Commercial Aircraft Landing Gear Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

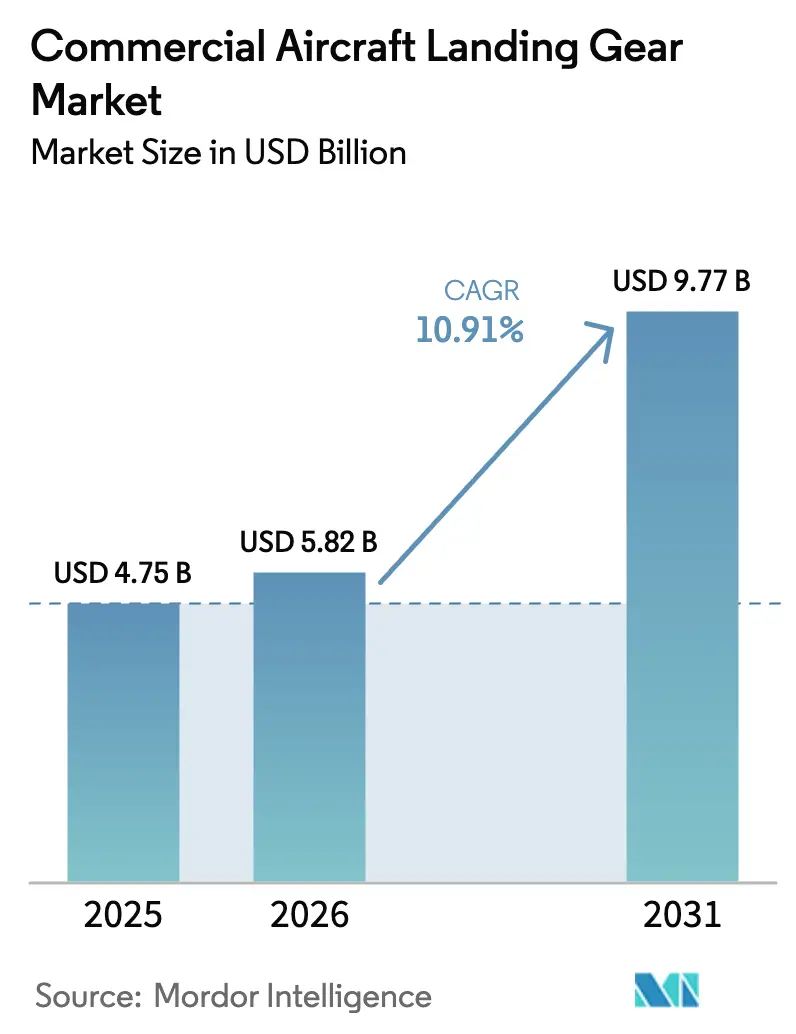

| Market Size (2026) | USD 5.82 Billion |

| Market Size (2031) | USD 9.77 Billion |

| Growth Rate (2026 - 2031) | 10.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | South America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Landing Gear Market Analysis by Mordor Intelligence

The commercial aircraft landing gear market size is expected to grow from USD 4.75 billion in 2025 to USD 5.82 billion in 2026 and is forecasted to reach USD 9.77 billion by 2031 at a 10.91% CAGR over 2026-2031. Airlines are rapidly replacing their aging fleets with fuel-efficient models, while original equipment manufacturers (OEMs) are integrating lighter composite structures and electric actuation to reduce fuel burn and simplify maintenance. Rapid single-aisle ramp-ups underpin demand, as Airbus targets 75 A320neo deliveries per month by 2026 and Boeing plans to deliver 38 B737 MAX units monthly, despite ongoing quality audits.[1]Source: Airbus S.A.S., “Orders and Deliveries,” Airbus.com Main landing-gear assemblies continue to command premiums as they combine high-load structures, carbon brakes, and electric actuators that together cut weight by more than 300 kilograms per aircraft. Aftermarket revenues accelerate a few years behind OEM shipments; airlines extend the service life of B737NG and A320ceo jets with carbon-brake retrofits and health-monitoring sensors, stimulating independent maintenance, repair, and overhaul (MRO) opportunities even as power-by-the-hour (PBH) contracts allow OEMs to capture lifecycle value. Headline risks center on titanium and carbon-fiber shortages that inflate material costs; however, suppliers mitigate exposure through vertical integration and additive manufacturing, as evidenced by Safran’s 50% weight reduction in hydraulic manifolds produced via selective laser melting.

Key Report Takeaways

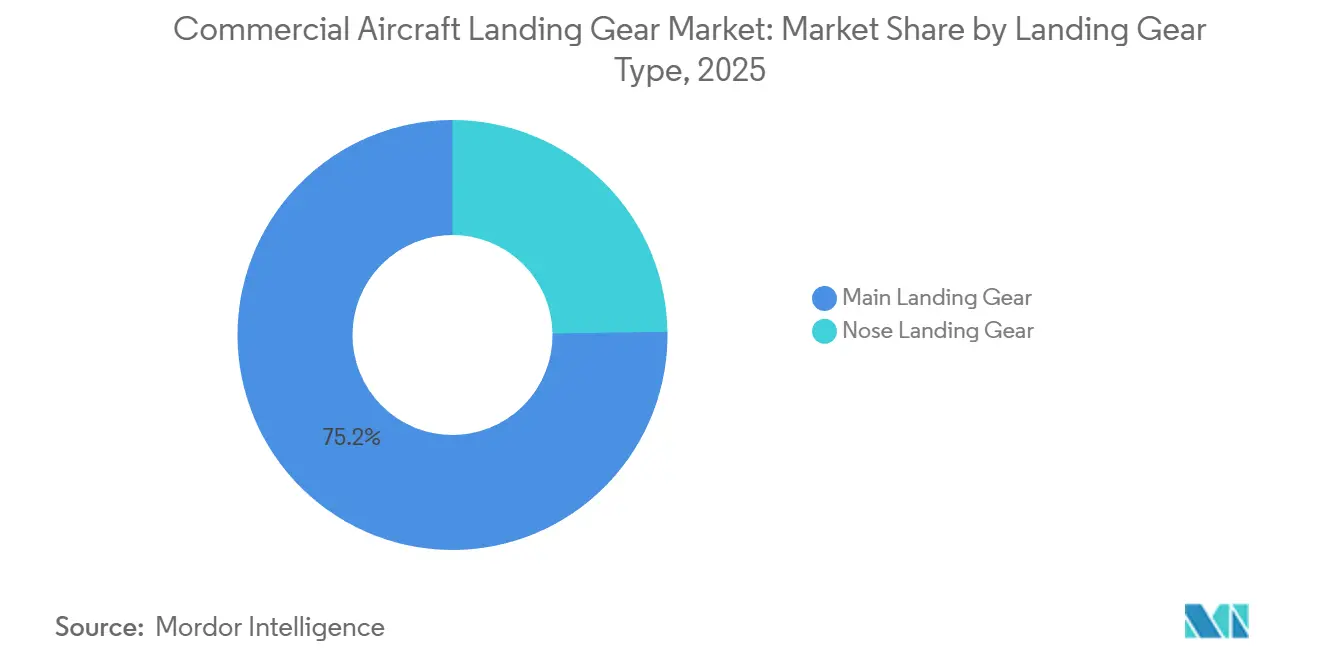

- By landing-gear type, main assemblies captured 75.24% revenue share in 2025, while nose assemblies are forecasted to expand at an 11.21% CAGR through 2031.

- By aircraft type, narrowbody platforms held 65.90% of the commercial aircraft landing gear market share in 2025, whereas widebody systems are projected to advance at a 12.00% CAGR to 2031.

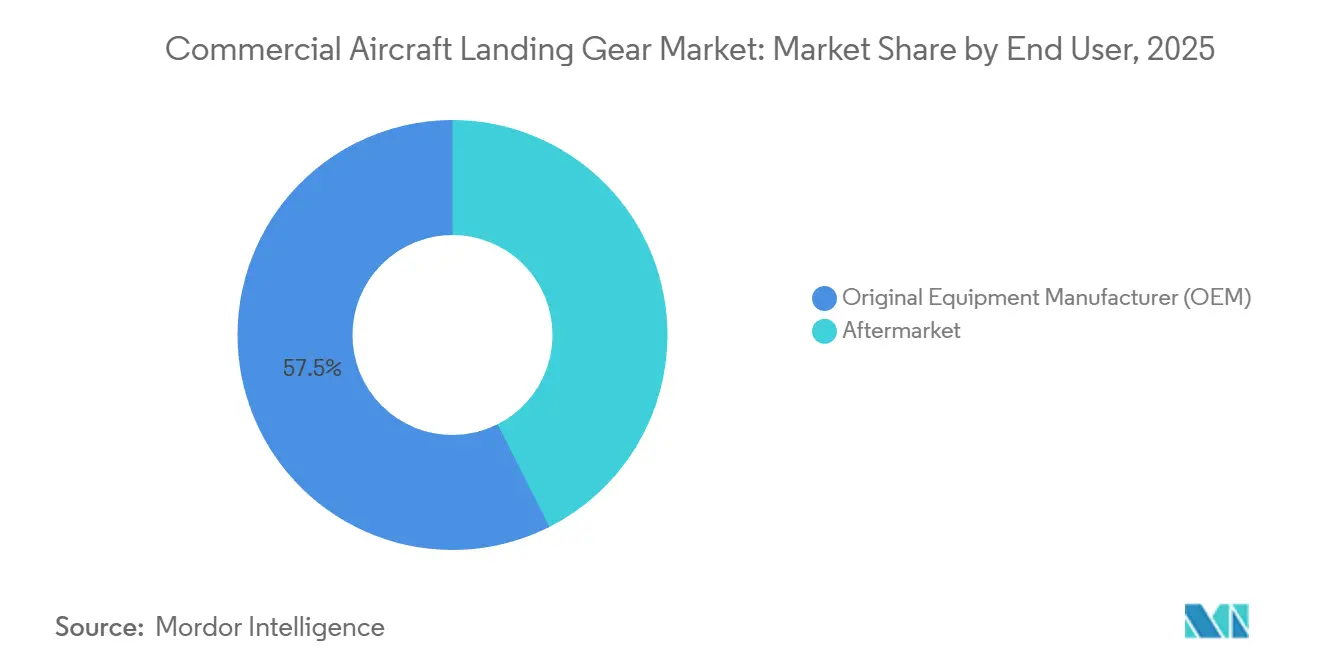

- By end user, OEM contracts accounted for 57.45% of the commercial aircraft landing gear market size in 2025; the aftermarket is expected to grow at an 11.94% CAGR through 2031.

- By sub-system, structural units dominated with a 44.40% share in 2025, and actuation packages are expected to register the strongest 14.04% CAGR by 2031.

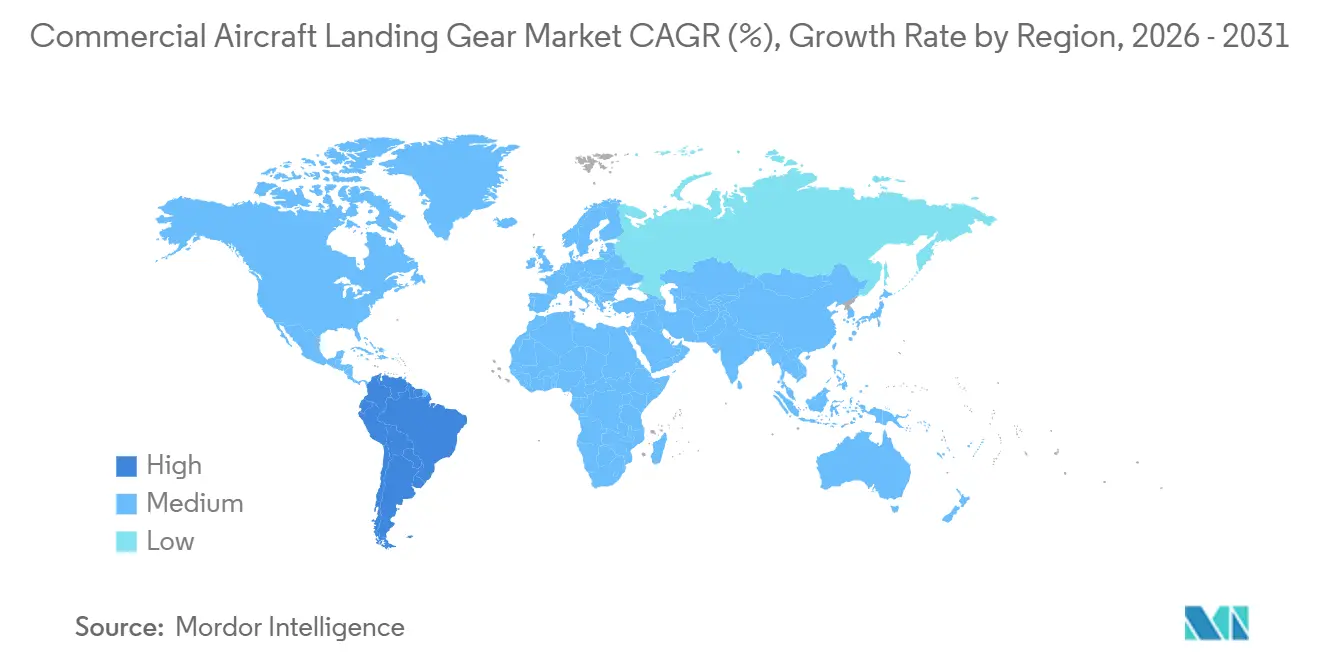

- By geography, the Asia-Pacific region led with a 32.78% revenue share in 2025, while South America is forecasted to post the fastest growth at a 14.95% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Aircraft Landing Gear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward lightweight composite and titanium-matrix materials for fuel-efficient aircraft | +2.3% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| OEM adoption of electric brake architectures enhancing safety and maintainability | +1.8% | Global, led by North America and Asia-Pacific | Short term (≤2 years) |

| Growth in global commercial aircraft production requirements | +2.1% | Asia-Pacific core, spillover to Middle East and South America | Medium term (2-4 years) |

| Integration of smart sensors for landing gear health monitoring | +1.5% | North America and Europe, expanding to Asia-Pacific | Long term (≥4 years) |

| Replacement of aging fleets with next-generation fuel-efficient aircraft | +1.9% | Global, concentration in North America and Europe | Short term (≤2 years) |

| Adoption of Industry 4.0 and 5.0 technologies enhancing landing gear design and assembly | +1.2% | North America and Europe, early pilots in Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Lightweight Composite and Titanium-Matrix Materials

Escalating carbon-offset fees and tightening emissions regulations motivate airlines to shed every unnecessary kilogram of carbon. TISICS won GBP 2.5 million (USD 3.36 million) in UK funding for titanium-matrix struts that promise 30%-70% weight savings. Cranfield University calculated that a 30% mass cut could eliminate 9.6 million tons of CO2 by 2050, based on current traffic projections.[2]Source: TISICS Ltd., “LightLand Project: Titanium Matrix Composites for Landing Gear,” TISICS.com Safran’s wire-arc additive manufacturing reduced lead times by 40% for titanium landing-gear parts on the A350, without compromising fatigue life. Certification remains the chokepoint because EASA and FAA fatigue-test composites to 100,000 simulated cycles, but cross-platform data sharing helps accelerate approvals. Airlines reward suppliers that master hybrid metal-composite designs because life-cycle fuel savings outweigh upfront premiums, reshaping sourcing decisions in favor of innovators that can document measurable operating-cost reductions.

OEM Adoption of Electric Brake Architectures Enhancing Safety and Maintainability

Electric brakes eliminate hydraulic lines, reduce fire risk, and enable regenerative energy capture that powers aircraft buses. Collins Aerospace reports that DURACARB carbon brakes reduce weight by 318 kilograms on the B737NG and, in their electric form, extend disk life by 25% through precise torque control. The B787 was introduced with fully electric brakes in 2011, and Safran followed with contracts for the A350 and now the A320neo, bundling disk replacements and health-monitoring analytics under PBH frameworks that boost recurring revenue.[3]Source: Safran Landing Systems, “Electric Brake Systems and Additive Manufacturing,” Safran-group.com Electric architectures dovetail with more-electric aircraft cabins as pneumatic and hydraulic loads migrate to simpler electrical subsystems. Liebherr pairs brake-control units with fly-by-wire avionics to adjust torque in real-time based on runway friction, a safety feature that regulators endorse by streamlining deferred-item lists. Suppliers holding type-certificate approvals for electric brakes enjoy regulatory moats because new entrants must prove reliability under edge-case conditions, such as asymmetric thrust or contaminated runways, a process that extends beyond two years, even with shared test data.

Growth in Global Commercial Aircraft Production Requirements

Supply-chain recovery has unleashed a synchronized production surge: Airbus aims to reach 75 A320neo units per month by 2026, while Boeing is pushing toward 38 B737 MAX aircraft despite ongoing fuselage inspections at Spirit AeroSystems. Asia-Pacific anchors this ramp; China alone projects 9,284 deliveries through 2043, and India’s IndiGo plus Air India ordered more than 970 jets in 2024. These volumes force landing-gear makers to scale automation and regionalize machining to satisfy offset mandates. Middle East dynamics add variability because Emirates delayed B777X acceptance, but Riyadh Air unveiled plans for more than 100 aircraft, creating new capacity needs. Production growth initially bolsters OEM revenues, with the aftermarket rising five to seven years later, as fleets enter heavy-maintenance cycles. Forward-looking suppliers are investing now in additive manufacturing cells and real-time quality analytics to align their capacity with this multi-year delivery wave.

Integration of Smart Sensors for Landing-Gear Health Monitoring

Fiber Bragg sensors, strain gauges, and vibration accelerometers are now integrated into struts to detect fatigue initiation. Collins Aerospace’s FlightSense portal aggregates sensor feeds. It predicts component failure 500 flight hours in advance, allowing maintenance during overnight checks rather than expensive aircraft-on-ground events that can exceed USD 150,000 per day. Safran trained machine-learning models on 10 million flight cycles and cut in-service removals by 18% during a 2025 pilot with a primary European carrier. SAE’s ARP6461 standardizes data formats, enabling third-party software vendors to hone analytics algorithms. Because hardware commoditizes quickly, sustainable margin accrues to firms that own the analytics layer and can quantify cost avoidance. Airlines are increasingly stipulating sensor-ready gear in RFPs, forcing late-adopting suppliers to either license algorithms or exit high-end tenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Titanium and composite material supply bottlenecks | −1.4% | Global, acute in North America and Europe | Short term (≤2 years) |

| Certification delays for advanced actuation and composite structures | −1.1% | Global, particularly North America and Europe | Medium term (2-4 years) |

| High cost of advanced materials and manufacturing processes | −0.9% | Global, greater impact in emerging markets | Medium term (2-4 years) |

| Expansion of OEM PBH agreements by reducing independent service opportunities | −0.7% | North America and Europe, expanding to Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Titanium and Composite Material Supply Bottlenecks

Western sanctions on Russian titanium removed roughly one-third of the supply in 2022, pushing aerospace-grade prices as high as USD 35 per kilogram in 2024 and stretching qualification timelines for new mills to 18 months. Carbon-fiber prepreg, priced from USD 20 to USD 150 per kilogram, experienced a nine-month lead time in 2025 due to automotive and wind-energy demand diverting capacity. Spirit AeroSystems’ fuselage quality issues cascaded through Boeing build plans, forcing landing-gear suppliers to juggle inventory against shifting delivery slots. Safran’s investment in a French titanium-forging plant and Collins Aerospace’s long-term pact with Toray for prepreg illustrate vertical integration strategies that secure critical materials at predictable costs. Smaller suppliers, lacking scale or capital for backward integration, face a margin squeeze, as long-term OEM contracts limit price-pass-through flexibility.

Certification Delays for Advanced Actuation and Composite Structures

EASA’s CS-25 framework requires 100,000-cycle fatigue tests, drop tests, and damage-tolerance trials, which can extend programs by up to two years. FAA’s AC 25.735-1 added electromagnetic-interference cases for electric brakes, setting back multiple supplier schedules. Liebherr experienced a nine-month delay in its electro-hydrostatic actuator due to regulators requiring additional fail-safe validation under scenarios involving hydraulic fluid contamination. Smaller companies lack parallel engineering teams to run duplicative tests, entrenching incumbents that maintain dedicated certification units. The outcome is fewer disruptive entrants, lengthier innovation cycles, and higher capital barriers, which together restrain CAGR momentum by an estimated 1.1%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Landing Gear Type: Main Assemblies Capture Structural and Brake Integration Premiums

Main assemblies seized 75.24% of the commercial aircraft landing gear market revenue in 2025 and are projected to grow steadily through 2031, buoyed by integrated carbon brakes and electric actuators that command higher unit prices. The inclusion of shock absorbers, wheel pairs, and load-bearing trunnions makes each main-gear shipset complex and capital-intensive. Collins Aerospace’s electric DURACARB package alone delivers 318-kilogram weight savings and extends disk life by a quarter, generating recurring overhaul demand every 2,000–3,000 landings. In comparison, nose gear is projected to expand at an 11.21% CAGR through 2031 and focuses on steering and ground-handling loads; Liebherr’s electro-hydraulic steering for the A350 enhances taxi precision but offers fewer monetization levers.

The transition toward electric brake architectures skews value creation toward main-gear suppliers who can bundle actuation, braking, and digital-health modules under PBH contracts, thereby simplifying OEM sourcing and ensuring consistent revenue throughout the product lifecycle. Nose-gear innovation centers on compact cameras and smart steering actuators that trim runway excursion risk in low-visibility conditions, but the price premium remains modest. Vertically integrated players that deliver both gear types on a sole-source basis reduce interface risk and typically secure 15-year exclusivity per platform, fortifying market positions against mid-tier challengers.

By Aircraft Type: Narrowbody Dominance Reflects Single-Aisle Production Surge

Narrowbody jets accounted for 65.90% of the commercial aircraft landing gear market share in 2025. They will expand at a robust 12.00% CAGR through 2031 as Airbus and Boeing together target more than 110 monthly single-aisle deliveries. Their shorter stage lengths yield higher takeoff-and-landing cycles, accelerating wear on struts, bushings, and brakes, which in turn powers aftermarket demand. Widebody gear, although representing lower volumes, carries heavier load ratings; a B777X main truck weighs around 3,000 kilograms compared with 1,200 kilograms for the B737 MAX, supporting premium pricing. Regional jets, led by the Embraer E2 and A220, occupy a middle ground where weight and cycle requirements spur suppliers like Heroux-Devtek to tailor gear for shorter runways and higher sortie rates.

Widebody recovery trails narrowbody because long-haul traffic, particularly in Asia and Europe, has to fully normalize, prompting airlines to defer B787 and A350 orders. Regional jets face turboprop competition on routes under 500 kilometers, but retain a preference on longer commuter routes due to their speed and cabin comfort. Suppliers therefore invest in flexible production lines and cross-trained workers who are able to pivot between gear shipsets as the OEM mix fluctuates. This agility minimizes capital under-utilization while preserving readiness for any widebody rebound post-2027.

By End User: Aftermarket Gains Traction as Retrofit Demand Accelerates

OEM deliveries contributed 57.45% of the commercial aircraft landing gear market size in 2025, as gear shipsets are embedded in each new airframe contract. However, aftermarket services are expected to notch an 11.94% CAGR through 2031 as installed fleets mature. Overhaul intervals every eight to 12 years furnish predictable demand for bushings, actuators, and carbon-disk replacements. Airlines facing B737 MAX delivery delays are extending their legacy B737NG operations by installing carbon brakes and sensor suites, effectively bridging capability gaps while awaiting the new jets.

PBH frameworks are increasingly dominating heavy-maintenance economics; Safran and Collins lock airlines into proprietary parts and analytics for a per-cycle fee, stabilizing cash flows and raising switching costs. Independent MROs counter by forming purchasing consortia to negotiate data access or focusing on out-of-production fleets where OEM interest wanes. Regulatory pushes, such as EASA’s 2025 mandate for enhanced health monitoring on European operations, further incentivize retrofit installations. Suppliers offering turnkey kits that combine hardware, software, and on-wing support capture higher margins than those selling parts alone, underscoring the strategic imperative to integrate services with product portfolios.

By Sub-Systems: Actuation Systems Lead Growth as Electric Architectures Proliferate

Structural assemblies delivered 44.40% of the revenue in 2025; actuation packages are expected to outpace all others at a 14.04% CAGR, as electro-hydrostatic and fully electric drives replace legacy hydraulics. Electro-hydrostatic units on the A350 eliminate fluid lines, reducing fault-finding time and scheduled inspections by 15%. Braking systems rank second in growth because the adoption of carbon discs, coupled with electric torque modulation, materially lowers weight and extends service life. Steering modules benefit from fly-by-wire integration but remain a smaller slice of value.

Electric actuation introduces a two-tier product landscape: premium widebodies adopt fully electric gear. At the same time, price-sensitive narrowbodies employ hybrid electro-hydraulic schemes that strike a balance between cost and performance. Safran’s electric brake-control unit for the B787 opens recurring software upgrade revenue, signaling how electronics content can extend supplier annuities well beyond hardware sales. Parker Hannifin hedges its hydraulic legacy by investing in electric linear actuators, ensuring relevance as fluid power cedes ground. Suppliers capable of delivering multi-sub-system bundles simplify OEM procurement and warranty administration, reinforcing competitive differentiation in an otherwise cost-driven environment.

Geography Analysis

The Asia-Pacific secured 32.78% of the commercial aircraft landing gear market revenue in 2025, driven by a surge in orders from China and India. It is expected to retain its primacy through 2031, as urbanization, liberalized air travel policies, and rising disposable incomes are expected to boost seat demand. China’s COMAC C919 relies on Western gear suppliers while seeking progressive localization, placing technology-transfer pressure on incumbents. India’s IndiGo and Air India surpassed 970 combined orders in 2024, prompting gear makers to consider local assembly to meet offset clauses. Japan’s Sumitomo Precision Products delivers actuators for Boeing and Airbus programs, cementing the region’s role in the global value chain. Low-cost carriers, such as AirAsia and Vietjet, sustain high-cycle demand profiles that favor carbon brakes and predictive maintenance sensors.

South America is primed for the fastest 14.95% CAGR from 2026 to 2031, anchored by LATAM and Azul fleet renewals and by Embraer’s E2 penetration into secondary city pairs where regional jets outperform narrowbody economics. Domestic travel rebounded swiftly in 2025, drawing investment into airport infrastructure that supports higher movement frequencies. Heroux-Devtek’s multi-year contract for Embraer E2 gear positions the supplier to ride this momentum. North America and Europe combined for 45% of the revenue in 2025. Still, their mature fleets are shifting emphasis toward retrofit rather than new deliveries as airlines leverage PBH agreements to manage lifecycle costs. Regulatory frameworks, such as the EU ETS, intensify incentives to adopt electric brakes and sensors that reduce emissions and capture more verified carbon-credit savings.

The Middle East offers a meaningful upside because Emirates, Qatar Airways, and newcomer Riyadh Air have placed episodic mega-orders. However, wide-body certification slippages and oil-price volatility inject uncertainty into forecasting. Africa continues to trail, hindered by limited airline profitability and underdeveloped MRO infrastructure; however, flag carriers such as Ethiopian Airlines invest cautiously in fleet modernization, signaling a nascent demand for performance-optimized gear. Suppliers weigh near-term volume against geopolitical and payment-risk profiles when allocating sales resources across emerging geographies.

Regulatory Landscape

Commercial aircraft landing gear design, production, and continued airworthiness are governed by transport-category certification rules and mandatory corrective actions. In the United States, FAA airworthiness standards under 14 CFR Part 25 (including landing gear requirements such as 14 CFR 25.729) set baseline performance and safety expectations. In Europe, EASA applies CS-25 for similar certification objectives, and these frameworks are reinforced through Airworthiness Directives (ADs) that mandate inspections, part replacements, and life-limit compliance.

In 2026, regulator actions targeted landing-gear integrity and supporting systems on in-service fleets, shifting near-term maintenance demand toward specific subassemblies. EASA issued AD 2026-0007 (January 2026) addressing component life limits for landing gear, and published ADs in April and May 2026, including AD 2026-0076 (main landing gear shock strut cylinder inspection/replacement) and AD 2026-0092 (A350 main landing gear bogie pivot pin and bush inspections). The FAA also published 2026 ADs affecting Airbus aircraft, including an April 2026 directive tied to A350-941 main landing gear brake rod center pin nut subassemblies and a May 2026 directive concerning main landing gear door actuators. Together, these actions raise compliance requirements for operators, OEMs, and MROs to incorporate mandated work scopes into Approved Maintenance Programs quickly.

Value Chain Analysis

The landing gear value chain begins with upstream materials and special processes, moves through precision machining and complex assembly, and then reaches OEM installation and the aftermarket. Titanium and advanced composites supply structural members (cylinders, pistons, bogie beams, trunnions), while specialized coatings and surface treatments support fatigue and corrosion performance. These steps depend on tightly controlled critical processes and quality systems, commonly aligned to aerospace standards such as AS9100, and on extensive non-destructive testing.

Tier-1 integrators such as Safran Landing Systems, Collins Aerospace (RTX), and Liebherr-Aerospace combine structures with braking and actuation packages, then deliver complete shipsets to Airbus, Boeing, and regional-jet OEMs, with configuration control managed across long platform lives. Downstream, aftermarket value is captured through overhaul shops, spare-parts distribution, and exchange or power-by-the-hour style support models. Supply-chain actions show active regionalization and partner development: Liebherr-Aerospace signed a long-term agreement with Jeh Aerospace to manufacture high-precision landing gear components from Hyderabad, India (April 2026), and collaborated with Bharat Forge in India to establish manufacturing capability with ring mill forging and machining technologies (February 2025). Capacity and localization moves also extend to Europe, with Collins Aerospace announcing an expansion of its Tajecina, Poland facility to increase landing gear production capacity (September 2025). On the services side, OEM-aligned MRO networks and specialist repair providers support fleets through overhaul and spares pipelines, including Safran and Revima renewing a long-term contract for spare parts supply and technical support to landing gear repair and overhaul facilities in France and Thailand (June 2025).

Competitive Landscape

Safran Landing Systems, Collins Aerospace, and Liebherr-Aerospace hold a significant share of the commercial aircraft landing gear market in 2025. This dominance is attributed to their long-standing sole-source positions on flagship Boeing and Airbus platforms. Their vertical integration across structures, brakes, and actuation enables single-shipset delivery, streamlining OEM procurement processes and bundling PBH service contracts, which secure long-term revenue streams. Companies such as Heroux-Devtek, Triumph Group, and Sumitomo Precision Products occupy the next tier, focusing on niche areas within regional-jet programs and selective subsystems where agility and engineering responsiveness outweigh economies of scale. Opportunities remain in retrofit kits for aging B737NG and A320ceo fleets, providing a competitive space for independent MROs and specialized suppliers to operate without directly competing with entrenched OEM service networks.

Additive manufacturing is emerging as a disruptive force, challenging traditional cost structures by enabling the production of titanium parts that previously required capital-intensive forging. However, the lengthy certification cycles, often spanning multiple years, limit the immediate market penetration of these technologies. In 2024, Safran introduced a patented modular landing gear design that enables the independent swapping of actuation or brake modules, resulting in a 30% reduction in maintenance time. This innovation strengthens the competitive position of companies that integrate hardware with digital twins and analytics. Regulatory compliance, governed by FAA AC 25.735-1 and EASA CS-25, continues to impose high costs while acting as a barrier to entry, thereby sustaining incumbent profit margins of 12%-15% EBIT, despite pressures from raw material inflation.

Trends in market consolidation reflect broader patterns within the aerospace industry. OEMs are increasingly vertically integrating aftermarket support to capture value that was previously directed to independent repair shops. Meanwhile, Tier-2 suppliers are pursuing alliances or acquisitions to scale capital-intensive technologies, such as electric actuation systems or composite struts. Despite these trends, competitive intensity remains high as production ramps up, increasing volume visibility and attracting investments from component specialists and Asian joint ventures that aim to localize their supply chains. Incumbent players are responding by enhancing regional service centers and embedding proprietary health-monitoring analytics, which tie airlines into long-term service ecosystems. Consequently, market shares are expected to shift only marginally over the forecast period, with platform mix and technological differentiation playing a more significant role than pricing strategies in determining competitive positioning.

Commercial Aircraft Landing Gear Industry Leaders

Safran SA

Honeywell International Inc.

RTX Corporartion

Liebherr-International Deutschland GmbH

Héroux-Devtek Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity area is the expansion of landing-gear manufacturing and overhaul capacity closer to high-rate single-aisle production and to large installed widebody fleets, driven by lead-time reduction and aircraft-on-ground risk management. In June 2026, Collins Aerospace (RTX) opened an expanded manufacturing facility in Tajecina, Poland following a USD 69 million expansion that increased landing gear production capacity by nearly 25%, signaling continued investment to support OEM build rates and stabilize supply continuity. Safran Landing Systems also announced in June 2026 that it is expanding global MRO capabilities for Boeing 787 and Airbus A350/A330 programs with investments across sites including Singapore, Molsheim, and Queretaro, aligning aftermarket throughput with long-haul fleet maintenance cycles.

A second opportunity is in service-led commercial models that bundle inventory access, overhaul scheduling, and on-wing support, particularly for airlines managing utilization alongside downtime constraints. Boeing’s Landing Gear Exchange activity reflects this shift, with the company signing its largest Landing Gear Exchange contract in company history with Singapore Airlines in February 2026, covering more than 75 aircraft across the 737 MAX and 787 families. Beyond service bundling, suppliers pursuing lighter structures and more-electric architectures can convert regulatory and airline focus on maintainability into more differentiated offerings, especially where sensor-ready gear and electric braking or actuation reduce inspection burden and simplify maintenance planning for high-cycle narrowbody fleets.

Recent Industry Developments

- June 2026: RTX, through Collins Aerospace, opened an expanded manufacturing facility in Tajecina, Poland, backed by a USD 69 million investment that increased landing gear production capacity by nearly 25%. The site expansion strengthens regional supply to Airbus and Boeing programs and adds resilience against high-rate production variability by expanding qualified output capacity.

- December 2025: GA Telesis signed a five-year overhaul agreement with a major US airline to service and overhaul A320-family landing gear assemblies. The contract reinforces the role of integrated aviation services providers in capturing aftermarket work scopes as operators seek predictable turnaround times and lifecycle cost control.

- June 2025: Safran unveiled upgraded facilities for landing and braking systems in Molsheim to enhance production and maintenance capabilities for landing gear and carbon brake lines. The added industrial capacity supports both OEM delivery schedules and the growing overhaul pipeline, while also pulling more demand for upstream precision forging, coatings, and heat-treatment services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from landing gear systems used on commercial aircraft, covering new installations on delivered aircraft and replacement demand linked to in-service fleets.

Scope exclusions: We exclude landing gear used for military aircraft, helicopters, business jets, and standalone wheel or tire sales that are not part of an integrated landing gear system.

Segmentation Overview

- By Landing Gear Type

- Main Landing Gear

- Nose Landing Gear

- By Aircraft Type

- Narrowbody

- Widebody

- Regional Jet

- By End User

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Sub-Systems

- Actuation System

- Steering System

- Braking System

- Strutural System

- Other Sub-Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by anchoring the demand pool for commercial aircraft using open aviation and macro datasets, then narrowing to landing gear relevant indicators. For reference points, we use sources such as FAA and EASA airworthiness and safety publications, ICAO and IATA traffic statistics, World Bank macro indicators, UN Comtrade trade codes for relevant materials and parts, and open technical literature and patents that signal design shifts (for example, actuation changes or material moves).

To convert these signals into usable model inputs, we also review public company filings, investor presentations, OEM order and delivery updates, and credible aerospace press releases that track program ramps and retrofit cycles. In addition, we use paid subscriptions focused on company financials and intelligence, news and financials, aircraft and fleet level aviation databases, and patent coverage to cross-check timelines, production ramp assumptions, and cost drivers. The sources listed here are illustrative, and many other public references were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work was used to stress-test the desk assumptions on landing gear shipset pricing, overhaul frequency, and the split between OEM fitment and aftermarket events. We spoke with supply chain participants, maintenance-focused experts, and airline or fleet contacts across major aviation regions. These inputs helped us refine adoption assumptions for newer subsystems (such as actuation and braking upgrades) and adjust any ramp patterns that did not align with observed shop and airline planning cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | APAC: 49% |

| Mid tier: 47% | Functional/Unit leaders: 28% | EMEA: 33% |

| Smaller Players: 21% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where aircraft production and fleet activity are reconstructed into landing gear demand, and then translated into value using gear shipset and overhaul pricing logic. The model is set up around aircraft deliveries by type, the in-service fleet count, typical landing gear overhaul intervals, and the share of events that result in major repair versus replacement, so the OEM and aftermarket pools are derived in a consistent way.

To keep totals realistic, we corroborate results with selective bottom-up checks, such as sampled shipset ASPs multiplied by estimated unit volumes for narrowbody, widebody, and regional jets, followed by channel checks on MRO throughput capacity. Inputs that materially move the numbers include delivery ramp rates, retirement and utilization patterns, landing gear shop visit frequencies, material and machining cost trends for high strength components, and braking and actuation retrofit intensity where it is actually practiced. Forecasting is run using scenario analysis supported by expert consensus, since build rates, shop capacity, and supply constraints can change quickly and are better handled through a few clear cases than one smooth curve. When gaps appear in bottom-up signals, we use conservative interpolation and then re-test during interviews so outliers do not distort the total.

Data Validation & Update Cycle

Model outputs are validated through triangulation across delivery and fleet indicators, aftermarket activity signals, and interview-based pricing and cycle assumptions, then inconsistencies are investigated before sign-off. Variance checks are done at multiple levels, including aircraft type totals, OEM versus aftermarket splits, and region-level patterns, so one strong assumption does not unintentionally over-inflate the full market.

A multi-step analyst review is followed, and respondents are re-contacted when a material mismatch is found, such as a sudden change in delivery guidance, a supply disruption, or an unexpected shift in overhaul timing. Reports are refreshed annually, and interim updates are made when large aircraft program changes or major regulatory events create a clear step change. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Commercial Aircraft Landing Gear Market Size Measured Against Other Published Estimates

It is normal to see different market size figures for commercial aircraft landing gear because publishers do not always count the same revenue streams, and they also make different assumptions on overhaul intensity and pricing over time. Differences also come from the year used as the starting point, how currency conversion is applied, and how quickly estimates are refreshed after changes in aircraft delivery plans.

Some sources expand the scope by treating adjacent wheel and tire revenue as part of landing gear or by using broader aircraft coverage assumptions that are not separated cleanly by commercial category. For Mordor Intelligence, the count is limited to integrated landing gear systems for commercial aircraft, including OEM and aftermarket demand, and standalone wheel or tire sales are kept out to avoid double counting against braking and structural assemblies.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.75 B (2025) | |

| Industry Publisher A | USD 5.80 B (2024) | Uses a different base year and does not clearly state an OEM versus aftermarket split, which can shift totals depending on whether overhaul revenue is fully captured or partially implied. |

| Industry Publisher B | USD 10.50 B (2025) | Appears to apply a broader value scope, which may include adjacent components and wider content-per-aircraft assumptions that raise ASPs beyond integrated landing gear system revenue. |

The spread across the three figures mainly comes from what is counted inside landing gear revenue and how aftermarket activity is converted into dollars. By keeping the demand pool tied to commercial aircraft deliveries and fleet-driven overhaul cycles, and then testing the ASP and cadence assumptions through interviews, the estimate remains traceable to clear inputs that a reader can follow and replicate.

Key Questions Answered in the Report

What is the projected value of the commercial aircraft landing gear market in 2031?

The commercial aircraft landing gear market is forecasted to reach USD 9.77 billion by 2031 on the back of a 10.91% CAGR.

Which aircraft category drives the highest landing-gear demand?

Narrowbody jets hold the lead with 65.90% revenue share in 2025 and are growing at a 12% CAGR through 2031.

Why are electric brake systems gaining momentum?

They cut up to 318 kilograms of weight, reduce fire risk and extend brake-disk life by 25%, offering significant operating-cost savings.

Which region is expanding the fastest?

South America is set to post the quickest 14.95% CAGR from 2026 to 2031 because carriers like LATAM and Azul are modernizing fleets.

How do power-by-the-hour agreements affect independent MROs?

PBH contracts bundle maintenance under OEM control, tightening airline lock-in and reducing work scopes available to independent repair shops.

What technologies are suppliers adopting to speed development?

Additive manufacturing, digital twins, and collaborative robots are compressing design cycles and enabling lighter, more customized gear assemblies.

Page last updated on: