Commercial Aircraft Engines Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 98.86 Billion |

| Market Size (2031) | USD 117.13 Billion |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

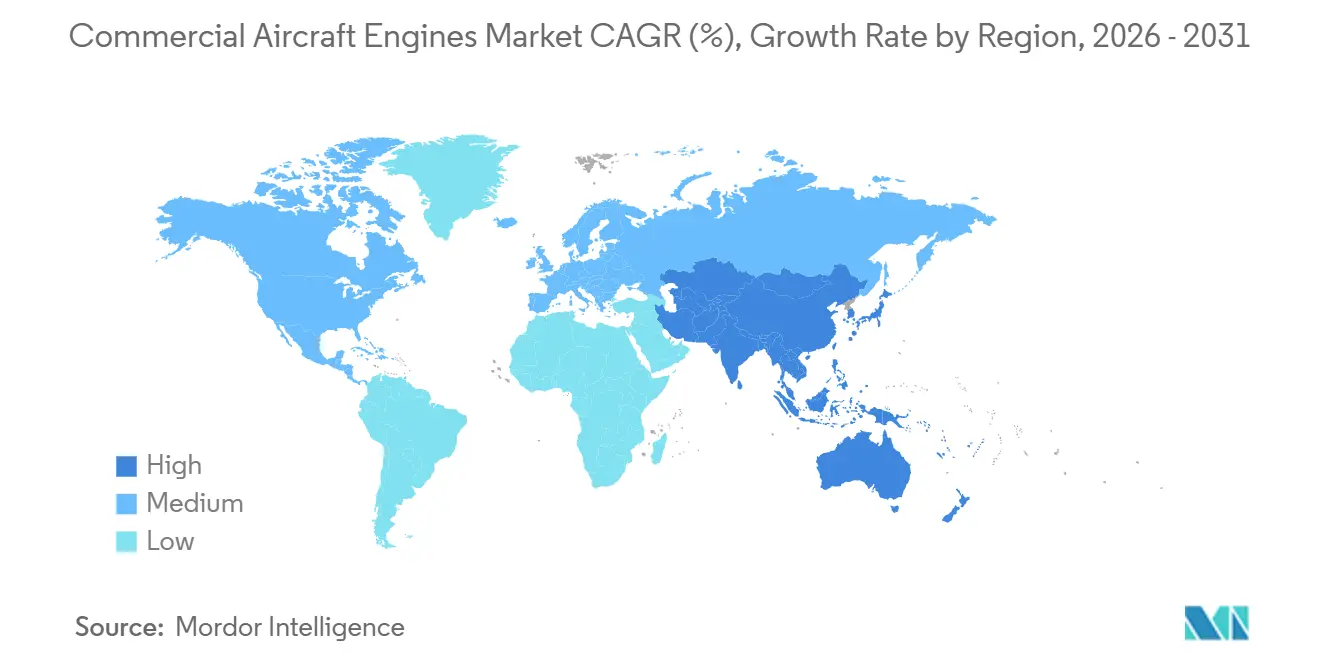

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Engines Market Analysis by Mordor Intelligence

The commercial aircraft engines market size is expected to grow from USD 95.56 billion in 2025 to USD 98.86 billion in 2026 and is forecasted to reach USD 117.13 billion by 2031 at a 3.45% CAGR over 2026-2031. This expansion is tied to the growth of low-cost-carrier fleets in the Asia-Pacific region, elevated shop-visit volumes for PW1100G and LEAP engines, and a steady shift toward power-by-the-hour contracts, which enhance aftermarket revenue visibility. Turbofan platforms continue to dominate new-build deliveries, yet turboprop programs supplying thin regional routes are regaining momentum as operators in Southeast Asia and Africa replace aging ATR fleets with PW127XT-M powerplants. Technology migration remains gradual; conventional architectures still anchor much of the installed base, but hybrid-electric demonstrators from NASA and Collins Aerospace have accelerated certification road maps for sub-regional aircraft. On the supply side, persistent bottlenecks in titanium and nickel forgings are prompting GE Aerospace, Safran, and Pratt & Whitney to deepen additive manufacturing adoption and vertically integrate strategic material sources to secure engine output.

Key Report Takeaways

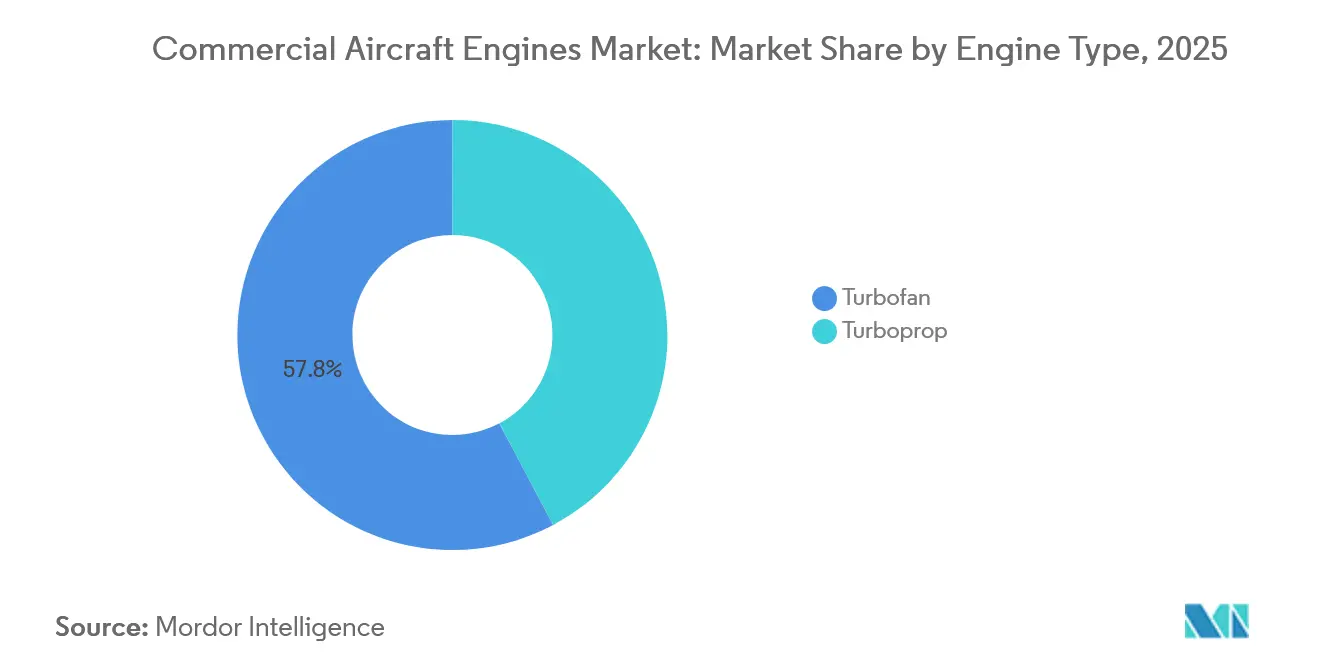

- By engine type, turbofan powerplants led with 57.76% commercial aircraft engines market share in 2025, while turboprops are forecast to post a 4.24% CAGR through 2031.

- By aircraft type, narrowbody installations accounted for 61.27% of the 2025 commercial aircraft engines market size, whereas regional-jet engines are expected to expand at a 5.3% CAGR through 2031.

- By technology, conventional turbofan/turboprop designs captured 38.45% of the 2025 share, and hybrid-electric propulsion is poised for the fastest growth at 5.21% through 2031.

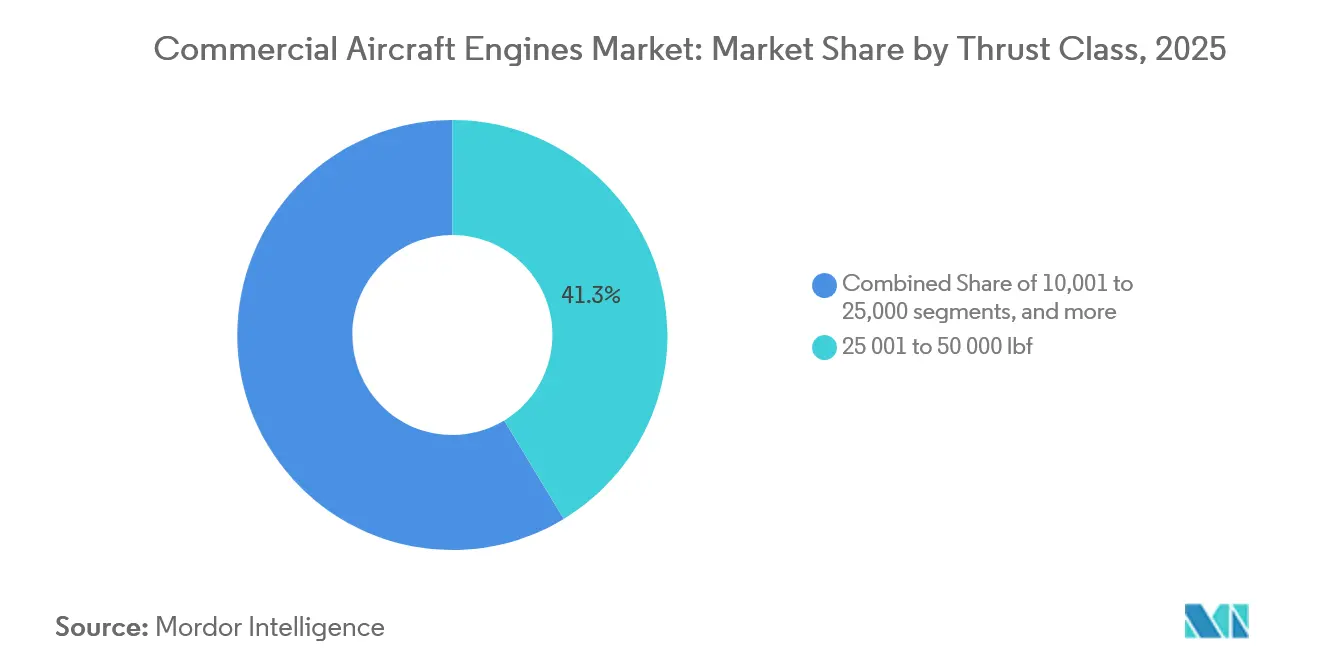

- By thrust class, the 25,001–50,000 lbf band commanded 41.34% share in 2025, and engines above 50,000 lbf are projected to grow at a 4.87% CAGR.

- By component, turbine sections accounted for a 45.87% share in 2025, while compressor modules are forecast to achieve a 4.21% CAGR over the outlook period.

- By end-user, OEM factory-fit engines represented 61.35% of demand in 2025, and the replacement/aftermarket channel is expected to accelerate at a 4.92% CAGR through 2031.

- By geography, the Asia-Pacific region captured 36.87% of the 2025 revenue, while North America is expected to register the fastest regional expansion at a 4.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Aircraft Engines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| APAC fleet expansion led by LCCs | +1.80% | Asia-Pacific core, spill-over to Middle East | Medium term (2-4 years) |

| Accelerated narrow-body replacement | +2.10% | Global, concentration in North America and Europe | Short term (≤ 2 years) |

| Ageing fleet pushing engine-MRO demand | +1.50% | Global, mature markets in North America and Europe | Long term (≥ 4 years) |

| Unscheduled PW1100G and LEAP shop-visit surge | +1.30% | Global, acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| OEM digital-twin subscription revenues | +0.90% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Long-term SAF-backed offtake agreements | +1.20% | North America and Europe, regulatory push | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Asia-Pacific Fleet Expansion Led by LCCs

Low-cost carriers in India, Vietnam, and Indonesia continue to order single-aisle aircraft at volumes that exceed historic delivery averages. IndiGo’s 500-unit A320neo family order and VietJet’s 100-unit A321neo commitment underscore a structural rise in passenger traffic in the region, prompting engine makers to pre-position MRO capacity in Bangalore, Ho Chi Minh City, and Jakarta. Daily utilization exceeding 12 hours accelerates hot-section wear, which pulls forward shop-visit schedules and stabilizes aftermarket demand. Engine suppliers are therefore earmarking narrowbody spare-engine pools for Asia-Pacific operators to mitigate dispatch reliability risks. The commercial aircraft engines market benefits from the fact that every frame requires two propulsion units, along with corresponding multi-year service agreements.[1]Airbus, “AirAsia orders 100 A321neo aircraft,” airbus.com

Accelerated Narrow-Body Replacement with Fuel-Efficient Engines

United Airlines, Southwest, and European carriers are retiring CFM56-7B and V2500-A5 engines well ahead of their economic life to capture 15-20% fuel-burn savings from LEAP-1B and PW1100G successors. Surging jet-fuel costs have sharpened payback periods, making rapid fleet turnover economically rational. Early retirements, however, inject a wave of used serviceable material into secondary parts channels, depressing OEM spare-part pricing and nudging engine makers to emphasize digital-service revenue. Accelerated replacements also compress certification timetables for thrust-rating changes, pressuring engineering teams but reinforcing the value proposition of next-generation engines. Consequently, commercial aircraft engines market players are bundling long-term power-by-the-hour contracts to lock in predictable margins.

Ageing Fleet Pushing Engine-MRO Demand

Global average fleet age reached 12.3 years in 2025. Airlines that deferred new-aircraft deliveries during the pandemic must now shoulder elevated maintenance liabilities, driving a 35% year-over-year rise in CFM56 shop visits at Lufthansa Technik. OEM and independent MRO expansions in Singapore, San Antonio, and Hamburg are targeting this backlog. At the same time, proprietary repair techniques such as high-pressure turbine-blade coatings allow certain shops to charge price premiums. The sustained maintenance intensity underpins a resilient aftermarket revenue floor even if new-build deliveries slow. As a result, the commercial aircraft engines market is deriving an increasing share of EBIT from overhaul activities rather than hardware sales.[2]Lufthansa Technik, “Q2 2025 shop-visit surge,” lufthansa-technik.com

Unscheduled PW1100G and LEAP Shop-Visit Surge

Powder-metal contamination in PW1100G turbine disks and premature combustor-liner wear on LEAP engines have prompted unexpected removals, resulting in the grounding of scores of A320neo and 737 MAX jets. OEM capacity constraints created overflow demand, which was captured by independents such as StandardAero, which opened a dedicated GTF repair line to absorb the excess work. Airlines negotiating risk-transfer clauses now place greater emphasis on guaranteed turnaround times and on-wing durability metrics, shrinking engine-sale margins by 150–200 basis points. In parallel, spare-engine leasing rates increased, prompting carriers to diversify their engine selections to hedge against availability risks. These knock-on effects reinforce the commercial aircraft engines market’s pivot to service-centric value capture.[3]StandardAero, “GTF repair line opens in San Antonio,” standardaero.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent forge and casting supply bottlenecks | -1.40% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Escalating certification and R&D costs | -0.90% | Global, regulatory burden in North America and Europe | Long term (≥ 4 years) |

| Powder-metal contamination grounding (GTF) | -1.10% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Coming CFM56 USM glut eroding aftermarket margins | -0.80% | Global, mature markets in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Forge and Casting Supply Bottlenecks

High-pressure turbine disks and nickel-alloy forgings remain the rate-limiting factor across LEAP and GTF production lines. GE Aerospace, Safran, and Pratt & Whitney have responded by acquiring equity stakes in forging houses and expanding their additive-manufacturing footprints, thereby bypassing capacity shortfalls for non-critical parts. Despite these measures, a 15-20% supply gap in 2025 delayed multiple engine shipments, compelling airframers to revise their delivery schedules. Medium-term relief hinges on new press capacity and the qualification of powder-metal billets, but vertical integration will likely increase capital intensity for prime contractors. This bottleneck keeps commercial aircraft engines market lead times extended into 2027.[4]Safran, “Safran acquires stake in Aubert & Duval,” safran-group.com

Escalating Certification and R&D Costs

FAA and EASA scrutiny of FADEC software and high-bypass architectures has lengthened certification cycles to 36 months, pushing CFM’s RISE program past USD 1.2 billion in cumulative R&D outlays. Only scale players with multi-billion-dollar cash flows can absorb such burdens, reinforcing market oligopoly. Smaller aspirants have shifted toward business-jet niches with lower regulatory thresholds. Elevated development costs raise entry barriers, but they also encourage platform exclusivity agreements that secure decades of spares revenue. Consequently, the commercial aircraft engines industry is concentrated around a handful of conglomerates that can amortize these investments across a broad installed base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type: Turbofan Dominance Meets Turboprop Resurgence

Turbofan platforms supplied 57.76% of 2025 revenue in the commercial aircraft engines market. Narrowbody variants, such as the LEAP-1A/B and PW1100G families, remain production workhorses, whereas widebody programs, like the Trent XWB and GE9X, underpin long-haul growth. Turboprops, however, are on a 4.24% CAGR trajectory as regional carriers refresh ATR 42/72 fleets with PW127XT-M powerplants that deliver 3% lower fuel burn and 50% cabin noise reduction.

Growth polarity is evident: developing economies favor turboprops for short-range connectivity, while network airlines in Europe retire Dash 8 fleets for high-capacity regional jets. OEMs respond by bundling fuel-efficiency upgrades with maintenance-cost caps to entice operators who balance capital expenditures (capex) and operating expenditures (opex) trade-offs. Engine manufacturers are increasingly promoting the readiness of sustainable aviation fuel, even in the turboprop segment, to future-proof asset values. As such, the commercial aircraft engines market continues to diversify propulsion portfolios to cover both jet-dense and prop-centric route structures.

By Aircraft Type: Narrowbody Supremacy, Regional Jet Acceleration

Narrowbody engines represented 61.27% of the 2025 commercial aircraft engines market share on the back of A320neo and 737 MAX deliveries. Regional-jet engines, though smaller in unit value, are set for a 5.3% CAGR as Embraer’s E2 family gains traction among carriers serving thin routes where widebodies or high-capacity single-aisles are uneconomical.

Fleet planners in Southeast Asia and Latin America prefer sub-150-seat jets to balance load factors and frequency, boosting PW1700G and PW1900G demand. Conversely, fleet densification in North America sees major airlines up-gauging to A321neo, requiring marginal thrust enhancements. Such dual dynamics sustain a healthy pipeline for both large and small thrust classes within the commercial aircraft engines market, ensuring balanced aftermarket workloads.

By Technology: Conventional Architectures Persist, Hybrid-Electric Emerges

Conventional turbofan/turboprop designs secured 38.45% of 2025 revenue, reflecting the vast in-service CFM56, V2500, and PW100 fleets. Hybrid-electric demonstrators, however, hold the highest growth outlook at 5.21% as NASA’s X-57 and Collins Aerospace’s 1-MW motor validate distributed propulsion concepts.

Regulatory uncertainty persists: EASA standards for electric systems exceeding 500 kW remain under development, potentially delaying the entry into service of large aircraft. Still, OEMs hedge with incremental technology, gear systems, CMC internals, and open-fan designs, to secure double-digit efficiency gains absent full electrification. This measured path maintains a robust conventional backlog while positioning the commercial aircraft engines market for a smoother transition once certification guardrails mature.

By Thrust Class: Mid-Range Dominance, Ultra-High-Thrust Growth

Engines rated 25,001–50,000 lbf delivered 41.34% of 2025 revenue and anchor the commercial aircraft engines market size for single-aisle programs. The greater than 50,000 lbf bracket is forecast to grow at a 4.87% CAGR, driven by orders for the GE9X and Trent XWB-97 engines supporting the 777X and A350-1000 fleets.

Ultra-high-thrust programs form a strategic moat, as metallurgical hurdles lock out newcomers. Meanwhile, the 10,001–25,000 lbf category retains relevance for regional jets and large turboprops, ensuring balanced industrial loading across facilities. OEMs therefore maintain dual competencies, servicing both high-volume, mid-thrust engines and capital-intensive, widebody giants within the commercial aircraft engines market.

By Engine Component: Turbine Sections Lead, Compressor Modules Accelerate

Turbine hardware comprised 45.87% of 2025 revenue, underscoring the cost concentration in single-crystal blades operating above 1,600 °C. Compressor assemblies are projected to grow at a 4.21% CAGR as additive manufacturing trims weight by 15% on LEAP modules and slashes lead times by 40%.

CMC adoption in nozzles and shrouds raises thermal ceilings, allowing for hotter core temperatures and improved fuel burn without the need for exotic alloys. Gearboxes unique to PW1000G engines remain a niche but commercially crucial subset, delivering 12% higher bypass ratios. Collectively, these advances enhance durability and efficiency, sustaining aftermarket revenue as each upgrade cascades through the installed commercial aircraft engines base.

By End-User: OEM Factory-Fit Leads, Aftermarket Surges

Factory-fit shipments accounted for 61.35% of 2025 demand thanks to record Airbus and Boeing narrowbody output. The replacement/aftermarket channel, however, is advancing at a 4.92% CAGR as power-by-the-hour arrangements shift maintenance risk from operators to OEMs. Rolls-Royce’s TotalCare covered 70% of its Trent fleet in 2025, delivering greater than 20% EBIT margins.

Independents, such as Lufthansa Technik and ST Engineering, leverage used, serviceable material to undercut OEM shops by 20-30% on mature engines. This competition intensifies pricing pressure yet broadens service accessibility, reinforcing the commercial aircraft engines market’s transition toward lifecycle-service economics over hardware margins.

Geography Analysis

Asia-Pacific generated 36.87% of 2025 revenue for the commercial aircraft engines market, anchored by IndiGo’s and VietJet’s blockbuster A320neo orders that drove engine demand exceeding USD 30 billion. Fleet expansion responds to rising middle-class travel and liberalized air-service agreements, compelling OEMs to invest in localized MRO hubs to secure future maintenance, repair, and overhaul (MRO) streams.

North America is projected to record a 4.55% CAGR through 2031, as United Airlines, American Airlines, and Delta Air Lines collectively firm more than 500 single-aisle orders in 2025. The trend is replacement-driven: carriers retire CFM56-powered 737-800s to capitalize on LEAP-1B fuel efficiency, simultaneously releasing used, serviceable material that reshapes parts pricing. Europe, with a 24% share in 2025, benefits from Toulouse- and Hamburg-centric Airbus output, while Wizz Air’s diversification to LEAP engines exemplifies risk-mitigation strategies amid PW1100G supply issues.

The Middle East contributes a significant share of revenue, but widebody weighting lifts ASPs: Emirates’ 205-unit 777X deal alone underwrites USD 15 billion in GE9X business. South America and Africa remain small yet strategic, favoring turboprops and regional jets for short-haul connectivity; Azul’s ATR 72-600 purchase illustrates this niche. China, representing 18% of the Asia-Pacific market, pursues self-sufficiency via AECC’s CJ-1000A, signaling a potential bifurcation of global supply chains post-2028. Mature US fleets generate outsized aftermarket volumes, reinforcing North America’s status as the commercial aircraft engines market’s service revenue anchor.

Competitive Landscape

The commercial aircraft engines market operates in a highly concentrated market. CFM International and Pratt & Whitney control a significant share of narrowbody propulsion, while Rolls-Royce dominates A350 widebody applications, and GE Aerospace anchors 777X powerplants. Competition is shifting from marginal fuel-burn deltas to digital-service monetization: GE’s Flight Deck and Pratt & Whitney’s eFAST platforms command subscription fees of USD 50k–100k per aircraft and deliver margins of 35-40%, surpassing hardware returns.

Supply-chain resilience strategies differentiate players. Safran’s stake in Aubert & Duval secures forging capacity, and GE’s additive-manufacturing ramp accelerates LEAP output. Meanwhile, hybrid-electric entrants, such as Collins Aerospace, target the 19- to 50-seat segment, posing a long-term challenge to incumbent turboprop suppliers. China’s AECC invests USD 5 billion to field the CJ-1000A, potentially fracturing market geography into Western and Chinese spheres by 2030.

Independent MROs are emerging as formidable competitors. Lufthansa Technik leverages proprietary repair IP to win shop visits, and StandardAero capitalizes on overflow from OEM bottlenecks. These firms utilize cost-advantaged USM sourcing to price aggressively, compelling OEMs to sweeten power-by-the-hour terms or risk erosion of their market share. Consequently, strategic partnerships, vertical integration, and digital ecosystems define the next phase of rivalry within the commercial aircraft engines market.

Commercial Aircraft Engines Industry Leaders

Safran SA

Pratt & Whitney (RTX Corporation)

CFM International

Rolls-Royce PLC

GE Aerospace

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Pegasus Airlines has entered into an agreement with CFM International for up to 300 LEAP-1B engines, including spare units and long-term maintenance services. These engines will power its future 737-10 fleet and support the airline's objectives for fuel efficiency and emissions reduction.

- June 2025: Airbus and MTU Aero Engines signed a Memorandum of Understanding (MoU) at the Paris Airshow to collaborate on advancing hydrogen fuel-cell propulsion. This partnership aims to support the development of fully electric, hydrogen-powered aircraft under Airbus' ZEROe initiative.

Global Commercial Aircraft Engines Market Report Scope

This report examines the global commercial aircraft engines market, focusing on the design, manufacturing, integration, delivery, and aftermarket support of engines that provide thrust during taxi, takeoff, cruise, and landing operations for commercial aircraft. The market encompasses turbofan and turboprop engines used in narrow-body, wide-body, and regional aircraft, along with their critical subsystems, including fans, compressors, combustors, turbines, gearboxes, nozzles, and electronic control systems.

The study evaluates both OEM factory-fit engines and replacement/aftermarket engines and services, driven by factors such as fleet expansion, fuel-efficiency upgrades, regulatory compliance, and increasing maintenance, repair, and overhaul (MRO) requirements.

The report provides market size and growth forecasts (in USD value) segmented by aircraft type (narrowbody, widebody, and regional aircraft), engine type (turbofan and turboprop engines), engine component (compressor, turbine, nozzle, gearbox, and other components), thrust class (less than 10,000 lbf, 10,001–25,000 lbf, 25,001–50,000 lbf, and greater than 50,000 lbf), end-user (OEM factory-fit and replacement/aftermarket engines), technology (conventional turbofan/turboprop, geared turbofan, contra-rotating open rotor, and hybrid-electric propulsion), and geography (North America, South America, Europe, Asia-Pacific, the Middle East, and Africa, with detailed country-level analysis). The report also evaluates value-chain dynamics, regulatory and technological developments, competitive intensity, and strategic initiatives undertaken by leading engine OEMs and MRO providers.

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Aircraft |

| Turbofan |

| Turboprop |

| Compressor |

| Turbine |

| Nozzle |

| Gearbox |

| Other Components (Fan, Combustor,FADEC and Control Electronics, etc.) |

| Less than 10,000 |

| 10,001 to 25,000 |

| 25,001 to 50,000 |

| Greater than 50,000 |

| OEM Factory-Fit |

| Replacement/Aftermarket |

| Conventional Turbofan/Turboprop |

| Geared Turbofan (GTF) |

| Contra-Rotating Open Rotor |

| Hybrid-Electric Propulsion |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional Aircraft | |||

| By Engine Type | Turbofan | ||

| Turboprop | |||

| By Engine Component | Compressor | ||

| Turbine | |||

| Nozzle | |||

| Gearbox | |||

| Other Components (Fan, Combustor,FADEC and Control Electronics, etc.) | |||

| By Thrust Class | Less than 10,000 | ||

| 10,001 to 25,000 | |||

| 25,001 to 50,000 | |||

| Greater than 50,000 | |||

| By End-User | OEM Factory-Fit | ||

| Replacement/Aftermarket | |||

| By Technology | Conventional Turbofan/Turboprop | ||

| Geared Turbofan (GTF) | |||

| Contra-Rotating Open Rotor | |||

| Hybrid-Electric Propulsion | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the commercial aircraft engine market in 2031?

It is forecast to reach USD 117.13 billion, rising from USD 98.86 billion in 2026 on a 3.45% CAGR.

Which engine type holds the largest share today?

Turbofan powerplants account for 57.76% of 2025 revenue, reflecting their dominance on single-aisle and twin-aisle aircraft.

Which geographic region is expected to grow the fastest through 2031?

North America leads with a 4.55% CAGR, driven by fleet replacement orders from major US carriers.

Why are hybrid-electric engines attracting interest?

Demonstrators show double-digit fuel-burn cuts for sub-regional aircraft, positioning the technology for future carbon-reduction mandates.

How are OEMs responding to supply-chain bottlenecks?

They are vertically integrating forging capacity and expanding additive-manufacturing lines to secure turbine-disk and compressor-part output.

Page last updated on: