Empty Capsule Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

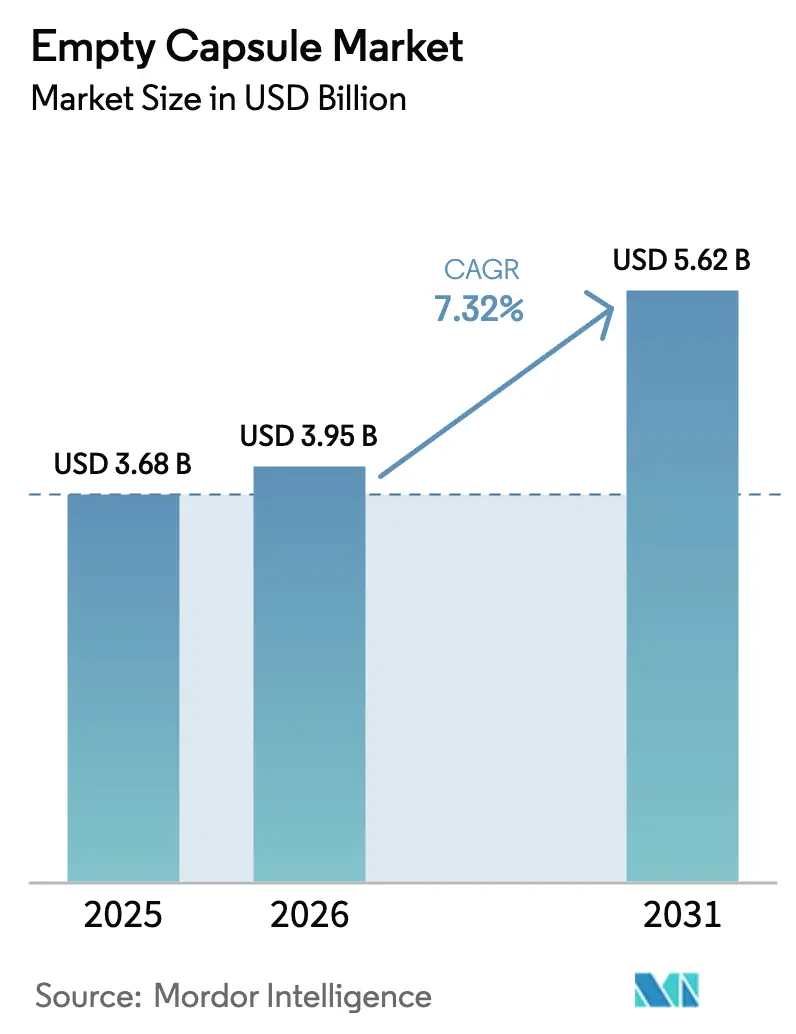

| Market Size (2026) | USD 3.95 Billion |

| Market Size (2031) | USD 5.62 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Empty Capsule Market Analysis by Mordor Intelligence

The Empty Capsule Market size was valued at USD 3.68 billion in 2025 and is estimated to grow from USD 3.95 billion in 2026 to reach USD 5.62 billion by 2031, at a CAGR of 7.32% during the forecast period (2026-2031).

Growth reflects pharmaceutical companies’ shift toward modular oral doses that protect moisture-sensitive actives, while nutraceutical brands adopt hard-shell formats to overcome taste-masking challenges in personalized supplement programs. Premium pricing for plant-based shells, wider Halal and vegan certifications, and the spread of controlled-release designs from oncology to mass-market probiotics collectively fuel value expansion rather than pure volume gains. Manufacturers with vertically integrated HPMC plants or diversified gelatin sourcing capture outsized margins as supply security becomes a competitive differentiator. Continuous manufacturing, AI-enabled inspection, and on-demand filling further compress time-to-market, supporting the empty capsule market’s evolution from commodity shell production to functionality-led differentiation.

Key Report Takeaways

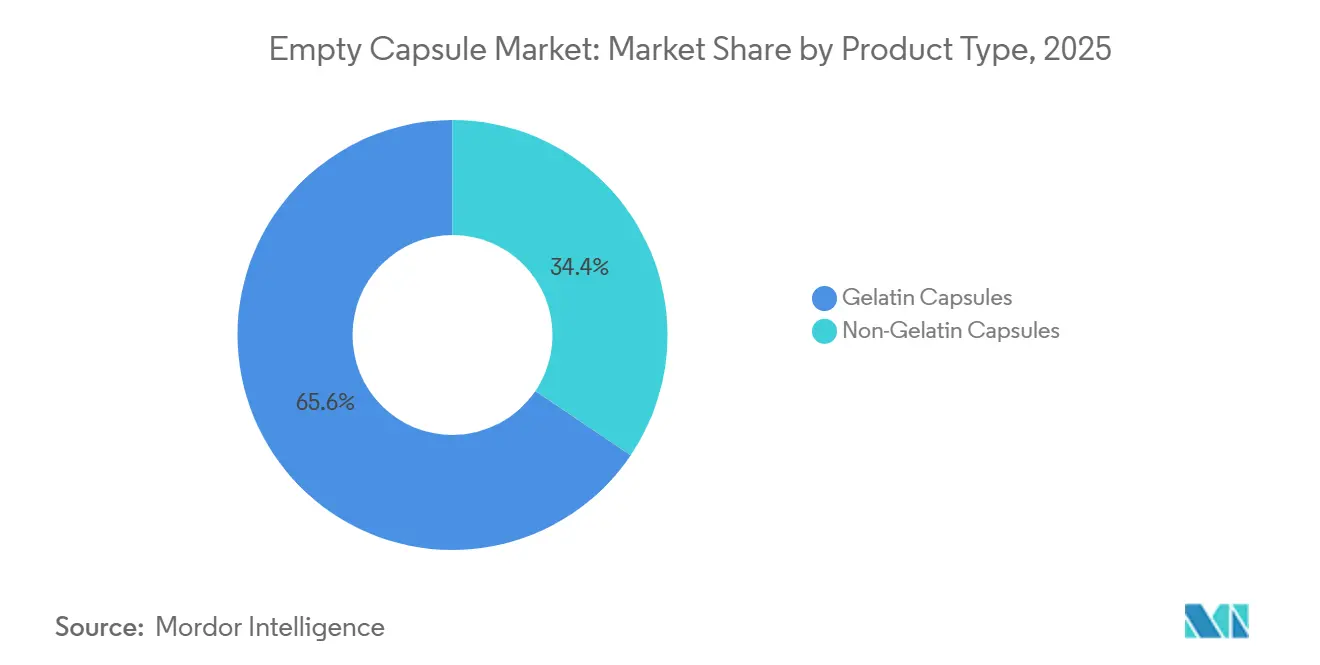

- Gelatin capsules held a 65.56% empty capsule market share in 2025, while non-gelatin formats are forecast to grow 10.25% CAGR through 2031.

- Animal-derived raw materials represented 68.53% of sourcing in 2025; plant and fermentation inputs will expand 10.85% CAGR, raising the segment’s portion of the empty capsule market size despite continuing supply bottlenecks.

- Immediate-release capsules dominated with 70.63% revenue in 2025; enteric and delayed-release shells will advance at 8.87% CAGR as probiotic and enzyme products move mainstream.

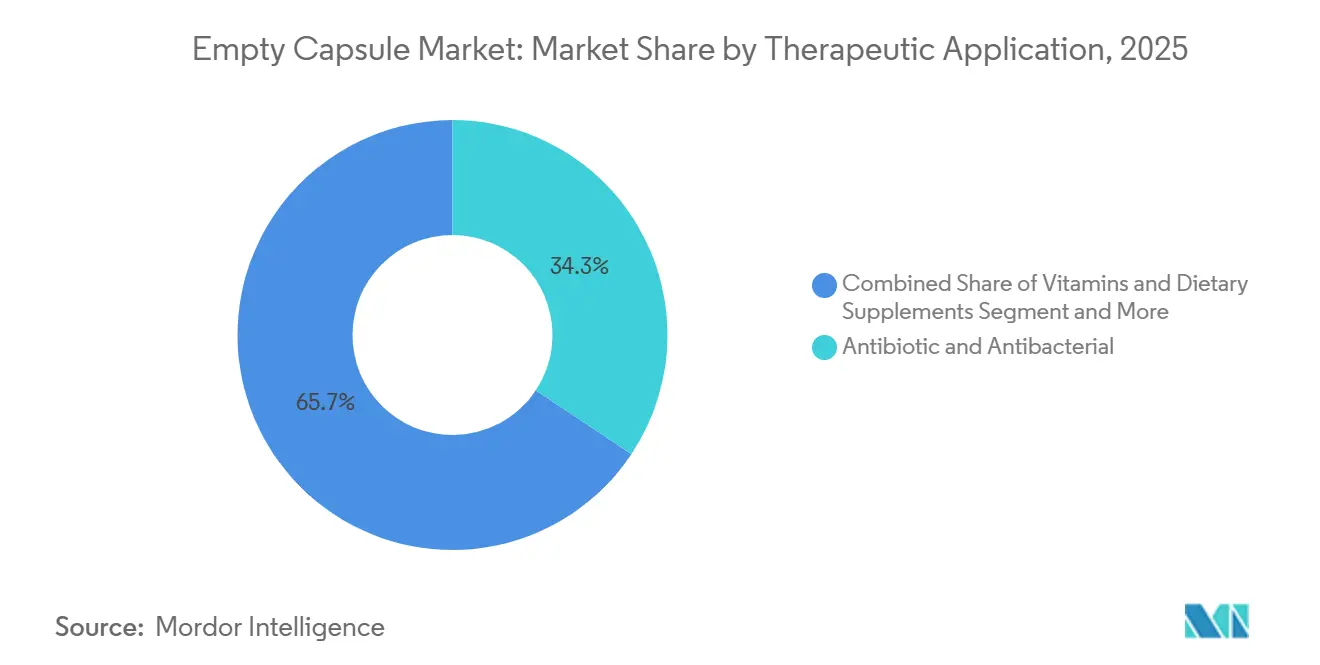

- Antibiotic formulations accounted for 34.33% of therapeutic demand in 2025, yet vitamins and dietary supplements will record the fastest 8.7% CAGR as personalized nutrition scales.

- The pharmaceutical sector contributed 52.52% of demand in 2025; nutraceutical end users will post a 9.21% CAGR as direct-to-consumer brands embrace capsule economics.

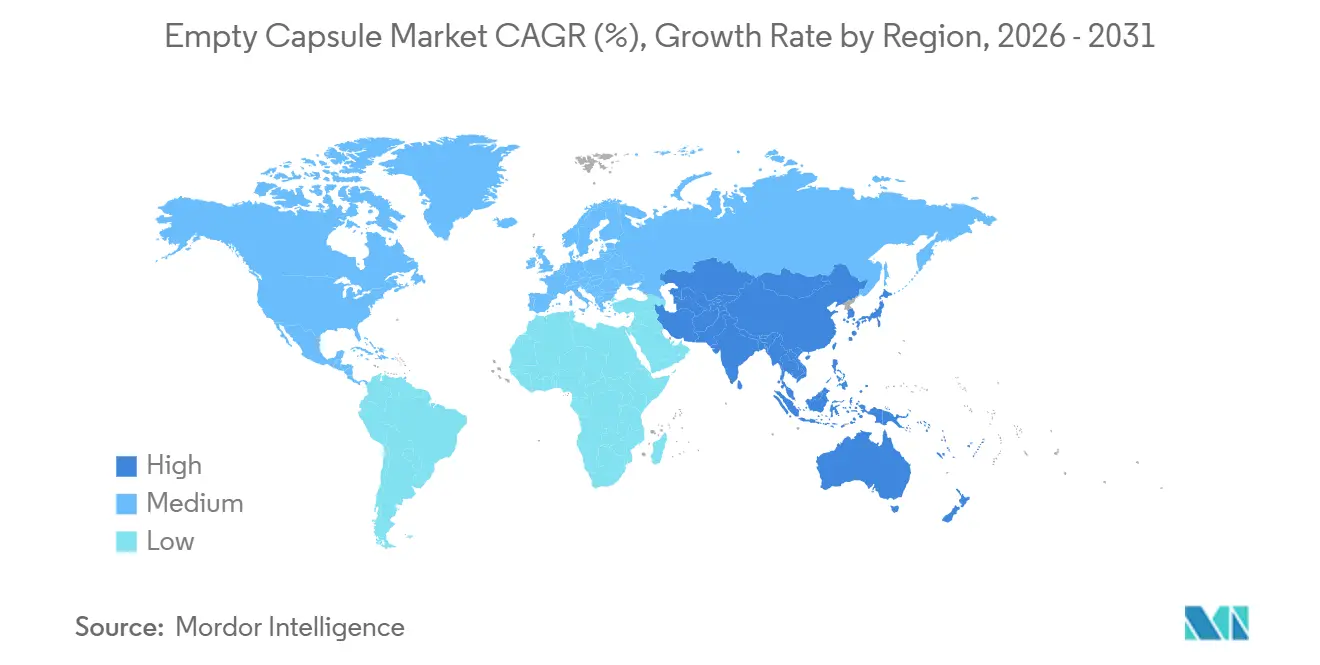

- North America commanded 42.13% of global revenue in 2025; Asia-Pacific will expand at 10.51% CAGR through 2031 as production migrates to China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Empty Capsule Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing pharmaceutical manufacturing volume | +1.8% | Global, concentrated in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising nutraceutical consumption | +1.5% | North America and Europe lead, Asia-Pacific accelerating | Short term (≤2 years) |

| Advancements in capsule-filling technology | +1.2% | North America, Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Shift toward personalized dose packaging | +0.9% | North America, Europe, urban Asia-Pacific | Long term (≥4 years) |

| Integration of digital health technologies | +0.7% | North America, Europe, pilot programs in Asia-Pacific | Long term (≥4 years) |

| Expansion of continuous manufacturing infrastructure | +0.6% | North America, Europe, emerging in China and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Pharmaceutical Manufacturing Volume

Global drug makers earmarked more than USD 100 billion for new capacity between 2024 and 2026, amplifying demand for encapsulation lines that occupy less floor space and reach validation faster than tablet presses. The FDA cleared 12 advanced continuous capsule-filling applications under its Emerging Technology Program during 2024-2025, accelerating adoption of closed-loop processes with real-time quality control. Redundant plants across multiple regions address supply-chain-resilience mandates that surfaced after pandemic shortages, tilting new oral dose programs toward flexible capsule formats. As a result, suppliers of enteric-coated and sustained-release shells capture premium margins because these formats align with complex dosing regimens in chronic care.

Rising Nutraceutical Consumption

Global supplement sales reached USD 177 billion in 2024, with capsule formats gaining share as consumers associate hard shells with dosage accuracy and premium positioning[1]Council for Responsible Nutrition, “Dietary Supplement Market Overview 2024,” crnusa.org. DNA-guided nutrition brands pushed custom capsule orders up 22% year over year in 2025, sidestepping the tooling costs that discourage small-batch tablets. Probiotic makers increasingly rely on capsules for gastric-acid protection; encapsulated strains deliver 40-60% higher survivability in simulated gastric fluid than uncoated tablets. Updated FDA labeling guidance emphasizing bioavailability transparency also nudges brands toward capsule formats that simplify dissolution testing.

Advancements in Capsule-Filling Technology

ICH Q13 guidelines, adopted by the FDA in 2024, legitimized continuous production lines that integrate blending, dosing, and sealing, cutting changeovers to under 90 minutes and shrinking fill-weight variability below 2%. Modular stations introduced in 2025 switch between gelatin and HPMC shells without mechanical overhaul, preserving raw-material optionality. Embedded PAT sensors monitor humidity and electrostatic charge, curbing shell defects by as much as 5 percentage points and reducing downstream rejections.

Shift Toward Personalized Dose Packaging

Unit-dose capsule systems combine filling with patient-specific labeling, enabling pharmacies to dispense custom strengths such as 3.5 mg warfarin approved through an AI dose-optimization platform in 2024. Children’s hospitals saw a 35% jump in extemporaneous capsule compounding between 2024 and 2025 as weight-based dosing superseded one-size tablets. Edible RFID tags embedded in shells, cleared for select chronic therapies in 2025, feed ingestion data to payers, underpinning outcome-based reimbursement.

Restraints Impact Analysis of Empty Capsule Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in gelatin raw-material supply | -0.8% | Global, acute in Asia-Pacific and Europe | Short term (≤2 years) |

| Stringent religious & dietary compliance | -0.5% | Muslim-majority markets, vegetarian segments worldwide | Medium term (2-4 years) |

| Limited availability of pharma-grade HPMC | -0.6% | North America, Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Climate-induced supply-chain instability | -0.4% | Global, high-risk agricultural regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Gelatin Raw-Material Supply

Capsule makers now hold 60-90 days of inventory - double pre-2024 norms - tying up working capital and shaving up to 300 basis points off gross margins during tight markets.

Stringent Religious & Dietary Compliance

Halal and Kosher rules fracture supply chains, forcing separate bovine or fish-gelatin lines that carry 25-35% higher raw-material costs and extend product-launch timelines by up to a year[2]Halal Food Authority, “Halal Certification Requirements,” halalfoodauthority.com. Vegan consumers, roughly 8-10% of the U.S. and European populations, reject any animal-derived shell, steering brands toward HPMC or pullulan formats despite higher humidity requirements on filling lines. Divergent standards among certifying bodies, such as JAKIM and MUI, further complicate global rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Empty Capsule Market Segment Analysis

By Product Type:

Non-Gelatin Formats Capture Premium PositioningNon-gelatin shells will grow 10.25% CAGR to 2031, outperforming the empty capsule market by close to 300 basis points as Halal compliance, vegan demand, and probiotic stability concerns rise. Gelatin still delivered 65.56% of revenue in 2025, anchored by its low cost and rapid dissolution, yet HPMC and pullulan now secure premium niches. HPMC capsules extend probiotic shelf life by virtue of their 4-6% moisture content, while pullulan’s superior oxygen barrier serves antioxidants despite a 40-50% price premium.

Softgels remain vital for lipophilic APIs but face scrutiny over 8-12% API loss during sealing. Starch-based and modified-starch shells, still in pilot phases, promise mid-term alternatives with moisture resilience. Hybrid gelatin-HPMC blends launched in 2025 balance certification and performance, signaling more SKU convergence ahead.

By Raw-Material Source:

Fermentation Platforms Challenge Animal DominanceAnimal-derived gelatin held 68.53% share in 2025, yet plant and fermentation inputs will log 10.85% CAGR, aided by disease-related supply shocks and ethically driven consumption. Porcine gelatin’s cost edge keeps it a staple outside Muslim-majority markets, while bovine gelatin satisfies Halal claims at a 15-20% premium. Pharma-grade HPMC supply remains tight, capping rapid migration, but pullulan’s 0.5 cc/m²/day oxygen permeability secures high-value nutraceutical orders. Starch and algal polysaccharides lag amid brittleness and harvest variability.

By Functionality:

Enteric Coatings Migrate from Niche to MainstreamImmediate-release shells captured 70.63% of sales in 2025; however, enteric and delayed-release formats will expand 8.87% CAGR as enzymes, probiotics, and colon-targeted drugs proliferate. High-throughput coating lines now process up to 300,000 capsules per hour, halving per-unit costs and widening adoption beyond oncology. Dual-release designs combining pulsatile and sustained layers remain specialty but illustrate capsules’ modular potential for lifecycle management.

By Therapeutic Application:

Supplements Outpace Antibiotics as Growth EngineAntibiotics delivered 34.33% of 2025 demand, yet stewardship programs and low reimbursement curb future expansion. Vitamins and dietary supplements will rise 8.7% CAGR, propelled by direct-to-consumer personalization platforms. Probiotics, with 11-13% forecast growth, dominate new capsule launches due to stability advantages versus chewables or powders, while GLP-1 agonists herald peptide-protected shells for metabolic care.

By End User:

Nutraceutical Brands Embrace Capsule EconomicsPharmaceutical companies absorbed 52.52% of 2025 volume, but nutraceuticals will post 9.21% CAGR as startups prefer minimum batches of 50,000 units and 4-6-week commercialization timelines that tablets cannot match. CDMOs invest in flexible suites switching between gelatin and HPMC, charging premiums for mixed-mode capacity. Veterinary, cosmetic, and research segments collectively remain under 10% but offer high-margin pockets for regional suppliers.

Geography Analysis

North America Empty Capsule Market

North America generated 42.13% of 2025 revenue, driven by FDA incentives that favor domestic continuous manufacturing and by USD 27 billion in recent U.S. pharma investment, yet labor costs hold regional CAGR below Asia-Pacific. Canada benefits from clinical-trial clustering, while Mexico rises as a near-shore alternative circumventing trans-Pacific logistics. Environmental compliance - such as California’s Proposition 65 - adds incremental per-unit costs but reinforces quality differentiation.

Broader European Markets

Europe accounted for roughly 29% of global demand in 2025. Germany, France, and the United Kingdom lead consumption, yet fragmented national rules lengthen validation cycles. Onshoring accelerates after pandemic-era shortages, as evidenced by Lonza’s CHF 150 million Swiss expansion and Roquette’s French HPMC line. Dual inventories for EU and post-Brexit UK specifications add complexity, while Southern European austerity caps price escalation.

APAC, MEA and South America Empty Capsule Market

Asia-Pacific is the growth engine, advancing 10.51% CAGR through 2031. China and India, together supplying nearly 70% of regional capsules, add capacity under NMPA and PLI incentives, respectively. Sirio Pharma’s acquisition spree and ACG’s 50-billion-unit Mumbai expansion underscore scale ambitions. Japan targets premium enteric niches, South Korea pursues vegetarian communities, and Australia leverages its clinical-trial ecosystem. The Middle East & Africa, at a significant share in 2025, gain from Halal mandates and GCC healthcare spend, while South America struggles with currency swings despite Brazil’s localized expansions.

Regulatory Landscape

Empty capsule manufacturing and use are governed by a mix of drug-product GMPs, excipient documentation, and pharmacopoeial specifications. In the United States, capsule shells used in drug products are produced under FDA current GMP expectations (21 CFR Part 211), and OTC capsule presentations must also meet tamper-evident packaging requirements (21 CFR 211.132). Suppliers commonly support customer filings through Type III Drug Master Files (DMFs) that provide CMC information for capsule shells while protecting proprietary manufacturing details.

Across regions, monographs and general chapters in major pharmacopoeias (including USP-NF and parallel national pharmacopoeias) set baseline tests such as identification, disintegration, loss on drying, microbiological quality, and limits for impurities. Packaging-material GMP is frequently anchored to ISO 15378:2017 for primary packaging materials, while newer regional standards continue to emerge, including China group standard T/QAS 153-2026 for gelatin hollow capsule manufacturing. Quality-by-design concepts referenced in USP chapter 1059 also reinforce tighter control of critical material attributes (CMAs) and change-control expectations, which increases compliance burden for multi-site and multi-material (gelatin, HPMC, pullulan) supply chains.

Competitive Landscape

The top players, Lonza (Capsugel), Qualicaps, ACG, Sirio Pharma, and Patheon, control a significant percentage of the empty capsule market, leaving space for regional specialists and niche innovators. Lonza’s 2024 enteric-coating line illustrates a pivot toward functionality over volume, chasing higher margins. Qualicaps leverages Roquette’s HPMC integration to guarantee supply amid raw-material scarcity. ACG pioneers AI-enabled inspection, boosting throughput and defect detection tenfold. Sirio’s consolidation builds scale but raises Western procurement risk under emerging BIOSECURE restrictions. Pullulan-focused newcomers such as Hayashibara target oxygen-sensitive nutraceuticals, while starch-based startups position for cost-down disruption once brittleness hurdles fall. Commodity shells face pricing pressure as Asian capacity expands, whereas specialty capsules maintain premiums through technology and certification barriers.

Empty Capsule Industry Leaders

Lonza Group (Capsugel)

Qualicaps (Roquette)

ACG Worldwide

Sirio Pharma Co., Ltd.

Patheon (Thermo Fisher)

- *Disclaimer: Major Players sorted in no particular order

Empty Capsule Market Companies Covered in this Report

- ACG Worldwide

- Aenova Group

- Bright Pharma Caps

- CapsCanada Corporation

- Er-Kang Pharmaceutical Co. Ltd.

- Fujifilm Corp. (Fujicaps)

- HealthCaps India Ltd.

- Lonza Group

- Medi-Caps Ltd.

- Natural Capsules Ltd.

- Nectar Lifesciences Ltd.

- Patheon (Thermo Fisher)

- Qingdao Yiqing Medicinal Capsules Co. Ltd.

- Qualicaps (Roquette)

- Shanxi Guangsheng Medicinal Capsules Co. Ltd.

- Shanxi JC Biological Technology Co. Ltd.

- Sirio Pharma Co., Ltd.

- Suheung Capsule Co., Ltd.

- Sunil Healthcare Ltd.

- Zhejiang Huangyan Gelatin Capsule Co. Ltd.

- Zhejiang Ruixin Capsules Co. Ltd.

Market Opportunities and Future Outlook

Capacity localization and material diversification are creating whitespace for suppliers able to provide reliable, certified shells close to major demand centers. Recent investments and line additions illustrate this shift, including Lonza commissioning additional hard gelatin capsule manufacturing lines in December 2024 at Rewari (India) and Suzhou (China). ACG also announced a USD 200 million phased investment in October 2025 for a new US empty-capsule manufacturing facility in Atlanta, Georgia, with production targeted for early 2027. Together, these moves reflect buyer priorities around supply assurance, shorter lead times, and qualification of multiple sources.

Non-gelatin platforms also offer a commercialization pathway where religious compliance, clean-label positioning, and stability needs intersect. Shaoxing Renhe Capsule Co., Ltd. launched an intelligent plant-based (HPMC) capsule production line in January 2026, with capacity rising to 20 billion units annually through online quality monitoring and low-moisture control. In parallel, there has been increased activity around specialty formats such as organic-certified pullulan capsules (Lonza Capsugel Organicaps, October 2025). Formulation-driven work, including efforts on titanium dioxide-free hard capsule shells identified in a 2026 patent application, creates additional room for capsule makers that can validate alternative opacifiers and impurity controls to meet evolving customer specifications and regional compendial expectations.

Recent Industry Developments in Empty Capsule Market

- May 2026: Lonza Capsugel published Pharmaceutics research on its Licaps DUOCAP capsule-in-capsule technology, reporting up to four times higher enzyme activity versus standard capsules. The data supports premium positioning for specialty oral-delivery formats used in enzymes and other sensitive actives, reinforcing the shift from commodity shells toward performance-led differentiation.

- October 2025: ACG announced a USD 200 million phased investment to build its first US hard-shell capsule manufacturing facility in Atlanta, Georgia, with production targeted for early 2027. The project strengthens domestic sourcing options for North American pharma and nutraceutical customers and adds competitive pressure on lead times and supply resilience.

- December 2024: Lonza expanded hard gelatin capsule manufacturing capacity by commissioning additional lines at its Rewari (India) and Suzhou (China) sites. The added output increases availability in two key production hubs, supporting both pharmaceutical and nutraceutical demand while reducing single-region dependency.

Empty Capsule Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the value of newly manufactured, unfilled empty capsule shells that are sold to be filled later by pharmaceutical, nutraceutical, cosmetic, and research users. It includes hard gelatin and non-gelatin shells, and the value is tracked at the factory gate in USD.

Scope exclusions: We do not count capsule filling machines, pre-filled softgels, or secondary packaging such as blisters and cartons.

Segments Covered in This Report

- By Product Type

- Gelatin Capsules

- Hard Gelatin Capsules

- Soft Gelatin Capsules

- Non-Gelatin Capsules

- HPMC Capsules

- Pullulan Capsules

- Starch-based Capsules

- Other Plant-based Capsules

- Gelatin Capsules

- By Raw-Material Source

- Animal-Based

- Porcine Gelatin

- Bovine Gelatin

- Fish-derived Gelatin

- Plant & Fermentation-Based

- HPMC

- Pullulan

- Starch

- Algal Polysaccharides

- Animal-Based

- By Functionality

- Immediate-Release

- Sustained / Extended-Release

- Delayed / Enteric-Release

- Others (Colon-Targeted / pH-Sensitive and Dual / Multiple-Release)

- By Therapeutic Application

- Antibiotic & Antibacterial

- Vitamins & Dietary Supplements

- Antacid & Antiflatulent

- Cardiovascular Therapy

- Pain Management & CNS

- Probiotics & Gut Health

- Metabolic & Endocrine Disorders

- Other Applications

- By End User

- Pharmaceutical Industry

- Nutraceutical & Functional-Food Industry

- Cosmetic & Personal-Care Industry

- Contract Development & Manufacturing Org. (CDMOs)

- Research & Academic Laboratories

- Veterinary & Animal-Health Sector

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on demand drivers and supply capacity, and then it is used to sanity check what we hear in interviews. For empty capsules, we reviewed public health and manufacturing signals such as the US FDA databases and publications (including dosage form and manufacturing change references), plus CDC health statistics (to understand therapy area direction).

We also referred to sources such as UN Comtrade and national customs portals (to see trade movement of capsule shells and related materials), the World Bank and IMF macro series (for currency and inflation context), and patent databases (to spot activity around HPMC, pullulan, and functional capsule features). Company annual reports, investor presentations, and credible press were used to confirm capacity additions, plant locations, and product mix shifts, and a paid subscription for company financials and news helped speed up cross-checks. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what is actually sold as an empty capsule, how pricing moves by material type, and how demand differs across pharma and nutraceutical customers. We spoke with a mix of capsule shell makers, distributors, and formulation and procurement stakeholders. Respondent coverage was balanced across major consuming and manufacturing regions, so gaps from desk findings could be closed with practical assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 19% | APAC: 45% |

| Mid tier: 52% | Functional/Unit leaders: 37% | EMEA: 37% |

| Smaller Players: 19% | Managers: 44% | Americas: 18% |

Market-Sizing & Forecasting

The core model is built using top-down logic where production, trade flows, and end-use demand pools are reconstructed into a total value for empty capsule shells, and then the math is tested with selective bottom-up approximations before the total is finalized. Those bottom-up checks use sampled supplier revenue splits, channel discussions, and an ASP times volume build from typical capsule counts by end user. This helps us adjust for places where public data is thin.

Key inputs used in the model include the mix shift between gelatin and non-gelatin shells, utilization and capacity expansion signals, import and export direction by major producing regions, and pricing movement by raw material type (animal-based versus plant and fermentation-based). We also track application-side signals, such as pull from antibiotics and antibacterial therapies and the growing nutraceutical fill volumes, because these move demand differently across regions.

For forecasting, we use scenario analysis with a light multivariate overlay, where volume growth, pricing trend, and material substitution are projected separately and then recombined. When gaps appear in country-level volumes or ASPs, the missing pieces are filled using regional benchmarks and rechecked through interviews so the final series stays consistent across years.

Data Validation & Update Cycle

Validation is done in steps so unusual results are caught early, and it is not left to a single check at the end. We compare outputs against independent signals such as trade movement, capacity announcements, and mix shares, and then variances are reviewed until the drivers are clearly explained.

Before sign-off, the model and assumptions go through peer review, and re-contact is triggered if a data point changes the demand pool, pricing path, or material split in a meaningful way. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery scan to ensure clients receive the latest view.

Mordor Intelligence's Empty Capsule Market Size Versus Other Published Estimates

Published estimates for empty capsules can look far apart, even when everyone is discussing gelatin and non-gelatin shells, because the boundaries and pricing logic are not always aligned. Differences usually come from what is counted as an empty capsule sale, whether values are taken at factory gate or later in the channel, and how quickly assumptions are refreshed when mix and prices change.

By tracking factory-gate sales scope and refreshing currency timing, mix shares, and ASP progression within Mordor Intelligence's model, the total stays tied to unfilled shell demand rather than packaging add-ons or downstream markups that can creep into some estimates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.95 B (2026) | |

| Global Consultancy A | USD 3.97 B (2024) | Uses an earlier base year and a shorter horizon, and the scope is not clearly limited to factory-gate unfilled shells, which can shift value if distributor pricing or adjacent capsule formats are blended. |

| Industry Publisher B | USD 3.21 B (2024) | Leans heavily on a functionality and application split with limited visibility into regional price and mix changes, which can understate totals when non-gelatin share rises and premium pricing expands. |

The spread across the table is mainly explained by timing and scope discipline, not by a different view on demand growth. When the counting boundary is kept on unfilled shells at the factory gate and the mix and pricing are updated with interview checks, the output becomes easier to reproduce and compare across years.

Key Questions Answered in the Report

How fast is the empty capsule market growing through 2031?

The empty capsule market is set to advance at a 7.32% CAGR, lifting revenue from USD 3.95 billion in 2026 to USD 5.62 billion by 2031.

Which capsule type will add the most incremental revenue?

Non-gelatin shells, chiefly HPMC and pullulan, are forecast to expand 10.25% CAGR, outpacing overall market growth thanks to religious compliance and probiotic stability advantages.

Why are nutraceutical brands favoring capsules over tablets?

Capsules require lower minimum orders, avoid costly tablet tooling, and offer superior taste masking, cutting commercialization time by roughly one month for emerging direct-to-consumer labels.

Which region offers the highest growth potential for suppliers?

Asia-Pacific, especially China and India, will post a 10.51% CAGR as global drug makers relocate production to cost-efficient hubs and domestic supplement demand accelerates.

What raw-material constraint could slow the shift to vegetarian shells?

Limited global capacity for pharma-grade HPMC keeps lead times at 16-20 weeks, capping rapid conversion from animal-derived gelatin despite rising vegan and Halal demand.

How are manufacturers defending margins amid gelatin price swings?

Leading suppliers secure multi-source contracts, integrate gelatin production, or pivot to plant-based shells, insulating themselves from raw-material volatility that can compress margins by 200-300 bps.

Page last updated on: