Connected Aircraft Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

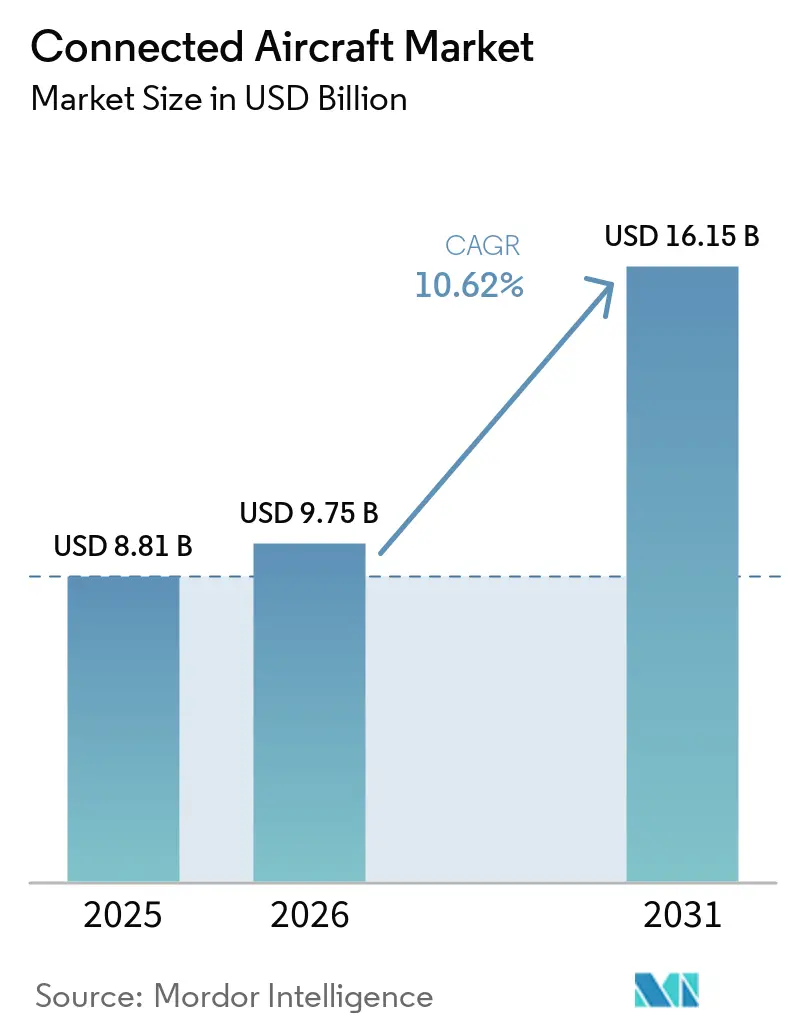

| Market Size (2026) | USD 9.75 Billion |

| Market Size (2031) | USD 16.15 Billion |

| Growth Rate (2026 - 2031) | 10.62% CAGR |

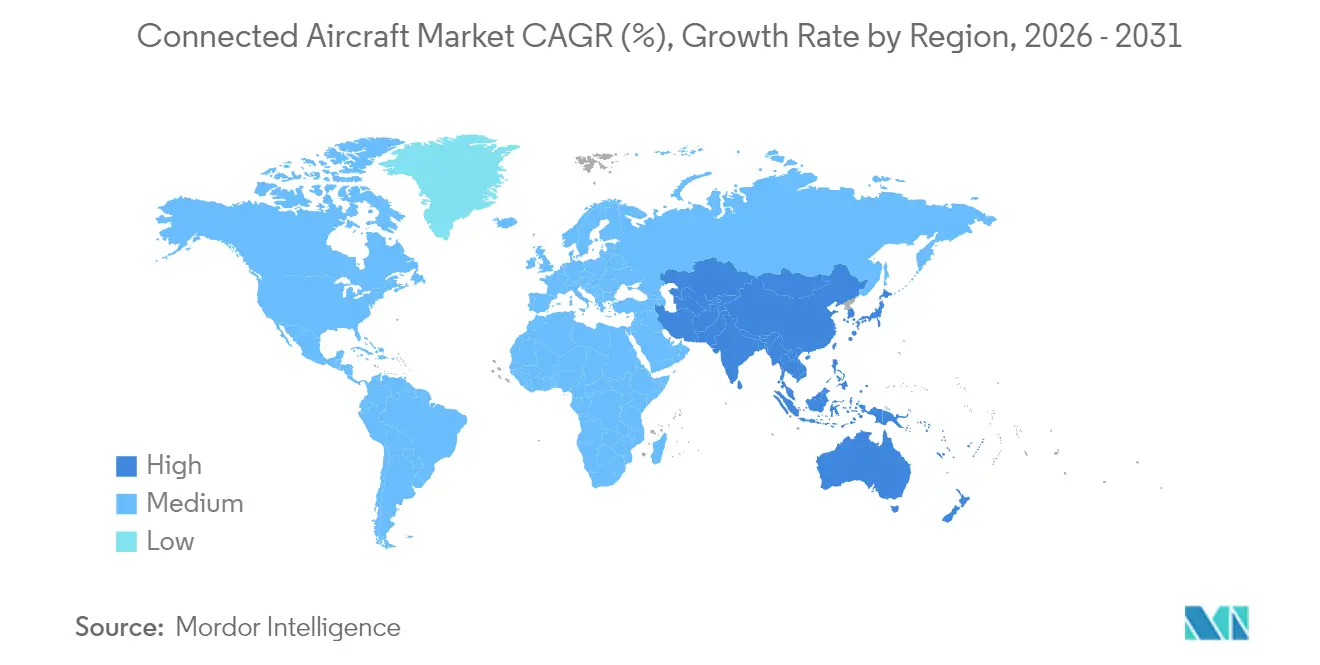

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connected Aircraft Market Analysis by Mordor Intelligence

The connected aircraft market size is expected to grow from USD 8.81 billion in 2025 to USD 9.75 billion in 2026 and is forecast to reach USD 16.15 billion by 2031 at 10.62% CAGR over 2026-2031. Sustained growth stems from rising passenger expectations for gate-to-gate broadband, mandated real-time tracking under the ICAO GADSS rule, and multi-orbit satellite deployments that cut latency and bandwidth cost. Airlines broadened retrofit programs to speed digital cabin upgrades, while defense ministries funded network-centric warfare projects that link fourth-generation fighters with advanced sensors. Competitive intensity stayed moderate as incumbents defended positions through long-term service contracts, yet faced pricing pressure from Starlink and other LEO entrants. Cyber-security rules, spectrum congestion, and high retrofit costs moderated near-term rollout plans but did not alter the long-term digital trajectory of the connected aircraft market.[1]Source: International Civil Aviation Organization, “Aircraft Tracking,” icao.int

Key Report Takeaways

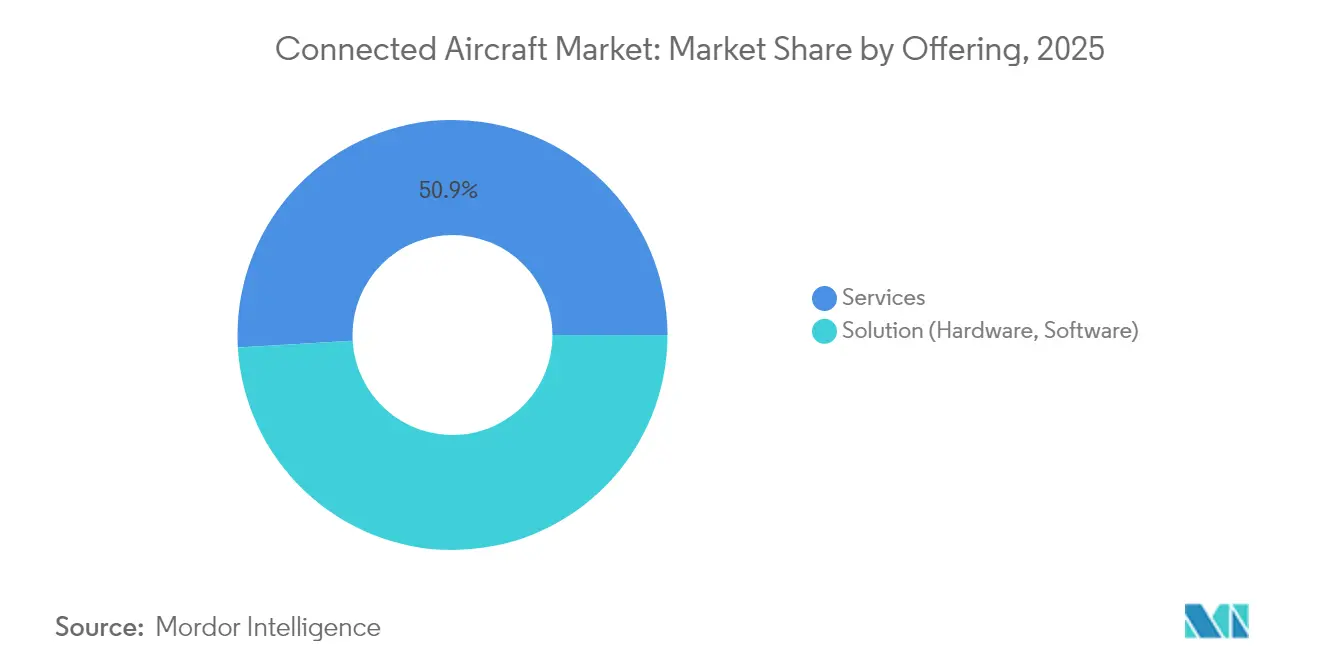

- By offering, services led with 50.92% of the connected aircraft market share in 2025; the segment also recorded the fastest 12.18% CAGR to 2031.

- By connectivity type, inflight connectivity held 61.85% revenue share in 2025, while air-to-ground solutions are projected to grow at 13.55% through 2031, driven by rising demand in the Connected Aircraft Market.

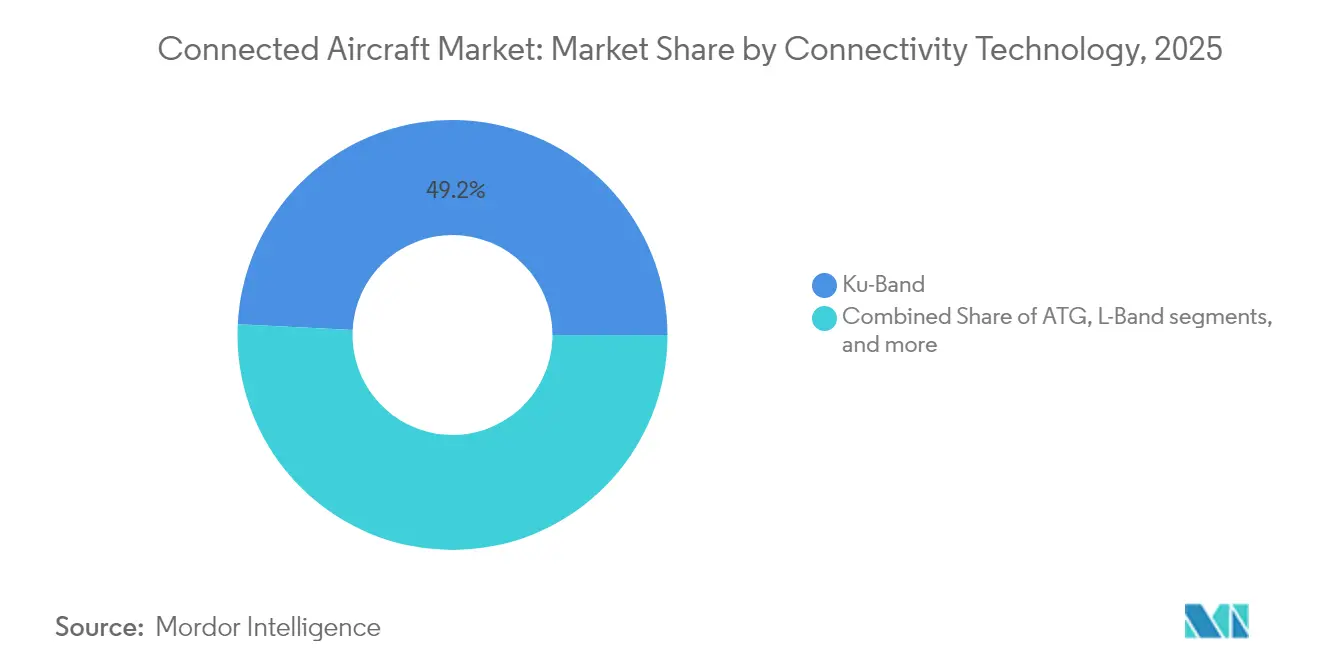

- By connectivity technology, satellite Ku-band commanded 49.20% share in 2025; satellite Ka-band is set to accelerate at 12.88% CAGR to 2031.

- By application, commercial aviation accounted for 69.55% of the connected aircraft market size in 2025, whereas general aviation is poised for a 11.95% CAGR to 2031.

- By geography, North America led with 38.35% share in 2025, while Asia-Pacific is forecasted to record the fastest 12.12% CAGR through 2031 in the Connected Aircraft Market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Connected Aircraft Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for passenger inflight connectivity | +2.8% | Global, highest in North America and Asia-Pacific | Medium term (2-4 years) |

| Adoption of network-centric warfare driving military connectivity | +1.9% | North America and Europe, expanding to Asia-Pacific allies | Long term (≥ 4 years) |

| Global ICAO GADSS mandate for real-time flight tracking | +1.5% | Global | Short term (≤ 2 years) |

| Fleet-wide retrofit programs by leading airlines | +1.7% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| LEO satellite constellations cutting bandwidth cost | +2.1% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Data-monetization-led ancillary revenue models | +1.4% | Global, led by North American carriers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Passenger Inflight Connectivity

Passenger expectations shifted from sporadic email access to streaming-grade bandwidth. An industry survey in 2024 found that 81% of South Korean travelers would rebook with airlines offering quality Wi-Fi, and 80% ranked connectivity important to the flight experience. Carriers like Delta expanded fast, free Wi-Fi to more than 720 aircraft, signaling a shift from paid service to a brand differentiator. Broadband-enabled ancillary revenue was projected to reach USD 30 billion by 2035, reinforcing connectivity as a strategic income stream.[2]Source: London School of Economics, “Sky-High Economics,” lse.ac.uk The connected aircraft market consequently prioritized passenger-facing upgrades, particularly in North America and Asia-Pacific, where digital engagement drives loyalty.

Adoption of Network-Centric Warfare Driving Military Connectivity

Defense agencies invested in airborne data links that fuse real-time intelligence across domains. The US Air Force Battle Network plan integrated aircraft into a unified digital architecture for seamless information exchange. Lockheed Martin’s Sniper Networked Targeting Pod created secure mesh networks between F-35s and fourth-generation fighters. Similar initiatives in the United Kingdom and NATO allies indicated international alignment, extending growth prospects for secure connectivity solutions across the connected aircraft market.

Global ICAO GADSS Mandate for Real-Time Flight Tracking

ICAO required autonomous distress tracking for aircraft over 27,000 kg starting January 2025, compelling airlines to install one-minute position reporting in emergencies. Airbus certified an Emergency Locator Transmitter with autonomous distress tracking, showing compliance pathways for manufacturers. The regulation’s global reach accelerated retrofit schedules and standardized connectivity baselines that support additional digital services in the Connected Aircraft Market.

LEO Satellite Constellations Cutting Bandwidth Cost

Multi-thousand-satellite constellations reduced latency and pricing, disrupting the legacy GEO model. Goldman Sachs forecasts the LEO segment to grow from USD 15 billion to USD 108 billion by 2035. Panasonic demonstrated seamless LEO-to-GEO hand-offs that delivered 193 Mbps forward link speeds in flight. United Airlines adopted Starlink for over 1,000 aircraft, showing how lower orbit economics enabled free passenger Wi-Fi in the Connected Aircraft Market.

Restraints Impact Analysis of Connected Aircraft Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retrofit and certification cost | -1.8% | Global, higher impact in cost-sensitive markets | Medium term (2-4 years) |

| Bandwidth / coverage limits on polar routes | -0.9% | Trans-polar corridors | Short term (≤ 2 years) |

| Cyber-security compliance delays | -1.2% | Europe and North America | Medium term (2-4 years) |

| Ku/Ka-band spectrum congestion | -0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Retrofit and Certification Cost

Cabin retrofits required expensive equipment, detailed supplemental type certificates, and aircraft downtime. The FAA estimated that cyber-secure connectivity for the US mobility fleet would cost USD 500 million. Airlines balanced these outlays against constrained capital as delivery delays from Airbus and Boeing limited new-build replacements.

Cyber-Security Compliance Delays

New regulations, such as EU Part-IS and FAA special conditions, obliged operators to adopt ISO 27001-based systems and prove resilience against unauthorized access. Airlines allocated time and resources to audits and system hardening, slowing some connectivity installations even as threat volumes rose 74% since 2020. These compliance requirements are reshaping cybersecurity investments across the Connected Aircraft Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Connected Aircraft Market Segment Analysis

By Offering:

Services Drive Managed Connectivity AdoptionServices held 50.92% of the connected aircraft market share in 2025 and are projected to grow at 12.18% CAGR through 2031, underscoring airline preference for turnkey solutions over hardware ownership. The connected aircraft market size for services is expected to expand in line with multi-year agreements that bundle equipment, certification, and 24/7 network operations. Airlines favored predictable operating expenses, particularly when rapid technology refresh cycles risked asset obsolescence.

Service providers deepened value propositions by offering continuous performance analytics, cybersecurity monitoring, and flexible bandwidth plans. Panasonic’s 10-year maintenance pact with Riyadh Air illustrated the lifecycle model that keeps fleets current without large upfront costs. Recurring revenue streams improved vendor cash visibility while enabling carriers to focus on customer experience and punctuality.

By Connectivity Type:

Inflight Connectivity Dominates Multi-Modal IntegrationInflight connectivity accounted for 61.85% of connected aircraft market share in 2025 as passenger digital lifestyles influenced product roadmaps. Given higher flight frequencies and brand touchpoints, airlines equipped narrowbody fleets first. Air-to-ground links emerged as the fastest-growing subsegment at 13.55% CAGR, supported by 5G surface networks that extend gate connectivity into the climb phase.

Future architectures will blend satellite, cellular, and aircraft-to-aircraft pathways for uninterrupted coverage. The Seamless Air Alliance advanced standards that integrate 3GPP 5G non-terrestrial networks, aligning performance across ground and orbit domains. This evolution keeps the connected aircraft market at the forefront of aviation digitalization.

By Connectivity Technology:

Ka-Band Leads Multi-Orbit EvolutionSatellite Ku-band retained a 49.20% share in 2025 due to its mature footprint and broad terminal base, yet Ka-band is forecast to expand at a 12.88% CAGR due to superior throughput. Honeywell promoted Ka-band speeds up to 20 Mbps, enabling HD streaming and cloud cockpit services. The connected aircraft market size for Ka-band solutions will rise as airlines migrate high-density routes to higher capacity links.

Multi-orbit concepts that combine GEO, MEO, and LEO satellites emerged as the de-risking strategy for polar coverage and redundancy. SES’s Open Orbits network and ThinKom’s tri-band antennas showed real-time switching among orbits without service dropouts.

By Application:

Commercial Aviation Anchors Market GrowthCommercial aviation represented 69.55% of the connected aircraft market size in 2025 as carriers raced to differentiate on passenger experience and operational efficiency. Narrowbody jets formed the largest installed base, while wide-body aircraft required premium multi-orbit packages to serve long-haul expectations. Cargo operators adopted real-time data links for unit load tracking and predictive maintenance.

General aviation is anticipated to post a 11.95% CAGR, reflecting corporate demand for office-in-the-sky bandwidth. Gogo’s Galileo LEO launch signaled strong uptake in this segment. Military fleets sustained steady procurement under network-centric doctrines, ensuring diversified demand across the connected aircraft industry.

Geography Analysis

North America Connected Aircraft Market

North America led the connected aircraft market in 2025 with a 38.35% share, supported by early compliance with GADSS, robust satellite infrastructure, and carrier commitments to fleet-wide free Wi-Fi. Delta, United, and American rolled out multi-orbit retrofits that aligned regional jets with mainline performance expectations. Defense programs like BACN and the F-22A modernization also lifted demand for secure links across US air assets.

Europe Connected Aircraft Market

Europe followed with strong regulatory impetus from EASA cybersecurity rules and pan-EU coordinated air traffic modernization. Flag carriers balanced passenger connectivity with operational priorities such as electronic flight bag integration and predictive maintenance platforms. The region’s satellite operators accelerated Ka-band deployments to defend their market position against LEO newcomers.

APAC Connected Aircraft Market

Asia-Pacific posted the fastest 12.12% CAGR outlook through 2031. China’s aviation services revenue was projected to rise from USD 23 billion in 2024 to USD 61 billion by 2043, embedding connectivity with a 5.6% CAGR within the broader digital services mix. Thai Airways partnered with Neo Space Group on 80 aircraft retrofits, and Korean Air began commercial B787 flights equipped with Viasat Ka-band. Government support for aviation infrastructure and rising middle-class travel sustained regional tailwinds.

Competitive Landscape

The connected aircraft market featured moderate concentration as incumbents maintained global support footprints while new entrants altered pricing dynamics. Panasonic Avionics, Viasat, and Thales held extensive installed bases and leveraged end-to-end packages that combined antennas, modems, cybersecurity, and certification services. Panasonic’s memorandum with Airbus to co-develop future connected aircraft platforms reinforced its OEM alignment.

SpaceX’s Starlink disrupted the market by offering high-speed service that enabled airlines to remove passenger fees. More than 2,000 aircraft commitments since 2022 underscored rapid traction, and FAA approval on Embraer 175s paved the way for regional fleet upgrades. Price competition prompted legacy operators to accelerate Ka-band and multi-orbit rollouts.

Consolidation reshaped supplier strategies. SES announced a USD 3.1 billion agreement to acquire Intelsat, targeting scale benefits in orbit diversity and managed services. Gogo acquired Satcom Direct for USD 375 million to broaden business aviation reach and capture government contracts. Vendors with polar connectivity, cybersecurity depth, or data-monetization analytics carved niches that large groups could not fully address.

Connected Aircraft Industry Leaders

Gogo Inc.

Viasat, Inc.

Thales Group

Panasonic Avionics Corporation

SITA N.V.

- *Disclaimer: Major Players sorted in no particular order

Connected Aircraft Market Companies Covered in this Report

- Panasonic Avionics Corporation

- Viasat, Inc.

- Thales Group

- Gogo Inc.

- RTX Corporation

- SITA N.V.

- Honeywell International Inc.

- Kontron AG

- Anuvu Operations LLC,

- Burrana Pty Ltd.

- Intelsat S.A.

- Astronics Corporation

- OnOneWeb Holdings Ltd.

- SkyFive AG

- Telekom Deutschland GmbH

- AeroMobile Communications Ltd.

- Hughes Network Systems, LLC

Recent Industry Developments in Connected Aircraft Market

- June 2025: Qatar Airways selected Panasonic Avionics’ Converix platform for 60 B777X aircraft, adding AI-powered virtual cabin crew and integrated data management.

- March 2025: United Airlines received FAA approval for Starlink-equipped Embraer 175s, targeting 300 installations by year-end.

- March 2025: Delta Air Lines chose Hughes Fusion multi-orbit connectivity for A350 and A321neo fleets, plus 400 existing aircraft.

Connected Aircraft Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the connected aircraft market as all fixed and rotary-wing platforms equipped with IP-based links that stream data between cabin, cockpit, and ground, covering onboard hardware, enabling software, and the satellite or air-to-ground bandwidth they consume. According to Mordor Intelligence, the value chain begins with spectrum and network owners and ends with airlines and defense forces that pay recurring connectivity fees.

Scope Exclusion: stand-alone passenger-paid Wi-Fi subscriptions sold after hardware installation are not quantified.

Segments Covered in This Report

- By Offering

- Solution (Hardware, Software)

- Services

- By Connectivity Type

- Inflight Connectivity

- Air-to-Ground Connectivity

- Air-to-Air Connectivity

- By Connectivity Technology

- Satellite – L-Band

- Satellite – Ku-Band

- Satellite – Ka-Band

- ATG (Air-to-Ground)

- By Application

- Commercial Aviation

- Narrowbody

- Widebody

- Regional Jets

- Commercial Helicopters

- Military Aviation

- Combat Aircraft

- Special Mission Aircraft

- Military Transport Aircraft

- Military Helicopters

- General Aviation

- Business Jets

- Others

- Commercial Aviation

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Mexico

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts spoke with avionics engineers, airline IFEC managers, satellite network planners, and defense program officers across North America, Europe, the Gulf, and Asia-Pacific. Their insights on retrofit labor, bandwidth price curves, and expected penetration trajectories filled information gaps and validated secondary inputs.

Desk Research

We pulled fleet counts, flight hours, and retrofit volumes from FAA and ICAO databases, Eurocontrol traffic dashboards, and EASA safety circulars, then linked them to antenna trade codes within UN Comtrade. Company filings, investor decks, and airline annual reports added price and uptake clues, while patents captured on Questel signaled upcoming technology shifts. Financial snapshots on D&B Hoovers and real-time news in Dow Jones Factiva flagged capacity expansions. The sources named illustrate breadth; many other reputable outlets were reviewed in building our dataset.

Market-Sizing & Forecasting

A top-down traffic and fleet reconstruction anchors the model. Global aircraft totals are multiplied by connectivity penetration and average annual spend per equipped tail. Supplier roll-ups and sampled deal checks provide bottom-up cross-tests before values are finalized. Key variables include passenger RPK growth, 5 G/LEO satellite launch schedules, retrofit cycle length, defense ISR funding, and service price per megabyte. Multivariate regression paired with scenario analysis projects each driver, while an ARIMA overlay smooths near-term shocks. Data voids in smaller regions are bridged with nearest-neighbor benchmarks that later pass expert review.

Data Validation & Update Cycle

Outputs undergo automated variance flags, peer checks, and senior analyst sign-off. We refresh annually and reopen models when material events, such as major spectrum auctions or fleet groundings, occur, ensuring clients always receive the latest view.

How Mordor Intelligence's Connected Aircraft Market Size Compares to Other Published Estimates

Published figures often diverge because firms choose different revenue buckets, fleet definitions, and refresh cadences.

Key gap drivers include whether retrofit labor is counted, the choice of satellite versus air-to-ground service prices, currency conversion timing, and the treatment of military platforms.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.16 billion | Mordor Intelligence | |

| USD 10.0 billion (2023) | Global Consultancy A | Uses list prices and assumes 100 percent penetration on new deliveries |

| USD 3.45 billion (2022) | Industry Journal B | Omits defense spending and most retrofit revenue |

These comparisons show that by aligning unit counts, realistic penetration curves, and verified price data, Mordor Intelligence offers a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the connected aircraft market?

The connected aircraft market reached USD 9.75 billion in 2026 and is projected to climb to USD 16.15 billion by 2031 at a 10.62% CAGR over 2026-2031.

Which segment holds the largest connected aircraft market share?

Inflight connectivity led by capturing 61.85% revenue share in 2025.

Why are airlines shifting to service-based connectivity contracts?

Services allow carriers to avoid heavy capital expenditure, gain 24/7 technical support, and keep pace with rapid satellite upgrades.

How does the ICAO GADSS rule affect market growth?

The rule mandates autonomous distress tracking from 2025, compelling airlines worldwide to install real-time connectivity hardware across fleets.

Which region is expected to grow fastest through 2031?

Asia-Pacific is forecast to expand at 12.12% CAGR, driven by fleet modernization and rising passenger Wi-Fi demand.

What role do LEO satellites play in the connected aircraft industry?

LEO constellations reduce latency, improve coverage, and lower bandwidth cost, enabling airlines to offer free streaming-quality Wi-Fi and reshaping supplier competition.

Page last updated on: