America AI Retail Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.43 Billion |

| Market Size (2031) | USD 12.66 Billion |

| Growth Rate (2026 - 2031) | 14.51% CAGR |

| Fastest Growing Market | South America |

| Largest Market | North America |

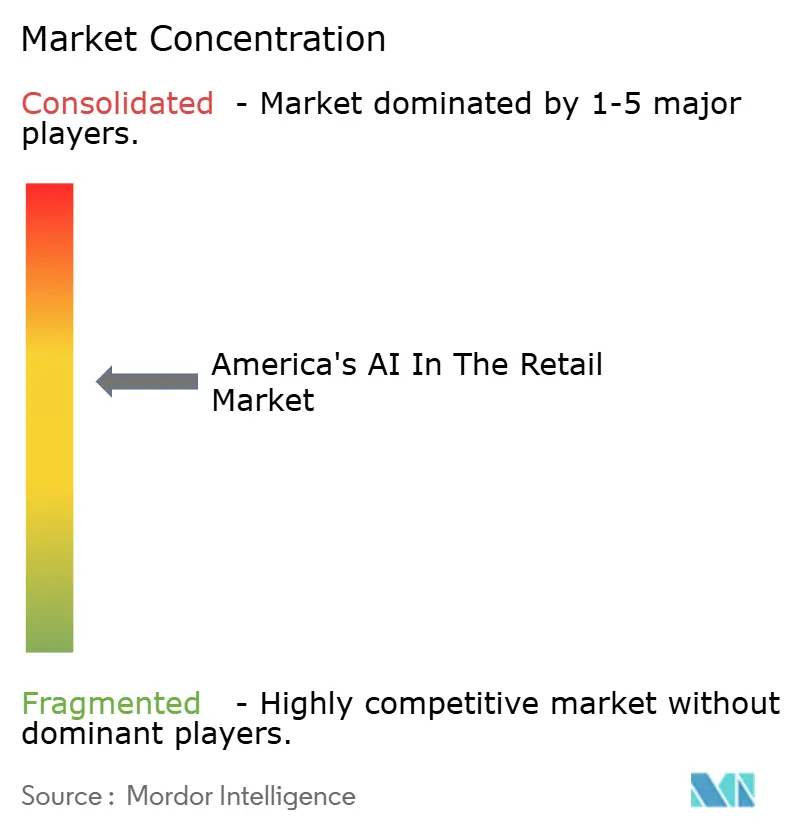

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

America AI Retail Market Analysis by Mordor Intelligence

The America AI Retail Market reached USD 6.43 billion in 2026 and is projected to grow to USD 12.66 billion by 2031, registering a 14.51% CAGR. This rapid expansion is led by tier-1 retailers that are shifting from pilots to production-scale deployments, embedding agentic AI frameworks across merchandising, supply chain, and customer engagement. GPU and edge-inference innovations are cutting latency for real-time personalization, while unified data platforms are turning omnichannel transaction histories into granular training sets. Vendor competition now centers on end-to-end platforms capable of bundling hardware, models, and orchestration, a dynamic reinforced by hyperscaler alliances with semiconductor leaders. Growth opportunities remain concentrated in pure-play online retail, home improvement applications, and swarm intelligence technologies that coordinate multi-agent decision making. Taken together, these forces position the AI retail market for compound growth as retailers prioritize automation to protect margins amid persistently thin cost structures.

Key Report Takeaways

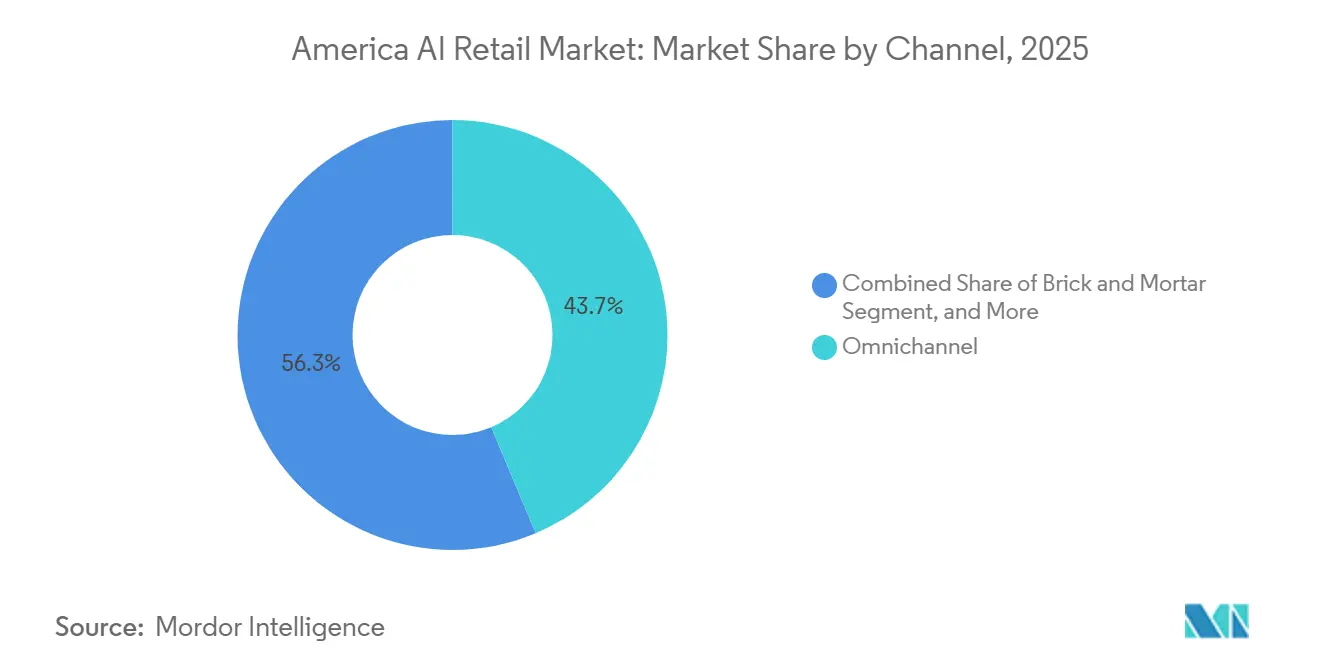

- By channel, omnichannel strategies captured 43.67% of the America AI retail market share in 2025, while pure-play online retailers are expanding at a 15.19% CAGR through 2031.

- By solution, software accounted for 52.89% of 2025 revenue, and service offerings are poised to grow at a 14.92% CAGR as retailers outsource integration complexity.

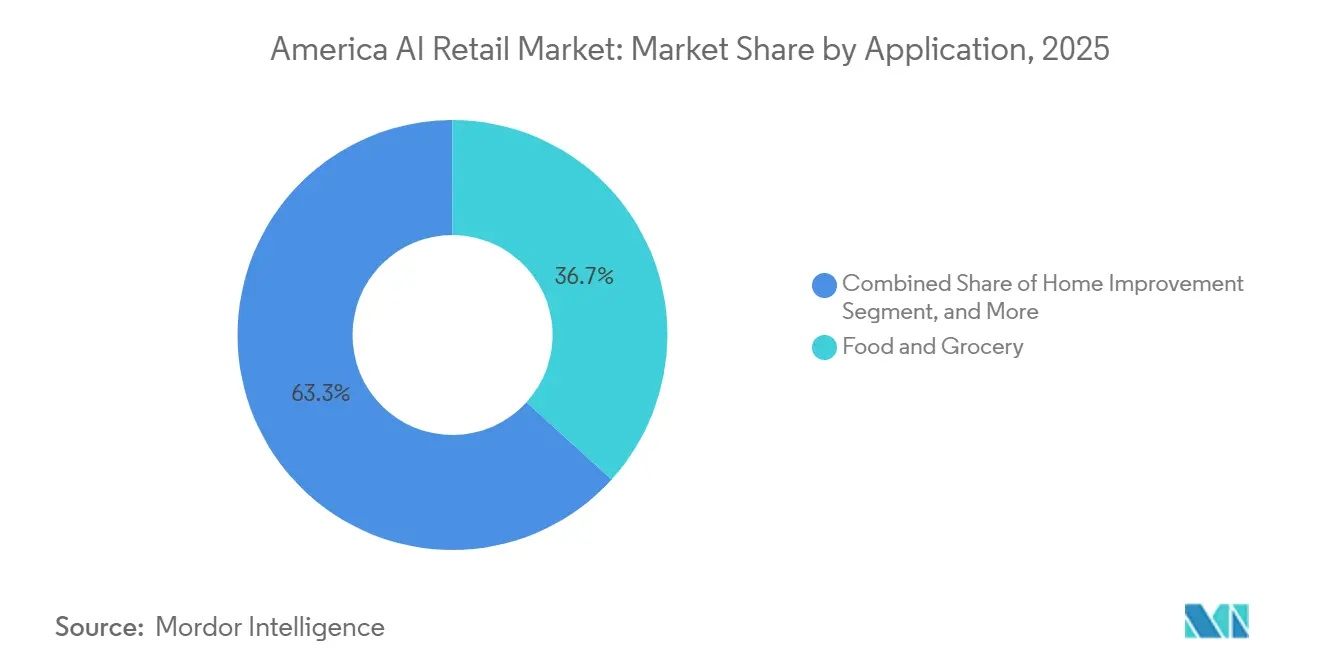

- By application, food and grocery commanded 36.72% of 2025 spending, whereas home improvement is accelerating at a 15.49% CAGR driven by project-planning assistants.

- By technology, machine learning accounted for 47.83% of 2025 deployments, and swarm intelligence is rising at a 15.53% CAGR as retailers pilot multi-agent optimization frameworks.

- By geography, North America accounted for 66.83% of the 2025 market value, while South America led growth with a 15.59% CAGR on the back of cloud-native e-commerce platforms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

America AI Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated GPU and edge-AI hardware innovation | +2.8% | Global, early uptake in North America and major Asia-Pacific metros | Medium term (2-4 years) |

| Omnichannel personalization imperative | +2.5% | North America and Europe, spreading to South America hubs | Short term (≤ 2 years) |

| AI-first operating models among tier-1 retailers | +2.3% | North America, pilots in Brazil and Mexico | Medium term (2-4 years) |

| Supply-chain optimization for last-mile efficiency | +2.1% | Global, acute need in South America and Southeast Asia | Short term (≤ 2 years) |

| Real-time computer-vision loss-prevention systems | +1.9% | North America and Europe | Short term (≤ 2 years) |

| Quantum-inspired inventory optimization pilots | +1.2% | North America and select European retailers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated GPU And Edge-AI Hardware Innovation

NVIDIA’s retail blueprints released in January 2025 trimmed model latency to sub-50 milliseconds, enabling real-time personalization at the point of sale without round-tripping data to cloud centers.[1]NVIDIA, “Retail AI Blueprints: Edge Inference for Real-Time Personalization,” blogs.nvidia.com More than 12,000 EGX edge nodes processed 4.2 billion daily inference calls by December 2025, validating at-scale performance. Intel’s Gaudi 3 accelerators, launched in April 2025, delivered 70% of comparable throughput at 55% of the capital outlay, carving space for cost-sensitive regional chains. As hardware footprints proliferate, demand is rising for model-compression and federated-learning tools that protect data-residency requirements while keeping training local. Hardware vendors have responded by packaging silicon, software, and deployment expertise, lowering entry barriers for mid-market adopters and adding momentum to the America AI Retail Market.

Omnichannel Personalization Imperative

Retailers integrating browsing, in-store, and mobile data into unified profiles saw double-digit increases in conversion rates in 2025. Adobe’s real-time CDP processed 18 billion customer events per day, demonstrating that data-rich profiles unlock 2.7-times higher conversion rates when individualized messaging is delivered within 24 hours.[2]Adobe, “Adobe Real-Time Customer Data Platform: Retail Performance 2025,” business.adobe.com Microsoft deepened this trend in June 2025 by embedding Azure OpenAI Service into Dynamics 365 Customer Insights, generating natural-language content tuned to each shopper’s context, a move that trimmed bounce rates by nearly one-third. As retailers merge e-commerce, store operations, and marketing into unified data teams, omnichannel personalization has become a board-level mandate, driving incremental spending that supports the America AI Retail Market.

AI-First Operating Models Among Tier-1 Retailers

Walmart signaled a strategic pivot in January 2026, moving from augmenting decisions to delegating workflows to autonomous agents built on its Wallaby large language model. Pilot results cut manual inventory interventions by 78% and lowered labor cost per transaction by 12%. Such outcomes illustrate the operational leverage of AI-first models. Yet adoption divides the sector: capital-rich leaders advance, while mid-market peers struggle with talent and budget constraints. The spread of AI-first strategies is expected to pull forward platform revenue as laggards pursue managed services, bolstering overall America AI retail market growth.

Supply-Chain Optimization For Last-Mile Efficiency

Last-mile delivery accounts for more than half of e-commerce logistics expenses. AI-driven route densification can reduce those costs by almost one-fifth, according to field data collected across 2025 deployments. Blue Yonder’s Luminate platform integrated traffic, weather, and customer availability to support 97% on-time delivery, up eight percentage points year over year.[3]Blue Yonder, “Blue Yonder Luminate Delivery Performance 2025,” blueyonder.com Symbotic’s swarm-based warehouse robots increased throughput by 35% in Walmart distribution centers, a capability underpinned by a USD 8.35 billion agreement announced in July 2024. These operational efficiencies free working capital, reinforcing spending on end-to-end AI supply-chain suites and sustaining upside for the AI retail market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of retail-specific data-science talent | -1.8% | Global, most acute in North America and Western Europe | Medium term (2-4 years) |

| Legacy IT integration complexity and costs | -1.6% | North America and Europe, heavier on mid-market chains | Short term (≤ 2 years) |

| Increasing data-privacy and AI-audit regulations | -1.3% | Europe, North America, emerging in South America | Medium term (2-4 years) |

| Sustainability concerns over AI energy footprint | -0.9% | Europe and select North American markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Retail-Specific Data-Science Talent

Retailers face a structural talent gap as hybrid expertise in machine learning and merchandising remains scarce. Median salaries for North American AI engineers climbed to USD 185,000 in 2025, yet turnover topped 30% as hyperscalers lured specialists with equity packages. Talent scarcity inflates project budgets, extends timelines, and forces many chains to embrace low-code platforms or managed services. Although retailers sponsor university programs and acquire analytics boutiques, these measures take years to bear fruit, sustaining drag on near-term adoption.

Legacy IT Integration Complexity And Costs

Connecting modern AI platforms to decades-old point-of-sale and enterprise systems can cost more than USD 50 million for national chains. Legacy databases rarely expose real-time APIs, forcing retailers to build middleware that introduces latency and maintenance overhead. Implementation roadmaps stretch beyond 18 months, diverting budgets from customer-facing innovation and discouraging risk-averse boards. Cloud migration promises relief, but operational risks during the cut-over leave many retailers in a transitional limbo, tempering overall AI retail market momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: Pure-Play Online Retailers Outpace Omnichannel

Pure-play online operators are forecast to grow at 15.19% through 2031, surpassing the overall America AI retail market CAGR as they exploit flexible infrastructure and rapid experiment cycles to roll out recommendation engines, dynamic pricing, and conversational commerce. Omnichannel retailers accounted for 43.67% of 2025 revenue by leveraging store footprints for click-and-collect services, yet they shoulder heavier integration burdens that slow the rollout of new use cases. The AI retail market size for brick-and-mortar chains continues to expand, but competitive intensity is rising as Amazon’s Just Walk Out setup has been extended to more than 140 North American sites, setting new expectations for frictionless checkout.

Shopify democratized advanced tooling in May 2025 when it launched Magic AI for 2.1 million merchants, compressing the capability gap between small sellers and large e-commerce leaders. Physical retailers are fighting back with edge-AI kiosks that deliver personalized offers in-store; Lowe’s Mylow Companion reduced average visit times by 28% while increasing basket sizes by 17%. As experiential differentiation eclipses pure assortment breadth, data density will determine winners, reinforcing investment in unified-commerce AI stacks and sustaining expansion of the America AI retail market.

By Solution: Service Growth Reflects Integration Demand

Software held 52.89% of 2025 revenue, but services are rallying with a 14.92% CAGR through 2031 as retailers outsource architecture design, model tuning, and change management. Enterprises adopting on-premise modules do so to preserve data residency, while mid-market retailers typically favor multitenant clouds. The America AI retail market for managed services is growing as integration complexity and talent shortages are tilting the total cost of ownership toward external providers.

Infosys and Cognizant each report multiyear agreements that bundle platform selection, data migration, and operational analytics. SAP’s Joule assistant automates low-value queries, yet the vendor’s own services arm spends up to 9 months tailoring workflows to each client's unique schema. Salesforce’s 2025 debut of Agentforce follows the same pattern: license revenue is paired with professional services that shoulder configuration tasks. As buyers mature, procurement teams specify time-to-value metrics, turning implementation prowess into a primary differentiator and driving sustained expansion of the service slice of the America AI retail market.

By Application: Home Improvement Leads Vertical Growth

Home improvement chains are adopting AI at a 15.49% annual pace, eclipsing every other vertical as project guidance tools unlock higher average order values. Food and grocery retained 36.72% of 2025 spending, driven by perpetual demand forecasting and spoilage-mitigation initiatives that protect razor-thin margins. The America AI retail market share for apparel and footwear remained notable, driven by virtual try-on and trend-forecasting engines.

Home Depot’s Magic Apron, rolled out in April 2025, improved cross-sell rates by 19%, demonstrating that generative AI drives incremental spend when tackling complex DIY tasks. Electronics retailers leverage predictive maintenance alerts that cut return rates, while grocers prioritize shelf-scanning vision systems that surface replenishment needs in minutes rather than hours. Vertical adoption velocities correlate with data richness and margin headroom: categories with higher ticket values can justify deeper personalization investments. As retailers refine application-specific blueprints, the America AI retail market size linked to specialized vertical use cases will compound.

By Technology: Swarm Intelligence Emerges As Fastest-Growing Segment

Machine learning accounted for 47.83% of 2025 technology spend, anchoring core functions such as demand forecasting and segmentation. Swarm intelligence, however, is expanding at 15.53% through 2031, reflecting momentum behind multi-agent systems that optimize interdependent retail decisions. Walmart’s reinforcement-learning framework coordinated pricing, inventory, and fulfillment across 4,700 stores, lifting gross margin by 1.2 percentage points, a clear testament to systemic gains from cross-domain co-optimization.

Natural language processing underpins chatbots that now resolve the majority of routine inquiries, while image and video analytics have crossed the 95% accuracy threshold for product recognition, enabling the confident rollout of autonomous checkout. 2026 announcements from Microsoft bundle vision, language, and reinforcement models into unified orchestration layers, raising the table stakes for point-solution vendors. The convergence of modalities ensures that platform providers capturing high market share can upsell supplementary functions, reinforcing revenue scale in the America AI retail market.

Geography Analysis

North America retained 66.83% of the 2025 market value, reflecting deep concentrations of hyperscale infrastructure and retail technology specialists. Most large U.S. and Canadian chains have shifted from pilots to production deployment, and although sequential growth is moderating, installed-base expansion continues as retailers broaden use-case portfolios. Mexico follows a similar glide path, with leading grocers layering AI onto omnichannel frameworks and upgrading supply-chain telemetry.

South America is accelerating at a 15.59% CAGR through 2031, led by cloud-native e-commerce firms that are leapfrogging legacy integrations. Mercado Libre invested USD 2.1 billion in 2025 to expand its AI-enabled logistics hubs, reducing last-mile costs by 18% and boosting conversion rates by 24%. Brazilian retailers such as Magazine Luiza deploy generative chatbots that handle Portuguese inquiries with 91% accuracy, while Argentine conglomerate Cencosud uses Google Cloud models to cut stockouts by nearly one-third.

Regulatory environments are diverging. The European Union AI Act requires transparency and audit trails, thereby indirectly increasing North American vendors’ compliance costs as they serve global retailers. South American jurisdictions remain largely permissive, allowing rapid rollout of personalization and computer-vision systems. Over the forecast horizon, converging rules are expected, but early movers are capturing data and model advantages that will be difficult for late entrants to replicate, expanding the America AI retail market size in high-growth geographies.

Competitive Landscape

Competition is intensifying as hyperscalers, enterprise software incumbents, and retail-tech specialists vie for overlapping accounts. Amazon Web Services strengthened its position in December 2025 with AgentCore, a framework that simplifies the deployment of autonomous agents. Microsoft partnered with NVIDIA and Anthropic in November 2025 on a USD 45 billion infrastructure build that combines silicon, training clusters, and retail-tuned foundation models. Google Cloud continues to expand its retail-specific accelerators, solidifying its position as a tri-polistic platform.

Enterprise vendors safeguard installed bases by embedding AI into existing ERP and CRM suites. SAP integrates Joule across its retail cloud, while Oracle layers machine learning into merchandising modules. Specialized players such as Blue Yonder focus on deep supply-chain optimization, Symbotic automates warehouses with swarm robotics, and Shopify empowers the long tail of merchants through plug-and-play generative tools. White-space remains in the mid-market, where chains numbering 50-500 stores require turnkey offerings that blend affordability with flexibility. Vendors that align pricing, services, and compliance features for this cohort are positioned to capture incremental share in the America AI retail market.

Intellectual-property intensity is rising. Amazon filed transformer-based patents that combine RFID and vision signals to achieve 99.2% checkout accuracy, while Walmart’s Wallaby model demonstrates a competitive advantage from proprietary datasets. Regulatory compliance, especially around data privacy, is a selection filter increasingly favoring providers that can embed audit functionality at the platform level. As capabilities converge, go-to-market differentiators hinge on speed-to-value, reliable ROI metrics, and the breadth of pre-integrated retail tools.

America AI Retail Industry Leaders

Amazon Web Services Inc.

Microsoft Corporation

Oracle Corporation

Salesforce Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Amazon Web Services introduced AgentCore for building retail agents, integrating with AWS Bedrock and Amazon Nova foundation models to streamline multi-agent orchestration.

- November 2025: Microsoft, NVIDIA, and Anthropic unveiled a USD 45 billion retail-optimized AI infrastructure partnership intended to lower deployment costs by 40% for mid-market chains.

- October 2025: Salesforce debuted Agentforce, automating 68% of customer inquiries and lifting satisfaction scores by 24% in pilots.

- September 2025: Walmart rolled out Wallaby, a proprietary language model powering inventory and pricing agents across 4,700 stores.

America AI Retail Market Report Scope

The America AI Retail Market Report is Segmented by Channel (Omnichannel, Brick and Mortar, Pure-Play Online Retailers), Solution (Software, and Service), Application (Apparel and Footwear, Food and Grocery, Electronics and Home Appliances, Home Improvement, Other Applications), Technology (Machine Learning, Natural Language Processing, Chatbots, Image and Video Analytics, Swarm Intelligence), and Geography (North America, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Omnichannel |

| Brick and Mortar |

| Pure-Play Online Retailers |

| Software | On Premise |

| Cloud | |

| Service |

| Apparel and Footwear |

| Food and Grocery |

| Electronics and Home Appliances |

| Home Improvement |

| Other Applications |

| Machine Learning |

| Natural Language Processing |

| Chatbots |

| Image and Video Analytics |

| Swarm Intelligence |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Channel | Omnichannel | |

| Brick and Mortar | ||

| Pure-Play Online Retailers | ||

| By Solution | Software | On Premise |

| Cloud | ||

| Service | ||

| By Application | Apparel and Footwear | |

| Food and Grocery | ||

| Electronics and Home Appliances | ||

| Home Improvement | ||

| Other Applications | ||

| By Technology | Machine Learning | |

| Natural Language Processing | ||

| Chatbots | ||

| Image and Video Analytics | ||

| Swarm Intelligence | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the AI retail market in the Americas today?

The market reached USD 6.43 billion in 2026 and is forecast to nearly double to USD 12.66 billion by 2031.

Which retail application is growing fastest?

Home improvement is leading growth at a 15.49% CAGR as generative assistants drive higher basket sizes through contextual project guidance.

Why are services growing almost as fast as software?

Retailers are outsourcing integration and change management to address talent shortages and legacy system complexity, lifting service revenue at a 14.92% CAGR.

What technology segment offers the highest upside?

Swarm intelligence is expanding at 15.53% annually because multi-agent coordination yields systemic gains across pricing, inventory, and logistics.

Which geography is the top growth hotspot?

South America leads with a 15.59% CAGR as cloud-native e-commerce firms deploy AI stacks without legacy constraints.

How are mid-market retailers addressing skills gaps?

Many are adopting managed AI platforms that bundle infrastructure, models, and monitoring, reducing the need for in-house data-science teams.

Page last updated on: