Aircraft Computers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

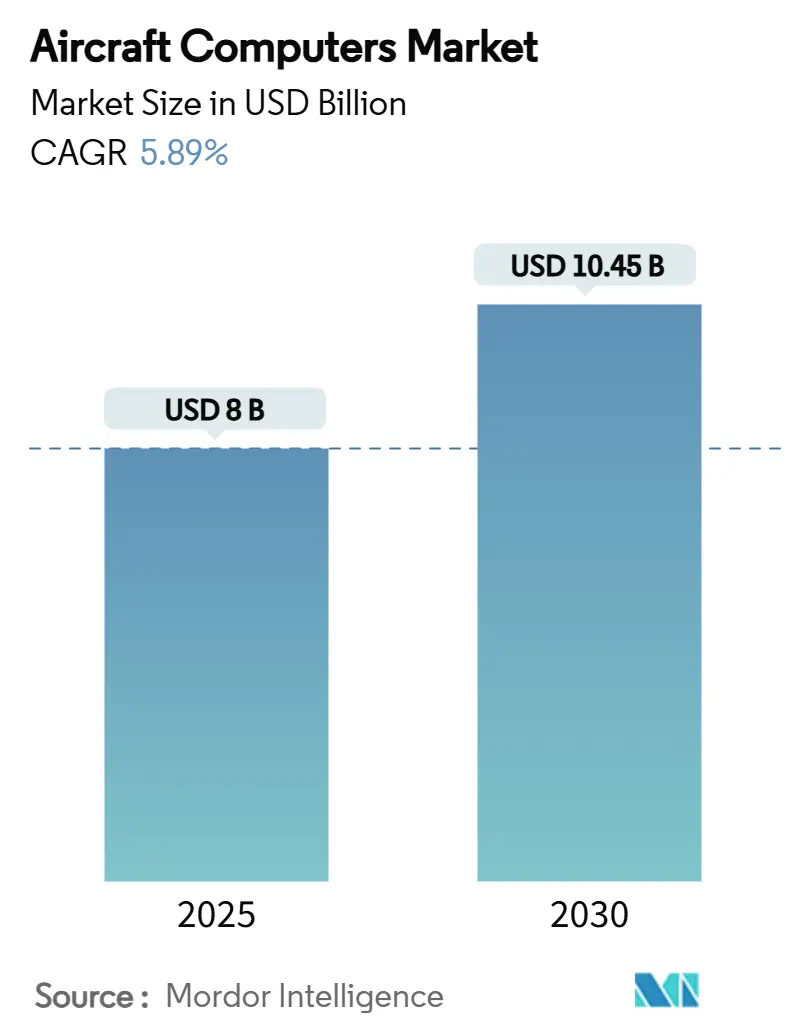

| Market Size (2025) | USD 8 Billion |

| Market Size (2030) | USD 10.45 Billion |

| Growth Rate (2025 - 2030) | 5.89% CAGR |

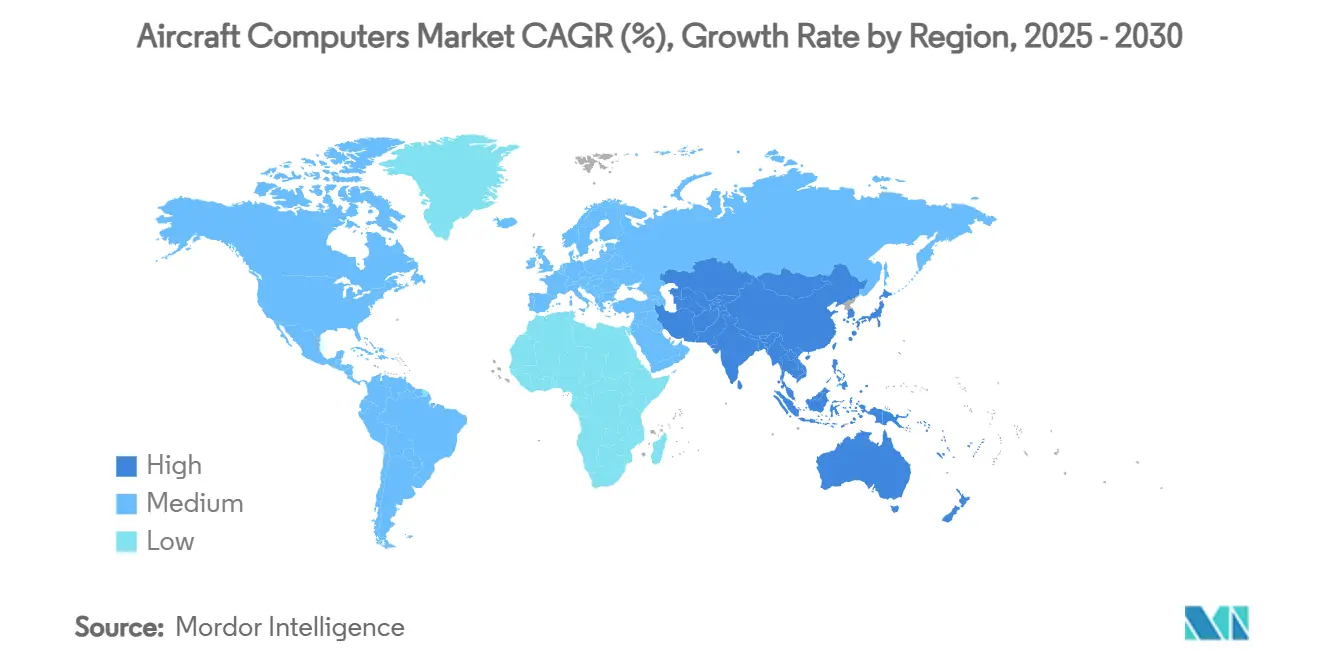

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Computers Market Analysis by Mordor Intelligence

The aircraft computers market size stands at USD 8.00 billion in 2025 and is forecasted to reach USD 10.65 billion by 2030, advancing at a steady 5.89% CAGR. Escalating aircraft build rates, mandatory avionics-modernization programs, and airlines’ rapid shift toward data-centric flight operations underpin this multi-year expansion. North America’s backlog of single-aisle jets provides near-term volume, while Asia-Pacific’s rising passenger traffic and defense procurements ramp the long-term revenue base. Innovations in open-systems architectures, edge-AI processors, and more-electric-aircraft (MEA) power management expand computer content per airframe. Meanwhile, supply-chain reshoring for radiation-hardened semiconductors and stricter cybersecurity rules reshape sourcing strategies and competitive positioning across the aircraft computers market.

Key Report Takeaways

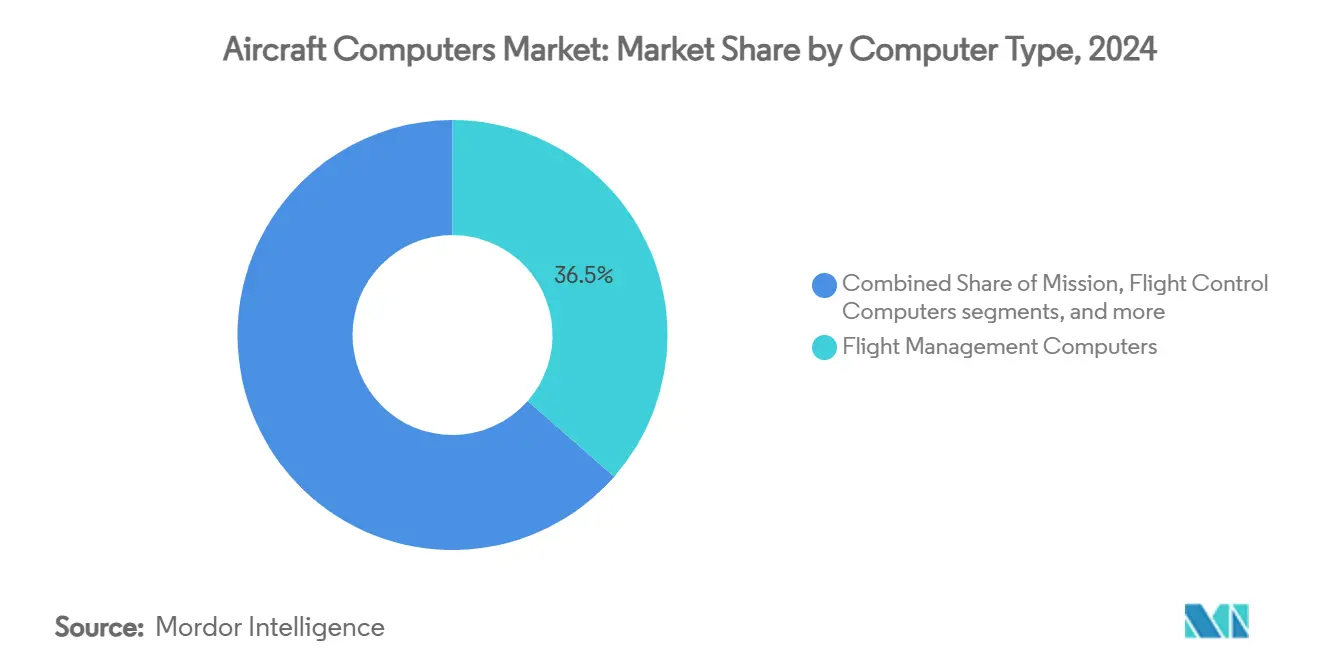

- By computer type, flight management computers led 36.45% of the aircraft computers market share in 2024, whereas mission computers posted the fastest 7.89% CAGR through 2030.

- By aircraft type, fixed-wing platforms accounted for 71.87% of the aircraft computers market size in 2024, while unmanned aerial vehicles (UAVs) recorded the highest 8.60% CAGR to 2030.

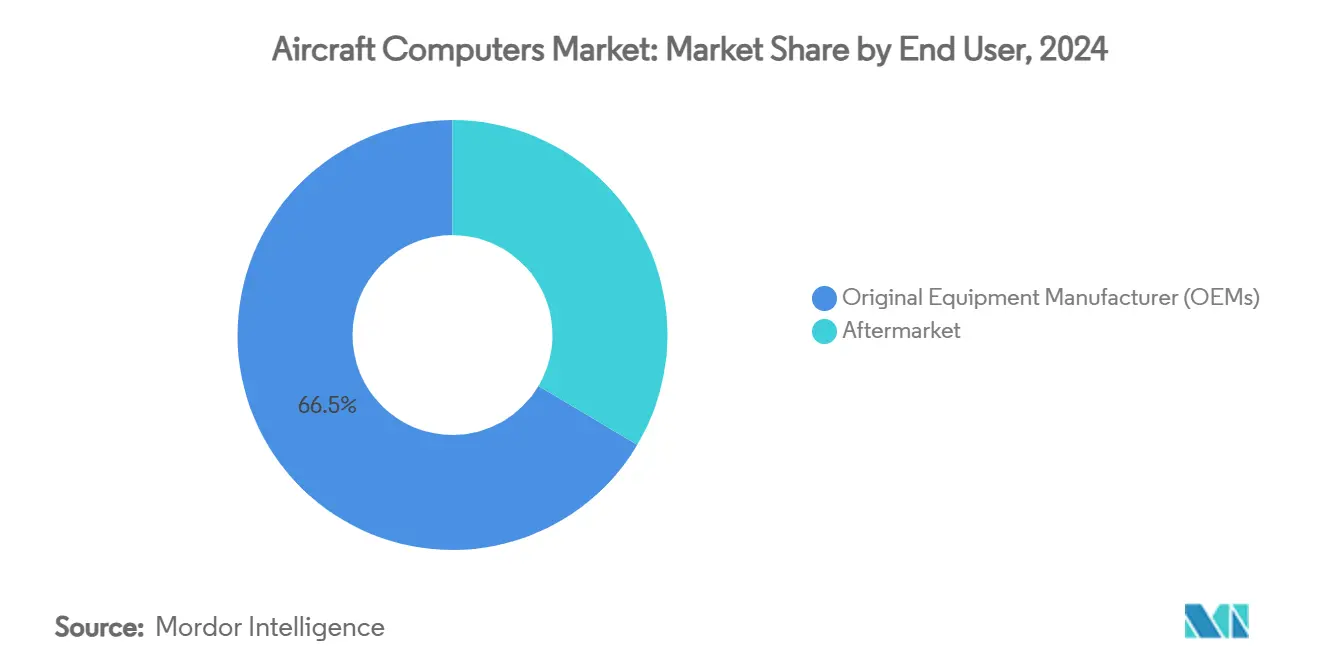

- By end user, OEMs captured 66.47% of demand in 2024, and the aftermarket segment is projected to expand at a 7.10% CAGR between 2025 and 2030.

- By component, hardware held an 82.35% share of the aircraft computers market in 2024; software is advancing at an 8.04% CAGR through the decade's end.

- By geography, North America represented 41.54% revenue in 2024, but Asia-Pacific is set to grow at a 7.68% CAGR and narrow the gap by 2030.

Global Aircraft Computers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aircraft production rebound post-COVID | +1.2% | North America, Europe | Short term (≤ 2 years) |

| NextGen and SESAR avionics compliance deadlines | +0.9% | United States and European Union | Medium term (2-4 years) |

| Rapid shift to More-Electric-Aircraft architectures | +0.8% | Global commercial aviation | Long term (≥ 4 years) |

| Fleet modernization and retrofit demand | +0.7% | Asia-Pacific and global fleets | Medium term (2-4 years) |

| AI-enabled predictive maintenance boosts onboard processing | +0.6% | North America and EU, spreading Asia | Medium term (2-4 years) |

| UAV proliferation requires lightweight mission computers | +0.5% | Global, defense-driven | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aircraft Production Rebound Post-COVID

Boeing’s delivery of 150 jetliners in Q2 2025, its strongest quarterly tally since 2018, and Airbus’s plan to hand over 820 aircraft in 2025 mark a decisive production resurgence that forces avionics suppliers to accelerate capacity.[1]Source: Airbus, “Global Market Forecast 2025-2043,” airbus.com Each additional airframe contains several safety-critical computers, and higher build rates squeeze inventories of certified line-replaceable units. Airlines simultaneously demand lower fuel burn and streamlined maintenance, so new platforms specify multi-core processors capable of optimizing trajectories, monitoring engine health, and balancing electrical loads in real time. Shorter delivery cycles, therefore, privilege manufacturers with in-house DO-178C design, testing, and documentation expertise, reinforcing incumbent advantages.

NextGen and SESAR Avionics Compliance Deadlines

The FAA and EASA require every IFR aircraft to support ADS-B, CPDLC, and ACAS Xa by 2029, turning regulatory calendars into non-negotiable upgrade schedules.[2]Source: Federal Aviation Administration, “ADS-B & CPDLC Compliance Bulletin,” faa.gov Operators must replace legacy boxes with integrated computers that fuse surveillance, navigation, and datalink tasks while meeting deterministic-latency rules. Capital budgets are already allocated, insulating demand for flight, mission, and display processors from typical traffic downturns. Certification timelines push OEMs toward modular hardware and field-loadable software, enabling future standard updates without extensive recertification. Suppliers offering partitioned operating systems and pre-qualified datalink protocols gain preference because they reduce downtime and engineering risk for fleet managers

Rapid Shift to More-Electric-Aircraft Architectures

Commercial and military programs increasingly replace hydraulic or pneumatic systems with electrically driven actuators, landing-gear motors, and environmental-control compressors, doubling average cruise-phase power draw on wide-bodies. Collins Aerospace verified its Enhanced Power and Cooling System in February 2025, providing twice the thermal headroom demanded by F-35 avionics refresh packages. Higher voltage distribution raises heat, electromagnetic interference, and load-balancing challenges. Hence, aircraft now specify power-management computers that execute microsecond-level switching, predictive current limiting, and real-time fault isolation. Vendors embed silicon-carbide power modules, model-based control firmware, and digital twin analytics to keep electrical efficiency high while protecting wiring and batteries from transient spikes.

AI-Enabled Predictive Maintenance Boosts Onboard Processing

In 2025, the FAA cleared airlines to replace calendar inspections with data-driven predictive maintenance programs, legitimizing machine-learning models anticipating component failures. Mission computers ingest terabytes of vibration, temperature, and flight-control data daily, run neural-network inference locally, and transmit condensed health reports to ground stations for decision support. Higher memory bandwidth, redundant encryption engines, and secure boot loaders become baseline specifications. Airlines using these systems report lower unscheduled maintenance and reduced spare-parts inventory, converting IT investment into day-to-day operating savings. Hardware makers bundle over-the-air software updates and analytics subscriptions, creating recurring revenue streams beyond initial equipment sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High DO-178C certification cost and schedule risk | -0.8% | Global, small and mid-tier suppliers | Long term (≥ 4 years) |

| Cyclical air-transport demand shocks | -0.6% | Global, tourism-dependent regions | Short term (≤ 2 years) |

| Radiation-hardened semiconductor supply bottlenecks | -0.5% | United States, European Union | Medium term (2-4 years) |

| Escalating avionics-cybersecurity compliance burden | -0.4% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High DO-178C Certification Cost and Schedule Risk

Bringing 100,000 lines of critical avionics code to Design Assurance Level A can add USD 2.5 million–10 million in verification expense and stretch development timelines by 12–18 months.[3]Source: Synopsys, “Cost of DO-178C Compliance,” synopsys.com Documentation, traceability, structural-coverage analysis, and tool qualification consume specialist labor, creating a fixed overhead that discourages new entrants. Airlines often favor suppliers with proven certification track records because delays jeopardize fleet-upgrade schedules. Consequently, the financial burden consolidates market share among large incumbents that amortize process infrastructure across multiple product lines. Smaller firms mitigate by partnering with authorized representatives or targeting less stringent DAL C or D applications in cabins and galleys.

Escalating Avionics-Cybersecurity Compliance Burden

The FAA’s 2023 Aircraft Systems Information Security Protection order obliges every network-connected avionics computer to undergo threat analysis, penetration testing, and life-cycle patch management. Compliance adds specialist engineering hours, cryptographic key-management infrastructure, and continuous monitoring costs that can erode pricing flexibility for low-margin suppliers. Airlines also must schedule periodic software uploads, placing a premium on secure bootloaders and remote-update architectures. Manufacturers delivering hardware root-of-trust, encrypted data buses, and federated logging satisfy audit requirements faster, gaining competitive leverage. Conversely, vendors lacking dedicated cybersecurity teams face longer certification queues and risk being excluded from regulated airspace approvals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Computer Type: Mission Platforms Command Growth Potential

Flight management computers retained 36.45% of the aircraft computer market share in 2024, owing to line-fit dominance across commercial jets and business aircraft. Mission computers, however, confront the highest 7.89% CAGR on the strength of defense modernization and UAV integration. The aircraft computer market size tied to mission systems is expected to climb steadily as open-systems standards simplify multi-domain integration.

Mercury Systems’ SOSA-ready 3U VPX cards deliver 40× performance uplift at half the power draw, demonstrating the leap in edge-AI capability demanded by next-generation strike and surveillance aircraft. Meanwhile, Collins Aerospace’s Mosarc architecture merges flight-control, engine, and tactical apps onto partitioned multicore processors, reducing LRU count and saving weight. Suppliers that pre-qualify such hardware/software stacks to DAL C for UAVs and DAL A for crewed jets occupy a compelling competitive niche in the aircraft computers market.

By Aircraft Type: UAV Momentum Reshapes Demand Mix

Fixed-wing aircraft generated 71.87% of 2024 revenue, yet UAVs posted the fastest 8.60% CAGR. Growing autonomy requirements and swarm-control logic push computer density upward, enlarging the aircraft computers market size for low-SWaP boards. Multi-core SoCs operating at extended temperature ranges serve MALE drones and tactical loitering munitions.

Conversely, commercial narrowbody programs remain volume anchors. As Boeing and Airbus climb toward 75-80 monthly units on B737 MAX and A320neo lines, every production-rate increase of a single unit per month equates to roughly USD 15-20 million in incremental annual computer demand. Widebody recovery further elevates dollar content since each twin-aisle hosts more redundant computer channels.

By End User: Retrofit Cycle Boosts Aftermarket

OEM line-fit retained 66.47% spending in 2024, but the aftermarket grew 7.10% annually as carriers pursued life-extension upgrades rather than wholesale replacement. Airlines favor plug-and-play retrofit kits that cut downtime to under five days. Computer vendors holding parts-manufacturer approvals capture lucrative spares revenue, cementing long-tail cash flows across the aircraft computers market.

Simultaneously, the OEM segment benefits from new program launches such as eVTOL air taxis and regional turboprop replacements. Each platform selection often locks the chosen computer supplier into a 15 to 20-year production run, reinforcing the importance of early design-in wins.

By Component: Software Value Pool Expands

Hardware still commands 82.35% of 2024 billings, yet software accelerates at 8.04%. FAA clearance of multi-core processors in 2024 unlocked partitioned operating systems capable of mixing DAL A flight functions with DAL D passenger-Wi-Fi services on shared silicon. Vendors now monetize recurring license fees, predictive analytics subscriptions, and cybersecurity-patch contracts.

Hardware suppliers respond by embedding secure boot, cryptographic accelerators, and hardware root-of-trust to meet Part ISAC specifications. The co-design imperative fosters strategic alliances between chipmakers and avionics primes, changing value-capture patterns across the aircraft computers market.

Geography Analysis

North America retains a 41.54% share and remains the most significant regional contributor. Robust defense spending underpins high-margin mission-computer demand for programs such as F-35, KC-46, and new-generation uncrewed aircraft. Simultaneously, FAA NextGen mandates drive steady retrofit volumes across legacy commercial fleets. Semiconductor-industrial-policy grants worth USD 49 billion strengthen local access to radiation-hardened processors, reducing geopolitical supply risk. Agile certification pipelines and a dense ecosystem of DERs further buttress regional competitiveness in the aircraft computers market.

Asia-Pacific exhibits the highest 7.68% CAGR, propelled by double-digit passenger-traffic growth, state-backed airline expansion, and defense modernization in China, India, Japan, and South Korea. Airbus projects the region’s aircraft-services outlay will more than double, from USD 52 billion in 2024 to USD 129 billion by 2043. Indigenous programs like China’s C919 and India’s AMCA embed domestic computing content, while local eVTOL start-ups tap urban-air-mobility budgets. Regulators increasingly align with global safety and cybersecurity practices, creating new certification consulting revenue inside the aircraft computers market.

Europe maintains mid-single-digit growth, sustained by SESAR compliance and Airbus widebody production hikes. Environmental regulations accelerate MEA research, spurring demand for advanced power-distribution computers. Defence budgets edge toward 2% of GDP across NATO members, funding Eurofighter upgrades and the FCAS next-gen fighter. These programs stipulate modular open-systems architectures, opening procurement doors to second-tier suppliers specialized in encryption or AI accelerators. However, the continent’s strict data-protection laws raise certification hurdles for connected avionics and moderately slow time-to-market.

Competitive Landscape

The aircraft computers market remains moderately consolidated. Honeywell, Collins Aerospace (RTX), Thales, BAE Systems, and Safran are some of the key players in the market. Their advantage lies in decades-long DO-178C track records, vertically integrated design-to-certification pipelines, and exclusive line-fit positions on high-volume aircraft families.

Strategic focus shifts from proprietary black-box LRUs to open-systems ecosystems. Collins Aerospace’s Mosarc and Honeywell’s Anthem embed modular slots and common virtualization layers, allowing airlines to upgrade processing power without swapping entire racks. Partnerships with semiconductor leaders such as NXP and AMD speed AI accelerator insertion. To address cybersecurity mandates, market leaders incorporate hardware-root-of-trust and support over-the-air patch management, locking customers into multi-year service contracts and reinforcing share within the aircraft computers market.

White-space competition emerges around UAV mission computers, predictive maintenance analytics, and safety-certified edge AI coprocessors. Niche suppliers leverage SOSA standards to insert hardware into defense programs as plug-in cards rather than full LRUs. Established primes respond with targeted acquisitions: Honeywell extended its pact with Vertical Aerospace on the VX4 eVTOL, while Collins Aerospace secured a USD 80 million US Army Black Hawk upgrade contract. These moves illustrate how incumbents protect their installed base yet remain agile enough to capture emerging demand pockets that collectively lift overall aircraft computers market revenues.

Aircraft Computers Industry Leaders

Honeywell International Inc.

RTX Corporation

Thales Group

Safran SA

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Northrop Grumman Corporation was awarded a USD 20.4 million contract to supply 63 upgraded FlightPro Gen III mission computers for allied attack and utility helicopters. The US Naval Air Systems Command has tasked Northrop Grumman's Mission Systems division to deliver these for AH-1Z and UH-1Y helicopters in Nigeria, the Czech Republic, and Bahrain.

- August 2024: Boeing selected BAE Systems to upgrade the fly-by-wire (FBW) flight control computers (FCC) for the F-15EX Eagle II and F/A-18E/F Super Hornet fighter jets. These FCCs, featuring common core electronics, enhance the quad-redundant FBW flight control systems (FCS) to deliver the safety, reliability, and performance required for advanced missions.

- May 2024: Airbus contracted German avionics specialist Aircraft Electronic Engineering GMBH (AEE) to produce special mission computers for its H145 and H145M helicopters. In 2020, AEE developed the first prototype, IDEFIX, and now the second generation enters series production. AEE also created SONAF, ensuring secure communication for the H145M military variant.

Global Aircraft Computers Market Report Scope

| Flight Management Computers |

| Flight Control Computers |

| Mission Computers |

| Engine/FADEC Computers |

| Utility and Environmental Control Computers |

| Display Processing Computers |

| Fixed-Wing Aircraft | Commercial | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Military | Fighter Jets | |

| Transport Aircraft | ||

| Special-Mission Aircraft | ||

| General Aviation | Piston and Turboprops | |

| Business Jets | ||

| Rotorcraft | Civil Helicopters | |

| Military Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| Original Equipment Manufacturer (OEMs) |

| Aftermarket |

| Hardware |

| Software |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Computer Type | Flight Management Computers | ||

| Flight Control Computers | |||

| Mission Computers | |||

| Engine/FADEC Computers | |||

| Utility and Environmental Control Computers | |||

| Display Processing Computers | |||

| By Aircraft Type | Fixed-Wing Aircraft | Commercial | Narrowbody |

| Widebody | |||

| Regional Jets | |||

| Military | Fighter Jets | ||

| Transport Aircraft | |||

| Special-Mission Aircraft | |||

| General Aviation | Piston and Turboprops | ||

| Business Jets | |||

| Rotorcraft | Civil Helicopters | ||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By End User | Original Equipment Manufacturer (OEMs) | ||

| Aftermarket | |||

| By Component | Hardware | ||

| Software | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current aircraft computers market size?

The aircraft computers market stands at USD 8 billion in 2025 and is projected to reach USD 10.65 billion by 2030.

How fast is the aircraft computers market expected to grow?

It is forecasted to expand at a 5.89% CAGR over the 2025-2030 period.

Which computer type shows the strongest growth?

Rising airline orders, defense modernization, and a doubling aircraft-services spend propel a 7.68% CAGR.

How do DO-178C certification costs influence competition?

Certification expenses of up to USD 10 million per 100,000 lines of code create high entry barriers, favoring incumbents with established engineering infrastructure.

What technological shift most influences future demand?

The move toward MEA architectures and edge-AI predictive maintenance sharply increases onboard processing needs, generating new design-win opportunities for high-performance computers.

Page last updated on: