Aircraft Cabin Management Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.65 Billion |

| Market Size (2030) | USD 2.44 Billion |

| Growth Rate (2025 - 2030) | 8.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Cabin Management Systems Market Analysis by Mordor Intelligence

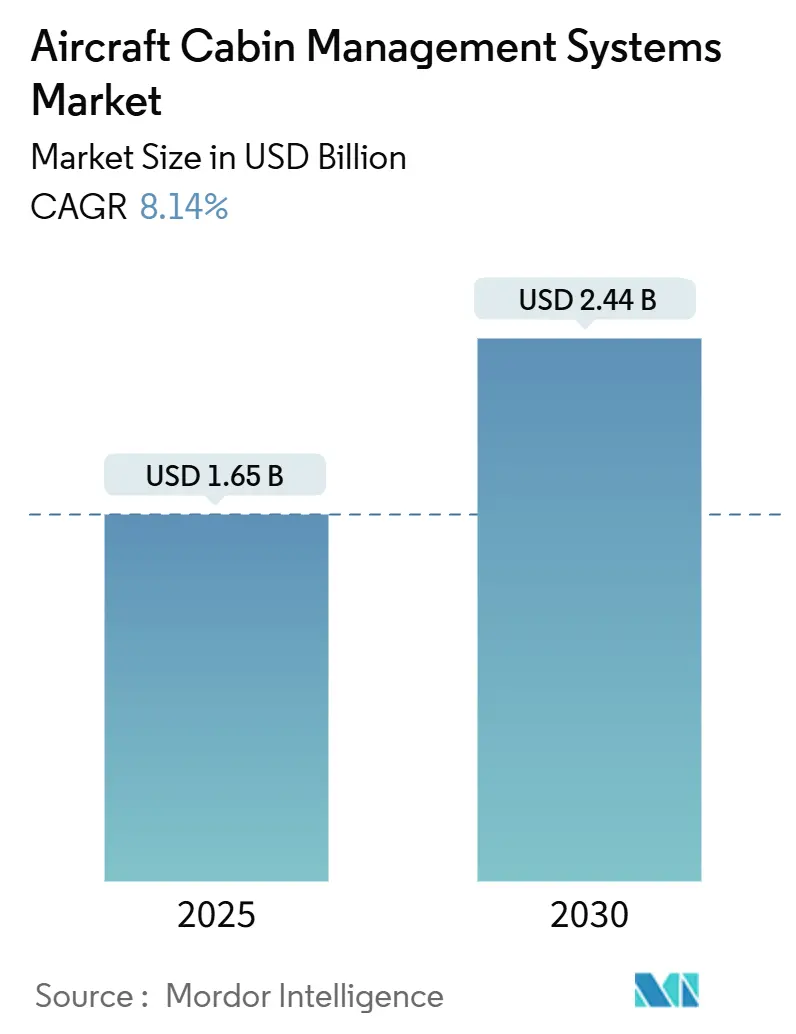

The current aircraft cabin management systems market size stands at USD 1.65 billion in 2025 and is forecasted to reach USD 2.44 billion by 2030, advancing at an 8.14% CAGR. This acceleration reflects airlines’ synchronized push to digitize cabin environments, monetize passenger data, and future-proof fleets against emerging regulatory mandates. Growing narrowbody output, rapid business jet deliveries, and high-bandwidth satellite roll-outs combine to lift demand across line-fit and retrofit channels. Component demand tilts toward software-defined network and connectivity suites as operators prioritize real-time analytics and personalized passenger controls. Meanwhile, OEM and Tier-1 suppliers use acquisitions to consolidate fragmented value chains, expand intellectual-property portfolios, and deliver turnkey cabin ecosystems that lower airlines’ integration risk.

Key Report Takeaways

- By aircraft type, narrowbody models held 46.24% of the aircraft cabin management systems market share in 2024, while business jets are projected to post the fastest 10.45% CAGR through 2030.

- By component, cabin management units and servers led with 26.78% revenue share in 2024; network and connectivity modules are set to expand at a 9.27% CAGR over the same horizon.

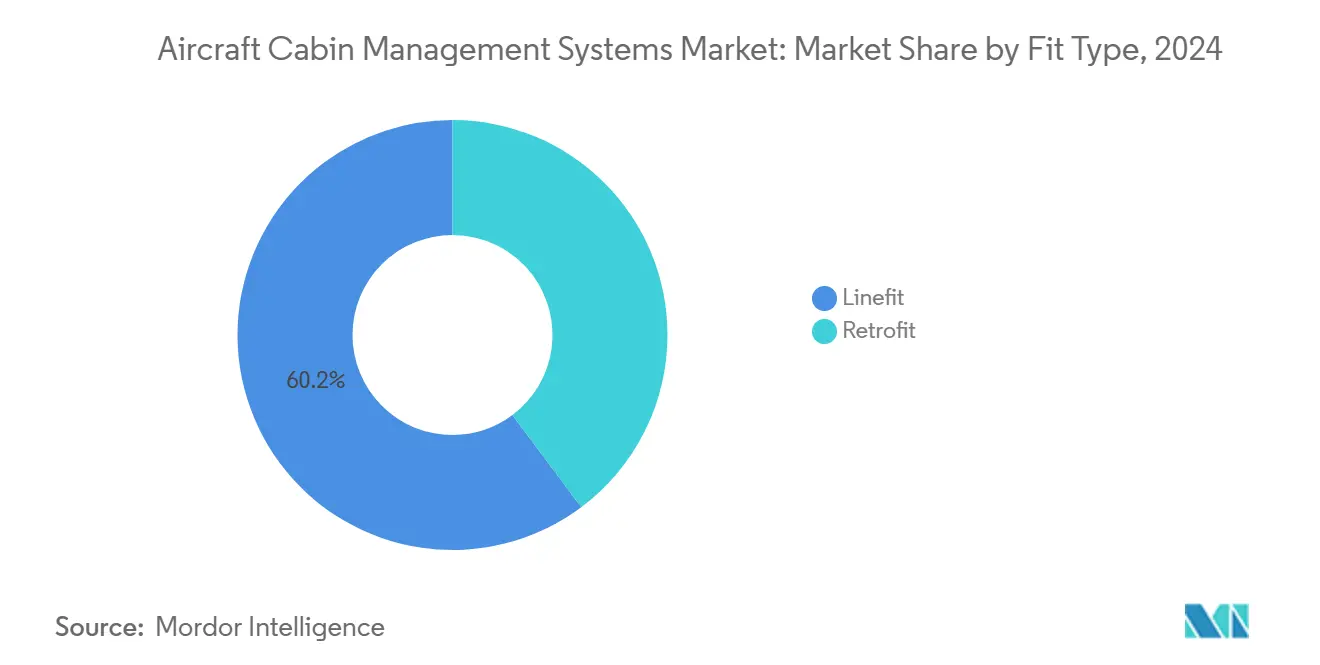

- By fit type, line-fit installations dominated with a 60.22% share in 2024, yet retrofit programs are pacing ahead at an 8.76% CAGR to 2030.

- By geography, North America captured 32.87% revenue in 2024, whereas Asia-Pacific is anticipated to log the highest 9.25% CAGR during the forecast period.

Global Aircraft Cabin Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing deliveries of next-generation narrowbody aircraft | +1.8% | Global; North America and Europe leading | Medium term (2-4 years) |

| Rising adoption of wireless and IoT-enabled cabin management architectures | +2.1% | Global; Asia-Pacific early adoption | Short term (≤ 2 years) |

| Surge in retrofit programs to upgrade legacy fleets with premium economy cabins | +1.5% | North America and Europe core, spill-over to APAC | Medium term (2-4 years) |

| Regulatory mandates promoting real-time cabin safety and environmental monitoring | +1.2% | Global; FAA and EASA leadership | Long term (≥ 4 years) |

| Shift in airline business models to monetize cabin data through ancillary services | +0.9% | Global; North America pioneering | Medium term (2-4 years) |

| Expansion of on-demand business aviation driving customized CMS deployments | +0.6% | North America and Europe, expanding to MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Deliveries of Next-Generation Narrowbody Aircraft

B737 MAX and A320neo production ramps are triggering synchronized demand for factory-installed digital cabin infrastructure. Standardized data networks embedded in the system build lower integration complexity for airlines and bring real-time analytics within reach, factors demonstrated by Southwest Airlines’ commitment to retrofit more than 800 B737s by December 2025.[1]Aviation Week, “Southwest To Begin 737 Fleet Retrofits Next Month,” aviationweek.com Elevated utilization of these aircraft keeps cabin systems in near-continuous service, intensifying the need for predictive-maintenance modules that minimize unplanned downtime and enhance fleet yield. Airlines forecast that every delivered narrowbody will enter service with embedded CMS, reducing lifetime retrofit costs and standardizing maintenance procedures. The surge also enables suppliers to amortize R&D across high-volume programs, lowering per-aircraft pricing and enlarging the addressable customer base.

Rising Adoption of Wireless and IoT-Enabled Cabin Management Architectures

IoT spending across commercial aviation rose to USD 7.4 billion in 2022 and is projected to exceed USD 50.9 billion by 2031, with cabin-sensor clusters leading growth.[2]Moment, “Top 3 of Inflight Digital Trends To Watch in 2025,” moment.tech Airlines like Delta have deployed phase-based lighting that auto-adapts to boarding, sleeping, and wake cycles, trimming crew workload and elevating customer experience. Edge-compute nodes process sensor data locally, cutting latency for seat-level environmental adjustments and boosting system reliability on long-haul sectors. Streaming health-monitoring data from seats, galleys, and lavatories allows predictive maintenance scheduling, improving aircraft turnaround times. These wireless architectures also reduce harness weight, supporting airlines’ sustainability goals without compromising passenger-service enrichment.

Surge in Retrofit Programs to Upgrade Legacy Fleets with Premium Economy Cabins

The average global fleet age moved to 14.8 years, compelling carriers to modernize interiors rather than wait for delayed deliveries. Emirates scaled its cabin overhaul to 220 aircraft, while Etihad allocated USD 1 billion to similar programs. Premium-economy installations require integrated seat-control, lighting, and IFE synchronization, driving incremental demand for up-rated cabin-management software and power-efficient hardware. Delta and Southwest have aligned major CMS retrofits with heavy-maintenance checks, minimizing incremental ground time while maximizing customer-facing upgrades. Suppliers benefit from predictable slot windows that smooth production planning and raise throughput efficiency.

Regulatory Mandates Promoting Real-Time Cabin Safety and Environmental Monitoring

The FAA’s evolving standards call for continuous air quality surveillance, emergency-equipment readiness, and passenger flow, elevating baseline sensor counts and data-bus throughput. Suppliers must embed redundancy and fail-safe logic that meets stringent DO-178C software guidelines. EASA is running parallel initiatives emphasizing environmental-parameter traceability, forcing global carriers to align with the most demanding rules to maintain cross-border fleet flexibility. Certification packages now routinely include cyber-resilience and data-integrity test plans, lengthening documentation cycles but enhancing passenger safety. Over time, unified global standards are expected to compress multi-region compliance costs and spur broader technology adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of certification and compliance with DO-178C/DO-254 standards | -1.4% | Global; stricter in North America and Europe | Long term (≥ 4 years) |

| Growing cybersecurity concerns in digitally connected cabin environments | -1.1% | Global; heightened focus in developed markets | Short term (≤ 2 years) |

| Persistent supply chain constraints for specialized avionics-grade components | -0.8% | Global; acute shortages in Asia-Pacific manufacturing | Medium term (2-4 years) |

| Reduced airline capital expenditure due to sustainability and SAF-related investments | -0.7% | Global; European carriers ahead in SAF | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Certification and Compliance with DO-178C/DO-254 Standards

Developing a Level A cabin-management application can cost USD 2 million and extend verification timelines beyond 24 months, locking up engineering resources and slowing innovation. Smaller entrants often defer upgrades or exit the market because recertification of minor software updates triggers a new compliance cycle. Extensive requirement-based testing, structural-coverage analysis, and independent verification add layers of documentation that inflate overhead. Investors demand predictable returns, yet protracted certification milestones can stretch project payback horizons. As a result, incumbents with amortized toolchains and larger DER pools widen their competitive moat.

Growing Cybersecurity Concerns in Digitally Connected Cabin Environments

The FAA’s draft rule on aircraft cybersecurity obliges carriers to demonstrate continuous protection of cabin networks against external intrusion. System suppliers must now integrate threat-detection agents and secure-boot architectures, inflating bill-of-materials costs and prolonging installation. Airlines also need specialized teams to manage patches across mixed-generation fleets, adding new layers of operating expense. Reputational risk from ransomware-induced service disruptions elevates board-level scrutiny of new CMS procurements. Pending global guidelines could tighten approval gates further, pushing some projects into later budget cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbody Scale Meets Business-Jet Customization

Narrowbody aircraft collectively represented 46.24% of the aircraft cabin management systems market size in 2024, benefiting from common-type rating efficiencies that enable operators to standardize cabin electronics across large fleets. Airlines use these platforms to deploy unified content-delivery networks and energy-saving lighting programs that shrink per-seat operating costs. Looking ahead, narrowbody growth will hinge on OEM commitment to higher-capacity single-aisle variants that support long-range missions and require more advanced environmental-control loops to maintain passenger comfort.

While accounting for a smaller revenue pool, business jets are forecast to clock a 10.45% CAGR—the fastest within the aircraft cabin management systems market—because on-demand charter and fractional-ownership models multiply the number of aircraft requiring premium, personalized systems. Custom sound zones, biometric cabin entry, and satellite-supported videoconferencing are becoming baseline specifications for new-build Gulfstream and Bombardier models. Suppliers who blend modular hardware with software-driven customization fetch price premiums that lift margin mixes even amid relatively low production volumes.

By Component: Connectivity Infrastructure Reshapes Feature Roadmaps

Cabin management units and servers held a 26.78% 2024 revenue share. Yet, the momentum clearly lies with network and connectivity modules expanding at a 9.27% CAGR in the aircraft cabin management systems market. Airlines migrating to low-earth-orbit satellite services view gigabit-class throughput as a ticket to streaming entertainment and real-time e-commerce, which in turn fuels installations of multi-access edge-compute routers and high-gain antennas.

Software continues to absorb formerly hardware-bound functionality. Modern graphical user interfaces push updates over the air, enabling seasonal theme changes and quick rollouts of ancillary revenue widgets without taking aircraft out of service. Suppliers that master cyber-hardened middleware and open-API frameworks stand to pivot from one-time equipment sales to high-margin licensing and analytics subscriptions, reinforcing a transition toward service-centric revenue streams inside the aircraft cabin management systems industry.

By Fit Type: Retrofit Momentum Counters Line-Fit Dominance

Linefit programs commanded 60.22% revenue share in 2024 because OEM installation simplifies certification and spreads cost over the aircraft’s financing term. A320 family and B737 MAX line integrate distributed power architectures that make adding cabin sensors plug-and-play, trimming per-aircraft labor hours, and lowering warranty risk.

Even so, retrofit demand is gaining pace at an 8.76% CAGR through 2030 as delivery slots tighten and sustainability metrics encourage carriers to maximize existing asset utility. Southwest’s ambitious plan to refurbish more than 800 B737s by December 2025 exemplifies the sheer scale of retrofit activity. MRO shops are responding with modular installation kits and pre-certified wiring looms that can be swapped during overnight checks, compressing ground-time and safeguarding fleet availability.

Geography Analysis

North America accounted for 32.87% of 2024 revenue within the aircraft cabin management systems market, underpinned by long-established manufacturing nodes and FAA-driven regulatory clarity. The region’s dense concentration of major airlines promotes fleet-wide deployment of standardized cabin platforms, creating steady replacement cycles for successive hardware and software upgrades. Integrated supply chains—exemplified by Collins Aerospace’s Winston-Salem interiors facility—further streamline certification workflows and shorten lead times.

Asia-Pacific is projected to log a 9.25% CAGR through 2030, the fastest of any region. China and India are leading the regional surge in fleet additions, while low-cost carriers (LCCs) across Southeast Asia accelerate cabin retrofits to keep product offerings competitive. Labor-cost advantages allow operators to carry out large-scale interior overhauls at lower capital outlays, though ongoing semiconductor bottlenecks still pose execution risk. Airbus predicts the total Asia-Pacific services pie will double to USD 129 billion by 2043, outlining a robust runway for connected-cabin investments.[3]Routes Online, “Aircraft Interiors – industry development summary: Jan/Feb-2025,” routesonline.com

Europe maintains a solid but slower expansion path as premium carriers channel budgets into lightweight, energy-efficient cabin solutions that dovetail with their decarbonization roadmaps. EASA’s rigorous oversight drives early adoption of air-quality monitoring and fire-suppression upgrades, pushing local airlines—and their suppliers—to pioneer safety-led designs that eventually proliferate worldwide. However, high SAF-related spending can crowd out near-term retrofits, nudging some carriers to extend refurbishment timelines.

Competitive Landscape

The aircraft cabin management systems market remains moderately fragmented, though recent transactional activity signals a gradual consolidation trend. Astronics Corporation and Burrana, for example, co-developed open-platform seat-centric IFE modules that enable third-party app deployment, reducing airline vendor lock-in.

Competitive advantage focuses on software-defined architectures and data analytics engines. Legacy hardware specialists are forging alliances with Silicon Valley-style startups to import agile sprint methodologies and cloud-native toolchains.

Certification prowess remains a decisive moat. Tier-1 incumbents such as Collins Aerospace and Honeywell retain sizable in-house DER (Designated Engineering Representative) pools that speed compliance across multiple jurisdictions. New entrants face prohibitive time-to-market if targeting DO-178C Level A functions, steering many toward non-safety-critical entertainment or lighting sub-niches within the broader aircraft cabin management systems market.

Aircraft Cabin Management Systems Industry Leaders

Honeywell International Inc.

Astronics Corporation

Diehl Stiftung & Co. KG

Panasonic Avionics Corporation (Panasonic Corporation)

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Cyient DLM expanded its partnership with Deutsche Aircraft through a multi-year contract. Under this agreement, Cyient DLM will design, develop, and manufacture the Cabin Management System (CMS) for the D328eco, a 40-seater regional turboprop aircraft.

- October 2024: Collins Aerospace delivered its new Venue cabin management system (CMS). The system features smart monitors and an enhanced graphical user interface (GUI), improving operators' and passengers' entertainment capabilities and user experience.

Global Aircraft Cabin Management Systems Market Report Scope

| Narrowbody |

| Widebody |

| Regional Jets |

| Business Jets |

| Cabin Management Units and Servers |

| Control Panels and Interfaces |

| Network and Conncectivity |

| Audio/Video System Units |

| Cabin Management Software |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Narrowbody | ||

| Widebody | |||

| Regional Jets | |||

| Business Jets | |||

| By Component | Cabin Management Units and Servers | ||

| Control Panels and Interfaces | |||

| Network and Conncectivity | |||

| Audio/Video System Units | |||

| Cabin Management Software | |||

| By Fit Type | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 valuation of the aircraft cabin management systems market?

The market is valued at USD 1.65 billion in 2025 and is forecasted to reach USD 2.44 billion by 2030, advancing at an 8.14% CAGR.

Which aircraft category is expanding the fastest in cabin management adoption?

Business jets are projected to grow at a 10.45% CAGR through 2030, driven by premium customization demand.

How important are retrofit programs to future demand?

Retrofits are forecasted to outpace line-fit growth at an 8.76% CAGR because airlines are extending fleet life amid delivery delays.

Why is Asia-Pacific expected to lead regional growth?

Rapid fleet expansion in China and India pushes Asia-Pacific toward a 9.25% CAGR as airlines invest in digitally connected cabins.

Which component segment is currently accelerating fastest?

Network and connectivity modules are advancing at a 9.27% CAGR due to bandwidth-heavy services like streaming and edge analytics.

How are regulatory mandates shaping system specifications?

FAA and EASA requirements for real-time safety and environmental monitoring are driving integration of redundant sensor networks and certified software architectures.

Page last updated on: