Chronic Pain Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

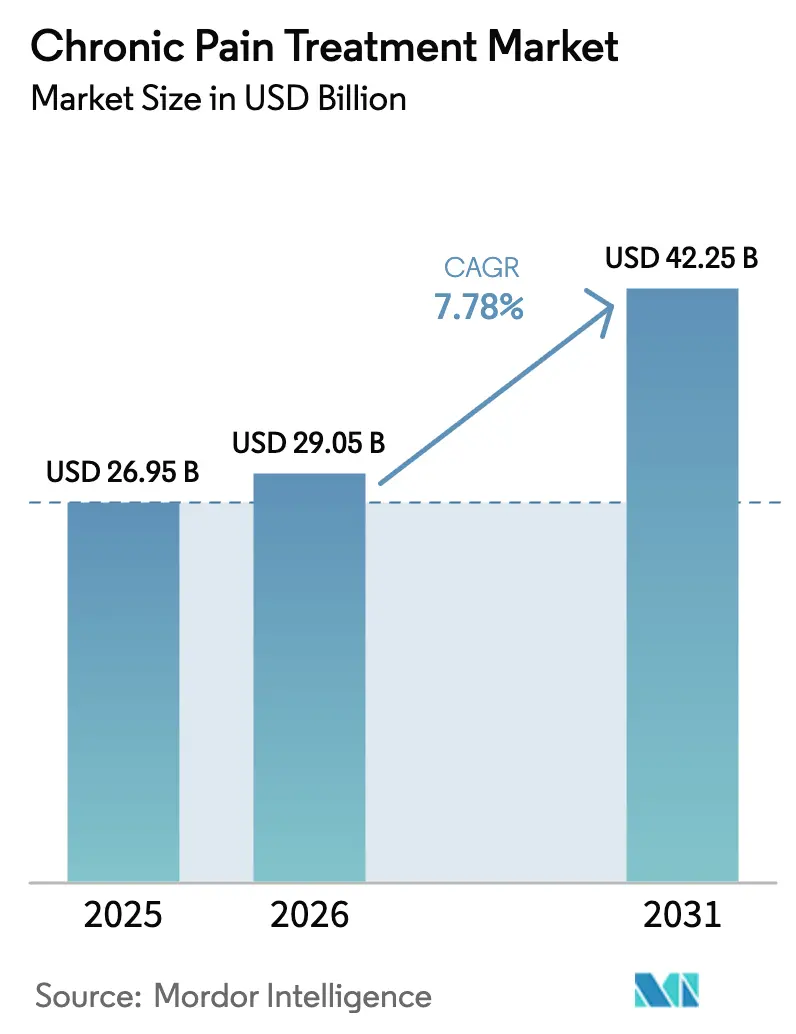

| Market Size (2026) | USD 29.05 Billion |

| Market Size (2031) | USD 42.25 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

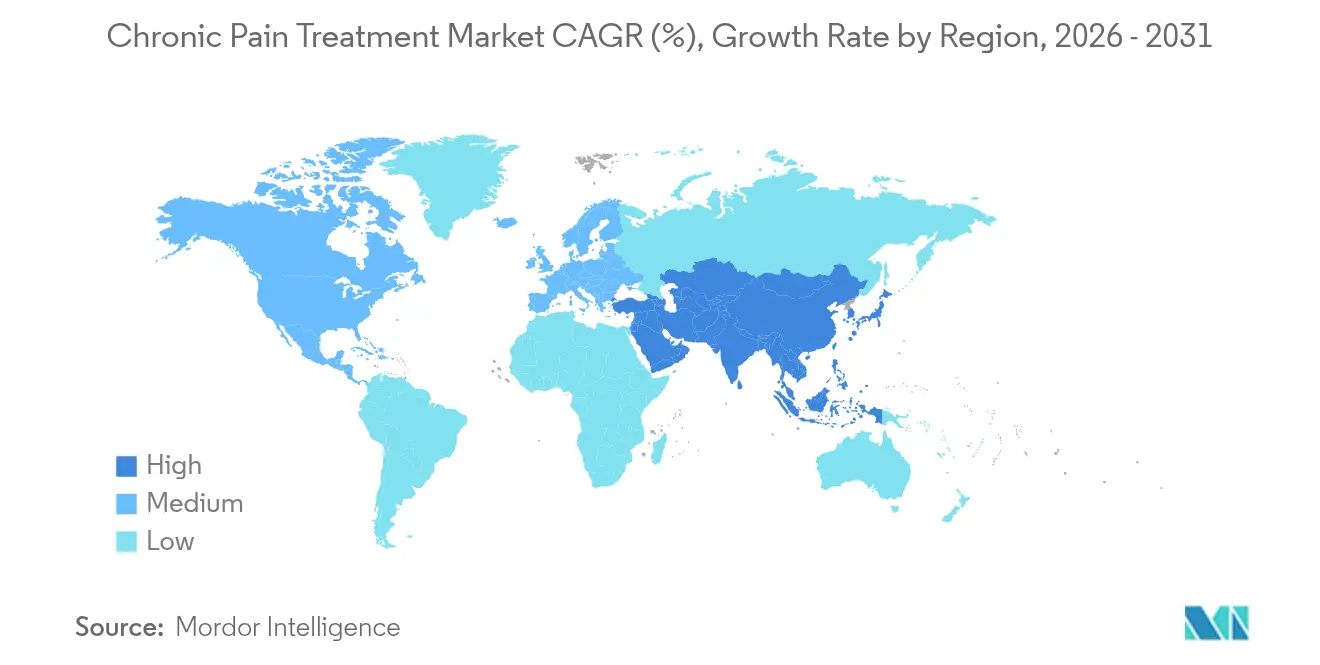

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chronic Pain Treatment Market Analysis by Mordor Intelligence

The chronic pain treatment market size was valued at USD 26.95 billion in 2025 and estimated to grow from USD 29.05 billion in 2026 to reach USD 42.25 billion by 2031, at a CAGR of 7.78% during the forecast period (2026-2031). Demand is being lifted by regulatory incentives for non-opioid options, rapid device innovation, and an aging demographic that requires long-term pain relief. Device-based therapies continued to lead revenue with 54.43% of 2024 sales, while pharmaceuticals posted the fastest expansion at an 8.25% CAGR as novel mechanisms such as highly selective sodium-channel blockers secure fast-track approvals. Opioid-substitution policies, the growth of telemedicine prescribing, and reimbursement reforms that reward non-opioid modalities are supporting additional upside. Asia-Pacific is set to narrow the historical gap with North America through healthcare modernization and rising clinical adoption of Western treatment protocols, while digital therapeutics are emerging as a measurable force in both treatment adherence and payer cost containment.

Key Report Takeaways

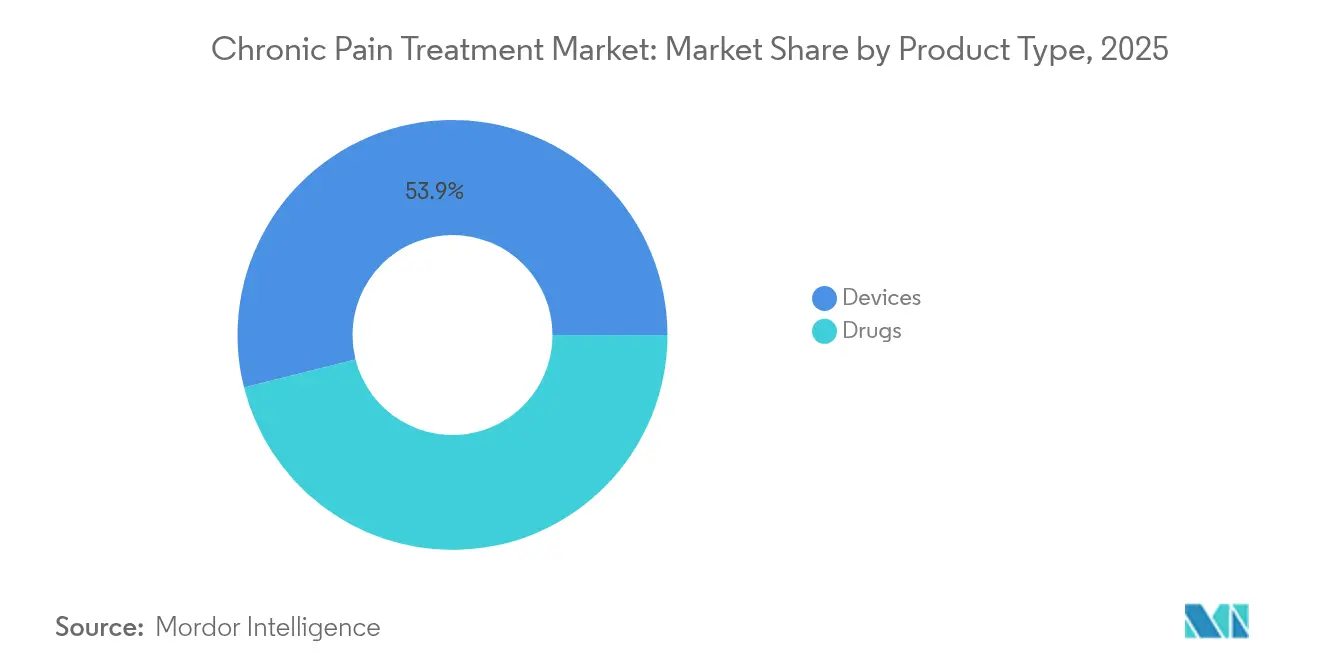

- By product type, device-based solutions captured 53.92% revenue share in 2025; pharmaceuticals are projected to grow at an 8.12% CAGR to 2031.

- By pain type, neuropathic presentations accounted for 34.10% of the 2025 chronic pain treatment market share, whereas cancer pain is advancing at an 8.48% CAGR through 2031.

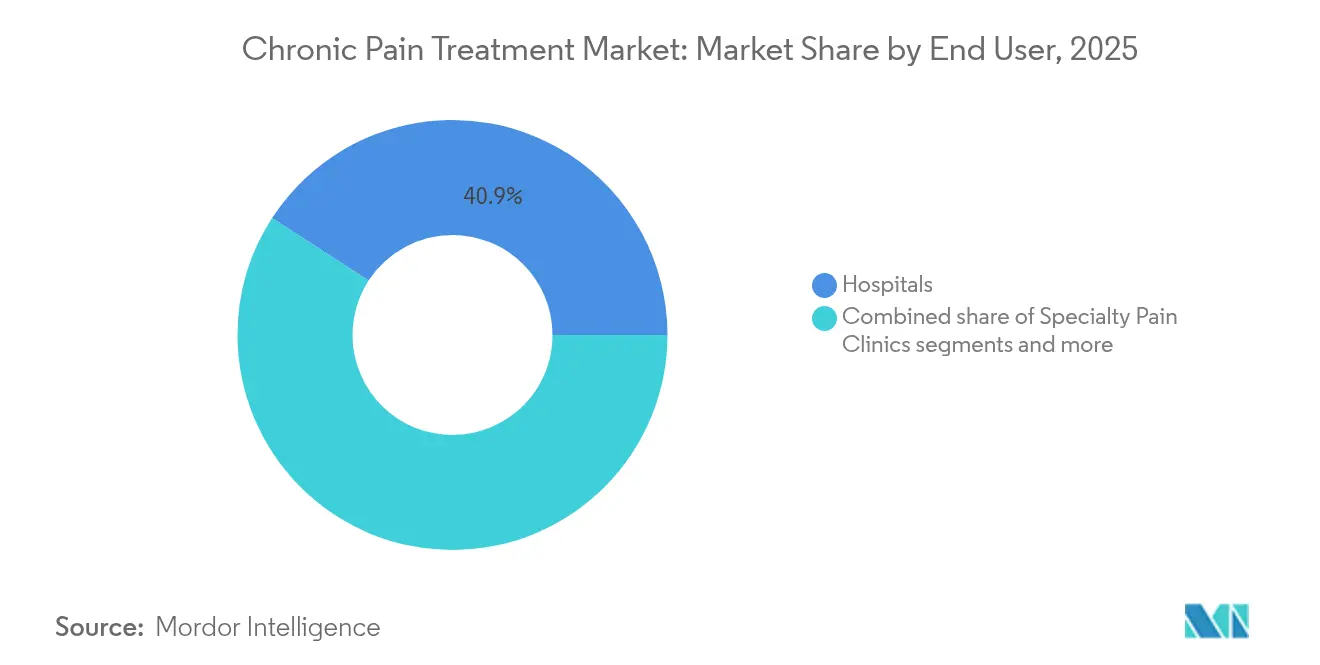

- By end user, hospitals commanded 40.85% of the 2025 chronic pain treatment market size, while specialty pain clinics are expanding at an 8.79% CAGR between 2026 and 2031.

- By distribution channel, retail pharmacies held 50.10% of 2025 revenues; online pharmacies represent the fastest growth at 9.19% CAGR to 2031.

- By geography, North America retained 41.75% revenue leadership in 2025, yet Asia-Pacific is on track for a 9.55% CAGR, the highest regional pace to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chronic Pain Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +2.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Growing geriatric population | +1.8% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Favourable reimbursement scenarios | +1.5% | North America, select European markets | Medium term (2-4 years) |

| Advancements in neuromodulation technologies | +1.3% | Global, led by North America and Europe | Medium term (2-4 years) |

| Digital therapeutics adoption | +0.9% | North America & Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Employer-driven pain-management benefits | +0.7% | North America, expanding to multinational corporations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of chronic diseases

More than 60% of U.S. adults now live with at least one long-term condition, and multimorbidity amplifies pain complexity exponentially rather than additively. European epidemiology mirrors this dynamic, with 21.45% of citizens reporting persistent pain at an annual economic burden above EUR 300 billion when productivity loss is included. Pharmaceutical pipelines are therefore shifting toward condition-specific regimens that layer anti-inflammatory, neuropathic, and behavioral elements within a single protocol.

Growing geriatric population

The 65+ cohort is expanding faster than any other age group, driving unique pharmacokinetic and polypharmacy challenges. Japan records a 22.5% chronic pain prevalence among seniors and spends almost USD 13.2 billion (2 trillion JPY) annually on direct care, spurring device manufacturers to redesign interfaces with simpler programming and larger displays.

Favourable reimbursement scenarios

The Non-Opioids Prevent Addiction in the Nation (NOPAIN) Act, effective January 2025, compels Medicare to reimburse non-opioid products separately in outpatient surgery, impacting 64 million beneficiaries and catalyzing commercial-payer parity. Pacira’s EXPAREL now bills under J0666, removing administrative friction for office-based procedures.

Advancements in neuromodulation technologies

Closed-loop spinal cord stimulators, led by Medtronic’s Inceptiv platform, lowered overstimulation events by 93% and delivered 82% pain reduction at 12 months in the latest pivotal study. AI-enabled parameter adjustment produces individualized therapy while collecting population-level data that can refine programming algorithms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory scrutiny on opioids | -1.4% | Global, most severe in North America | Short term (≤ 2 years) |

| Side-effect & addiction risks | -0.9% | Global, varying by regulatory environment | Medium term (2-4 years) |

| Limited clinician training in emerging markets | -0.6% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Social stigma around psychological therapies | -0.4% | Asia-Pacific, Middle East, select European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory scrutiny on opioids

The U.S. FDA required new boxed warnings in July 2025, obligating manufacturers to highlight addiction risk, overdose potential, and contraindications for long-term use[1]. Parallel DEA quota cuts continue to shrink national supply by 15% annually, compelling clinicians to prioritize alternative modalities. Priority-review lanes for non-opioid products further tilt the regulatory balance toward device, biologic, and digital solutions.

Side-effect & addiction risks

Patients and providers share growing reluctance around therapies with severe gastrointestinal, cognitive, or dependence profiles. Clinical programs such as Vertex’s VX-993 were abandoned despite acceptable safety because they failed to clear the heightened efficacy threshold regulators now demand[2]Source: Vertex Pharmaceuticals, “Suzetrigine FDA Approval Press Release,” vrtx.com . Rising consumer interest in unregulated botanicals like kratom underscores unmet needs but also introduces new safety challenges, prompting the FDA to increase import alerts on high-alkaloid strains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Retain Leadership While Drugs Accelerate

The device segment contributed 53.92% of 2025 revenue, giving it the largest chronic pain treatment market share. Neuromodulation systems uphold much of this weight, and the new closed-loop generation is positioned to widen clinical preference over open-loop predecessors. Ablation technologies have gained new life through cooled-radiofrequency and focused-ultrasound offerings that improve lesion precision. Intrathecal pumps, now reporting 99% mechanical survival after one year, are capturing opioid-reduction protocols in cancer centers.

Pharmaceutical growth, though starting from a smaller base, surpassed devices at an 8.12% CAGR to 2031. Sodium-channel blockers such as suzetrigine provide opioid-equivalent analgesia without central-nervous-system receptor interaction. Formulation science is redirecting NSAIDs into nano-encapsulated depots that localize drug exposure, reducing systemic side-effect load. Muscle relaxants like tizanidine are scaling quickly in geriatric cohorts due to safer sedation profiles relative to benzodiazepines.

By Pain Type: Neuropathic Prevalence Meets Oncology-Driven Growth

Neuropathic conditions accounted for 34.10% of 2025 revenue, the single-largest slice of the chronic pain treatment market size. Diabetes-linked peripheral neuropathy and post-herpetic neuralgia dominate volumes, while chemotherapy-induced variants add a rising share from expanding survivorship pools. Cancer pain, although smaller today, is forecast to grow at 8.48% CAGR, the fastest in the field. Longer oncology survival exposes patients to chronic treatment courses, and guideline revisions now recommend earlier adoption of multimodal regimens that pair sustained-release local anesthetics with neuromodulation.

Musculoskeletal pain maintains the highest incident case load but assigns lower per-patient revenue, making it a prime target for high-value, low-cost cryoneurolysis systems. Fibromyalgia and migraine are benefiting from digital therapeutic approvals that deliver cognitive behavioral content via VR headset, often in lieu of systemically acting drugs.

By End User: Hospitals Hold Scale, Clinics Post Pace

Hospitals delivered 40.85% of 2025 sales thanks to high-acuity cases and implant procedures. However, specialty pain clinics are projected to expand at an 8.79% CAGR, reflecting economic incentives to shift elective interventions to lower-cost outpatient environments. Dedicated centers integrate pharmacologic, device, and behavioral offerings under one roof, demonstrating lower readmission rates and higher patient-reported outcomes.

Homecare is achieving stable single-digit growth as miniaturized pumps and wearable stimulators extend sophisticated therapy beyond institutional walls. Ambulatory surgical centers, though still the smallest share, are trending upward rapidly on the back of streamlined reimbursement and shorter scheduling lead times.

By Distribution Channel: E-Commerce Rewrites Fulfillment

Retail pharmacies preserved 50.10% of 2025 revenue by combining extensive physical networks with in-person counseling. Yet the online channel, growing at 9.19% CAGR, is the clear disruptor. E-pharmacies leverage telehealth prescriptions, discrete packaging, and subscription pricing to win refills. Specialty pharmacies are emerging to handle biologics and devices that involve complex cold-chain and training requirements—areas where generalist chains struggle.

Direct-to-consumer strategies likewise surfaced, with manufacturers operating virtual clinics that deliver personalized dosage titrations and on-demand nurse support. The chronic pain treatment market is therefore aligning fulfillment architecture with patient preference for convenience and payers’ appetite for lower total cost of care.

Geography Analysis

North America secured 41.75% of 2025 revenue, owing to robust reimbursement and continuous regulatory encouragement of non-opioid solutions. Market expansion is easing as penetration nears maturity, yet innovation throughput remains highest in the United States, where priority-review designations for breakthrough devices and drugs shorten commercialization timelines by 25% on average. Canada’s universal coverage supports steady device adoption, especially for spinal cord stimulators, while domestic manufacturers benefit from favorable R&D tax credits.

Europe follows with strong universal-payer backing that prizes long-term outcomes over immediate unit cost. Implementation of the EU Health Technology Assessment Regulation in 2025 begins a mandatory joint-clinical-assessment process that should harmonize evidence thresholds across member states, thereby reducing duplication and accelerating market entry for innovators. Germany leads synchronous digital-therapeutic reimbursement under the DiGA framework, while France and the United Kingdom expand multidisciplinary pain centers inside public hospitals.

Asia-Pacific is projected for the fastest regional growth at 9.55% CAGR to 2031. Japan’s high prevalence and associated USD 13.2 billion direct annual spend underscore the urgency of scalable solutions. China accelerated device approvals through its Hainan Real-World Evidence pilot, allowing foreign companies early access before nationwide listing. India’s National Digital Health Mission creates a framework for e-prescription and remote-monitoring reimbursement, setting the stage for online pharmacy growth. Clinician shortages, however, still limit uptake in secondary cities, placing a ceiling on near-term revenue.

South America and the Middle East & Africa remain nascent but promising. Brazil is adding neuromodulation coverage to its supplemental insurance plans, whereas Saudi Arabia’s Vision 2030 health reforms include pain-management specialty certification tracks. Infrastructure constraints and economic volatility temper the immediate outlook, yet early-stage clinics already report double-digit annual procedure growth.

Competitive Landscape

Market concentration is moderate. Multinational pharmaceuticals such as Pfizer, Johnson & Johnson, and Eli Lilly rely on extensive commercial footprints and payer contracting leverage, though their opioid portfolios are in structural decline. Device majors—including Medtronic, Boston Scientific, and Abbott—invest heavily in firmware and cloud-integration features that fetch premium pricing and generate recurring service revenues. The January 2025 approval of Vertex’s suzetrigine illustrates how a mid-cap innovator can reset therapeutic expectations and rapidly attain preferred-formulary status.

Consolidation is accelerating. Globus Medical’s February 2025 acquisition of Nevro for USD 250 million merges orthopedic hardware with neuromodulation IP, enabling single-vendor spinal repair and pain-relief solutions. Similar vertical pairings are expected as payers steer towards bundled payments covering surgery and chronic-phase management in one package. Digital-therapeutic entrants such as AppliedVR target chronic low-back pain and fibromyalgia, positioning themselves as adjuncts that can delay costly device implantation.

Intellectual-property cliffs on widely prescribed antidepressants and anticonvulsants invite generic erosion, motivating incumbents to pivot toward abuse-deterrent formulations and combination products. Collaborative research agreements between device and pharma companies now span sensor-enabled injectable depots that sync with stimulation cycles, opening the door to titrated multimodal regimens.

Chronic Pain Treatment Industry Leaders

Pfizer Inc.

Medtronic PLC

Abbott Laboratories

Novartis AG

Becton, Dickinson, and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Globus Medical completed acquisition of Nevro Corporation for USD 250 million, integrating spinal hardware and neuromodulation capabilities

- January 2025: The U.S. FDA approved Journavx (suzetrigine) from Vertex Pharmaceuticals, the first new analgesic class in more than two decades

Global Chronic Pain Treatment Market Report Scope

As per the scope of this report, encompasses a range of treatments, including pharmaceuticals and medical devices, aimed at alleviating persistent pain conditions that significantly impact patients' quality of life. The chronic pain treatment market is segmented by product type, application, end-user, and geography. The product type segment is further divided into drugs, and devices. The drugs segment is further segmented into Non-Narcotic Analgesics. The Non-Narcotic Analgesics segment is further divided into non-Steroidal anti-Inflammatory drugs, anesthetics, anticonvulsants, antidepressants, and other non-narcotic analgesics. The device segment is further divided into neurostimulation devices, and analgesic infusion umps. The neurostimulation devices segment is further segmented into transcutaneous electrical nerve stimulation devices, and brain and spinal cord stimulation devices. The analgesic infusion pumps segment is further divided into intrathecal infusion umps, and external infusion pumps. The application segment is further segmented into neuropathic pain, arthritic pain, post-surgical pain, cancer pain, and others . The other application is further divided into joint pain, musculoskeletal pain, among others. The end-user segment is divided into hospitals, clinics, and other end-users. The geography segment is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Drugs | NSAIDs | |

| Opioids | ||

| Antidepressants | ||

| Anticonvulsants | ||

| Muscle Relaxants | ||

| Others | ||

| Devices | Neuromodulation Devices | Spinal Cord Stimulators |

| Peripheral Nerve Stimulators | ||

| Dorsal Root Ganglion Stimulators | ||

| Ablation Devices | Radiofrequency Ablation Devices | |

| Cryoablation Devices | ||

| Implantable Intrathecal Pumps | ||

| Neuropathic Pain |

| Musculoskeletal / Orthopedic Pain |

| Cancer Pain |

| Fibromyalgia |

| Migraine & Headache Pain |

| Others |

| Hospitals |

| Specialty Pain Clinics |

| Homecare Settings |

| Ambulatory Surgical Centers |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Drugs | NSAIDs | |

| Opioids | |||

| Antidepressants | |||

| Anticonvulsants | |||

| Muscle Relaxants | |||

| Others | |||

| Devices | Neuromodulation Devices | Spinal Cord Stimulators | |

| Peripheral Nerve Stimulators | |||

| Dorsal Root Ganglion Stimulators | |||

| Ablation Devices | Radiofrequency Ablation Devices | ||

| Cryoablation Devices | |||

| Implantable Intrathecal Pumps | |||

| By Pain Type (Value) | Neuropathic Pain | ||

| Musculoskeletal / Orthopedic Pain | |||

| Cancer Pain | |||

| Fibromyalgia | |||

| Migraine & Headache Pain | |||

| Others | |||

| By End User (Value) | Hospitals | ||

| Specialty Pain Clinics | |||

| Homecare Settings | |||

| Ambulatory Surgical Centers | |||

| By Distribution Channel (Value) | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online Pharmacies | |||

| By Geography (Value) | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

How large is the chronic pain treatment market in 2026?

The chronic pain treatment market size stands at USD 29.05 billion in 2026.

What is the forecast growth rate through 2031?

The sector is projected to expand at a 7.78% CAGR, reaching USD 42.25 billion by 2031.

Which product category leads current revenue?

Device-based therapies hold 53.92% of 2025 revenue, led by neuromodulation systems.

Which pain type is growing fastest?

Cancer-related pain is expected to rise at an 8.48% CAGR through 2031 due to improved oncology survival.

Which region will experience the highest growth?

Asia-Pacific is forecast for a 9.55% CAGR to 2031, the highest regional pace.

How will reimbursement trends influence adoption?

Medicare's NOPAIN Act payments for non-opioid modalities are accelerating outpatient uptake and prompting commercial-payer alignment.

Page last updated on: