Eosinophilic Esophagitis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

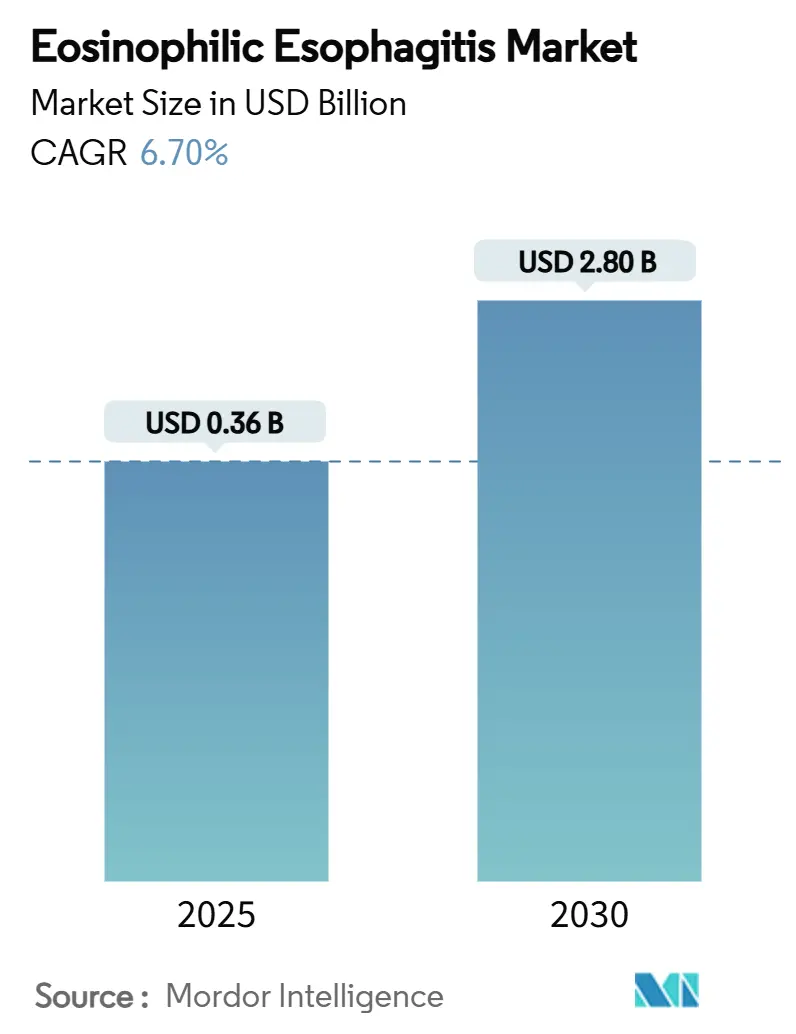

| Market Size (2025) | USD 0.36 Billion |

| Market Size (2030) | USD 2.80 Billion |

| Growth Rate (2025 - 2030) | 6.70% CAGR |

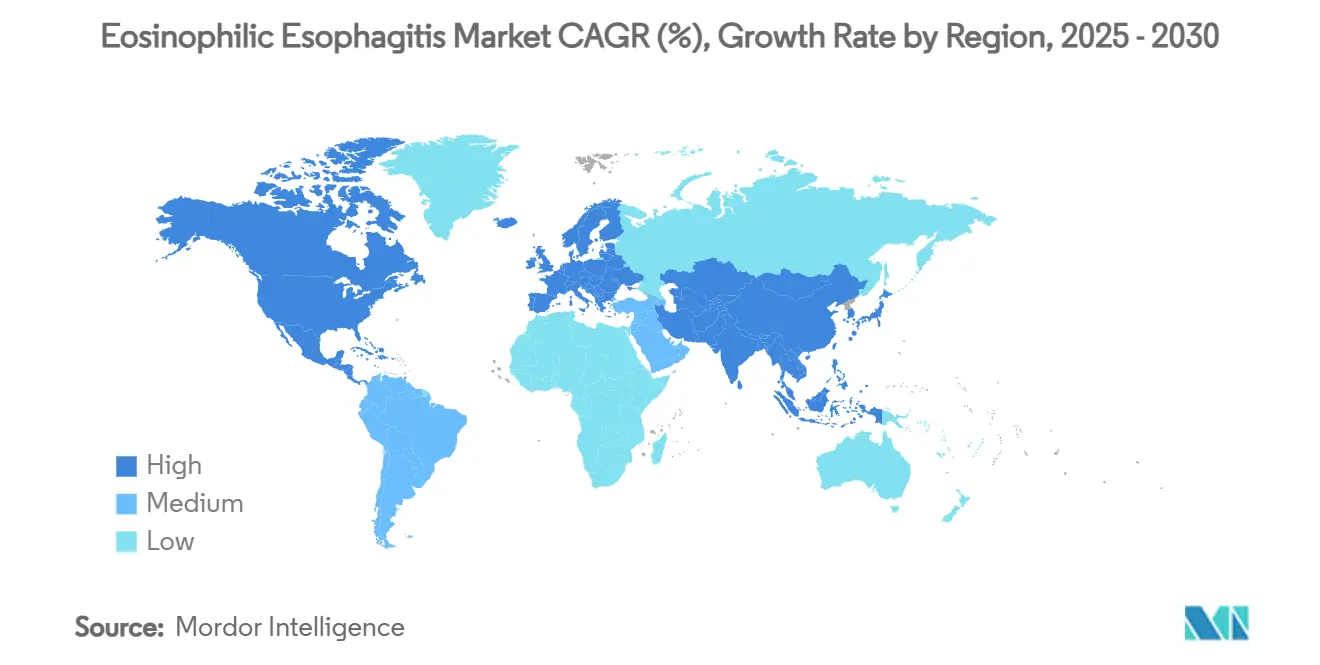

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Eosinophilic Esophagitis Market Analysis by Mordor Intelligence

The eosinophilic esophagitis market size is USD 0.36 billion in 2025 and is forecast to reach USD 2.80 billion by 2030, reflecting a 6.7% CAGR for the review period. Robust growth stems from earlier diagnosis, accelerated biologic approvals, and precision-therapy uptake that is moving clinical practice away from symptom suppression toward immunological disease control. Premium biologics command high prices, yet rising payer appetite for value-based contracts signals a willingness to reimburse when outcomes are proven. Regional performance diverges: North America benefits from advanced endoscopy penetration and specialty reimbursement, whereas Asia Pacific is adding capacity quickly and producing the fastest incremental volume. The competitive field is consolidating around two commercialized assets, while a broad pipeline explores IL-5, IL-15, Siglec-8, and long-acting local delivery technologies that could widen therapeutic choice and lower immunogenicity risk.[1]American Journal of Managed Care, “Value-Based Agreements in Specialty Drugs,” ajmc.com

Key Report Takeaways

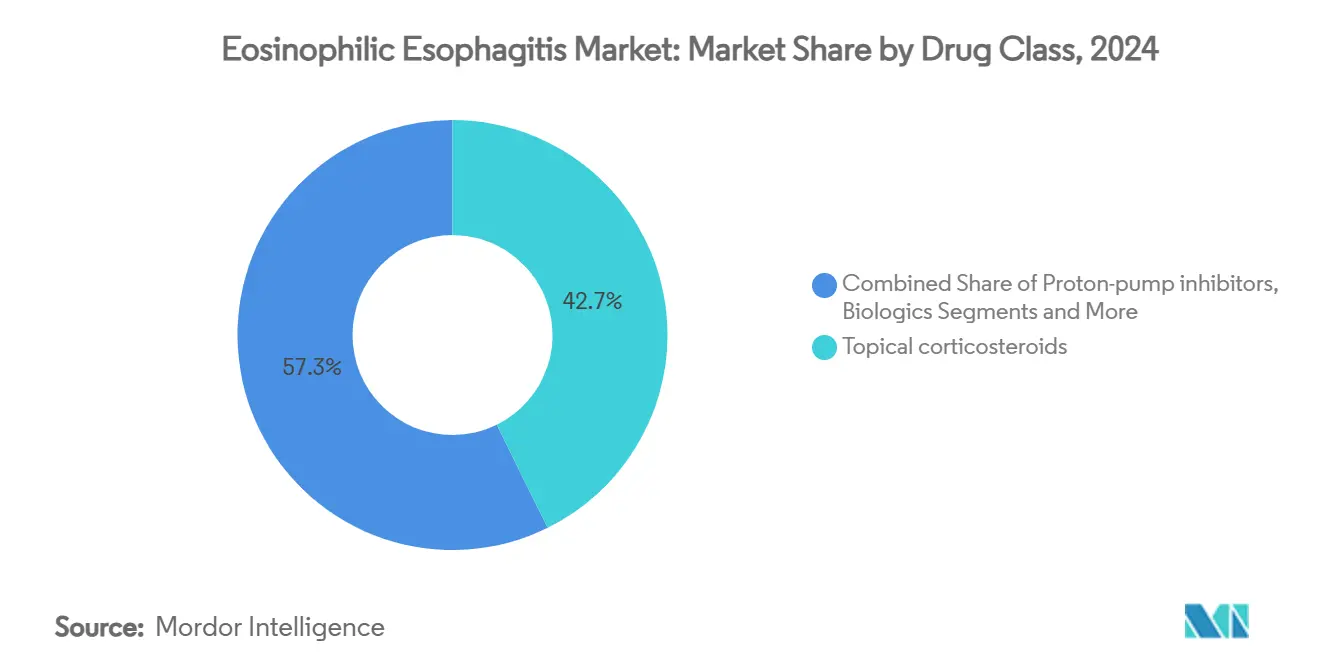

- By drug class, topical corticosteroids held 42.7% of the eosinophilic esophagitis market share in 2024, while biologics are advancing at an 8.8% CAGR through 2030.

- By route of administration, swallowed topical therapies captured 49.4% share of the eosinophilic esophagitis market size in 2024, and parenteral injection is expanding at a 6.3% CAGR to 2030.

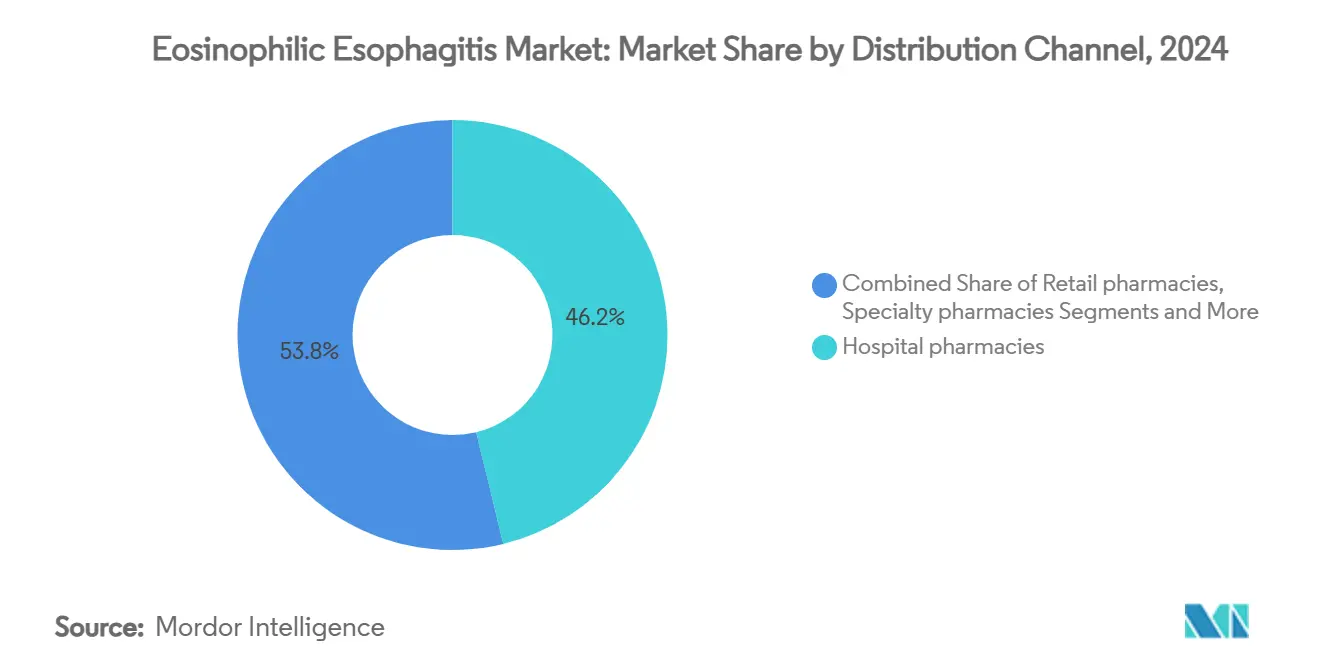

- By distribution channel, hospital pharmacies commanded 46.2% revenue in 2024; specialty pharmacies post the highest projected CAGR at 7.1% through 2030 as biologic dispensing requirements broaden.

- By geography, North America led with 55.1% revenue share in 2024, whereas Asia Pacific is growing at a 9.4% CAGR to 2030.

Global Eosinophilic Esophagitis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence & improved diagnosis rates | +1.80% | North America, Europe | Medium term (2-4 years) |

| FDA approval of first targeted biologics | +2.10% | North America, Europe, expanding to Asia Pacific | Short term (≤ 2 years) |

| Launch of budesonide oral suspension | +1.20% | North America core, expanding globally | Short term (≤ 2 years) |

| Adoption of peptide-based non-invasive tests | +0.90% | Early adoption in North America & Europe | Medium term (2-4 years) |

| Long-acting local delivery platforms | +0.70% | Global, development phase | Long term (≥ 4 years) |

| Value-based contracts for high-cost biologics | +0.60% | Mature markets in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence & Improved Diagnosis Rates

Improved biopsy protocols and higher gastroenterologist awareness have lifted prevalence to 163.08 cases per 100,000 among commercially insured populations. The widening diagnostic net is funneling previously missed patients into the eosinophilic esophagitis market, enlarging therapeutic demand and supporting specialist clinic formation. Training programs standardize histological criteria, thereby reducing under-diagnosis that once constrained revenue opportunity. Screening of atopic cohorts is gaining traction, meaning addressable volume will keep expanding during the medium term. These dynamics underpin sustained uptake of both traditional and biologic therapies in the eosinophilic esophagitis market.

FDA Approvals of First Targeted Biologics

Dupixent achieved 59% histological remission versus 6% for placebo in pivotal trials and set a new efficacy benchmark. It's 2022 U.S. clearance and 2023 European nod positioned biologics as front-line care for severe cases, propelling premium growth within the eosinophilic esophagitis market. The approval validated IL-4/IL-13 signaling as a target and sparked pipeline interest in IL-5 and Siglec-8 antibodies. Physician guidelines now list Dupixent ahead of long-term corticosteroids, accelerating switch dynamics. Payer adoption remains robust under outcome-based contracts, further strengthening momentum.[3]European Medicines Agency, “Dupixent EPAR,” ema.europa.eu

Launch of Budesonide Oral Suspension

Eohilia delivered 53% and 38% histological remission across two Phase III arms and, after a prior rejection, won FDA approval in February 2024. The oral suspension optimizes esophageal contact time and offers pediatric and compliance advantages versus injectables. Takeda projects USD 300–500 million peak sales, illustrating commercial appetite for novel formulations in the eosinophilic esophagitis market. The asset’s success confirms that differentiated delivery science can secure regulatory wins even in crowded corticosteroid classes.

Adoption of Peptide-Based Non-Invasive Diagnostics

String tests and peptide assays under development can monitor mucosal inflammation without repeat endoscopies, easing patient burden and reducing costs. Early use in specialist centers shows correlation with biopsy outcomes, and wider rollout could raise monitoring frequency and refine dosing decisions. Non-invasive options are especially attractive for children, a segment that often avoids repeated sedation. As validation builds, these platforms may become standard adjuncts, raising the quality of disease management in the eosinophilic esophagitis market.[2]UCSF, “Non-Invasive Diagnostics for EoE,” ucsf.edu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of biologic therapies | -1.40% | Global, more acute in emerging markets | Short term (≤ 2 years) |

| Under-diagnosis in primary care | -0.80% | Global, pronounced in rural settings | Medium term (2-4 years) |

| 12-week treatment cap for steroid suspensions | -0.60% | Global regulatory requirement | Short term (≤ 2 years) |

| Limited long-term pediatric safety data | -0.50% | Global, impacts decision making for minors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologic Therapies

Annual biologic spend can exceed USD 36,000, leading to step-therapy protocols and prior authorizations that delay initiation. Cost hurdles are steeper in low- and middle-income settings, reinforcing a two-tiered global therapeutic landscape within the eosinophilic esophagitis market. Even in high-income markets, administrative complexity can discourage prescribing in marginal cases, curbing potential volume. Ancillary expenses such as injection training and monitoring raise the total burden further.

Under-Diagnosis in Primary Care Settings

Symptom overlap with reflux disease causes delayed referrals and missed cases, constraining patient flow into specialty pipelines. Educational campaigns exist but remain uneven, especially outside urban centers. Chronic misclassification slows adoption of premium products, reducing overall revenue potential for the eosinophilic esophagitis market until diagnostic literacy spreads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Precision Biologics Fuel Premium Uptake

Market leaders’ topical corticosteroids generated 42.7% revenue in 2024, reflecting broad guideline endorsement and affordability. That share is expected to moderate as biologics expand at an 8.8% CAGR, propelled by Dupixent’s clinical profile and pipeline antibodies such as CC-93538 and lirentelimab. Proton-pump inhibitors retain value as adjunct therapy, while elemental diets occupy a specialized niche. The eosinophilic esophagitis market size for biologics is projected to reach USD 1.25 billion by 2030, underscoring the shift toward pathway-specific modulation. Traditional therapies remain relevant because payers often mandate a steroid trial before biologic escalation, yet patient and clinician preference is tilting toward earlier precision intervention.

Investment patterns reinforce biologics’ ascendancy. Novartis paid USD 250 million to add an anti-IL-15 monoclonal antibody, illustrating the strategic urgency to diversify mechanisms of action. Competitors differentiate via dosing schedules, safety tolerability, and pediatric labeling, seeking advantage in a still-concentrated therapeutic class. As evidence grows, first-line biologic placement could emerge for severe phenotypes, expanding addressable volume for the eosinophilic esophagitis market.

By Route of Administration: Oral Convenience Versus Injectable Efficacy

Swallowed topical formulations led with 49.4% of the eosinophilic esophagitis market share in 2024, thanks to ease of use and favorable safety. Parenteral injection, dominated by subcutaneous biologics, posts the highest 6.3% CAGR as systemic immunomodulation secures guideline traction. Oral tablets and capsules sustain proton-pump inhibitor demand, while orodispersible forms grow slowly in pediatric care. For adults, willingness to self-inject rises when remission odds prove superior. The eosinophilic esophagitis market size attached to parenteral agents could exceed USD 1.5 billion by 2030, provided pipeline success.

Formulation science remains pivotal. Companies pursue muco-adhesive polymers to extend esophageal exposure, while device makers refine auto-injectors that lower administration anxiety. Long-acting depot injections such as EP-104GI may recalibrate the adherence equation by reducing dosing frequency. Patient-centric delivery will therefore remain a core competitive lever in the eosinophilic esophagitis market.

By Distribution Channel: Specialty Infrastructure Gains Momentum

Hospital pharmacies supplied 46.2% of prescriptions in 2024, consistent with specialist-led diagnosis. Specialty pharmacies are growing at a 7.1% CAGR because biologic cold-chain handling, prior authorization services, and nursing support align with their business model. Retail outlets retain maintenance therapy refills, while online options rise for chronic reorder convenience. The eosinophilic esophagitis market size routed through specialty channels could more than double by 2030, mirroring biologic penetration.

Manufacturers increasingly embed nurse hotlines, adherence apps, and copay support into specialty contracts, integrating distribution with patient engagement. Payers also favor these channels for tighter utilization oversight and data capture. Consequently, channel strategy is now as crucial as clinical differentiation in the eosinophilic esophagitis market.

Geography Analysis

North America produced 55.1% of global revenue in 2024, buoyed by early regulatory approvals, broad insurance coverage, and an extensive gastroenterology network. Dupixent and Eohilia both launched first in the United States, and value-based contracts propel formulary acceptance despite premium pricing. Canada shows rising uptake as provincial formularies adopt biologic reimbursement, whereas Mexico advances more slowly, given budget limits and specialist scarcity. The region’s innovation density should preserve leadership, although cost-containment policies may temper near-term acceleration in the eosinophilic esophagitis market.

Europe ranks second with cohesive European Medicines Agency processes accelerating multi-country rollouts. Germany and the United Kingdom are vanguards, hosting specialized centers and active clinical trials that inform guideline evolution. France, Italy, and Spain follow with reimbursement frameworks that typically require steroid failure before biologic initiation. Eastern European states lag in both diagnostics and high-cost therapy funding, softening collective growth. Still, EMA approval of Dupixent opened access for an estimated 50,000 patients, supplying meaningful volume to the eosinophilic esophagitis market.

Asia Pacific is the fastest mover, expanding at a 9.4% CAGR through 2030. Japan leads regional diagnosis and guideline adoption, aided by robust endoscopic capacity. South Korea and Australia accelerate on the back of universal insurance and academic research hubs. China and India remain under-penetrated but show improving specialist numbers and public-private hospital investment. Long-term, rising middle-class demand and healthcare modernization position Asia Pacific to narrow the revenue gap, provided biologic affordability improves within the eosinophilic esophagitis market.

Competitive Landscape

The eosinophilic esophagitis market shows moderate concentration with two commercial front-runners. Sanofi-Regeneron’s Dupixent anchors the biologic class, while Takeda’s Eohilia pioneers FDA-cleared oral suspension therapy. Combined, they generate the majority of current branded sales and enjoy regulatory exclusivity windows that deter near-term parity challengers. Pipeline candidates from Bristol Myers Squibb, Allakos, and AstraZeneca seek to differentiate by novel cytokine targets and administration ease, increasing medium-term rivalry.

Investment in mechanism diversity is brisk. Novartis paid USD 250 million for Calypso Biotech’s anti-IL-15 antibody, evidencing an appetite for early-stage assets with first-in-class potential. Eupraxia’s polymer depot technology offers longer dosing intervals that could threaten daily oral suspensions, whereas Allakos explores Siglec-8 inhibition for simultaneous mast-cell modulation. Company strategies now extend beyond molecules to integrated patient support, specialty distribution partnerships, and data-driven reimbursement models that align with payer expectations.

Barriers remain steep: complex biologic manufacturing, stringent pediatric safety mandates, and diagnostic underreach restrict rapid follower emergence. Nonetheless, white space exists in pediatric-specific formulations, combination regimens, and diagnostic-therapy bundles. Firms with robust real-world evidence programs and scalable patient-engagement infrastructure will likely secure a durable edge in the eosinophilic esophagitis market.

Eosinophilic Esophagitis Industry Leaders

Sanofi SA

Takeda Pharmaceutical Co. Ltd.

Dr. Falk Pharma GmbH

GlaxoSmithKline plc

AstraZeneca plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Eupraxia Pharmaceuticals announced positive data from the fifth cohort of its RESOLVE Phase 1b/2a trial for EP-104GI, including one complete histological remission.

- June 2025: EA Pharma and Ensho Therapeutics signed a worldwide exclusive license for EA1080, an oral α4β7 integrin antagonist. Phase 2 trials are slated for early 2025.

- March 2025: AstraZeneca initiated a clinical trial assessing the efficacy and safety of Tezepelumab in patients with eosinophilic esophagitis, expanding the company's pipeline in allergic and inflammatory diseases.

- February 2024: Takeda received FDA approval for EOHILIA (budesonide oral suspension) for patients aged 11 and older.

Global Eosinophilic Esophagitis Market Report Scope

| Biologics (IL-4/IL-13, IL-5, Siglec-8 mAbs) |

| Topical corticosteroids |

| Proton-pump inhibitors |

| Dietary therapies & elemental formulas |

| Others |

| Parenteral injection |

| Oral suspension / viscous slurry |

| Oro-dispersible tablet (ODT) |

| Oral tablet / capsule |

| Hospital pharmacies |

| Retail pharmacies |

| Specialty pharmacies |

| Online pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Biologics (IL-4/IL-13, IL-5, Siglec-8 mAbs) | |

| Topical corticosteroids | ||

| Proton-pump inhibitors | ||

| Dietary therapies & elemental formulas | ||

| Others | ||

| By Route of Administration | Parenteral injection | |

| Oral suspension / viscous slurry | ||

| Oro-dispersible tablet (ODT) | ||

| Oral tablet / capsule | ||

| By Distribution Channel | Hospital pharmacies | |

| Retail pharmacies | ||

| Specialty pharmacies | ||

| Online pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the eosinophilic esophagitis market growing?

Revenue is advancing at a 6.7% CAGR from USD 360 million in 2025 to USD 2.80 billion by 2030, driven by biologic adoption and earlier diagnosis.

Which region leads global sales?

North America holds 55.1% of 2024 revenue due to early approvals and broad insurance coverage, although Asia Pacific records the fastest 9.4% CAGR.

What drug class is expanding quickest?

Biologics grow at 8.8% CAGR through 2030 owing to superior histological remission compared with topical corticosteroids.

Why are specialty pharmacies gaining share?

They support cold-chain storage, prior authorization and patient training required for biologics, rising at a 7.1% CAGR.

What limits long-term steroid use?

Global guidelines cap continuous budesonide suspension therapy at 12 weeks, encouraging the shift toward maintenance biologics.

Page last updated on: