Neuropathic Pain Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

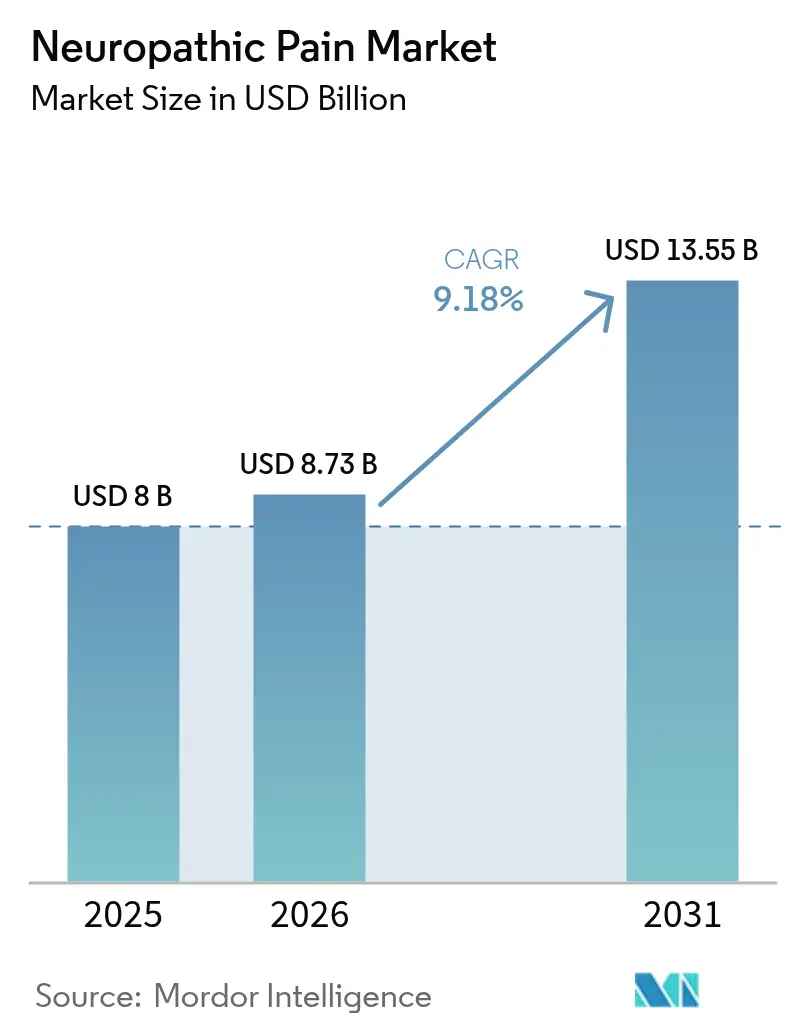

| Market Size (2026) | USD 8.73 Billion |

| Market Size (2031) | USD 13.55 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

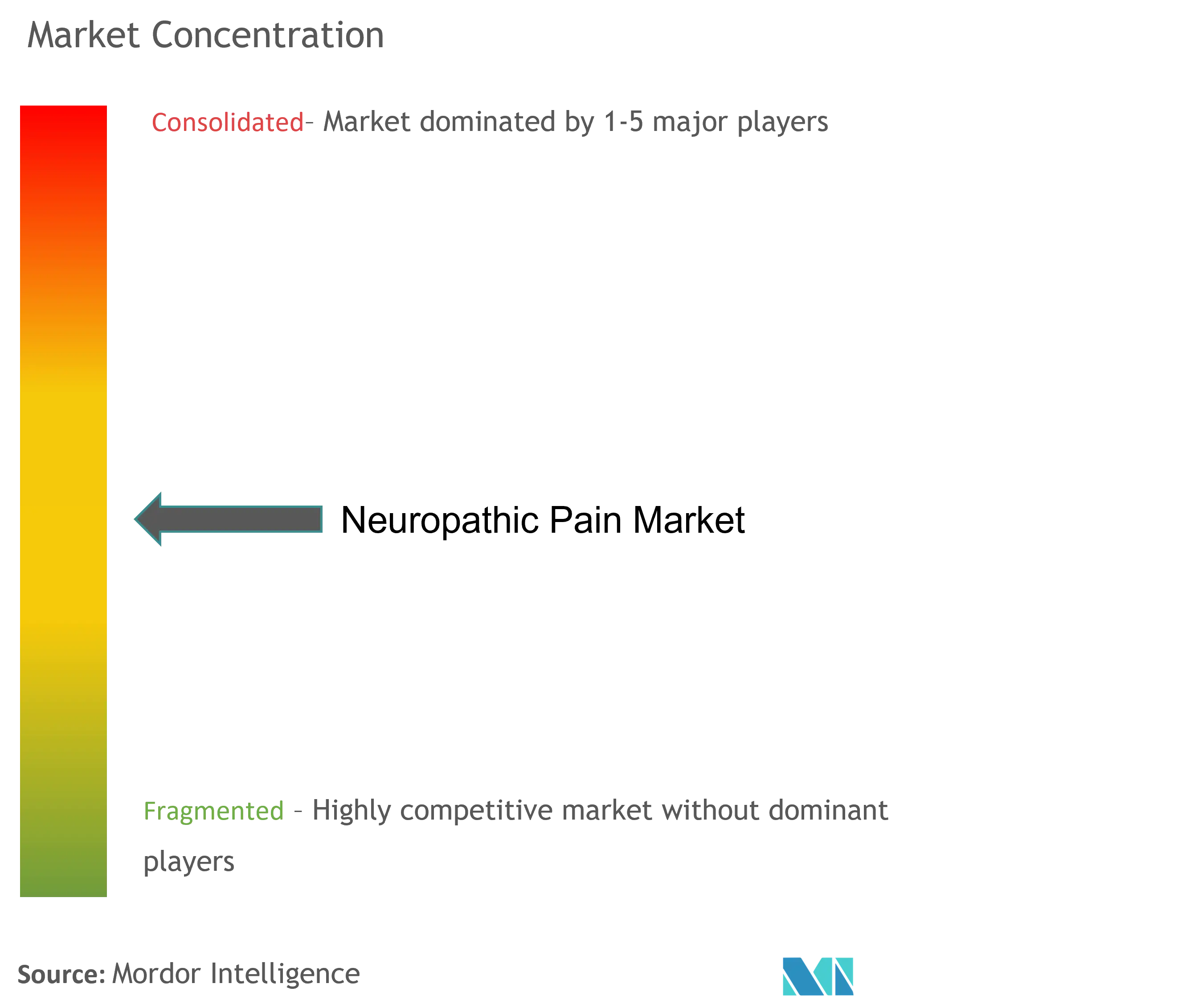

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neuropathic Pain Market Analysis by Mordor Intelligence

Neuropathic Pain market size in 2026 is estimated at USD 8.73 billion, growing from 2025 value of USD 8.00 billion with 2031 projections showing USD 13.55 billion, growing at 9.18% CAGR over 2026-2031.

Escalating prevalence of diabetes, cancer survivorship and viral infections is enlarging the treated population, while regulators, payers and clinicians increasingly favour non-opioid options that lower abuse risk. Evidence from real-world prescription audits shows a steady shift away from centrally acting painkillers toward peripherally selective agents, hinting at a structural rebalancing of Neuropathic Pain market share. Pipeline diversity spanning small-molecule sodium-channel blockers, biologic nerve-growth-factor antagonists and advanced topical formulations underscores commercial confidence in mechanism-based differentiation. An additional observation is that the fastest uptake is occurring in provider settings able to measure functional gains, suggesting that outcome-linked reimbursement is already shaping treatment choices.

Key Take Aways

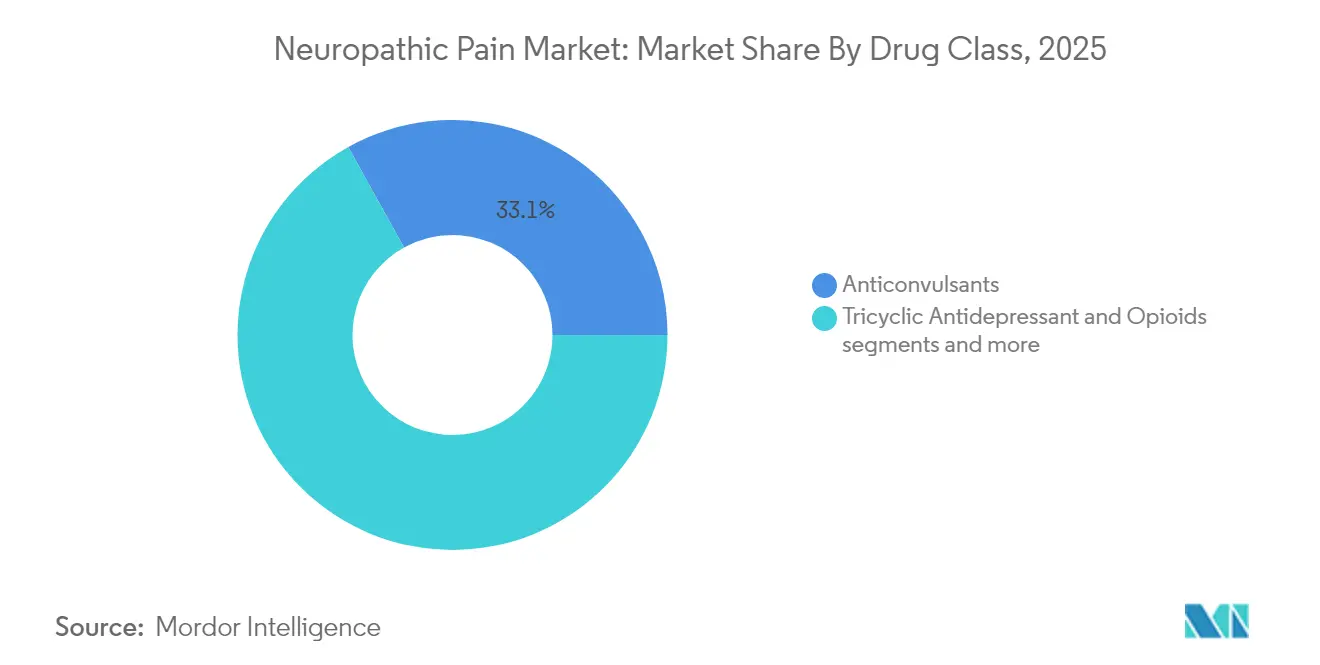

- By drug class, anticonvulsants commanded a 33.05 % revenue share in 2025, whereas topical formulations are forecast to expand at a 9.78 % CAGR through 2031

- By indication, diabetic peripheral neuropathy accounted for 31.88 % of 2025 sales, whereas chemotherapy-induced peripheral neuropathy is projected to grow at an 11.05 % CAGR through 2031

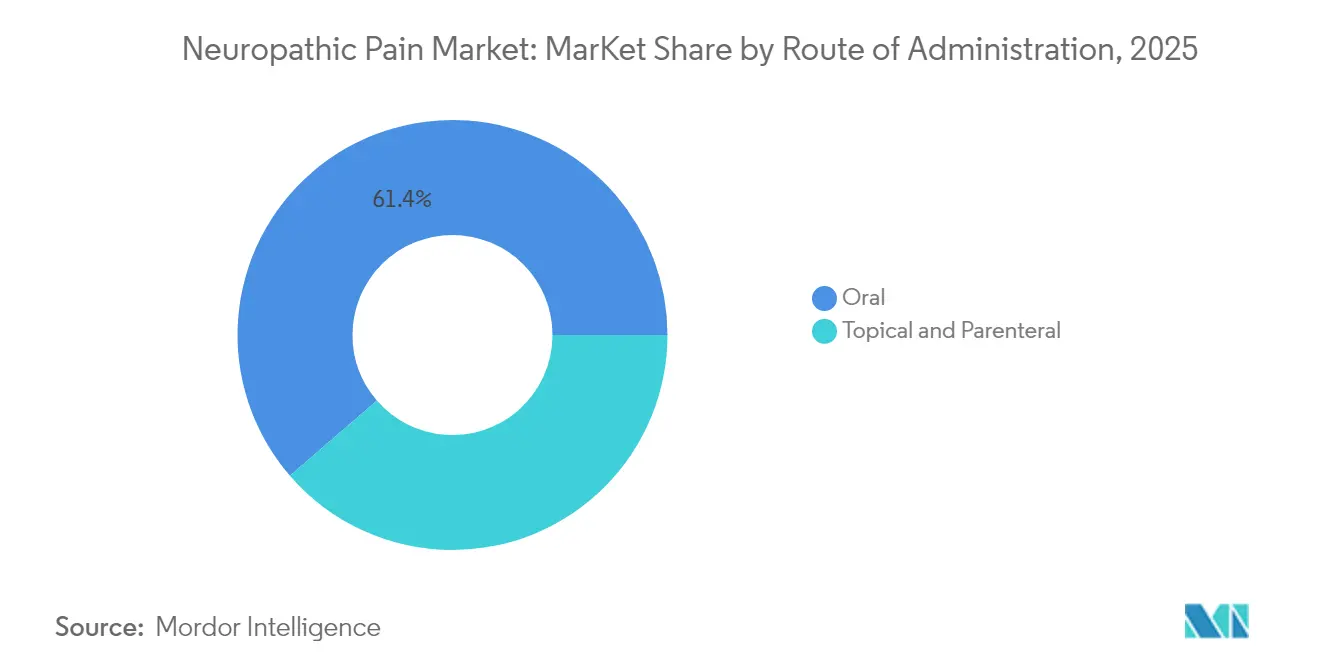

- By route of administration, oral therapies led with 61.35 % revenue share in 2025, whereas topical delivery is expected to advance at a 11.54 % CAGR through 2031

- By geography, North America dominated with 41.90 % market share in 2025, whereas Asia-Pacific is forecast to expand at a 11.88 % CAGR through 2031

- By distribution channel, hospital pharmacies captured 41.72 % of 2025 revenues, whereas online pharmacies are poised to grow at an 11.42 % CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neuropathic Pain Market Trends and Insights

Driver Impact Analysis*

| Driver | ~% Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Growing Global Prevalence of Diabetes & Obesity | ~2.1% | Global, with highest impact in APAC and MEA | Medium term (~ 3-4 yrs) |

| Increasing Cancer Survival Rates Elevating CIPN Burden | ~1.8% | North America & EU primarily, expanding to APAC | Long term (≥ 5 yrs) |

| Rapid Clinical Adoption of Next-Generation Sodium-Channel Blockers | ~2.3% | North America early adoption, EU and APAC follow | Short term (≤ 2 yrs) |

| Accelerating R&D Investments in Non-Opioid Analgesics | ~1.6% | Global, concentrated in North America and EU | Medium term (~ 3-4 yrs) |

| Expanding Availability of Long-Acting Topical Formulations | ~1.4% | Global, with faster uptake in developed markets | Medium term (~ 3-4 yrs) |

| Favorable Global Reimbursement & HTA Outcomes | ~1.2% | North America & EU primarily, gradual APAC expansion | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Growing Global Prevalence of Diabetes & Obesity Driving Diabetic Peripheral Neuropathy

The escalating global diabetes epidemic is fundamentally reshaping the neuropathic pain landscape, with diabetic peripheral neuropathy (DPN) affecting approximately 50% of diabetic patients. This high prevalence translates to a substantial patient population requiring effective pain management solutions. Recent epidemiological studies reveal that DPN is often underdiagnosed, with 75% of cases remaining undetected until symptoms become severe, creating a significant untapped market opportunity Elafros et al.. The economic burden of DPN extends beyond direct treatment costs, as patients with painful DPN experience reduced productivity and higher healthcare utilization across multiple specialties, driving demand for more effective and tolerable treatment options that can improve functional outcomes while minimizing side effects.

Increasing Cancer Survival Rates Elevating Chemotherapy-Induced Peripheral Neuropathy Burden

As cancer treatment efficacy improves, the population of survivors experiencing chemotherapy-induced peripheral neuropathy (CIPN) continues to expand, creating an urgent need for effective management strategies. CIPN affects 30-40% of patients receiving neurotoxic chemotherapy agents, with symptoms often persisting long after treatment completion Dove Press. The condition significantly impacts quality of life and may necessitate chemotherapy dose reductions, potentially compromising oncological outcomes. Recent advances in understanding CIPN pathophysiology have revealed the role of oxidative stress and neuroinflammation, opening new therapeutic avenues beyond traditional analgesics. Biomarker development for early CIPN detection is gaining momentum, with neurotrophic factors and microRNAs showing promise for identifying high-risk patients Widyadharma. This trend could potentially reduce the addressable market for CIPN treatments, as preventive interventions might decrease the incidence of severe cases requiring pharmaceutical management. Pharmaceutical companies face the strategic challenge of balancing innovation in treatment with the market-constraining effects of improved prevention and early intervention strategies.

Rapid Clinical Adoption of Next-Generation Sodium-Channel Blockers & NGF Antagonists

The therapeutic landscape for neuropathic pain is undergoing a fundamental transformation with the emergence of highly selective sodium channel blockers that target peripheral pain pathways while minimizing central nervous system effects. The FDA approval of suzetrigine (Journavx) in January 2025 as the first selective NaV1.8 inhibitor marks a watershed moment in pain management Vertex Pharmaceuticals. This breakthrough addresses the longstanding challenge of developing non-opioid analgesics with favorable safety profiles. Concurrently, nerve growth factor (NGF) antagonists are advancing through late-stage clinical development, offering a complementary approach by targeting the neuroinflammatory component of neuropathic pain. The pipeline diversity suggests a future treatment paradigm characterized by mechanism-based prescribing rather than the current symptom-based approach, potentially improving outcomes through more precise targeting of underlying pathophysiology

Accelerating R&D Investments in Non-Opioid Analgesics by Big Pharma & Biotech

The urgent need for safer pain management alternatives has catalyzed unprecedented investment in non-opioid analgesic development across the pharmaceutical industry. Major players are strategically repositioning their neuroscience portfolios to capitalize on the growing demand for effective neuropathic pain treatments without abuse potential. Pfizer is advancing PF-05089771, a selective Nav1.7 inhibitor targeting diabetic peripheral neuropathy and other neuropathic pain conditions PatSnap. This investment surge extends beyond traditional pharmaceutical approaches to include innovative modalities such as gene therapy, which has shown promise in preclinical models of neuropathic pain by delivering transgenes that produce GABA, effectively blocking pain signals without detectable side effects University of California - San Diego. The diversification of therapeutic approaches reflects a strategic recognition that addressing the complex pathophysiology of neuropathic pain requires multiple mechanistic angles

Restraint Impact Analysis*

| Restraint | ~% Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Safety Concerns & Abuse Potential Limiting Opioid and Gabapentinoid Utilization | ~-1.8% | Global, most pronounced in North America | Short term (≤ 2 yrs) |

| Patent Expirations of Blockbuster Therapies Driving Price Erosion | ~-1.3% | Global, with highest impact in developed markets | Medium term (~ 3-4 yrs) |

| Stringent Regulatory Requirements Delaying Approval of Novel Analgesics | ~-1.6% | North America & EU primarily, expanding to APAC | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Safety Concerns & Abuse Potential Limiting Opioid and Gabapentinoid Utilization

The clinical utility of traditional neuropathic pain treatments is increasingly constrained by mounting safety concerns and regulatory scrutiny. Opioids, despite their analgesic efficacy, face severe prescribing restrictions due to their high abuse potential and the ongoing public health crisis associated with opioid misuse. Gabapentinoids (pregabalin and gabapentin), while effective for many neuropathic pain conditions, are encountering growing regulatory oversight due to emerging evidence of misuse potential and dependence issues. These safety challenges are driving a fundamental market shift toward treatments with improved risk-benefit profiles. The development of peripherally-acting analgesics that do not cross the blood-brain barrier represents a strategic response to these concerns, offering pain relief without central nervous system effects that contribute to abuse potential NIH. This safety-driven market evolution is creating opportunities for novel therapeutic approaches that can maintain efficacy while addressing the limitations of current standard-of-care treatments.

Patent Expirations of Blockbuster Therapies Driving Price Erosion & Generic Entry

The neuropathic pain market is experiencing significant competitive reconfiguration as key patents for established therapies expire, triggering generic entry and price erosion across multiple drug classes. This dynamic is particularly pronounced in the anticonvulsant segment, where pregabalin and gabapentin face intensifying generic competition. The resulting price pressure is compelling innovator companies to redirect their strategic focus toward novel mechanisms and differentiated formulations that can command premium pricing. Concurrently, the generic availability of established treatments is expanding access in price-sensitive markets, particularly in developing regions where cost barriers have historically limited treatment options. This market evolution is creating a bifurcated competitive landscape with commodity-like dynamics for off-patent molecules and premium positioning opportunities for truly innovative approaches with demonstrable advantages over existing options. The strategic imperative for pharmaceutical companies is increasingly centered on developing treatments with clear mechanistic differentiation and compelling value propositions that can justify premium pricing in an increasingly cost-conscious healthcare environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Anticonvulsants Lead By Drug Class

Anticonvulsants command the largest market share at 33.05% in 2025, with pregabalin and gabapentin serving as cornerstone therapies due to their established efficacy across multiple neuropathic pain conditions. Their mechanism of action, primarily involving calcium channel modulation and enhanced GABA activity, effectively addresses the hyperexcitability that characterizes neuropathic pain states. Recent comparative analyses reveal that pregabalin demonstrates superior pain reduction and fewer adverse events compared to gabapentin, potentially explaining its growing preference among clinicians Mayoral et al.. Despite their dominance, anticonvulsants face challenges from emerging drug classes with potentially superior safety profiles and more targeted mechanisms. Topical agents represent the fastest-growing segment with a 9.78% CAGR (2026-2031), driven by their favorable risk-benefit profile, particularly for localized neuropathic pain. SNRIs maintain significant market presence due to duloxetine's established efficacy in diabetic peripheral neuropathy, while opioids face declining utilization amid safety concerns and regulatory restrictions. The "Other Classes" segment, including NMDA antagonists and cannabinoids, shows promising growth potential as research advances on novel mechanisms targeting neuropathic pain pathways.

The competitive dynamics within drug classes are evolving as pharmaceutical companies strategically reposition their portfolios toward differentiated mechanisms. Emerging evidence suggests that combination approaches targeting multiple pain pathways simultaneously may offer superior outcomes compared to monotherapy, potentially reshaping treatment algorithms Kumar et al.. This trend is driving increased interest in rational polypharmacy and fixed-dose combinations that can address the complex pathophysiology of neuropathic pain while minimizing individual drug side effects. The recent approval of novel agents like suzetrigine signals a potential paradigm shift toward mechanism-based prescribing rather than the current symptom-based approach, which could fundamentally alter market share distribution across drug classes in the coming years.

Indication: Diabetic Peripheral Neuropathy Leads Market Transformation

Diabetic peripheral neuropathy (DPN) dominates the indication landscape with 31.88% market share in 2025, reflecting its high prevalence among the growing diabetic population worldwide. The condition affects approximately 50% of patients with diabetes duration exceeding 10 years, creating a substantial and expanding patient pool. Treatment approaches for DPN are evolving beyond symptom management to address underlying pathophysiological mechanisms, with increasing focus on disease-modifying therapies that can prevent or slow neuropathy progression. Chemotherapy-induced peripheral neuropathy (CIPN) represents the fastest-growing indication segment with an 11.05% CAGR (2026-2031), driven by improving cancer survival rates and growing recognition of CIPN's impact on quality of life. Postherpetic neuralgia maintains significant market share due to its distinctive pathophysiology and treatment challenges, while trigeminal neuralgia represents a smaller but therapeutically distinct segment with specific treatment algorithms.

The indication landscape is being reshaped by advances in diagnostic capabilities and biomarker development that enable earlier intervention and more precise patient stratification. Recent research has identified potential biomarkers for CIPN, including neurotrophic factors and microRNAs, which could facilitate preventive strategies in high-risk patients Widyadharma. For HIV-associated neuropathy, antiretroviral therapy optimization is increasingly recognized as a critical component of management alongside direct pain interventions. Phantom limb pain is benefiting from innovative approaches, including the FDA-approved Altius Direct Electrical Nerve Stimulation System, which demonstrated significant pain reduction in clinical studies FDA. These advances in indication-specific approaches are driving market segmentation and creating opportunities for targeted therapies that address the unique pathophysiological features of each neuropathic pain condition.

Route of Administration: Oral Dominance Challenged by Topical Innovation

Oral administration continues to dominate the neuropathic pain market with 61.35% share in 2025, reflecting the established position of systemic therapies like anticonvulsants and antidepressants in treatment guidelines worldwide. The convenience and familiarity of oral dosing for both patients and prescribers sustain this dominance despite challenges from alternative routes. Topical administration represents the fastest-growing segment with a 11.54% CAGR (2026-2031), driven by innovations in drug delivery technology and growing recognition of the benefits of localized therapy. High-concentration capsaicin patches (8% w/w) have demonstrated particular efficacy in various neuropathic pain conditions, with clinical studies showing significant pain reduction and improved quality of life . The appeal of topical agents extends beyond efficacy to their favorable safety profile, particularly in elderly patients with multiple comorbidities and polypharmacy concerns.

Parenteral administration maintains a specialized but critical role in the treatment algorithm, particularly for refractory cases and specific indications. The updated 2024 PACC guidelines for PRIALT (ziconotide) administration highlight the importance of intrathecal therapy for severe chronic pain unresponsive to other treatments Tersera Therapeutics. Emerging technologies are expanding the potential of each administration route, with extended-release oral formulations improving convenience and adherence, while advanced topical delivery systems enhance drug penetration and duration of action. The strategic focus on developing non-systemic delivery approaches reflects growing recognition of the benefits of targeted therapy that maximizes local efficacy while minimizing systemic exposure and associated adverse effects. This trend is expected to continue reshaping the route of administration landscape, with increasing market share for topical and novel delivery systems at the expense of traditional oral formulations.

Distribution Channel: Hospital Pharmacies Lead Amid Digital Transformation

Hospital pharmacies maintain market leadership with 41.72% share in 2025, leveraging their integrated care model and specialized expertise in managing complex neuropathic pain cases. Their dominant position is reinforced by their role in initiating therapy for severe or refractory pain, particularly for treatments requiring specialized administration or monitoring. Retail pharmacies continue to play a crucial role in maintenance therapy and community-based care, benefiting from their accessibility and established patient relationships.

The distribution landscape is evolving in response to changing patient expectations and healthcare delivery models. Convenience, availability, and price advantages consistently enhance online medication purchase intentions, creating competitive pressure on traditional brick-and-mortar channels . The recent launch of Journavx in retail pharmacies marks a strategic move to enhance access to innovative pain treatments in community settings Chain Drug Review. Hospital pharmacies are responding to competitive pressures by enhancing their value proposition through specialized pain management services and integrated care coordination. The evolving distribution dynamics reflect broader healthcare trends toward patient-centered care and seamless integration across care settings, with implications for market access strategies and channel optimization for neuropathic pain therapies.

Geography Analysis

North America dominates the neuropathic pain market with 41.90% share in 2025, driven by high disease prevalence, advanced healthcare infrastructure, and favorable reimbursement policies. The region's leadership position is reinforced by its role as the primary launch market for innovative therapies, exemplified by the recent FDA approval of Journavx (suzetrigine) as the first new analgesic class in over two decades FDA. The implementation of the NOPAIN Act represents a significant policy advancement, creating reimbursement pathways specifically for non-opioid pain management in outpatient settings Vertex Pharmaceuticals. This regulatory tailwind is expected to accelerate market access for novel neuropathic pain therapies, particularly those with demonstrated advantages over existing options. The United States accounts for the largest share within North America, reflecting its substantial patient population and high healthcare expenditure, while Canada and Mexico contribute significantly to regional growth through expanding access programs and improving diagnostic capabilities.

Europe represents the second-largest regional market, characterized by strong healthcare systems and comprehensive reimbursement frameworks that facilitate access to advanced neuropathic pain therapies. The region's market dynamics are shaped by stringent health technology assessment processes that emphasize comparative effectiveness and cost-utility, driving demand for treatments with demonstrable advantages over existing options. The United Kingdom and Germany lead in adoption of innovative therapies, while France, Italy, and Spain maintain substantial market shares due to their large patient populations and established pain management infrastructure. Recent European approvals of novel treatments and devices, including advanced spinal cord stimulation systems, reflect the region's commitment to expanding therapeutic options for neuropathic pain patients Medtronic.

Asia-Pacific represents the fastest-growing regional market with a 11.88% CAGR (2026-2031), driven by increasing disease prevalence, improving healthcare access, and rising healthcare expenditure. China leads regional growth with expanding insurance coverage and significant investments in healthcare infrastructure, while Japan contributes substantial market share through its advanced healthcare system and aging population with high neuropathic pain prevalence. India is emerging as a key growth market due to its large diabetic population and improving diagnostic capabilities, though access challenges persist in rural areas. The region is witnessing increasing adoption of traditional medicine approaches alongside conventional therapies, with recent research highlighting the potential of traditional Chinese medicine in treating neuropathic pain Zhang et al.. South Korea's market is characterized by rapid technology adoption and strong pharmaceutical research capabilities, contributing to regional innovation. The Middle East & Africa and South America regions represent smaller but growing markets, with improving healthcare infrastructure and increasing disease awareness driving expansion from a lower base.

Competitive Landscape

The neuropathic pain market exhibits moderate concentration with established pharmaceutical companies maintaining significant market share while facing disruption from innovative entrants with novel mechanisms of action. Traditional leaders including Pfizer, GlaxoSmithKline, and Eli Lilly leverage their extensive neuroscience portfolios and global commercial infrastructure to maintain strong positions across multiple drug classes and geographies. The competitive dynamics are evolving as patent expirations for key products drive generic entry and price erosion, compelling innovator companies to redirect strategic focus toward differentiated mechanisms and formulations. Vertex Pharmaceuticals has emerged as a disruptive force with the January 2025 FDA approval of Journavx (suzetrigine), the first selective NaV1.8 inhibitor for pain, priced at USD 15.50 per 50 mg tablet with projected first-year sales of USD 110 million.

Strategic patterns reveal increasing focus on mechanism-based differentiation rather than incremental improvements to existing drug classes, reflecting recognition that addressing the complex pathophysiology of neuropathic pain requires novel approaches. Companies are pursuing targeted acquisitions and partnerships to access innovative technologies and expand therapeutic capabilities, exemplified by the advancement of specialized delivery systems for localized pain relief. White-space opportunities exist in developing disease-modifying therapies that address underlying pathophysiology rather than merely managing symptoms, particularly for conditions like diabetic peripheral neuropathy where prevention or reversal of nerve damage represents a significant unmet need. The competitive landscape is further shaped by technological innovation, with companies leveraging digital health solutions and advanced analytics to enhance clinical development efficiency and demonstrate real-world value. Medtronic's FDA approval for the Inceptiv closed-loop spinal cord stimulator in April 2024 exemplifies this trend, introducing the first device with adaptive stimulation based on biological feedback for personalized pain relief.

Neuropathic Pain Industry Leaders

Grünenthal

Mallinckrodt Pharmaceuticals

Pfizer, Inc.

Novartis AG

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vertex Pharmceuticals completed the nationwide retail pharmacy distribution of Journavx (suzetrigine), making the first-in-class non-opioid analgesic broadly available for patients with moderate to severe acute pain.

- March 2025: Halneuron, a novel NaV1.7 sodium channel blocker, entered Phase 2b clinical trials for chemotherapy-induced neuropathic pain, with the first patient dosed and interim analysis planned for late 2025 .

- January 2025: The FDA approved Journavx (suzetrigine), the first new analgesic class in over 20 years, for the treatment of moderate to severe acute pain in adults.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global neuropathic pain market as all prescription drugs and regulated neuromodulation devices that specifically alleviate pain arising from structural or functional damage to the somatosensory nervous system, tracked at ex-manufacturer prices across hospital, retail, and online channels. According to Mordor Intelligence, the market is valued at USD 8.0 billion in 2025 and is forecast to reach USD 12.73 billion by 2030.

Scope exclusion: pure over-the-counter analgesics formulated for nociceptive pain are kept outside this boundary.

Segmentation Overview

- By Drug Class

- Anticonvulsants

- Serotonin and Norepinephrine Reuptake Inhibitors

- Tricyclic Antidepressant

- Opioids

- Topical Agents

- Other Classes

- By Indication

- Diabetic Peripheral Neuropathy

- Postherpetic Neuralgia

- Chemotherapy-Induced Peripheral Neuropathy

- Trigeminal Neuralgia

- HIV-Associated Neuropathy

- Phantom Limb Pain

- Others (MS, Spinal Cord Injury)

- By Route of Administration

- Oral

- Topical

- Parenteral

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Fortnightly conversations with pain specialists, endocrinologists, oncology nurses, reimbursement advisors, and device distributors across North America, Europe, and key Asia-Pacific economies let us pressure-test prevalence ratios, typical treatment lines, and country-level average selling prices. Surveys with pharmacists and procurement heads validate channel weights and discount practices before we finalize assumptions.

Desk Research

We begin with public evidence: incidence and prevalence series on diabetes, shingles, and cancer from the World Health Organization, International Diabetes Federation, and GLOBOCAN; prescription audits from agencies such as IQVIA MIDAS; patent trends via Questel; and import-export filings captured on Volza for pregabalin, duloxetine, and spinal cord stimulators. Financial details in 10-Ks, FDA and EMA approval databases, and peer-reviewed journals such as Pain and Neurology help us map treatment mix shifts. To ground regional splits, analysts also review hospital discharge data and payer formularies published by CMS, NHS Digital, and Japan's MHLW. These are illustrative only; many other open and paid sources feed the evidence stack.

Market-Sizing & Forecasting

We apply a top-down prevalence-to-treated-cohort build-up, layering country epidemiology with diagnosis and treatment penetration, then valuing therapy days at blended ASPs. Select bottom-up roll-ups of stimulant device shipments and sampled prescription volumes act as guardrails. Key variables like diabetic adult population, post-herpetic neuralgia incidence, pregabalin generic erosion curve, neuromodulation adoption rate, and opioid restriction intensity feed a multivariate regression model whose coefficients are adjusted through expert consensus. Scenario analysis captures policy shocks and pipeline launches; gaps where bottom-up evidence is thin are filled by analyst interpolation capped at +/-10% of observable proxies.

Data Validation & Update Cycle

Outputs undergo variance checks against hospital procurement dashboards, insurer spend tallies, and historical treatment cost ratios. Senior reviewers sign off after anomalies are resolved. Reports refresh yearly, and interim revisions trigger when regulatory approvals, major recalls, or significant epidemiology revisions occur.

Why Our Neuropathic Pain Baseline Commands Reliability

Published figures vary because research firms pick different patient pools, include or exclude emerging device classes, convert currencies at divergent reference dates, or project generic price erosion with contrasting aggressiveness.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.0 B (2025) | Mordor Intelligence | - |

| USD 7.37 B (2023) | Global Consultancy A | excludes device-based neuromodulation and uses historical exchange rates |

| USD 8.20 B (2024) | Industry Research Firm B | applies constant ASP despite accelerating generic penetration |

| USD 6.39 B (2024) | Trade Journal C | omits Asia-Pacific secondary care usage and relies on limited hospital survey panel |

Taken together, the comparison shows that our disciplined scope, annually refreshed epidemiology inputs, and dual-track validation produce a balanced baseline that decision-makers can retrace, stress-test, and adopt with confidence.

Key Questions Answered in the Report

What is the Neuropathic Pain market size?

The Neuropathic Pain market size is USD 8.73 billion in 2026.

Which drug class holds the largest Neuropathic Pain market share?

Anticonvulsants remain the leading class, although topical and selective sodium-channel inhibitors are gaining ground.

Why are topical therapies increasingly popular?

They provide localized relief with fewer systemic side effects, making them attractive for elderly and polymedicated patients.

How does the NOPAIN Act influence the Neuropathic Pain industry?

It creates dedicated reimbursement for non-opioid pain treatments in outpatient settings, accelerating uptake of novel agents.

Which region shows the fastest Neuropathic Pain market growth?

Asia-Pacific leads with a forecast 11.88 % CAGR, driven by rising disease prevalence and expanding healthcare access.

What competitive strategies help firms stay ahead after patent expiry?

Companies invest in extended-release versions, combination products and partnerships with device makers to maintain differentiation and pricing power.

Page last updated on: