Aircraft Gears Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

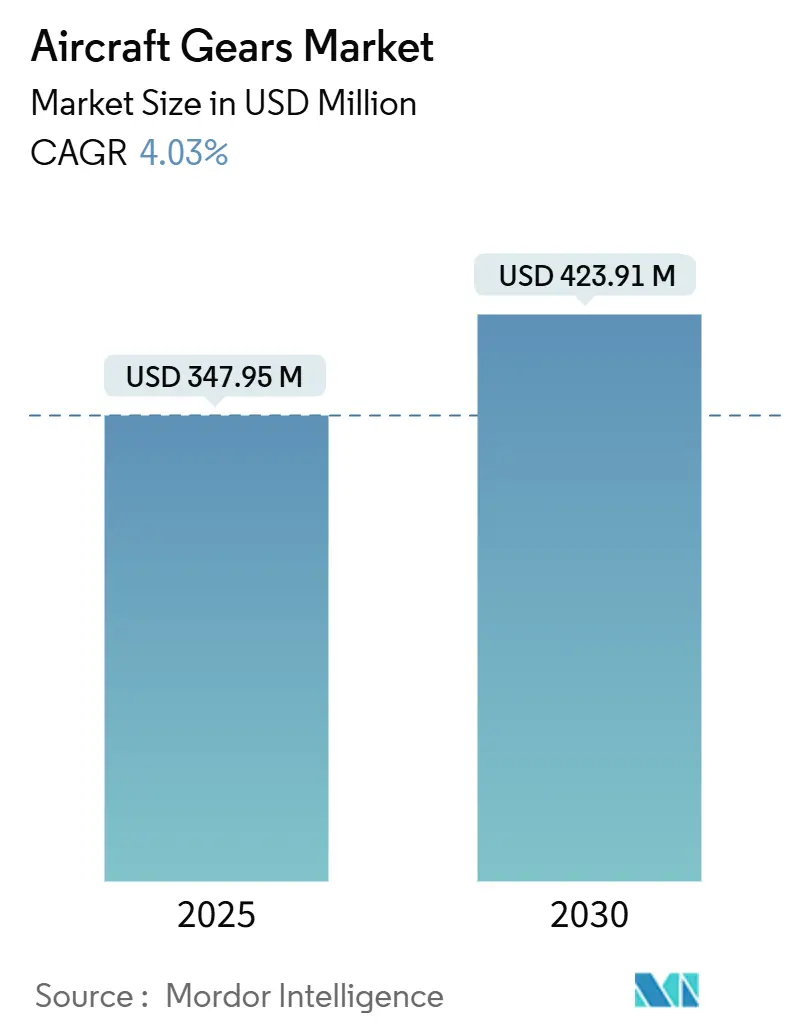

| Market Size (2025) | USD 347.95 Million |

| Market Size (2030) | USD 423.91 Million |

| Growth Rate (2025 - 2030) | 4.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Gears Market Analysis by Mordor Intelligence

The aircraft gears market size stands at USD 347.95 million in 2025, and it is forecasted to advance to USD 423.91 million by 2030 on a 4.03% CAGR trajectory. Geared-turbofan adoption, especially on popular narrow-body programs, drives precision gear demand as airlines push for higher fuel efficiency and lower emissions.[1]Source: Aviation Week, “Commercial Aircraft Deliveries and Engine Requirements 2025-2034,” aviationweek.com Fixed-wing fleets are undergoing large-scale renewal and continuing military rotorcraft upgrade, sustaining baseline orders even when macroeconomic headwinds slow discretionary spending.[2]Source: U.S. Army, “Future Long Range Assault Aircraft,” army.milAsia-Pacific’s manufacturing surge, supported by widening supply-chain localization in India and China, channels additional volume toward regional gear vendors able to meet AS9100 quality standards. Meanwhile, digital-twin–enabled predictive maintenance solutions gain traction among operators seeking to cut gearbox lifecycle costs and avoid unplanned AOG events.

Key Report Takeaways

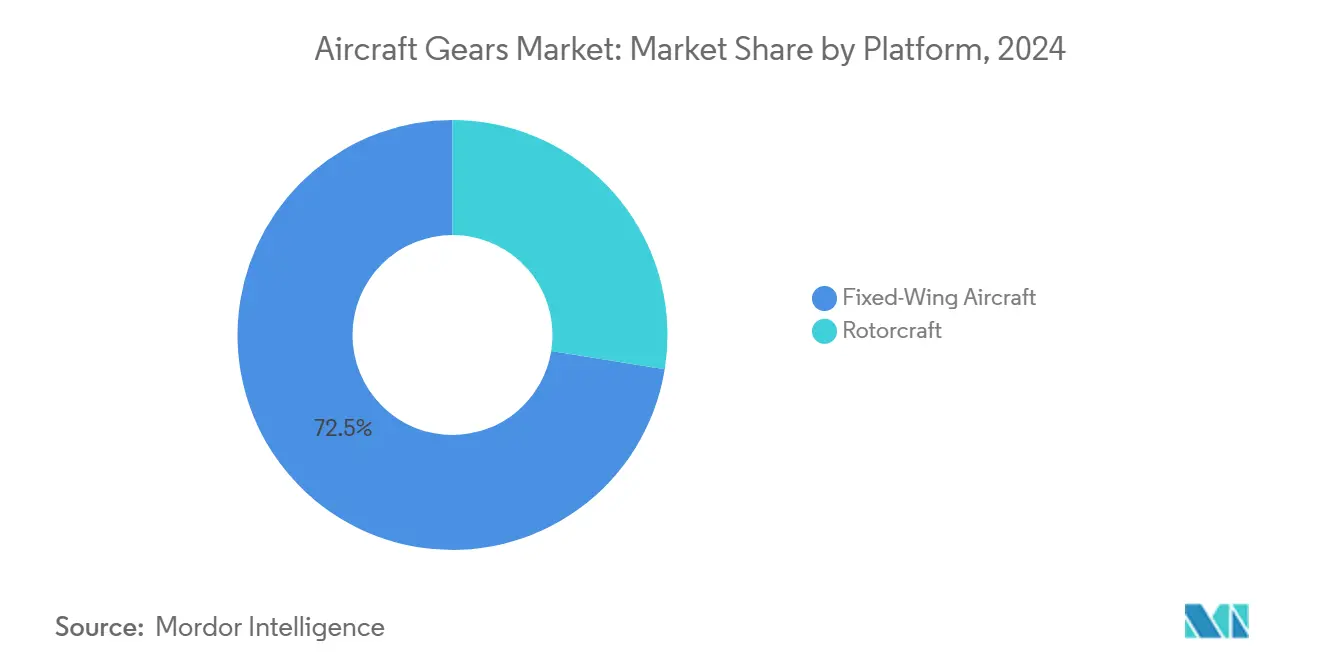

- By platform, fixed-wing aircraft commanded 72.45% of the aircraft gears market share in 2024, while military rotorcraft recorded the highest CAGR at 4.34% through 2030.

- By application, auxiliary power units led with 37.87% revenue share in 2024; actuators are projected to expand at a 4.62% CAGR to 2030.

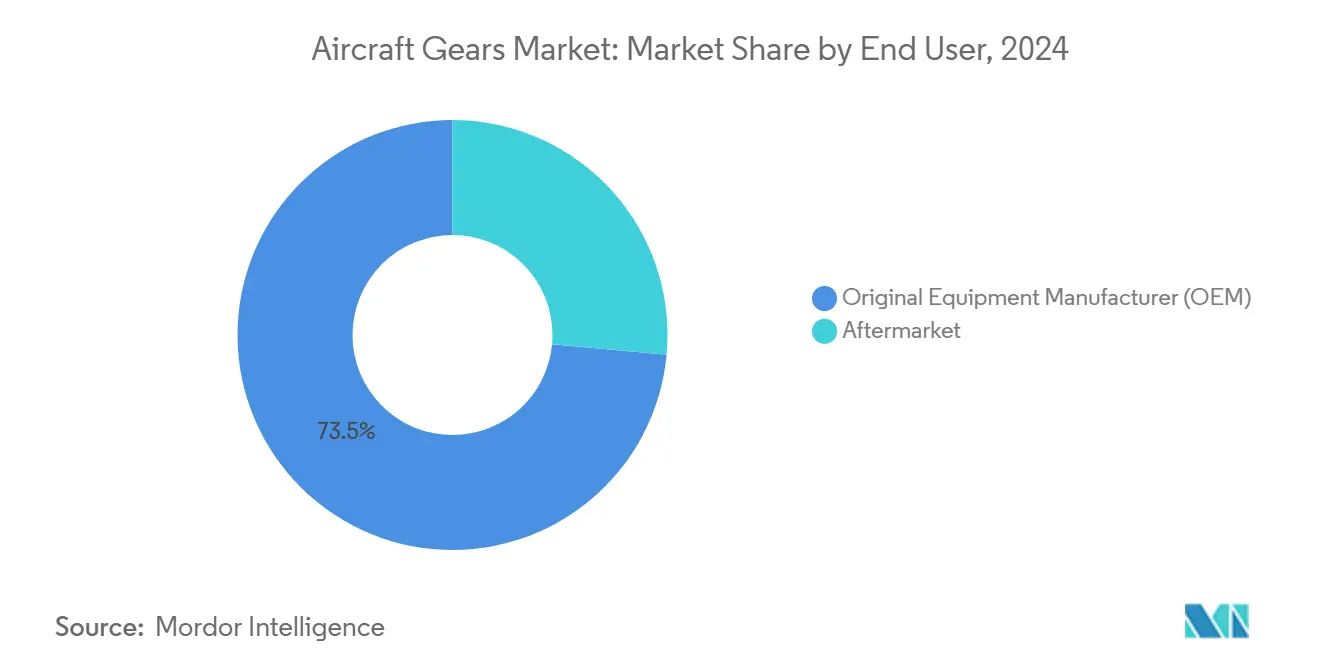

- By end user, the OEM channel held 73.54% of the aircraft gears market size in 2024, whereas the aftermarket is progressing at a 4.87% CAGR between 2025 and 2030.

- By gear type, spur gears accounted for a 31.95% share of the aircraft gears market in 2024, and helical gears are advancing at a 4.85% CAGR through 2030.

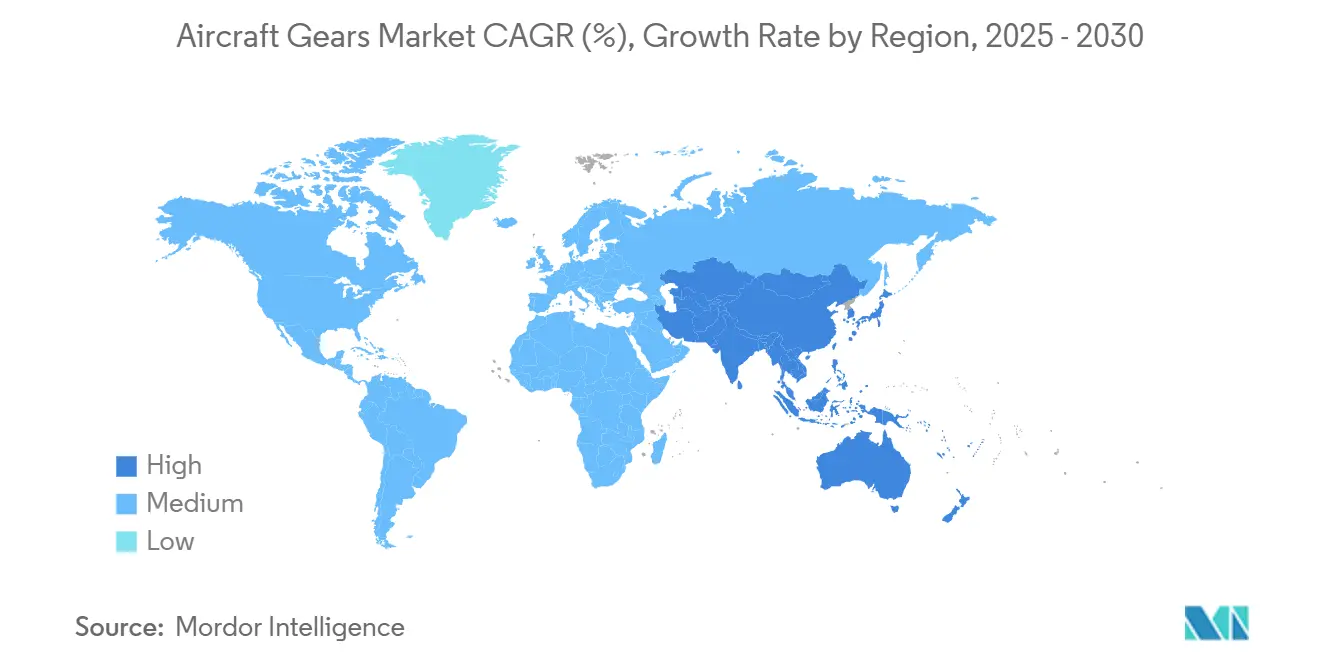

- By geography, Asia-Pacific captured 32.50% revenue share in 2024 and is tracking the fastest regional CAGR at 5.20% during the forecast window.

Global Aircraft Gears Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of geared-turbofan (GTF) engines | +0.8% | North America and Europe | Medium term (2-4 years) |

| Rising commercial aircraft deliveries and fleet renewals | +0.7% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Surge in military rotorcraft modernization programs | +0.5% | North America, Europe, APAC | Long term (≥ 4 years) |

| Shift toward lightweight, carburized, and vacuum-carburized gear materials | +0.4% | Global | Medium term (2-4 years) |

| Digital-twin based predictive maintenance for gearboxes | +0.3% | Developed markets | Long term (≥ 4 years) |

| Accelerated investment in composite-hybrid bull gears for weight savings | +0.2% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adoption of Geared-Turbofan Engines

Geared-turbofan powerplants reshape tolerance, wear and thermal-cycle requirements for reduction gears, as demonstrated by Pratt & Whitney’s PW1100G-JM architecture that uses an 18:1 gear ratio to decouple fan and low-pressure turbine speeds Although early service disruptions spurred remedial retrofit campaigns, the platform’s 15-20% fuel-burn benefit maintains airline interest and underpins multi-year backlogs, ensuring steady visibility for qualified gear suppliers able to process carburized steels with high case-depth consistency.[3]Source: Clean Aviation, “Electrical Landing Gear,” clean-aviation.eu Sub-tier vendors with vacuum carburizing lines and in-house hard-finishing capabilities enjoy elevated switching costs that protect margins when OEMs renegotiate pricing. Updated AS9110 and AS9120 revisions tighten traceability for repair stations and distributors, pushing less-sophisticated shops out of the certification funnel and further consolidating demand. The net result is a favorable demand outlook for precision bull, sun, and ring gears tailored to GTF kinematics, particularly across the A320neo and Embraer E2 families slated for 2030 deliveries.

Rising Commercial Aircraft Deliveries and Fleet Renewals

Narrowbody production has returned to pre-pandemic run-rates, with Airbus guiding for 75 A320-family frames per month by 2026 and Boeing ramping the B737 MAX toward 55 units monthly, thereby amplifying content opportunities across APU, actuator, and compressor gear assemblies. Airlines capitalizing on favorable fuel economics retire older fleets earlier than planned, compelling OEMs to pressure suppliers for dual-source capabilities to safeguard schedules. Component shortages in A321 engines and A330 landing gear assemblies emphasize the premium carriers' place on vendors that can guarantee shipment slots under long-term agreements. Because gear manufacturers face 18-24 month qualification cycles, incumbents with proven statistical process control are in a strong negotiating posture, capturing incremental value even as airframers squeeze tier-one margins. Certifications such as NADCAP for heat treating remain decisive differentiators in contract awards.

Surge in Military Rotorcraft Modernization Programs

Budget allocations for Future Long Range Assault Aircraft (FLRAA), Apache “E-model” upgrades, and UH-60V avionics retrofits translate to a steady stream of transmission, main-rotor, and tail-rotor gear orders, each requiring elevated fatigue limits and improved micro-pitting resistance. Unlike high-volume commercial gears, military gearbox orders deliver healthy unit prices and attract specialized materials, including Ferrium C64, whose cost premiums are acceptable within defense cost per flight hour thresholds. International customers such as Australia and South Korea request local work-share, compelling Western suppliers to explore joint ventures or licensed production, expanding geographic footprint while mitigating export-control constraints. Because program timelines extend beyond 2040, vendors secure a durable backlog that buffers civil-aviation demand swings, although lengthy security-clearance processes can delay facility expansions.

Shift Toward Lightweight, Carburized and Vacuum-Carburized Gear Materials

Weight-sensitive aircraft programs specify vacuum-carburized alloys that achieve up to 20% mass savings without sacrificing bending fatigue strength, enabling airlines to shave fuel burn by several basis points per cycle. Process repeatability hinges on precise furnace pressure control and rapid quenching systems, requiring multi-million-dollar investments that discourage new entrants. Suppliers owning advanced metallurgy laboratories accelerate R&D on carbonitriding profiles to boost core hardness and case uniformity further. The knowledge spillover into helical and bevel designs supports quieter operation, a priority for next-generation urban-air-mobility craft. As landing gear OEMs migrate to hybrid steel-composite housings, gear makers that co-engineer mating surfaces lock in design wins for future derivative models.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity of precision carburizing and super-finishing lines | -0.6% | Global manufacturing centers | Medium term (2-4 years) |

| Turbine gearbox reliability issues causing groundings (e.g., PW1100G) | -0.4% | GTF-equipped fleets | Short term (≤ 2 years) |

| Volatility in aerospace-grade alloy and titanium supply chains | -0.5% | China-dependent chains | Short term (≤ 2 years) |

| Skills shortage in high-precision gear manufacturing | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity of Precision Carburizing and Super-Finishing Lines

State-of-the-art vacuum carburizing cells capable of treating gears up to 620 mm diameter exceed USD 5 million per line when factoring in dry furnaces, manipulators, and auxiliary gas panels. Add USD 1-3 million for dual-flank grinding and isotropic super-finishing centers needed to achieve 0.3 µm surface roughness targets, and only a handful of mid-tier suppliers can secure financing. Payback periods stretch beyond seven years unless order books remain fully loaded, discouraging capacity additions that could ease delivery pressures. As airframers demand dual sourcing to hedge geopolitical risk, the shortage of capitalized suppliers becomes a structural bottleneck.

Turbine Gearbox Reliability Issues Causing Groundings

Groundings stemming from PW1100G planetary-carrier distress illustrate the cascading financial impact of gearbox failures: airlines lost revenue while OEMs funded unscheduled removals, and gear vendors faced expedited rebuilds under punitive turnaround-time clauses. Each incident dents confidence in geared architectures, pushing a subset of carriers to favor conventional engines, thereby tempering short-term order flow. Insurance premiums climb for component pools covering these fleets, and suppliers absorb higher warranty reserves, squeezing gross margins until field fixes stabilize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Fixed-Wing Dominance Amid Rotorcraft Acceleration

Fixed-wing programs generated 72.45% of the aircraft gears market size in 2024, anchored by heavy A320neo and B737 MAX deliveries that pack multiple gear sets into APUs, flap drive, and environmental-control subsystems. Each narrow-body typically contains over 200 precision gears, ensuring that even moderate production tempo sustains volume throughput at specialized grinding cells. Wide-body models add higher-torque bevel gears and planetary sets for extensive hydraulic pumps, thereby lifting dollar content per unit. Government transport programs such as the KC-46 tanker and A400M airlifter provide supplementary demand layers, shielding suppliers from single-platform dependence.

Rotorcraft orders expand at a 4.34% CAGR, reflecting escalating defense budgets and civil helicopter fleet requirements for emergency medical services in Asia-Pacific. Military upgrade kits for Apache, Osprey, and Black Hawk platforms include high-hardness spiral-bevel gear replacements designed for 3,000-hour overhaul intervals. Civil operators, particularly offshore wind farm service providers, demand low-noise main-rotor gearboxes that meet stringent vibration ceilings, pushing helical tooth micro-geometry innovation. The combination of premium pricing and long depot cycles positions rotorcraft gears as a strategic profit center for shops willing to navigate rigorous ITAR compliance.

By Application: APU Systems Lead Critical Power Applications

APU assemblies accounted for 37.87% of 2024 revenue, demonstrating their high replacement value when maintenance events run USD 400,000 per shop visit and each unit houses sun, ring, and planetary gears running at 40,000 rpm. Airlines equate APU reliability with gate turnaround efficiency, prompting them to favor suppliers offering case-carburized gearsets polished to Ra ≤ 0.2 µm, extending mean time between overhauls. The transition toward SAF-ready units further revalidates gear designs to handle altered combustion by-products, creating an engineering-change backlog.

Actuators, forecasted to grow 4.62% annually, ride the electrification wave as electro-hydrostatic units integrate compact geartrains mated to brushless DC motors. Nose and primary landing-gear actuators adopt duplex helical stages aimed at halving weight relative to hydraulic counterparts, while spoiler and slat devices privilege planetary epicyclic layouts for redundancy. This shift opens design windows for vendors capable of tight coaxiality control across stacked gear carriers in additive-machined housings, an emerging differentiation lever.

By End User: OEM Dominance with Aftermarket Momentum

Original-equipment contracts represented 73.54% of the aircraft gears market share in 2024 because airframers lock multi-year agreements that guarantee production slots in return for price concessions. Airbus’s Approved Supplier List Vendors enforce statistical capability indices (CpK ≥ 1.33) across heat treatment lots, driving sustained capital improvement cycles. Lockheed Martin and Boeing employ similar vendor surveillance, so incumbency provides tangible moat effects.

Aftermarket value, posting a 4.87% CAGR, hinges on mature fleets whose gearboxes reach overhaul thresholds every 5-7 years. MRO organizations like Lufthansa Technik leverage DER-approved repairs that blend OEM drawings with proprietary inspection criteria, reducing unit cost versus new manufacture. Independent distributors stock standard spur and bevel replacements for legacy types such as the MD-80, fueling transactional volume below USD 10,000 per gear but aggregating into meaningful segment revenue.

By Gear Type: Spur Gears Lead with Helical Growth

Spur geometries captured 31.95% of the aircraft gears market share in 2024, owing to straightforward cutting operations and high load-bearing capability at moderate speeds. AGMA Q8-plus tolerances suffice for many actuator and pump roles, enabling batch production on CNC hobbing centers with quick fixture swaps. For APU sun gears, surface carburizing to 0.6 mm case depth and tooth grinding to 0.005 mm flank tolerance satisfy cyclic thermal stress requirements, maintaining robust margins.

Helical designs are forecasted to expand 4.85% through 2030, mitigating vibration and flank-to-flank impact at the higher peripheral speeds seen in geared-fan and rotorcraft gearboxes. Suppliers equipped with five-axis grinding machines achieve controlled lead modifications that distribute load across the face width, dampening signature noise audible inside modern quiet cabins. Bevel gears remain indispensable for helicopter main-rotor drive paths, while rack-and-pinion pairs underpin several slide-rail actuators in cargo doors and thrust reversers. Additionally, specialized planetary configurations form the heart of electric taxiing systems under evaluation by European OEMs.

Geography Analysis

Asia-Pacific generated 32.50% of 2024 sales and is tracking a 5.20% CAGR, underscoring the region’s dual role as a manufacturing hub and demand center. India’s tier-two suppliers, benefiting from Make-in-India policies, secure gearbox machining packages for the A320neo and GTF variants, leveraging lower labor costs blended with increasingly automated cells. Chinese joint-ventures address C919 and ARJ21 domestic programs, yet stringent IP protection oversight keeps critical gear design concentrated among Western licensors.

North America remains a cornerstone due to entrenched defense procurement and significant civil backlogs managed out of Seattle and Mobile. US suppliers focus on high-value and spiral bevel sets for rotorcraft, and many run vertically integrated metallurgical labs to retain ITAR-controlled processes internally. Skilled-labor shortages, however, inflate wage structures and spur selective relocation to Mexico for secondary operations. Canada’s niche players emphasize spur and helical gears for regional jets and business aircraft.

Europe’s ecosystem clusters around Toulouse, Hamburg, and Derby, which provide ring gears, drive shafts, and actuation gearboxes to Airbus and Rolls-Royce programs. Brexit customs frictions encourage dual-sourcing within continental plants, leading to capacity transfers to Spain and Poland. The Middle East witnesses budding offset programs tied to Gulf carriers' fleet purchases, emphasizing assembly rather than raw gear manufacture. South America’s presence remains modest, dominated by support for Embraer jets and helicopter MRO operations in Brazil and Argentina.

Competitive Landscape

The aircraft gears market hosts a blend of diversified aerospace groups and specialist machinists. Warburg Pincus/Berkshire Partners’ USD 3 billion acquisition of Triumph Group’s geared solutions division exemplifies private-equity confidence in steady cash flows stemming from proprietary process capability. Arrow Gear, Precipart, and BMT Aerospace concentrate on high-precision helical and bevel units under long-term agreements, often supplying multiple integrators to dilute platform risk.

Technology leadership revolves around advanced heat treatment, tooth topography modeling, and on-machine inspection systems that shorten first-article acceptance cycles. Digital twin offerings bundle sensor packages with predictive analytics to unlock service-based revenue streams, a strategy gaining traction among gear makers courting airline power-by-the-hour contracts. Composite hybrid gear R&D differentiates early adopters who partner with academia to file patents on carbon-wrap retention methods.

Emerging entrants from the automotive forge sector, notably Motherson and Mubea, leverage scale in cold-forming to backfill supply gaps for lower-complexity spur and rack sets. Still, AS9100 certifications, NADCAP approvals, and extended PPAP timelines insulate aerospace incumbents from abrupt displacement. Consolidation proceeds selectively, exemplified by AGMA’s merger with ABMA to form Motion and Power Manufacturers Alliance, signalling increased lobbying coordination among power-transmission firms.

Aircraft Gears Industry Leaders

Batom Co., Ltd.

Arrow Gear LLC

Precipart Group Ltd.

Gear Motions, Inc.

Gibbs Gears Precision Engineers Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Indian Ministry of Defence (MoD) contracted Hindustan Aeronautics Limited (HAL) to supply 156 Light Combat Helicopters (LCH) Prachand, with 66 units for the Air Force and 90 for the Army. The deliveries will span five years, starting from the third year. This procurement represents a significant shift toward indigenous defense manufacturing, with over 65% local content planned. Developing high-altitude combat capabilities through domestic production indicates India's growing self-reliance in defense equipment, potentially expanding the market for local manufacturers and suppliers.

- February 2025: Warburg Pincus and Berkshire Partners agreed to acquire TRIUMPH Group, Inc. through a newly formed entity. The USD 3 billion transaction will convert TRIUMPH into a privately held company under the joint control of both private equity firms. This strategic acquisition aims to accelerate TRIUMPH's market expansion and operational capabilities in the aerospace sector.

Global Aircraft Gears Market Report Scope

| Fixed-Wing Aircraft | Commercial Aviation | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Military Aviation | Fighter Jets | |

| Transport Aircraft | ||

| Special Mission Aircraft | ||

| Others | ||

| General Aviation | Business Jets | |

| Piston and Turbo Aircraft | ||

| Rotorcraft | Civil Helicopters | |

| Military Helicopters | ||

| Auxiliary Power Units |

| Actuators |

| Pumps |

| Air Conditioning Compressors |

| Other Applications |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| Spur Gear |

| Bevel Gear |

| Helical Gear |

| Rack and Pinion gear |

| Other Gears |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Fixed-Wing Aircraft | Commercial Aviation | Narrowbody |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Fighter Jets | ||

| Transport Aircraft | |||

| Special Mission Aircraft | |||

| Others | |||

| General Aviation | Business Jets | ||

| Piston and Turbo Aircraft | |||

| Rotorcraft | Civil Helicopters | ||

| Military Helicopters | |||

| By Application | Auxiliary Power Units | ||

| Actuators | |||

| Pumps | |||

| Air Conditioning Compressors | |||

| Other Applications | |||

| By End User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Gear Type | Spur Gear | ||

| Bevel Gear | |||

| Helical Gear | |||

| Rack and Pinion gear | |||

| Other Gears | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What CAGR is forecast for the Aircraft gears market between 2025 and 2030?

The market is projected to grow at a 4.03% CAGR, rising from USD 347.95 million in 2025 to USD 423.91 million in 2030.

Which platform segment contributes the most revenue?

Fixed-wing aircraft dominate with 72.45% market share in 2024 due to sustained narrowbody production.

Why are APUs a key application for gear suppliers?

APUs demand high-precision, high-speed gears, and each overhaul can cost USD 400,000, driving strong, recurring component demand.

Which region is expanding the quickest?

Asia-Pacific leads growth with a 5.20% CAGR, buoyed by India’s and China’s expanding aerospace manufacturing ecosystems.

How will digital-twin technology influence aftermarket sales?

Predictive analytics reduce unplanned gearbox removals, fostering service-based revenue models and strengthening supplier–operator partnerships.

What obstacles restrict new entrants in this field?

High capital equipment costs, rigorous AS9100 certifications and advanced heat-treatment expertise create formidable entry barriers for newcomers.

Page last updated on: