Air-to-Air Refueling System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

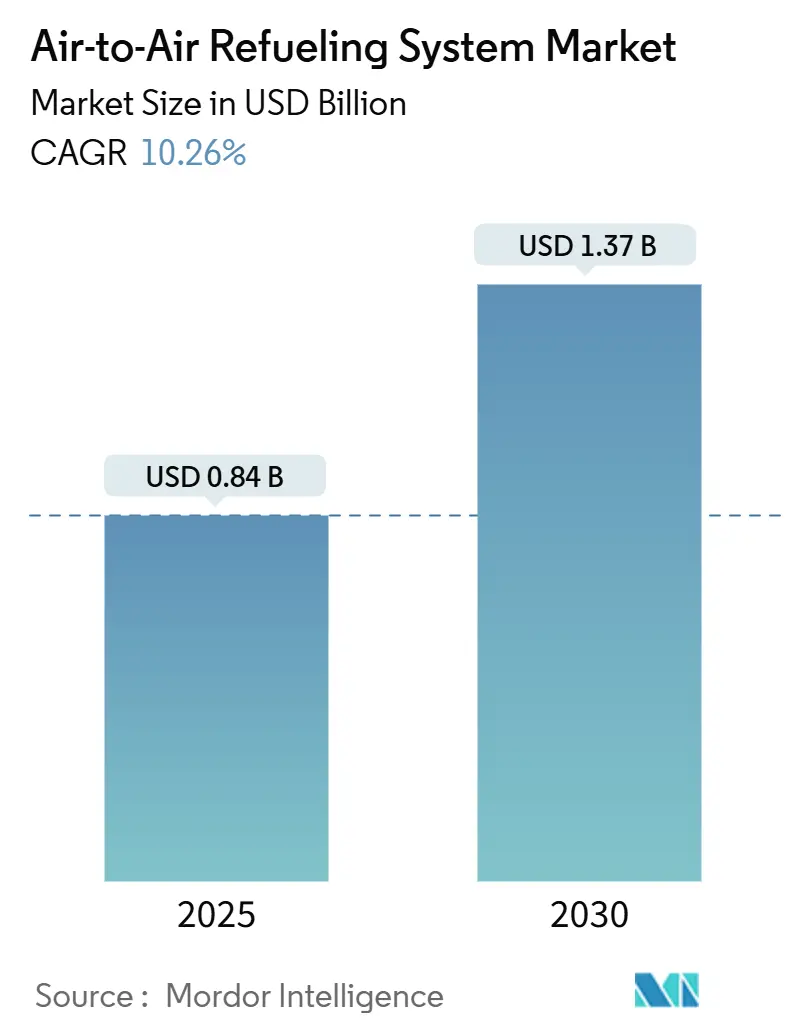

| Market Size (2025) | USD 0.84 Billion |

| Market Size (2030) | USD 1.37 Billion |

| Growth Rate (2025 - 2030) | 10.26% CAGR |

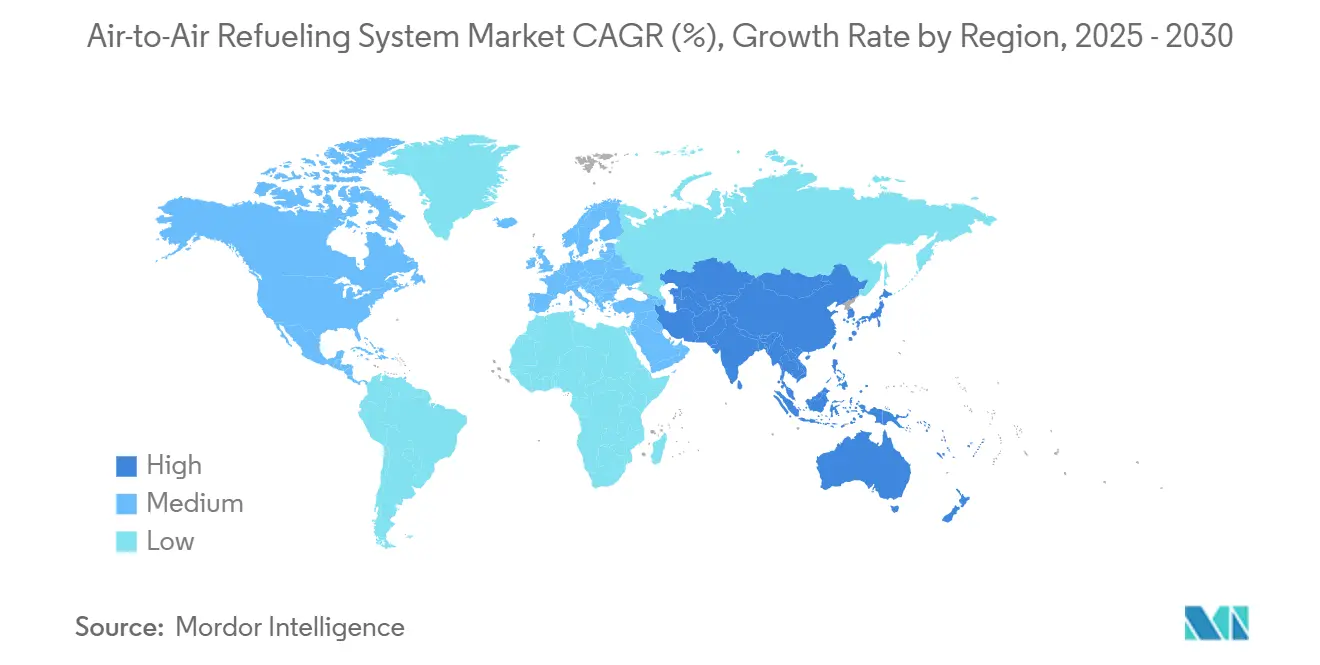

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air-to-Air Refueling System Market Analysis by Mordor Intelligence

The global air-to-air refueling system market size stood at USD 841.69 million in 2025 and is forecasted to expand at a 10.26% CAGR, reaching USD 1.37 billion by 2030. The primary drivers behind this strong outlook are the surge demand for longer-range missions, accelerated fleet-modernization cycles, and rapid progress in autonomous tanker technology. Programs such as the KC-46A Pegasus and the A330 MRTT+ continue to lift procurement volumes, while component suppliers invest heavily in digital-twin analytics to improve reliability and cut maintenance costs. The trend toward multi-domain operations reshapes technical requirements, ushering in hybrid boom/probe architectures and unmanned aerial refueling vehicles that can safely operate in contested airspace. Operators in Asia-Pacific are raising defense budgets at double-digit rates, spurring regional adoption. Meanwhile, North America preserves its lead thanks to sustained US Air Force spending and large-scale upgrade programs.

Key Report Takeaways

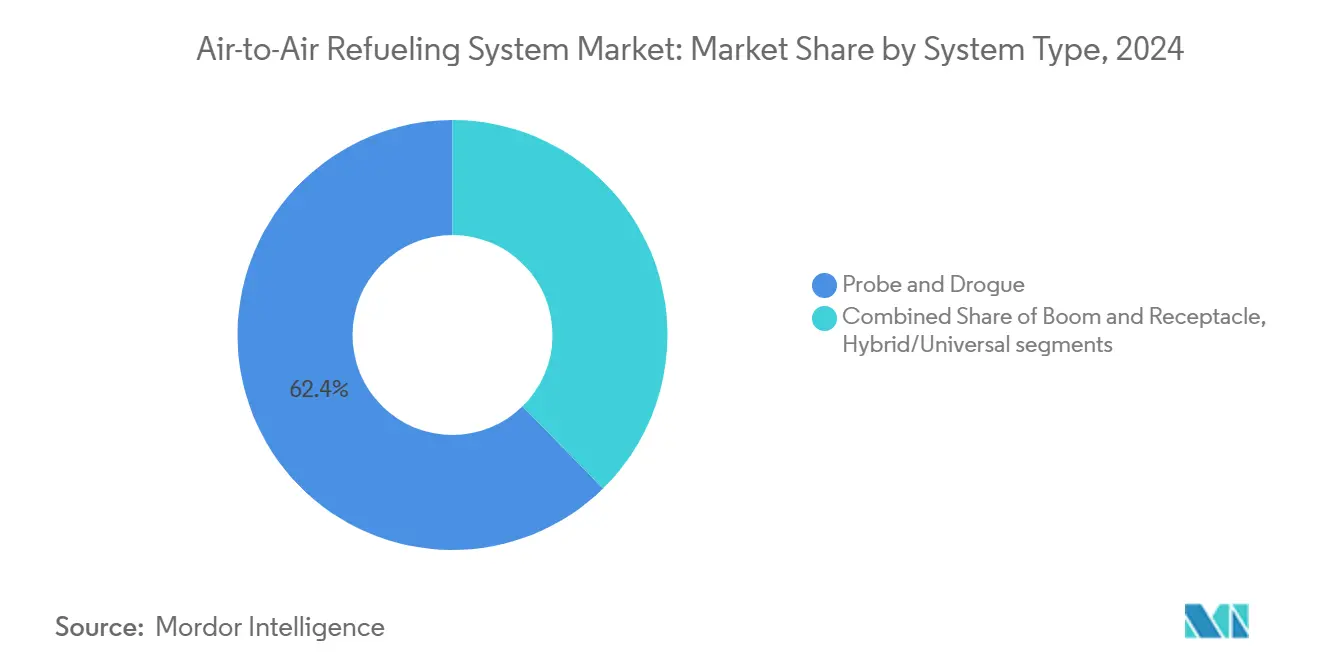

- By system type, the probe and drogue configuration held 62.35% of the air-to-air refueling system market share in 2024, while hybrid/universal systems are projected to grow at an 11.38% CAGR through 2030.

- By tanker platform, manned aircraft dominated with an 85.75% revenue share in 2024; unmanned aerial refueling vehicles are the fastest-growing platform, with a 12.45% CAGR to 2030.

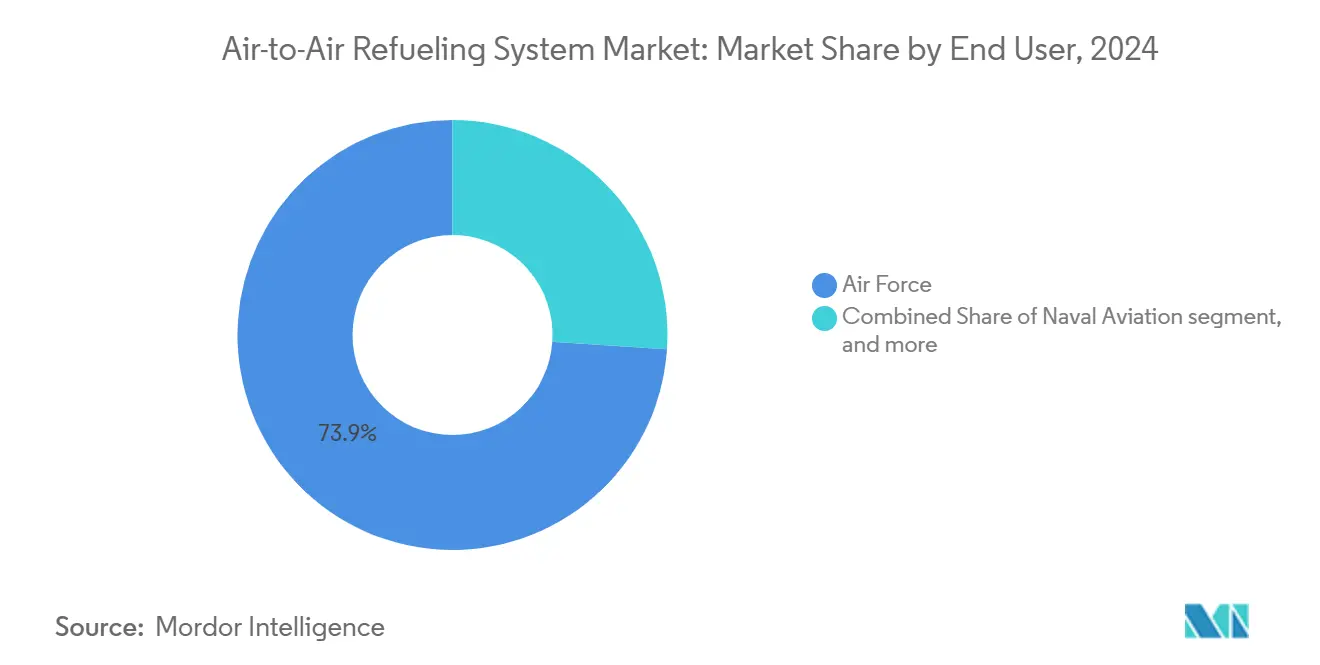

- By end user, air force operators accounted for 73.94% of the air-to-air refueling system market size in 2024, whereas naval aviation led growth at a 10.21% CAGR over the same period.

- By component, fuel tanks captured 42.41% of 2024 revenue, and probes are advancing at a 10.84% CAGR through 2030.

- By geography, North America led 40.87% of the air-to-air refueling system market share in 2024; Asia-Pacific is projected to expand at an 11.65% CAGR through 2030.

Global Air-to-Air Refueling System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing multi-domain operations demand | +2.10% | Global, early gains in Indo-Pacific and North America | Medium term (2-4 years) |

| Fleet life-extension programs for legacy tankers | +1.80% | North America and EU with allied spill-over | Long term (≥ 4 years) |

| Rising defense budgets of Asian countries | +2.30% | Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Autonomously-coupled UAV tankers | +1.90% | Global, earliest adoption in US Navy | Medium term (2-4 years) |

| In-orbit boom health-monitoring analytics | +1.20% | North America, EU advanced markets | Long term (≥ 4 years) |

| Adoption of predictive-maintenance “digital twin” analytics for booms, hoses and pumps | +1.40% | Global, tech-centric operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Multi-Domain Operations Demand

Forces synchronize air, land, sea, cyber, and space assets, creating new tanker performance benchmarks. The US Air Force’s deployment of KC-46A aircraft to Indo-Pacific bases underscores how refueling platforms must support simultaneous fighter, ISR, and transport missions.[1]Boeing, “Pride in the Pegasus,” boeing.com Artificial-intelligence-enabled flight-management systems now optimize fuel offload in real time, boosting mission flexibility and reducing crew workload. NATO’s standardized datalink protocols enhance cross-alliance interoperability, positioning allied fleets to refuel diverse receiver types during complex joint sorties. These factors elevate requirements for multi-nozzle capability, autonomous boom positioning, and rapid fuel accounting. As doctrine evolves, air-to-air refueling system market participants channel R&D into flexible architectures that handle heterogeneous receiver fleets without sacrificing sortie rhythm.

Fleet Life-Extension Programs for Legacy Tankers

Aging KC-135, A310 MRTT, and Il-78 airframes are undergoing deep structural and avionics overhauls instead of early retirement. For example, the KC-135 Block 45 upgrade replaces analog gauges with modern glass cockpits, extends mean flight hours between failures, and feeds condition-based maintenance algorithms. Operators choose life extension because unit costs for new widebody tankers exceed USD 180 million, while a full digital retrofit averages one-third that amount. European programs such as France’s A330 MRTT “Phénix” Standard 2 upgrade add electronic-warfare suites and SATCOM gateways, ensuring relevance in contested airspace.[2]Airbus, “How the Airbus A330 MRTT Helps Provide Security and Deliver Aid,” airbus.com Modernization also supports compliance with ICAO communication, navigation, and surveillance mandates, protecting access to civilian corridors. Collectively, these investments stimulate the air-to-air refueling system market by driving demand for advanced valves, hoses, sensors, and mission-system software.

Rising Asian Defense Budgets

Regional governments are boosting procurement to counterbalance-of-power shifts. Japan committed USD 4.1 billion for additional KC-46A tankers in 2024; South Korea validated KF-21 compatibility with KC-330 platforms, adding indigenous demand; and India has tapped commercial leases while evaluating future acquisitions to cover immediate gaps. These outlays propel supply-chain localization, such as composite hose production in South-East Asia and probe-manufacturing partnerships in India. The vast Pacific theater magnifies the operational premium on tanker range, pushing OEMs to integrate higher-capacity fuel cells and lighter structural alloys. This capital inflow underpins the air-to-air refueling system market’s double-digit regional CAGR.

Autonomously Coupled UAV Tankers

After completing the first unmanned refueling of an F/A-18, Boeing's MQ-25 now targets initial operational capability in 2026. The platform can transfer roughly 15,000 lb of fuel at 500 nmi from the carrier, extending fighter reach by up to 30%. Integrated relative-navigation sensors guide the boom without human input, a technological leap that will soon migrate to land-based fleets. Lockheed Martin's optional-pilot NGAS concepts illustrate how stealth tankers may accompany fifth-generation fighters into anti-access bubbles. Unmanned designs also alter cost calculus because a UAV's life-cycle expenditure is 30-40% below that of a crewed widebody aircraft. These developments expand the addressable air-to-air refueling system market, encouraging suppliers of pumps, valves, and vision systems to adapt hardware for higher-voltage electric architectures common in UAVs.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget sequestration risk in the US | -1.60% | North America with global supply-chain effects | Short term (≤ 2 years) |

| High retrofit integration cost | -1.30% | Worldwide, acute in emerging markets | Medium term (2-4 years) |

| Spectrum-congestion certification delays | -0.80% | Global, pronounced in dense airspace | Short term (≤ 2 years) |

| Export-control tightening on boom-control software | -1.10% | International markets excluding domestic US | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budget Sequestration Risk in the United States

Future federal belt-tightening could delay new tanker procurement and defer spare-parts funding. The US Air Force acknowledges that a USD 1.5 billion shortfall would ground hundreds of aircraft, including KC-135 variants, reducing tanker availability in strategic theaters.[3]United States Government Accountability Office, “Defense Budgetary Risks,” usa.gov OEMs mitigate this risk by offering performance-based logistics contracts that shift readiness responsibility to industry, but payment still hinges on stable appropriations. Should sequestration return, allied export sales may temporarily sustain production lines, yet supply-chain workforce attrition would remain a threat. The uncertainty depresses near-term award volumes and lengthens request-for-proposal cycles within the air-to-air refueling system market.

High Retrofit-Integration Cost

Modern multi-role tankers must house boom and probe-and-drogue kits, dual receptacle configurations, cyber-secure avionics, and open mission systems. Integrating these features into legacy airframes demands extensive structural reinforcement and flight-test campaigns. For instance, certification of the KC-46 Wing Aerial Refueling Pods required prolonged trials to validate aerodynamic stability, adding millions to program cost. For emerging-market operators, such expenses can exceed 60% of an aircraft’s book value, forcing trade-offs between capability depth and fleet size. High barriers restrain the pace at which small fleets can modernize, constraining addressable demand for the broader air-to-air refueling system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Hybrid Systems Drive Technological Convergence

The probe-and-drogue configuration held 62.35% of the air-to-air refueling system market share in 2024 because international operators value its compatibility with helicopters, fast jets, and maritime patrol aircraft. Variable-drag drogue designs now support speed envelopes from 100–325 knots, covering low-speed rotary missions and high-speed NATO receivers without airframe changes. Operators also favor the system’s lighter plumbing and more straightforward certification path, which lowers upfront modification costs for legacy transports and carrier aircraft. These advantages keep probe-and-drogue solutions central to current fleet strategies even as technology moves toward automation.

Hybrid or “universal” architectures are expanding at an 11.38% CAGR through 2030, making them the fastest-growing slice of the air-to-air refueling system market size. The KC-46A illustrates this shift by carrying both a fly-by-wire boom and hose-and-drogue pods, letting a single sortie service multiple receiver types and boosting fleet productivity. Airbus adds further momentum with its A330 MRTT automatic refueling suite, which reduces operator workload while improving safety margins during contact maneuvers. Looking ahead, US SHARK “buddy-store” programs could let fighters act as ad-hoc tankers, broadening distributed refueling concepts and raising demand for modular pod kits.

By Tanker Platform: Unmanned Vehicles Rewrite the Playbook

Manned tankers delivered 85.75% of revenue in 2024, yet UAV tankers will grow 12.45% annually through 2030. The MQ-25’s successful deck handling and refueling trials validate autonomous operations in carrier environments. Land-based heavy-lift designs on the drawing board promise stealthy apertures and reduced radar cross sections, enabling covert logistics inside anti-access areas.

While the traditional widebody tanker fleet remains indispensable for bulk fuel carriage, doctrinal shifts are apparent: distributed operations prioritize survivability and flexibility over single-platform capacity. As a result, the air-to-air refueling system market size for UAV hardware, software, and control stations will rise sharply, opening lanes for suppliers skilled in advanced composites, electric actuation, and secure datalinks.

By End User: Naval Aviation Accelerates

Air Force commands controlled 73.94% of spending in 2024, reflecting their expansive global posture. Naval aviation posts the highest 10.21% CAGR because carrier groups require organic tanker capacity to free fighters for their strike roles. Boeing’s MQ-25 alone could release up to five F/A-18s per deck cycle from buddy-refueling duty, translating to higher combat-air-patrol density.[4]Boeing, “MQ-25 Program Update,” boeing.com Amphibious-ready groups and surface fleets also experiment with ship-launched UAV tankers, broadening addressable demand.

Joint and special-operations communities value compact roll-on/roll-off kits, such as palletized hose-reel drums for C-130 variants. These niche requirements add incremental volume to the air-to-air refueling system market, particularly for modular plumbing and mission-planning software.

By Component: Probes Outpace Tanks

Fuel tanks accounted for 42.41% of revenue in 2024, driven by large monolithic cell deliveries for widebody platforms. Composite designs now combine puncture resistance with weight savings, supporting increased offload without sacrificing range. Though with a smaller base, probes will climb fastest at a 10.84% CAGR, spurred by growth in probe-equipped receivers across Asia and Europe.

Advanced probe systems feature retractable housings to reduce drag and radar signature. Sensor-rich nozzles supply real-time alignment feedback, which autonomous software translates into micro-adjustments. High-speed valve technology enables faster fuel flow rates while minimizing surge, making probes a critical differentiator in next-generation designs. Together, these shifts reinforce the upward trajectory of the air-to-air refueling system market.

Geography Analysis

North America commanded 40.87% revenue in 2024 as the US Air Force continued accepting KC-46A aircraft under a USD 2.4 billion Lot 11 contract for 15 additional units. Despite budget pressure, the region’s focus on predictive maintenance and autonomous refueling upgrades sustains procurement. Canada’s A330 MRTT program exemplifies allied spill-over, further cementing North American dominance.

Asia-Pacific is the fastest-growing territory at an 11.65% CAGR. Japan’s incremental KC-46A buys, South Korea’s KC-330 enhancements, and India’s hybrid leasing-and-buy strategy illustrate varied yet aggressive fleet-expansion paths. Vast oceanic distances amplify tanker demand, pushing operators toward higher-capacity hybrid systems. Consequently, regional suppliers ramp up composite hose and drogue production, reinforcing the air-to-air refueling system market size across the Pacific Rim.

Europe maintains steady growth under NATO’s Multinational MRTT Unit, which inducted its eighth A330 MRTT in 2024. Standardization boosts interoperability, and France’s “Phénix” Standard 2 upgrade signals a commitment to high-spec electronic warfare and connectivity suites. The Middle East and Africa see selective uptake, highlighted by the UAE’s additional A330 MRTT deliveries and nascent interest from North African states seeking strategic reach. Latin America remains a smaller, replacement-driven market, with Chile and Brazil exploring cost-effective retrofits over new builds.

Competitive Landscape

The market is moderately concentrated, with Boeing and Airbus controlling nearly all large multi-role tanker deliveries. Boeing’s KC-46 program has accrued over 200 million pounds of fuel offload and logged 100,000 flight hours, reinforcing platform maturity. Airbus leverages its commercial A330 foundation to secure over 90% of non-US orders, and the A330 MRTT+ promises an additional 8% fuel-burn improvement.

Component suppliers are more fragmented. Eaton’s USD 2.8 billion acquisition of Cobham’s refueling business formed a vertically integrated leader in hoses, drogues, probes, and valves.[5]Eaton, “Eaton Completes Acquisition of Cobham Mission Systems,” eaton.com Safran invests in digital-vision systems, while Moog refines fly-by-wire boom actuators. Commercial operators such as Omega Air Refueling expand contracted services, pioneering civil-registered boom operations that widen global service options. Technology leadership—especially in autonomy, digital twins, and sustainable-fuel compatibility—now trumps price competition, shaping the next phase of the air-to-air refueling system market.

Air-to-Air Refueling System Industry Leaders

Airbus SE

The Boeing Company

Eaton Corporation plc

Lockheed Martin Corporation

Israel Aerospace Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Boeing completed the handover of the first Lot 11 KC-46A, part of a USD 2.4 billion contract covering 15 units.

- September 2024: Japan received US government approval to acquire nine additional KC-46A tankers valued at USD 4.1 billion.

- July 2024: Airbus unveiled the A330 MRTT+ based on the A330-800, featuring 8% better fuel efficiency and extended range.

- June 2024: NATO’s Multinational MRTT Unit accepted its eighth A330 MRTT at Eindhoven Air Base, enhancing pooled refueling capacity.

Global Air-to-Air Refueling System Market Report Scope

| Boom and Receptacle |

| Probe and Drogue |

| Hybrid/Universal |

| Manned Tankers |

| Unmanned Aerial Refueling Vehicles Tankers (UAV-T) |

| Air Force |

| Naval Aviation |

| Joint/Other Services |

| Pumps |

| Valves and Nozzles |

| Hoses |

| Boom |

| Probes |

| Fuel Tanks |

| Other Components |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System Type | Boom and Receptacle | ||

| Probe and Drogue | |||

| Hybrid/Universal | |||

| By Tanker Platform | Manned Tankers | ||

| Unmanned Aerial Refueling Vehicles Tankers (UAV-T) | |||

| By End User | Air Force | ||

| Naval Aviation | |||

| Joint/Other Services | |||

| By Component | Pumps | ||

| Valves and Nozzles | |||

| Hoses | |||

| Boom | |||

| Probes | |||

| Fuel Tanks | |||

| Other Components | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the global forecast for the air-to-air refueling system market up to 2030?

The air-to-air refueling system market size is projected to reach USD 1.37 billion in 2030, advancing at a 10.26% CAGR from its 2025 base.

Which tanker platform segment shows the fastest growth?

Unmanned aerial refueling vehicles lead growth with a 12.45% CAGR, driven by programs like Boeing’s MQ-25.

Why are hybrid boom/probe systems gaining popularity?

Hybrid systems support diverse receiver fleets in a single sortie, boosting mission flexibility and lowering lifecycle cost, which fuels an 11.38% CAGR in this segment.

Which region is expanding fastest in aerial refueling capability?

Asia-Pacific posts the highest regional CAGR at 11.65%, propelled by Japan’s, India’s, and South Korea’s defense-budget increases.

What technologies are shaping the next generation of refueling systems?

Autonomy, digital-twin maintenance analytics, sustainable-fuel compatibility, and advanced composite probes dominate current R&D roadmaps.

How concentrated is the competitive landscape?

Boeing and Airbus dominate large-platform deliveries, yielding a high concentration score of 7.

Page last updated on: