Snow Mobile Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

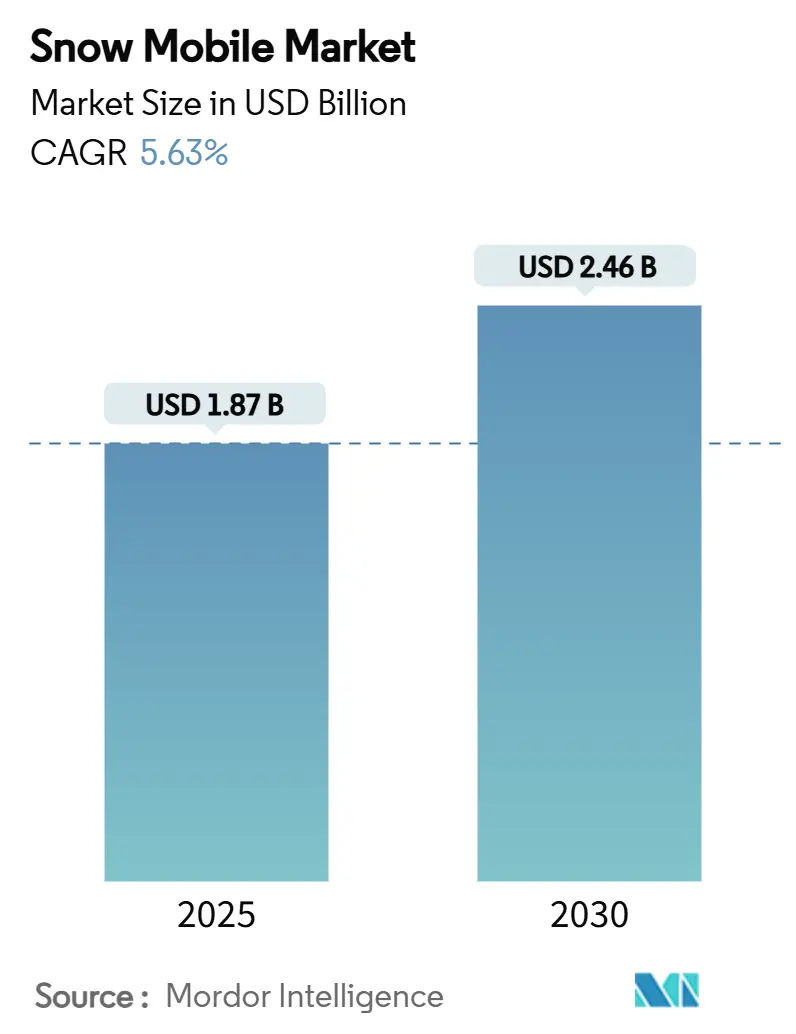

| Market Size (2025) | USD 1.87 Billion |

| Market Size (2030) | USD 2.46 Billion |

| Growth Rate (2025 - 2030) | 5.63% CAGR |

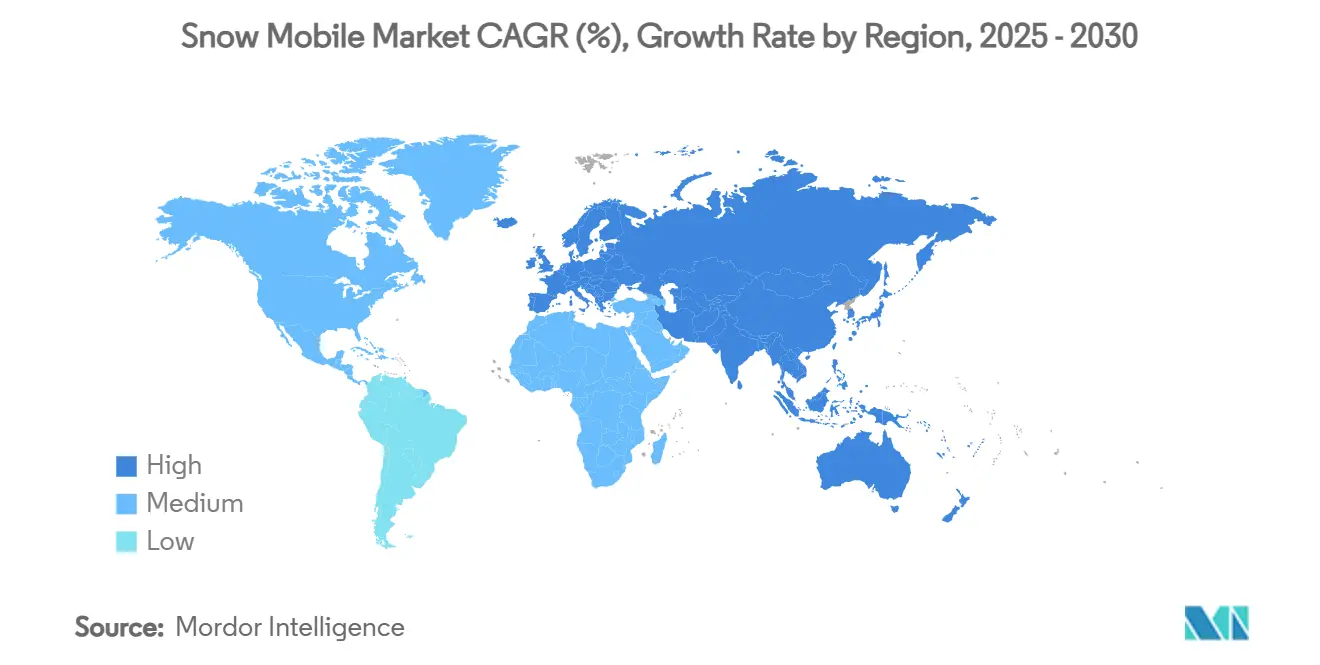

| Fastest Growing Market | Europe |

| Largest Market | Europe |

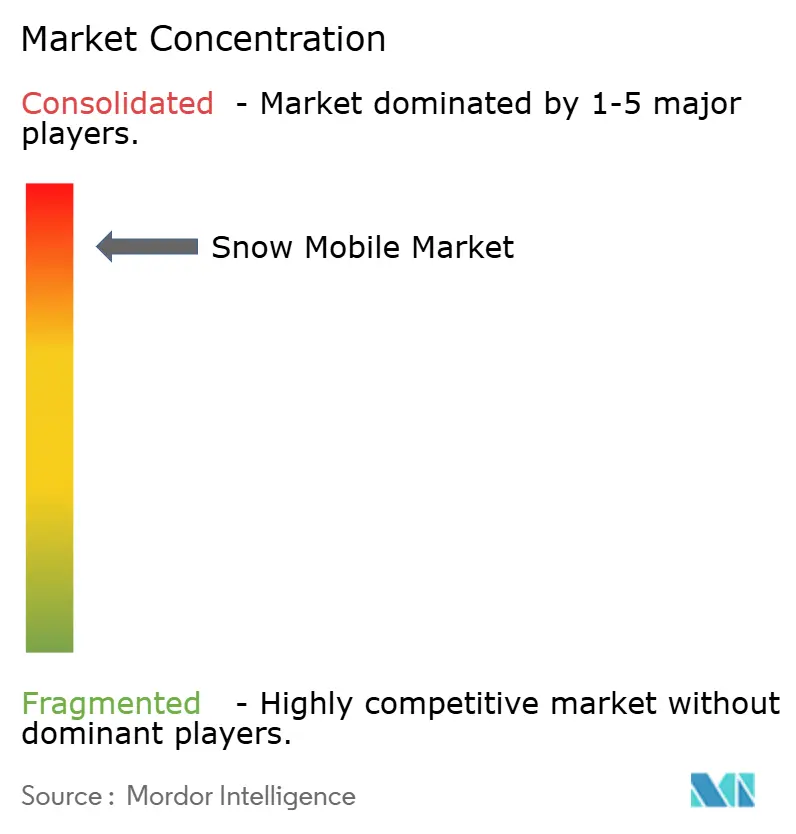

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Snow Mobile Market Analysis by Mordor Intelligence

The global snowmobile market size stands at USD 1.87 billion in 2025 and is expected to reach USD 2.46 billion in 2030, translating into a 5.63% CAGR during the forecast window. This expansion comes even as the snowmobile market wrestles with climate-driven variability, elevated compliance costs, and lingering supply-chain tightness. Fleet electrification, turbo powertrain upgrades, and data-rich digital rental platforms are widening the customer base far beyond core enthusiasts, while ongoing consolidation among original-equipment manufacturers (OEMs) is reshaping competitive conduct. Europe’s leadership position stems from well-funded winter tourism infrastructure and Arctic-logistics procurement programs that feed sustained demand. In parallel, North American OEMs are safeguarding margins through stricter build-to-order strategies and premium trim lines that deliver higher average selling prices. The snowmobile market also benefits from relatively high consumer attachment to outdoor recreation in key economies and from governments that view modern sleds as cost-effective cold-weather mobility solutions.

Key Report Takeaways

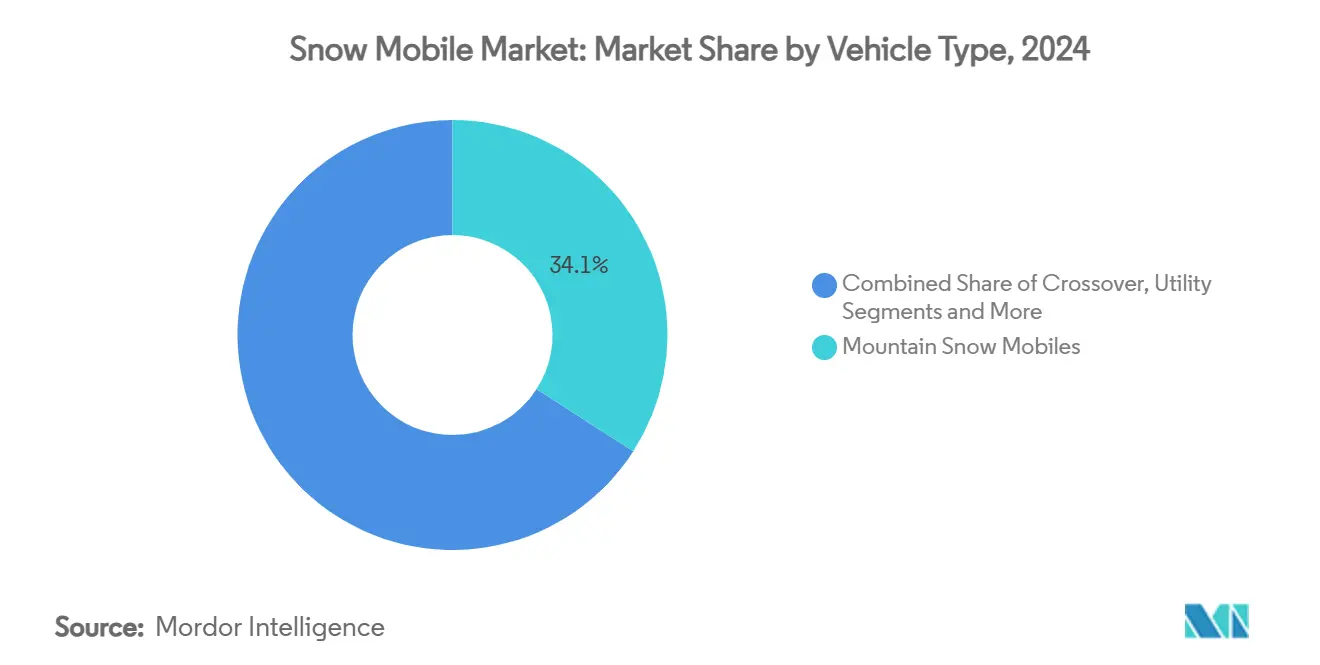

- By vehicle type, the mountain segment captured 34.15% of snowmobile market share in 2024; it is forecast to accelerate at a 9.12% CAGR through 2030.

- By engine type, 4-stroke models held 28.87% of the snowmobile market size in 2024, while turbocharged 2-stroke variants are projected to expand at a 6.94% CAGR by 2030.

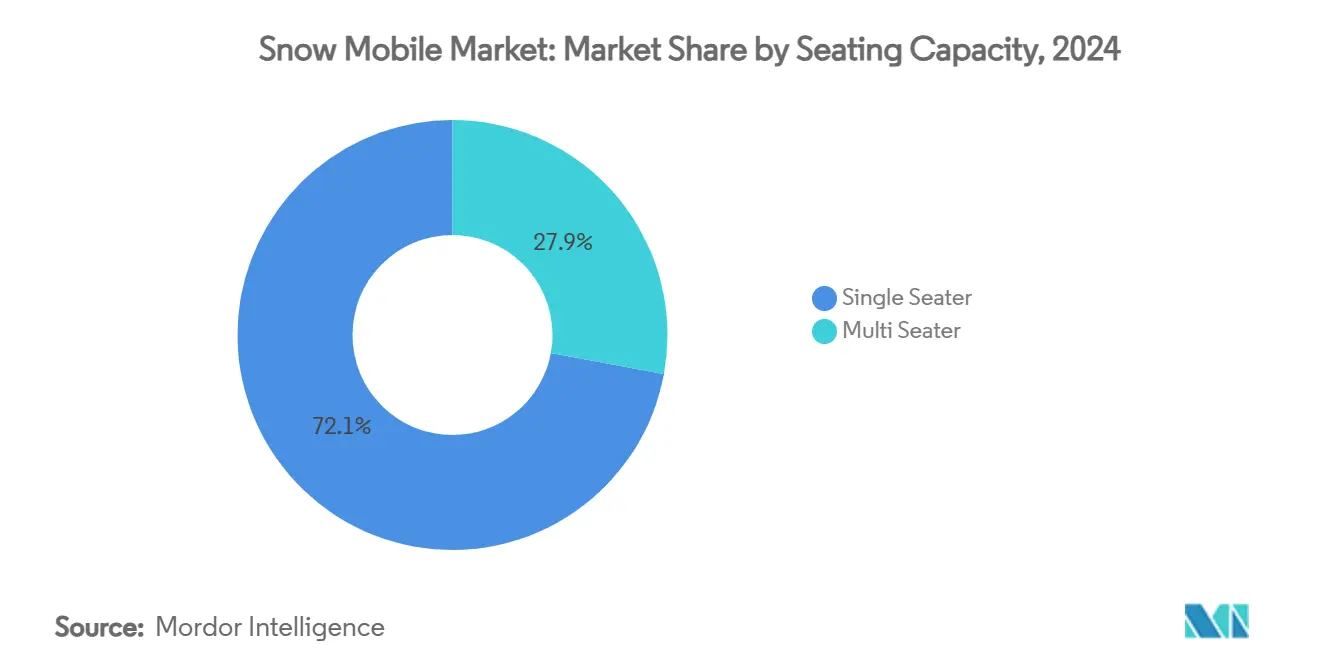

- By seating capacity, single-seater sleds accounted for 72.08% of the snowmobile market size in 2024, and they are on track for an 8.03% CAGR over 2025-2030.

- By application, recreation and tourism commanded 23.02% of the snowmobile market share in 2024; the segment is advancing at a 7.89% CAGR in the same period.

- By geography, Europe led with an 18.17% revenue share in 2024, and it is the fastest-growing region at a 6.95% CAGR to 2030

Global Snow Mobile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Winter-Tourism Expenditures | +1.2% | Europe, North America, Japan | Medium term (2-4 years) |

| Advances in Turbo 2-stroke and 4-stroke Powertrains | +0.8% | Global | Long term (≥ 4 years) |

| Electrification Enabling Noise-sensitive Eco-tourism | +0.6% | Europe, North America | Long term (≥ 4 years) |

| Online Rental Platforms Expanding Casual Ridership | +0.4% | Global | Short term (≤ 2 years) |

| Government Arctic-logistics Procurements | +0.3% | North America, Europe | Medium term (2-4 years) |

| OEM Accessories Pull-through | +0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Winter-Tourism Expenditures

Winter tourism expenditures are reshaping snowmobile demand patterns as destinations invest in premium experiences to attract high-spending international visitors. Japan's ski resorts recorded 10.5 million international visitors from December 2024 to February 2025, representing a 33% increase from pre-pandemic levels, while domestic skiing demand has plummeted 75% since the 1990s[1]Monica Pitrelli, "International visitors pour into Japan — to the delight and dismay of its ski towns," CNBC, cnbc.com.. This demographic shift favors guided snowmobile tours and rental operations over traditional ownership models, creating opportunities for manufacturers to partner with tourism operators. European destinations are leveraging electric snowmobiles to access noise-sensitive wilderness areas, with Hurtigruten Svalbard deploying battery-powered units for Arctic wildlife tours[2]"Wilderness Safari by Electric Snowmobile," Hurtigruten Svalbard, hurtigrutensvalbard.com.. The tourism-driven demand provides revenue stability that partially insulates manufacturers from weather-dependent recreational sales volatility. Saudi Arabia's bid to host the 2029 Asian Winter Games at the TROJENA project signals emerging market potential, with projected economic impact of USD 798 million by 2030.

Advances in Turbo 2-Stroke and 4-Stroke Powertrains

Turbo engine technology represents the industry's most significant powertrain advancement, enabling manufacturers to deliver higher performance while meeting stringent emissions standards. Ski-Doo's Rotax 850 E-TEC Turbo became the world's first factory-built 2-stroke turbocharged engine, delivering 165 horsepower on pump fuel with no turbo lag. Arctic Cat's new 858 engine for the CATALYST platform demonstrates similar forced induction capabilities, allowing smaller displacement engines to match traditional larger variants while reducing weight and improving fuel efficiency. These technological advances enable manufacturers to maintain performance leadership while complying with EPA emissions standards that require maximum 150 g/kW-hr for hydrocarbons and 400 g/kW-hr for carbon monoxide. The turbo technology also addresses high-altitude performance degradation, maintaining power output at elevations up to 8,000 feet where naturally aspirated engines lose significant horsepower. This innovation cycle positions turbo variants as the premium segment's growth driver, justifying higher price points despite manufacturing complexity.

Electrification Enabling Noise-Sensitive Eco-Tourism

Electric snowmobile adoption is accelerating beyond environmental compliance to unlock new market segments in noise-sensitive wilderness areas and eco-tourism applications. Taiga Motors' Atlas electric snowmobile delivers up to 180 horsepower with 0-100 km/h acceleration in 2.9 seconds, demonstrating that electric powertrains can match traditional performance metrics. The elimination of noise pollution enables access to wildlife viewing areas previously restricted to traditional snowmobiles, expanding the addressable market for tourism operators. Electric models also reduce maintenance complexity by eliminating oil changes and engine upkeep, lowering the total cost of ownership for rental fleets. However, cold-weather battery performance remains a constraint, with current ranges of 31-103 kilometers limiting applications to short-distance tours and day trips rather than extended backcountry exploration.

Online Rental Platforms Expanding Casual Ridership

Digital rental platforms are democratizing snowmobile access by reducing barriers to entry for casual riders and expanding the customer base beyond traditional ownership models. Polaris Adventures operates rental networks across multiple winter destinations, offering guided tours and self-guided excursions with models ranging from 2-up trail sleds to deep powder mountain variants. The platform model enables manufacturers to maintain utilization rates for rental fleets while introducing new customers to their brands without requiring significant capital investment. Online booking systems also provide valuable customer data and usage patterns that inform product development and marketing strategies. The rental model particularly appeals to younger demographics and urban populations who prioritize access over ownership, aligning with broader sharing economy trends. This channel expansion helps offset declining traditional dealership sales while creating recurring revenue streams for manufacturers and their partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global Emissions Standards | -1.1% | Global | Long term (≥ 4 years) |

| Shorter Snow Seasons from Climate Change | -0.9% | Global, acute in lower latitudes | Long term (≥ 4 years) |

| Cannibalization by Compact Tracked Utility Vehicles | -0.5% | North America, Europe | Medium term (2-4 years) |

| Aging Core Ridership Demographic | -0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Emissions Standards

Emissions regulations are imposing significant compliance costs and technological constraints that limit product development flexibility while increasing manufacturing complexity. The EPA's 40 CFR Part 1051 standards require snowmobiles to meet maximum emissions of 150 g/kW-hr for hydrocarbons and 400 g/kW-hr for carbon monoxide, with full compliance required over 8,000 kilometers or 400 hours of operation[3]"What are the exhaust emission standards for snowmobiles?," Code of Federal Regulations, ecfr.gov.. These standards necessitate expensive catalytic converter systems, fuel injection technologies, and advanced engine management systems that increase unit costs by an estimated 15-20% compared to pre-regulation models. Small-volume manufacturers face particular challenges, as they can only produce up to 600 units annually under relaxed standards, limiting their ability to scale operations. The regulatory burden also accelerates consolidation as smaller players lack resources to develop compliant powertrains, contributing to market concentration. Transport Canada's requirement for Vehicle Identification Numbers on snowmobiles adds additional compliance complexity for cross-border trade.

Shorter Snow Seasons from Climate Change

Climate change is fundamentally altering the snowmobile market's seasonal dynamics, creating demand volatility that challenges traditional business models and inventory management strategies. Hokkaido University research indicates that global temperature increases of 4 degrees Celsius would transform Japan's renowned powder snow into heavier, wetter conditions typical of lower-latitude regions. Ontario's warmer winters have already impacted snowmobile safety and profitability, forcing trail closures and reducing rideable days per season. Poor winter conditions directly correlate with sales declines, as evidenced by BRP's low-thirties percentage drop in snowmobile sales during the 2024 season due to unfavorable weather. Manufacturers are responding by diversifying into year-round products and investing in electric models that can operate in marginal snow conditions. The climate impact also drives geographic market shifts toward higher-latitude regions with more reliable snowfall, potentially reshaping distribution strategies and dealer networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Mountain Segment Drives Premium Growth

Mountain snowmobiles command 34.15% market share in 2024 and represent the fastest-growing segment at 9.12% CAGR through 2030, reflecting the premium positioning of backcountry-capable models and their higher profit margins. The segment's growth is driven by technological innovations like Ski-Doo's Summit X, featuring a 14-pound weight reduction and new T Motion X with Coilover suspension, along with advanced features including 10.25-inch touchscreen displays with built-in GPS and GroupRide capabilities. Trail models maintain steady demand for groomed-path riding, while Crossover variants bridge the gap between trail and mountain applications. Utility snowmobiles serve specialized applications including rescue operations and government procurement, with models like the D900 Diesel Multi-Fuel Snowmobile designed for Canadian Armed Forces Arctic missions with over 500-kilometer range capabilities.

The mountain segment's premium pricing power stems from its technical complexity and specialized engineering requirements for deep powder performance. Advanced features like turbocharged engines, electronic suspension systems, and lightweight construction justify price points exceeding USD 20,000 for top-tier models. This segment also benefits from lower price sensitivity among enthusiast customers who prioritize performance over cost, enabling manufacturers to maintain healthy margins despite rising material and compliance costs.

By Engine Type: Turbo Technology Reshapes Powertrain Landscape

4-stroke engines hold the largest market share at 28.87% in 2024, benefiting from fuel efficiency advantages and smoother power delivery characteristics preferred by touring and utility applications. However, 2-stroke turbo variants are emerging as the fastest-growing subsegment at 6.94% CAGR, driven by breakthrough technologies like Ski-Doo's Rotax 850 E-TEC Turbo that delivers 165 horsepower while meeting stringent emissions standards. Electric powertrains remain niche but are gaining traction in specific applications, with Taiga Motors' production milestone of first customer-ready electric snowmobiles marking a significant industry development. Traditional 2-stroke engines maintain relevance in performance applications due to their superior power-to-weight ratios, though manufacturers are investing heavily in emissions compliance technologies.

The engine segmentation reflects broader industry trends toward electrification and forced induction as manufacturers balance performance requirements with environmental regulations. Turbo technology enables smaller displacement engines to match larger naturally aspirated variants while improving fuel efficiency and reducing emissions, positioning this subsegment for continued growth as regulations tighten globally.

By Seating Capacity: Single-Seater Dominance Reflects Performance Focus

Single-seater configurations capture 72.08% market share in 2024 and grow at 8.03% CAGR through 2030, reflecting the market's performance orientation and the premium positioning of solo-rider models. This segment benefits from weight optimization advantages and specialized ergonomics that enhance rider control in challenging terrain conditions. Multi-seater models serve touring and family applications, offering shared riding experiences and utility for recreational users who prioritize comfort over maximum performance. The single-seater preference also aligns with the mountain segment's growth trajectory, as backcountry riding typically favors individual machines over passenger-carrying configurations.

The seating capacity segmentation reveals distinct use case patterns, with single-seater models commanding premium pricing due to their specialized engineering and performance focus. Multi-seater variants serve broader market segments including rental operations and family recreation, though they typically operate at lower price points and margins compared to performance-oriented single-seater models.

By Application: Recreation and Tourism Leads Market Expansion

Recreation and Tourism applications dominate with 23.02% market share in 2024 and accelerate at 7.89% CAGR, driven by growing winter tourism expenditures and the expansion of guided tour operations in international destinations. This segment benefits from the democratization of snowmobiling through rental platforms and the emergence of electric models that enable access to noise-sensitive wilderness areas. Utility, Rescue, and Law Enforcement applications provide stable demand through government procurement programs, with specialized models like those used by New York State Police for patrol operations and search-and-rescue missions. Military and Industrial applications represent niche but high-value opportunities, exemplified by the D900 Diesel Multi-Fuel Snowmobile's development for Canadian Armed Forces Arctic sovereignty patrols.

The application segmentation reflects the market's evolution from purely recreational origins toward diverse commercial and governmental uses. This diversification provides revenue stability and reduces dependence on weather-dependent recreational sales, while creating opportunities for specialized product development and premium pricing in professional applications.

Geography Analysis

Europe leads the global snowmobile market with 18.17% share in 2024 and represents the fastest-growing region at 6.95% CAGR through 2030, driven by robust winter tourism infrastructure and significant manufacturing presence. BRP's celebration of producing half a million snowmobiles in Finland underscores the region's manufacturing importance, while Lynx Commander's position as Europe's best-selling snowmobile demonstrates strong local brand preference. Scandinavian countries particularly benefit from reliable snowfall patterns and established trail networks, with destinations like Finnish Lapland and Swedish Kiruna ranking among the world's top snowmobiling locations. The region's emphasis on environmental sustainability also drives electric snowmobile adoption, with operators like Hurtigruten Svalbard deploying battery-powered units for eco-tourism applications.

North America maintains its position as the traditional snowmobile heartland, with the United States and Canada contributing significantly to global volumes. The region's economic impact remains substantial, while supporting over 100,000 full-time jobs. However, climate change poses increasing challenges, with shorter snow seasons and warmer winters affecting trail conditions and sales patterns. The region's mature market characteristics also contribute to demographic aging, with the average snowmobiler now 54 years old and spending approximately USD 2,500 annually on the sport.

Asia-Pacific emerges as a growth frontier, led by Japan's winter sports renaissance that recorded 10.5 million international visitors from December 2024 to February 2025, representing a 33% increase from pre-pandemic levels. Hokkaido's powder snow reputation attracts global snowmobiling enthusiasts, though climate change threatens the region's snow quality advantages. The domestic Japanese market faces challenges from declining participation, with skiing numbers dropping 75% since the 1990s, necessitating increased reliance on international tourism. Other regional markets including South Korea and China present long-term opportunities as winter sports infrastructure develops, though current penetration remains limited compared to traditional snowmobiling regions.

Competitive Landscape

The snowmobile market exhibits high concentration, with BRP (Ski-Doo) commanding over a significant share in the global market as of 2025, creating oligopolistic dynamics that enable pricing power while limiting competitive intensity. This consolidation accelerated following Arctic Cat's operational challenges under Textron ownership, including factory layoffs and production suspension that culminated in the brand's acquisition by the Brad Darling Investment Group in April 2025. Yamaha's strategic restructuring of its snowmobile business signals potential market exit, further concentrating the competitive landscape among fewer players.

Technology differentiation drives competitive positioning, with manufacturers investing heavily in turbo engine development, electrification capabilities, and digital integration features. BRP's Rotax 850 E-TEC Turbo represents the industry's first factory-built 2-stroke turbocharged engine, while Arctic Cat's new 858 engine for the CATALYST platform demonstrates similar forced induction capabilities. Electric vehicle specialist Taiga Motors emerged as a potential disruptor despite financial challenges, securing CAD 50.15 million in convertible debentures to fund production scaling. White-space opportunities exist in utility applications, government procurement, and emerging markets where established players have limited presence, though high barriers to entry from emissions compliance requirements favor incumbent manufacturers with existing engineering capabilities.

Snow Mobile Industry Leaders

-

Polaris Inc.

-

Arctic Cat (Textron)

-

BRP Inc. (Ski-Doo and Lynx)

-

Taiga Motors Corp.

-

Alpina Snowmobiles

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Polaris unveiled its 2026 snowmobile lineup featuring innovation across multiple segments, including enhanced suspension systems and performance upgrades. The announcement signals continued investment in product development despite challenging market conditions.

- February 2025: Ski-Doo announced 2026 model year enhancements including Summit X weight reduction and T Motion X suspension technology. The updates demonstrate continued innovation in mountain segment products.

- November 2024: BRP celebrated production milestone of half a million snowmobiles manufactured in Finland, highlighting European manufacturing capabilities and market presence.

Global Snow Mobile Market Report Scope

| Trail |

| Mountain |

| Crossover |

| Utility |

| 2-Stroke |

| 4-Stroke |

| Electric |

| Single Seater |

| Multi Seater |

| Recreation and Tourism |

| Utility/Rescue/Law-Enforcement |

| Military and Industrial |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Finland | |

| Sweden | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Trail | |

| Mountain | ||

| Crossover | ||

| Utility | ||

| By Engine Type | 2-Stroke | |

| 4-Stroke | ||

| Electric | ||

| By Seating Capacity | Single Seater | |

| Multi Seater | ||

| By Application | Recreation and Tourism | |

| Utility/Rescue/Law-Enforcement | ||

| Military and Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Finland | ||

| Sweden | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the snowmobile market?

The global snowmobile market size is USD 1.87 billion in 2025.

How fast is the snowmobile market growing?

It is projected to expand at a 5.63% CAGR from 2025 to 2030.

Which region is the fastest-growing in the snowmobile market?

Europe leads growth at a 6.95% CAGR through 2030, supported by robust winter-tourism infrastructure.

What technology trends are influencing new snowmobile models?

Turbocharged 2-stroke engines and battery-electric powertrains are driving performance upgrades while meeting tightening emissions rules.

Page last updated on: