Alpha Mannosidosis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

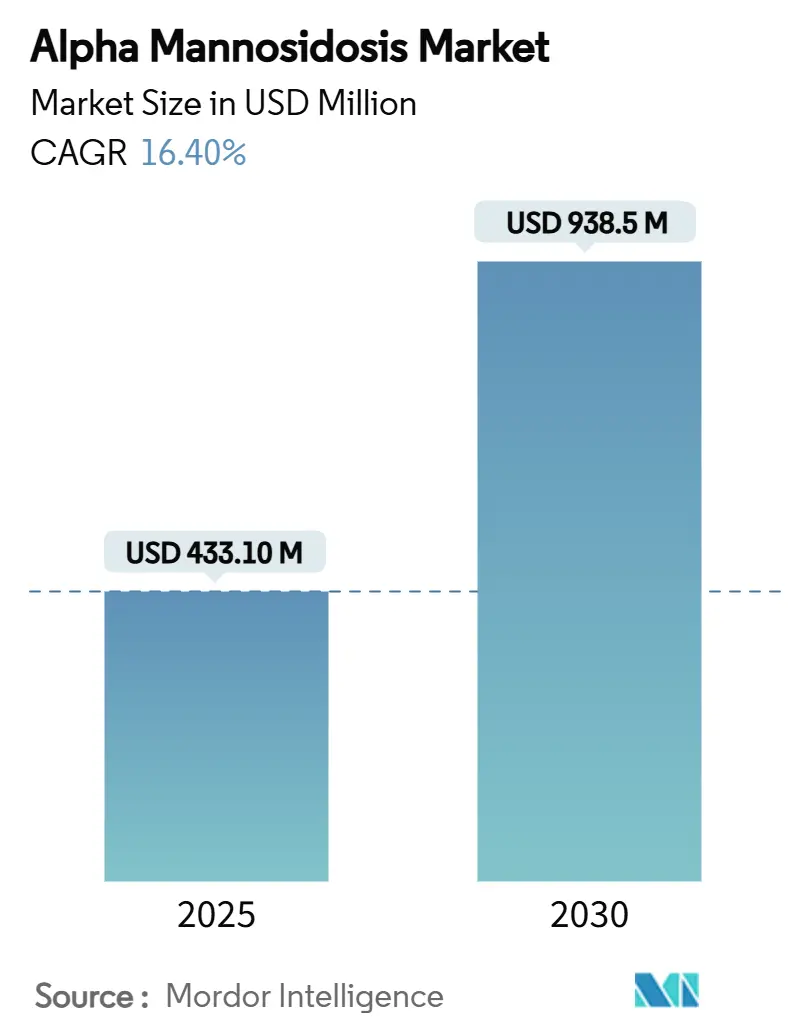

| Market Size (2025) | USD 433.10 Million |

| Market Size (2030) | USD 938.5 Million |

| Growth Rate (2025 - 2030) | 16.40% CAGR |

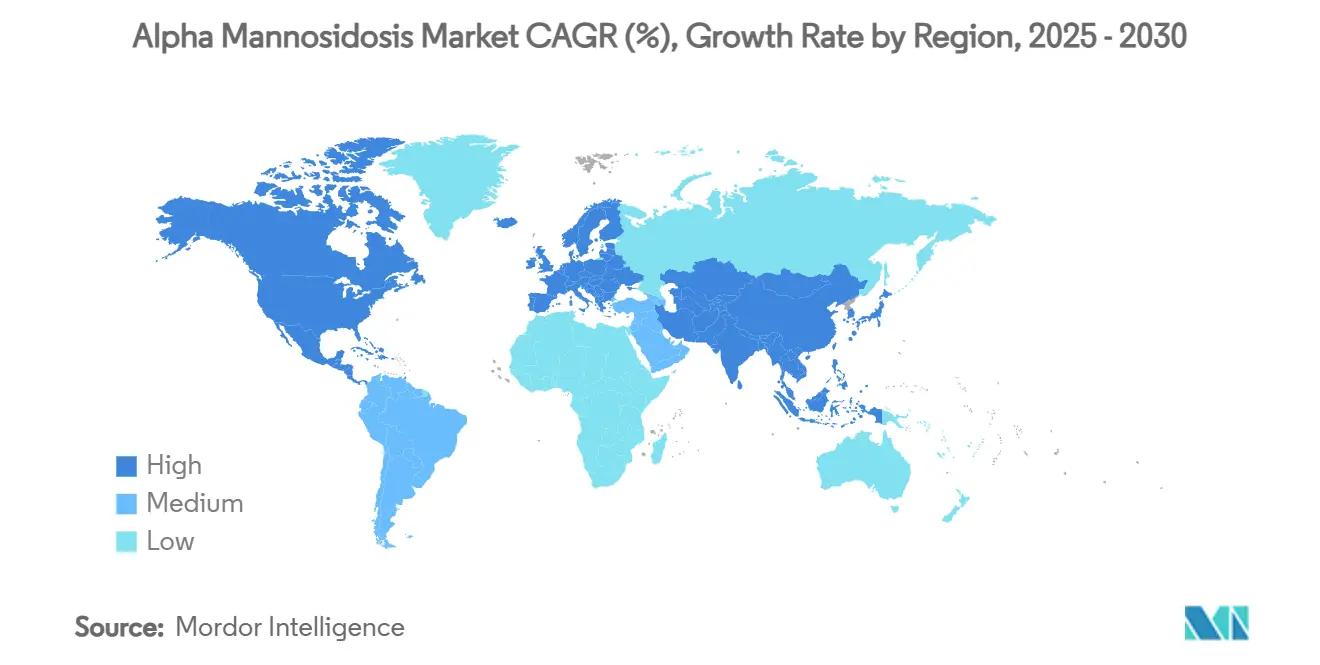

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alpha Mannosidosis Market Analysis by Mordor Intelligence

The Alpha Mannosidosis Market size is estimated at USD 433.10 million in 2025 and is expected to reach USD 938.50 million by 2030, at a CAGR of 16.40% during the forecast period (2025-2030). Mounting post-approval demand for velmanase alfa, pipeline progress in gene therapy, and expanding newborn-screening programs collectively fuel this double-digit trajectory. Intensifying diagnosis efforts shift discovery from symptomatic to presymptomatic stages, widening the addressable pool of roughly 5,000 diagnosed patients. Competitive intensity rises as single-treatment gene therapies threaten the chronic-infusion model that currently dominates revenue. Europe retains first-mover advantage through earlier reimbursement, yet North America now propels overall growth after the FDA’s 2024 approval of Lamzede. Persistently high annual treatment costs, however, temper near-term penetration in price-sensitive regions, compelling manufacturers to explore value-based agreements and patient-assistance funds.

Key Report Takeaways

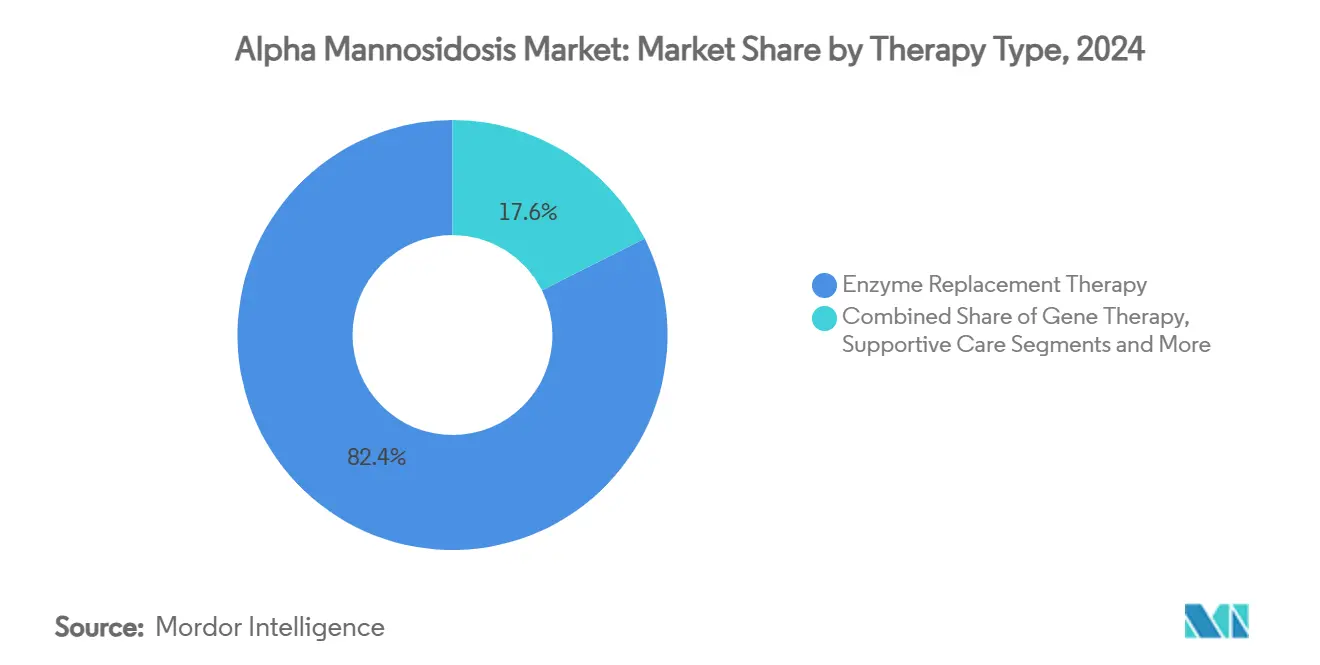

- By therapy type, enzyme replacement therapy held 82.4% of the alpha-mannosidosis market share in 2024, while gene therapy is projected to surge at an 18.4% CAGR through 2030.

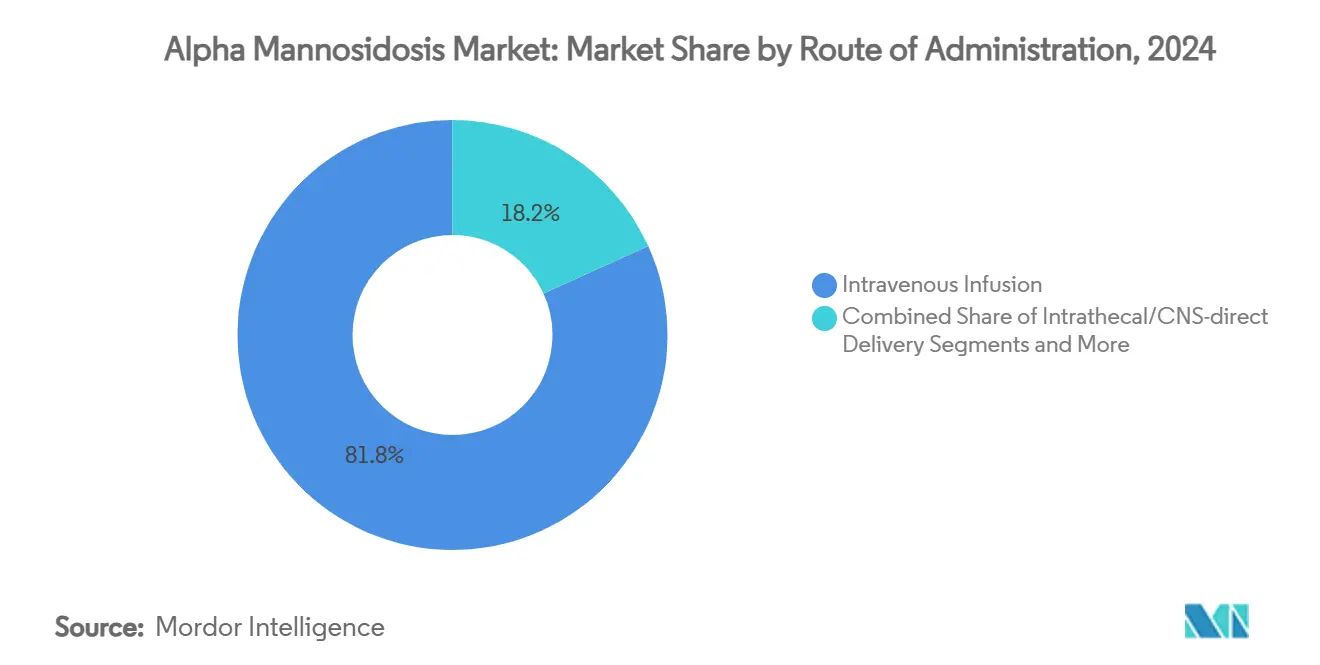

- By route of administration, intravenous infusion accounted for 81.8% of the alpha-mannosidosis market size in 2024; systemic viral-vector delivery is forecast to grow at a 17.3% CAGR to 2030.

- By geography, Europe commanded 41.3% revenue in 2024, whereas North America will post the fastest 15.7% CAGR during 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alpha Mannosidosis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-approval uptake of velmanase alfa ERT | +3.20% | North America & Europe | Short term (≤ 2 years) |

| Increasing newborn-screening pilots | +2.80% | China, Italy, New Jersey; expanding globally | Medium term (2-4 years) |

| Gene-therapy pipeline breakthroughs | +2.10% | Global | Long term (≥ 4 years) |

| Compassionate-use & early-access programs | +1.90% | Europe & North America | Short term (≤ 2 years) |

| EU orphan-drug reimbursement harmonization | +1.50% | Europe with spill-over | Medium term (2-4 years) |

| AI-enabled patient-finding algorithms | +1.20% | Developed markets first, then global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Approval Uptake of Velmanase Alfa ERT

Lamzede’s June 2024 FDA approval unlocked commercial access for US patients who had relied on importation or compassionate use. Trial data showed a 77.6% reduction in serum oligosaccharides at 52 weeks, and the SPARKLE registry will track outcomes over 15 years, reinforcing prescriber confidence. Earlier pediatric initiation correlates with improved hearing and immune profiles, prompting guideline updates that advocate treatment soon after diagnosis.[1]Line Borgwardt et al., “Efficacy and Safety of Velmanase Alfa,” Journal of Inherited Metabolic Disease, jimd.orgWeekly infusions require specialized centers, but growing home-care programs mitigate logistical burden for stable patients. Rapid US uptake thus adds meaningful near-term volume to the alpha-mannosidosis market.

Increasing Newborn-Screening Pilots for Lysosomal Storage Disorders

Large-scale pilots in China uncovered lysosomal storage disorders in 1 in 1,512 births, validating next-generation sequencing coupled with tandem-mass-spectrometry reflex testing.[2]Z.-F. Xu, “Newborn Genomic Screening in China,” Genome Medicine, genomemedicine.biomedcentral.com New Jersey’s experience covering 438,515 newborns demonstrates operational feasibility in a US setting. Tuscany’s inclusion of metachromatic leukodystrophy proves European payers’ willingness to broaden rare-disease panels. Earlier detection shifts treatment to pre-symptomatic stages, maximizing therapeutic benefit and curbing long-term costs, arguments now resonating with policymakers. As more jurisdictions legislate universal screening, the alpha-mannosidosis market captures incremental patients who would previously have remained undiagnosed.

Gene-Therapy Pipeline Breakthroughs

Eight adeno-associated-virus gene therapies have secured regulatory approval in other indications, de-risking platform safety and manufacturing for ultra-rare settings. Lipid-nanoparticle mRNA constructs enable redosable expression without genome integration, a design that addresses lingering vector-immunity concerns.[3]Caitlin Menello, “Newborn Screening for Gaucher Disease: The New Jersey Experience,” International Journal of Neonatal Screening, mdpi.com M6P Therapeutics holds six FDA Rare Pediatric Disease Designations, accelerating review timelines and providing priority-voucher economics upon approval. SmartPharm’s gene-encoded enzyme replacement aims to marry ERT pharmacology with gene-therapy durability. Together, these advances underpin long-term upside for the alpha-mannosidosis market by promising single-administration cures.

Expansion of Compassionate-Use & Early-Access Programs

EMA frameworks have provided velmanase alfa under compassionate protocols since 2018, bridging patients to commercial rollout while supplying real-world evidence. Streamlined advanced-therapy regulations in Europe now extend similar pathways to investigational gene therapies, compressing the time from trial completion to bedside. US Right-to-Try expansions and institution-led early-access boards further widen availability for ultra-rare populations. Patient-advocacy groups cite compassionate-use outcomes when negotiating payer coverage, enhancing reimbursement prospects. These programs therefore add marginal volumes and bolster payer confidence in clinical value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Annual Treatment Cost & Pricing Pushback | -4.10% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Limited Blood–Brain-Barrier Penetration Of Current ERT | -2.50% | Global | Long term (≥ 4 years) |

| Scarce Long-Term Real-World Safety Data | -1.80% | Global, more pronounced in regulatory-strict regions | Short term (≤ 2 years) |

| Competition For Bone-Marrow Donor Matches Limiting HSCT Uptake | -1.10% | Global, acute in regions with limited donor registries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Annual Treatment Cost & Pricing Pushback

Weekly velmanase alfa infusions translate into yearly drug spend above USD 650,000, a burden that challenges single-payer and emerging-market budgets. Gene-therapy benchmarks, such as Lenmeldy's USD 4.25 million launch price, heighten affordability concerns for one-time cures. Central and Eastern Europe report fewer than 20 reimbursed orphan medicines, underscoring access gaps within the very region that originally adopted Lamzede. Insurers increasingly demand outcome-based contracts linking payment to long-term functional benefits, shifting financial risk back to manufacturers. Without innovative financing, sticker shock will limit near-term uptake, slowing growth in the alpha-mannosidosis market.

Limited Blood–Brain-Barrier Penetration of Current ERT

Velmanase alfa clears somatic oligosaccharide accumulation yet fails to reach neuronal tissue, leaving cognitive decline unchecked. Hematopoietic stem-cell transplantation can deliver enzyme across the barrier but entails conditioning toxicity and donor-match hurdles, restricting eligibility to severe pediatric cases. Exploratory receptor-mediated transport and intrathecal infusion studies remain preclinical, keeping the neurological burden largely unmanaged. Caregivers voice dissatisfaction when somatic gains fail to halt cognitive regression, potentially dampening ERT adherence. Absent CNS-penetrant solutions, the alpha-mannosidosis market loses potential value locked in neuroprotective outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: ERT Dominance Faces Gene Therapy Disruption

The enzyme-replacement segment represented 82.4% of the alpha-mannosidosis market in 2024, anchored by velmanase alfa’s first-to-market advantage. Gene therapies, buoyed by six pediatric-disease designations and venture-capital inflows, are forecast to post an 18.4% CAGR through 2030, setting a disruptive tone. Hematopoietic stem-cell transplants secure clinical relevance for severe neurologic phenotypes, with post-2000 survival at 86% versus 64% pre-2000. Supportive multidisciplinary care—including audiology, immunology, and physiotherapy—expands as standard protocols mature. Pharmacological-chaperone candidates seek to correct misfolded lysosomal enzymes, though none have yet reached pivotal trials.

Robust real-world registry data underscore velmanase alfa durability, convincing payers of sustained clinical return. However, single-dose AAV vectors threaten recurring-revenue models, compelling Chiesi to diversify via grants that fund next-generation research. SmartPharm’s gene-encoded-enzyme platform illustrates hybrid approaches that could lengthen expression without permanent genome integration. As these modalities converge, the alpha-mannosidosis market will increasingly reward therapies that pair CNS reach with simplified administration schedules.

By Route of Administration: IV Infusion Leadership Challenged by Viral Vectors

Intravenous infusion held 81.8% of the alpha-mannosidosis market size in 2024, reflecting the entrenched velmanase alfa protocol and reimbursed infusion-center networks. Systemic viral-vector delivery, still investigational, shows a 17.3% forecast CAGR as clinical programs advance toward pivotal readouts. Surgical transplant routes apply to allogeneic stem-cell procedures for high-risk pediatric cases, while intrathecal AAV dosing is under exploration to overcome CNS exposure gaps. Subcutaneous-ERT formulations in preclinical stages aim to shift administration from hospital to home, aligning with broader rare-disease convenience trends.

Health-economic analyses in Germany reveal that home-infusion incurs no cost premium over hospital administration, encouraging wider insurer adoption. Viral-vector suppliers tout single-visit dosing as a transformative patient-experience upgrade, yet long-term immunological monitoring remains mandatory. Advances in receptor-mediated transport technologies envision intravenous ERT that crosses the blood–brain barrier, potentially reviving infusion’s relevance. Route-of-delivery innovation thus mirrors the competitive tension between chronic and curative paradigms within the alpha-mannosidosis market.

Geography Analysis

Europe, with a 41.3% revenue share in 2024, benefits from EMA's 2018 approval of velmanase alfa and well-established orphan-drug reimbursement mechanisms. Germany and France each reimburse more than 100 rare-disease medicines, fostering early and sustained uptake. In contrast, Central and Eastern Europe still struggle with limited reimbursement pathways, perpetuating unequal access gaps. MetabERN harmonizes clinical pathways across member states, easing cross-border knowledge transfer and bolstering adoption rates.

North America now represents the fastest-growing region, projected at a 15.7% CAGR through 2030, following the FDA's landmark 2024 green light. The United States leverages orphan-drug incentives and an expanding newborn-screening infrastructure exemplified by New Jersey's operational rollout. Canada and Mexico are aligning regulatory review procedures with US precedents, though differential pricing hurdles remain. Public debate over ultra-high-cost medicines intensifies pressure for outcome-based funding models, yet payer appetite for transformative rare-disease therapies persists.

Asia-Pacific and Latin America offer long-term upside, tempered by reimbursement constraints and limited infusion-center capacity. China's genomic newborn-screening pilot demonstrates technological readiness, recording lysosomal disorder detection at population scale. Japan participates actively in pivotal gene-therapy trials, which may accelerate domestic approval once global filings commence. Regional governments weigh the economic rationale of early detection against per-patient therapy costs, suggesting phased adoption as prices normalize. Collectively, geographic heterogeneity shapes a multi-speed growth pattern for the alpha-mannosidosis market.

Competitive Landscape

The market exhibits moderate concentration, anchored by Chiesi Farmaceutici, whose Lamzede franchise enjoys multinational approvals and dedicated real-world evidence programs. M6P Therapeutics advances mannose-6-phosphate-tagged gene constructs, leveraging six Rare Pediatric Disease Designations to secure expedited reviews. SmartPharm Therapeutics pursues a gene-encoded enzyme platform that could extend expression while sidestepping permanent genome edits. Orchard Therapeutics, now under Kyowa Kirin, brings commercial expertise from Lenmeldy’s launch, positioning the acquirer to cross-pollinate manufacturing and market-access capabilities.

Strategic collaborations intensify: Sobi broadened its Ionis alliance to deepen rare-disease reach, while REGENXBIO partnered with Nippon Shinyaku to commercialize MPS gene therapies that share manufacturing platforms with alpha-mannosidosis candidates. Chiesi’s 2024 research-grant initiative aims to foster academic breakthroughs in lysosomal science, signaling pre-emptive defense against gene-therapy disruption.

White-space competition centers on CNS-penetrant modalities: any company that demonstrates convincing neurocognitive benefit could rapidly capture share from velmanase alfa’s somatic-only relief. Manufacturer success will depend on differentiating across durability, convenience, and neurological efficacy rather than marginal biochemical endpoints. As pipeline heterogeneity grows, sustained portfolio-level expertise across multiple lysosomal storage disorders will increasingly determine bargaining power with payers and regulators alike. These factors collectively shape a dynamic competitive narrative for the alpha-mannosidosis market.

Alpha Mannosidosis Industry Leaders

Chiesi Farmaceutici S.p.A.

Sobi

Orchard Therapeutics plc

Avrobio Inc.

Ultragenyx Pharmaceutical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sobi expanded its partnership with Ionis Pharmaceuticals to include olezarsen commercialization outside the US.

- January 2025: REGENXBIO forged a USD 110 million collaboration with Nippon Shinyaku covering RGX-121 and related lysosomal-storage-disorder gene therapies

- June 2024: FDA granted approval to Lamzede, inaugurating enzyme replacement therapy access for US alpha-mannosidosis patients.

- January 2024: Kyowa Kirin completed its acquisition of Orchard Therapeutics to secure a rare-disease gene-therapy platform.

Global Alpha Mannosidosis Market Report Scope

| Enzyme Replacement Therapy |

| Hematopoietic Stem-Cell Transplantation |

| Gene Therapy |

| Supportive & Adjunctive Care |

| Investigational Pharmacological Chaperones |

| Intravenous Infusion |

| Surgical Transplant Administration |

| Intrathecal / CNS-direct Delivery |

| Systemic Viral Vector Delivery |

| Other Routes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Enzyme Replacement Therapy | |

| Hematopoietic Stem-Cell Transplantation | ||

| Gene Therapy | ||

| Supportive & Adjunctive Care | ||

| Investigational Pharmacological Chaperones | ||

| By Route of Administration | Intravenous Infusion | |

| Surgical Transplant Administration | ||

| Intrathecal / CNS-direct Delivery | ||

| Systemic Viral Vector Delivery | ||

| Other Routes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the addressable patient population for alpha-mannosidosis worldwide?

Fewer than 5,000 diagnosed patients are currently identified, reflecting an incidence of 1 in 500,000-1,000,000 live births.

What CAGR is projected for alpha-mannosidosis treatment spending between 2025 and 2030?

Aggregate spending is expected to climb at a 16.4% CAGR, rising from USD 433 million in 2025 to USD 938 million in 2030.

Which therapy type is forecast to grow fastest through 2030?

Gene therapy is projected to post an 18.4% CAGR, outpacing enzyme-replacement therapy as programs advance toward late-stage trials.

How do annual drug costs influence payer access decisions?

Price points above USD 650,000 per year trigger outcome-based contracts and patient-assistance schemes, especially in price-sensitive or single-payer systems.

Which region is expected to record the highest growth by 2030?

North America is set to achieve the fastest 15.7% CAGR following the FDA's approval of velmanase alfa and expanding newborn-screening initiatives.

Why is CNS penetration a critical unmet need in current treatments?

Present enzyme-replacement regimens do not cross the blood-brain barrier, leaving cognitive decline unmanaged and underscoring the need for CNS-targeted solutions.

Page last updated on: