Aircraft Flight Control Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

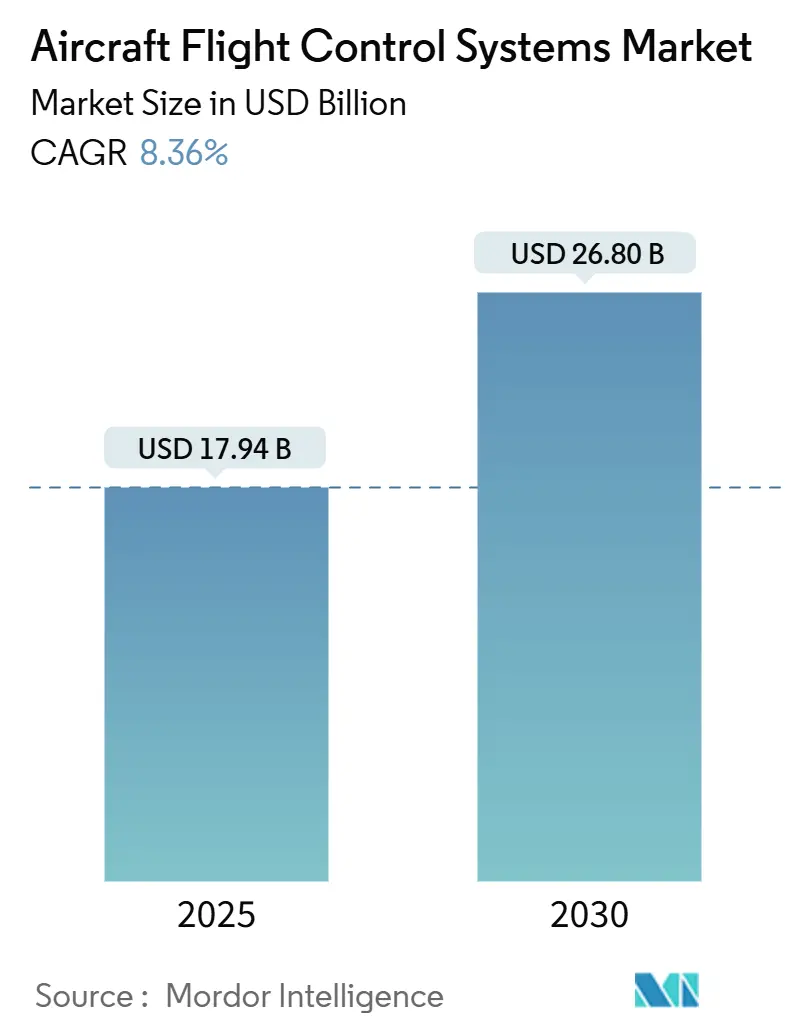

| Market Size (2025) | USD 17.94 Billion |

| Market Size (2030) | USD 26.80 Billion |

| Growth Rate (2025 - 2030) | 8.36% CAGR |

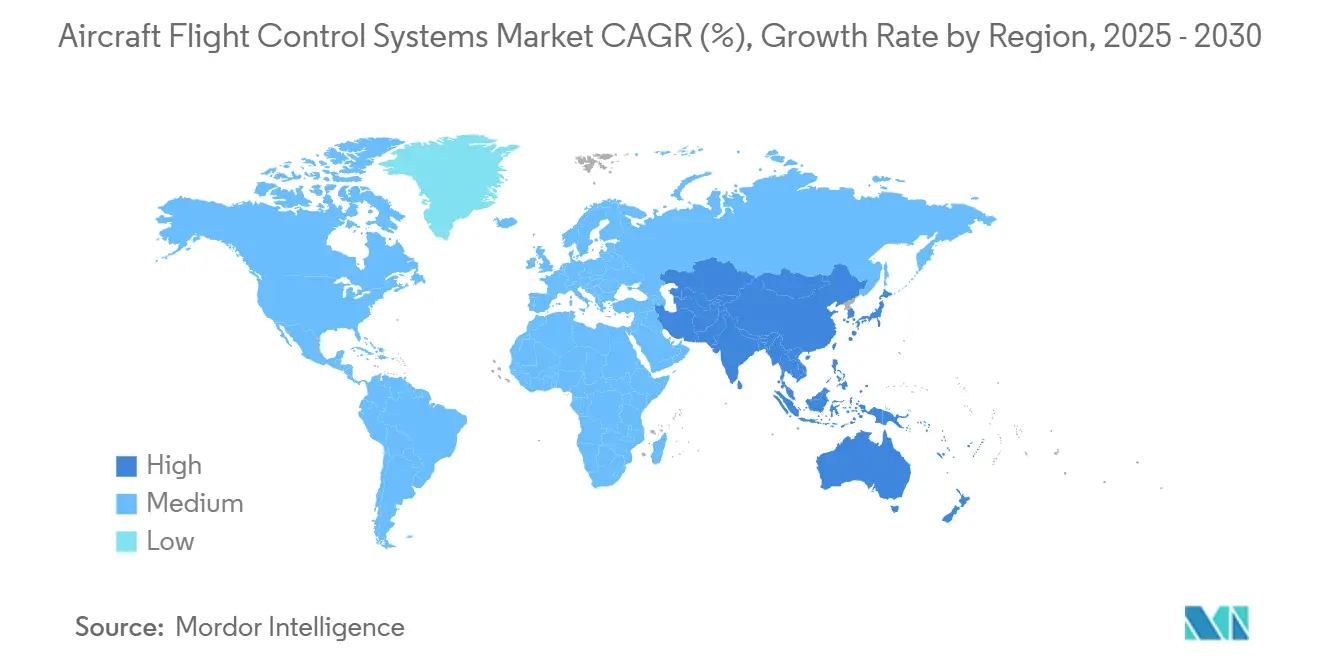

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Flight Control Systems Market Analysis by Mordor Intelligence

The aircraft flight control systems market size reached USD 17.94 billion in 2025 and is forecast to expand to USD 26.80 billion by 2030, registering an 8.36% CAGR. Growth is propelled by the commercial production rebound, military fleet modernization, and the industry-wide transition from hydraulic to electric actuation. North America retains demand leadership thanks to sustained defense spending, while Asia-Pacific gains momentum as regional carriers order next-generation narrowbodies. OEMs prioritize suppliers with proven cyber-resilient architectures, as 64% of recent aviation cyber events targeted networked assets. Consolidation among tier-one vendors continues, with Woodward’s agreement to acquire Safran’s electromechanical actuation unit underscoring the rush to secure electric-flight expertise.

Key Report Takeaways

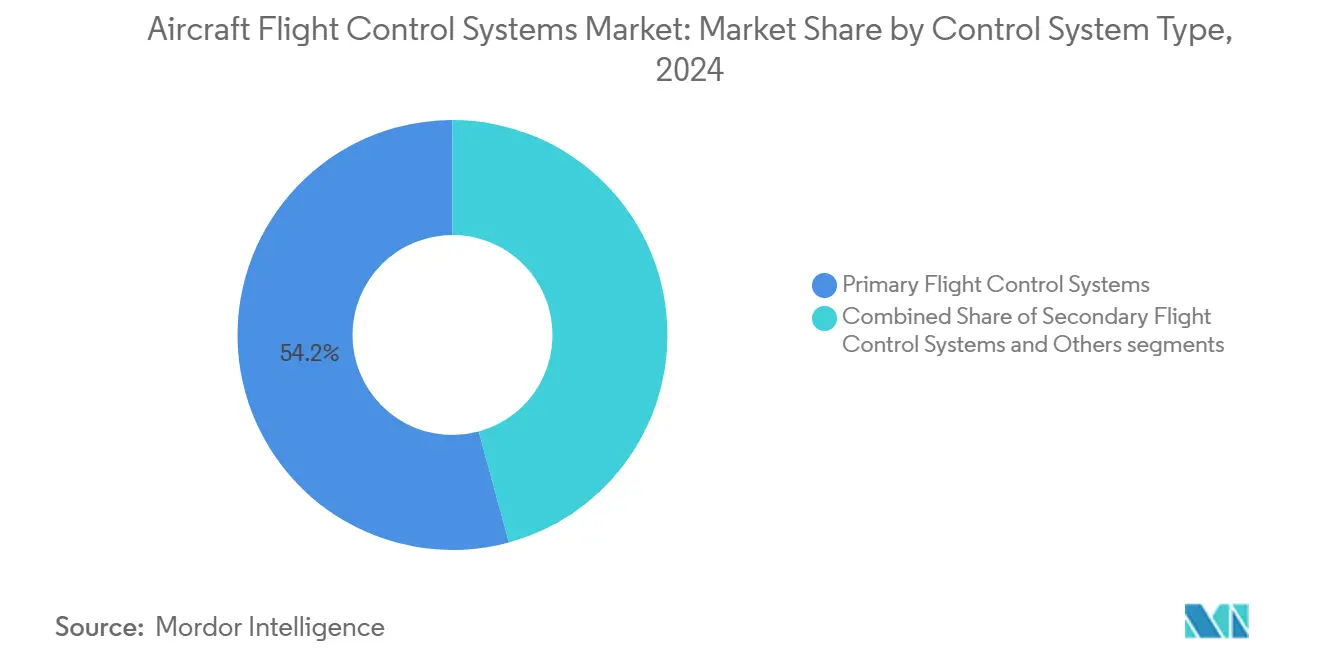

- By control system type, primary systems led with 54.23% revenue share in 2024; the same segment is projected to advance at a 9.21% CAGR through 2030.

- By component, flight-control computers held 53.88% of the aircraft flight control systems market share in 2024; the category is expected to post a 9.45% CAGR to 2030.

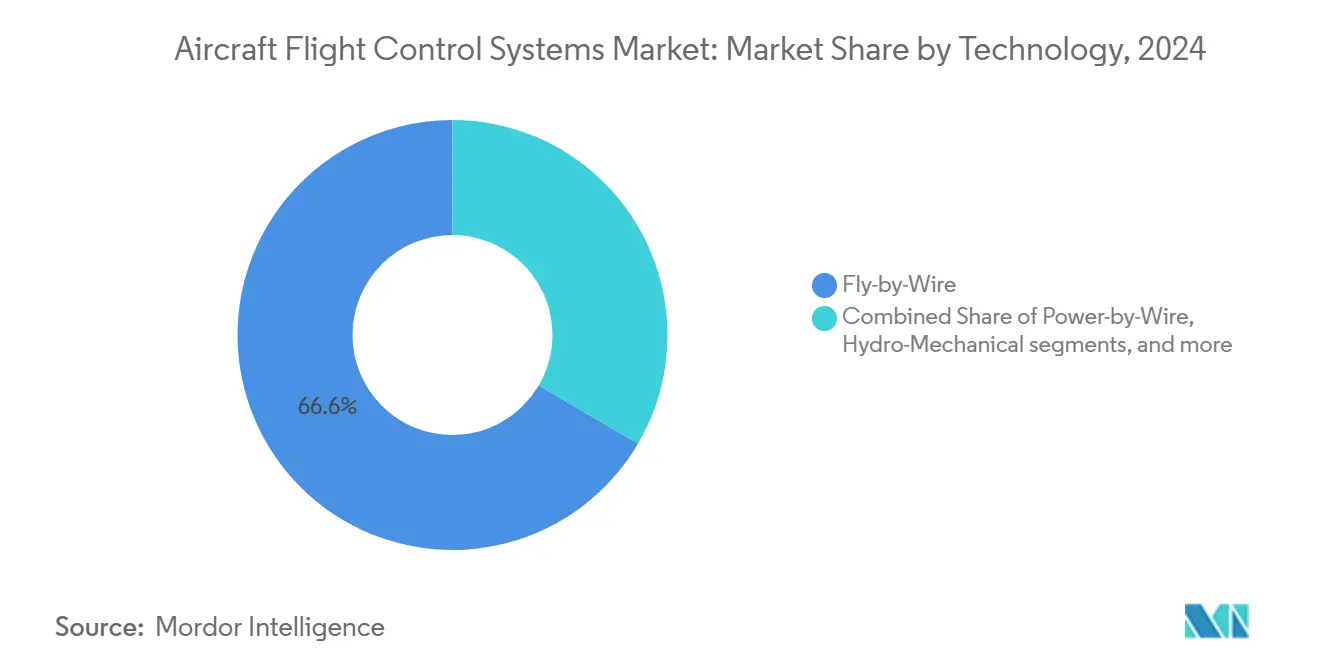

- By technology, fly-by-wire dominated with a 66.56% share in 2024; power-by-wire is set to grow fastest at a 10.21% CAGR through 2030.

- By aircraft type, commercial platforms accounted for 54.55% of 2024 revenue; advanced air mobility (AAM) platforms are forecast to expand at a 10.87% CAGR to 2030.

- By fit, line-fit installations captured 60.24% of 2024 revenue; retrofit demand is rising at an 8.75% CAGR to 2030.

- By geography, North America commanded 33.67% of 2024 sales; Asia-Pacific is on track for the highest regional growth, with a 9.10% CAGR to 2030.

Global Aircraft Flight Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovery in global commercial aircraft production driving system demand | +1.8% | North America and Europe | Medium term (2-4 years) |

| Military fleet modernization fueling adoption of advanced flight control technologies | +1.5% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Widespread shift to fly-by-wire and power-by-wire architectures for weight and maintenance reduction | +1.2% | Global | Long term (≥ 4 years) |

| Deployment of lightweight electro-mechanical actuators enabling urban air mobility platforms | +0.9% | North America and EU | Medium term (2-4 years) |

| Integration of AI-based active control for autonomous flight and envelope protection | +0.7% | Global, early adoption in North America | Long term (≥ 4 years) |

| Certification-driven emphasis on flight envelope protection for emerging eVTOL aircraft | +0.5% | North America and EU regulatory frameworks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Recovery in Global Commercial Aircraft Production Driving System Demand

Boeing’s 2024 outlook indicates nearly 44,000 new aircraft deliveries through 2043, reinstating stable production slots and a backlog of roughly 15,700 jets. Airlines are standardizing on fully digital flight controls to reduce pilot workload and cut fuel burn, particularly on single-aisle platforms that will comprise 71% of the future fleet. Growth in South and Southeast Asia is accelerating supplier partnerships with local carriers, yet 66% of aerospace firms still face parts shortages that pressure delivery schedules.

Military Fleet Modernization Fueling Adoption of Advanced Flight Control Technologies

BAE Systems secured 2024 contracts to upgrade F-15EX and F/A-18E/F flight-control computers, adding processing headroom and cybersecurity layers.[1]BAE Systems plc, “Flight-Control Computer Upgrades for F-15EX and F/A-18E/F,” baesystems.com The US Department of Defense’s USD 49 billion on-shoring program for semiconductors underpins component availability. Twelve successful AI-assisted F-16 sorties validate autonomous control algorithms migrating toward commercial use cases. Quad-redundant architectures verified in defense aircraft are becoming the blueprint for new civil transports.

Widespread Shift to Fly-by-Wire and Power-by-Wire Architectures for Weight and Maintenance Reduction

Collins Aerospace’s Enhanced Power and Cooling System reached TRL 6 in 2025, doubling the thermal headroom essential for high-voltage actuation.[2]RTX Corporation, “Enhanced Power and Cooling System Achieves TRL 6,” rtx.com Power-by-wire solutions cut system weight 15-20%, translating into measurable fuel savings across the lifecycle. FAA system-safety rules issued in August 2024 explicitly address electric-flight risks, accelerating certification pathways for OEMs willing to retire the hydraulic circuit.

Deployment of Lightweight Electro-Mechanical Actuators Enabling Urban Air Mobility Platforms

Liebherr delivers integrated electro-mechanical actuators (EMAs) for Eve Air Mobility’s eVTOL, eliminating gearboxes and trimming up to 50 kg per aircraft. Honeywell’s dual-lane architecture assures the fault tolerance required for urban routes where close-in operations demand rapid fail-safe transitions. Partnerships such as Supernal-UMBRAGROUP are setting new performance benchmarks for size, weight, and reliability in the sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development and certification costs for safety-critical flight control systems | -1.2% | North America and EU | Long term (≥ 4 years) |

| Strict reliability and redundancy compliance extending time-to-market | -0.9% | Global | Short term (≤ 2 years) |

| Supply chain shortages affecting precision servo valves and aerospace-grade electronics | -0.8% | Global regulatory frameworks | Medium term (2-4 years) |

| Cybersecurity risks associated with networked and connected flight control architectures | -0.6% | Global, heightened in connected aircraft operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Development and Certification Costs for Safety-Critical Flight Control Systems

FAA special conditions for new aircraft types now require exhaustive validation of novel architectures, adding USD 100 million and up to seven years to many programs. Smaller AAM entrants face steep financing hurdles, favoring incumbents with in-house certification know-how. The Bell 525 experience shows regulators writing bespoke criteria for each innovation cycle, slowing time-to-market.

Supply-Chain Shortages Affecting Precision Servo Valves and Aerospace-Grade Electronics

Sixty-six percent of aerospace companies report delayed component deliveries, with servo-valve and micro-electronics bottlenecks the most acute. Because commercial off-the-shelf chips seldom meet DO-254 requirements, OEMs redesign boards or dual-source strategic parts. Consolidation among tier-one vendors has further reduced redundancy, exposing programs to single points of failure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Control System Type: Primary Systems Lead Digital Evolution

Primary systems captured 54.23% of 2024 revenue, and their share of the aircraft flight control systems market size is on track to widen at a 9.21% CAGR through 2030. Adoption of AI-enabled envelope protection raises safety margins and supports semi-autonomous operations. Secondary systems remain essential for high-lift devices, yet electrification slowly displaces hydraulic trim tabs on new wings.

Demand for thrust-vectoring controls within experimental eVTOL designs adds niche growth. However, strict FAA safety-assessment rules mandate redundant monitoring, elevating system-integration complexity and cost. Continuous software updates extend functional life without hardware swaps, reinforcing vendors' dominant position controlling hardware and code bases.

By Component: Flight-Control Computers Anchor the Digital Stack

Flight-control computers owned 53.88% of component revenue in 2024 and headline the growth outlook at 9.45% CAGR, confirming their role as the brain of the aircraft flight control systems market. Quad-core processors enable model-based control while embedded cyber defenses counter network threats. Actuators are the second-largest slice; electro-mechanical variants show double-digit unit growth as airlines weigh life-cycle cost reductions.

Sensors and feedback devices expand steadily because higher control-law sophistication requires granular state data. EU plans to certify Level 1 AI support tools by 2025 are prompting computer suppliers to pre-qualify hardware for software upgrades, ensuring future compliance and smoother certification of autonomous features.

By Technology: Electrification Push Lifts Power-by-Wire Prospects

Fly-by-wire systems held 66.56% of 2024 sales, reflecting decades of reliability, yet power-by-wire is anticipated to post the highest 10.21% CAGR as OEMs retire central hydraulic circuits. Certification agencies now reference high-voltage safety cases, encouraging incremental adoption. Hydro-mechanical controls persist in legacy fleets but receive minimal R&D allocation.

Advances in motor efficiency and cooling unlock higher force densities, closing the performance gap with hydraulics. Thales’ new system delivers the same authority at half the mass, underscoring why airlines see electrification as a sustainability and maintenance play.

By Aircraft Type: Commercial Stronghold, AAM Upswing

Commercial airframes accounted for 54.55% of 2024 demand, reinforcing the sector’s core contribution to the aircraft flight control systems market. Widebody programs revive as long-haul travel rebounds, while narrowbodies remain the production workhorse. Advanced Air Mobility platforms, although small today, post the fastest 10.87% CAGR due to clear FAA operating rules issued in November 2024.

From F-15EX upgrades to next-generation rotorcraft, military procurement maintains a stable demand baseline. General aviation and regional jets uphold retrofit opportunities for digital upgrades, particularly where mandatory ADS-B or cybersecurity rules apply.

By Fit: Line-Fit Dominance Sustained, Retrofit Closes the Gap

Line-fit held 60.24% of 2024 installations, securing economies of scale in new-build programs. Retrofit applications, however, are on an 8.75% CAGR trajectory as operators commit to USD 58 billion of fleet-modernization projects over the next decade. The aircraft flight control systems market size for retrofits grows as STC holders roll out kit solutions that integrate seamlessly with older avionics.

Capacity constraints at MRO shops and limited OEM engineering bandwidth remain headwinds. Regulatory mandates on cybersecurity and connectivity add urgency, influencing airlines to prioritize flight-control upgrades during heavy-check intervals.

Geography Analysis

North America generated 33.67% of 2024 revenue, powered by a dense OEM–supplier network, substantial defense budgets, and proactive FAA rule-making that accelerates technology adoption.[3]Federal Aviation Administration, “Integration of Powered-Lift Aircraft; Final Rule,” faa.gov The region benefits from sustained fighter and bomber upgrade cycles and a single-aisle production recovery. Canada and Mexico complement the ecosystem through specialized machining and near-shore electronics assembly.

Asia-Pacific achieved the fastest 9.10% CAGR outlook, driven by fleet expansion that will triple regional aircraft counts to roughly 13,200 by 2034. China’s indigenous narrowbody programs create captive demand, while Japan’s avionics leadership and India’s maintenance-repair push amplify the need for digital flight controls. South-East Asian governments fund AAM testbeds, building local competence in power-by-wire systems.

Europe remains a technological force through Airbus programs and EASA’s cybersecurity mandates, which shape global compliance norms. The Clean Aviation SWITCH project underwrites hybrid-electric developments, lifting demand for high-voltage control electronics. The Middle East and Africa present emerging opportunities tied to fleet renewals and defense offsets, but limited domestic production capacity tempers growth for now.

Competitive Landscape

The aircraft flight control systems market exhibits high concentration, with Honeywell International Inc., RTX Corporation, Parker Hannifin Corporation, Moog Inc., and Safran SA dominating by multi-program content and certification portfolios. Woodward’s planned acquisition of Safran’s electromechanical actuation line extends vertical integration and signals continued consolidation.[4]Woodward Inc., “Agreement to Acquire Safran’s Electromechanical Actuation Business,” woodward.com Vendors increasingly combine in-house electronics with AI partnerships—Honeywell’s alliance with NXP exemplifies the shift toward software-defined architectures.

Emerging AAM players such as Vertical Aerospace introduce disruptive designs yet rely on tier-one suppliers for certifiable controls. Cybersecurity features now rank beside weight and reliability in airline RFPs, prompting suppliers to embed intrusion-detection at the actuator and computer level. Overall, innovation focuses on electrification, autonomy, and supply-chain resilience.

Aircraft Flight Control Systems Industry Leaders

Honeywell International Inc.

Moog Inc.

RTX Corporation

Safran SA

Parker Hannifin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: JetZero completed partnership agreements with Tier One suppliers for the Flight Control System components of its full-scale blended wing body (BWB) demonstrator.

- August 2024: The Boeing Company selected BAE Systems plc to upgrade the fly-by-wire (FBW) flight control computers (FCC) on its F-15EX Eagle II and F/A-18E/F Super Hornet fighter aircraft.

Global Aircraft Flight Control Systems Market Report Scope

| Primary Flight Control Systems |

| Secondary Flight Control Systems |

| Others |

| Flight-Control Computers |

| Actuators |

| Sensors and Feedback Devices |

| Others (Servo Valves, Trim and Tab Systems) |

| Fly-by-Wire |

| Power-by-Wire |

| Hydro-Mechanical |

| Electro-Mechanical |

| Commercial | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military | Combat |

| Transport | |

| Special Missions | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Unmanned Aerial Systems | Civil and Commercial |

| Defense and Government | |

| Advanced Air Mobility (AAM) | eVTOL |

| Urban Air Mobility (UAM) |

| Line Fit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Control System Type | Primary Flight Control Systems | ||

| Secondary Flight Control Systems | |||

| Others | |||

| By Component | Flight-Control Computers | ||

| Actuators | |||

| Sensors and Feedback Devices | |||

| Others (Servo Valves, Trim and Tab Systems) | |||

| By Technology | Fly-by-Wire | ||

| Power-by-Wire | |||

| Hydro-Mechanical | |||

| Electro-Mechanical | |||

| By Aircraft Type | Commercial | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military | Combat | ||

| Transport | |||

| Special Missions | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| Unmanned Aerial Systems | Civil and Commercial | ||

| Defense and Government | |||

| Advanced Air Mobility (AAM) | eVTOL | ||

| Urban Air Mobility (UAM) | |||

| By Fit | Line Fit | ||

| Retrofit | |||

| By Region | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the aircraft flight control systems market in 2030?

It is forecasted to reach USD 26.80 billion on an 8.36% CAGR trajectory.

Which region will grow fastest through 2030?

Asia-Pacific is expected to register a 9.10% CAGR driven by fleet expansion and AAM projects.

Why are power-by-wire systems gaining traction?

They remove hydraulic circuits, cut system weight by up to 20%, and lower maintenance costs.

Which component segment grows quickest?

Flight-control computers lead with a 9.45% CAGR as software-defined architectures expand.

How are cybersecurity risks being addressed?

Suppliers embed intrusion detection in computers and actuators while regulators add safety-assessment requirements.

Page last updated on: