General Anesthesia Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

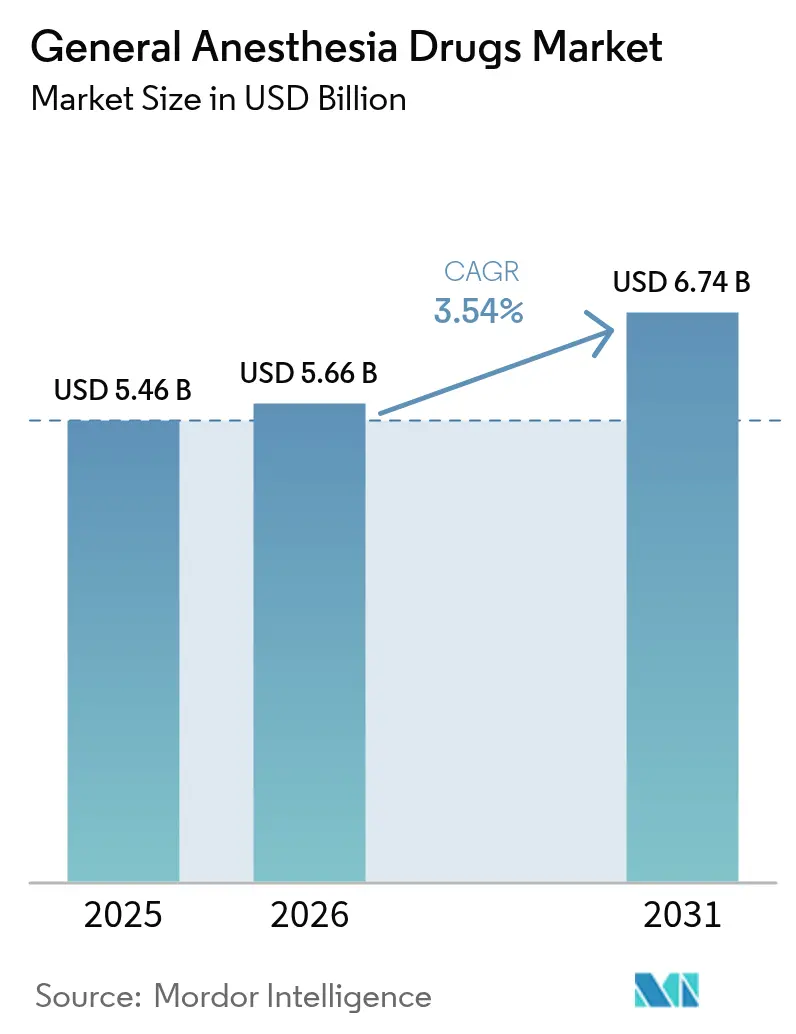

| Market Size (2026) | USD 5.66 Billion |

| Market Size (2031) | USD 6.74 Billion |

| Growth Rate (2026 - 2031) | 3.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

General Anesthesia Drugs Market Analysis by Mordor Intelligence

The General Anesthesia Drugs Market size was valued at USD 5.46 billion in 2025 and is estimated to grow from USD 5.66 billion in 2026 to reach USD 6.74 billion by 2031, at a CAGR of 3.54% during the forecast period (2026-2031).

Growth stems from higher surgical throughput, oncology-driven complexity, and substitution toward eco-friendly or rapid-offset molecules. However, off-patent price erosion and tighter formulary budgets temper absolute value gains. Hospitals continue to anchor demand, but ambulatory surgical centers (ASCs) are capturing incremental volume as payers migrate low-acuity cases to outpatient settings stocked with short-acting intravenous agents. Technology is reshaping the competitive landscape: AI-enabled closed-loop pumps trim drug waste by up to 22%, while low global warming potential (GWP) inhalational formulations position suppliers for looming European environmental levies. Margin pressure from biosimilar propofol and group-purchasing rebates is pushing incumbents into vertical integration around lipid feedstocks and co-development of innovative workstations. White-space opportunities cluster around pediatric-friendly excipient profiles, abuse-deterrent ketamine systems, and inhalational agents compliant with F-gas phase-downs yet equivalent in minimum alveolar concentration potency.

Key Report Takeaways

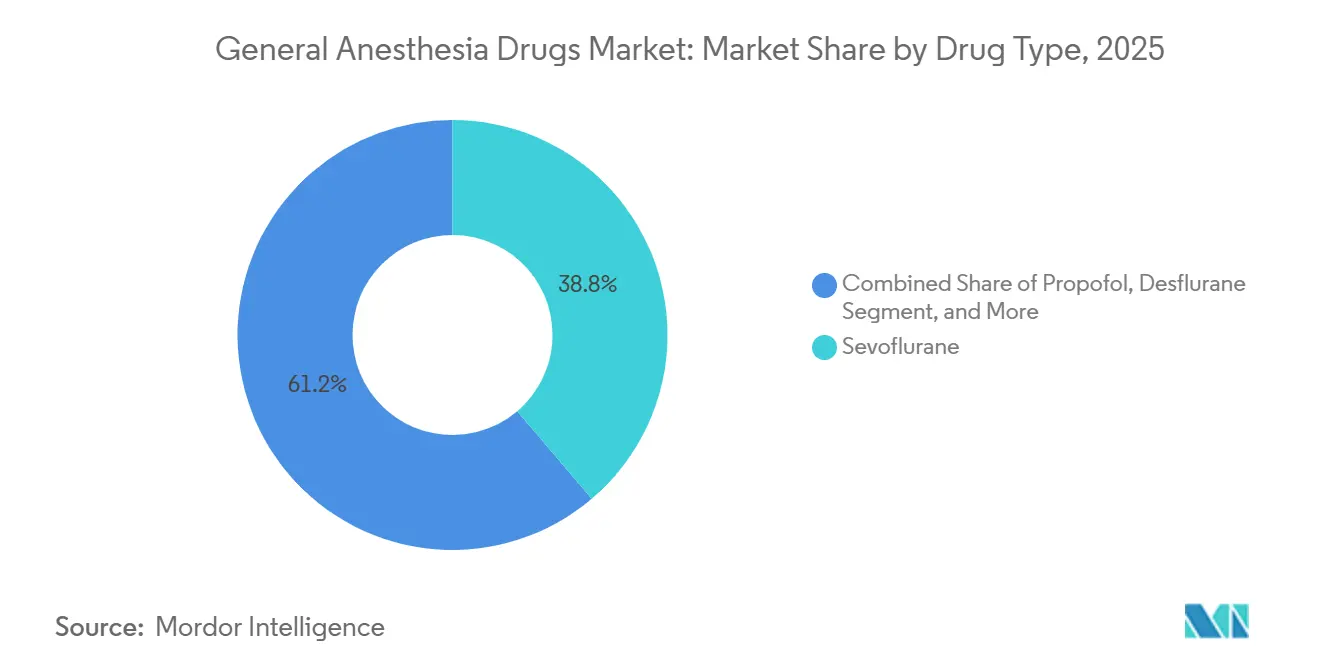

- By drug type, sevoflurane led the general anesthesia drugs market with a 38.78% share in 2025, whereas propofol is forecast to expand at a 4.98% CAGR through 2031.

- By route of administration, inhalational delivery accounted for 61.20% of the general anesthesia drugs market in 2025; however, intravenous formats are projected to grow at a 5.88% CAGR between 2026 and 2031.

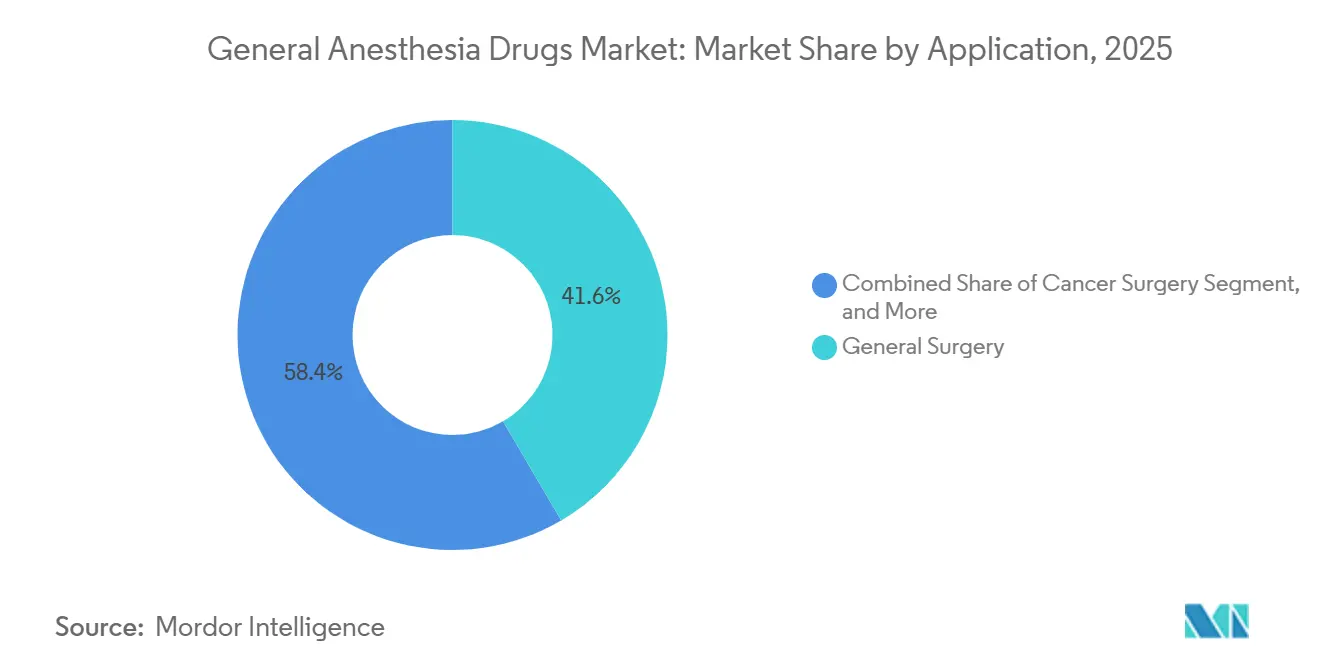

- By application, general surgery accounted for 41.56% of revenue in 2025, while cancer-related procedures are projected to grow at a 4.89% CAGR through 2031.

- By end user, hospitals accounted for 62.95% of spending in 2025; ASCs are projected to post a 6.38% CAGR through 2031.

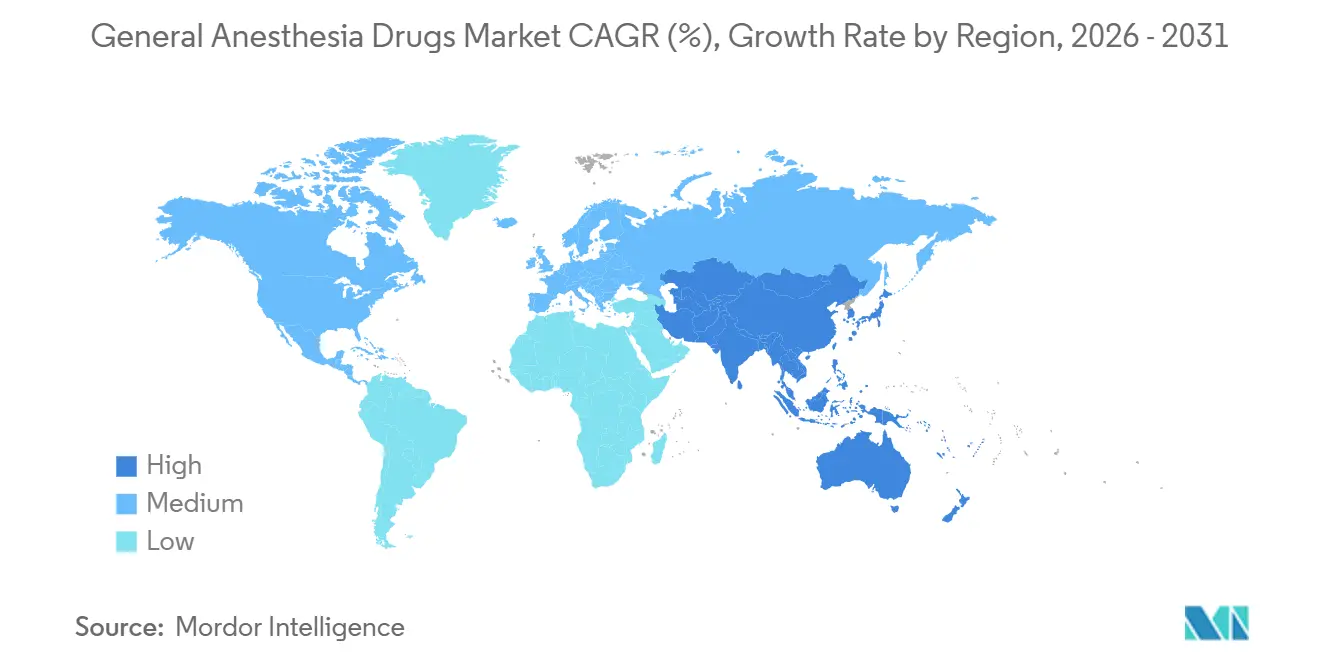

- North America accounted for 38.50% of 2025 revenue, yet Asia-Pacific is on track for a 5.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global General Anesthesia Drugs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising global surgical volumes | +1.2% | Global, Asia-Pacific and Middle East dominate gains | Medium term (2-4 years) |

| Product approvals & launches surge | +0.8% | North America & Europe (novel); Asia-Pacific (generics) | Short term (≤2 years) |

| Growing ambulatory surgical center adoption | +0.9% | North America core; spillover to Western Europe & urban APAC | Medium term (2-4 years) |

| AI-driven closed-loop infusion uptake | +0.5% | North America and select European academic centers | Long term (≥4 years) |

| Shift to eco-friendly low-GWP inhalational agents | +0.3% | Europe (UK, Germany, Nordics); emerging in Canada & Australia | Medium term (2-4 years) |

| Increase in essential procedure volumes | +0.9% | Low- and middle-income regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Surgical Volumes

Worldwide surgical cases surpassed 400 million in 2025, up 4.2% year on year, driven by aging populations, expanded insurance coverage, and clearance of pandemic backlogs.[1]U.S. FDA, “DailyMed Label: Suzetrigine,” dailymed.nlm.nih.gov High-income countries are layering complex, long-duration interventions, boosting demand for multi-agent anesthesia, while emerging markets are scaling essential surgeries that favor single-agent ketamine or generic propofol. China’s Healthy China 2030 plan set aside USD 12 billion to fund 300 tertiary hospitals by 2026, each with 8-12 operating rooms, guaranteeing baseline bulk contracts for sevoflurane and propofol. In India, Ayushman Bharat added 50 million surgical beneficiaries in 2025, though an INR 15,000 (USD 180) cap per case pushes facilities to source domestic generics. WHO emergency care guidelines require district hospitals to maintain minimum anesthesia stockpiles to shield demand during downturns.

Product Approvals & Launches Surge

Accelerated clearance of ciprofol and remimazolam has widened the therapeutic toolkit for anesthesiologists, reducing injection-site pain from 77.1% to 18.0% and providing superior cardiovascular stability in elderly patients. The United States Food and Drug Administration’s 2025 nod for JOURNAVX (suzetrigine) underscores a wider pivot toward non-opioid peri-operative analgesia that complements general anesthesia protocols.[2]U.S. Food and Drug Administration, “Drugs@FDA Database,” fda.gov

Amneal’s 2024 launch of single-dose propofol vials aimed at easing recurrent shortages is projected to generate USD 314 million in annual revenue.[3]CNBC Editors, “Mallinckrodt-Endo Merger Details,” cnbc.com Collectively, these approvals expand the number of viable intravenous options, intensify competition, and raise the innovation bar throughout the general anesthesia drugs market.

Growing Ambulatory Surgical Center Uptake

United States ASC expenditure reached USD 6.1 billion for 3.3 million Medicare fee-for-service beneficiaries in 2022, and the segment’s revenue base is poised to advance from USD 37 billion in 2021 to USD 59 billion by 2028. The CMS-backed NOPAIN Act will grant distinct reimbursement for non-opioid analgesics such as EXPAREL from January 2025, sharpening the economic case for fast-recovery anesthesia protocols in outpatient settings. Growing ASC footprints are therefore heightening demand for rapid-onset drugs like ciprofol, driving measurable incremental volumes across the general anesthesia drugs market. ASCs logged 28.3 million U.S. procedures in 2025, 7.1% more than 2024, buoyed by Medicare’s ASC-approved list expansion to knee arthroplasty and lumbar decompressions. Propofol-driven total intravenous anesthesia (TIVA) dominates these sites because rapid emergence trims post-anesthesia care unit (PACU) bottlenecks.

AI-Driven Closed-Loop Infusion Adoption

Closed-loop platforms that modulate propofol and remifentanil infusions using real-time EEG and hemodynamic feedback have delivered 15-20% gains in intraoperative stability compared with manual dosing.[4]National Health Service, “Greener NHS Desflurane Phase-Down,” england.nhs.uk Early adopters are reporting marginally higher drug consumption per case but reduced postoperative complications, creating a net positive economic effect for hospitals. Broader roll-outs are expected to reinforce demand elasticity in the general anesthesia drugs market. GE HealthCare’s Aisys CS² workstation adjusts propofol, remifentanil, and sevoflurane dosing every 10 seconds, lowering consumption by 18–22%. The FDA classifies these platforms as Class II devices requiring 510(k) clearance, whereas the EU Medical Device Regulation requires non-inferiority trials, which elongate timelines for startups.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Side-effect profile & PONV concerns | -0.6% | Global, acute in outpatient same-day settings | Short term (≤2 years) |

| Reimbursement pressure on premium agents | -0.7% | North America and Western Europe | Medium term (2-4 years) |

| Volatile API-lipid supply chain for IV emulsions | -0.4% | Global, notable shortages in 2023-2024 | Short term (≤2 years) |

| Environmental levies on higher-GWP gases | -0.3% | Europe (UK, Germany); pilot programs in Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Side-Effect Profile & PONV Concerns

PONV affects 25–30% of volatile-agent cases versus 10–15% under propofol TIVA, adding USD 50–100 per patient in antiemetics and lengthening PACU stay 15–25 minutes. Automated Apfel scoring embedded in 40% of U.S. electronic records flags high-risk patients for TIVA and prophylaxis. A 2024 meta-analysis of 87 trials showed propofol TIVA cuts PONV by 19 percentage points relative to sevoflurane; however, propofol’s USD 8–12 acquisition cost per case versus USD 4–6 for sevoflurane restrains complete migration in cost-conscious systems.[5]Ashish Sinha et al., “Artificial-Intelligence-Based Closed-Loop Anesthesia,” Springer Nature, springer.com Joint Commission quality audits further spotlight PONV, nudging departments toward lower-emetogenic regimens.

Reimbursement Pressure on Premium Agents

Reimbursement pressure on anesthesia providers, specifically commercial and Medicare rate declines, and increased claim denials, creates significant financial strain, particularly for independent practices and in rural areas. To cope, providers face pressure to improve efficiency, which can lead to longer work hours and reduced staffing levels to manage overhead costs, often resulting in increased burnout.

This pressure directly affects general anesthesia by shifting focus from individualized care to speed-oriented, high-throughput models. To cut costs, some payers are limiting compensation to "scheduled" rather than actual, necessary operative time, potentially pressuring anesthesiologists to expedite cases. This can compromise patient safety by increasing risks related to premature reversal of anesthetics, inadequate pre-operative assessment, and less personalized intraoperative management, as providers work under the constraint of lower compensation for complex, time-intensive cases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Propofol’s TIVA Tailwind Outpaces Sevoflurane’s Installed Base

Sevoflurane retained 38.78% of 2025 revenue, reflecting entrenched vaporizer infrastructure and familiarity with pediatric mask induction. Yet the global tilt toward TIVA positions propofol to register a 4.98% CAGR through 2031. The general anesthesia drugs market size for propofol-based formulations is set to expand further as ciprofol demonstrates non-inferiority while slashing injection-site pain rates. Desflurane’s trajectory remains negative because of impending European environmental bans, whereas dexmedetomidine and remifentanil maintain specialized, procedure-specific niches. Regulatory withdrawals affecting dexmedetomidine in 2024 temporarily tightened supply but did not materially alter long-term demand. Midazolam’s stricter scheduling in China is pushing providers toward remimazolam, which offers rapid recovery without the same regulatory burden. Ketamine and etomidate continue to occupy stable, smaller segments, with etomidate indispensable for hemodynamically unstable cases despite periodic shortages.

Underlying drivers include tighter environmental regulations, heightened interest in the immunomodulatory benefits of intravenous agents, and the operational efficiency of AI-driven infusion pumps. Collectively, these trends cement the intravenous pivot and reinforce propofol’s leadership role within the evolving general anesthesia drugs market.

By Route of Administration: Intravenous Gains as Hospitals Automate and Decarbonize

Inhalational administration accounted for 61.20% of 2025 consumption, yet intravenous delivery is projected to grow at a 5.88% CAGR through 2031, the fastest across any segment. Environmental imperatives to slash volatile emissions, combined with PACU throughput needs, steer anesthesiologists toward propofol and remifentanil TIVA. Smart infusion pumps reduce drug overrun, saving USD 30–50 per case and trimming pharmacy budgets under capitated contracts. The general anesthesia drugs market size for intravenous formulations is forecast to reach USD 3.25 billion by 2031, up from USD 2.35 billion in 2025.

However, TIVA diffusion hinges on BIS or entropy monitors, continuous IV access, and staff skill; in low-resource geographies, it still relies on low-flow sevoflurane. European F-gas laws exempt intravenous agents from atmospheric reporting, a regulatory nudge for hospitals to invest in target-controlled pumps rather than next-gen vaporizers.

By Application: Cancer Resections Drive Anesthetic Complexity and Agent Mix

General surgery captured 41.56% of 2025 revenue, but oncology-related procedures will pace growth at a 4.89% CAGR to 2031. Rising cancer detection through screening and robot-assisted resections lengthens case duration beyond 4 hours, requiring multi-agent regimens for hemodynamic fine-tuning. The general anesthesia drugs market share attributed to cancer surgery is expected to increase to 18.2% in 2031 from 15.4% in 2025. Robotic systems create demand for dexmedetomidine sedation during docking and propofol maintenance for rapid post-op neuro checks.

Orthopedic replacements are pivoting to ASCs, capitalizing on remimazolam’s ultra-fast emergence and regional blocks to minimize opioid reliance. Neurosurgical suites prefer propofol to limit cerebral metabolic demand, while trauma theaters keep ketamine on hand for hypovolemic shock. Cesarean sections and obstetric emergencies still lean on rapid-induction agents safe for fetal transfer.

By End-User: Ambulatory Centers Outpace Hospitals as Payers Shift Volume

Hospitals accounted for 62.95% of 2025 consumption, reflecting cardiac, neuro, and multi-trauma caseloads. Yet ASCs will chalk up a 6.38% CAGR through 2031 as Medicare DRGs and private payers channel elective volumes to lower-cost outpatient hubs. The general anesthesia drugs market size for ASCs is projected to grow from USD 1.63 billion in 2025 to USD 2.35 billion by 2031. Propofol TIVA dominance in these centers underpins demand for prefilled syringes and closed-loop pumps calibrated for short, repetitive cases.

Dental and specialty clinics remain sub-5% of spend, chiefly using midazolam and low-dose propofol for conscious sedation. Regulatory accreditation, such as Joint Commission ambulatory standards, mandates depth-of-sedation monitoring, nudging smaller practices toward predictable pharmacokinetic agents and away from variable-uptake inhalational gases.

Geography Analysis

North America accounted for 38.50% of the general anesthesia drugs market revenue in 2025, reflecting advanced surgical infrastructure, early adoption of AI-driven delivery systems, and supportive reimbursement policies. North America accounted for 38.50% of 2025 revenue, led by 6,100 Medicare-certified ASCs and early uptake of remimazolam post-2020 FDA approval. Per-capita procedure density stands at 220 procedures per 1,000 residents annually, surpassing that of any other region. The U.S. shift to bundled payments pressures branded price points, encouraging the adoption of generic propofol, while lift-and-shift adoption of closed-loop pumps sustains volume. Canada’s single-payer system limits uptake of premium agents but fast-tracks low-GWP transitions, with provincial formularies phasing out desflurane ahead of Europe’s 2030 target.

Asia-Pacific is the fastest-growing geography, with a 5.22% CAGR through 2031, driven by rising surgical volumes, government incentives to upgrade operating theatres, and national policies to reduce volatile-agent emissions. China’s Category I scheduling of midazolam is already steering clinicians toward remimazolam, while India’s phased GMP compliance program seeks to raise manufacturing quality without choking supply.

Europe faces both opportunities and constraints as sustainability agendas phase out desflurane; the United Kingdom’s National Health Service completed full withdrawal in 2024, and the wider European Union is weighing region-wide bans by 2026. German and Scandinavian hospitals lead trials of volatile capture systems but admit that sub-100% efficiencies will leave TIVA as the primary compliance pathway. European suppliers such as Fresenius are responding with expanded injectable lines, evidenced by Q1 2025 revenue growth of 7% despite stringent regulatory landscapes.

Competitive Landscape

The general anesthesia drugs industry exhibits moderate concentration: multinationals such as Baxter, Fresenius, and Pfizer dominate core inhalational and intravenous portfolios, yet emerging firms target niche opportunities with specialized injectables. Baxter’s USD 3.8 billion kidney care spin-off refocuses the company on anesthesia and injectables, underlining an industry-wide shift toward higher-margin specialty arenas. Amneal leveraged rapid FDA clearance to supply propofol during shortage periods, proving that agile manufacturing can unlock material share gains. Meanwhile, merger moves like Mallinckrodt’s USD 7 billion tie-up with Endo seek economies of scale in sterile injectables, though antitrust offices remain vigilant.

Baxter’s Carestation 850, unveiled in October 2025, extends from neonates to geriatrics with precision vapor control, supporting ultra-low-flow sevoflurane. AbbVie leverages Diprivan brand equity to market extended-stability vials, banking on lower microbial-growth risk as a hospital labor offset.

General Anesthesia Drugs Industry Leaders

AbbVie Inc.

Baxter International Inc.

Fresenius SE & Co. KGaA

Aspen Pharmacare Holdings Ltd.

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Meitheal Pharmaceuticals launched propofol sedation vials in three single-dose sizes, targeting waste reduction and dosing error minimization in ICU and surgical applications.

- April 2025: Avenacy introduced Propofol Injectable Emulsion, USP to the United States, a Diprivan-equivalent for induction and maintenance in patients ≥3 years.

- March 2025: Mallinckrodt and Endo agreed to merge in a USD 7 billion deal, blending generics and sterile injectables with USD 150 million synergy aims by year 3.

- February 2025: Teleflex acquired BIOTRONIK’s vascular intervention unit for EUR 760 million (USD 820 million), expanding cardiovascular reach.

- February 2025: Baxter reported USD 10.64 billion FY 2024 revenue, completing its Kidney Care exit and refocusing on anesthesia and critical-care injectables.

Global General Anesthesia Drugs Market Report Scope

As per the scope of the report, general anesthesia is a medically induced, reversible state of total unconsciousness and unresponsiveness, often described as a deep, controlled sleep. It utilizes a combination of intravenous drugs and inhaled gases to ensure the patient feels no pain, has no memory of the procedure, and experiences muscle relaxation.

The general anesthesia drugs market is segmented by drug type, route of administration, surgery type, end user, and geography. By type of drugs, the market is segmented into Sevoflurane, Desflurane, Isoflurane, Nitrous Oxide, Propofol, and Other Drugs. By route of administration, the market is segmented into inhalation and intravenous. The market is segmented by application into general surgery, cancer surgery, heart surgery, knee and hip replacements, and other surgery types. End users segment the market into hospitals, ambulatory surgical centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Propofol |

| Sevoflurane |

| Desflurane |

| Dexmedetomidine |

| Remifentanil |

| Midazolam |

| Etomidate |

| Ketamine |

| Other Drugs |

| Inhalation |

| Intravenous (TIVA) |

| General Surgery |

| Cancer Surgery |

| Heart Surgery |

| Orthopedic Replacements |

| Neurological Surgery |

| Other Application |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty & Dental Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Propofol | |

| Sevoflurane | ||

| Desflurane | ||

| Dexmedetomidine | ||

| Remifentanil | ||

| Midazolam | ||

| Etomidate | ||

| Ketamine | ||

| Other Drugs | ||

| By Route of Administration | Inhalation | |

| Intravenous (TIVA) | ||

| By Application | General Surgery | |

| Cancer Surgery | ||

| Heart Surgery | ||

| Orthopedic Replacements | ||

| Neurological Surgery | ||

| Other Application | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty & Dental Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will spending on general anesthesia drugs be by 2031?

The general anesthesia drugs market size is projected to reach USD 6.74 billion by 2031, up from USD 5.66 billion in 2025.

Which anesthetic molecule is gaining share fastest?

Propofol is forecast to advance at a 4.98% CAGR to 2031, powered by total intravenous anesthesia protocols and ASC penetration.

Why are hospitals phasing out desflurane?

Carbon taxes and environmental mandates in the UK, Germany, and other EU states target desfluranes 2,540 GWP, prompting switches to sevoflurane or TIVA.

What technologies are reshaping dosage practices?

AI-enabled closed-loop systems integrate EEG depth monitoring with smart pumps, trimming propofol and remifentanil use by up to 22% while standardizing care.

Which region will grow fastest through 2031?

Asia-Pacific, aided by hospital buildouts in China and India and competitively priced generics, is forecast for a 5.22% CAGR.

How concentrated is supplier power?

The top five pharmaceutical firms hold about 45-50% of revenue, reflecting moderate concentration yet rising generic encroachment.

Page last updated on: