Aircraft Heat Exchanger Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 3.09 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Heat Exchanger Market Analysis by Mordor Intelligence

The aircraft heat exchanger market size is expected to grow from USD 1.85 billion in 2025 to USD 2.08 billion in 2026 and is forecast to reach USD 3.09 billion by 2031, at an 8.24% CAGR over 2026-2031. Production normalization across commercial programs, ongoing electrification of aircraft subsystems, and maturing hydrogen-electric demonstrators are shaping steady unit demand and raising thermal performance baselines in the aircraft heat exchanger market. Airlines and MRO networks continue to prioritize environmental control system upgrades to meet tighter cabin air-quality expectations and fuel-efficiency targets, which keeps retrofit pipelines active through the decade in the aircraft heat exchanger market. Additive manufacturing (AM) enables microchannel geometries and topology-optimized cores that increase heat rejection per unit mass and volume, improving packability and reducing drag penalties in the aircraft heat exchanger market. Megawatt-scale electrified powertrains and advanced fuel-cell systems expand the design space for high-temperature, high-flux exchangers, turning thermal management into a core enabler rather than a commodity in the aircraft heat exchanger market.

Key Report Takeaways

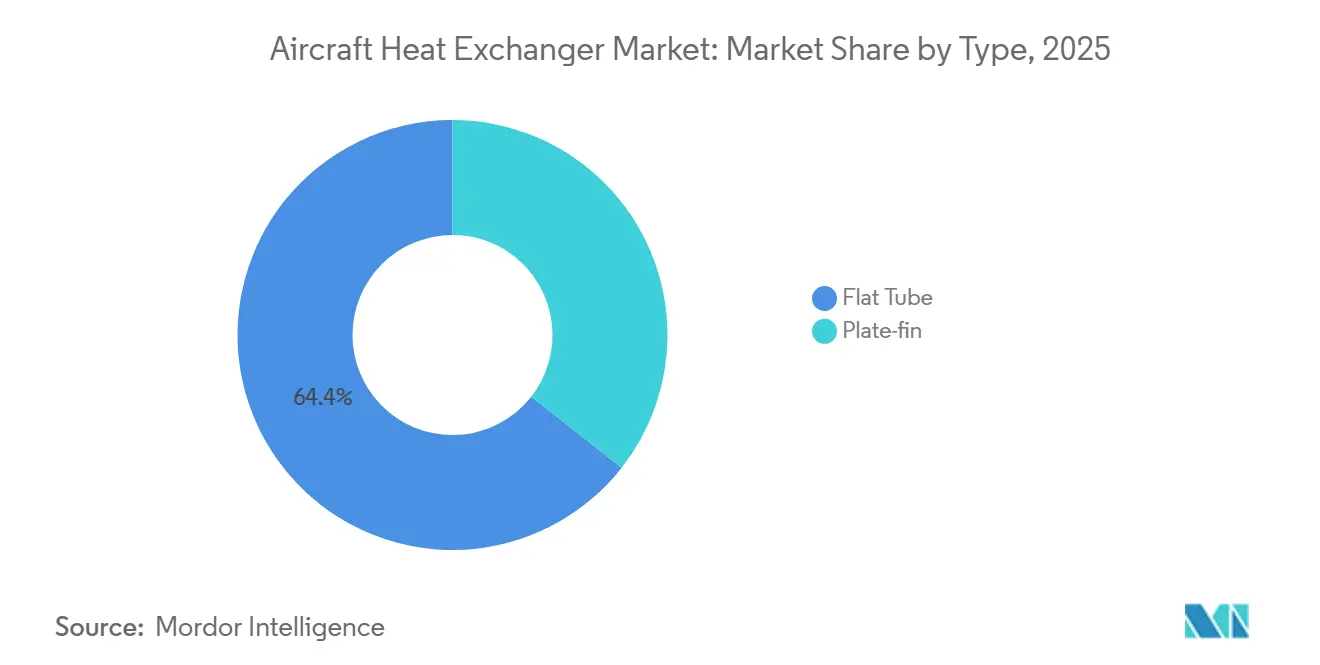

- By type, flat-tube heat exchangers held 64.42% of the aircraft heat exchanger market share in 2025 and are projected to advance at an 8.80% CAGR through 2031.

- By platform, fixed-wing aircraft held a 69.72% share of the aircraft heat exchanger market in 2025 while expanding at an 8.97% CAGR.

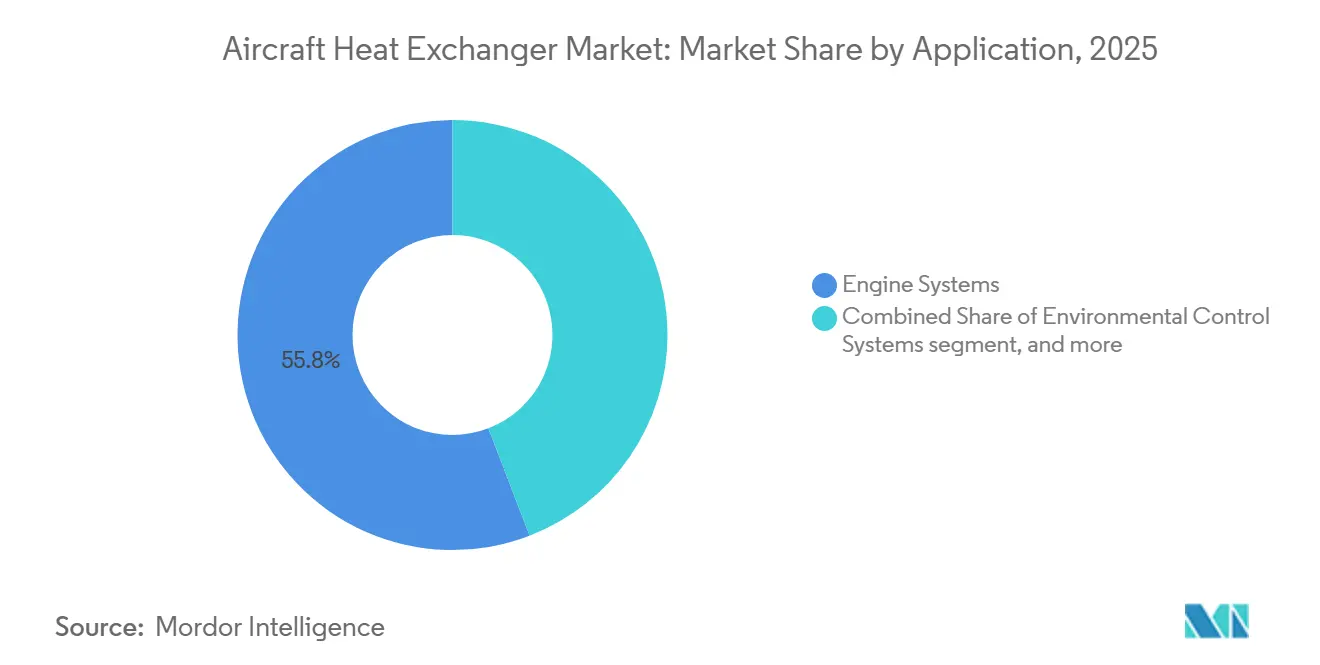

- By application, engine systems retained a 55.84% share in 2025, whereas environmental control systems are projected to grow at the fastest pace of 8.78% CAGR through 2031.

- By vendor, OEM sales represented 64.96% of 2025 revenue; aftermarket services are growing at the fastest rate, with a 9.02% CAGR through 2031.

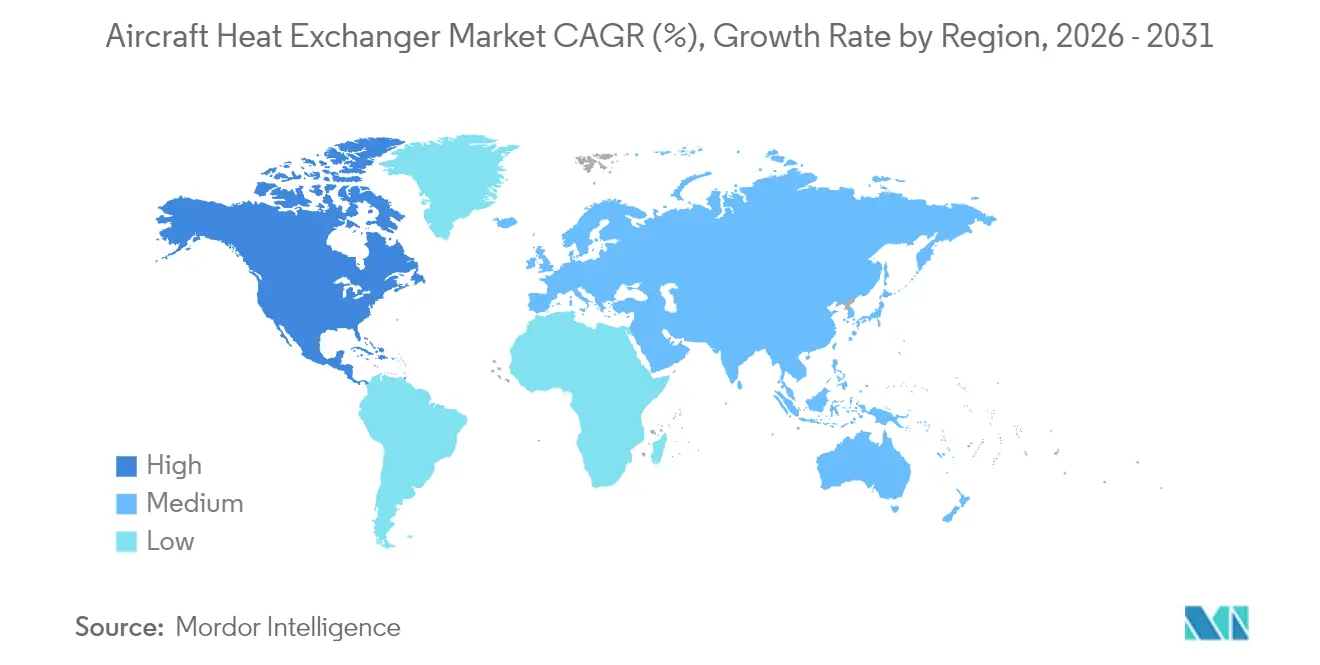

- By geography, North America commanded a 39.88% share of the aircraft heat exchanger market in 2025 and registered the highest CAGR of 9.21% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Heat Exchanger Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ramp-up in narrowbody and regional jets production | +2.1% | Global, with early gains in North America and Europe, and Asia-Pacific spillover | Medium term (2–4 years) |

| Fleet-wide ECS retrofit programs for cabin air-quality | +1.8% | Global, accelerated in EASA and FAA jurisdictions post-2024 guidance | Short term (≤ 2 years) |

| Shift to high-temperature ceramic HX materials | +1.4% | North America and EU R&D hubs, with production scaling in Asia-Pacific | Long term (≥ 4 years) |

| Hydrogen-electric propulsion waste heat recovery | +1.3% | Europe and Japan lead, with early US participation | Long term (≥ 4 years) |

| Additive manufactured micro channel cores | +1.0% | Asia-Pacific manufacturing scale-up, North America and EU design leadership | Medium term (2–4 years) |

| Defense UAV endurance extension initiatives | +0.7% | North America, Middle East, and Asia-Pacific ISR fleets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Ramp-Up in Narrowbody and Regional Jets Production

Higher production targets for single-aisle programs and stable regional jet deliveries drive sustained demand for engine, hydraulic, ECS, and avionics cooling hardware, providing long-term visibility for growth in the aircraft heat exchanger market. Airframes use multiple exchanger types across core systems, driving higher production rates and increased demand for shipments and spares in the aircraft heat exchanger market. Specifications are tightening as airframers seek higher thermal effectiveness at lower pressure drops and mass, which increases the value of microchannel and lattice-fin geometries that are printable with modern metal AM systems.[1]EOS Editorial Team, “AM Pushes the Boundaries of Thermal Management,” EOS, eos.info The combined pull of refreshed OE build slots and sustained aftermarket needs positions high-performance, lightweight exchangers as standard fit in the aircraft heat exchanger market rather than optional upgrades.

Fleet-Wide ECS Retrofit Programs for Cabin Air-Quality

Post-2024, operators have aligned with higher fresh-air supply expectations and better filtration standards, shifting the retrofit focus to environmental control systems and their heat-exchanger cores in the aircraft heat-exchanger market. Honeywell's compact vapor-cycle pack reduces weight and enhances efficiency, helping airlines meet air-quality targets while mitigating fuel-burn penalties on legacy narrowbody aircraft in the aircraft heat exchanger market. Predictive maintenance tied to connected aircraft platforms flags exchanger fouling and leakage earlier, reducing unscheduled removals and directing timely replacements to restore cooling margins in the aircraft heat exchanger market. Airlines and MROs value shorter turn times and re-core capabilities, so repair network depth and re-certification speed become key differentiators as ECS retrofits scale in the aircraft heat exchanger market.

Shift to High-Temperature Ceramic HX Materials

Hydrogen-related demonstrators and hot-running next-generation cores are raising operating temperatures, where metallic exchangers approach creep and oxidation limits, strengthening the case for ceramic designs in the aircraft heat exchanger market. Ceramic matrix composite solutions and advanced ceramics enable higher-temperature heat transfer and lower thermal expansion, reducing thermal stress during rapid transients and supporting tighter packaging targets in the aircraft heat exchanger market. Japan’s ongoing hydrogen engine and systems work under the Green Innovation Fund includes high-temperature exchanger development and rigorous weld and transient stress testing, which support the maturation of ceramic designs for airframes that will need cryogenic-to-hot loop management in the aircraft heat exchanger market. As additive processes for ceramics and inspection workflows improve, production costs and timelines are likely to fall, opening broader adoption beyond defense and early hydrogen pilots. Standards and qualification frameworks already exist for complex printed hardware and help guide inspection and process control for novel exchanger designs in the aircraft heat exchanger market.[2]Conflux Technology Editorial Team, “How NASA-STD-6030 Is Transforming Additive Manufacturing for Aerospace Heat Exchangers,” Conflux Technology, confluxtechnology.com

Hydrogen-Electric Propulsion Waste-Heat Recovery

Fuel-cell and hybrid-electric architectures generate megawatt-class heat loads that demand compact exchangers with high frontal heat flux and low drag, a central technical hurdle for zero-emission airframes in the aircraft heat exchanger market. Evaporative and two-phase cooling methods improve specific power in thermal subsystems and reduce the weight of loop components, which is valuable for weight-sensitive propulsion stacks and power electronics in the aircraft heat exchanger market. Europe and Japan are pacing early integration and ground testing, while North American programs emphasize retrofit pathways that can scale within existing certification and operating envelopes in the aircraft heat exchanger market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nickel and aluminum input cost volatility | -1.1% | Global, with acute effects in North America and Europe | Short term (≤ 2 years) |

| Qualification bottlenecks for new HX designs | -0.9% | North America and Europe certification ecosystems | Medium term (2–4 years) |

| Supply chain consolidation raising OEM dependency | -0.7% | Global, more visible in mature aftermarket hubs | Long term (≥ 4 years) |

| Weight penalties versus integrated thermal management | -0.4% | Program-specific across regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Nickel and Aluminum Input-Cost Volatility

Commodity volatility affects core alloys used in airworthy exchangers, complicating pricing for long-duration OE contracts and creating quarterly variability in retrofit kits for the aircraft heat exchanger market. Larger primes typically use hedging and long-term agreements to dampen volatility, while smaller firms rely on index-linked clauses and staggered purchases that add administrative overhead. As certification rules constrain recycled content in critical components, room to offset primary metal exposure is limited, which sustains a pricing headwind even when programs ramp.

Qualification Bottlenecks for New HX Designs

Flight-critical and essential systems require rigorous environmental and structural testing, which lengthens the time needed for first-article approval for new exchanger designs. Printed, high-complexity cores with fine internal features often require computed tomography and coupon witness plans, which add inspection time and specialized tooling to the path to certification in the aircraft heat exchanger market. Harmonized guidance for AM is improving, yet cross-acceptance across authorities still takes additional cycles for novel geometries. DO-160 environmental test campaigns add months and cost but remain essential to validate performance across temperature, altitude, humidity, shock, vibration, and EMI parameters in the aircraft heat exchanger market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Flat-Tube Geometries Dominate Through AM-Enabled Miniaturization

Flat-tube heat exchangers held 64.42% of 2025 revenue and are advancing at an 8.80% CAGR through 2031, supported by microchannel designs that improve heat flux without proportional pressure drop penalties in the aircraft heat exchanger market. Flat tube cores are widely used in engine oil cooling, hydraulic systems, and compact ECS packs, efficiently supporting both new build and retrofit program requirements. Performance-focused adopters also benefit from accelerated design loops and integrated verification enabled by AM workflows, which shorten time-to-qualification for derivative designs in the aircraft heat exchanger market.

Plate-fin designs continue to meet high surface-area needs in avionics bays and mission equipment, and they are evolving as AM and advanced brazing improve joint reliability and thin-wall integrity. Innovative geometry, standardized processes, and defined qualification paths are enhancing flat-tube leadership and modernizing plate-fin applications in the aircraft heat exchanger market.

By Platform: Fixed-Wing Ascendancy Masks Rotary-Wing and UAV Niches

Fixed-wing programs accounted for 69.72% of the 2025 market and are expected to grow at the highest CAGR of 8.97%, primarily driven by commercial transports and tactical military jets. Each narrowbody and widebody integrates a network of exchangers, creating a unit multiplier that aligns with airframe output cadence. Electrification of subsystems, higher-bypass engines, and tighter cabin air-quality standards combine to increase exchanger duty compared to earlier generations. Onboard power growth also increases avionics and power-electronics cooling requirements, shifting more programs toward liquid- and two-phase-loop systems that depend on compact, high-efficiency cores in the aircraft heat exchanger market.

Rotary-wing aircraft and special-mission fixed-wing fleets sustain healthy niches where vibration, salt fog, and sand ingestion define durability targets for exchanger materials and joints. On the defense side, UAVs are the fastest-growing niche as ISR and EW payloads push continuous heat loads that exceed the capabilities of legacy convection schemes. The integration of advanced avionics cooling technologies into UAV payload bays is driving the adoption of next-generation thermal modules within unmanned fleets in the aircraft heat exchanger market.

By Application: Engine Systems Lead, ECS Growth Accelerates on Air-Quality Push

Environmental control systems are advancing at an 8.78% CAGR through 2031 as airlines upgrade packs and cores to deliver higher fresh-air rates and better filtration without incurring fuel burn penalties in the aircraft heat exchanger market. Efficiency-driven ECS retrofits add value when they also reduce maintenance events tied to fouling or leakage, strengthening the case for high-efficiency, low-pressure-drop exchangers. Engine systems (Oil/Fuel/Air) held a 55.84% share of the aircraft heat exchanger market in 2025, driven by continuous thermal loads from higher core temperatures, increased gearbox loads, and greater power densities, which significantly impact oil and fuel system performance during flight cycles.

Avionics and power electronics cooling are scaling as more-electric architectures proliferate across commercial and defense platforms. Qualification remains central across applications, and DO-160 test capabilities that are available in-house at some suppliers help compress schedules and de-risk new designs in the aircraft heat exchanger market.[3] ACE Thermal Systems Team, “Qualification Testing,” ACE Thermal Systems, acethermalsystems.com Taken together, ECS momentum, engine thermal intensity, and growing electronics loads support resilient, multi-application demand through the forecast period in the aircraft heat exchanger market.

By Vendor: Aftermarket acceleration challenges OEM dominance

OEM channels captured 64.96% of the revenue in 2025, as integrators embedded exchangers in new-build aircraft; however, aftermarket revenue grew faster at a 9.02% CAGR. Airlines are extending the fleet age beyond 13 years, and Parts Manufacturer Approval (PMA) providers are introducing cost-competitive core-replacement kits, eroding OEM spares sales. MRO groups, such as AMETEK MRO, invest in vacuum-brazing furnaces and coupon rigs to rebuild high-temperature units, thereby bridging the expertise gap with OEMs.

Digital twins and predictive analytics further empower independent repair houses to achieve turnaround times and residual-life metrics comparable to those of factory service. This technology-led leveling of the service playing field is reshaping the competitive contours of the aircraft heat exchanger market.

Geography Analysis

North America accounted for 39.88% market share in 2025, and is growing at the highest CAGR of 9.21% supported by a broad installed base and deep tier-1 networks spanning engine, ECS, and avionics thermal systems. Retrofit momentum is reinforced by airlines’ focus on cabin environment and operational reliability, which aligns with ECS re-core and pack upgrades available with lighter, more efficient units. Defense programs across fighters and UAVs also preserve specialized demand for higher-capacity thermal subsystems, which favors suppliers with ruggedized offerings validated under harsh environmental envelopes in the aircraft heat exchanger market. In parallel, connected aircraft ecosystems and predictive tools help airlines and MRO providers act earlier on exchanger degradation, reducing aircraft-on-ground time and supporting gains in uptime.

Europe benefits from sustained single-aisle production targets and active hydrogen-electric R&D that places thermal management at the center of clean-sheet architectures in the aircraft heat exchanger market. Airbus has highlighted power and heat flows in its hydrogen concept showcase, confirming the central role of high-effectiveness exchangers in megawatt-class stacks and power electronics. Regional MRO expansions and competence centers for re-coring support faster turnarounds, which help airlines and lessors keep older fleets competitive while deferring replacements in the aircraft heat exchanger market.

Asia-Pacific’s growth is anchored by rising local integration capability, national programs, and active hydrogen research, especially in Japan, where industry and public funding support the development of fuel, combustors, and heat exchangers for the aircraft heat exchanger market. Precision manufacturing strengths in Japan and emerging AM ecosystems across the region support serial production of complex cores and larger brazed assemblies for commercial and defense fleets.[4]Sumitomo Corporation Editorial Team, “Sumitomo Precision Products’ No.1 Products,” Sumitomo Corporation, sumitomocorp.com

Competitive Landscape

The aircraft heat exchanger market is moderately consolidated, with the five largest suppliers accounting for the majority of global revenue. Companies such as Honeywell International Inc., Liebherr Group, Safran SA, RTX Corporation, and Parker-Hannifin Corporation leverage advanced systems integration capabilities and proprietary alloy patents to maintain margins. Their vertical integration into casting, machining, and brazing mitigates raw material volatility and reduces supplier tiers.

Technology advances continue to shift the performance baseline for exchangers serving ECS, engine, and electronics cooling. AM is advancing from prototyping to serial production of topology-optimized cores, supported by evolving qualification frameworks and improved multi-laser platforms in the aircraft heat exchanger market. Suppliers that align AM process control, CT-based inspection, and design-for-AM methods can deliver thinner walls, tighter passages, and higher heat flux per frontal area.

Ecosystem collaboration is central to the aircraft heat exchanger market. Airbus is advancing hydrogen-electric propulsion through multi-technology validation, prioritizing heat exchanger design for power and safety. Industry events align fuel-cell, component, and airframe leaders on technical roadmaps. Startups and SMEs are co-developing advanced exchangers with airframers and propulsion innovators for electric and hydrogen demonstrators, integrating agility with incumbents' certification capabilities. This collaborative model ensures alignment of technical expertise and scalability to meet evolving propulsion and safety requirements.

Aircraft Heat Exchanger Industry Leaders

Honeywell International Inc.

RTX Corporation

Liebherr Group

Parker-Hannifin Corporation

Safran S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Through the Department of the Air Force, the US Department of Defense (DoD) announced a request for contractors to remanufacture the Primary and Secondary Heat Exchangers for the B-52. This procurement is set as a firm-fixed-price requirements contract over five years. It encompasses a three-year basic period, with an optional two-year extension. Contractors are tasked with supplying all essential labor, facilities, equipment, and materials to rejuvenate the heat exchangers to a condition akin to new.

- October 2025: Conflux Technology (Conflux) collaborated with Airbus on the ZEROe project to develop an additively manufactured heat exchanger for hydrogen-electric propulsion. Currently undergoing readiness assessment, the component is critical for thermal regulation in megawatt-class fuel cell systems, ensuring efficient operation and supporting advancements in sustainable aviation technology.

- March 2025: Conflux partnered with AMSL Aero to develop hydrogen fuel-cell cooling for Vertiia VTOL aircraft, creating three heat-exchanger concepts to optimize weight, volume, heat load management, and drag reduction, enabling zero-emission flights up to 1,000 km.

- February 2025: Liebherr-Aerospace and GMR Aero Technic signed a service agreement to maintain, repair, and overhaul Airbus A320 heat transfer equipment. This collaboration ensures efficient servicing during maintenance checks, supporting optimal aircraft performance and compliance with airworthiness standards.

Global Aircraft Heat Exchanger Market Report Scope

A heat exchanger is a system used to transfer heat between a source and a working fluid. Heat exchangers are used in both heating and cooling processes. Aircraft heat exchangers are used in aircraft engines and environmental control systems.

The aircraft heat exchanger market is segmented by type, platform, application, vendor, and geography. By type, the market is segmented into plate-fin and flat tube. By platform, the market is segmented into fixed-wing aircraft, rotary-wing aircraft, and unmanned aerial vehicles (UAVs). By application, the market is segmented into environmental control systems, engine systems, electronic pod cooling, and hydraulic cooling. By vendor, the market is segmented into OEM and aftermarket. The report also covers the market sizes and forecasts for the aircraft heat exchanger market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Plate-fin |

| Flat Tube |

| Fixed-Wing Aircraft |

| Rotary-Wing Aircraft |

| Unmanned Aerial Vehicles |

| Environmental Control Systems |

| Engine Systems (Oil/Fuel/Air) |

| Electronic Pod Cooling |

| Hydraulic Cooling |

| OEM |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Plate-fin | ||

| Flat Tube | |||

| By Platform | Fixed-Wing Aircraft | ||

| Rotary-Wing Aircraft | |||

| Unmanned Aerial Vehicles | |||

| By Application | Environmental Control Systems | ||

| Engine Systems (Oil/Fuel/Air) | |||

| Electronic Pod Cooling | |||

| Hydraulic Cooling | |||

| By Vendor | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook of the aircraft heat exchanger market?

The aircraft heat exchanger market size was USD 1.85 billion in 2025 and is forecasted to reach USD 3.09 billion by 2031 at an 8.24% CAGR.

Which application is growing the fastest within the aircraft heat exchanger market?

Environmental control systems are advancing at an 8.78% CAGR through 2031 as airlines upgrade packs and cores to meet stronger cabin air-quality expectations.

Why is additive manufacturing important to the aircraft heat exchanger market?

AM enables microchannel and lattice-fin cores with higher heat flux per unit mass and volume, improving packability and efficiency, and accelerating design-to-qualification cycles.

How does hydrogen-electric propulsion influence the aircraft heat exchanger market?

Megawatt-class propulsion and fuel-cell systems create large heat loads that demand compact, high-effectiveness exchangers, placing thermal management at the center of hydrogen aircraft design.

What are the main barriers to faster productization in the aircraft heat exchanger market?

Qualification bottlenecks from DO-160 campaigns and AM-specific process and inspection requirements extend first-article timelines for new, complex cores.

Where are service and MRO capabilities expanding within the aircraft heat exchanger market?

Europe has added capacity for re-coring and MRO, while global partnerships aim to reduce turnaround times and link predictive maintenance insights with hardware serviceability.

Page last updated on: