All Weather Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 38.73 Billion |

| Market Size (2030) | USD 50.12 Billion |

| Growth Rate (2025 - 2030) | 5.29% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

All Weather Tire Market Analysis by Mordor Intelligence

The All-Weather Tire market size stands at USD 38.73 billion in 2025 and is forecast to reach USD 50.12 billion by 2030 with a projected CAGR of 5.29% during the forecast period (2025-2030). This expansion reflects the All-Weather Tire market’s transition from a niche replacement option toward a mainstream choice driven by rising vehicle ownership in emerging economies, regulatory encouragement for 3PMSF-certified products, and compound innovations that now align winter safety with low rolling resistance. Automakers’ electrification roadmaps intensify demand because battery-electric vehicles create 20% higher tread wear and stricter cabin-noise targets, compelling tire makers to prioritize durability and acoustics simultaneously. Online tire retail and subscription models accelerate penetration by reducing search frictions, while silica-rich compounds narrow the performance gap that once limited adoption among performance-oriented drivers. Competitive focus therefore shifts from scale-driven price wars to platform-specific engineering partnerships that secure OEM fitments and long-term data-sharing agreements within the connected-vehicle ecosystem.[1]Reuters Staff, “Asia-Pacific Tire Growth Drivers,” Reuters, reuters.com

Key Report Takeaways

- By vehicle type, passenger vehicles led with a 50.25% share of the All-Weather Tire market in 2024, while the light commercial vehicles segment is expected to grow at a 6.88% CAGR during the forecast period (2025-2030).

- By tread pattern, symmetrical designs accounted for 38.73% share of the All-Weather Tire market in 2024; the multi-directional patterns segment is expected to grow at a 5.26% CAGR during the forecast period (2025-2030).

- By end-use, personal use commanded 48.68% of the All-Weather Tire market share in 2024. In contrast, the fleet vehicle applications segment is expected to grow at a 6.58% CAGR during the forecast period (2025-2030).

- By sales channel, offline distribution retained an 85.84% share of the All-Weather Tire market in 2024; the online channels segment is expected to grow at a 14.58% CAGR during the forecast period (2025-2030).

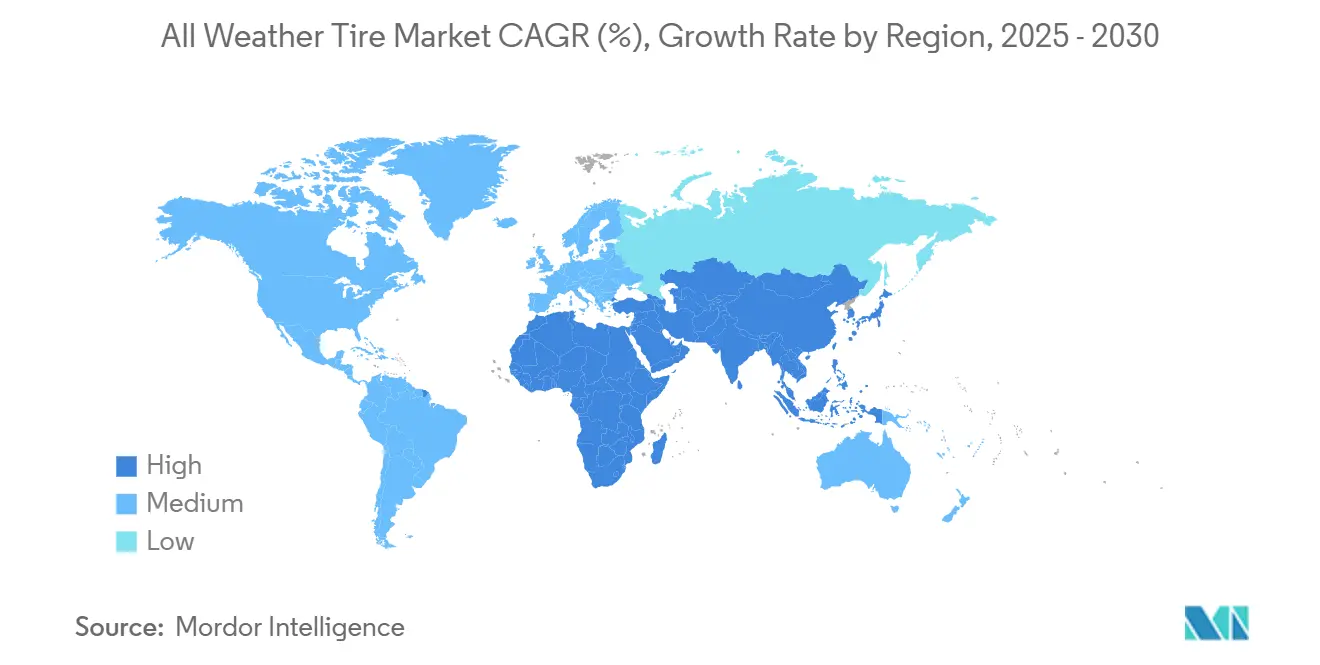

- By geography, the Asia-Pacific captured a 43.97% share of the All-Weather Tire market in 2024, while the Middle East and Africa region segment is expected to grow at a 7.19% CAGR during the forecast period (2025-2030).

Global All Weather Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Passenger-Vehicle Parc | +1.3% | Asia-Pacific core, spillover to MEA | Medium term (2-4 years) |

| Preference for Year-Round Tyres | +1.1% | Global, strongest in North America & Europe | Short term (≤ 2 years) |

| E-Commerce and Last-Mile | +0.9% | Global urban centers, led by Asia-Pacific | Medium term (2-4 years) |

| Silica-Compound Tech | +0.7% | Global, premium segments first | Long term (≥ 4 years) |

| OEM Platform Consolidation | +0.6% | North America & Europe, expanding to Asia | Long term (≥ 4 years) |

| Climate-Variability Regulatory Support | +0.5% | Europe, potential spillover to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Passenger-Vehicle Parc in Emerging Economies

Accelerating motorization in India, Indonesia, and the Philippines introduces millions of first-time buyers who consider year-round convenience a baseline requirement rather than an upgrade. Urban density shrinks household storage space, making seasonal swap-outs impractical and nudging consumers toward single-set solutions that perform across monsoon rains and mild winters. OEMs reinforce this trend by equipping entry-level models with factory-fitted all-weather products to avoid supply-chain complexity. Financial institutions contribute by bundling tire maintenance into vehicle-financing packages, shifting cost conversations from price per unit to holistic mobility budgets. The upshot is that emerging-market growth fuels a structural uplift in All-Weather Tire market demand rather than merely reallocating share away from summer or winter lines.

Convenience Preference for Year-Round Tires

Household time constraints and rising workshop labor rates raise the implicit cost of semi-annual changeovers. Surveys across North American metro areas show drivers ranking “eliminating seasonal swaps” as the top purchase factor, eclipsing even price. Fleet operators echo that sentiment: predictive telematics combined with all-weather compounds reduced maintenance-related downtime significantly between 2022 and 2024. Insurance underwriters in several U.S. states now offer premium rebates for vehicles fitted with 3PMSF-certified all-weather products, further tilting the value equation. As digital retail makes model comparisons transparent, consumers gravitate toward products promising four-season safety with no logistical burden, reinforcing the All-Weather Tire market’s steady share gains.

Growth of E-Commerce and Last-Mile LCV Fleets

Global parcel volumes rose significantly in 2024, pressuring logistics companies to extend service hours regardless of the weather. Operators of light commercial vans seek tread designs that can run from dawn freeze to afternoon downpour without depot-based tire swaps. Telematics data highlights that operators face hefty costs from rerouting and customer-service penalties every time an LCV makes an unscheduled stop, making uptime a quantifiable metric. Consequently, procurement policies increasingly specify all-weather tires with reinforced load indices and silica-based rubber compounds that mitigate winter braking distance penalties. The result is outsized growth for the LCV slice of the All-Weather Tire market, especially in Asia-Pacific megacities where same-day delivery promises hinge on operational continuity.

Silica-Compound Tech Boosting All-Weather Performance

Breakthrough compounding integrates high-dispersion silica, functionalized polymers, and tailored plasticizers to reconcile wet-grip, rolling resistance, and snow-traction objectives once deemed mutually exclusive. Continental’s generation-4 silica tread earned both 3PMSF certification and the EU’s “A” rolling-resistance grade, an alignment previously limited to dual-season lineups[2]“Annual Report 2024,” Continental AG, continental.com. Engineering momentum trickles down product portfolios within two model years, erasing the traditional performance stigma around all-season products in alpine or Nordic regions. As performance parity becomes more visible, consumer word-of-mouth pivots from trade-off skepticism to endorsement, catalyzing an adoption flywheel that sustains the All-Weather Tire market’s mid-single-digit CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Rubber Prices | -0.8% | Global, strongest impact in price-sensitive segments | Short term (≤ 2 years) |

| Low-Cost Imports / Retreads | -0.6% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Trade-Offs Vs. Seasonal Tyres | -0.4% | Europe & Northern North America | Long term (≥ 4 years) |

| ADAS Sensor-Integration Lag | -0.3% | Premium segments globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural and Synthetic-Rubber Prices

Spot prices for RSS-3 natural rubber jumped considerably in 2024 as Southeast Asian monsoons disrupted tapping schedules, while butadiene-based synthetics tracked crude oil volatility. All-weather products often carry slimmer gross margins than high-performance summer lines, giving manufacturers less headroom to absorb cost spikes. Hedging programs mitigate near-term shocks but cannot fully protect cash flows when price swings coincide with contracted OEM deliveries. Smaller regional producers with limited bargaining power face disproportionate margin compression, potentially restraining R&D budgets for compound upgrades and slowing the All-Weather Tire market’s innovation cadence.

Competition From Low-Cost Imports / Retreads

Tires imported from lower-cost regions undercut premium all-weather SKUs at retail in the U.S. Midwest, widening further in Latin American markets where duties are minimal. Retread penetration in long-haul trucking exceeds 40%, diverting replacement-cycle volumes away from new-tire suppliers. While safety regulators scrutinize uncertified imports, enforcement gaps persist at land borders, particularly for small shipments entering through e-commerce channels. The resulting price pressure forces established brands to run promotional campaigns that erode profitability and risk brand dilution, challenging the All-Weather Tire market’s value-capture potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive the Electrification Transition

Passenger vehicles contributed the most significant revenue in 2024, capturing 50.25% share of the All-Weather Tire market share. However, their growth moderates as replacement cycles lengthen and consumers favor durability upgrades over cosmetic tread changes. Light commercial vehicles, propelled by e-commerce boom dynamics, exhibit the most robust adoption trajectory, expanding at 6.88% CAGR during the forecast period (2025-2030) and signaling a structural pivot toward professional fleet demand. Medium and heavy-duty trucks adopt all-weather compounds chiefly to consolidate inventories across diverse routes, although weight-class regulations still necessitate specialized retreads for certain axle positions. Electric vans’ 20% higher torque and rapid acceleration curves further rationalize premium compound investments that manage accelerated tread wear without compromising energy efficiency.

Fleet electrification amplifies engineering challenges because battery packs increase gross vehicle weight, heightening the need for reinforced sidewalls and minimizing heat build-up. Consequently, tire makers design bead fillers that endure higher instantaneous loads during regenerative braking. Passenger-car prospects remain attractive in emerging economies where first-time owners leapfrog straight to all-weather solutions, sidestepping the summer-winter dichotomy. Two-wheeler and three-wheeler categories stay niche but show potential, especially in Southeast Asian ride-hailing fleets that prize convenience over maximal cornering grip. This compositional shift underlines a broader narrative in which commercial duty cycles, rather than private commuting needs, increasingly steer innovation priorities within the All-Weather Tire market.

By Tread Pattern: Multi-Directional Innovation Accelerates

Symmetrical tread designs dominated 38.73% share of the All-Weather Tire market in 2024, because their uniform blocks simplify mass production and rotation routines, which suits the cost sensitivities of family sedans and budget-oriented crossovers. Nonetheless, multi-directional patterns are projected to register a 5.26% CAGR during the forecast period (2025-2030), becoming the vanguard of a technology wave that merges snow-siping density with aquaplaning channels absent directional-mounting constraints. The All-Weather Tire market size associated with multi-directional offerings is expected to double by 2030 as car makers specify them for global vehicle platforms to avoid regional stocking complexity. Once prized for aquaplaning resistance, directional patterns lose share because mounting errors incur performance penalties that digital-retail customers find unacceptable. Asymmetrical designs retain relevance in high-performance niches where lateral stiffness and wet-cornering precision remain differentiators, yet their higher mold costs restrict penetration in economy segments.

Advances in computer-aided tread-block sequencing allow multi-directional designs to mimic the noise-cancellation benefits of asymmetric layouts without their orientation constraints. Manufacturers couple this geometry with advanced silica compounds, enabling 3PMSF certification and low rolling resistance in one SKU. Service centers benefit from reduced installation time, while fleets appreciate the option to rotate tires front-to-rear without violating tread-direction rules. These user-experience dividends resonate strongly with online buyers who often self-install, thus reinforcing the momentum behind multi-directional adoption across the All-Weather Tire market.

By End-Use: Fleet Optimization Drives Growth

Personal-use vehicles account for a 48.68% share of the All-Weather Tire market in 2024. Yet, the headline growth story resides in fleet applications, which are forecast to advance at a 6.58% CAGR during the forecast period (2025-2030). Fleet asset managers quantify downtime to the minute, rendering the older practice of switching to winter sets economically unattractive. Predictive analytics platforms interface directly with tire-pressure-monitoring systems, auto-generating work orders synchronizing with driver schedules, enhancing operational efficiency. Commercial-use sub-segments, such as municipal service vans, follow suit as city councils impose emissions zones that favor electric drivetrains paired with low-rolling-resistance footwear.

The rise of gig-economy delivery services intensifies mileage accumulation per vehicle, compressing replacement intervals and amplifying the importance of compound longevity. Responding to fluctuating tourist demand, rental car agencies now build procurement tenders that stipulate all-weather compounds to avoid storage costs across diverse depots. Conversely, personal-use growth plateaus in mature markets because inflation-adjusted household budgets delay discretionary upgrades. Nonetheless, emerging-market consumers, confronting climate unpredictability and storage constraints, continue to perceive all-weather tires as a value-added standard, ensuring the segment’s foundational relevance within the All-Weather Tire market.

By Sales Channel: Digital Transformation Accelerates

Offline retail, including franchised dealers and independent workshops, retained an 85.84% share of the All-Weather Tire market in 2024, reflecting entrenched consumer habits and the safety-critical nature of installation. However, online channels are forecast to surge at a 14.58% CAGR during the forecast period (2025-2030), capturing incremental share as click-and-fit models integrate logistics, appointment scheduling, and financing on a single screen. The All-Weather Tire market size transacted through digital storefronts could exceed USD 9 billion by 2030, given rising smartphone penetration and consumer confidence in e-commerce for automotive parts. E-tailers leverage recommendation algorithms that map trend ratings to local weather data, simplifying decision journeys and fostering brand-agnostic comparisons.

Subscription services tie sensor-read tread-depth data into automatic re-ordering workflows, transferring purchasing agency from driver to cloud platform. Offline incumbents respond by partnering with online marketplaces to provide last-mile installation, morphing into hybrid models that monetize service bays while tapping digital lead pools. Price transparency compresses margins at the SKU level but opens ancillary revenue streams in alignment, nitrogen fills, and disposal fees. The convergence of data-driven targeting and localized service fulfillment transforms sales channels from transactional gateways into recurring-service ecosystems, expanding the influence of digital touchpoints across the All-Weather Tire market.

Geography Analysis

Asia-Pacific sustained 43.97% revenue share in 2024 and is on course for a 5.23% CAGR through 2030, underpinned by India’s automotive road-map and China’s regulatory mandates that peg EV adoption to provincial carbon-credit quotas. Local governments subsidize 3PMSF-rated tires within cold-climate prefectures, accelerating volume ramp-ups, while capacity expansions in Thailand and Indonesia ensure supply stability. Urban consumers gravitate toward all-weather convenience to sidestep storage fees in space-constrained high-rise parking structures. Fleet electrification further amplifies demand.

Europe posts a steadier 3.83% CAGR, leveraging the EU’s Tire Labelling Regulation 2020/740 that couples energy-grade visibility with snow-grip icons to steer consumer choice[3]“Tire Labeling Regulation 2020/740,” European Commission, ec.europa.eu. Multi-country winter-tire mandates incentivize fleets to adopt all-weather SKUs that achieve 3PMSF certification, simplifying cross-border compliance. OEMs headquartered in Germany and France integrate all-weather lines into factory builds for cross-continental model trims, boosting first-fit volumes and feeding replacement cycles. Scandinavian markets, though small in volume, serve as technology proving grounds because their extreme weather benefits highlight compound efficacy, shaping global marketing narratives.

The Middle East & Africa emerges as the fastest-growing cluster at 7.19% CAGR, propelled by logistics corridor investments spanning the UAE, Saudi Arabia, and Morocco. Gulf fleet operators favor all-weather tires to accommodate steep temperature swings between desert highways and mountain routes. Morocco’s ascension as a manufacturing hub, underscored by new capacity additions in Tangier, shortens shipping lanes to European customers and captures duty-free advantages under EU association agreements. North America’s 4.05% CAGR reflects mature replacement cycles offset by surging EV registrations in California and Quebec, where state incentives encourage purchase of low-rolling-resistance, 3PMSF-certified products. South America tracks a 4.28% CAGR as e-commerce penetration expands in Brazil and Chile, making fleet uptime a critical operating metric.

Competitive Landscape

The All-Weather Tire market shows moderate consolidation: Michelin, Bridgestone, and Goodyear collectively account for the majority of 2024 revenue, yet more than a dozen regional specialists hold footholds in niche tread patterns and geography-specific SKUs. Leaders diversify risk by vertically integrating compound production and by securing renewable-rubber supply agreements to buffer price volatility. Strategic intent centers on securing OEM fitments for scalable EV platforms; for example, Michelin’s CrossClimate 3 line debuted as factory equipment on multiple C-segment electric SUVs in 2025, locking in future replacement cycles.

Technology partnerships redefine competitive rules. Continental collaborates with high-frequency sensor manufacturers to embed tread-wear telemetry into sidewalls, positioning the tire as a data node within vehicle health-monitoring stacks. Goodyear’s codevelopment of bio-based polymers with U.S. chemical suppliers aligns brand equity with sustainability agendas, catering to ESG-oriented corporate fleets. Meanwhile, Asian challengers scale global ambitions: Sumitomo leverages low-cost Indonesian capacity to undercut incumbents in price-sensitive European segments, while Giti pairs with ride-sharing platforms to pilot subscription-tire bundles.

Market entrants exploit e-commerce channel growth, bypassing traditional wholesalers through direct-to-consumer drop-ship models that package installation at franchised centers. Incumbents counter by piloting predictive analytics services that alert drivers of remaining tread life via smartphone apps, thereby preserving brand touchpoints post-sale. As autonomous-vehicle pilots advance, tire makers race to certify functional-safety standards under ISO 26262, tightening regulatory hurdles for latecomers and reinforcing the strategic premium on R&D outlays in the All-Weather Tire market.

All Weather Tire Industry Leaders

Bridgestone

Goodyear Tire and Rubber Company

Continental AG

Hankook Tire and Technology

Nokian Tyres

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: API Tire expanded its Gladiator line-up with the Armor 4S, an all-weather product available in 43 passenger/CUV/SUV sizes and 4 transit sizes for commercial vans, spanning 15–22 in rim diameters.

- August 2025: Bridgestone Americas introduced the W920 drive tire featuring next-generation ENLITEN technology aimed at extended life and maximum traction in year-round trucking applications.

- May 2025: Michelin launched the CrossClimate 3 and CrossClimate 3 Sport globally, incorporating enhanced silica compounds that attain 3PMSF winter certification and improved fuel-efficiency ratings.

- March 2025: Nokian Tyres debuted the Seasonproof 2 all-season line containing up to 38% renewable and recycled materials, including 2% ISCC PLUS mass-balance-certified bio-based feedstock.

Global All Weather Tire Market Report Scope

| Passenger Vehicle |

| Light Commercial Vehicle |

| Medium and Heavy-Duty Commercial Vehicle |

| Two-Wheeler |

| Three-Wheeler |

| Symmetrical |

| Asymmetrical |

| Directional |

| Multi-Directional |

| Personal Use |

| Commercial Use |

| Fleet Vehicle |

| Online |

| Offline |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Vehicle | |

| Light Commercial Vehicle | ||

| Medium and Heavy-Duty Commercial Vehicle | ||

| Two-Wheeler | ||

| Three-Wheeler | ||

| By Tread Pattern | Symmetrical | |

| Asymmetrical | ||

| Directional | ||

| Multi-Directional | ||

| By End-Use | Personal Use | |

| Commercial Use | ||

| Fleet Vehicle | ||

| By Sales Channel | Online | |

| Offline | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecasted value of the All-Weather Tire market by 2030?

The market is projected to reach USD 75.98 billion by 2030 at a 5.29% CAGR.

Which vehicle class is expanding fastest within all-weather adoption?

Light commercial vehicles lead with a 6.88% CAGR, driven by e-commerce logistics and fleet electrification.

How are online sales influencing tire procurement?

Digital channels are growing at a 14.58% CAGR, pairing e-commerce convenience with professional installation to capture share from traditional retail.

Why are all-weather tires critical for electric vehicles?

EVs impose 20% higher tread wear and stricter cabin-noise limits, making durable low-noise all-weather compounds crucial for range and comfort.

Which region will add the most incremental demand through 2030?

The Middle East and African region is the fastest-growing contributor, bolstered by rising vehicle ownership and government EV mandates.

What technological innovation is accelerating all-weather performance gains?

High-dispersion silica compounds deliver simultaneous 3PMSF winter certification and low rolling resistance, eliminating historical performance trade-offs.

Page last updated on: