Aircraft Switches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Switches Market Analysis by Mordor Intelligence

The aircraft switches market size is expected to grow from USD 2.58 billion in 2025 to USD 2.68 billion in 2026 and is forecast to reach USD 3.27 billion by 2031 at 4.02% CAGR over 2026-2031. This trajectory mirrors the aviation sector’s steady pivot toward more-electric architectures, where electrical subsystems replace legacy mechanical and hydraulic components, multiplying the number of switching points across each airframe. Airlines’ fleet-renewal schedules and defense modernization programs ensured a consistent order flow for both commercial and military platforms in 2024 and early 2025. Solid-state power controllers, silicon-carbide devices, and smart switches with built-in diagnostics became mainstream as the emphasis shifted from discrete electromechanical parts to software-defined, data-sharing modules capable of predictive maintenance integration. Vendor selection criteria increasingly include cybersecurity compliance and supply-chain integrity, forcing mid-tier suppliers either to invest in certification upgrades or accept consolidation offers from larger peers. Across regions, North America retained the revenue lead owing to sustained defense spending. Yet, Asia-Pacific posted the fastest growth as China and India accelerated aircraft production and MRO capacity expansion.[1]Source: Airbus, “China aviation services market is expected to be the largest by 2043,” airbus.com

Key Report Takeaways

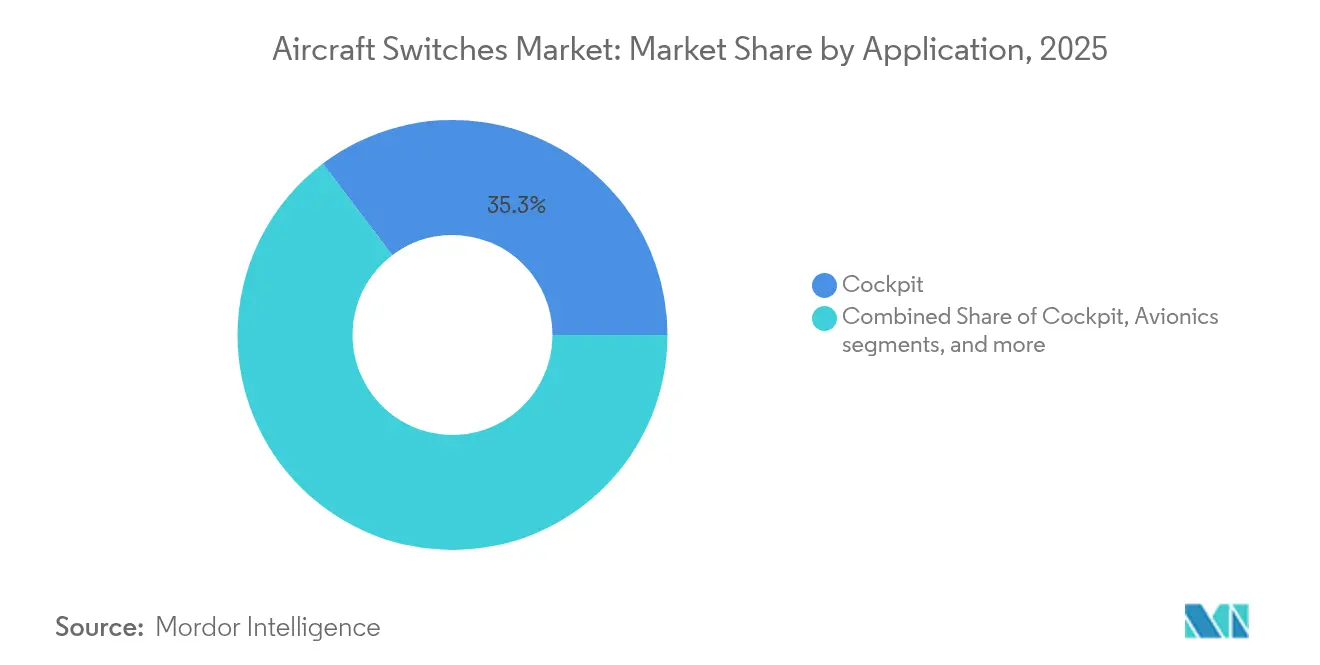

- By application, cockpit systems led the aircraft switches market with 35.30% of the share in 2025, while avionics switches are projected to record a 4.89% CAGR through 2031.

- By switch type, manual switches retained 65.10% revenue share in 2025; automatic switches are set to grow at a 5.72% CAGR to 2031.

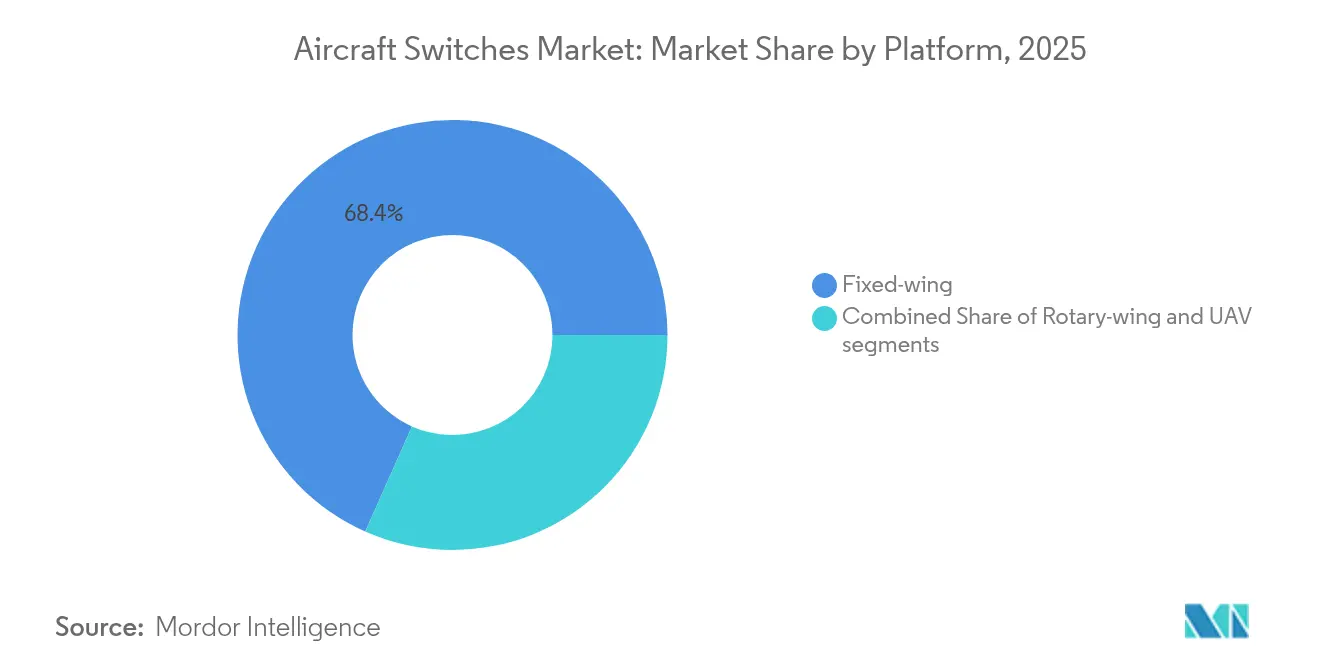

- By platform, fixed-wing aircraft held 68.35% of the aircraft switches market size in 2025; unmanned aerial vehicles are poised for the highest 6.24% CAGR.

- By end user, OEM programs commanded 60.10% of 2025 revenue, whereas the aftermarket is forecasted to expand at a 4.43% CAGR.

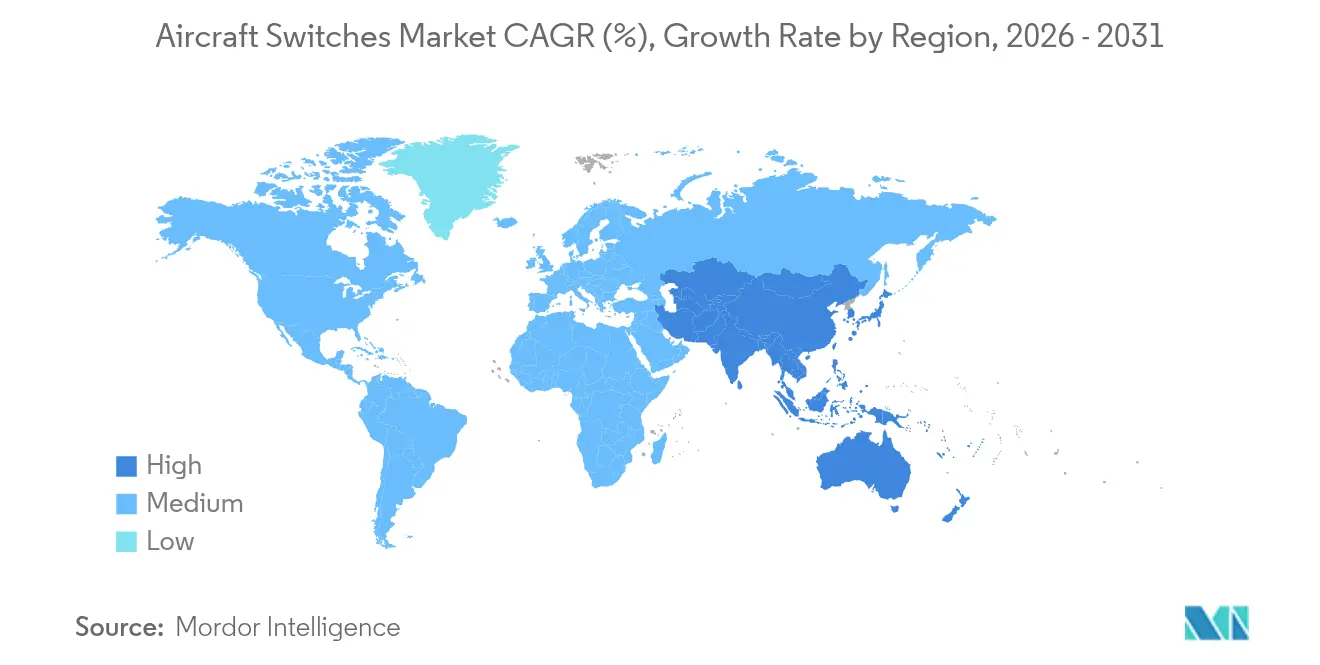

- By geography, North America accounted for 37.40% of the 2025 revenue base, and Asia-Pacific is expected to post the strongest 5.43% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Switches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet renewal wave in next-gen narrow-body programs | +0.8% | Global, high in North America and Asia-Pacific | Medium term (2-4 years) |

| Surge in more-electric subsystems needing solid-state switching | +1.2% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Cabin-retrofit boom for IFEC and lighting upgrades | +0.6% | Global, strong in North America and Europe | Short term (≤ 2 years) |

| Rapid military rotorcraft recapitalization budgets | +0.5% | North America, Europe, Asia-Pacific defense markets | Medium term (2-4 years) |

| Data-driven predictive-maintenance contracts bundling smart switches | +0.4% | Global, early adoption in North America | Long term (≥ 4 years) |

| Silicon-on-insulator (SOI) power‐device breakthroughs enabling ultra-compact relays | +0.3% | Global, tech hubs in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fleet Renewal Wave in Next-Gen Narrow-Body Programs

Airlines accelerated replacement of aging single-aisle fleets in 2024, specifying electrical architectures that require denser switching networks for power distribution and flight-deck controls. Boeing’s B777X certification effort and Air India’s large multitype order packages typified how every new delivery triggered bundled switch installations spanning cockpit, avionic bay, and cabin zones.[2]Source: Aviation Week, “Boeing Readies For 777X Certification Push,” aviationweek.com Operators insisted on future-proof hardware able to accommodate software upgrades across the 20-year airframe life, favoring suppliers offering configurable solid-state units with health-monitoring outputs.

Surge in More-Electric Subsystems Requiring Solid-State Switching

Aircraft electrification expanded from secondary systems to high-power actuation lines, pushing switch ratings beyond 500A and 1,000V. Collins Aerospace prototyped megawatt-class power-distribution modules under the Clean Aviation SWITCH program, validating silicon-carbide devices for continuous high-temperature operation. Honeywell’s silicon-on-insulator CMOS processes supported components rated to 300°C, enabling power-conversion bays to migrate closer to engines and reducing harness weight. These advances underpinned the aircraft switches market as platform OEMs shifted to distributed electrical propulsion concepts.

Cabin-Retrofit Boom for IFEC and Lighting Upgrades

Cabin interior refresh cycles peaked in 2024–2025, with airlines upgrading LED lighting, Bluetooth audio, and high-bandwidth connectivity. Airbus prepared A350 retrofit kits as nine-year-old airframes entered heavy maintenance visits, creating immediate demand for low-profile rocker and rotary switches integrated into passenger-service units. Studies indicating 68% energy savings from LED substitution strengthened the business case, and smart switches capable of linking to cabin-management systems through ARINC 429 or CAN bus interfaces became standard. Vendors supplying configurable switch panels won multi-airline contracts tied to harmonized cabin branding initiatives.

Rapid Military Rotorcraft Recapitalization Budgets

The US Army’s Future Long Range Assault Aircraft contract and parallel Apache modernization drove new build and retrofit activity for helicopter fleets, each aircraft using hundreds of sealed switches for avionics, weapons release, and environmental control. Bell’s V-280 Valor and GE Aerospace’s integrated power systems required fly-by-wire compatible switching modules hardened for vibration and sand-ingress environments. Similar recapitalization programs in Europe and Asia-Pacific sustained double-digit order growth for military-grade toggle, guarded, and automatic contactor assemblies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Qualified-component certification queue delays at FAA and EASA | -0.7% | Global, mostly North America and Europe | Short term (≤ 2 years) |

| Raw-material price volatility for silver-cadmium oxide contacts | -0.4% | Global supply chain | Medium term (2-4 years) |

| Counterfeit part infiltration in MRO supply chains | -0.3% | Global, concentrated in secondary markets | Short term (≤ 2 years) |

| Cyber-hardening requirements raising BOM cost of smart switche | -0.5% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Qualified-Component Certification Queue Delays

FAA and EASA engineering directorates faced case backlogs as cybersecurity and software assurance reviews deepened, stretching component approval lead times from 12 months to more than 24 months. Boeing’s B777X program delays highlighted the cascading impact on tier-1 and tier-2 suppliers waiting for type-certification data to finalize production release. [3]Source: Federal Register, “Equipment, Systems, and Network Information Security Protection,” federalregister.gov Smaller switch vendors lacking dedicated certification teams risked losing line-fit positions, tempering overall aircraft switches market momentum.

Cyber-Hardening Requirements Raising BOM Cost of Smart Switches

Regulatory proposals issued in 2024 mandated embedded encryption engines, secure boot, and continual threat-monitoring within network-connected components. Airbus positioned cyber-secure design as a strategic imperative after noting that 64% of aviation cyber incidents targeted ground and airborne connectivity gateways. Implementing hardware root-of-trust circuits and tamper-evident enclosures added up to 12% material cost per smart switch, pressuring price-sensitive retrofit campaigns and capping short-term adoption rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Cockpit Leadership Amid Avionics Surge

Cockpit switches retained 35.30% of 2025 revenue as pilots relied on tactile pushbuttons, guarded toggles, and rotary selectors for flight-critical tasks. Manual designs dominated because regulators required physical backup control lines in case of display or data bus failure. The segment benefited from sustained deliveries of single-aisle aircraft, where standardized overhead panels simplified integration and lowered per-unit costs.

Avionics installations generated the fastest 4.89% CAGR forecast through 2031. Multi-function displays, flight-management computers, and health-monitoring units demanded high-density, low-bounce automatic relays linked over Ethernet-based backbones. Airlines embedded smart switches that streamed usage data into predictive-maintenance platforms, improving dispatch reliability. Overall, avionics growth supported incremental additions to the aircraft switches market size for integrated modular avionics suites.

By Switch Type: Manual Core, Automatic Ascendancy

Manual units supplied 65.10% revenue in 2025, led by pushbutton assemblies preferred for clear tactile affirmation and straightforward line maintenance. Rocker variants won cabin positions where design language and illumination effects improved passenger perception. Manual demand preserved manufacturing economies of scale and stable replacement part numbers across multiple fleets.

Automatic switches are projected to climb at a 5.72% CAGR as more-electric architectures substitute electromechanical contactors with solid-state controllers. Hybrid relays that pair arc-free semiconductor paths with mechanical redundancy entered serial production, combining low voltage drop with fail-safe positioning. This migration enlarges the aircraft switches market as each power-distribution center now contains dozens of intelligent, addressable switches instead of a handful of legacy breakers.

By Platform: Fixed-Wing Mass, UAV Momentum

Fixed-wing programs, ranging from regional jets to strategic airlifters, accounted for 68.35% of the 2025 aircraft switches market share. Widebody development restarted after pandemic-era pauses, and narrow-body backlogs returned to pre-2020 levels, ensuring high order stability. Mature qualification documents allowed suppliers to reuse approved parts across derivative models, sustaining volume.

Unmanned aerial vehicles (UAVs) are forecasted to record a 6.24% CAGR, supported by autonomous surveillance, cargo, and combat missions. Each UAV demands weight-optimized, hermetically sealed miniature switches resistant to temperature extremes and electromagnetic interference. GE Aerospace’s small-engine roadmap and Kratos’ airframe pipeline signal escalating volumes that will diversify the platform mix within the aircraft switches market.

By End User: OEM Base, Aftermarket Upswing

OEM lines commanded 60.10% of 2025 sales as every delivery aircraft incorporated customized switch suites validated at type certification. Long production cycles secured predictable multi-year demand, and risk-sharing partnerships locked in pricing frameworks.

Aftermarket orders are set to advance at a 4.43% CAGR as aging fleets require life-extension upgrades. Cabin retrofits, avionics modernization, and condition-based replacement campaigns broaden part numbers in circulation. Safran recorded 17.7% year-on-year equipment and defense aftermarket growth in early 2025, illustrating how MRO networks lift recurring revenue for switch vendors. Expanding inventory pools positively influence the aircraft switches market size by adding service and repair contracts to traditional hardware sales.

Geography Analysis

North America generated 37.40% of 2025 revenue, underpinned by comprehensive defense budgets and active commercial production lines. Boeing, Honeywell, Curtiss-Wright, and Eaton anchored the regional supplier ecosystem, while FAA certification expertise concentrated program approvals within the United States borders. Several USD 10 billion-plus contracts for NGAD and helicopter upgrades ensured consistent switch demand across fighter, tanker, and rotorcraft categories.

Asia-Pacific, forecast to expand at 5.43% CAGR, benefited from China’s climb up the MRO value chain and India’s surging aircraft orders. Airbus projected China’s services segment to reach USD 61 billion by 2043, with maintenance representing 83%—a switch-intensive activity. India’s government earmarked USD 12 billion for airport expansion and encouraged local component production, prompting Western suppliers to establish joint ventures, as seen in Eaton’s partnership with SIAEC. The region’s focus on indigenization opened opportunities for mid-sized players to license technology and capture domestic content quotas.

Europe remained stable, supported by Airbus assembly, defense cooperation under GCAP, and R&D projects backed by EU climate funds. Collins Aerospace’s Clean Aviation SWITCH prototypes in France and Ireland validated high-voltage distribution strategies for hybrid-electric demonstrators, elevating regional intellectual-property stakes. Simultaneously, EASA’s cybersecurity mandates heightened certification complexity, favoring suppliers with in-house compliance resources and thus maintaining moderate barriers to entry within the aircraft switches market.

Competitive Landscape

The aircraft switches market exhibited moderate fragmentation throughout 2024, with roughly a dozen multinational corporations eclipsing hundreds of niche specialists. Safran pursued portfolio expansion by acquiring Collins Aerospace’s actuation and flight-control assets, bringing complementary electromechanical expertise under one roof. Honeywell invested in silicon-on-insulator fabrication to differentiate its high-temperature solid-state offerings and announced the spin-off of its aerospace division, signaling a strategic focus on next-generation avionics and power systems. Eaton leveraged cash flow to fund hydrogen-aircraft research consortia, aiming to position its contractor line for emerging zero-emission platforms.

Technology leadership increasingly hinged on embedded diagnostics and cyber-secure design. Vendors integrating cryptographic authentication, real-time health monitoring, and field-programmable logic captured premium line-fit slots on the latest Boeing and Airbus variants. Supply-chain integrity emerged as a key differentiator after counterfeit titanium and seal incidents prompted the formation of the Aviation Supply Chain Integrity Coalition. Companies able to prove part traceability through blockchain-enabled certificates improved their win ratio during competitive tendering. Simultaneously, white-space opportunities opened in UAV-specific, SWaP-optimized switch modules, where smaller firms could commercialize rapid prototypes without the legacy burdens borne by incumbent conglomerates.

Strategic alliances complemented acquisitions. Curtiss-Wright secured a USD 80 million IDIQ with the US Air Force for high-speed data-acquisition hardware, cross-selling embedded switch cards into instrumentation racks. Collins Aerospace partnered with the US Army to develop modular open-systems avionics for the UH-60M, locking in future retrofit streams featuring standard-format power-distribution switchboards. Such collaborations underlined how integration capability—as much as hardware performance—determined bidding success in the aircraft switches market.

Aircraft Switches Industry Leaders

Honeywell International Inc.

Eaton Corporation plc

Safran SA

RTX Corporation

TE Connectivity Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vertical Aerospace and Honeywell expanded their VX4 eVTOL collaboration, a deal valued at USD 1 billion over ten years.

- March 2025: Collins Aerospace was awarded a USD 80.2 million contract to create a modular avionics architecture for UH-60M Black Hawk upgrades.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global aircraft switches market as the annual revenue generated from factory-built manual and automatic electrical switches, including toggle, rocker, push-button, rotary, pressure, and relay units, installed on fixed-wing, rotary-wing, and unmanned aircraft across civil and military fleets. These components regulate power or signals for cockpit controls, avionics, engines, cabin, and auxiliary systems.

Scope Exclusion: Retrofit of non-aviation grade switches supplied through informal channels is not included.

Segmentation Overview

- By Application

- Cockpit

- Cabin

- Engine and Power Auxiliary Power Unit (APU)

- Avionics

- Others

- By Switch Type

- Manual

- Pushbutton Switches

- Toggle Switches

- Rocker Switches

- Rotary Switches

- Others

- Automatic

- Pressure Swicthes

- Temperature Switches

- Flow Switches

- Relays and Contactor Switches

- Others

- Manual

- By Platform

- Fixed-wing Aircraft

- Rotary-wing Aircraft

- Unmanned Aerial Vehicles (UAV)

- By End User

- OEM

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed air-frame electrical architects, purchasing managers at OEM and tier-1 harness integrators, and senior MRO engineers across North America, Europe, and Asia-Pacific. The conversations confirmed usage density by platform family, emerging smart-switch specifications, and price dispersion before we finalized assumptions.

Desk Research

We started with open civil-aviation statistics, FAA and EASA equipment certification logs, international trade records for HS-8536 articles, and association yearbooks such as IATA, GAMA, and AIA. Company filings, investor presentations, and reputable press sources offered shipment mix and average selling prices, while accident databases clarified replacement rates. Paid resources from D&B Hoovers and Dow Jones Factiva added financial sanity checks. The sources named are illustrative; many other publications informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down demand pool was built from annual aircraft production, in-service fleet size, and planned retirements, which are then multiplied by switch counts segmented by platform and application. Supplier roll-ups of sampled ASP × volume provided a bottom-up sense check that aligned within five percent. Key variables shaping the model include new-build output, fleet utilization hours, electrification content per aircraft, certification cycle length, average switch life, and inflation-adjusted ASP trends. Forecasts employ multivariate regression blended with scenario analysis, letting us flex macro demand, technology adoption, and defense budgets through 2030.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst scrutiny, and sector-lead sign off. Reports refresh each year, with interim updates when air-framer rate changes, major program shifts, or regulatory rulings materially move the market, so clients receive the latest view.

Why Mordor's Aircraft Switches Baseline Commands Operator Confidence

Published estimates often diverge because providers choose different switch categories, platform mixes, currency bases, and refresh cadences.

Key gap drivers include whether sensor-type automatic switches are counted, if UAVs sit inside military totals, and how each firm escalates historical ASPs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.58 B (2025) | Mordor Intelligence | |

| USD 2.60 B (2025) | Regional Consultancy A | Captures headline deliveries only, ignores installed-base replacements |

| USD 2.30 B (2024) | Global Consultancy B | Excludes aftermarket revenue and converts at constant 2019 exchange rates |

| USD 1.11 B (2024) | Trade Journal C | Counts cockpit electromechanical units only, omitting rotary-wing platforms |

The comparison shows that when scope breadth, currency realism, and dual-track modeling are considered, Mordor Intelligence provides a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the aircraft switches market?

The aircraft switches market stood at USD 2.68 billion in 2026 and is projected to reach USD 3.27 billion by 2031, advancing at a 4.02% CAGR.

Which application segment holds the largest revenue share?

Cockpit systems led with 35.30% of 2025 revenue due to the concentration of safety-critical controls in the flight deck.

Why are automatic switches growing faster than manual designs?

Automatic switches integrate solid-state technology and embedded diagnostics that support more-electric architectures, driving a 5.72% CAGR to 2031.

Which region is expected to grow the fastest?

Asia-Pacific is forecasted to record a 5.43% CAGR through 2031, spurred by Chinese MRO expansion and Indian aircraft orders.

How are cybersecurity mandates affecting switch design?

New FAA and EASA rules require encryption, secure boot, and continuous monitoring, increasing bill-of-materials cost by up to 12% for smart switches.

What factors influence supplier selection today?

Operators prioritize proven certification status, integrated diagnostics, cybersecurity compliance, and traceable supply chains when choosing switch vendors.

Page last updated on: