Aircraft Wires And Cables Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.86 Billion |

| Market Size (2030) | USD 3.89 Billion |

| Growth Rate (2025 - 2030) | 6.34% CAGR |

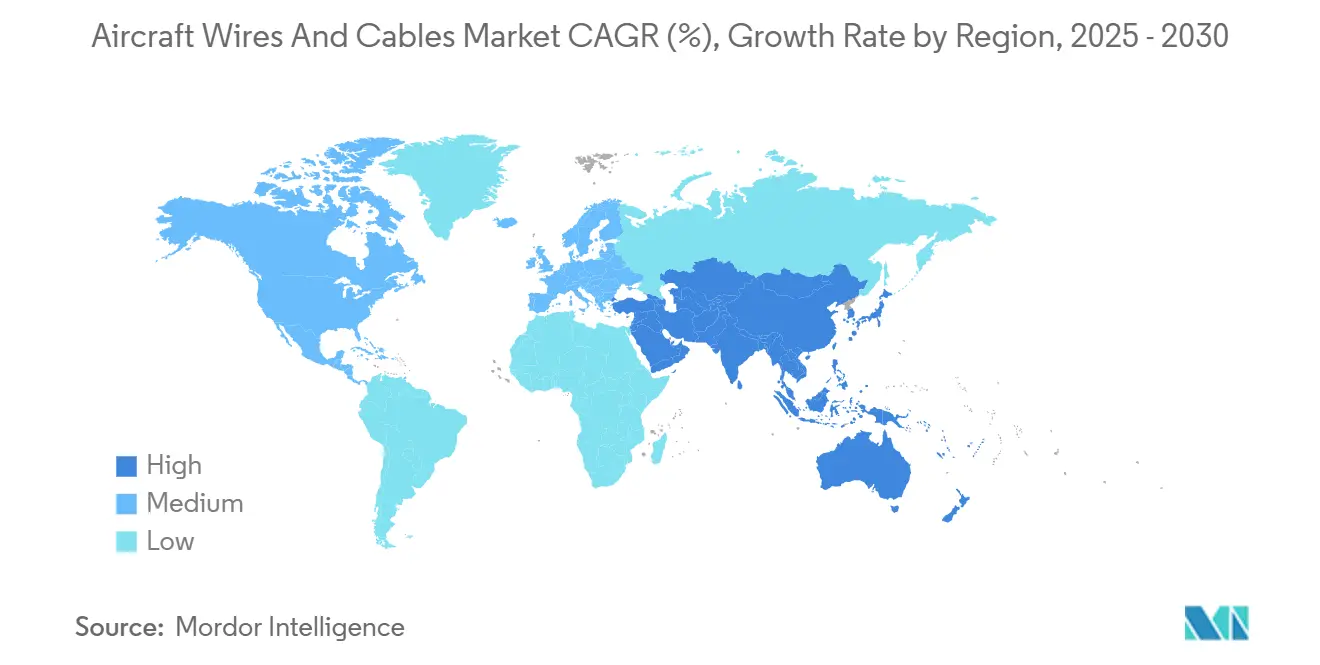

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

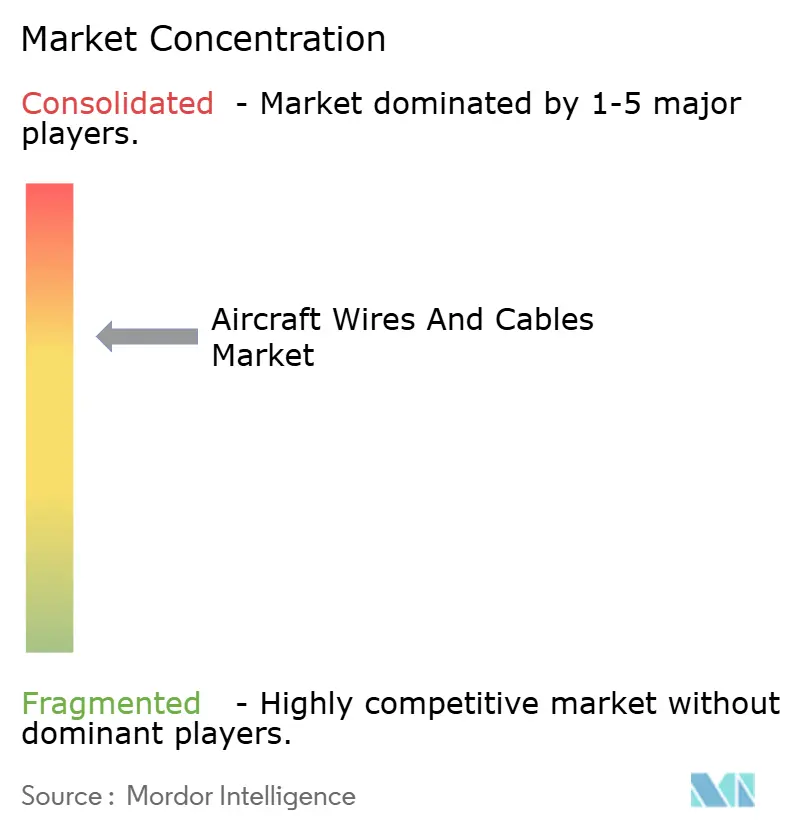

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Wires And Cables Market Analysis by Mordor Intelligence

The aircraft wires and cables market size is estimated at USD 2.86 billion in 2025 and is projected to reach USD 3.89 billion by 2030, growing at a CAGR of 6.34%. The rebound of air-travel demand, the push toward more-electric aircraft, and a widening pipeline of eVTOL prototypes are accelerating demand for sophisticated electrical interconnects. Single-aisle production backlogs at Boeing and Airbus have stretched to eight-plus years of output, locking in forward demand for wiring content and giving established suppliers pricing leverage. Mandatory electric-wire-interconnect-system (EWIS) retrofit programs on aircraft older than 14 years are expanding the aftermarket opportunity pool, while the shift to lightweight aluminium conductors is mitigating copper price volatility and helping airlines cut operating weight. Regionally, North America maintains its lead through substantial defense budgets, whereas the Asia-Pacific region races ahead as the fastest-growing geography, fueled by record fleet expansion in China and India.

Key Report Takeaways

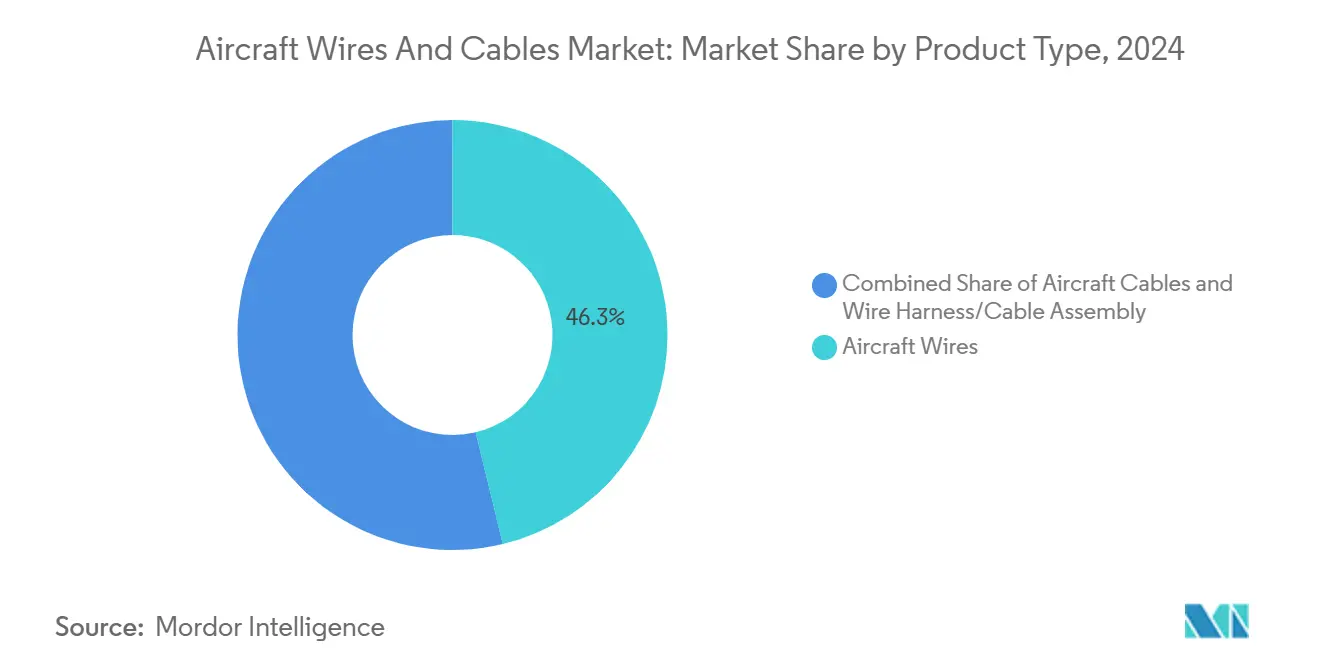

- By product type, aircraft wires held 46.25% of the aircraft wires and cables market share in 2024; aircraft cables are poised to grow at a 7.35% CAGR to 2030.

- By application, power distribution accounted for 36.56% of the aircraft wires and cables market size in 2024, while the data and communication segment is advancing at a 7.57% CAGR through 2030.

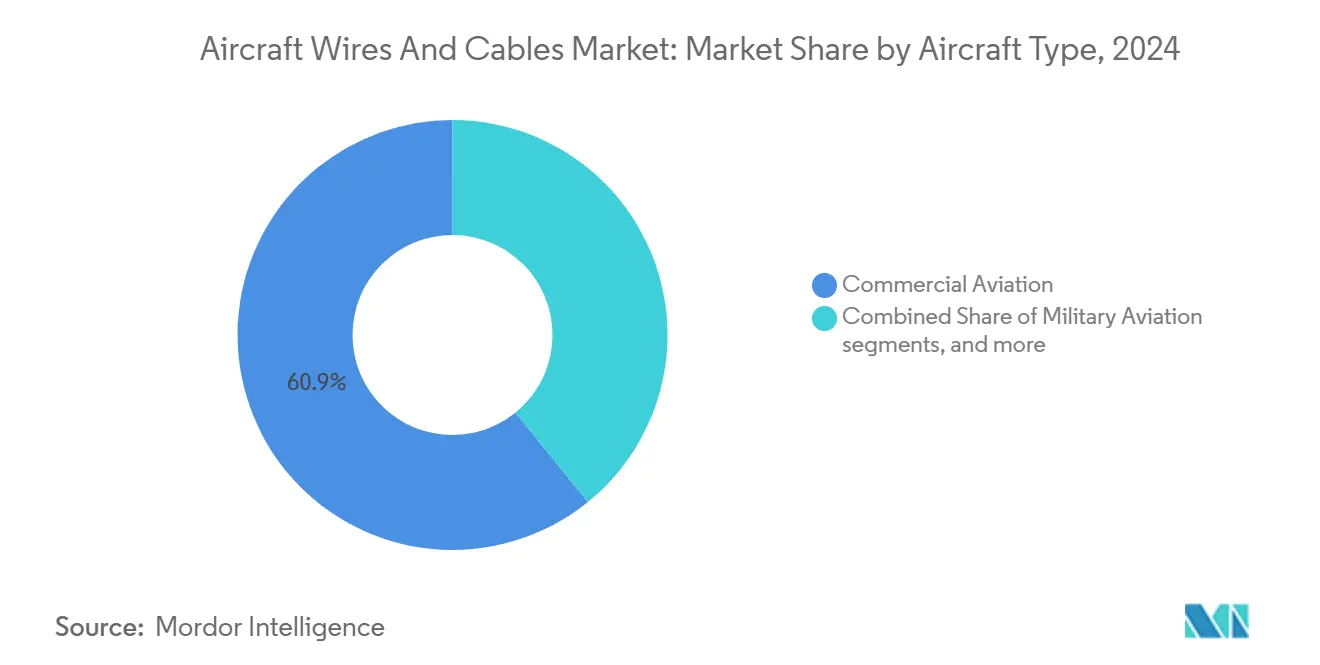

- By aircraft type, commercial aviation platforms commanded a 60.85% share in 2024, whereas the emerging platforms segment is projected to expand at a 9.15% CAGR between 2025 and 2030.

- By fit, line-fit (OEM) installations dominated with a 74.65% share in 2024; retrofit/aftermarket will post the fastest growth at a 7.68% CAGR through 2030.

- By geography, North America led with a 39.75% share in 2024, while Asia-Pacific is set to record the highest 6.55% CAGR to 2030.

Global Aircraft Wires And Cables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in single-aisle aircraft production backlog | +1.20% | North America and Asia-Pacific | Medium term (2-4 years) |

| Mandatory electric wire interconnect system retrofit programs for aging fleets | +0.80% | North America and Europe | Short term (≤ 2 years) |

| Lightweight conductor shift to cut fuel-burn | +0.60% | Global | Long term (≥ 4 years) |

| High-speed inflight entertainment and connectivity (IFEC) driving fiber-optic demand | +0.90% | Global, led by premium carriers in North America and Europe | Medium term (2-4 years) |

| High-voltage architectures for more-electric aircraft | +0.70% | Europe and North America | Long term (≥ 4 years) |

| eVTOL prototypes requiring thermal-robust harnesses | +0.40% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Single-Aisle Aircraft Production Backlog

Boeing’s B737 backlog of 4,296 units and Airbus’s A320 family order book above 20,000 units effectively lock in eight to ten years of narrowbody production, sustaining baseline demand for the aircraft wires and cables market.[1]FlightGlobal Staff, “Boeing Accelerated 737 Deliveries in January Following Tumultuous 2024,” flightglobal.com Supply-chain resilience has overtaken cost-cutting as an OEM priority, enabling tier-one wiring suppliers to negotiate longer-term, value-based contracts. Installation capacity, not component availability, now constrains deliveries, with labor shortages for certified EWIS technicians delaying completions. These bottlenecks favor suppliers that can provide kitted, ready-to-install harnesses requiring fewer touch-labor hours. Resultant schedule certainty is increasingly priced into aircraft-level contracts, lifting average selling prices for wiring sets.

Mandatory Electric Wire Interconnect System Retrofit Programs for Aging Fleets

The FAA’s Enhanced Airworthiness Program enforces EWIS maintenance on transport aircraft built after 1958, making retrofit spending non-discretionary for operators.[2]Federal Aviation Administration, “AC 25.1701-1 – Certification of Electrical Wiring Interconnection Systems on Transport Category Airplanes,” faa.gov American Airlines’ 150-aircraft A320ceo upgrade underscores the scale of mandated work scopes, blending avionics, airframe, and wiring packages into single contracts. EASA’s AMC-20 harmonization exports similar rules to European fleets, aligning timelines and technical documentation across jurisdictions. Predictable retrofit windows let suppliers sequence production more efficiently than in the cyclical OEM channel. Training revenue for EWIS inspection and maintenance further complements hardware sales, turning service capability into a margin buffer.

Lightweight Conductor Shift to Cut Fuel-Burn

Prysmian achieved 30% weight savings on Airbus A380 wiring by swapping copper for aluminium conductors, demonstrating the real-world viability of lighter metallurgy.[3]Prysmian Group, “30% Weight Saving with Aluminium Wires,” prysmiangroup.com Advance RF coaxial products from PIC Wire and Cable cut weight by up to 81% while preserving shielding integrity, a critical parameter for safety-of-flight systems. Copper hit USD 5.20 per lb in May 2024 and is projected to remain supply-constrained this decade, making aluminium-based designs attractive hedges against raw-material risk. Next-gen Si-Mg-Al alloys now close conductivity gaps enough to satisfy high-load circuits, ensuring the shift is structural, not cyclical.

High-Speed Inflight Entertainment and Connectivity (IFEC) Driving Fiber-Optic Demand

Airline satisfaction surveys show 83% of passengers pick carriers with better onboard Wi-Fi, turning connectivity into a revenue lever rather than a cost line. Gore’s ARINC-compliant fiber-optic cables deliver data rates above 100 Gbps, weighing only 4.2 kg per km, versus 41 kg for equivalent copper ethernet bundles. The fiber’s immunity to electromagnetic interference reduces shielding needs and simplifies routing in crowded fuselages. With streaming services and predictive-maintenance feeds battling for bandwidth, OEMs have begun to specify fiber backbones even on short-haul aircraft, accelerating volume growth of the aircraft wires and cables market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expensive electric wire interconnect system (EWIS) certification and qualification cycles | −0.5% | North America and Europe | Short term (≤ 2 years) |

| Copper and aluminium price volatility | −0.3% | Global | Medium term (2-4 years) |

| Thermal-runaway risk in high voltage harness insulation | −0.2% | Global | Long term (≥ 4 years) |

| Limited skilled labor for novel wiring installation | −0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expensive Electric Wire Interconnect System Certification and Qualification Cycles

Aircraft wiring must clear far tougher safety gates than most industrial products, making new designs slow and costly. Each wire type faces environmental, electromagnetic-compatibility, and failure-mode tests that can push certification costs past USD 1 million and add up to five extra years to a development schedule. Operators must also map every cable run and prove it stays accessible for maintenance under the FAA’s Enhanced Zonal Analysis Procedure. This task favors suppliers with big documentation libraries already in place. Europe’s EASA has aligned its rules with the FAA, so companies cannot avoid the burden by certifying elsewhere; meeting both requirements can swallow 15-20% of a new product budget. The hurdle grows higher for novel materials such as advanced aluminium alloys or high-temperature polymers, because limited flight history forces engineers to carry out extra validation work. As a result, smaller or newer firms often struggle to break in, and even large players think twice before betting on radical wiring ideas.

Thermal-Runaway Risk in High-Voltage Harness Insulation

Shifting from the long-standing 28V systems to high-voltage power networks makes today’s insulation materials run hotter than they were ever designed to handle. Laboratory studies show that moisture, dirt, and rapid temperature swings can trigger “arc tracking,” where tiny electrical arcs burn through the plastic jacket, leading to thermal runaway or fire. The B787 already uses ±270 V DC lines, and future electric or hybrid aircraft could need kilovolt-class circuits, further stressing the insulation. Collins Aerospace and other suppliers are experimenting with new polymers and cooling layouts, yet they admit that thermal management remains one of the most complex barriers to megawatt-level propulsion. The problem reaches beyond raw materials; current cable spacing and routing rules were written for low-voltage systems and may not protect against higher energy levels. Unless the industry finds a reliable fix, airlines and regulators could limit how fast high-voltage designs enter everyday service.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fibre-Optic Cables Drive Innovation

Aircraft wires accounted for 46.25% of the aircraft wires and cables market size revenue in 2024, while aircraft cables, although smaller, are forecasted to grow at 7.35% CAGR, the fastest among all products.

The growth of fiber-based cables stems from aircraft digitalization: real-time analytics, 4K cabin streaming, and cloud-linked health monitoring require multi-gigabit links that copper cannot supply efficiently. Aluminium-core aircraft wire still anchors power circuits, yet OEM design teams increasingly pair it with photonic networks for data traffic. Wire harness/cable assembly retains complexity-driven pricing power because each harness is uniquely engineered, and the aircraft wires and cables market share for this sub-segment benefits from scarce integration skills.

Hook-up/single-core wire sustains retrofit demand because its drop-in nature eases line-maintenance swaps. Coaxial/RF cable is ceding high-frequency functions to fiber but endures in legacy radars and transponders. Mechanical/control cable stays niche, constrained to applications where electronic redundancy is harder to certify. Emerging single-mode variants dominate long-run backbone spines, whereas multi-mode offers cheaper short-haul inter-rack links, allowing suppliers to tier their portfolios.

By Application: Data Communication Accelerates Growth

Power distribution retained 36.56% of the aircraft wires and cables market size in 2024, reflecting its ubiquity across platforms. Data and communication, however, will clock 7.57% CAGR through 2030, outstripping every other application.

Digital cabin concepts, predictive maintenance hubs, and autonomous flight-control test beds swamp existing bandwidth headroom, turning aircraft into airborne data centres. Consequently, wiring weight budgets are shifting from copper-heavy power looms to lightweight fiber, improving overall fuel burn. Flight control and actuation keep steady momentum as fly-by-wire penetration rises in business jets and military UAVs. LED mood-lighting and smart-cabin systems lift wire counts per seat, while environmental and utility circuits gain sensors for condition-based monitoring. Landing gear subsystems remain a reliability-critical niche served by premium-priced, abrasion-resistant looms.

By Aircraft Type: eVTOL Disrupts Traditional Segments

Commercial aviation aircraft platforms commanded 60.85% of revenue in 2024 and thus anchor baseline volumes for the aircraft wires and cables market. Emerging platforms, though nascent, lead growth at 9.15% CAGR as urban-air-mobility (UAM) prototypes transition to certification.

Narrowbody dominance owes to relentless order books and their wiring-intensive avionics upgrades. Widebodies maintain lower-growth but high-value niches, especially in premium IFEC installations. Regional jets confront substitution risk from re-engined narrowbodies yet retain routes unsuitable for larger aircraft. Business jet OEMs incorporate high-voltage batteries for taxi-assist systems, nudging up wire counts per unit. Military variants need ruggedised looms that fetch higher margins. Rotorcraft wiring must withstand vibratory loads, spawning dedicated product lines. eVTOL architectures run on megawatt-class electric propulsion, elevating voltage and temperature ratings beyond conventional standards and opening greenfield specification slots for nimble suppliers.

By Fit: Retrofit Market Gains Momentum

Line-fit installations captured 74.65% of the aircraft wires and cables market revenue during 2024, reflecting OEM dominance, yet retrofit/aftermarket will expand at a 7.68% CAGR to 2030. Tight OEM schedules and delivery-slot scarcity motivate airlines to extend asset lives with cabin, avionics, and EWIS upgrades instead of ordering new frames. Retrofit work packages blend wiring, sensors, and connectivity hardware, raising average dollar-per-tail values compared with routine parts replacement. Aftermarket contracts also mitigate OEM cyclicality, giving suppliers backlog optionality. For line-fit, production tempo depends on labor availability; suppliers offering semi-finished, labelled, and tested harness kits reduce final-assembly takt times and face strong pull from airframers chasing rate ramps.

Geography Analysis

North America’s leadership rests on Boeing’s airframer hub, a deep tier-one ecosystem, and the USD 886 billion FY25 defence budget, which embeds sizeable wiring procurements for fighter and lift platforms.[4]Senate Armed Services Committee, “FY25 NDAA Bill Text,” senate.gov Canada contributes composite-wing and wiring sub-assemblies, while Mexico hosts cost-competitive harness production that feeds Boeing and Airbus lines. FAA regulations set global benchmarks, meaning innovations proven in US programs ripple worldwide, reinforcing the region’s standards influence.

Asia-Pacific’s 6.55% growth trajectory springs from a swelling middle-class traveller base; China alone intends to triple its fleet by 2043, necessitating high-throughput MRO hubs and billions in spare-parts stocking. India’s government-backed industrial corridors promise incentives for wiring-harness factories, offsetting currency-risk exposure for global suppliers. Japan and South Korea, with mature electronics sectors, are carving out high-value niches in fibre-optic connectors.

Europe offers relatively slow unit growth but remains a test-bed for sustainability-focused electrical systems. Airbus’s Toulouse-based research into 1.2 kV distribution requires next-gen insulation solutions, presenting an early-mover advantage to local suppliers. The UK, Germany, and France host dense aerospace clusters that speed design cycles, while EASA alignment with the FAA simplifies cross-market product approvals.

South America and the Middle East and Africa represent less than 8% of 2024 revenue but post above-average retrofit demand as carriers modernise avionics and cabins rather than buy new jets. Local content rules and customs complexity favour suppliers willing to partner with regional MROs for stocking and field-engineering support.

Competitive Landscape

The aircraft wires and cables market remains moderately consolidated. TE Connectivity Corporation (TE Connectivity plc), Amphenol Corporation, Safran Electrical & Power (Safran), and Collins Aerospace (RTX Corporation) hold over half of 2024 revenue, benefitting from long-term supply agreements and broad product breadth. Amphenol’s USD 2.025 billion takeover of Carlisle Interconnect Technologies added USD 900 million in sales and lifted its harsh-environment offering. Safran renewed multi-year contracts with Boeing for B737 MAX and B777-X wiring, entrenching its OEM channel.

White-space opportunities cluster around eVTOL and high-voltage harnesses, where no incumbent commands scale. Collins Aerospace’s prototypes for the EU SWITCH project signal an R&D race to secure first-mover pricing premiums. PIC Wire and Cable leverages materials innovation, posting 81% weight savings that resonate with fuel-burn reduction targets. Niche specialists like SASMOS HET align with emergent OEMs such as Deutsche Aircraft, proving that agile partnerships can bypass incumbent inertia.

Competitive intensity rises as raw-material inflation pressures margins. Suppliers owning both aluminium- and copper-based portfolios hedge input swings better than mono-metal peers. Service capabilities—kitting, installation training, and AOG support—are differentiators when hardware specs commoditise. Digital twins of harness routings, now offered by several vendors, shorten installation learning curves and lock customers into software ecosystems.

Aircraft Wires And Cables Industry Leaders

Amphenol Corporation

Safran Electrical & Power (Safran Group)

TE Connectivity Corporation (TE Connectivity plc)

GKN Aerospace (Melrose Industries PLC)

LATECOERE S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Molex announced the signing of an agreement to purchase AirBorn, Inc.. This company specializes in designing and manufacturing rugged connectors and electronic components for global OEMs serving the aerospace and defense, commercial air, space exploration, medical, and industrial markets.

- July 2024: GKN Aerospace announced an extension of its agreement with Airbus, ensuring the continued production of electrical wiring interconnection systems (EWIS) for the A220 aircraft. This multi-year contract solidifies GKN Aerospace's position as a primary EWIS supplier for Airbus.

- April 2024: Safran Electrical & Power launched GENeUSCONNECT, a new series of high-power electrical harnesses. This addition completes the company's range of electrical systems designed for the newest all-electric and hybrid aircraft generations.

- February 2024: Malaysia Airlines Berhad (MAB) entrusted Safran Electrical & Power with a three-year exclusive service contract to maintain the electrical harnesses for MAB's CFM56-7B engines.

Global Aircraft Wires And Cables Market Report Scope

| Aircraft Wires | Hook-Up/Single-Core Wire | |

| Coaxial/RF Cable | ||

| Aircraft Cables | Mechanical/Control Cable | |

| Fiber-Optic Cable | Single-Mode Fiber | |

| Multi-Mode Fiber | ||

| Wire Harness/Cable Assembly | ||

| Power Distribution |

| Data and Communication |

| Flight Control and Actuation |

| Lighting and Cabin Systems |

| Environmental and Utility Systems |

| Landing Gear and Braking |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat Aircraft |

| Non-Combat Aircraft | |

| Unmanned Aerial Vehicles (UAVs) | |

| General Aviation | Business Jets |

| Piston and Turboprop Aircraft | |

| Rotorcraft | Civil Helicopters |

| Military Helicopters | |

| Emerging Platforms | eVTOL/Urban Air Mobility |

| Commercial Drones |

| Line-Fit (OEM) |

| Retrofit/Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| Product Type | Aircraft Wires | Hook-Up/Single-Core Wire | |

| Coaxial/RF Cable | |||

| Aircraft Cables | Mechanical/Control Cable | ||

| Fiber-Optic Cable | Single-Mode Fiber | ||

| Multi-Mode Fiber | |||

| Wire Harness/Cable Assembly | |||

| Application | Power Distribution | ||

| Data and Communication | |||

| Flight Control and Actuation | |||

| Lighting and Cabin Systems | |||

| Environmental and Utility Systems | |||

| Landing Gear and Braking | |||

| Aircraft Type | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat Aircraft | ||

| Non-Combat Aircraft | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| General Aviation | Business Jets | ||

| Piston and Turboprop Aircraft | |||

| Rotorcraft | Civil Helicopters | ||

| Military Helicopters | |||

| Emerging Platforms | eVTOL/Urban Air Mobility | ||

| Commercial Drones | |||

| Fit | Line-Fit (OEM) | ||

| Retrofit/Aftermarket | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft wires and cables market in 2025?

The aircraft wires and cables market size is estimated at USD 2.86 billion in 2025 and is projected to reach USD 3.89 billion by 2030, reflecting a 6.34% CAGR.

Which product class grows fastest through 2030?

Aircraft cables are forecasted to rise at 7.35% CAGR, the highest among all product types.

Why is Asia-Pacific the quickest-growing region?

Fleet expansion in China and India plus a push for local aerospace manufacturing drive a 6.55% CAGR to 2030.

What makes retrofit demand attractive for suppliers?

Regulatory EWIS mandates and airline cabin upgrades lift retrofit spending, giving the segment a 7.68% CAGR outlook.

How are raw-material trends shaping conductor choices?

Copper price volatility and weight-saving goals are accelerating a structural shift toward aluminium conductors.

Which new aircraft category offers the highest growth upside?

EVTOL platforms are expected to post a 9.15% CAGR as certification pathways clear and UAM services scale.

Page last updated on: