Antacids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.30 Billion |

| Market Size (2031) | USD 8.65 Billion |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

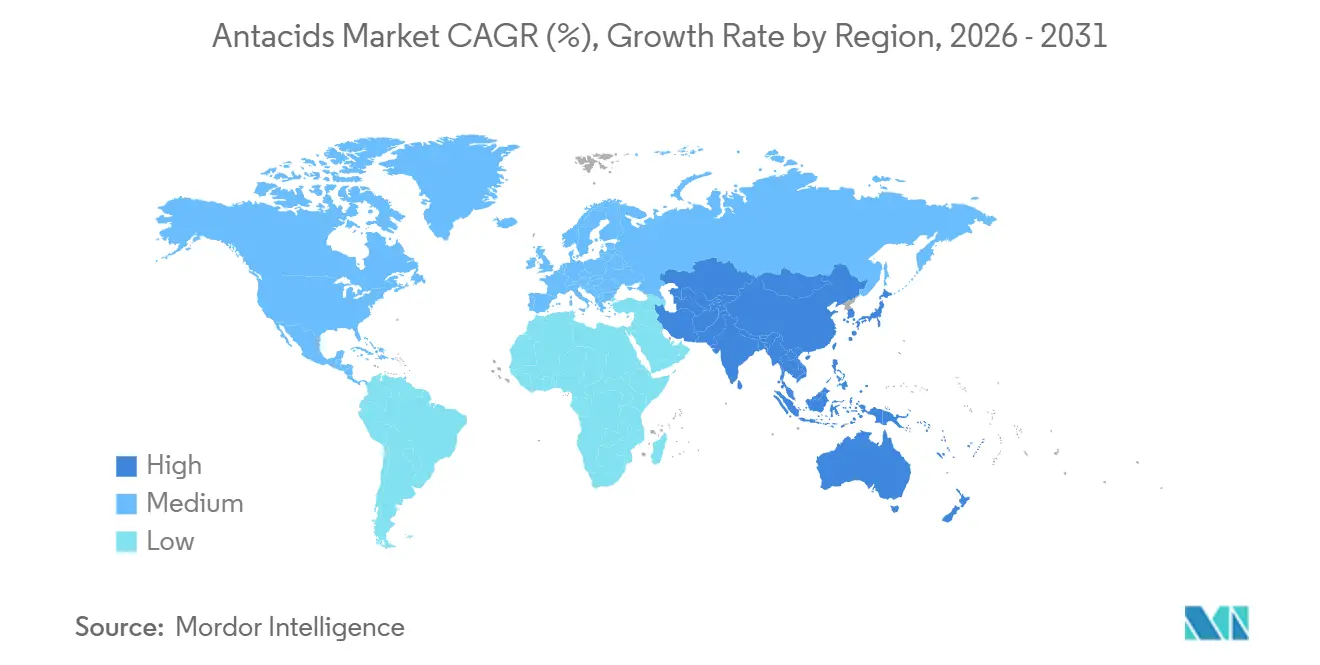

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

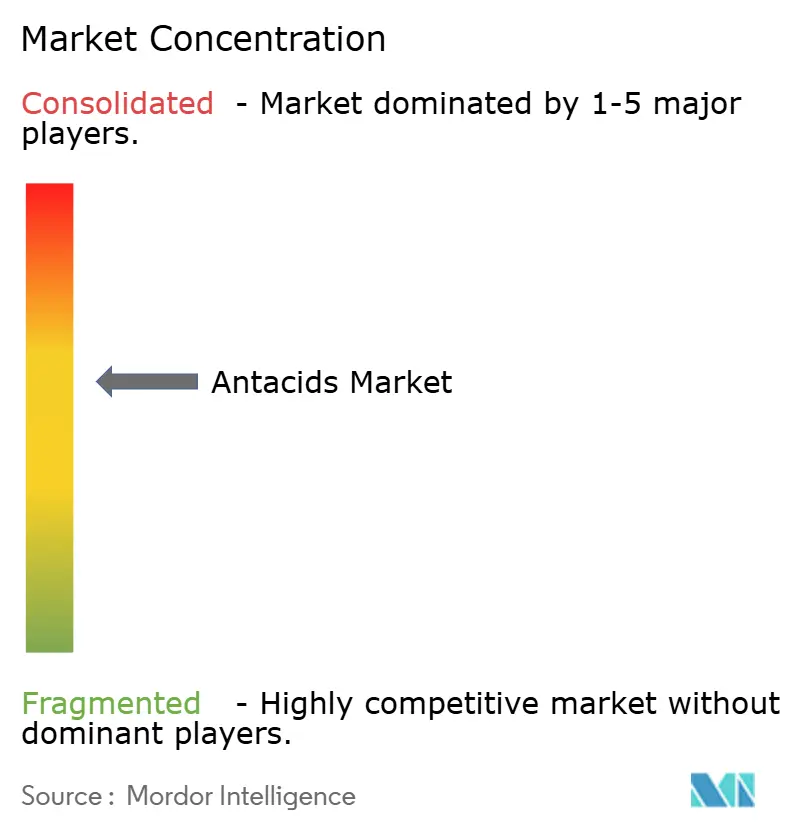

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antacids Market Analysis by Mordor Intelligence

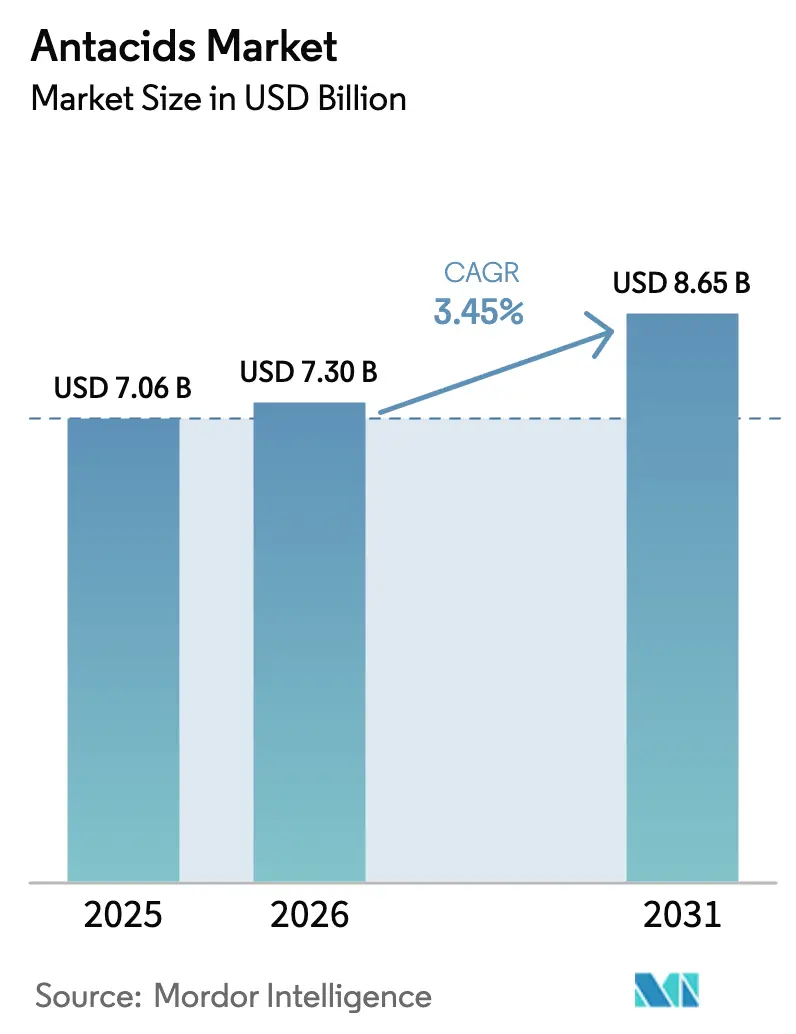

The Antacids Market size is projected to expand from USD 7.06 billion in 2025 and USD 7.30 billion in 2026 to USD 8.65 billion by 2031, registering a CAGR of 3.45% between 2026 to 2031.

The figures underscore a category that grows through formulation upgrades rather than surging volume, yet the underlying antacids market size remains resilient in the face of prescription alternatives. Consistent demand is being lifted by aging populations, widening e-commerce access, and the rapid uptake of alginate-based products that promise drug-free mechanical reflux protection. Retail pharmacies still generate most unit sales, but Amazon Pharmacy and other digital storefronts are shifting consumer expectations toward auto-replenishment and same-day delivery, prompting incumbents to overhaul supply chains. Ingredient innovation favors clean-label calcium carbonate replacements, while gummy and soft-gel formats turn a previously utilitarian remedy into a lifestyle item. Competitive intensity is moderate because the five largest companies control roughly half of the antacids market, leaving space for region-specific specialists and online challengers to pursue price-sensitive niches.

Key Report Takeaways

- By active ingredient, calcium carbonate retained 35.53% antacids market share in 2025, whereas alginates are the fastest-growing class at an 8.85% CAGR to 2031.

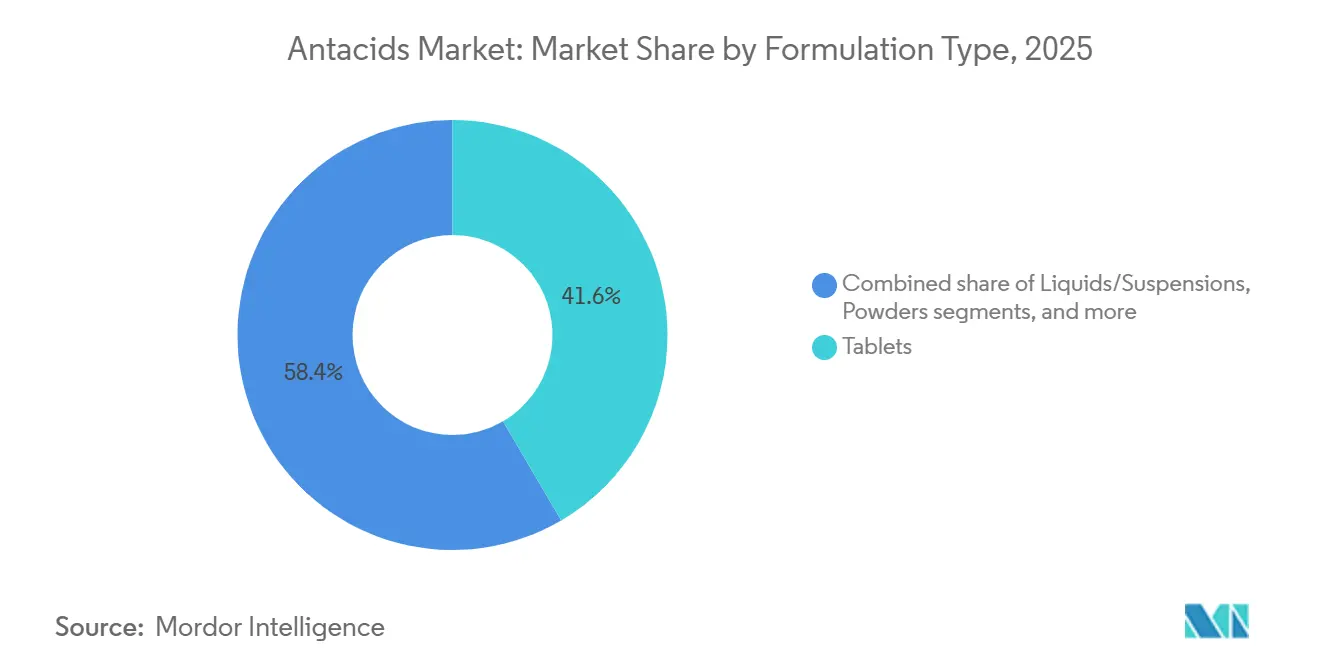

- By formulation, tablets led with 41.56% revenue in 2025, while gummies and chewable soft-gels are advancing at 9.25% CAGR through 2031.

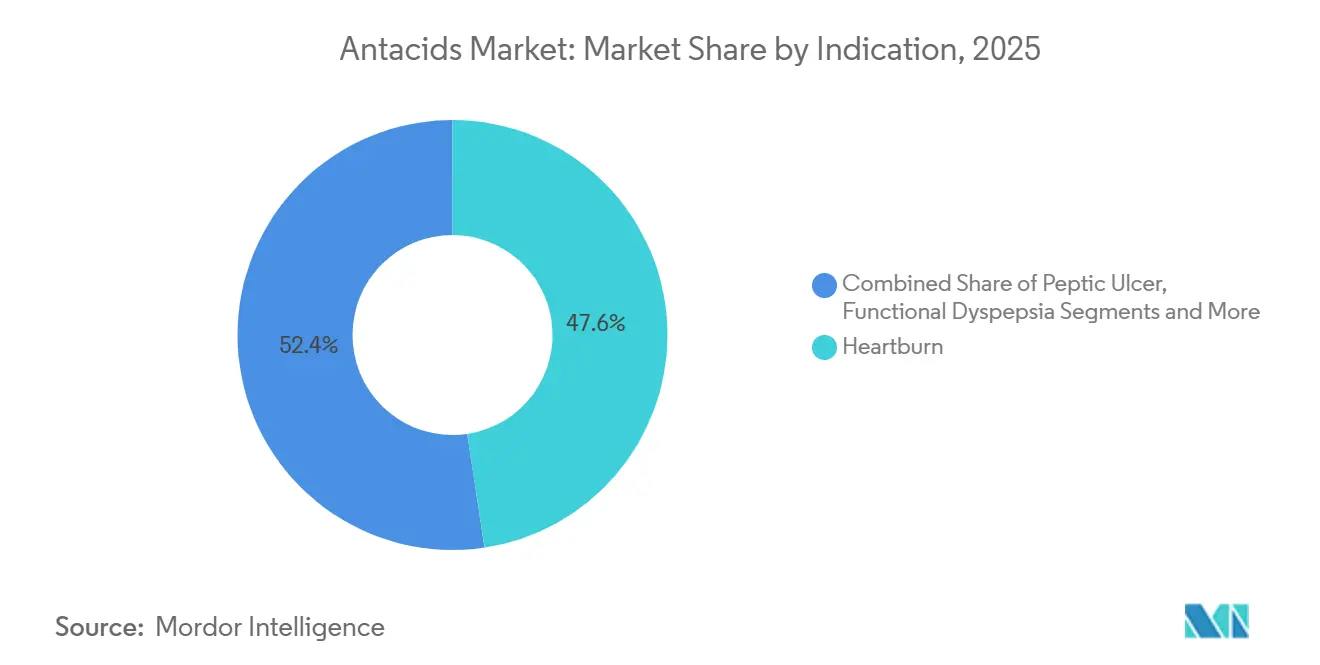

- By indication, heartburn held 47.63% volume share in 2025; functional dyspepsia is expanding most rapidly at 9.27% CAGR.

- By distribution channel, retail pharmacies captured 53.63% of 2025 sales, whereas e-commerce is rising at a 12.11% CAGR.

- By geography, North America accounted for 39.53% of 2025 revenue, but Asia-Pacific is the fastest-growing region at 9.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antacids Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and rising gastrointestinal disorder incidence | +0.8% | Global, notably Japan, Western Europe, North America | Long term (≥ 4 years) |

| Unhealthy dietary habits and sedentary lifestyles | +0.7% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Over-the-counter accessibility and self-medication culture | +0.6% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Expansion of retail pharmacy and e-commerce channels | +0.9% | Global, first movers in United States, United Kingdom, Australia | Medium term (2-4 years) |

| Microbiome-focused combination research and development | +0.3% | North America, European Union | Long term (≥ 4 years) |

| Digital gut-symptom tracking partnerships | +0.2% | North America, select Asia-Pacific metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Gastrointestinal Disorder Incidence

Adults aged 65 and older will comprise 16% of the world’s residents by 2030, and this demographic experiences gastroesophageal reflux disease at nearly twice the rate of younger cohorts, making them habitual purchasers in the antacids market. Japan already reports more than 29% of its population in the senior bracket, and per-capita antacid use there outpaces all other countries. European economies such as Italy and Germany will reach senior shares of roughly 28% by 2031, sustaining baseline demand even as prescription proton pump inhibitors (PPIs) address chronic reflux. Manufacturers are answering with lower-sodium liquids that accommodate hypertension management and with bundle packs that pair antacids with bone-health nutrients. Collectively, demographic tailwinds secure a dependable slice of the antacids market over the long term.

Unhealthy Dietary Habits and Sedentary Lifestyles

Urbanization across Asia-Pacific is amplifying consumption of high-fat convenience foods, pushing heartburn incidence upward and generating fresh demand in the antacids market. Obesity rates in China are on course to exceed 14% by 2025, while India’s largest cities are recording functional dyspepsia prevalence near 20%. Producers have an untapped opportunity to localize formulations—such as adding herbal demulcents helpful against spicy cuisines—yet most brands continue to export global SKUs without regional tweaks, leaving room for domestic challengers.

Over-the-Counter Accessibility and Self-Medication Culture

L23: Pharmacy-counter liberalization lets consumers self-treat episodic heartburn without a doctor’s visit, supporting rapid off-take for the antacids market in North America and much of Western Europe. China streamlined over-the-counter approvals in 2024, accelerating multinational launches, while India retains mandatory pharmacist counseling for some formulations, moderating growth but encouraging premium SKU introductions.[1]National Medical Products Administration, “Notice on OTC Registration Reform,” nmpa.gov.cn.

Microbiome-Focused Combination Research and Development

New research linking long-term acid suppression to dysbiosis has accelerated patent filings that pair alginates with probiotics. While evidence remains at an early stage, major suppliers view microbiome claims as a premiumization lever inside the antacids market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Switch to proton pump inhibitors and H2 antagonists | -0.9% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Safety concerns with chronic antacid use | -0.4% | North America, European Union | Medium term (2-4 years) |

| Volatile mineral-based raw-material supply | -0.3% | Global, supply concentrated in China | Medium term (2-4 years) |

| Environmental, social, and governance aluminum scrutiny | -0.2% | European Union, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Switch to Proton Pump Inhibitors and H2 Antagonists

United States PPIs exceed USD 4 billion in annual retail sales, reflecting physician preference for once-daily acid suppression and placing a ceiling on potential volume gains for the antacids market. Yet emerging safety concerns regarding chronic PPI use are nudging certain patients back toward intermittent antacids, creating a partial offset.

Safety Concerns with Chronic Antacid Use

Magnesium-based products risk hypermagnesemia in renal-impaired users, and high-dose calcium carbonate can cause milk-alkali syndrome, prompting label-reading consumers to seek low-dose or non-systemic alternatives and tempering growth in the antacids market[2]United States FDA, “Drug Safety Communications for Antacids,” fda.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation Type: Gummies Reshape Dosage Preferences

The antacids market size for tablets reached 41.56% of revenue in 2025, whereas gummies and chewable soft-gels are climbing at a 9.25% CAGR, the fastest within this segmentation. Gummies benefit from confectionery textures and the ability to layer sleep-enhancing melatonin, recasting antacid use as part of a broader nighttime routine. Meanwhile, liquids grow at 7.7% as pediatric and geriatric cohorts expand. Powders and effervescents remain small but stable, prized for rapid onset by travelers and sports enthusiasts.

Liquids face logistic cost pressure because packaging is heavier and more fragile, but their palatability gains when manufacturers employ taste-masking technology. Traditional tablets will likely keep the largest slice of the antacids market, yet their dominance erodes as millennials and Gen-Z age into higher gastric-symptom prevalence and import gummy preferences from adjacent supplement categories.

By Active Ingredient Type: Alginates Gain Clinical Credibility

Calcium carbonate commanded 35.53% of 2025 revenue thanks to its dual benefit of neutralizing acid and delivering dietary calcium, but alginates are the standout growth engine at an 8.85% CAGR. The raft-forming mechanism resonates with consumers seeking drug-free solutions and differentiates brands such as Gaviscon. Magnesium and aluminum compounds maintain mid-tier status but face safety perceptions that limit heavy repeat use. Sodium bicarbonate remains a budget choice, useful for rapid, episodic relief yet hampered by high sodium content.

Combination products blend calcium with magnesium hydroxide or add simethicone to tackle bloating, appealing to functional dyspepsia sufferers. Raw-material cost is the primary brake on alginate roll-out because pharmaceutical-grade sodium alginate trades at a 50% premium to carbonate salts, but educational campaigns and growing clinician endorsement are beginning to justify the price differential inside the antacids market.

By Indication: Functional Dyspepsia Emerges from GERD's Shadow

Heartburn dominated 47.63% of 2025 purchases, yet functional dyspepsia is gaining share at 9.27% CAGR as Rome IV guidelines encourage symptom-specific therapy. Patients reporting early satiety and bloating respond better to formulations that combine antacids with simethicone or herbal carminatives, an area largely ignored by mainstream brands.

GERD sufferers often escalate to prescription PPIs, capping the antacids market opportunity in chronic cases, whereas peptic ulcer disease now occupies a minor niche due to Helicobacter pylori eradication programs. The growth runway hinges on whether marketers can reframe antacids as a first-step answer for complex upper-GI discomfort rather than a narrow heartburn fix.

By Distribution Channel: E-Commerce Disrupts Retail Pharmacy Dominance

Retail pharmacies captured 53.63% of 2025 sales, but online storefronts are expanding at 12.11% CAGR thanks to seamless reordering and last-mile delivery upgrades. Subscription customers exhibit 25% higher annual spend than one-off buyers, a metric that drives brand valuations for direct-to-consumer entrants.

Hospital pharmacies remain niche, covering in-patient transitions off intravenous PPIs. Convenience stores, supermarkets, and travel hubs account for the balance, providing impulse-purchase settings that digital channels cannot replicate. Incumbents respond with omnichannel programs that integrate loyalty points and curbside pickup, yet margins tighten as fulfillment costs stack up.

Geography Analysis

North America, at 39.53% of 2025 revenue, remains the largest territory in the antacids market because of high self-medication rates and fast product switching upon symptom onset. Unit volumes plateau as heavy PPI users emerge, but gummy and clean-label launches offset attrition. Canada and Mexico expand at mid-single-digit rates as cross-border e-commerce brings United States SKUs into previously insulated retail environments.

Asia-Pacific is the standout growth engine, forecast to add nearly USD 1 billion in incremental sales through 2031 at a 9.51% CAGR. Japan’s unprecedented aging profile propels liquids and low-sodium variants, while China’s streamlined over-the-counter rules shorten launch cycles for foreigners and domestic players alike. India illustrates urban–rural divergence: metropolitan dyspepsia prevalence hits 20%, yet price-sensitive rural consumers gravitate toward generic powders.

Europe sits in between, challenged by strict European Medicines Agency labeling and widespread PPI reimbursement. The United Kingdom follows a step-up protocol that begins with lifestyle modification and antacids, ensuring baseline demand. Brexit-related customs complexities inflate import costs, nudging some companies to regionalize manufacturing.

The Middle East, Africa, and South America together contribute a modest but rising share. Gulf Cooperation Council nations show obesity rates above 30%, stimulating heartburn complaints, yet e-commerce infrastructure is still developing. Brazil and Argentina remain volatile; currency swings push shoppers toward private-label products, favoring local contract manufacturers.

Regulatory Landscape

In the United States, antacids are regulated under the FDA OTC Monograph system, specifically OTC Monograph M001 for antacid products. The monograph sets standardized requirements on permitted active ingredients, indications (such as heartburn and acid indigestion), and mandatory warning statements and drug-interaction language. Manufacturing and packaging are governed by FDA current good manufacturing practice (CGMP) regulations, so quality-system maturity and compliant labeling often act as key launch gates and can trigger reformulation or artwork changes across portfolios.

Across Europe and the United Kingdom, many established antacid combinations (including sodium alginate, sodium bicarbonate, and calcium carbonate) proceed through marketing authorization pathways that rely on well-established use dossiers, including bibliographic applications under Article 10a of Directive 2001/83/EC. An anchor requirement is at least 10 years of recognized medicinal use in the EU. The EMA also maintains scientific guidance for development of medicines for gastro-oesophageal reflux disease (GORD), while distinguishing prescription GORD development expectations from OTC products positioned for symptomatic relief, which keeps the bar for new OTC claims tied to appropriate evidence and compliant product information rather than full prescription-style clinical programs.

Competitive Landscape

The antacids market shows moderate consolidation: Haleon, Bayer, Sanofi, and others capture significant share in 2025 revenue, leaving ample headroom for regional and digital disruptors. Haleon leads through multiformat franchises such as TUMS, Rolaids, and ENO and highlighted 3.8% digestive-health growth in its Q3 2024 investor call[3]Haleon, “Q3 2024 Earnings Call Transcript,” haleon.com. Reckitt’s alginate-driven Gaviscon maintains price premiums in the United Kingdom and Australia but trails in North America.

Private-label ranges from Perrigo and Akums own nearly one-quarter of unit sales, holding particular sway in price-sensitive markets. Digital-first entrants like Wonderbelly pursue millennials with clean-label narratives and social-commerce distribution, though combined turnover remains below USD 50 million. Technology partnerships are nascent; no manufacturer holds an exclusive with telehealth platforms, but pilots suggest algorithmic referrals could become an influential demand lever.

Innovation gaps include functional dyspepsia-specific blends and validated microbiome-friendly combinations. Both areas await robust clinical backing, offering incumbents a path to differentiate if they can move evidence from pilot to publication.

Antacids Industry Leaders

Sanofi S.A

Bayer AG

Haleon Plc

Sun Pharmaceutical Industries Ltd.

Johnson & Johnson (Kenvue)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product differentiation is moving beyond simple neutralization toward combination and format-led propositions that support premium pricing and stronger retail visibility. Bayer India introduced Alka-Seltzer in June 2026 as an effervescent antacid that incorporates Lactobacillus probiotics, positioning antacid use alongside broader digestive wellness behaviors in self-care. Quest Products also launched OraHealth Antacid Melts in May 2026, using a stick-on technology designed to adhere in the mouth and release calcium carbonate over time, creating room for nighttime and convenience-led use cases.

Supply-chain localization and manufacturing modernization are improving competitive positioning in high-growth and import-dependent regions, with direct implications for lead times, cost-to-serve, and channel fill rates. STADA signed to establish a manufacturing hub in Riyadh in February 2026, citing annual capacity above 300 million units across products that include antacids, while Bayer completed a USD 44 million expansion at its Myerstown, Pennsylvania consumer-health site in April 2025, adding packaging lines and automated logistics that can improve responsiveness for high-velocity OTC categories. In demand creation, India-focused clinical and real-world evidence around sodium alginate raft-forming antacids, including a multicenter post-marketing surveillance study published in March 2026 reporting high relief rates, supports more assertive education by alginate-led brands and can encourage line extensions across alginate-based and combination preparations.

Recent Industry Developments

- June 2026: Bayer India launched Alka-Seltzer in India as an effervescent antacid in single-use sachets that incorporates Lactobacillus probiotics. The new positioning expands antacid use from episodic symptom relief to a gut-health adjacent self-care proposition, increasing competitive pressure on local and multinational OTC portfolios to add differentiated claims and formats.

- April 2025: Sanofi completed the sale of a 50.0% controlling stake in its consumer healthcare business, Opella, to Clayton, Dubilier & Rice (CD&R). The transaction increases the likelihood of sharper capital allocation and tighter portfolio focus within large OTC digestive-health lines, given that Opella operates with a more independent ownership structure.

- June 2024: Sun Pharmaceutical Industries signed a non-exclusive patent licensing agreement with Takeda to commercialize vonoprazan tablets (Voltapraz) in India for acid peptic disorders. Expanded access to advanced acid-suppression therapies can influence the OTC antacid category by shifting some chronic sufferers toward prescription options while keeping antacids relevant for intermittent relief and step-up regimens.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers antacid products that neutralize stomach acid and are purchased for fast relief from heartburn, indigestion, and related acid discomfort. Revenue is counted from sales through retail and hospital-linked channels, and tracked across major geographies.

Scope exclusions: We exclude prescription-only acid suppression drugs (such as PPIs and H2 blockers), non-antacid digestive aids, herbal remedies, compounded mixes, and intravenous preparations.

Segmentation Overview

- By Formulation Type

- Tablets

- Liquids / Suspensions

- Powders

- Gummies / Chewable Soft-Gels

- Effervescent Granules

- Other Formulations

- By Active Ingredient Type

- Calcium Carbonate

- Magnesium Compounds

- Aluminium Compounds

- Sodium Bicarbonate

- Alginate-Based

- Combination Preparations

- By Indication

- Heartburn

- Gastroesophageal Reflux Disease (GERD)

- Peptic Ulcer

- Functional Dyspepsia

- Other Acid-Related Disorders

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- E-Commerce

- Other Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping demand conditions for reflux and dyspepsia symptoms using public health and demographic signals, then aligning those with how antacids are typically purchased and used. For context, we use sources such as the US CDC, the NIH and its PubMed-indexed clinical literature, the World Health Organization, and the World Bank for population and macro indicators.

To keep the market model grounded, we also check product and ingredient context from public references such as the FDA OTC monographs and safety communications. Where available, we use trade and shipment direction using customs and tariff-line statistics to confirm sourcing and flow patterns. On the supply side, we use company filings, investor presentations, and reputable press coverage to validate portfolio exposure, geographic mix, and channel emphasis. In a few cases, paid subscriptions are used only for company financials and intelligence and for patent look-ups to clarify formulation activity. These desk sources are illustrative, and additional public references were used to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure-test desk assumptions around what is counted as an antacid sale, how combination products are treated, and how pricing changes show up by channel. We speak with a balanced mix of manufacturers, distributors, pharmacists, and healthcare-facing respondents across APAC, EMEA, and the Americas, so gaps in public data can be resolved into selling patterns used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 13% | APAC: 46% |

| Mid tier: 44% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 18% | Managers: 58% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down structure where treated and self-care demand is reconstructed from population by age band, symptom prevalence for heartburn and related conditions, and the share of consumers that use antacid therapy for quick relief. Those demand pools are then translated into value using observed pack-size norms, channel mix, and typical price bands, and the totals are checked against selective bottom-up approximations such as sampled brand and private-label pricing, a light volume cross-check from retail-facing interviews, and supplier and distributor sense checks.

The model focuses on repeatable inputs that move the market each year, including OTC switch behavior, seasonality and diet-linked spikes in symptoms, changes in pharmacy and e-commerce share, and ingredient and packaging inflation that can shift average selling price. Forecasting is done using scenario analysis supported by a simple multivariate regression on macro indicators and health awareness proxies, and then adjusted using what primary respondents expect for channel growth and pricing actions. Where hard volume data is thin, we use conservative ranges first, then narrow them after at least two independent cross-checks align.

Data Validation & Update Cycle

Validation is done in layers, where model outputs are compared against independent signals such as OTC category growth commentary, channel-level pricing direction, and public health trend lines for reflux-related symptoms. When outliers show up, we revisit the inputs that drive them, and we trigger follow-up calls if the variance cannot be explained by currency timing, channel shift, or product-mix change.

Before sign-off, the work is reviewed in multiple steps so assumptions, formulas, and year-to-year movements stay consistent and explainable. The report is refreshed annually, and we also revisit key assumptions when a material event occurs, such as a regulatory change in OTC labeling or a noticeable shift in retail pricing. Right before delivery, a final pass is completed so the view reflects the latest available information.

Mordor Intelligence's Antacids Market Size Versus Other Published Estimates

Published antacids market values often differ because firms do not count the same products, years, or selling channels, and those choices can move the number even before forecasting begins. Differences also come from how prices are averaged across pack sizes, how currency is converted, and how often the model is refreshed.

The main gap comes from whether adjacent acid-related therapies are blended into the total, and in the Mordor Intelligence view only chemically neutralizing antacids and alginate-based blends sold through retail and hospital-linked channels are counted, while prescription-only PPIs or H2 blockers are kept out even if they treat similar symptoms. Another driver is the starting year, where some sources anchor on 2024 or 2025 and then apply faster growth assumptions, while others use a calmer base case tied to symptom prevalence and channel mix. Finally, ASP progression can be handled differently, since some estimates apply a single inflation uplift, whereas our model varies pricing by channel and checks it back with pharmacist and distributor inputs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.30 B (2026) | |

| Global Consultancy A | USD 7.73 B (2024) | Uses a 2024 anchor year and a 2025 to 2030 forecast window, which can pull forward growth expectations and price effects versus a 2026 estimate year. Scope detail on excluding prescription acid suppressants is not always made explicit, which can widen the total if adjacent therapies are implicitly included. |

| Industry Publisher B | USD 7.67 B (2025) | Starts from a 2025 estimate and extends the forecast to 2035, which often relies on longer-cycle growth assumptions that may not be fully tied to near-term channel mix and pack-price behavior. Limited disclosure on how combination products and channel-level ASP changes are normalized can also shift the headline value. |

The comparison shows that most of the spread is explained by year selection, product inclusion rules around acid-related therapies, and how pricing is rolled forward across channels. When the scope is kept tight to neutralizing antacids and the inputs are checked against symptom demand signals and real-world channel pricing, the market size becomes easier to trace and repeat from one update to the next.

Key Questions Answered in the Report

What is the projected value of the antacids market in 2031?

The antacids market is forecast to reach USD 8.65 billion by 2031, reflecting a 3.45% CAGR over the 2026-2031 period.

Which formulation type is growing fastest?

Gummies and chewable soft-gels lead growth at a 9.25% CAGR as consumers seek flavorful, easy-to-take options.

Why are alginate-based antacids gaining share?

Alginates form a physical raft that blocks reflux, delivering drug-free relief and advancing at an 8.85% CAGR through 2031.

How is e-commerce reshaping antacid sales?

Online channels are expanding at 12.11% CAGR, driven by subscription models and same-day delivery that improve convenience and retention.

Which region shows the highest growth potential?

Asia-Pacific is expected to grow the fastest at 9.51% CAGR, propelled by aging populations and dietary shifts that increase digestive disorders.

Page last updated on: