysis

In Ethiopia's automotive lubricants market, Addis Ababa takes the lead, accounting for the majority of registered vehicles and boasting the highest density of service stations. The city's ride-hailing fleets, logging significant daily mileage, drive a robust demand for multi-grade engine oils and automatic transmission fluids. Following Addis Ababa is Oromia, with a substantial share of the vehicle fleet, bolstered by agricultural mechanization and the Adama industrial park. National Oil Ethiopia, with numerous outlets stretching across regions, ensures a wide retail presence, and its logistics base in Djibouti effectively addresses port dwell-time challenges.

Emerging as secondary hubs, Hawassa, home to a flagship industrial park employing a large workforce, sees a rising demand for hydraulic and gear oils. Dire Dawa, benefiting from corridor enhancements towards Djibouti, positions itself as a lubricant transit point for cross-border trucking. Meanwhile, Bahir Dar and Gondar, witnessing an uptick in two-wheeler fleets, see ride-hailing operators expanding their reach, thus broadening sales beyond the capital.

As regional integration deepens, the interplay of supply becomes evident. TotalEnergies’ plant in Mombasa and FUCHS’ expanded facility in Johannesburg both send semi-synthetic blends northward, ensuring supply stability amidst Ethiopia’s foreign exchange constraints. Adding to the landscape, the groundbreaking of a large-scale refinery in Gode hints at a future of local base-oil production. Once operational, this domestic blending capability could significantly reduce import duties on landed costs, potentially transforming the pricing dynamics in Ethiopia's automotive lubricants arena.

Competitive Landscape

The Ethiopia Automotive Lubricants Market is moderately concentrated. Future contest will focus on technical services and synthetic portfolios. ExxonMobil entered aviation lubricants via a five-year Ethiopian Airlines deal, showcasing a template to lock in long-term supply with stringent testing regimes. GP Lubricants Ethiopia courts fleet operators with ISO-certified, OEM-approved synthetics at competitive price points, targeting buyers wary of counterfeit risks. The arrival of electric buses and trucks will reward players that already market e-axle greases and dielectric fluids, opening a technology edge over commodity blenders.

Ethiopia Automotive Lubricants Industry Leaders

TotalEnergies

Shell plc

NOC Ethiopia PLC

Oil Libya Ethiopia

Puma Energy SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ethiopia began construction on the Gode refinery, boasting a capacity of 3.5 million tons. This initiative seeks to curtail the nation's dependency on imported fuels and base oils, potentially bolstering local base oil production – a vital ingredient in automotive lubricants.

- January 2026: Ethiopian Airlines, with the help of Aeroservices, signed a five-year deal with ExxonMobil for aviation lubricants. This move is set to boost demand for premium aviation-grade lubricants in Ethiopia, spurring technological advancements in the lubricant sector.

Ethiopia Automotive Lubricants Market Report Scope

Ethiopia Automotive Lubricants are specialized fluids designed to reduce friction, protect components, and enhance performance in vehicles operating across Ethiopia’s varied terrain and climate. They include engine oils, transmission fluids, brake fluids, greases, and other lubricants essential for passenger cars, commercial vehicles, and two-wheelers. This market supports Ethiopia’s growing automotive sector by ensuring the durability, efficiency, and reliability of engines and mechanical systems.

The Ethiopia Automotive Lubricants Market is segmented by product type and vehicle type. By product type, the market is segmented into automotive engine oil (0W-XX, 5W-XX, 10W-XX, 15W-XX, monogrades, and other grades), manual transmission fluids (MTF), automatic transmission fluids (ATF), brake fluids, automotive greases, and other product types such as power steering fluids. By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. For each segment, the market sizing and growth forecasts have been done on the basis of volume (liters).

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids | |

| Automatic Transmission Fluids | |

| Brake Fluids | |

| Greases | |

| Other Fluids (Power Steering Fluid etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids | ||

| Automatic Transmission Fluids | ||

| Brake Fluids | ||

| Greases | ||

| Other Fluids (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

What is the current volume of the Ethiopia automotive lubricants market?

The Ethiopia Automotive Lubricants Market size is expected to grow from 32.19 million liters in 2025 to 33.69 million liters in 2026 and is forecast to reach 42.42 million liters by 2031 at 4.72% CAGR over 2026-2031.

How fast is demand for automatic transmission fluid growing?

ATF volumes are projected to rise at a 4.96% CAGR between 2026-2031, the fastest among product types.

Which company leads Ethiopia’s lubricants space?

National Oil Ethiopia lead Ethiopia automotive lubricants market share in 2025, ahead of TotalEnergies.

Why is commercial-vehicle lubricant demand accelerating?

Road-corridor expansions and local truck assembly are lifting truck kilometers traveled, driving a 5.04% CAGR for commercial-vehicle lubricants.

How will the Gode refinery impact domestic lubricants?

Once operational, the refinery could supply local base oils, cutting import costs and encouraging wider in-country blending capacity.

Page last updated on: