Orthobiologics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.06 Billion |

| Market Size (2031) | USD 9.52 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

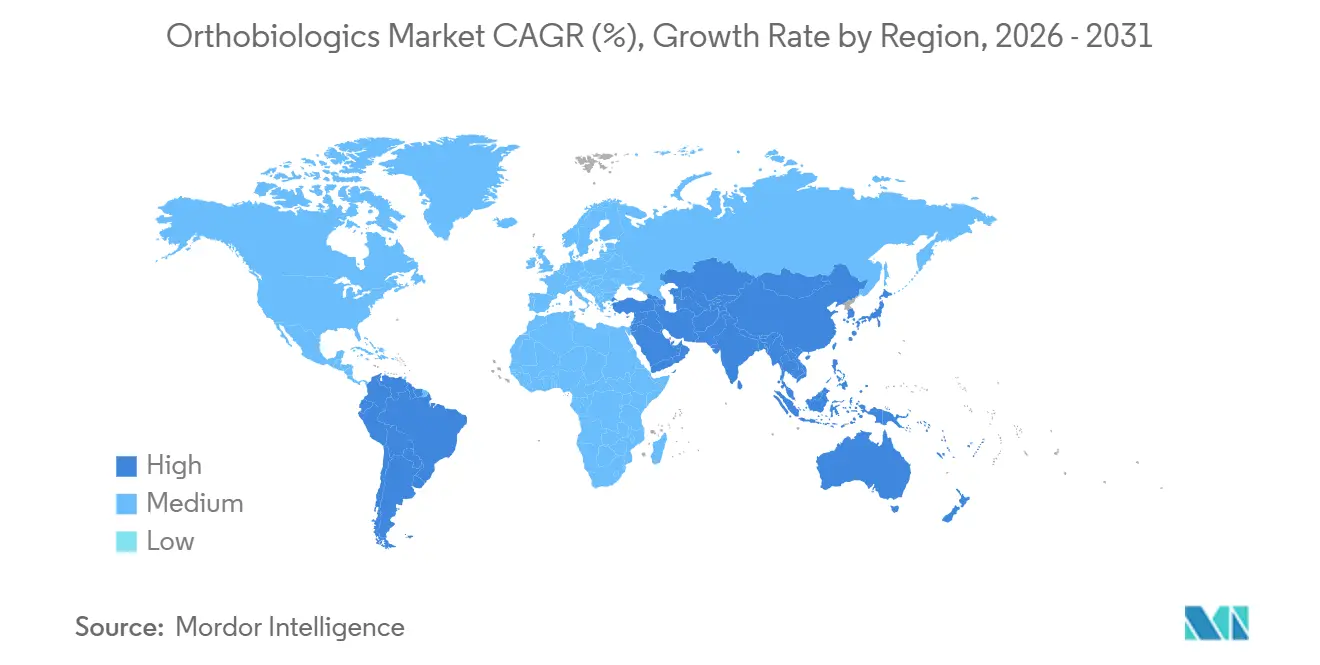

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Orthobiologics Market Analysis by Mordor Intelligence

The Orthobiologics Market size is expected to increase from USD 6.68 billion in 2025 to USD 7.06 billion in 2026 and reach USD 9.52 billion by 2031, growing at a CAGR of 6.17% over 2026-2031.

Short-term growth reflects rising clinical demand driven by the prevalence of osteoarthritis, which continues to accelerate as global populations age. Commercial momentum is tempered by patchy reimbursement for platelet-rich plasma (PRP) and stem cell therapies, leaving many interventions as cash-pay procedures despite 18 new PRP preparation devices clearing the FDA’s 510(k) pathway in 2024. Domestic manufacturing capacity expanded in 2025 as tissue processors reshored production to offset Section 232 steel and aluminum tariffs that added 25% to the cost of imported orthopedic hardware. Collectively, these forces position the orthobiologics market for steady rather than explosive growth during the forecast window.

Key Report Takeaways

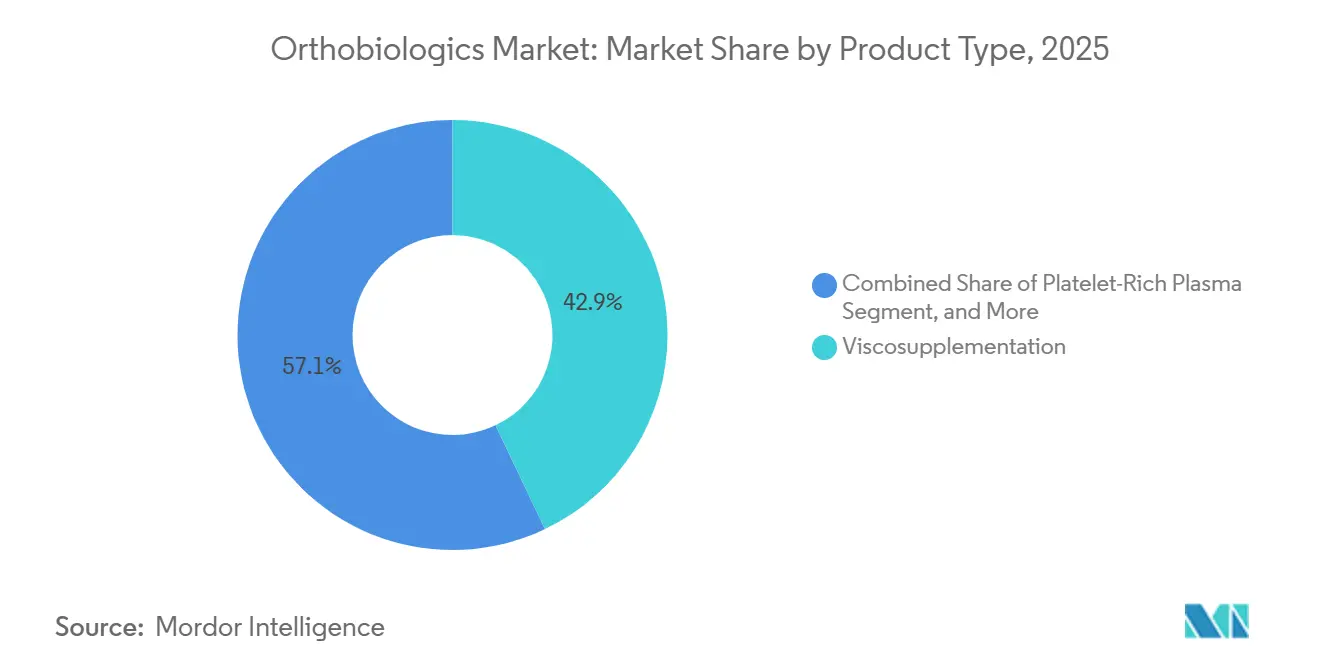

- By product type, viscosupplementation led with 42.92% of the orthobiologics market share in 2025, while platelet-rich plasma is forecast to expand at a 7.09% CAGR through 2031.

- By application, spinal fusion accounted for 52.64% of 2025 revenue, whereas osteoarthritis and joint degeneration are advancing at a 9.63% CAGR to 2031.

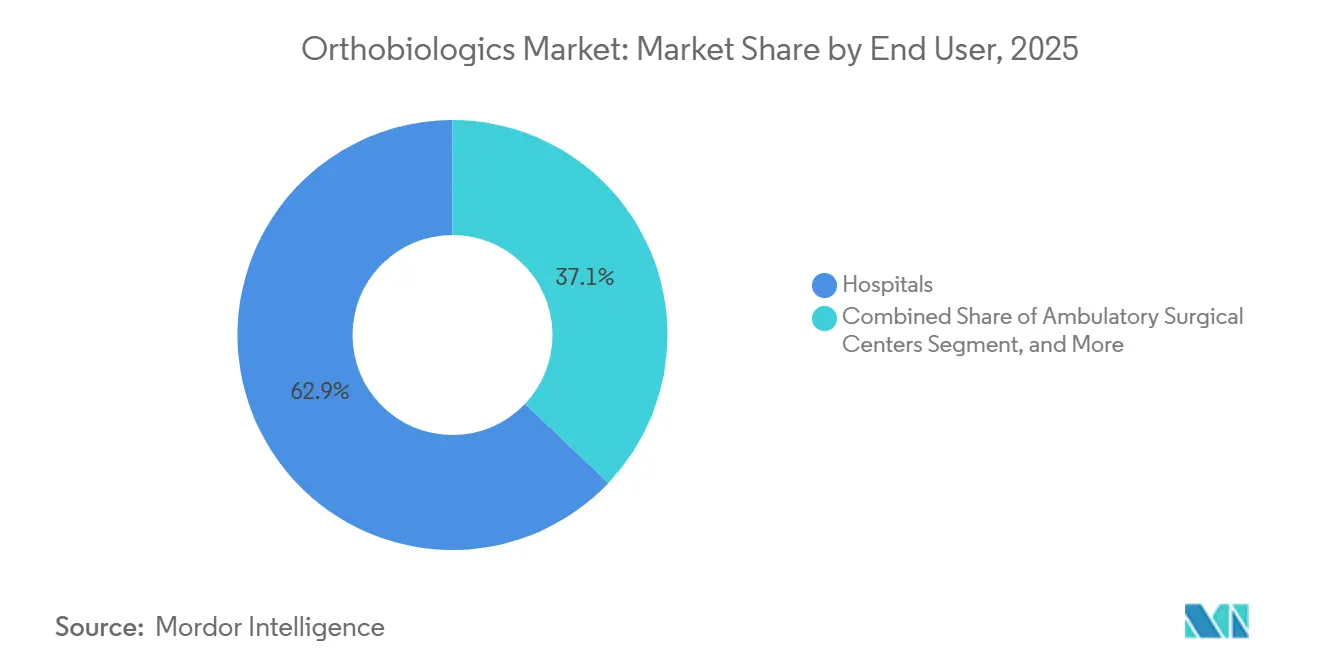

- By end user, hospitals controlled 62.92% of revenue in 2025; ambulatory surgical centers are growing fastest at an 8.18% CAGR over the same period.

- By geography, North America captured 43.17% of global 2025 revenue, while Asia-Pacific is projected to expand at an 11.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Orthobiologics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Osteoarthritis Prevalence & Aging Demographics | +1.2% | Global, acute in North America, Europe, East Asia | Long term (≥ 4 years) |

| Shift Toward Minimally-Invasive & Outpatient Orthopedic Procedures | +0.9% | North America, Europe, early adoption in urban Asia-Pacific markets | Medium term (2-4 years) |

| Advances in Regenerative Biomaterials | +0.7% | Global, led by North American and EU research hubs | Medium term (2-4 years) |

| Increasing Sports Injuries Demanding Faster Recovery Solutions | +0.6% | North America, Europe, affluent Asia-Pacific cities | Short term (≤ 2 years) |

| Proliferation of In-Hospital Biologics Labs | +0.5% | North America, Western Europe, select Asia-Pacific urban centers | Medium term (2-4 years) |

| Tariff-Driven Reshoring of Manufacturing | +0.3% | United States with spillover to Canada and Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Osteoarthritis Prevalence & Aging Demographics

Global osteoarthritis cases are forecast to top 700 million by 2030 as populations live longer and obesity rates climb.[1]World Health Organization, “Osteoarthritis,” who.int In the United States, clinically diagnosed prevalence reached 32.5 million adults in 2024, a 15% jump from 2015. Confronted with long surgical wait times, nine months for knee replacement in metropolitan Japan, surgeons increasingly deploy viscosupplementation and PRP as bridge therapies. Direct osteoarthritis care costs the United States USD 185 billion in 2024, prompting payers to consider biologics that may delay arthroplasty. As a result, the orthobiologics market is tightly linked to demographic trends that expand the candidate pool for non-operative biologic interventions.

Shift Toward Minimally-Invasive & Outpatient Orthopedic Procedures

Ambulatory surgical centers (ASCs) performed 5.2 million orthopedic cases in the United States during 2024, up 12% year on year after CMS added complex spine and joint reconstructions to its covered list.[2]Centers for Medicare & Medicaid Services, “ASC Covered Procedures List,” cms.gov ASCs value single-use PRP kits and ready-to-use allograft putties that fit fast-throughput workflows, as evidenced by Zimmer Biomet’s GPS III PRP system, which delivers a standardized 6 mL concentrate in under 15 minutes. Reimbursement for single-level lumbar fusion averages USD 18,000 in an ASC versus USD 35,000 in hospital outpatient departments, freeing budget for biologics that enhance fusion. Although Europe lags, Germany’s insurers still require hospital admission for most spine work; the outpatient shift is expected to broaden across developed regions, redirecting share within the orthobiologics market toward products optimized for ASC use.

Advances in Regenerative Biomaterials

Peptide-amphiphile nanofibers that mimic native bone extracellular matrix advanced to Phase II trials in 2025, demonstrating 30% faster radiographic union versus autograft in lumbar fusion. New demineralized bone matrix (DBM) lines now pair bone morphogenetic protein-2 at half the original dose, trimming inflammatory complications that once slowed adoption. A 2024 study showed that DBM enriched with platelet-derived growth factors achieved 92% single-level cervical fusion without donor-site morbidity. Organogenesis earned FDA Breakthrough Device designation in 2025 for a 3D-printed collagen-hydroxyapatite construct, signaling regulatory confidence in additive manufacturing for patient-specific implants.[3]Organogenesis, “Breakthrough Device Designation,” organogenesis.com Collectively, these innovations are eroding reliance on iliac-crest harvests, which carry a 10-15% complication rate.

Increasing Sports Injuries Demanding Faster Recovery Solutions

Professional athletics validate biologic efficacy: 42% of National Football League players with Grade II hamstring tears received PRP within 48 hours in 2024, reducing the median return-to-play time from 21 to 14 days. Comparable acceleration was reported for pitchers with ulnar collateral ligament sprains in Major League Baseball. Recreational adoption followed, with U.S. clinics performing about 380,000 PRP procedures in 2024, up 18% from 2023. India’s Regenerative Medicine Society formally endorsed PRP for Achilles tendinopathy in 2025, further validating demand in cash-pay markets. While outcomes vary with platelet concentration and activation protocols, the willingness of athletes and active adults to self-fund therapy sustains a robust growth pocket within the orthobiologics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Therapy Cost & Patchy Reimbursement | -0.8% | Global, acute in North America and Western Europe | Medium term (2-4 years) |

| Stringent Region-Specific Regulatory Pathways | -0.6% | Europe (MDR) and fragmented Asia-Pacific frameworks | Long term (≥ 4 years) |

| Lack of Standardized Preparation Protocols | -0.4% | Global, especially affecting autologous therapies | Medium term (2-4 years) |

| Physician Skepticism & Limited Long-Term Data | -0.3% | North America, Europe, developed Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Patchy Reimbursement Coverage

Medicare pays for bone graft substitutes but excludes PRP under most CPT codes, a policy mirrored by major commercial insurers, which label autologous blood-derived products as investigational. Consequently, patients often self-fund USD 1,500-2,500 per PRP series, restricting uptake to affluent demographics. Viscosupplementation enjoys broader coverage at about USD 200 per dose, though prior-authorization hurdles tighten annually. A 2024 cost-utility study found that PRP delayed knee arthroplasty by 2.1 years and saved USD 12,000 per patient, yet payers continue to deny coverage due to the absence of 10-year results. The reimbursement stalemate slows diffusion and moderates the growth curve of the orthobiologics market.

Stringent, Region-Specific Regulatory Pathways Slowing Approvals

Europe’s Medical Device Regulation upgraded many allografts to Class III in 2021, cutting notified-body capacity almost in half and stretching approval timelines beyond 18 months. Faced with bottlenecks, firms prioritize U.S. launches, where 510(k) predicates enable clearance in roughly 6 months. Japan introduced a conditional pathway in 2024 that halves review time but adds costly five-year registry mandates. China’s fast-track office approved 12 regenerative products in 2025, yet reimbursement remains provincial, creating revenue gaps between urban and rural markets. Divergent rules force sequential rather than global rollouts, delaying returns on R&D within the orthobiologics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Viscosupplementation Dominates, PRP Gains Momentum

Viscosupplementation held a commanding 42.92% share in 2025, supported by two decades of uninterrupted Medicare reimbursement. Platelet-rich plasma is forecast to grow at a 7.09% CAGR, benefiting from point-of-care systems that deliver uniform concentrates in minutes, reducing the variability that bedeviled early centrifuge sets. Bone graft substitutes and DBM together account for about 30% of revenue, driven by more than 550,000 spinal fusion procedures performed in the United States in 2024. Stem cell therapies remain confined to trials and cash-pay clinics because of FDA enforcement against non-homologous use under Section 361.

Bone morphogenetic proteins plateaued near 8% share following black-box safety warnings, yet low-dose BMP-2 formulations that cut adverse events 60% could reignite demand. Viscosupplementation faces payer scrutiny; Anthem now requires genetic testing to confirm responders before approving multi-injection series, signaling future volume pressure. The orthobiologics market size for PRP-based products is likely to expand fastest within this category as standardized devices and elite-athlete endorsements mitigate earlier concerns.

By Application: Spinal Fusion Leads, Osteoarthritis Accelerates

Spinal fusion accounted for 52.64% of application revenue in 2025, as the procedure relies on bone graft substitutes, such as DBM and allografts, to achieve arthrodesis. Transforaminal lumbar interbody fusion, accounting for 38% of lumbar fusions, often integrates PRP to hasten osseointegration, a practice linked to 15% faster radiographic union at six months. Osteoarthritis and joint degeneration applications are projected to grow at a 9.63% CAGR as patients pursue disease-modifying interventions earlier in their care journey.

Trauma and fracture repair represent lower revenue; surgeons favor DBM and cancellous allografts to stimulate healing in nonunions. Reconstructive surgery is a steady niche where structural allografts bridge large defects in oncology and revision arthroplasty cases. As early-stage osteoarthritis patients adopt biologics to defer arthroplasty, the orthobiologics market share of degenerative-joint applications is set to widen, especially if future formulations demonstrate cartilage preservation.

By End User: Hospitals Anchor Revenue, ASCs Surge

Hospitals controlled 62.92% of 2025 revenue due to their role in complex spine and trauma cases and their capacity for in-house biologics processing. However, ASCs are forecast to grow at an 8.18% CAGR with CMS payment parity across more than 3,800 orthopedic procedures. Orthopedic and sports medicine clinics contribute about 12% of revenue, mainly through cash-pay PRP and viscosupplementation that sidestep insurance hurdles.

UnitedHealthcare's site-of-care policies now direct many single-level lumbar decompressions to ASCs, shifting tens of thousands of cases annually. Nonetheless, many ASCs lack cold-chain infrastructure for fresh-frozen allografts, an obstacle addressed by new freeze-dried DBM launches with an 18-month shelf life. Hospitals respond by scaling biologics labs for point-of-care PRP, preserving their relevance within an orthobiologics market increasingly influenced by outpatient migration.

Geography Analysis

North America generated 43.17% of global revenue in 2025, buoyed by 550,000 annual spinal fusions and the world’s largest network of in-hospital biologics labs. Section 232 tariffs accelerated reshoring, prompting processors to expand to counter 10-25% import duties on orthopedic hardware. Canada’s single-payer system restricts PRP and caps viscosupplementation to 3 injections per year, sending some patients cross-border for care. Mexico’s orthopedics sector grew 14% in 2024 as medical tourism surged, but reimbursement remains fragmented across public and private insurers.

Asia-Pacific is projected to grow at an 11.27% CAGR through 2031, propelled by China’s 12 regenerative-medicine fast-track approvals in 2025 and India’s 22% jump in orthopedic-device imports. China’s Tier 1 cities now reimburse stem cell therapies, while rural provinces lag, creating a two-speed market. India’s clinical endorsement of PRP in early 2025 legitimized private-sector offerings in a predominantly cash-pay environment. Japan’s aging population is putting pressure on capacity, extending wait times for knee replacements, and prompting the use of biologic bridge therapies. Australia harmonized its biologics rules with the FDA in 2024, slashing approval timelines to 10 months. South Korea’s National Health Insurance now covers DBM in spinal fusion, expected to lift utilization 30% over two years.

Europe represented significant revenue but faces MDR-related delays that extend product approvals beyond 18 months. Germany’s mandatory hospital admission for most spine surgery limits ASC penetration to under 8%, though pilots in Munich and Frankfurt test outpatient models. The United Kingdom’s NICE backed PRP for lateral epicondylitis in 2024, opening prospects for wider NHS adoption. France’s delisting of viscosupplementation cut its utilization 60%, spurring a shift toward PRP in private practice. GCC countries and Brazil account for the bulk of revenue in the Middle East & Africa and South America, driven by private payers and selective reimbursement for bone graft substitutes.

Regulatory Landscape

Orthobiologics regulation continues to split between device-like pathways for graft materials and more stringent biologics pathways for cell and tissue-based products. In the United States, the FDA regulates human cell and tissue-based orthobiologics under 21 CFR Part 1271, where products that meet Section 361 criteria (minimal manipulation and homologous use) avoid premarket approval, while higher-risk products fall under Section 351 and require biologics licensing and related clinical evidence packages. As a result, point-of-care and tissue-derived offerings remain under active CBER oversight, with the FDA releasing its 2026 CBER guidance agenda that indicates continued clarification and enforcement attention for emerging biologic product categories.

In Europe, orthobiologics developers using cell and gene-based approaches continue to work within the ATMP framework and its centralized assessment process. The EMA Committee for Advanced Therapies (CAT) issues quarterly opinions on ATMPs, including positive draft opinions adopted in 2026, which reinforces expectations around formal review throughput. Parallel policy work on an EU-level biotech initiative (referenced in 2026 legislative documents) aims to streamline manufacturing and sector integration within existing rules such as Regulation (EC) No 1394/2007, which affects orthobiologics programs that pair scaffolds, cells, or gene-modified components across multi-country launches.

Competitive Landscape

The orthobiologics market is moderately concentrated; the five largest manufacturers account for a significant share of global revenue. Leading players pursue three tactics: acquiring point-of-care PRP platforms, expanding allograft catalogs, and investing in synthetic biomaterials that avoid donor variability. Stryker’s USD 340 million acquisition of a peptide-amphiphile scaffold developer in January 2025 highlights the pivot toward regenerative nanofiber platforms.

Smaller entrants emphasize data to stand out; Bioventus launched a 5,000-patient PRP outcomes registry in March 2024, giving surgeons comparative analytics that address variability concerns. Patent filings cluster around controlled-release BMP-2 and closed-loop PRP preparation; Medtronic filed seven BMP-2 delivery patents in 2024, while Arthrex automated centrifugation based on hematocrit feedback. Regulatory compliance under ISO 13485 and MDR strains small tissue banks, yet vertical integration into processing and distribution allows groups such as MTF Biologics and AlloSource to secure niche segments.

White-space opportunities include pediatric orthopedics, biologics tailored to osteoporotic bone, and scaffold-cell combination products. Organogenesis, for example, received FDA Breakthrough Device designation for a 3D-printed collagen-hydroxyapatite implant for tibial plateau fractures, with commercialization planned for late 2026. As the orthobiologics market advances, suppliers able to couple proprietary processing platforms with robust clinical data are positioned to consolidate share.

Orthobiologics Industry Leaders

BoneSupport AB

Stryker Corporation

Zimmer Biomet Holdings Inc.

Medtronic

DePuy Synthes (Johnson & Johnson)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace appears concentrated in products that improve reproducibility in outpatient workflows, and in indications where payers already reimburse core procedures such as spinal fusion and trauma repair. That dynamic leaves hospitals and ASCs with more room to add biologic adjuncts to standard care. U.S. procedure migration to ASCs (5.2 million orthopedic cases in 2024) supports demand for single-use, standardized kits and shelf-stable graft formats that fit fast-turnover settings. At the same time, ongoing variability concerns keep outcomes registries and protocol-standardization efforts relevant for vendors, including large-scale PRP outcomes tracking initiatives begun by industry participants.

A second opportunity pocket centers on higher-evidence, label-expanding graft and advanced biologic programs that broaden addressable segments without shifting the care site. In 2026, multiple FDA actions show active product-cycle momentum: Medtronic received FDA premarket approval expanding Infuse bone graft use into one- and two-level TLIF (L2-S1) with both PEEK and titanium cages, and Cerapedics received FDA approval expanding PearlMatrix P-15 indications across multiple lumbar fusion approaches. In osteoarthritis, late-stage pipelines advanced through regulatory and clinical milestones, including Organogenesis completing a rolling BLA submission for ReNu and receiving FDA acceptance for review in 2026, and MEDIPOST initiating U.S. Phase 3 activities for CARTISTEM after FDA alignment on a single pivotal study. These steps create a clearer path to commercialization for disease-focused orthobiologics beyond traditional graft substitution.

Recent Industry Developments

- May 2026: DePuy Synthes entered an exclusive distribution agreement for CGBio's Novosis bone graft substitute across the United States, Canada, and Australia. The move expands access to growth-factor containing graft options in spine and trauma channels. It also supports DePuy Synthes' orthobiologics portfolio with a cross-border rollout, indicating a strategic push in standard bone graft substitutes.

- June 2025: Stryker received FDA clearance for the Incompass Total Ankle System. Expanding reconstructive foot-and-ankle procedure volumes can pull through adjacent biologics and graft materials used to support bone healing and fusion in complex cases. The approval signals broader platform integration for orthobiologics within Stryker's joint reconstruction portfolio.

- June 2024: Stryker announced a definitive agreement to acquire Artelon, Inc. The acquisition broadened Stryker's soft tissue fixation and biomaterial footprint, enabling cross-selling into sports medicine and orthopedic repair settings where orthobiologics are frequently used as adjuncts. It also integrated Artelon's biomaterial capabilities with Stryker's portfolio, expanding scaffold and fixation options for musculoskeletal surgeons.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the orthobiologics market is defined as the revenue generated from biologic and biologically derived products used to support bone, cartilage, tendon, or ligament healing in orthopedic and sports medicine care, captured at the point of sale to the care delivery channel.

Scope exclusions: Adjacent orthopedic devices, general surgical consumables, rehabilitation services, and pharmaceutical pain management drugs are excluded unless sold as part of an orthobiologic product offering.

Segmentation Overview

- By Product Type

- Bone Graft Substitutes

- Demineralized Bone Matrix

- Allografts

- Bone Morphogenetic Proteins

- Viscosupplementation

- Stem Cell Therapy

- Platelet-Rich Plasma

- Other Product Types

- By Application

- Spinal Fusion

- Trauma & Fracture Repair

- Reconstructive Surgery

- Osteoarthritis & Joint Degeneration

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Orthopedic & Sports Medicine Clinics

- Research & Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by making sure the demand pool and product universe are defined in a practical way, and then mapping where value is created across hospital and outpatient settings. We review public sources such as the US FDA databases for approvals and safety communications, the US Centers for Medicare and Medicaid Services for procedure and payment context, and the US CDC for injury and arthritis burden indicators that influence procedure volumes.

We also use sources such as OECD health statistics, World Bank macro indicators, and peer reviewed orthopedic journals to understand procedure trends, clinical adoption shifts, and how usage differs by geography. To anchor the supply side, we refer to company filings, annual reports, investor presentations, and credible press releases, and then we cross-check with paid subscriptions focused on company financials and patent databases to keep product mapping current. This desk list is not exhaustive, and many other public sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what is actually counted as an orthobiologic in routine purchasing, and to test pricing and usage patterns that are not cleanly visible in public data. We speak with a mix of manufacturers, distributors, surgeons, and hospital and ambulatory procurement teams across major regions, and then we revisit outlier inputs until the assumptions line up with real-world ordering behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | APAC: 47% |

| Mid tier: 45% | Functional/Unit leaders: 32% | EMEA: 32% |

| Smaller Players: 16% | Managers: 52% | Americas: 21% |

Market-Sizing & Forecasting

Sizing is built from a top-down demand pool where procedure volumes and treated cohorts are reconstructed by major application areas (such as spinal fusion and trauma repair), and then translated into orthobiologic value using usage rates and average selling prices that match the care setting. To keep the math grounded, we input market fingerprints such as orthopedic procedure volumes by region, penetration of bone graft substitutes versus traditional grafting, average units used per procedure, typical price corridors by product family (for example DBM and BMP products), and the channel mix between hospitals, ambulatory surgical centers, and orthopedic clinics.

Once that view is created, we check totals with selective bottom-up approximations using supplier revenue splits, sampled price points, and channel checks, which helps catch overcounting when a product is used in multiple indications. Where product or region detail is thin, gaps are handled through conservative proxy assumptions that are agreed with interviewees and then tested in sensitivity cases. For forecasting, scenario analysis is used because procedure growth, reimbursement pressure, and adoption of newer therapies do not move in a straight line, and the final path is adjusted after stress-testing the variables that experts flag as the most sensitive.

Data Validation & Update Cycle

Validation is done in several steps so the final values are not dependent on one source or one assumption. We compare the model outputs with independent signals like procedure trend direction, product mix shifts, and known pricing behavior, and then we run variance checks at region and application levels to spot breaks that do not make practical sense. When an anomaly shows up, the input is re-checked against the source trail and, when needed, respondents are re-contacted to confirm whether the change is real or a data artifact.

Before sign-off, the work goes through multi-step analyst review so assumptions, currency handling, and year alignment are consistent across the full dataset. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or notable reimbursement updates. Right before delivery, a final pass is completed to ensure the view reflects the latest available public information.

Mordor Intelligence's Orthobiologics Market Sizing Compared With Other Published Estimates

Published market values for orthobiologics can differ a lot, even when the topic name looks the same, because the counted product set, the care settings included, and the price basis are not always aligned. Differences also show up when firms pick different base years, apply currency conversion at different points, or update assumptions on clinical uptake at different speeds.

The main gap comes from whether estimates fold in broad regenerative medicine revenue, where Mordor Intelligence counts orthobiologics only when it is tied to orthopedic use cases and priced as an orthobiologic purchase, which avoids inflating totals with loosely related biologic therapies.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.06 B (2026) | |

| Specialist Research Portal A | USD 7.10 B (2024) | Uses a different base year and a shorter forecast window, and the product inclusion language is broader, which can pull in adjacent regenerative therapies that are not consistently purchased as orthobiologics. |

| Market Intelligence Publisher B | USD 6.43 B (2024) | Relies on a lower 2024 starting point that appears sensitive to pricing and channel mix assumptions, especially when outpatient procedure growth and higher-priced product families are not fully reflected. |

Reading the three values together, the spread is mainly explained by scope and year alignment, followed by how pricing and setting mix are handled. By keeping the demand pool tied to orthopedic procedures and then pressure-testing usage and ASP inputs through interviews, the estimate stays traceable to a small set of repeatable steps.

Key Questions Answered in the Report

What is the current value of the orthobiologics market?

The orthobiologics market size reached USD 7.06 billion in 2026 and is on track to attain USD 9.52 billion by 2031.

Which product category holds the largest share of the orthobiologic market?

Viscosupplementation dominated 2025 revenue with 42.92%, driven by long-standing Medicare coverage for hyaluronic acid injections.

Which application segment is expanding fastest?

Applications for osteoarthritis and joint degeneration are advancing at a 9.63% CAGR through 2031, as patients seek biologics earlier in disease management.

How quickly are ambulatory surgical centers adopting biologics?

ASCs are projected to post an 8.18% CAGR through 2031, supported by CMS payment parity and workflow-friendly single-use biologic kits.

What geographic region is anticipated to grow most rapidly?

Asia-Pacific is forecast to register an 11.27% CAGR through 2031, reflecting accelerated regulatory approvals in China and expanding private demand in India.

Page last updated on: