Aircraft Refurbishing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

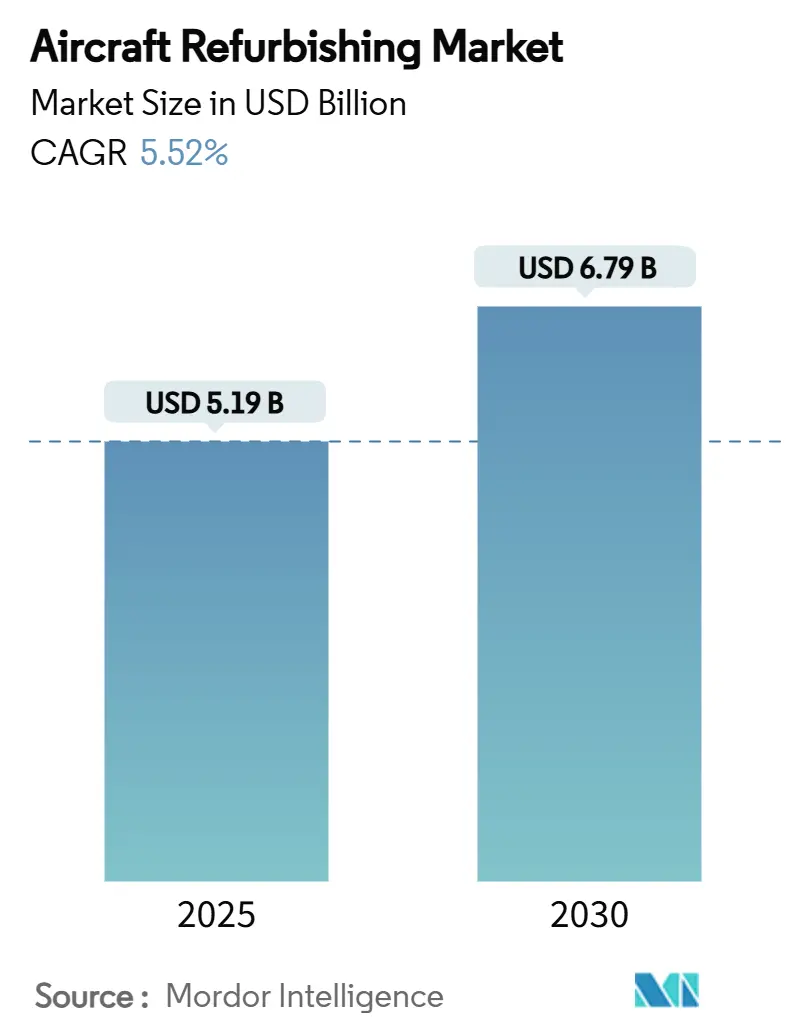

| Market Size (2025) | USD 5.19 Billion |

| Market Size (2030) | USD 6.79 Billion |

| Growth Rate (2025 - 2030) | 5.52% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Refurbishing Market Analysis by Mordor Intelligence

The aircraft refurbishing market is currently valued at USD 5.19 billion in 2025 and is forecasted to reach USD 6.79 billion by 2030, expanding at a 5.52% CAGR. Airlines are intensifying fleet-optimization strategies because supply-chain constraints have stretched new-aircraft delivery slots beyond seven years, making cabin and systems upgrades the faster route to capacity and revenue growth. Heightened passenger-experience competition, e-commerce cargo demand, and tightening sustainability mandates collectively reshape investment priorities. Interior refurbishing leads spending as carriers chase yield uplift from premium-seat retrofits, while exterior work gains momentum on fuel-saving coating technologies. Regionally, North America retains scale leadership, but rapid fleet expansion in Asia-Pacific positions that region as the long-term volume growth engine. Competitive rivalry remains moderate because certification barriers, capital intensity, and skilled-labor scarcity temper new entry despite solid demand visibility.

Key Report Takeaways

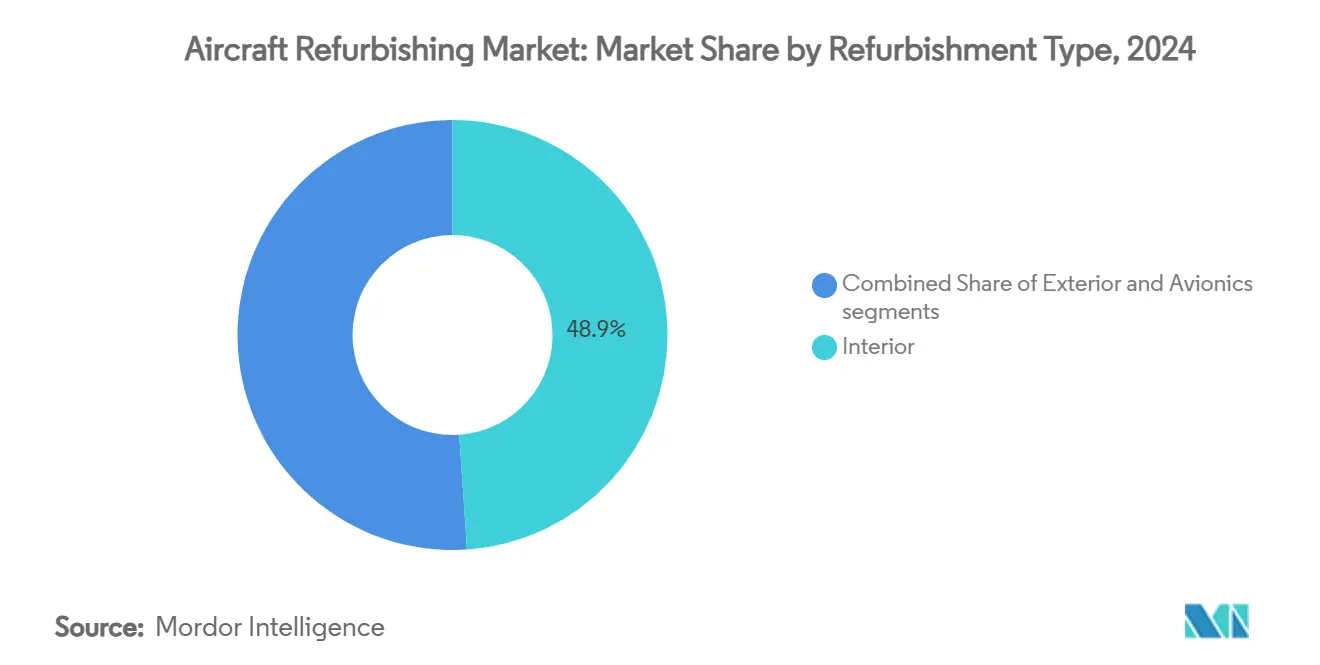

- By refurbishment type, interior refurbishing led with 48.92% of the aircraft refurbishing market share in 2024; exterior refurbishing is advancing at a 7.23% CAGR through 2030.

- By component, seats accounted for a 38.65% share of the aircraft refurbishing market size in 2024, while IFEC systems are projected to expand at a 6.21% CAGR to 2030.

- By aircraft type, narrowbody platforms held 44.22% of the aircraft refurbishing market share in 2024; regional jets recorded the highest CAGR at 8.38% through 2030.

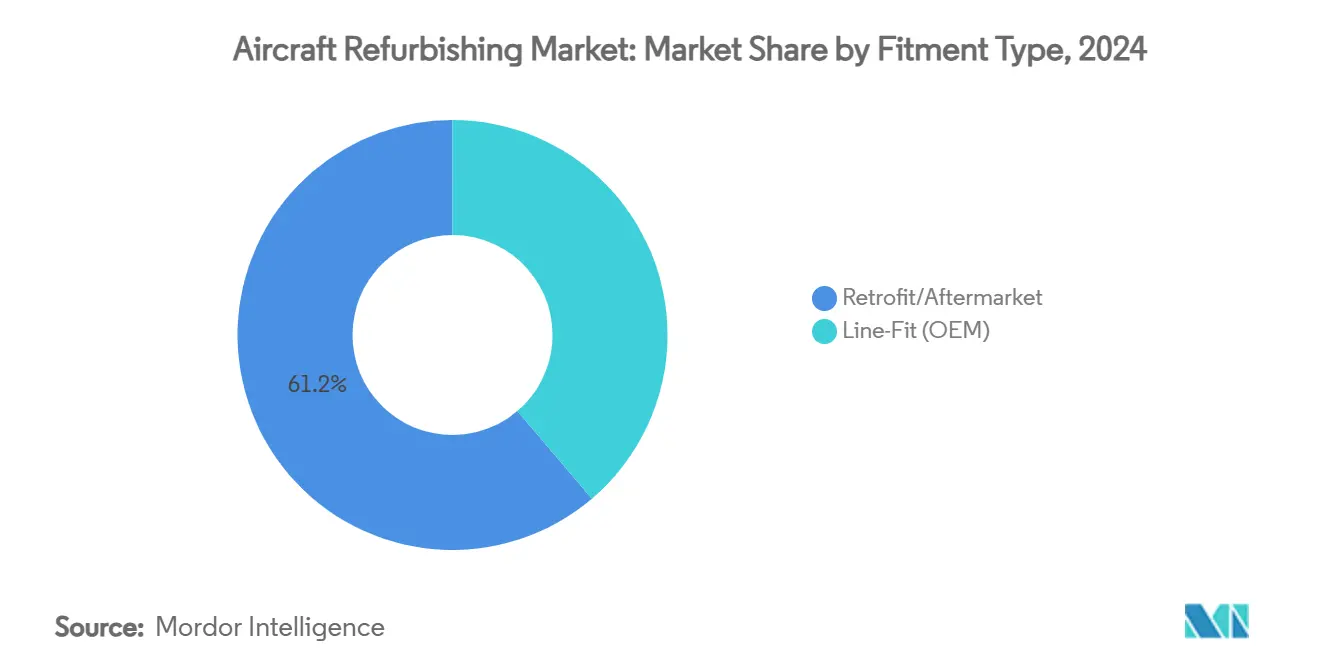

- By fitment type, retrofit projects commanded 61.23% of the aircraft refurbishing market in 2024; line-fit installations are set to grow at a 6.95% CAGR through 2030.

- By end-user, commercial airlines controlled 55.45% of the aircraft refurbishing market size in 2024, whereas military and government operators exhibited the quickest rise at 8.33% CAGR.

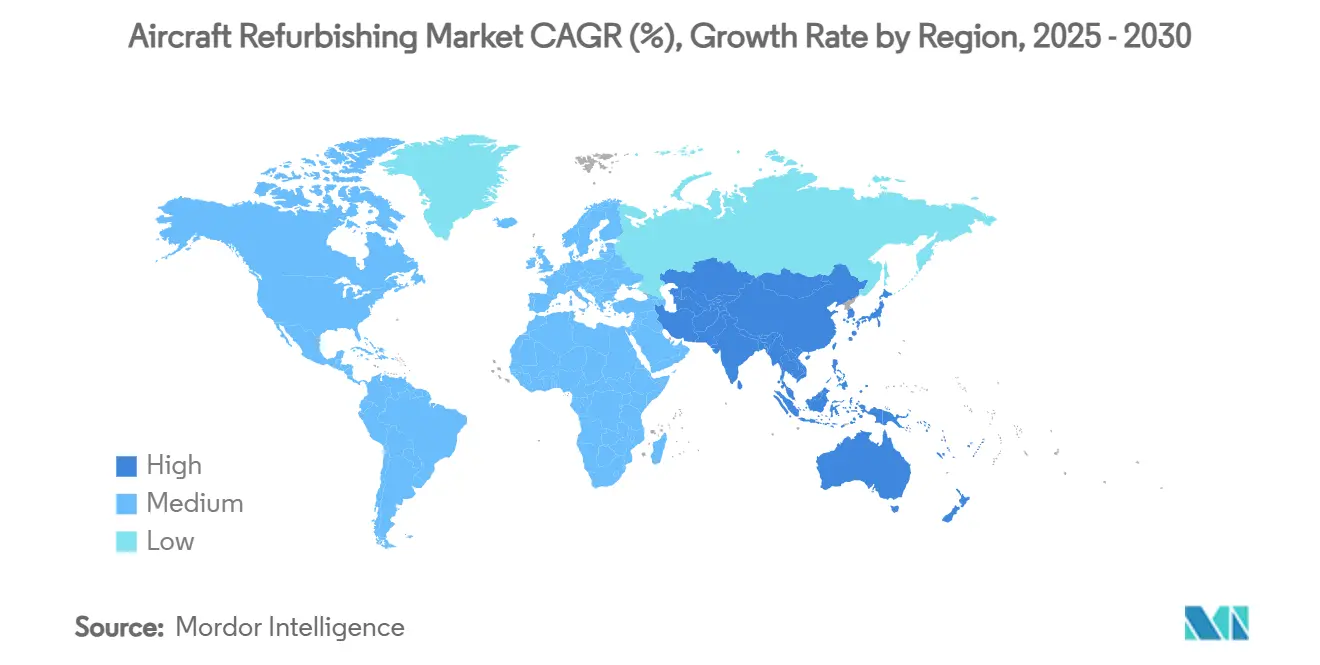

- By geography, North America captured 34.51% of the aircraft refurbishing market share in 2024; Asia-Pacific is forecasted to climb at a 5.74% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Aircraft Refurbishing Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in air-passenger traffic driving upgrade cycles | +1.8% | Global – strongest in APAC and North America | Medium term (2-4 years) |

| E-commerce-led demand for freighter conversions | +1.2% | Global – concentrated in North America and Europe | Short term (≤ 2 years) |

| Monetization push via premium-economy retrofits | +0.9% | North America, Europe and premium APAC routes | Medium term (2-4 years) |

| Sustainability mandates favouring bio-based interiors | +0.7% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Ultra-long-haul cabin re-configuration requirement | +0.5% | Global – focused on major airline hubs | Medium term (2-4 years) |

| New-generation satellite IFEC retrofit revenue streams | +0.4% | Global – led by North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Air-Passenger Traffic Driving Upgrade Cycles

International traffic has rebounded to within 95% of pre-pandemic levels on many routes, pushing airlines to differentiate cabins without grounding capacity. Swiss International Air Lines allocated CHF 1 billion (USD 1.2 billion) annually in 2024 for long-haul refurbishments, signalling how upgrade cycles have shifted from maintenance events to competitive imperatives.[1]Aviation Week Network, “Swiss Preps Long-Haul Fleet For Retrofit, Will Keep A340s Flying,” aviationweek.com Premium seat installations lift yield and Net Promoter Scores, encouraging recurring investment while balance-sheet repair is underway. The trend spans network and low-cost carriers that now view cabin ambience as a lever for ancillary revenue capture. Continuous retrofit demand supports a stable pipeline for MRO providers, sustaining the aircraft refurbishing market across economic cycles.

E-commerce-Led Demand for Freighter Conversions

Parcel-volume growth continues in double digits, preserving structural cargo capacity shortfalls. Passenger-to-freighter (P2F) programs allow operators to redeploy mid-life widebody aircraft quickly, avoiding seven-year waits for new-build freighters. Leasing companies in North America and Europe have accelerated orders for conversion slots, keeping hangars near full utilization.[2]AvBuyer, “Top MRO Trends & What They Mean for BizJet Owners,” avbuyer.com Asia-Pacific demand is especially acute as cross-border e-commerce surges and secondary airports lack wide-body belly capacity. The aircraft refurbishing market, therefore, benefits from dual-track demand in passenger and cargo interiors.

Monetization Push via Premium-Economy Retrofits

Premium economy yields an average of 40-60% above economy yet incurs modest incremental service costs. Singapore Airlines approved a SGD 1.1 billion (USD 835 million) A350 retrofit program in 2024 that introduces a new four-class cabin, illustrating the scale of revenue-focused refurbishments. The class appeals to cost-conscious corporates and affluent leisure travellers, especially on ultra-long-haul sectors. Because the refurbishment work scope is narrower than complete business-class installations, airlines can roll out premium-economy layouts fleet-wide within shorter downtimes, accelerating payback and bolstering aircraft refurbishing market momentum.

Sustainability Mandates Favouring Bio-Based Interiors

Regulators and corporate carbon targets compel measurable weight and lifecycle-emission reductions. European carriers are early adopters as they prepare for incoming environmental disclosure standards. Lufthansa Technik’s flax-based AeroFLAX panels, showcased widely during 2024 trade shows, cut component mass by about 20% while offering recyclability.[3]Runway Girl Network, “Boeing ecoDemonstrator to Test Cabin Recyclability,” runwaygirlnetwork.com Airlines can justify premium acquisition costs because lighter cabins translate to continuous fuel savings and lower emissions charges. Suppliers integrating bio-based resins into standard products capture pricing power, reinforcing sustainability as an enduring demand pillar within the aircraft refurbishing market.

Restraints Impact Analysis of Aircraft Refurbishing Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High downtime and MRO slot scarcity | −1.1% | Global – most acute in North America and Europe | Short term (≤ 2 years) |

| Skilled-labor shortage in cabin engineering | −0.8% | Global – particularly severe in North America and Europe | Medium term (2-4 years) |

| Component supply-chain delays for refurbishment materials | −0.6% | Global – affects wide-body heavy-check hubs | Short term (≤ 2 years) |

| Complex certification and regulatory approval processes | −0.4% | Global – highest impact on multi-authority retrofit projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Downtime and MRO Slot Scarcity

Airframe availability sits at a premium as post-pandemic schedules approach utilization ceilings. Major heavy-maintenance providers report full hangar occupancy into mid-2026, forcing operators to book refurbishment lines as much as 18 months ahead. Airlines weighing optional upgrades against revenue flights frequently defer non-mandatory projects, muting near-term aircraft refurbishing market uptake. Slot scarcity also encourages price escalation, which squeezes narrow-margin carriers and slows order conversion. Capacity additions are underway, yet lead times for facility expansion and tooling procurement imply the bottleneck will persist through the forecast horizon.

Skilled-Labor Shortage in Cabin Engineering

Composite lay-up, electrical integration, and regulatory-conformity tasks demand certified technicians who require multi-year apprenticeship pipelines. Retirement waves and pandemic-era attrition compounded shortages across North America and Europe. Virtual-reality (VR) training curricula launched in 2024 accelerate competency building, but time-to-proficiency spans two to three years. Providers routinely decline workscopes involving cutting-edge materials because of labor constraints, creating revenue leakage despite strong demand. Unless recruitment and up-skilling efforts scale faster, human-capital scarcity will remain a drag on aircraft refurbishing market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Aircraft Refurbishing Market Segment Analysis

By Refurbishment Type:

Interior Dominance Drives Market EvolutionInterior projects captured 48.92% of the aircraft refurbishing market share in 2024 as carriers prioritised revenue-generating cabin refreshes. The segment benefits from shorter downtime and immediate ROI through seat-count optimization, premium-seat installation, and ancillary-service enablement. Airlines also channel sustainability commitments into cabin elements by substituting traditional plastics with bio-based composites, trimming weight, and reducing lifecycle emissions. Premium-economy roll-outs spearheaded demand, supported by improved LED mood-lighting and power-delivery upgrades that enhance passenger comfort. Though smaller in current value, exterior refurbishments form the fastest-growing niche at 7.23% CAGR through 2030. Growth stems from nano-scale structural colour coatings that slash paint weight to under 10% of conventional levels, cutting 272 kg to 544 kg per aircraft and improving fuel burn. Automated spray robotics further shortens turnaround and addresses prior adhesion issues spotlighted in 2024 A350 paint disputes. Overall, the refurbishment-type mix illustrates a strategic tilt toward passenger-facing upgrades while still capitalising on exterior efficiency gains—both pillars reinforcing long-term aircraft refurbishing market growth.

The outlook shows interior workstreams maintaining volume leadership because fleet age profiles keep replenishing backlogs; however, exterior services will outpace in percentage growth as operators race to monetise fuel savings amid mounting carbon levies. Suppliers able to bundle cabin and livery packages under unified certification achieve schedule efficiencies valued by airlines juggling limited downtime windows. The combination of passenger-experience pressure, sustainability economics, and tighter emissions policy sustains robust double-digit demand for next-generation coatings, ensuring balanced contribution to the aircraft refurbishing market size through 2030.

By Component:

Seats Anchor Revenue While IFEC Captures GrowthSeats and upholstery commanded 38.65% of 2024 component revenue because they directly influence fare-class segmentation, load-factor optimization, and ancillary sales. Airlines executing fleet-wide premium-economy introductions install wider seats with integrated power and personal-device pairing, validating capital outlay by lifting yield per available seat mile. Lightweight seat frames further improve range and comply with emerging emissions narratives. IFEC systems, despite a smaller base, represent the component growth engine with a 6.21% CAGR to 2030. United Airlines’ 2025 commitment to retrofit 300 regional jets with Starlink underscores the scale of backlog creation. New antenna designs shave over 200 lb off legacy hardware, allowing simultaneous fuel savings and revenue-share agreements based on paid connectivity. Cabin lighting, PSU panels, and sidewalls migrate to high-efficacy LEDs and thermoplastics, consolidating incremental demand under broad sustainability and passenger-comfort themes. Consequently, the aircraft refurbishing market size for seating maintains numeric dominance, while IFEC accelerates valuation uplift, producing a complementary demand landscape.

Synergy emerges as seat suppliers integrate power-delivery and connectivity hubs, blurring boundaries between furniture and avionics. Modular architecture simplifies swap-out during heavy checks, encouraging airlines to align maintenance windows with revenue-accretive technology refreshes. Providers that bundle seats, IFEC, and cabin management into turnkey kits reduce certification friction and capture higher wallet share, reinforcing consolidation trends across the aircraft refurbishing market.

By Aircraft Type:

Narrowbody Leadership Meets Regional-Jet OpportunityNarrowbody aircraft retained 44.22% share of 2024 activity as high-cycle utilization accelerates interior wear and triggers more frequent make-overs. Standardised engineering documentation and part commonality lower per-project costs, supporting steady throughput across global MRO hubs. Regional jets, in contrast, represent the fastest growth at an 8.38% CAGR because operators reposition these assets for point-to-point connectivity and charter services. Multiple carriers ordered cabin-conversion kits in 2024 that transform 70-seat layouts into 30-seat premium or sky-freighter configurations, boosting residual values and extending fleet life cycles. Widebody refurbishments command higher ticket values but see fewer annual events due to longer check intervals and larger downtime blocks.

Demand dynamics underlying aircraft-type segmentation illuminate differing investment triggers: narrowbody programs chase competitive densification, while regional jet projects often support business-class shuttle or cargo roles. As ultra-long-haul route networks scale, wide-body re-configurations targeting premium suites and social zones add another high-margin tranche of work. Because each aircraft family now follows unique upgrade cadences, diversified capability remains essential for suppliers aiming to maximise exposure across the aircraft refurbishing market.

By Fitment Type:

Retrofit Dominance Signals Market MaturityRetrofit and aftermarket modifications accounted for 61.23% of the aircraft refurbishing market size in 2024, reflecting operators’ preference for value extraction from existing assets amid OEM production bottlenecks. Airlines gravitate to pre-certified retrofit kits that minimise downtimes and ensure cabin branding consistency across mixed-age fleets. Line-fit activity, although smaller, posts the highest growth at 6.95% CAGR as OEMs license independent centres to widen delivery capacity. Boeing’s 2024 agreement designating Lufthansa Technik a licensed B787 cabin modification centre exemplifies OEM-endorsed collaboration that merges factory engineering with third-party agility.

Hybrid delivery models reduce certification duplication and lower non-recurring engineering (NRE) fees, making line-fit-like quality attainable during scheduled heavy checks. The retro-versus-line-fit balance, therefore, reflects a continuum rather than a dichotomy, with modularity and digital twins enabling seamless migration. Retrofit’s headline weight in the aircraft refurbishing market will endure because the in-service fleet far outnumbers yearly production; nevertheless, line-fit’s faster-than-average growth rate underscores OEMs’ recognition of refurbishment revenue and positions the segment for long-term convergence.

By End-User:

Commercial Airlines Lead While Military AcceleratesCommercial airlines dominated 2024 with a 55.45% share as seat-yield optimization and brand repositioning drove large-scale cabin investments. Air India's USD 400 million program to transform legacy wide-body interiors, initiated in April 2025, typifies the airline's commitment to passenger-experience uplift. Leasing companies bolster airline demand by mandating standard cabin specifications that speed transitions between lessees and protect asset values. Military and government operators represent the fastest expansion at 8.33% CAGR because defence ministries prioritise mission-system upgrades and life-extension packages. Lockheed Martin's June 2025 C-5M contract demonstrates sustained spend on avionics, structural-life improvements, and interior re-role capability. Private charter and fractional fleets also seek bespoke interiors that mirror residential aesthetics, though volumes remain niche. Collectively, the diverse end-user mix underpins demand resilience across economic cycles, reinforcing a broad customer base for the aircraft refurbishing market.

The segment profile is expected to tilt slightly toward government accounts as geopolitical tensions spur transport-fleet modernization and multi-role flexibility. Commercial airline share will remain substantial because competitive differentiation through cabin experience is now embedded in the network carrier strategy. Service providers invest in multi-authority approvals to accommodate varying regulatory regimes, widen addressable segments, and stabilise the aircraft refurbishing market across business lines.

Geography Analysis

North America Aircraft Refurbishing Market

North America captured 34.51% of 2024 revenue, buoyed by a deep maintenance, repair, and overhaul (MRO) ecosystem, proximity to major OEMs, and high fleet utilization levels. AAR Corp reported record FY 2024 sales of USD 2.3 billion, up 16% yearly, reflecting expanded component repair and airframe-maintenance throughput. Regulatory processes are mature, allowing rapid certification of complex cabin modifications, while abundant investment capital supports facility upgrades. However, slot constraints and technician shortages are most acute in this region, tempering near-term capacity expansions and nudging some operators toward Latin-American or Asia-Pacific alternatives for heavy checks.

APAC Aircraft Refurbishing Market

Asia-Pacific is the fastest-growing geography at a 5.74% CAGR through 2030, propelled by accelerating fleet deliveries and improving domestic MRO capabilities. Singapore Airlines’ SGD 1.1 billion (USD 835 million) A350 retrofits and India’s projected 50% MRO expansion by 2026 highlight the region’s upward trajectory. HAECO’s 2025 “Asia MRO of the Year – Engine” award exemplifies emerging technical prowess and underlines Hong Kong and mainland China’s significance as modification hubs. Competitive labour costs and favourable time-zone positioning enable carriers to short-circuit North American slot shortages, further accelerating regional market share.

Europe Aircraft Refurbishing Market

Europe maintains a strong presence through technology leadership and sustainability regulation. Lufthansa Technik posted EUR 7.441 billion (USD 8.69 billion) revenue in 2024 and announced more than EUR 1 billion (USD 1.17 billion)in cumulative investments to 2030, underscoring its commitment to advanced materials and data-driven maintenance. Environmental standards in the European Union catalyse early adoption of bio-based composites, positioning the region at the forefront of green-cabin R&D. Brexit-related customs complexity and energy-cost inflation impose headwinds. Still, entrenched engineering expertise and premium airline customer bases preserve high-value refurbishment pipelines. Collectively, geographic interplay sustains balanced development of the aircraft refurbishing market and cushions region-specific risk exposures.

Competitive Landscape

The aircraft refurbishing market is moderately concentrated. Market leaders such as Lufthansa Technik, Collins Aerospace, and HAECO leverage global hangar networks, design engineering, and multi-authority certifications to win fleet-wide contracts. Lufthansa Technik’s 2024 revenue of EUR 7.44 billion (USD 8.69 billion) funds continuous R&D, including the scale-up of bio-composite AeroFLAX panels embraced by European flag carriers. Collins Aerospace maintains momentum through flight-deck and cabin-system integration; its Flight2 upgrade solution modernises legacy C-130 avionics under multi-year defence contracts.[4]Collins Aerospace, “Flight2 Integrated Avionics System,” collinsaerospace.com HAECO expands mainland-China joint ventures with COMAC, securing domestic airliner support while retaining international airline clientele.

Strategic alliances between OEMs and independent MROs are rising as airframers address backlog-induced capacity gaps. Boeing’s 2024 licence award to Lufthansa Technik for 787 cabin work exemplifies cross-pollination designed to speed modification throughput while preserving OEM design authority. Digital-thread initiatives—from 3-D scanning to VR-enabled remote inspections—enhance quoting accuracy and streamline approvals, differentiating technologically advanced providers. New entrants remain limited because of high capital requirements for composite shops, flammability-test labs, and certification staff. Nevertheless, white-space potential exists in growth regions where labour pools develop quickly and regulatory agencies extend bilateral recognition, offering measured opportunity for specialised niches within the aircraft refurbishing market.

Pricing power will remain with top-tier providers through 2030, given certification barriers and ongoing labour tightness. However, competitive intensity will likely rise in Asia-Pacific as domestic champions mature. Suppliers integrating sustainability, digital tooling, and rapid-retrofit kit portfolios are best positioned to convert backlog pipelines into profitable share gains.

Aircraft Refurbishing Industry Leaders

Collins Aerospace (RTX Corporation)

Hong Kong Aircraft Engineering Company Limited (HAECO)

AAR International, Inc.

Singapore Technologies Engineering Ltd.

Lufthansa Technik AG

- *Disclaimer: Major Players sorted in no particular order

Aircraft Refurbishing Market Companies Covered in this Report

- Lufthansa Technik AG

- Collins Aerospace (RTX Corporation)

- Hong Kong Aircraft Engineering Company Limited (HAECO)

- Singapore Technologies Engineering Ltd.

- AAR International, Inc.

- SR Technics Switzerland Ltd.

- Jet Aviation AG

- GKN plc

- Diehl Stiftung & Co. KG

- Safran SA

- FACC AG

- RECARO Holding GmbH

- Thompson Aero Seating (AVIC)

- Gogo Inc.

- Panasonic Group

- Thales Group

- SIA Engineering Company Limited

Recent Industry Developments in Aircraft Refurbishing Market

- July 2025: LATAM Airlines selected Viasat Amara for widebody long-haul connectivity, investing USD 60 million to retrofit more than 60 aircraft beginning in 2026.

- July 2025: Cessna unveiled new executive interior schemes for Grand Caravan EX as part of the model’s 40th anniversary program.

- July 2024: HAECO extended the B747-400ERF base-maintenance support agreement with Cargolux through 2028.

- July 2024: De Havilland Canada introduced a Dash 8-400 OEM-certified refurbishment program to boost turboprop performance.

Global Aircraft Refurbishing Market Report Scope

Segmentation Overview

| Interior |

| Exterior |

| Avionics |

| Seats and Upholstery |

| IFEC Systems |

| Galleys and Lavatories |

| Lighting and PSU Panels |

| Sidewalls, Overhead Bins and Panels |

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Business Jets |

| Piston and Turboprop Aircraft |

| Rotorcraft |

| Retrofit/Aftermarket |

| Line-Fit (OEM) |

| Commercial Airlines |

| Private/Charter Operators |

| Leasing Companies |

| Military and Government Operators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Refurbishment Type | Interior | ||

| Exterior | |||

| Avionics | |||

| By Component | Seats and Upholstery | ||

| IFEC Systems | |||

| Galleys and Lavatories | |||

| Lighting and PSU Panels | |||

| Sidewalls, Overhead Bins and Panels | |||

| By Aircraft Type | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional Jets | |||

| Business Jets | |||

| Piston and Turboprop Aircraft | |||

| Rotorcraft | |||

| By Fitment Type | Retrofit/Aftermarket | ||

| Line-Fit (OEM) | |||

| By End-User | Commercial Airlines | ||

| Private/Charter Operators | |||

| Leasing Companies | |||

| Military and Government Operators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft refurbishing market in 2025?

The market stands at USD 5.19 billion in 2025 and is forecasted to reach USD 6.79 billion by 2030, reflecting a 5.52% CAGR.

Which refurbishment type commands the largest share?

Interior projects hold the lead with 48.92% of 2024 revenue because airlines prioritise passenger-experience upgrades.

Why is Asia-Pacific the fastest-growing region?

Rapid fleet expansion, emerging MRO capacity in Singapore, China and India, and supportive government policy drive a 5.74% CAGR through 2030.

What is the biggest restraint on market growth?

Limited MRO slots and lengthy downtimes cap near-term capacity, trimming the overall growth rate by about 1.1 percentage points.

Which component segment is expanding fastest?

IFEC retrofits lead growth at a projected 6.21% CAGR as airlines roll out high-speed satellite connectivity across fleets.

How concentrated is the competitive landscape?

The top five players capture roughly 55% of global revenue, indicating moderate concentration and a score of 6 on a 1–10 scale.

Page last updated on: