Post-Operative Pain Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

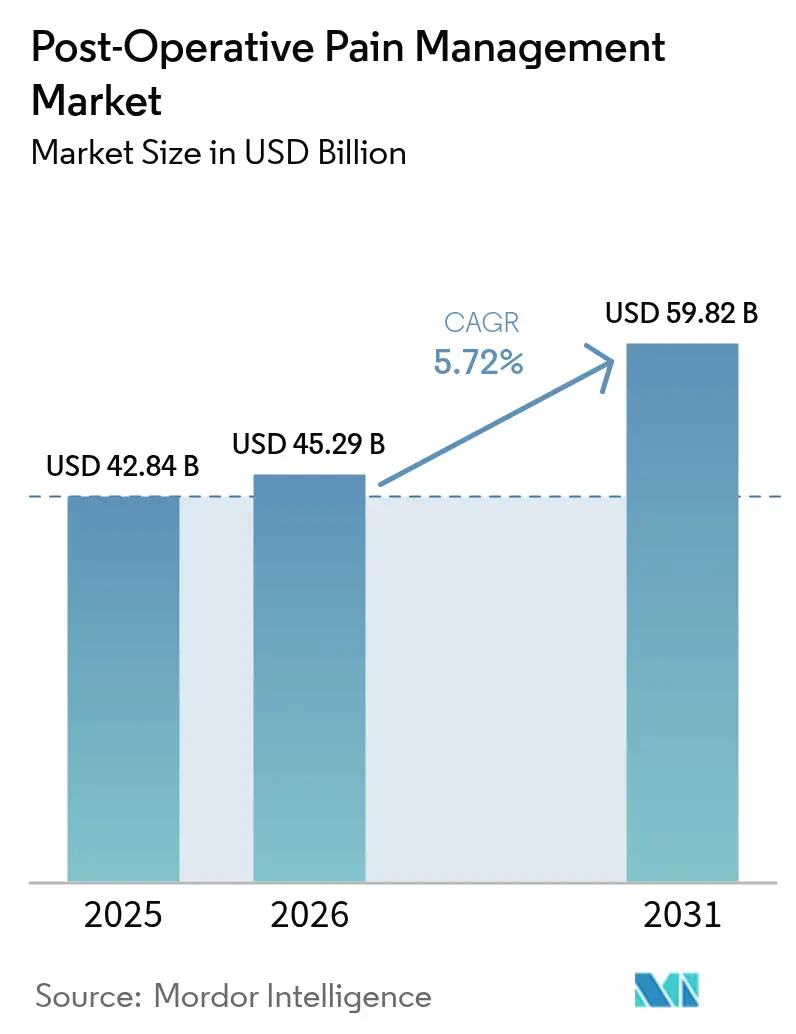

| Market Size (2026) | USD 45.29 Billion |

| Market Size (2031) | USD 59.82 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Post-Operative Pain Management Market Analysis by Mordor Intelligence

The Post-Operative Pain Management market size is projected to expand from USD 42.84 billion in 2025 and USD 45.29 billion in 2026 to USD 59.82 billion by 2031, registering a CAGR of 5.72% between 2026 to 2031. Payer carve-outs for non-opioid drugs, rapid growth of ambulatory surgery centers, and stricter opioid prescribing limits are the primary levers behind this steady advance. Hospitals are revising formularies because the Centers for Medicare & Medicaid Services created separate reimbursement pathways that fully offset the premium of long-acting local anesthetics, while the U.S. Food & Drug Administration clarified clinical endpoints for acute non-opioid analgesics, giving developers a clear approval roadmap. Health systems are also expanding AI-guided stewardship programs that tailor dosing and reduce adverse events, reinforcing multimodal protocols. Together, these forces keep the Post-Operative Pain Management market on a predictable value trajectory, even as cost pressures weigh on high-priced intravenous drugs and prescriber confidence in opioids continues to wane.

Key Report Takeaways

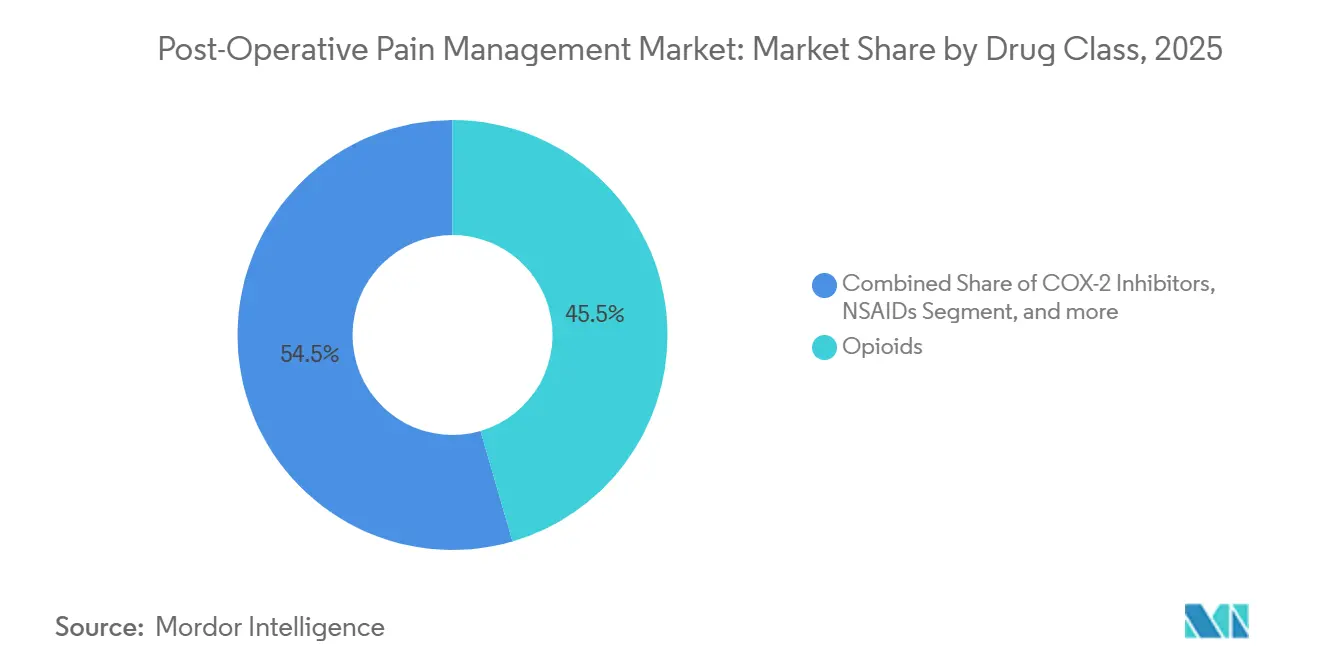

- By drug class, opioids led with 45.55% of Post-Operative Pain Management market share in 2025, yet local anesthetics are advancing at an 8.25% CAGR through 2031.

- By route, injectable products held 47.53% of Post-Operative Pain Management market size in 2025, while topical and transdermal formulations are set to expand at a 9.75% CAGR through 2031.

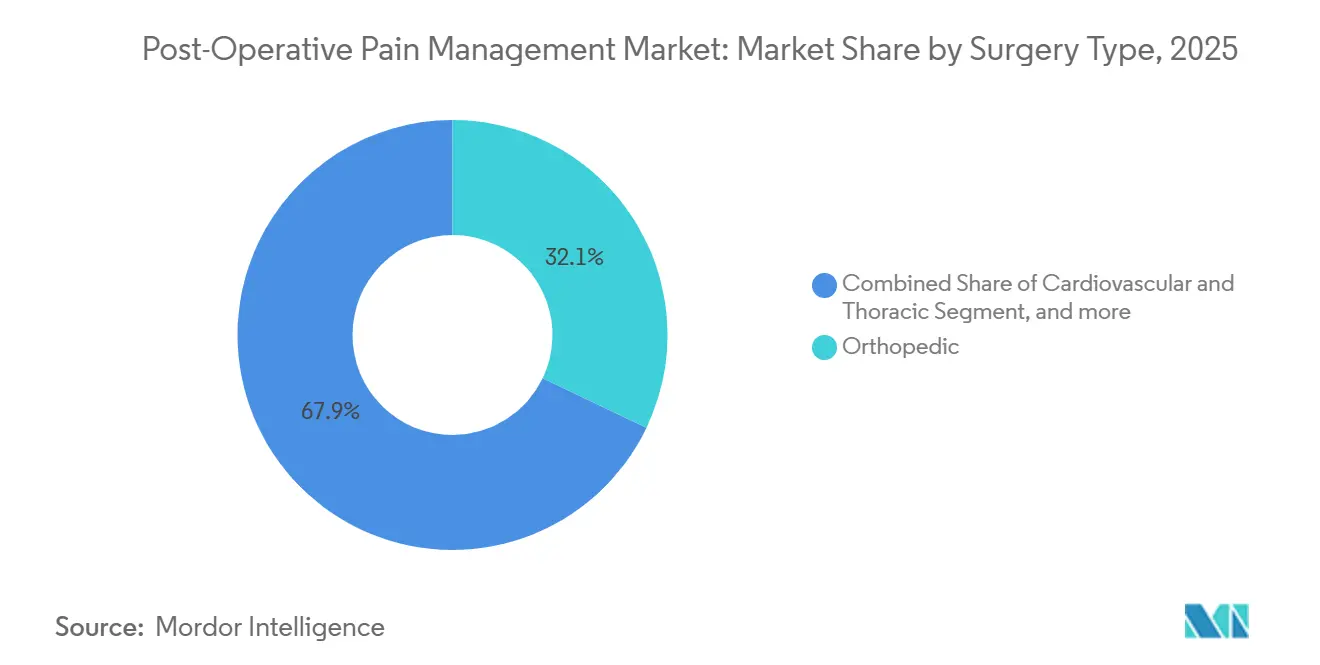

- By surgery type, orthopedic procedures accounted for 32.15% of Post-Operative Pain Management market size in 2025, whereas obstetrics and gynecology is growing fastest at an 8.82% CAGR through 2031.

- By distribution channel, hospital pharmacies dispensed 49.65% of total analgesics in 2025, although online pharmacies are rising at an 8.32% CAGR to 2031 as telehealth prescribing rules settle.

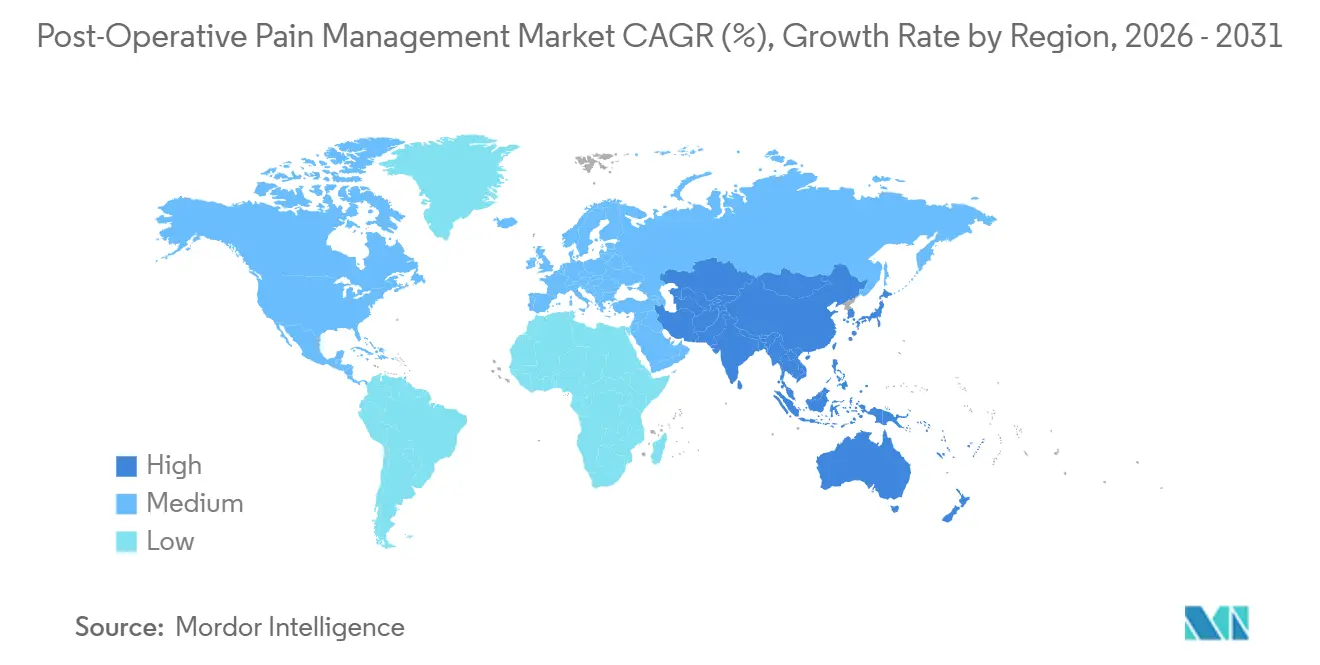

- North America captured 38.23% of global revenue in 2025; Asia-Pacific is the fastest region with a 7.42% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Post-Operative Pain Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Number of Surgical Procedures | +1.2% | Global, with strongest volume growth in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Shift Toward Multimodal & Non-Opioid Protocols | +1.5% | North America & Europe lead adoption; Asia-Pacific accelerating | Short term (≤ 2 years) |

| Adoption of Long-Acting Regional/Nerve-Block Anesthetics | +0.9% | North America, Western Europe, urban Asia-Pacific centers | Medium term (2-4 years) |

| Expansion of Ambulatory Surgery Centers (ASCs) | +0.8% | North America dominant; emerging in GCC and Australia | Long term (≥ 4 years) |

| AI-Driven Personalized Opioid Stewardship Algorithms | +0.5% | North America pilot sites; select European academic hospitals | Long term (≥ 4 years) |

| Legislated Separate Reimbursement for Non-Opioid Analgesics | +1.0% | United States (CMS mandate); exploratory in Canada and Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Number of Surgical Procedures

Elective surgeries have rebounded to pre-pandemic baselines and continue to climb, especially in hip and knee replacement programs that dominate orthopedic caseloads. Ambulatory migration of these high-volume procedures intensifies demand for opioid-sparing regimens that enable same-day discharge. Asia-Pacific health ministries are scaling theater capacity in tier-2 and tier-3 cities, a move that enlarges the Post-Operative Pain Management market by exposing millions of new patients to standardized multimodal protocols. At the same time, global non-government organizations highlight the backlog of untreated surgical cases in low-income regions, indicating strong latent demand that will surface as infrastructure matures. The cumulative effect is a durable volume tailwind that offsets price erosion in mature Western markets.

Shift Toward Multimodal & Non-Opioid Protocols

Guideline bodies and payers now designate multimodal therapy as first-line care, replacing opioid monotherapy in most inpatient and outpatient pathways[1]U.S. Food & Drug Administration, “Non-Opioid Analgesic Drug Products for the Management of Acute Pain,” fda.gov. CMS reimbursement carve-outs eliminate hospital budget penalties for premium non-opioid drugs, unleashing rapid formulary conversion throughout large U.S. systems. Europe proceeds more cautiously but German sickness funds are piloting similar models, signaling eventual continental uptake. Hospitals gravitate toward dual-mechanism formulations such as bupivacaine-meloxicam matrices that combine nociceptive and inflammatory control in one dose, reducing nursing workload and inventory complexity. Together, these shifts accelerate real-world adoption curves, deepening the revenue base of the Post-Operative Pain Management market.

Adoption of Long-Acting Regional/Nerve-Block Anesthetics

Extended-release local anesthetics continue to displace systemic opioids in orthopedic and abdominal surgeries, supported by robust though sometimes variable clinical evidence. Liposomal bupivacaine remains the flagship, yet next-generation depot technologies like CPL-01 show tighter pharmacokinetic profiles and may claim premium positioning. Hospitals accept modest unit costs when data prove shorter post-anesthesia care stays and fewer opioid rescue doses. Interest is also expanding for device-based modalities, exemplified by cryoanalgesia systems that offer non-pharmacologic nerve blockade. These options widen therapeutic choice without adding opioid exposure, a critical outcome metric in the Post-Operative Pain Management market.

Expansion of Ambulatory Surgery Centers (ASCs)

ASCs accounted for fewer than 20,000 total knee arthroplasties in 2020 but surpassed 38,000 by 2023, reflecting a 258% surge that is still accelerating. Because ASCs receive lower reimbursement than hospital outpatient departments, administrators champion rapid-recovery formularies that cap supply costs and facilitate early ambulation. Vendors are responding with bundled analgesic kits customized for ASC workflows, driving direct contracting that bypasses traditional group purchasing channels. Similar models are emerging in the Gulf Cooperation Council where elective orthopedic and ophthalmology centers follow U.S. blueprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Opioid Addiction Crisis & Tightening Regulations | -0.7% | North America and Europe; emerging awareness in Asia-Pacific | Short term (≤ 2 years) |

| Hospital Cost-Containment Pressures on Premium IV Formulations | -0.5% | Global, most acute in public health systems with fixed budgets | Medium term (2-4 years) |

| MHRA Ban on Modified-Release Opioids for Acute Post-Op Pain | -0.3% | United Kingdom; potential spillover to Commonwealth nations | Short term (≤ 2 years) |

| Pharmacist & Technician Workforce Shortages | -0.4% | North America, Western Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Opioid Addiction Crisis & Tightening Regulations

The CDC guideline restricting acute opioid prescriptions to 3-day courses is now enforced in most U.S. states, while electronic monitoring programs flag deviations from peer norms[2]Centers for Disease Control and Prevention, “Clinical Practice Guideline for Prescribing Opioids,” cdc.gov. UK regulators barred modified-release formulations for acute postoperative use, a precedent other Commonwealth regulators are evaluating. Although these rules reduce opioid unit volume, they implicitly enlarge demand for non-opioid alternatives, cushioning revenue loss across the broader Post-Operative Pain Management market.

Hospital Cost-Containment Pressures on Premium IV Formulations

Global pharmacy budgets are strained by labor inflation and specialty drug inflation. Extended-release bupivacaine can cost USD 300-400 per dose against USD 10 for its conventional counterpart, imposing tough value-for-money hurdles. Group purchasing rebates help but often mandate minimum quarterly volumes, exposing hospitals to financial penalties if surgeons under-utilize. Consequently, premium IV growth moderates outside high-margin elective pathways.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Local Anesthetics Rise on Opioid-Sparing Mandates

Local anesthetics generated USD x billion in 2025 and are forecast to grow at an 8.25% CAGR, capturing incremental Post-Operative Pain Management market share from opioids. Opioids still retained 45.55% of revenue in 2025, underlining their entrenched role despite mounting regulatory headwinds. In 2024, Pacira reported quarterly Exparel sales of USD 145 million, validating continuous uptake. Gabapentinoids, ketamine, and dexmedetomidine remain adjuncts rather than primaries, but combo products like bupivacaine-meloxicam are redefining value propositions.

Hospitals welcome local anesthetics because side-effect profiles improve patient satisfaction metrics tied to reimbursement. Next-wave depot technologies show promise for smoother plasma curves, which could further elevate preference over opioids. NSAIDs persist as backbone agents, yet safety considerations keep their dosage conservative, preserving headroom for anesthetic expansion within the overall Post-Operative Pain Management market.

By Route of Administration: Topical Products Lead Growth Curve

Topical and transdermal formats posted the fastest trajectory at 9.75% CAGR, although injectables still held the largest slice of Post-Operative Pain Management market size in 2025. Oral routes remain indispensable for home recovery, but concerns over opioid-induced ileus in enhanced recovery programs foster interest in oral non-opioid combinations. Intrathecal catheters continue in thoracic and abdominal contexts but demand specialized staffing that smaller centers often lack.

Hospitals are moving to line-free pain control to reduce infection risk and nursing time. The FDA guidance explicitly lists topical agents as viable for acute indications, accelerating dossier submissions. As staffing shortages hit IV compounding rooms, administrators green-light topical kits that nurses can apply without pharmacy verification, lifting practical barriers to adoption across the Post-Operative Pain Management market.

By Surgery Type: Obstetric Protocols Accelerate Ahead of Orthopedic Volume

Orthopedic procedures accounted for 32.15% of the 2025 revenue total, yet obstetrics and gynecology will outpace all other categories at an 8.82% CAGR. Enhanced recovery after cesarean protocols mandate baseline acetaminophen and NSAIDs, positioning opioids as rescue only. Cardiovascular and thoracic volumes soften due to minimally invasive techniques, but pain intensity remains high, supporting multimodal bundles.

ASCs are aggressively marketing same-day orthopedic joint programs using extended-release blocks engineered to last through the vulnerable first 72 hours. Cesarean pathways mirror this thinking, with hospitals standardizing dual-mechanism products that simplify nursing handoffs. Combined, these shifts maintain orthopedic volume leadership while allowing obstetrics to seize incremental Post-Operative Pain Management market share.

By Distribution Channel: Online Dispensing Finds Regulatory Clarity

Hospital pharmacies accounted for 49.65% of unit volume in 2025, yet online pharmacies are clocking an 8.32% CAGR as DEA telehealth rules settle and remote refill services mature[3]Drug Enforcement Administration, “Telemedicine Flexibilities Proposal,” dea.gov. Retail pharmacies suffer tightening margins but still dominate Schedule II fills due to in-person verification mandates.

ASCs setting up on-site take-home dispensaries blur the hospital–retail boundary, letting facilities capture downstream revenue and enforce multimodal adherence. Online portals integrate directly with telehealth follow-ups, automating refills for non-controlled SKUs and slowly encroaching on brick-and-mortar share. Collectively, these shifts continue to diversify distribution models within the Post-Operative Pain Management industry.

Geography Analysis

North America delivered 38.23% of 2025 revenue as CMS reimbursement changes neutralized hospital cost objections and ASC infrastructure matured quickly. The United States posts the widest installed base of AI-driven stewardship tools, further consolidating its leadership in the Post-Operative Pain Management market. Canada observes the U.S. rollout but provincial budget negotiations slow a national policy decision.

Asia-Pacific is the growth engine at 7.42% CAGR due to aggressive surgical capacity expansion in China and protocol differentiation by private Indian hospital chains. Tier-2 and tier-3 Chinese cities adopt standardized analgesic bundles that require minimal specialist oversight, favoring depot anesthetics and topical adjuncts. Japan’s aging demographic spikes orthopedic volume, while Australia weighs mirroring the UK opioid restrictions, decisions that could reshape delivery mix.

Europe moves cautiously. The MHRA ban forces the UK to pivot toward immediate-release opioids and non-opioid adjuncts, trimming unit value but lifting non-opioid volume. Germany pilots payment carve-outs yet national rollout hinges on federal–state consensus. France and Spain await more real-world data before approving premium depot products, keeping regional growth moderate relative to the broader Post-Operative Pain Management market.

Competitive Landscape

The market remains moderately fragmented. Pacira BioSciences and Heron Therapeutics dominate the extended-release local anesthetic niche, profiting from policy-driven uptake and procedure-specific kits. Generic houses control oral opioid and NSAID segments where patent cliffs force price competition. Device entrants offer cryoanalgesia and nerve stimulators that mesh with multimodal regimens, enabling joint commercial packages.

Abuse-deterrent opioid pipelines seek to recapture prescriber trust but face reimbursement skepticism. Pediatric indications are under-served, signaling white-space for weight-based depot formulations. Data-science vendors build opioid stewardship platforms that tether software subscriptions to drug sales, creating hybrid revenue models. Biosimilar challengers target liposomal bupivacaine patents set to expire post-2030, a shift likely to compress price but expand volume in the Post-Operative Pain Management market.

Post-Operative Pain Management Industry Leaders

AbbVie (Allergan)

Heron Therapeutics

Pfizer Inc.

AFT Pharmaceuticals

GSK plc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Nanjing Delova Biotech reported positive Phase 3 data for QP-6211, a long-acting ropivacaine injection for hemorrhoidectomy and bunionectomy pain control.

- May 2025: Cumberland Pharmaceuticals published results showing intravenous ibuprofen (Caldolor) is safe and effective in older surgical patients.

Global Post-Operative Pain Management Market Report Scope

As per the report's scope, post-operative pain is defined as a complex response to tissue trauma post-surgical procedures. It comprises both surgery-related pain and pain linked with central nervous system hypersensitivity. The purpose of post-operative pain management medications is to minimize adverse effects while reducing or eliminating pain and discomfort.

The segmentation of the post-operative pain management market is categorized by drug class, route of administration, surgery type, distribution channel, and geography. By drug class, the market includes opioids, NSAIDs, COX-2 inhibitors, local anesthetics, and adjuvant analgesics. By route of administration, it is segmented into injectable, oral, topical/transdermal, intrathecal/epidural, and inhalational. By surgery type, the market covers orthopedic, cardiovascular & thoracic, abdominal & gastrointestinal, obstetrics & gynecology, ophthalmic & ENT, and others. By distribution channel, it is divided into hospital pharmacies, retail pharmacies, and online pharmacies. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for all the above segments.

| Opioids |

| NSAIDs |

| COX-2 Inhibitors |

| Local Anesthetics |

| Adjuvant Analgesics |

| Injectable |

| Oral |

| Topical / Transdermal |

| Intrathecal / Epidural |

| Inhalational |

| Orthopedic |

| Cardiovascular & Thoracic |

| Abdominal & Gastrointestinal |

| Obstetrics & Gynecology |

| Ophthalmic & ENT |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Opioids | |

| NSAIDs | ||

| COX-2 Inhibitors | ||

| Local Anesthetics | ||

| Adjuvant Analgesics | ||

| By Route of Administration | Injectable | |

| Oral | ||

| Topical / Transdermal | ||

| Intrathecal / Epidural | ||

| Inhalational | ||

| By Surgery Type | Orthopedic | |

| Cardiovascular & Thoracic | ||

| Abdominal & Gastrointestinal | ||

| Obstetrics & Gynecology | ||

| Ophthalmic & ENT | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and expected value of the global post-operative pain management segment?

It is valued at USD 45.29 billion in 2026 and projected to reach USD 59.82 billion by 2031, reflecting a 5.72% CAGR.

Which drug class is expanding fastest in post-surgical pain control?

Long-acting local anesthetics are growing at an 8.25% CAGR, the highest among all classes as hospitals pivot to opioid-sparing protocols.

Why are ambulatory surgery centers so influential in post-operative pain care today?

ASCs have seen a 258% surge in total knee arthroplasties since 2020 and demand long-acting regional blocks and oral multimodal kits that support same-day discharge.

How are U.S. regulations accelerating non-opioid analgesic uptake?

CMS now reimburses qualifying non-opioid drugs separately, and FDA guidance clarifies approval endpoints, together removing previous budget and regulatory barriers.

Which region is forecast to see the quickest rise in post-operative pain therapies?

Asia-Pacific leads with a 7.42% CAGR through 2031 as China and India scale surgical capacity and adopt multimodal protocols.

What main obstacle limits wider use of premium intravenous analgesics?

Hospital cost-containment pressures and tight pharmacy budgets make the USD 300400 price tag of depot IV formulations hard to justify versus low-cost generics.

Page last updated on: