Market Overview

| Study Period | 2020 - 2031 |

|---|---|

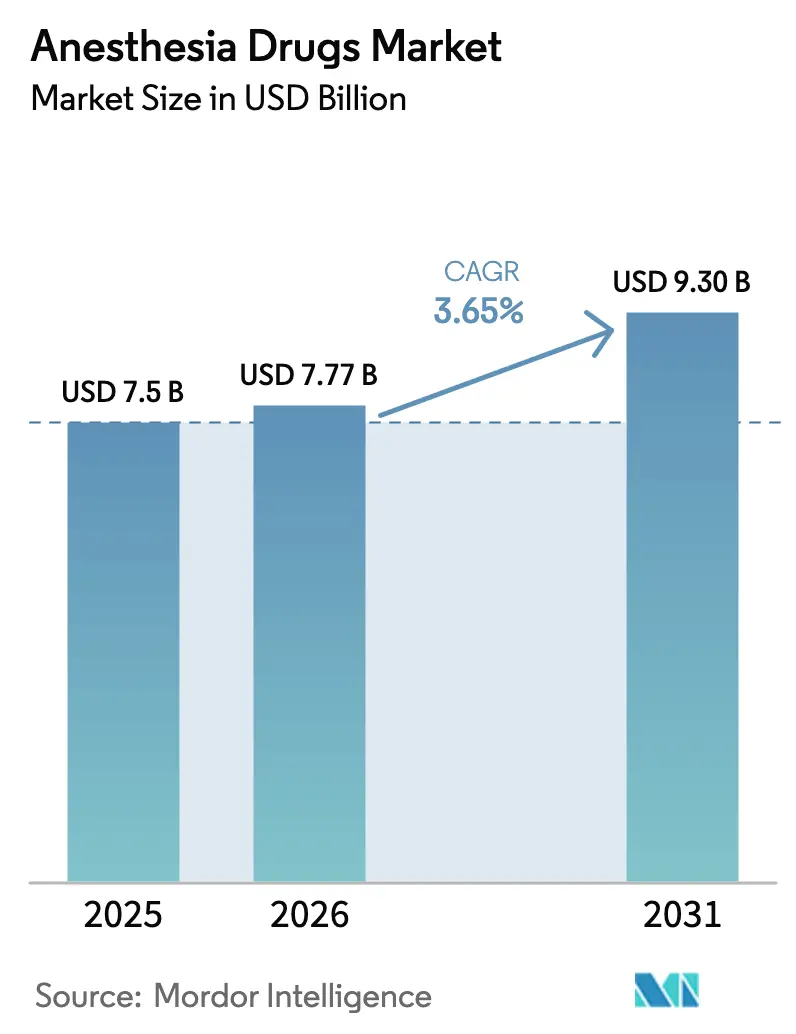

| Market Size (2026) | USD 7.77 Billion |

| Market Size (2031) | USD 9.30 Billion |

| Growth Rate (2026 - 2031) | 3.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

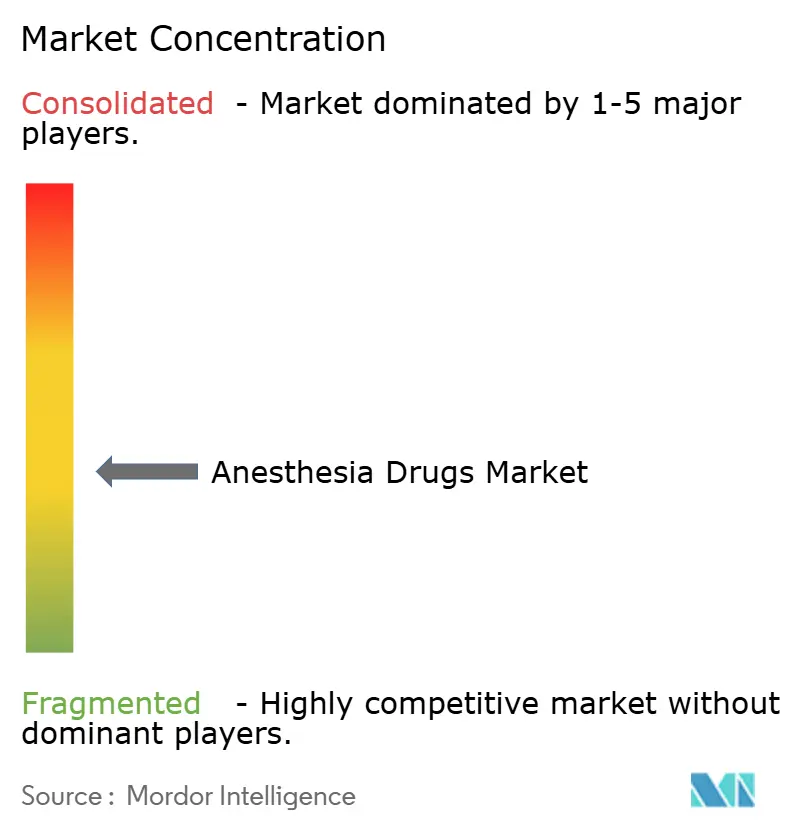

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anesthesia Drugs Market Analysis by Mordor Intelligence

The Anesthesia Drugs Market size is projected to expand from USD 7.5 billion in 2025 and USD 7.77 billion in 2026 to USD 9.30 billion by 2031, registering a CAGR of 3.65% between 2026 to 2031.

The headline CAGR conceals a transition away from high-global-warming-potential volatiles toward short-acting injectables as hospitals adopt total intravenous anesthesia and Enhanced Recovery After Surgery (ERAS) pathways. Surgical backlogs from the pandemic era are clearing, especially in orthopedics and bariatrics, which boosts volume even as generic pricing pressure squeezes margins. Robotic-assisted procedures add depth-of-sedation requirements that favor dexmedetomidine and remifentanil, while ASC networks accelerate demand for rapid-recovery protocols. Environmental regulations that phase out desflurane and restrict sevoflurane in several countries further reshape the anesthesia drugs market.

Key Report Takeaways

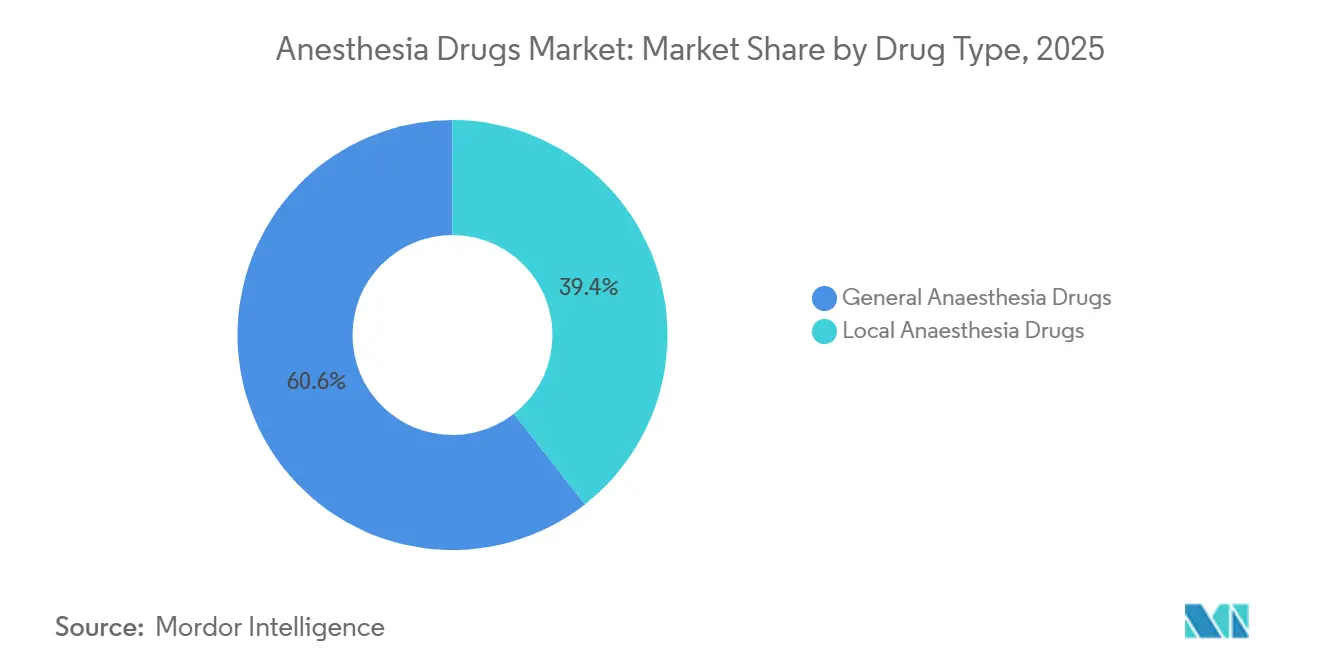

- By drug type, general anesthesia agents led with 60.56% anesthesia drugs market share in 2025, while local anesthetics are forecast to expand at an 8.25% CAGR through 2031.

- By route, injectables accounted for 70.53% of the anesthesia drugs market size in 2025; inhalation formulations are advancing at a 7.85% CAGR through 2031.

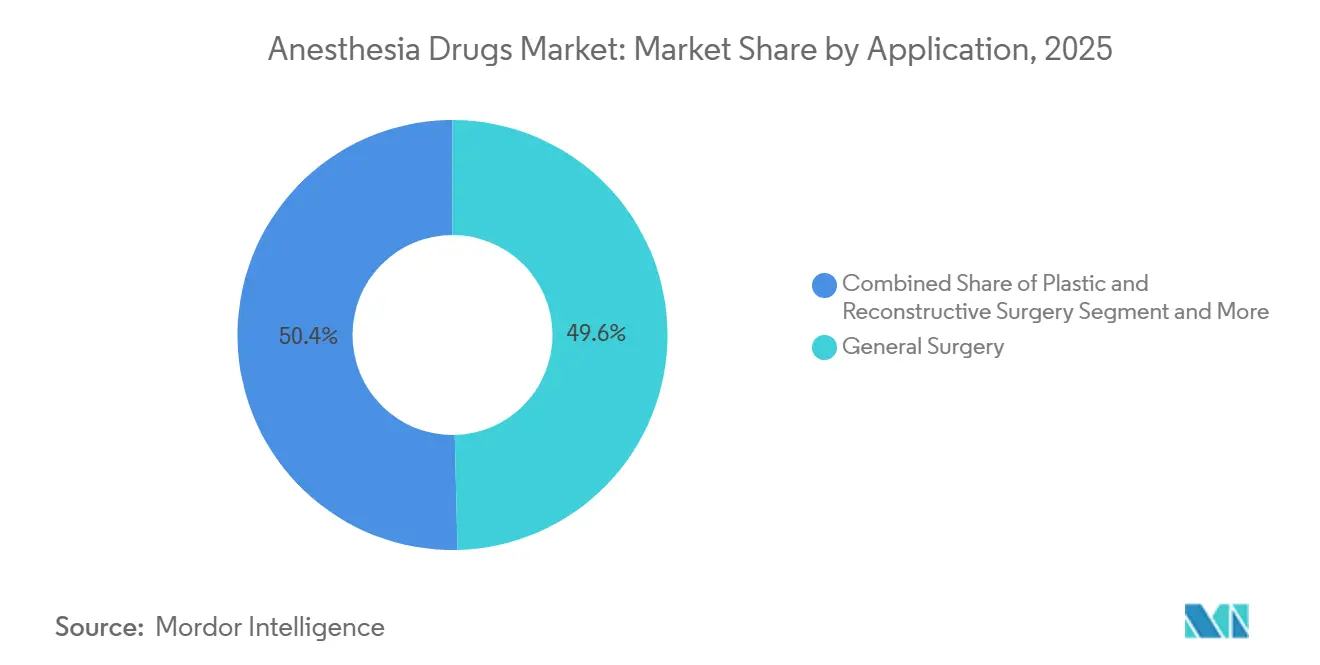

- By application, general surgery accounted for 49.63% in 2025, while cosmetic and aesthetic surgery posted an 8.87% CAGR outlook to 2031, surpassing the overall anesthesia drugs market.

- By end user, hospitals captured 62.53% of the global market in 2025, and Ambulatory Surgical Centers are growing at a 6.71% CAGR through 2031.

- By geography, Asia-Pacific is set to grow at an 8.51% CAGR, outpacing North America’s mature base of 38.13% share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anesthesia Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing number of surgeries (elective & trauma) | +0.9% | Global, with APAC and MEA showing highest elasticity due to infrastructure expansion and rising middle-class access | Medium term (2-4 years) |

| Rapid approvals of novel fixed-dose anesthetic combos | +0.6% | North America & EU regulatory corridors, with spillover to APAC markets following WHO prequalification pathways | Short term (≤ 2 years) |

| Shift to ambulatory & office-based procedures | +0.7% | North America (especially U.S. ASC networks), Western Europe, urban APAC hubs (Singapore, Seoul, Shanghai) | Medium term (2-4 years) |

| Growth of robotic-assisted surgery requiring deeper sedation | +0.5% | North America, EU, Japan, South Korea; limited penetration in cost-sensitive LMIC markets | Long term (≥ 4 years) |

| Peri-operative ERAS protocols boosting short-acting agents | +0.5% | Global adoption in academic medical centers; North America and Northern Europe leading implementation, gradual APAC uptake | Medium term (2-4 years) |

| AI-driven closed-loop anesthesia delivery systems | +0.3% | Concentrated in North America and EU research hospitals; regulatory approval timelines extend commercial impact to 2028-2030 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Number of Surgeries Driving Anesthetic Agent Consumption

Elective orthopedic and bariatric cases are clearing pandemic backlogs, lifting volume for neuromuscular blockers and longer-acting agents. The American Society of Anesthesiologists estimated 1.2 million deferred U.S. procedures still in queue mid-2024. Hospitals extend operating schedules, which raises consumption of predictable-offset drugs that reduce turnover delays. Japan and South Korea confront aging populations, and geriatric protocols increasingly substitute dexmedetomidine for benzodiazepines to cut postoperative delirium risk.

Rapid Approvals of Novel Fixed-Dose Anesthetic Combinations

Three U.S. FDA approvals between 2024 and 2025 introduced propofol-ketamine and sevoflurane-nitrous blends, locking institutions into single-supplier contracts that resist generic erosion. Uptake is slower than expected because clinicians prefer titration flexibility, yet ASCs value 30-40% prep-time savings and streamlined nurse sedation workflows. EU and APAC markets follow after WHO prequalification clears import pathways.

Shift to Ambulatory and Office-Based Procedures Reshaping Anesthetic Demand

Payer-driven site-of-care migrations favor agents with rapid recovery. In 2024, 68% of U.S. outpatient surgeries took place in ASCs. Propofol remains ubiquitous, while remimazolam gains traction where approved. Europe lags due to entrenched hospital day-surgery units, limiting addressable demand for office-friendly anesthetics.

Growth of Robotic-Assisted Surgery Requiring Deeper Sedation

Robotic procedures reached 2.3 million cases worldwide in 2024, up 17% year over year[1]Intuitive Surgical, “2024 Annual Report—Procedure Volume,” sec.gov. Deeper sedation and prolonged neuromuscular blockade increase propofol and sugammadex utilization. Early-adopting hospitals report 20-30% higher propofol consumption per hour, and training centers inflate drug usage during learning curves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-operative cognitive dysfunction concerns | -0.4% | Global, with heightened scrutiny in aging populations (Japan, Germany, Italy, North America); malpractice liability amplifies impact in U.S. | Medium term (2-4 years) |

| Volatile-agent greenhouse impact regulations tightening | -0.6% | EU (desflurane bans effective 2024-2028), UK (implemented 2024), select U.S. states (California, New York proposals); limited APAC penetration | Short term (≤ 2 years) |

| Shortage of fellowship-trained anesthesiologists in LMICs | -0.3% | Sub-Saharan Africa, South Asia (India, Bangladesh, Pakistan), parts of Latin America; constrains surgical volume growth and anesthetic safety protocols | Long term (≥ 4 years) |

| Supply-chain volatility for key APIs | -0.5% | Global impact with acute exposure in markets dependent on single-source APIs (propofol from China, rocuronium from EU); geopolitical tensions amplify risk | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-Operative Cognitive Dysfunction Concerns Constraining Agent Selection

Academic centers pivot toward total intravenous anesthesia for elderly patients after observational links between prolonged volatile exposure and cognitive decline. Updated American Geriatrics Society guidelines advise minimizing benzodiazepines. Yet a 2025 meta-analysis found no statistical difference when depth monitoring was applied, stalling formulary switches in cost-sensitive systems.

Volatile-Agent Greenhouse Impact Regulations Tightening

The UK banned desflurane purchases in 2024, and EMA guidance recommends EU phase-outs by 2028[2]European Medicines Agency, “Environmental Impact of Volatile Anesthetics,” ema.europa.eu. California and New York consider similar bills. Retrofitting scavenging systems costs USD 15,000–25,000 per machine, steering small facilities toward injectables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: TIVA Protocols Challenge Volatile Dominance

General anesthesia drugs accounted for 60.56% of the anesthesia drugs market in 2025. Sevoflurane leads mask inductions, but much of its growth replaces desflurane rather than generating net volume. Dexmedetomidine strengthens its neuro- and ICU niche, and remifentanil retains premium positioning in robotic suites. Local agents strengthen as ultrasound-guided nerve blocks cut postoperative opioid use by up to 50%.

The anesthesia drugs market continues to rebalance as regional techniques converge with ERAS protocols. Bupivacaine dominates long-acting blocks, while ropivacaine gains obstetric share. Lidocaine remains common for short dental and dermatological procedures. Chloroprocaine revives in ASCs for its rapid metabolism, though adoption remains limited to specialist centers.

By Route of Administration: Injection Entrenched, Inhalation Rebounds

Injectables represented 70.53% revenue in 2025. The anesthesia drugs market size for injectables benefits from standardized TIVA in neurosurgery and intraoperative monitoring cases. Dexmedetomidine is the fastest-growing infusion therapy in ICUs thanks to ventilator-sparing properties. Supply constraints linger because propofol’s lipid emulsion requires cold-chain logistics.

Inhalation agents are projected to grow at a 7.85% CAGR through 2031, driven by sevoflurane in pediatric and day-surgery settings across Asia-Pacific. Generic launches widen access, but manufacturing complexity caps supplier count. Topical and transdermal formats remain stable, serving chronic-pain and pediatric venipuncture niches without encroaching on surgical volume.

By Application: Cosmetic Surge Outpaces Core Surgical Demand

General surgery maintained 49.63% share in 2025, yet bundled-payment models cap its growth. Elective cosmetic procedures are forecast at an 8.87% CAGR to 2031, the fastest within the anesthesia drugs market. Office-based anesthesia relies on propofol-ketamine or moderate sedation, creating a separate supply chain from hospital formularies.

Dental demand scales with Asia-Pacific middle-class expansion, relying almost entirely on lidocaine and articaine. Obstetric protocols favor neuraxial bupivacaine or ropivacaine, and U.S. hospitals offered epidurals in 73% of births in 2025[3]American College of Obstetricians and Gynecologists, “Labor Analgesia Survey,” acog.org. Ophthalmic, ENT, and urologic cases round out the remainder.

By End User: ASCs Capture Share from Hospitals

Hospitals consumed 62.53% of anesthetic drugs in 2025, but payer steering and efficiency gaps erode share. Group purchasing organizations secure 30-40% discounts, yet overhead keeps per-case costs high. Hospital-owned ASCs attempt to retain revenue while chasing outpatient efficiencies.

Standalone ASCs grow at 6.71% CAGR, achieving 8-12 minute turnovers with rapid-acting agents. Specialty clinics for pain and aesthetics diversify fastest, matching office-based demand for same-day discharge. These shifts redistribute the anesthesia drugs market away from traditional inpatient settings.

Geography Analysis

North America commanded 38.13% of the anesthesia drugs market in 2025 on roughly 50 million annual procedures. Patent-protected injectables and branded generics sustain premium pricing, yet propofol fell below USD 2 per 100 mg vial in 2024, compressing margins. Environmental legislation in California and New York threatens inhalation formularies while office-based cosmetic demand insulates cash-pay segments.

Asia-Pacific is projected to register an 8.51% CAGR, the highest regional pace for the anesthesia drugs market. China recorded about 80 million surgeries in 2024, expanding 6-8% annually, and India adds OR capacity across tier-2 and tier-3 cities despite anesthesiologist shortages. Premium hubs in Singapore, Japan, and South Korea adopt remimazolam and dexmedetomidine, whereas rural facilities rely on older agents.

Europe balances cost containment with innovation. Germany’s decentralized system drives volume, while the U.K.’s centralized procurement delivers the world’s lowest propofol prices. Desflurane bans and pending EU phase-outs reshape inhalation demand. Southern and Eastern Europe lag in regional anesthesia adoption due to fewer ultrasound systems and training deficits. Smaller Middle East, Africa, and South American markets face infrastructure gaps and currency volatility that hinder broad anesthetic access.

Regulatory Landscape

Regulation of anesthesia drugs spans drug approvals, post-market safety actions, and technical quality standards that affect supply continuity for high-volume injectables and inhaled agents. In the United States, the FDA continues to clear new anesthetic options, including the May 2026 approval of Haisco Pharmaceutical Group's Cypsedo (cipepofol) for induction of general anesthesia in adults undergoing surgery, which adds a regulated IV alternative alongside entrenched propofol use.

In Europe, EMA and the Coordination Group for Mutual Recognition and Decentralized Procedures-human (CMDh) are tightening lifecycle obligations through pharmacovigilance-driven labeling updates and a more formal variations regime. CMDh adopted a position in November 2025 to update rocuronium product information following a safety review, with implementation deadlines extending into February 2026, while updated EU variations guidance became applicable in January 2026 and increases procedural rigor for manufacturing, quality, and labeling changes. Technical compliance is also shaped by pharmacopoeial requirements, with new and revised European Pharmacopoeia monographs entering into force in July 2026 under EDQM stewardship, reinforcing impurity controls and batch-release expectations for marketing authorization holders.

Competitive Landscape

The anesthesia drugs market exhibits moderate concentration in commoditized molecules but fragmentation in specialty niches. Top manufacturers, Fresenius Kabi, Baxter, and Aspen, control a significant percentage of propofol volume yet wield little pricing power under interchangeable generics. Chinese firms, notably Jiangsu Hengrui Pharma, discount 30-40% below Western prices regionally but face regulatory barriers in OECD markets. Pfizer retains dexmedetomidine loyalty in ICUs despite expiring exclusivity, and PAION’s remimazolam partners target procedural sedation whitespace.

Strategic responses diverge. Incumbents bolster vertical integration to secure APIs; Fresenius Kabi expanded Graz propofol output in 2025. Smaller entrants license novel emulsions or intranasal formats to extend patent tails. Technology bets coalesce around decision-support rather than fully autonomous closed-loop systems, reflecting regulatory caution. Environmental compliance costs for take-back programs on volatiles add 5-8% to COGS, favoring incumbents with existing reverse logistics. Biosimilar challengers in India and specialty U.S. compounders nibble at niche volumes but remain under 2% share.

Anesthesia Drugs Industry Leaders

Baxter International Inc.

B. Braun Melsungen AG

Fresenius SE & Co. KGaA

Pfizer Inc.

Aspen Pharmacare Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Persistent supply fragility in core anesthesia injectables creates an opening for manufacturers that can deliver reliable, regulator-compliant capacity across high-use hospital formats (vials, infusions, and ready-to-administer presentations). FDA-maintained drug shortage tracking and mitigation tools, including extended use date information for specific products, highlight availability as a differentiator alongside price for standardized agents used at scale in hospitals and ambulatory surgical centers.

Pipeline-to-market conversions in 2026 also point to whitespace in differentiated IV induction and reversal options that fit rapid-recovery workflows. FDA approval of Cypsedo (cipepofol) introduces a new branded IV anesthetic entrant for adult surgical induction, while B. Braun Medical Inc. received FDA approval for a generic sugammadex injection with U.S. availability starting July 28, 2026, expanding competition in neuromuscular blockade reversal where uptime and OR turnover are operational priorities. In Europe, EMA medicine-shortage coordination via the MSSG and SPOC Working Party indicates continued emphasis on resilience measures and alternate sourcing, supporting opportunities for suppliers that can implement validated manufacturing changes through the variations framework.

Recent Industry Developments

- April 2026: Baxter reported organizational changes in first-quarter 2026 results that integrated its former Pharmaceuticals segment (including inhaled anesthesia and specialty injectable pharmaceuticals) into the Infusion Therapies and Platforms division within Medical Products and Therapies. The realignment links anesthesia-related pharmaceuticals more directly with Baxter's infusion and hospital platform strategy, shaping how resources and commercial priorities are set for hospital customers.

- December 2025: Fresenius Kabi launched Rocuronium Bromide Injection Room Temperature Stable (RTS), a neuromuscular blocking agent that does not require refrigeration and is manufactured at its Grand Island, New York facility. By removing cold-chain constraints, the RTS format streamlines hospital inventory management and supports higher reliability in perioperative drug availability.

- December 2024: Baxter announced the launch of five injectable pharmaceutical products in the United States, bringing its total injectable launches for 2024 to 10. The cadence of new injectable introductions reinforces portfolio breadth in a category where hospitals and ASCs prioritize dependable supply and standardized formulations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the anesthesia drugs market covers prescription medicines used to induce, maintain, or reverse anesthesia and procedural sedation across inpatient and outpatient clinical settings, measured in value terms (USD) for the global demand pool.

Scope exclusions: It excludes anesthesia machines and disposables, as well as non-drug clinical services such as provider fees and facility charges.

Segmentation Overview

- By Drug Type

- General Anaesthesia Drugs

- Propofol

- Sevoflurane

- Desflurane

- Dexmedetomidine

- Remifentanil

- Midazolam

- Other General Anaesthesia Drugs

- Local Anaesthesia Drugs

- Bupivacaine

- Ropivacaine

- Lidocaine

- Chloroprocaine

- Prilocaine

- Benzocaine

- Other Local Anaesthesia Drugs

- General Anaesthesia Drugs

- By Route of Administration

- Injection

- Inhalation

- Topical & Transdermal

- By Application

- General Surgery

- Plastic & Reconstructive Surgery

- Cosmetic / Aesthetic Procedures

- Dental Procedures

- Obstetric & Gynecologic Surgery

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building a clean picture of the surgical and procedure demand base, since anesthesia drug usage is closely tied to case volumes by setting. We referenced public sources such as the World Health Organization for health-system indicators, the OECD for surgery and hospital activity datasets where available, and the World Bank for population and macro health metrics that influence procedure growth.

To connect demand to products, we reviewed regulatory and drug-use context from sources such as the US FDA labeling and safety communications, the European Medicines Agency public assessment reports, and peer reviewed journals covering anesthesia practice patterns. We also used company filings, investor presentations, reputable press, and a paid subscription for company financials and news to keep price and mix assumptions realistic when public disclosures were thin. This list is not exhaustive, and many other sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on checking how anesthesia protocols are evolving across hospitals, ambulatory surgical centers, and specialty clinics, and how that changes product mix by route (injection, inhalation, and topical/transdermal) and by use case. We spoke with a spread of stakeholders such as clinicians, pharmacy and procurement teams, and commercial managers, then reconciled differences across major regions so the assumptions fit real purchasing and utilization behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 17% | APAC: 45% |

| Mid tier: 43% | Functional/Unit leaders: 31% | EMEA: 33% |

| Smaller Players: 20% | Managers: 52% | Americas: 22% |

Market-Sizing & Forecasting

The sizing model begins with a top-down build where procedure and surgery activity, along with anesthesia penetration by care setting, is used to reconstruct the addressable drug demand pool by region. Because anesthesia usage is not uniform, we applied practical adjustment factors tied to anesthesia type mix (general versus local), route mix (inhalation versus injection versus topical/transdermal), and application patterns across general surgery, dental, and obstetric or gynecologic procedures.

Those totals were then checked with selective bottom-up approximations, mainly using sampled volume times average selling price logic for key molecules and channel checks on hospital and outpatient purchasing. When product level volume was hard to observe, gaps were handled by anchoring to clinical protocol norms and validated substitution rules (for example, when one agent is preferred versus used as a backup), and then rebalancing shares to match the demand signals seen in interviews.

Forecasts were built using scenario analysis, where procedure growth, outpatient shift, and price progression expectations were stress-tested before selecting the final trajectory. Inputs such as surgical backlog normalization, aging population trends, expected genericization timing, and regional reimbursement or formulary tightening were used as the main drivers, and then refined after expert feedback so the curve stays realistic year by year.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including procedure growth indicators, route and setting mix expectations, and the implied spend per case, which helps catch overstatement early. If a region or drug class showed an unusual jump, we revisited the underlying assumptions and triggered follow-up calls to confirm whether the change was real or a modeling artifact.

Before sign-off, the work goes through multiple analyst review steps, where assumptions, math checks, and unit consistency are rechecked and the narrative is aligned to the numbers. Reports refresh annually, with interim updates when material events occur, and a final pre-delivery pass so clients receive the most current view.

Mordor Intelligence's Global Anesthesia Drugs Market Market Size Compared Against Other Published Estimates

Published market sizes for anesthesia drugs often vary because sources do not always count the same drug scope, the same care settings, or the same timing for pricing and currency conversion. Differences also appear when one estimate leans more on broad pharma spend ratios while another ties value to procedure-linked utilization.

In this study, the key gap drivers are how general versus local anesthetics are treated, whether topical/transdermal anesthesia drugs are included alongside injection and inhalation routes, and how application demand (such as dental and obstetric or gynecologic procedures) is mapped into volumes. The spread can also come from how average selling prices are stepped forward during genericization windows, and whether assumptions are refreshed after new labeling, safety updates, or protocol shifts are observed, which is handled through the update cadence applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.77 B (2026) | |

| Trade Publisher A | USD 7.60 B (2025) | Uses a different base year and can blend route and setting assumptions into a single headline number, which may not fully separate local versus general anesthesia demand and mix shifts across hospitals and outpatient centers. |

| Global Advisory B | USD 6.34 B (2024) | Has a narrower product and route frame in the published view (focused on a shorter product list and mainly injection and inhalation), which can undercount topical/transdermal use and some application-led consumption. |

Taken together, the table shows that year selection and what is counted as an anesthesia drug are the two biggest reasons for the differences. When scope is aligned across general and local drugs, route coverage, and procedure-linked demand mapping, the resulting market value becomes easier to trace to clear inputs and to repeat in future updates.

Key Questions Answered in the Report

What is the current valuation of the anesthesia drugs market?

The anesthesia drugs market size is USD 7.77 billion in 2026 and is forecast to reach USD 9.30 billion by 2031.

Which region will grow fastest for anesthetic agents through 2031?

Asia-Pacific is projected to expand at an 8.51% CAGR, led by rising surgical volumes in China and India.

How are environmental regulations affecting inhalation anesthetics?

The U.K. banned desflurane in 2024 and the EU plans to phase out high-GWP volatiles by 2028, accelerating the shift toward injectables.

Why are ambulatory surgical centers important to anesthetic demand?

ASCs combine high procedure volume with rapid turnover, driving adoption of short-acting agents and growing at a 6.71% CAGR.

Which drug types are losing share within general anesthesia?

Desflurane usage is collapsing due to greenhouse-gas policies, while sevoflurane only grows by replacing desflurane rather than adding new volume.

Page last updated on: