AI In Fintech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

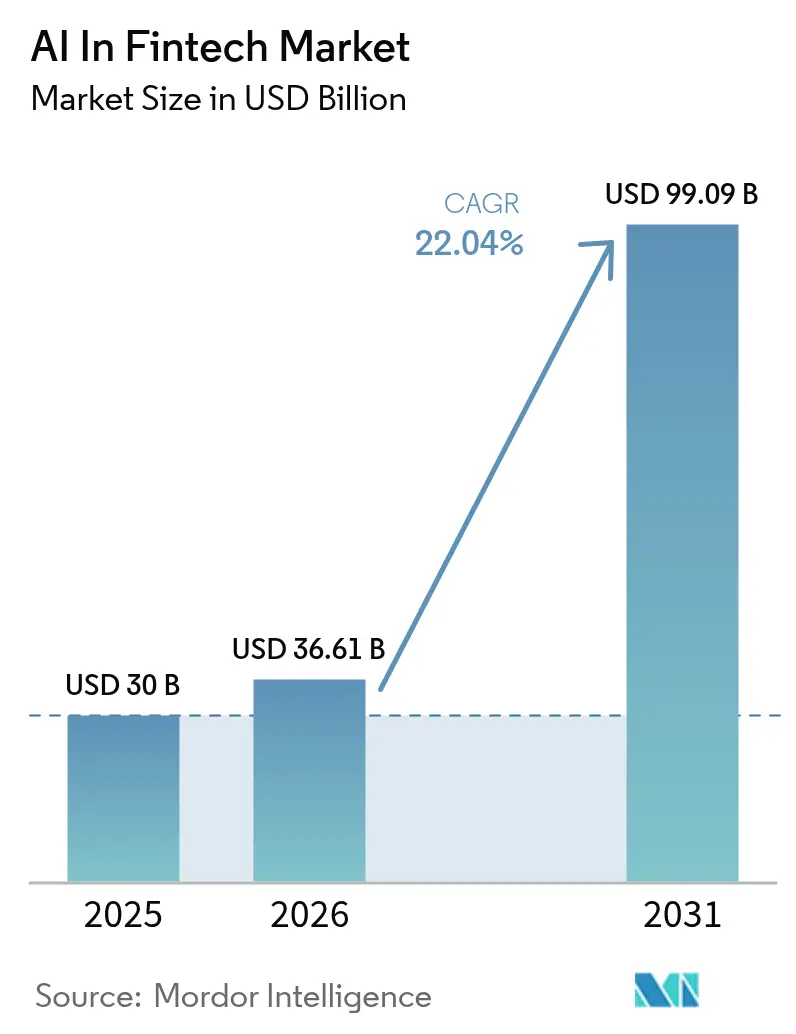

| Market Size (2026) | USD 36.61 Billion |

| Market Size (2031) | USD 99.09 Billion |

| Growth Rate (2026 - 2031) | 22.04% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Fintech Market Analysis by Mordor Intelligence

The AI in Fintech market size was valued at USD 30 billion in 2025 and estimated to grow from USD 36.61 billion in 2026 to reach USD 99.09 billion by 2031, at a CAGR of 22.04% during the forecast period (2026-2031).[1]Microsoft, “How Azure AI is redefining financial services productivity,” microsoft.com Growth is being propelled by open-banking mandates that liberate granular customer data, the maturation of real-time payment rails, and cloud-native AI platforms that trim operating costs for mid-tier banks.[2]IBM, “Generative AI in financial services: Accelerating risk model deployment,” ibm.com Generative AI copilots are compressing model-risk-management timelines from months to days, letting institutions release compliant risk models at unprecedented speed. High-frequency payment data, more than USD 9 trillion monthly at institutions such as BNY Mellon, feeds AI engines that sharpen fraud detection and liquidity forecasts. Convergence of these forces sustains a flywheel in which lower total cost of ownership invites wider adoption, and wider adoption produces richer datasets that reinforce model accuracy.

Key report Takeaways

- By component, solutions captured 71.45% of the AI in Fintech market share in 2025; services are advancing at a 27.95% CAGR through 2031.

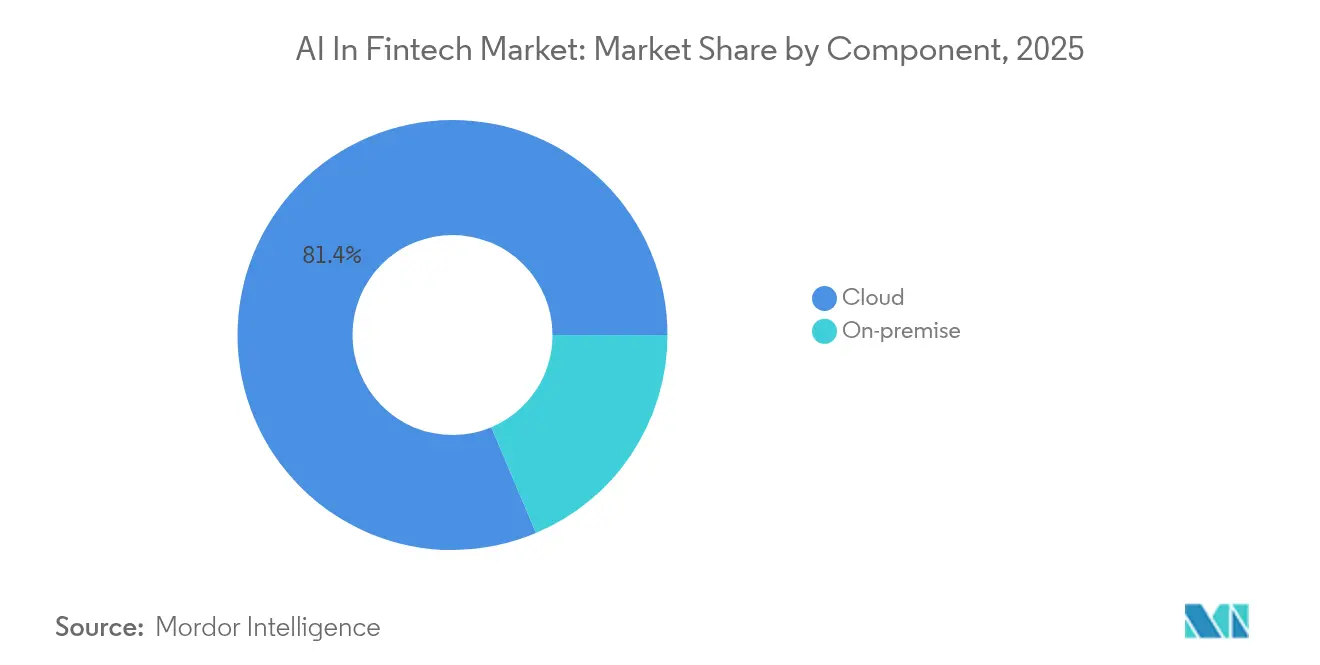

- By deployment mode, cloud accounted for 81.35% revenue share in 2025 in the AI in Fintech market, while hybrid deployment is expanding at a 27.4% CAGR to 2031.

- By application, fraud and risk management held 30.55% of the AI in Fintech market share in 2025; chatbots and virtual assistants record the fastest 34.8% CAGR to 2031.

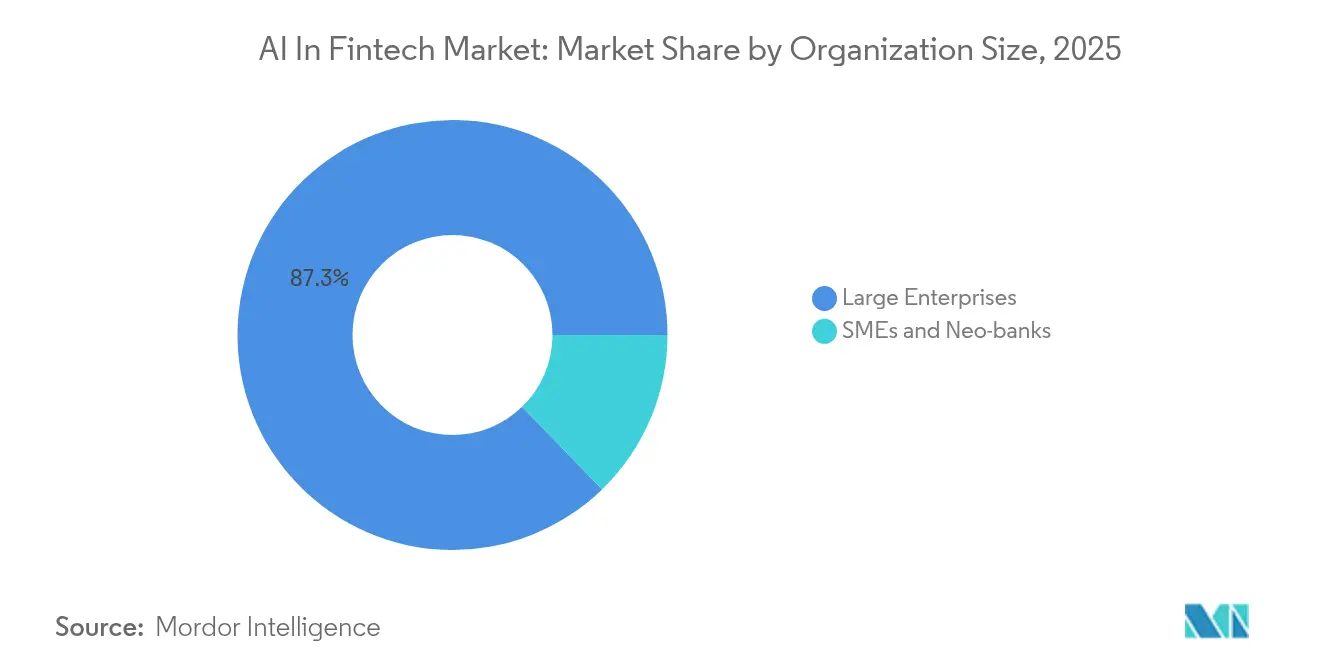

- By organization size, large enterprises commanded 87.25% share in 2025 in the AI in Fintech market, whereas SMEs and neo-banks are set to grow at 28.6% CAGR.

- By end-user, retail banking led with 33.75% revenue share in 2025 in the AI in Fintech market; payments and remittances providers are projected to rise at 32.2% CAGR.

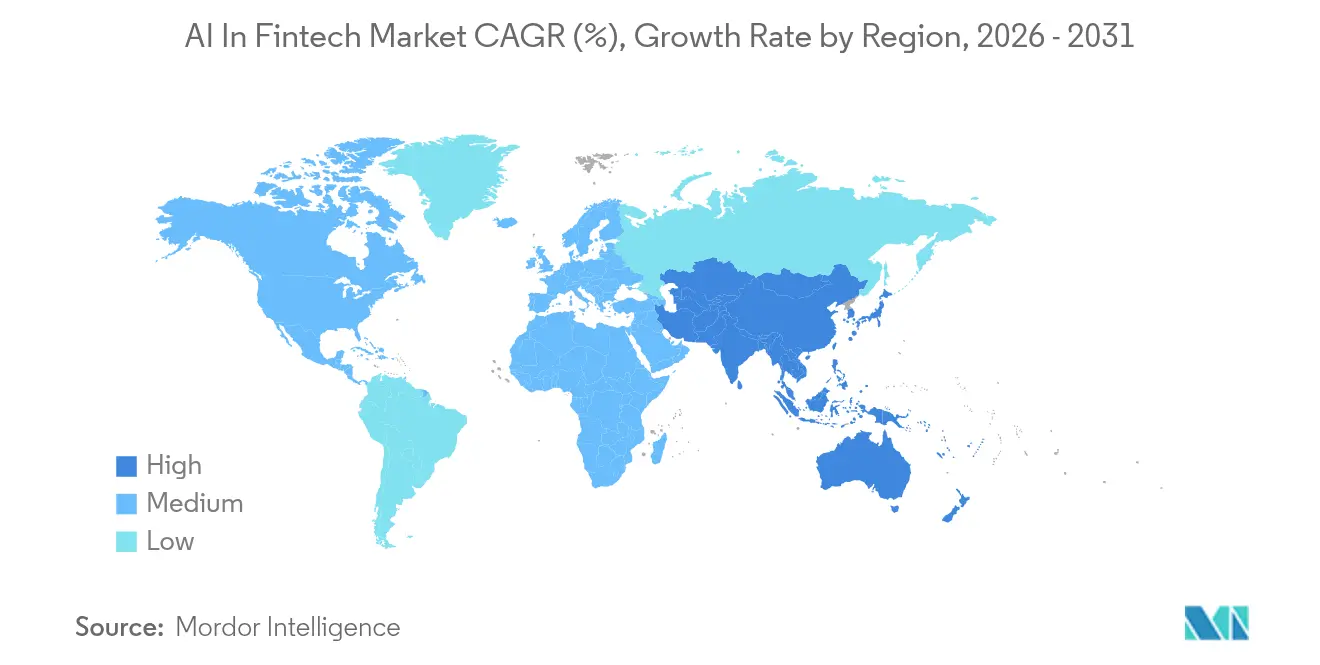

- By geography, North America contributed 37.60% revenue share in 2025 in the AI in Fintech market, while Asia-Pacific is poised for a 33.1% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI In Fintech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Open banking mandates accelerating AI-led process automation | +4.2% | Europe, North America, key APAC markets | Medium term (2-4 years) |

| Explosion of real-time payments data streams | +5.8% | Global with early gains in North America, APAC | Short term (≤ 2 years) |

| Cloud-native AI platforms lowering TCO | +3.1% | Global with spill-over to emerging markets | Medium term (2-4 years) |

| GenAI copilots slashing model-risk-management cycle times | +2.7% | North America, Europe, advanced APAC | Long term (≥ 4 years) |

| AI-powered ESG scoring unlocking green-finance incentives | +1.9% | Europe, North America, expanding APAC | Long term (≥ 4 years) |

| SME and neo-bank adoption of AI-native models | +2.3% | Global, strongest in APAC and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Open Banking Mandates Accelerating AI-Led Process Automation

Mandatory data-sharing rules such as PSD3 grant AI engines consistent, permissioned access to multi-institution bank records, enabling real-time credit scoring and hyper-personalized offers. PSD3 went live in 2024, prompting European banks to redesign product origination workflows around API-first architectures that feed machine-learning models with previously siloed datasets. Mid-tier institutions gain competitive parity because compliance investments double as innovation enablers, turning regulatory cost into revenue growth levers. Markets where open-banking adoption exceeds 87% of institutions already display elevated AI service penetration.

Explosion of Real-Time Payments Data Streams

VisaNet +AI processes each authorization with 98% stability prediction accuracy, while its Smarter Settlement Forecast adds seven-day cash-flow projections that shrink liquidity buffers.[3]Visa, “VisaNet +AI elevates authorization accuracy,” visa.com Real-time rails broadcast behavioral signals that batch systems miss, letting AI flag fraud milliseconds after initiation . Surveys show 94% of payments professionals view AI as indispensable for fraud mitigation, and 77% of consumers expect institutions to deploy it. BNY Mellon automated 90% of back-office payment instruction handling, freeing analysts for value-added tasks. Instant data availability also powers live credit decisions based on dynamic cash-flow metrics.

Cloud-Native AI Platforms Lowering TCO for Mid-Tier Financial Institutions

Azure AI lets UBS advisers retrieve investment insight in seconds, cutting research time and boosting client responsiveness. Finova trimmed Azure virtual machines from 1,200 to 100 and held latency steady, proving infrastructure right-sizing potential. JPMorgan Chase, which shifted 70% of workloads to cloud while funding USD 2 billion private facilities, illustrates how hybrid estates sustain sovereignty without sacrificing scale. These models collapse capital expenditure needs, letting regional banks access identical inference performance for a fraction of historic outlays.

GenAI Copilots Slashing Model-Risk-Management Cycle Times

Generative copilots draft model documentation, parse regulatory text, and assemble validation packs in hours, shrinking cycle time by up to 40%. Clearing brokers deploy real-time market-data analysis to pre-empt margin breaches, illustrating practical risk mitigation. Faster approvals translate into quicker deployment of trading or credit models, allowing institutions to monetize transient market windows that slower peers miss

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of domain-specific AI talent | -3.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Fragmented regulatory guidance on AI governance | -2.8% | Global, varies by jurisdiction | Medium term (2-4 years) |

| Rising GPU supply-chain volatility inflating inference costs | -1.6% | Global, concentrated in major data-center hubs | Short term (≤ 2 years) |

| Compliance cost overhead diverting AI budgets | -1.9% | Global, strongest in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Domain-Specific AI Talent

Demand for professionals who blend machine-learning mastery with regulatory fluency exceeds supply by 2-4 times, with 74% of employers reporting hiring struggles. European banks note that only 25% have formal GenAI training pipelines, widening capability gaps. Salary premiums of 40-60% over traditional finance roles tilt the playing field toward tech giants and tier-one banks. Mid-tier firms risk stalled deployments as talent scarcity inflates project timelines and costs.

Fragmented Regulatory Guidance on AI Model Governance

The EU AI Act designates high-risk financial systems for stringent oversight, while US and UK rely on sectoral guidance, producing compliance patchworks. Multinationals juggle divergent rules, with only 11% of European banks feeling prepared. Institutions now allocate up to 30% of AI budgets to compliance activities, trimming funds for innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Provide Integrated Value

Solutions generated USD 21.44 billion in 2025, equal to 71.45% of the AI in Fintech market. Enterprises favor platforms that unify fraud analytics, customer support, and governance within a single control plane. FICO’s blockchain-enabled governance suite, which won a 2025 innovation award, illustrates why integrated offerings dominate. The services segment is smaller today but is projected to grow at 27.95% CAGR through 2031 as banks seek advisory partners to configure complex GenAI pipelines and manage the daily swell of 234 regulatory notices.

Consultancies help translate compliance obligations into model design, accelerating time to value. This demand keeps specialized system integrators busy and cements service fees as a predictable revenue stream. As service expertise proliferates, mid-tier firms that once delayed AI adoption due to limited internal skill sets now jump in, broadening the AI in Fintech market customer base.

By Deployment Mode: Hybrid Architecture Balances Control and Scale

Cloud environments delivered 81.35% of deployment revenues in 2025 on the back of elastic compute that processes massive transaction volumes. JPMorgan Chase’s architecture shows 70% of applications in public cloud while sensitive workloads reside in USD 2 billion private facilities. Hybrid deployments are forecast to advance at 27.4% CAGR as regulators tighten residency rules and banks look to limit exposure to single-vendor outages.

Hybrid models place training pipelines on-premise for sovereignty yet run inference in cloud, unlocking the best of both worlds. This flexibility positions hybrid as a durable choice, particularly in jurisdictions enforcing strict data localization.

By Application: Conversational Interfaces Accelerate

Fraud and risk management retained 30.55% of 2025 revenues, confirming the segment’s role as mission-critical. Yapı Kredi’s 98.7% fraud reduction over seven years demonstrates a tangible return. Chatbots and virtual assistants will, however, record the strongest 34.8% CAGR to 2031 as customers demand always-on support. Bank of America’s Erica crossed 2 billion interactions by late 2024, proving that conversational AI boosts engagement.

RegTech tools that parse new rules in real time and auto-update policy frameworks are gaining traction. Credit scoring engines feed on alternative data to approve microloans within minutes. Collectively these trends expand the AI in Fintech market size for software vendors that can bundle multiple use cases under unified governance.

By Organization Size: SMEs Capture Cloud Leverage

Large enterprises retained 87.25% revenue share in 2025, reflecting deep budgets and in-house data science. Yet SMEs and neo-banks are slated for 28.6% CAGR thanks to pay-as-you-go cloud subscriptions. Roughly 46% of midsize businesses have either deployed or evaluated AI, focusing on operations and communications.

Neo Financial’s CAD 360 million funding round underlines investor faith in AI-native challengers. Lower entry barriers broaden participation, driving incremental AI in Fintech market growth beyond traditional banking incumbents.

By End-User: Payments Providers Outpace Retail Banks

Retail banking produced 33.75% of 2025 revenues on the strength of branch digitization and personalized advice engines. Payments and remittances providers will post the highest 32.2% CAGR through 2031 as real-time cross-border transfers become ubiquitous. Stripe’s USD 1.1 billion Bridge Network acquisition highlights strategic bets on stablecoin rails and AI-driven compliance.

Insurers automate claims triage, while wealth managers deploy robo-advisers for low-fee portfolios. Together, these shifts enlarge the AI in Fintech market and diversify its customer pool.

Geography Analysis

North America held 37.60% revenue share in 2025, supported by a mature financial stack and clear though fragmented regulatory guidance. JPMorgan Chase fields 2,000 AI specialists and over 400 live use cases, underscoring local skill depth. Canada’s challenger banks such as Neo Financial scale AI to underserved segments, and Mexico leverages AI for financial inclusion. Continued public-private investment sustains North America as an innovation laboratory, feeding global best practices back into the AI in Fintech market.

Asia-Pacific is projected to register the fastest 33.1% CAGR through 2031. China poured USD 2.1 billion into generative AI in 2024 and records 83% enterprise usage, dwarfing western penetration rates. India and Japan extend momentum through inclusive credit and quantitative trading desks that rely on AI engines. The region’s fintech revenue could move from USD 245 billion in 2021 to USD 1.5 trillion by 2030, with 87% of banks planning fintech partnerships. Singapore leads in mobile payments, while Australia and New Zealand expect disproportionate AI value capture relative to GDP.

Europe demonstrates strong adoption tempered by compliance overhead. The EU AI Act imposes a risk-tier system that elevates governance costs but assures ethical deployment. The UK reports 70% GenAI usage, leveraging post-Brexit agility to tailor banking sandboxes. Germany and France fund AI centers of excellence inside national champions, and the Nordics pilot green-finance scoring frameworks. Eastern markets experiment with AI for cross-border wage remittances, redrawing traditional service boundaries.

Competitive Landscape

The AI in Fintech market features moderate fragmentation with cloud hyperscalers, domain specialists, and incumbent banks vying for share. Microsoft’s Azure AI, AWS’s Bedrock, and Google Cloud’s Vertex position infrastructure as a gateway product, bundling managed models that shorten build cycles. FICO, SAS, and DataRobot defend niches in decision intelligence and model monitoring, reflected in FICO’s 12 new AI patents secured in March 2025.

Fintech disruptors such as Stripe, Plaid, and Upstart specialize in payments rails, data connectivity, and AI-driven credit, respectively. Stripe’s USD 1.1 billion Bridge purchase signals intent to blend stablecoin settlement with AI compliance screening. Traditional giants including JPMorgan Chase and UBS invest internally, exemplified by UBS co-creating smart assistants with Microsoft to boost advisory productivity.

Talent scarcity intensifies rivalry. Compensation premiums drain smaller firms, prompting creative approaches like university partnerships and internal bootcamps. Vendors able to bundle technology with explainability toolkits gain an edge because regulators scrutinize model bias and audit trails. In this dynamic, alliances between banks and fintechs, such as Fifth Third Bank teaming with Stripe for embedded services, illustrate convergence patterns that continue to reshape the AI in Fintech market.

AI In Fintech Industry Leaders

Intel Corporation

Amazon Web Services, Inc.

International Business Machines Corporation

ComplyAdvantage Ltd.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stripe finalized its USD 1.1 billion acquisition of Bridge Network, accelerating stablecoin-enabled payment services.

- January 2025: FICO received the 2025 BIG Innovation Award for its blockchain-based AI governance platform.

- January 2025: Experian Assistant won a 2025 BIG Innovation Award for trimming model-development timeframes.

- December 2024: KPay Group secured USD 55 million Series A funding to scale AI platforms for SMEs in Emerging Asia.

Global AI In Fintech Market Report Scope

Data analysis using AI data mining tools assists fintech organizations in gathering numerous angles of information and leads to data silos. AI and ML assist organizations in gathering numerous facets of data and in ingesting, analyzing, cleaning, and archiving the data by revealing useful information.

The AI in fintech market is segmented by type into solutions and services. By deployment, the market is segmented into cloud and on-premise. By application, the market is segmented into chatbots, credit scoring, quantitative and asset management, fraud detection, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions |

| Services |

| Cloud |

| On-premise |

| Fraud and Risk Management |

| Chatbots and Virtual Assistants |

| Credit Scoring and Underwriting |

| Quantitative and Asset Management |

| RegTech and Compliance Analytics |

| Others |

| Large Enterprises |

| SMEs and Neo-banks |

| Retail Banking |

| Insurance |

| Investment and Wealth Management |

| Payments and Remittances Providers |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-premise | |||

| By Application | Fraud and Risk Management | ||

| Chatbots and Virtual Assistants | |||

| Credit Scoring and Underwriting | |||

| Quantitative and Asset Management | |||

| RegTech and Compliance Analytics | |||

| Others | |||

| By Organization Size | Large Enterprises | ||

| SMEs and Neo-banks | |||

| By End-user | Retail Banking | ||

| Insurance | |||

| Investment and Wealth Management | |||

| Payments and Remittances Providers | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the AI in Fintech market?

The AI in Fintech market is valued at USD 36.61 billion in 2026.

How fast is the AI in Fintech market expected to grow?

It is projected to expand at a 22.04% CAGR, reaching USD 99.09 billion by 2031.

Which application area is growing the quickest?

Chatbots and virtual assistants lead with a 34.8% CAGR through 2031, reflecting rising demand for 24/7 digital support.

Why are hybrid deployments gaining traction?

Hybrid models let institutions keep sensitive data on-premise for compliance while using cloud inference for scale, expanding at 27.4% CAGR.

What regions present the strongest growth outlook?

Asia-Pacific is forecast to grow at 33.1% CAGR, driven by China’s heavy generative AI investment and widespread mobile payment adoption.

How severe is the AI talent shortage in financial services?

Demand for domain-specific AI professionals exceeds supply by as much as fourfold, prompting premium salaries and slower project timelines.

Page last updated on: