Aircraft Nacelle Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

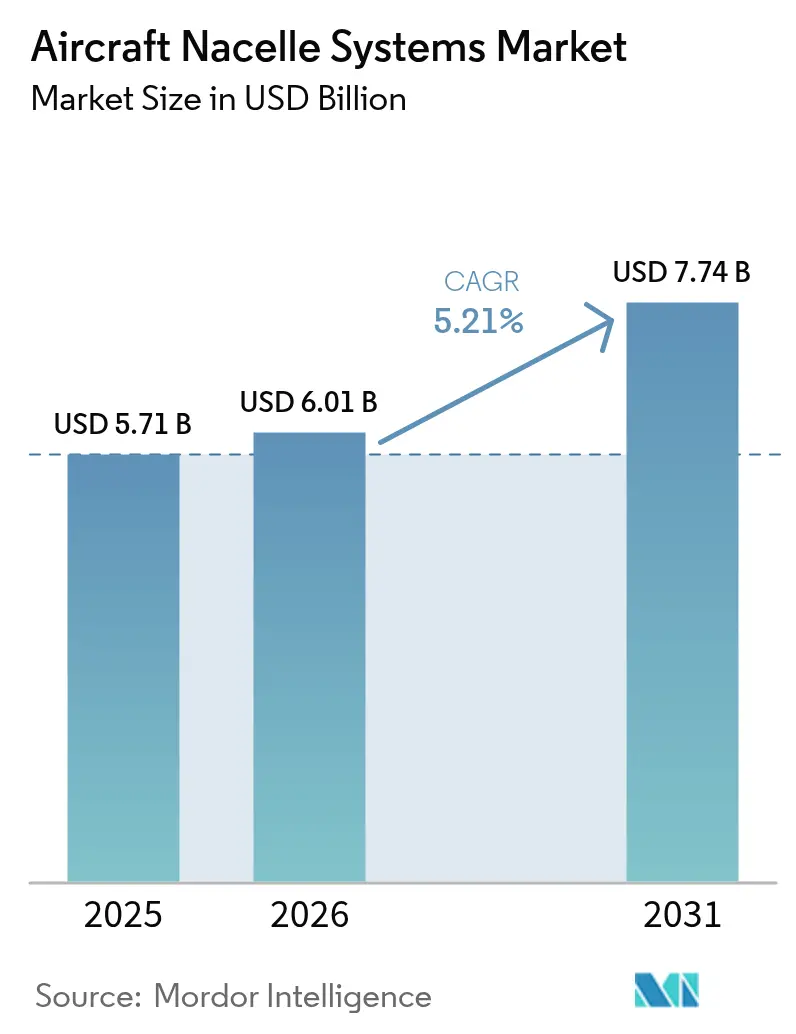

| Market Size (2026) | USD 6.01 Billion |

| Market Size (2031) | USD 7.74 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Nacelle Systems Market Analysis by Mordor Intelligence

The aircraft nacelle systems market size is expected to grow from USD 5.71 billion in 2025 to USD 6.01 billion in 2026 and is forecast to reach USD 7.74 billion by 2031 at 5.21% CAGR over 2026-2031. Robust backlogs at Airbus and Boeing, rising single-aisle output targets, and airlines’ continued shift toward high-bypass engines underpin the growth trajectory. Ongoing certification of new B737 MAX and A320neo family variants, plus sustained retirements of legacy fleets, will keep demand for advanced nacelles firmly positive despite intermittent supply-chain constraints. Growing preference for service-based contracts such as nacelle-as-a-service and digital health-monitoring upgrades widens the aftermarket’s strategic relevance.

Key Report Takeaways

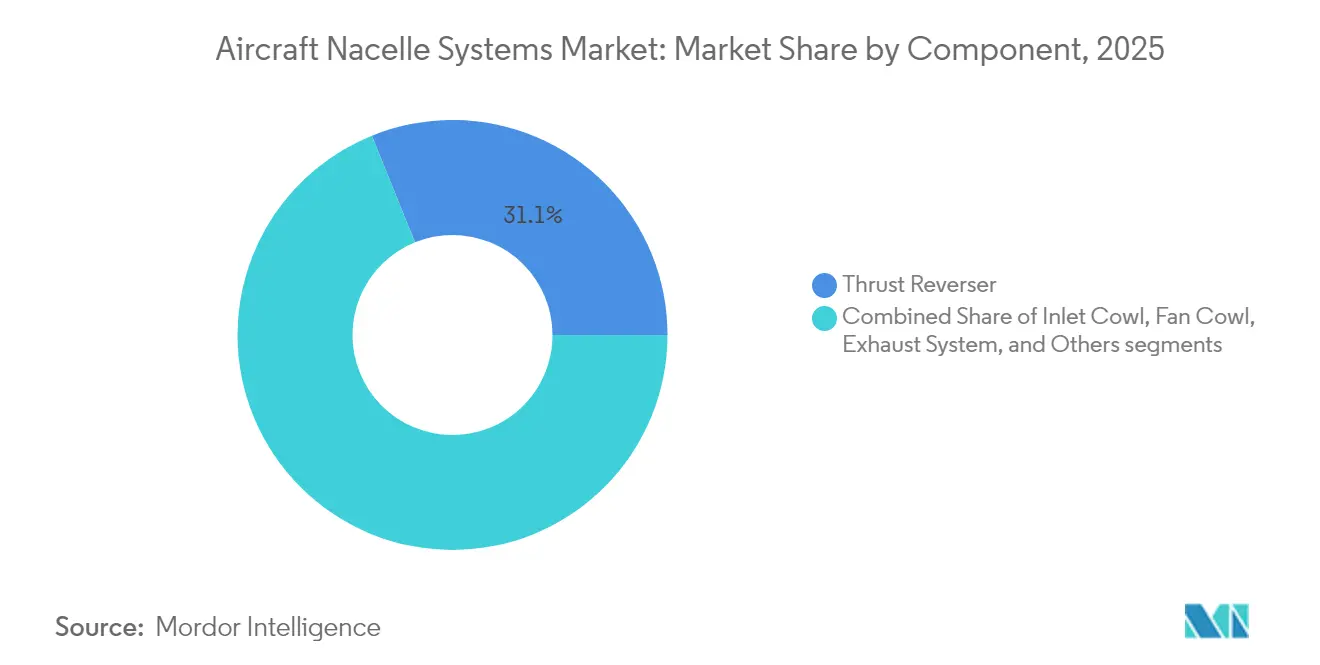

- By component, thrust reversers led with 31.12% of the aircraft nacelle systems market share in 2025; inlet cowls are projected to expand at a 5.64% CAGR through 2031.

- By aircraft type, commercial aviation held 57.30% revenue share in 2025, while general aviation is set to post the fastest 5.78% CAGR to 2031.

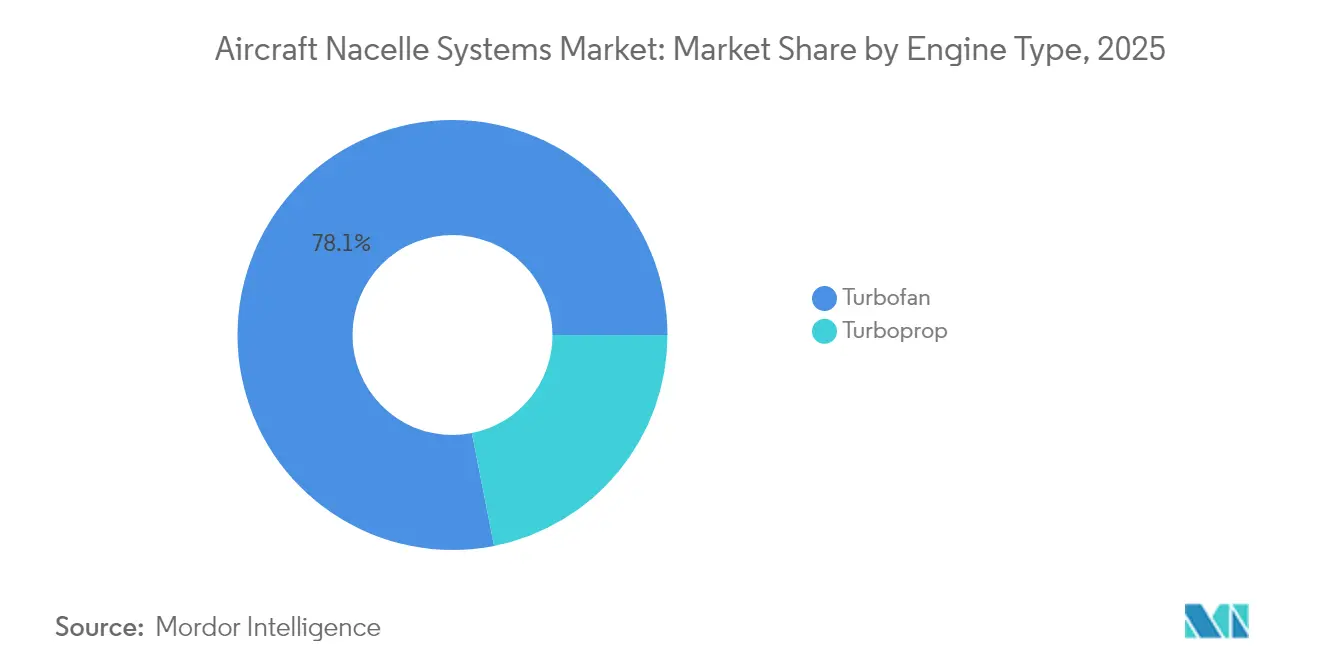

- By engine type, turbofan platforms captured 78.10% of the aircraft nacelle systems market size in 2025 and are advancing at a 5.86% CAGR into 2031.

- By end user, OEMs commanded 75.70% of the aircraft nacelle systems market size in 2025, whereas the aftermarket segment is forecasted to rise at a 5.39% CAGR to 2031.

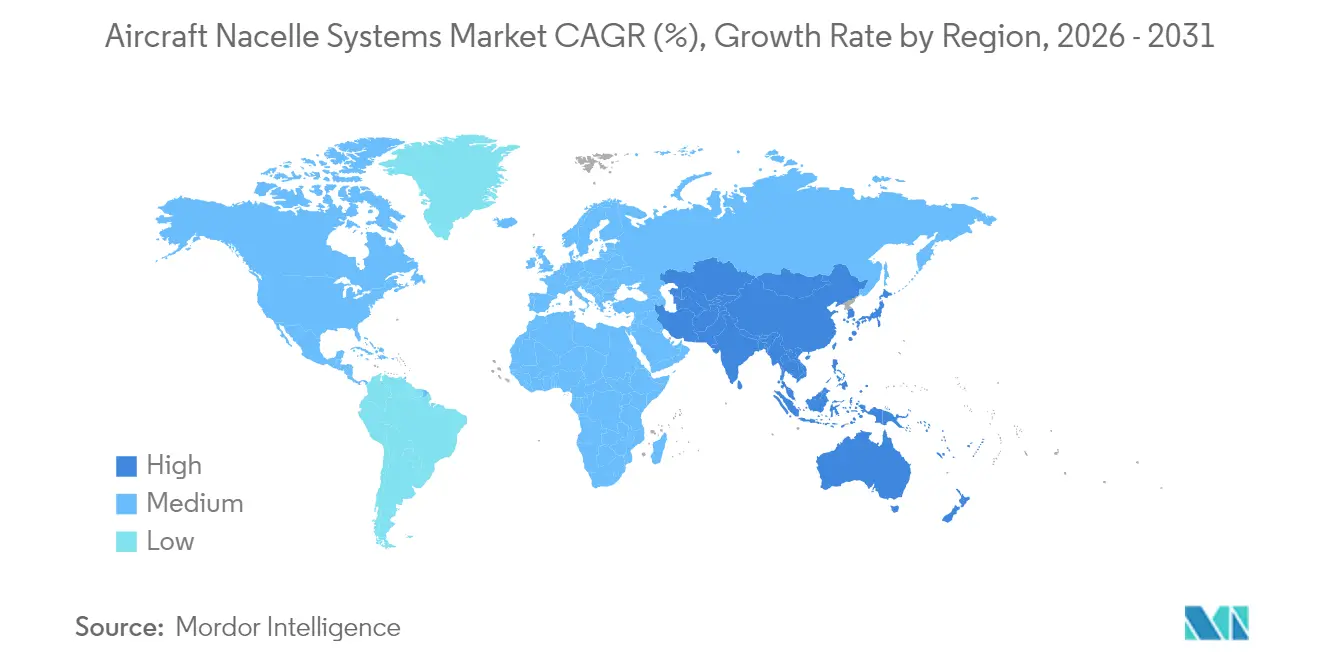

- By geography, North America accounted for a 38.30% share in 2025, yet Asia-Pacific is projected to log the quickest 5.62% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Nacelle Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing emphasis on fuel-efficient and next-generation aircraft | +0.8% | North America and Europe with global fleet adoption | Medium term (2-4 years) |

| Ongoing fleet modernization and rising single-aisle aircraft backlog | +1.0% | Asia-Pacific and North America | Medium term (2-4 years) |

| Ramp-up in production rates by Airbus and Boeing | +1.1% | North America and Europe manufacturing hubs | Short term (≤2 years) |

| Stricter airport noise regulations driving acoustic nacelle integration | +0.7% | Europe and North America, expanding to Asia-Pacific | Long term (≥4 years) |

| Adoption of nacelle-as-a-service subscription and maintenance models | +0.5% | Early uptake in North America and Europe | Medium term (2-4 years) |

| Advancements in nacelle designs supporting boundary-layer ingestion propulsion | +0.4% | North America and Europe R&D centers | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Emphasis on Fuel-Efficient and Next-Generation Aircraft

Airlines’ immediate focus on cutting fuel burn translates into nacelle designs that handle larger fan diameters, higher bypass ratios, and 15–20% lower specific fuel consumption for engines such as CFM LEAP-1A and LEAP-1B.[1]Sean Broderick, “Boeing Lays Out 737 Production-Ramp Path,” Aviation Week, aviationweek.com Weight penalties are countered through broader use of resin-infused carbon-fiber barrels that trim 20 to 25 kg per ship-set without compromising stiffness. Acoustic liners now integrate micro-perforated face-sheets and graded honeycomb cores to curb tonal noise peaks by up to 3 dB, ensuring Chapter 14 compliance on the A320neo and B737 MAX families. Sustained demand is evidenced by Boeing’s plan to surpass 50 B737 MAX units per month after 2H 2026, locking in five-year visibility for nacelle suppliers. Fuel-efficiency mandates extend to military tanker and transport upgrades, adding incremental volume beyond commercial fleets.

Ongoing Fleet Modernization and Rising Single-Aisle Backlog

Backlog pressures remain acute, as Airbus counted 8,754 open orders by mid-2025—82% concentrated in the A220/A320 lines—translating to more than eight years of forward production at current build rates.[2]ePlane AI, “Airbus Outlook 2025,” eplaneai.com Each A320neo ship-set requires roughly USD 1 million worth of nacelle hardware, giving suppliers high-volume recurring revenue once ramp-ups stabilize. Asia-Pacific airlines, notably IndiGo, are securing purchase rights for up to 100 A350 jets, signaling that widebody replacement is also gathering pace. Deferred deliveries owing to engine shortages widen the delta between orders and production, making slots on high-volume programs strategically valuable.

Ramp-Up in Production Rates by Airbus and Boeing

The FAA’s May 2025 authorization for Boeing to raise B737 MAX output to 42 jets monthly created an instant step-change in nacelle procurement, with each monthly uptick adding demand for 84 thrust-reverser halves, 84 fan cowls, and 84 inlet lips. Airbus, meanwhile, is working toward 75 A320-family aircraft per month by 2027 after pushing back the 2026 target because of supply tightness. Even a two-month slip in Boeing’s five-jet-per-increment ramp schedule can pull as much as USD 120 million in nacelle revenue forward or backward per quarter, underscoring how tightly linked suppliers are to OEM cadence.

Stricter Airport Noise Regulations

European hubs such as Heathrow and Amsterdam-Schiphol attach landing-fee surcharges of up to 15% on aircraft that fail to meet local decibel caps, nudging airlines toward nacelles with advanced chevron nozzles and triple-layer acoustic liners. Suppliers respond by integrating metamaterial liners that shrink nacelle length by 6–8 cm while keeping attenuation stable, freeing space for wing-to-body fairing redesigns. Investment costs average USD 7–10 million per new acoustic option, but pay back within four years through higher ship-set pricing and better aftermarket margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment and tooling costs for system manufacturing | -0.4% | Global, hitting small and mid-tier suppliers hardest | Short term (≤2 years) |

| Stringent FAA and EASA certification and regulatory compliance cycles | -0.5% | North America and Europe | Medium term (2-4 years) |

| Bottlenecks in the supply of aerospace-grade composite resins | -0.3% | North America and Europe | Short term (≤2 years) |

| Competitive threat from emerging podded electric propulsion systems | -0.2% | Europe and North America R&D nodes | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and Tooling Costs

Fabricating a next-generation thrust-reverser cascade tool set exceeds USD 12 million, while autoclave lines sized for A320neo fan cowls can cost another USD 25 million. Hexcel’s 2024 capex of USD 87 million mainly financed resin-injection machines and in-house NDI systems, yet payback horizons stretch 5–7 years because ship-set pricing remains under OEM cost-down pressure.[3]Hexcel Corporation, “2024 Full-Year Results,” hexcel.com Smaller tier-2 shops often finance through sale-leasebacks that raise effective borrowing costs by 150–200 basis points. As OEMs demand dual-sourcing to buffer supply shocks, some suppliers must duplicate capacity on separate continents, doubling upfront spend without guaranteed volumes.

Stringent FAA and EASA Certification Requirements

Boeing’s B737 MAX 7 nacelle ice-shape re-test campaign extended program approval by 14 months, highlighting how even minor design tweaks can restart validation loops. Suppliers must generate more than 8,000 pages of compliance data for a typical thrust reverser, including cyber-resilience assessments for digital valve actuators. Dual-authority sign-offs obligate up to 40 witnessed ground tests, costing USD 50,000 to 70,000 in instrumentation and crew. Any service history incident, however minor, can trigger Special Conditions that retroactively affect in-service fleets, adding retrofit costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Complexity Keeps Thrust Reversers Dominant

Thrust reversers held 31.12% of the aircraft nacelle systems market in 2025, buoyed by their safety-critical role and integration with engine-control logic. Although smaller in value, inlet cowls are on track for the fastest 5.64% CAGR through 2031 as carriers reward suppliers that can marry variable-geometry lips with low-noise liners. Suppliers that streamline removable acoustic panels and additive-manufactured lips stand to grow share, especially on re-engined narrowbodies expected to dominate deliveries this decade.

Fan cowls and exhaust systems still command steady demand that shadows airframe production, yet they face less aggressive redesign cycles than inlet cowls. Composite hot zones and metallic flow paths continue to converge, targeting reduced maintenance while defending margins in a cost-pressured environment. The emergence of boundary-layer ingestion further heightens inlet design complexity, steering supplier investment into lightweight, structurally stiff inlet ducts capable of managing distorted in-flow fields without inducing flutter.

By Aircraft Type: Commercial Aviation Drives Volume, General Aviation Outpaces Growth

Commercial programs delivered the bulk of revenue in 2025, accounting for 57.30% of the aircraft nacelle systems market. Narrowbodies, led by the A320neo and B737 MAX, sustain unmatched build-rates and thus the lion’s share of nacelle shipments. Meanwhile, general aviation is expected to clock a 5.78% CAGR, supported by fresh business jet introductions and early eVTOL prototypes that leverage scaled-down nacelle technologies. The aircraft nacelle systems market size for the business jet niche is predicted to climb alongside Gulfstream G700 and Bombardier Global 7500 roll-outs.

Widebody nacelles have the greatest per-unit value, with Airbus striving to increase A350 output to 12 aircraft per month by 2028. Regional jets and military transports supply steady, albeit lower-volume demand that diversifies supplier revenue and smooths commercial cycle volatility.

By Engine Type: Turbofan Supremacy Continues

Turbofan programs captured 78.10% of revenue in 2025 and are pegged to expand at a 5.86% CAGR, reflecting sustained preference for high-bypass typologies in commercial and defense fleets. The aircraft nacelle systems market size tied to turbofans is projected to rise with LEAP, GTF, and Trent deliveries.

Key design themes include composite fan-door barrels, integrated anti-icing systems, and real-time structural health sensors. Despite a smaller volume, turboprops remain relevant for regional and special-mission aircraft where short-field performance prevails.

By End User: OEM Contracts Dominate, Aftermarket Scales Faster

OEM deliveries produced 75.70% of 2025 revenue, yet the aftermarket’s 5.39% CAGR will gradually enlarge its slice as operators seek cost-predictable service loops. Airlines increasingly sign power-by-the-hour‐styled agreements that bundle nacelle spares, on-wing support, and predictive analytics dashboards. Safran’s multi-site MRO expansion in Singapore and Dubai is emblematic of how incumbents fortify global reach.

Geography Analysis

North America controlled 38.30% of 2025 revenue due to Boeing’s production rebound and dense aftermarket networks. FAA clearance in May 2025 for 42 units per month, B737 MAX output immediately lifted the nacelle order flow. Spirit AeroSystems’ Pearl 10X nacelle contract and Collins Aerospace’s blended wing body partnership with JetZero reflect the region’s innovation weight.

Asia-Pacific is predicted to pace the field with a 5.62% CAGR through 2031 as China, India, and Southeast Asia scale fleets and localize aerostructure work. IndiGo’s purchase rights for up to 100 A350s underline the region’s widebody appetite. Safran’s tie-up with Hindustan Aeronautics Limited to manufacture LEAP parts in India shows established suppliers embedding within emerging supply chains.

Europe remains a pillar supplier hub anchored by Airbus and top-tier vendors like Safran and GKN. Clean-Aviation-funded hybrid-electric prototypes keep continental R&D centered on low-drag, low-noise nacelles. Airbus’ target of 75 A320-family jets a month by 2027 underwrites volume stability. Regulatory rigor from EASA, particularly on acoustics, steers global design baselines.

Competitive Landscape

Competition is moderate, shaped by deep-rooted OEM alliances and certification prowess. Safran, Collins Aerospace, and Leonardo S.p.A. collectively oversee a substantive share, leveraging vertically integrated composites, thrust reverser patents, and worldwide MRO footprints. Safran’s EUR 1 billion (USD 1.17 billion) LEAP MRO rollout boosts aftermarket stickiness, while Collins’ JetZero project positions it for boundary-layer ingestion configurations.

White-space opens around electrified propulsion and blended-wing airframes where conventional nacelles may morph or vanish. Through its Raytheon Technologies subsidiary, RTX is co-developing nacelles for JetZero’s blended-wing demonstrator, aiming to preserve thermal management know-how in disruptive architectures. Hexcel’s new HexPly M51 prepreg promises lighter, more rigid hot-section panels.[4]Hexcel Corporation, “Launch of HexPly M51,” hexcel.com

Barriers to entry stay high: multi-year certification, soaring tooling capex, and tight supplier approval loops deter newcomers. However, regional composite houses in India and China could gain share in cost-sensitive sub-assemblies once local regulatory pathways mature.

Aircraft Nacelle Systems Industry Leaders

Leonardo S.p.A.

GKN Aerospace Services Limited (Melrose Industries plc)

Collins Aerospace (RTX Corporation)

Safran SA

Spirit AeroSystems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AAR CORP. entered into a multi-year agreement with Cebu Pacific Air to provide nacelle maintenance, repair, and overhaul (MRO) services for the airline's A320 fleet equipped with CFM56-5B engines.

- November 2024: GKN Aerospace delivered the first two C-27J nacelles to Leonardo Aircraft, demonstrating the restoration of its supply chain and production capabilities.

- April 2023: Spirit AeroSystems signed an exclusive cooperation agreement with ST Engineering's Commercial Aerospace business to provide aircraft engine nacelle MRO solutions in Middle Eastern countries, including Qatar, UAE, Jordan, Saudi Arabia, Kuwait, and Oman.

Global Aircraft Nacelle Systems Market Report Scope

An aircraft engine nacelle is the housing structure for an aircraft's engine. This market study encompasses a range of parts and components integral to aircraft nacelle systems' design. These include the engine cowling, inlet cowl, thrust reverser, fan cowl, pylon, and exhaust system.

The aircraft nacelle systems market is segmented by application and engine type. By application, the market is classified into commercial, military, and general aviation. By engine type, the market is segmented into turbofan and turboprop. Also, the report covers the market size and forecasts for the aircraft nacelle systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Inlet Cowl |

| Fan Cowl |

| Thrust Reverser |

| Exhaust System |

| Others |

| Commercial Aviation | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| Military Aviation | Combat Aircraft |

| Transport Aircraft | |

| Special Mission Aircraft | |

| Others | |

| General Aviation | Business Jets |

| Others |

| Turbofan |

| Turboprop |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Inlet Cowl | ||

| Fan Cowl | |||

| Thrust Reverser | |||

| Exhaust System | |||

| Others | |||

| By Aircraft Type | Commercial Aviation | Narrowbody Aircraft | |

| Widebody Aircraft | |||

| Regional Jets | |||

| Military Aviation | Combat Aircraft | ||

| Transport Aircraft | |||

| Special Mission Aircraft | |||

| Others | |||

| General Aviation | Business Jets | ||

| Others | |||

| By Engine Type | Turbofan | ||

| Turboprop | |||

| By End User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value of the aircraft nacelle systems market by 2031?

The aircraft nacelle systems market is projected to reach USD 7.74 billion by 2031.

Which geographic region is poised for the fastest nacelle growth?

Asia-Pacific is expected to post a 5.62% CAGR through 2031.

Which component currently leads revenue?

Thrust reversers held 31.12% share in 2025.

Why are inlet cowls the fastest growing component?

Airlines seek fuel economy and lower noise, prompting advanced inlet designs to grow at 5.64% CAGR.

How significant is the aftermarket compared with OEM sales?

OEMs still generate 75.70% of 2025 revenue, but aftermarket contracts are expanding faster at 5.39% CAGR.

What is the primary restraint hindering new entrants?

High tooling investment exceeding USD 50 million and lengthy certification timelines create steep entry barriers.

Page last updated on: