Aircraft Cooling Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

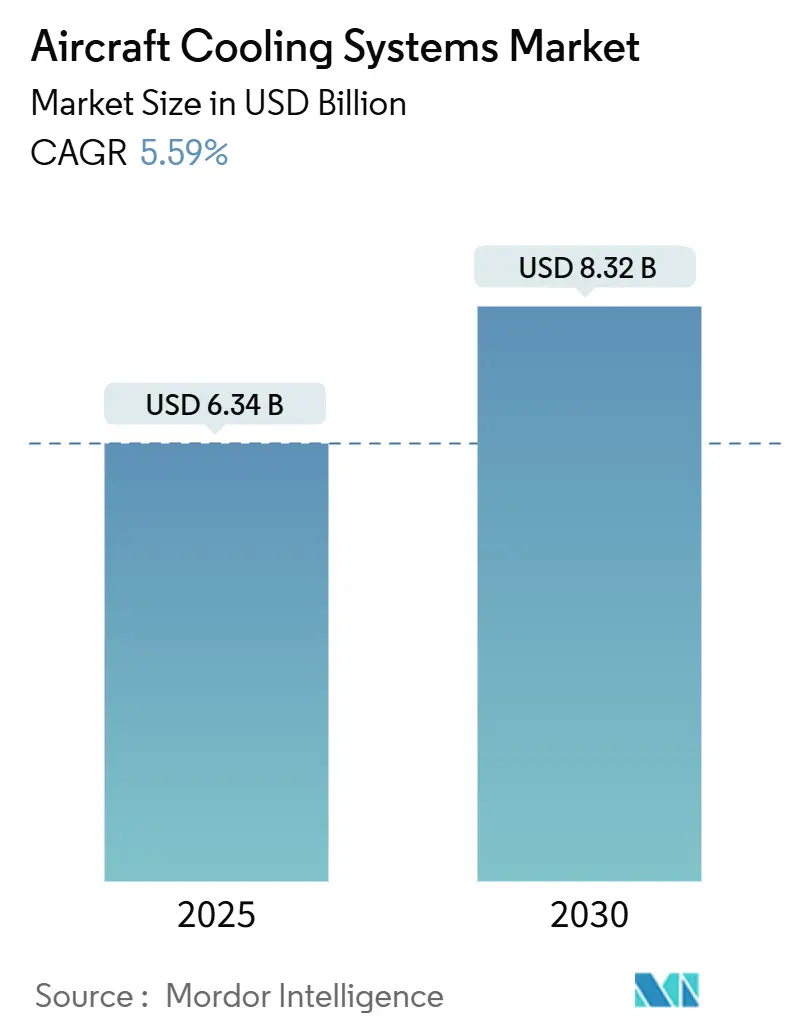

| Market Size (2025) | USD 6.34 Billion |

| Market Size (2030) | USD 8.32 Billion |

| Growth Rate (2025 - 2030) | 5.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Cooling Systems Market Analysis by Mordor Intelligence

The aircraft cooling systems market size stood at USD 6.34 billion in 2025 and is forecasted to climb to USD 8.32 billion by 2030, translating into a 5.59% CAGR. Escalating thermal loads created by more-electric architecture (MEA), higher avionics power densities, and in-flight connectivity upgrades are compelling airframers and system integrators to migrate from legacy pneumatic loops toward hybrid or liquid solutions that dissipate heat 3-4 times more efficiently. Adoption is reinforced by commercial jet production ramp-ups, the surge in business-jet retrofits, and proliferating UAV programs requiring compact, high-reliability cooling hardware. Suppliers that combine certification experience, additive manufacturing, and intelligent control software are gaining a competitive edge as airlines and defense operators demand lighter components, predictive maintenance, and shorter lead times. North American primes currently dominate the value chain. Yet, rapid fleet growth in China and India is shifting investment toward Asia-Pacific engineering centers, while Europe uses stringent environmental rules to push efficiency-focused innovations.

Key Report Takeaways

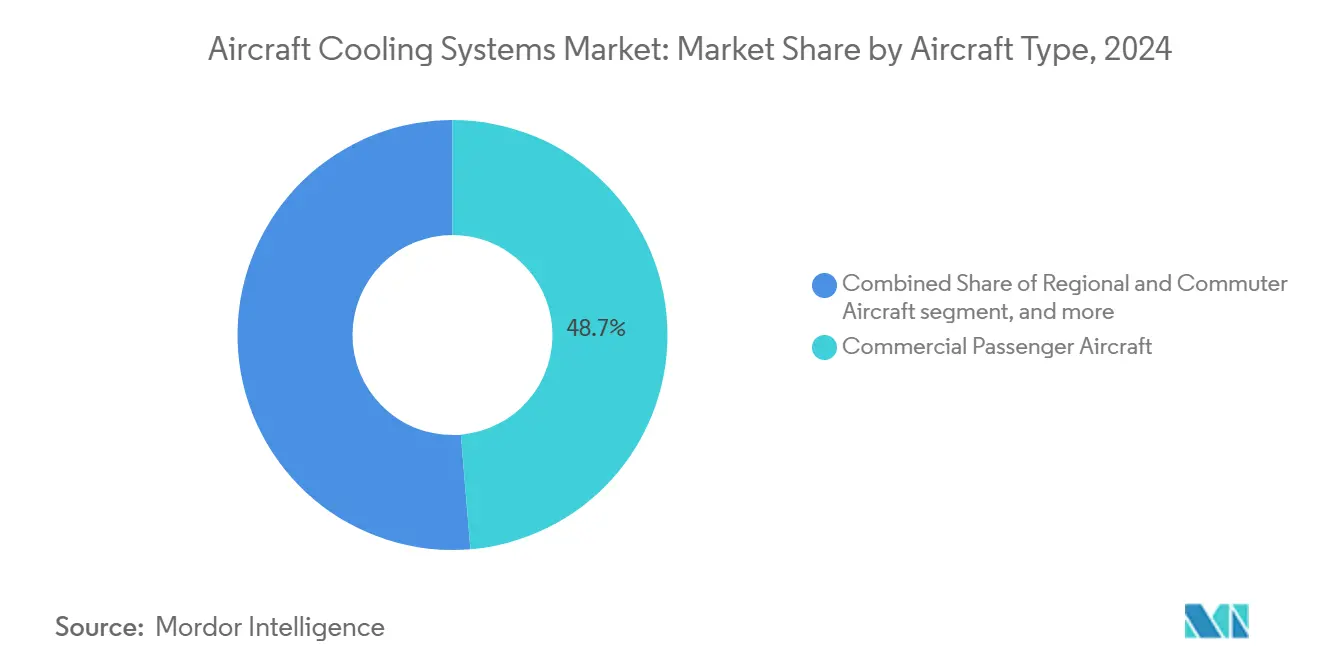

- By aircraft type, commercial passenger aircraft led with 48.67% revenue share in 2024; business jets are projected to expand at an 8.91% CAGR through 2030.

- By cooling technology, air-cycle systems held 56.23% of the aircraft cooling systems market share in 2024, while liquid cooling is advancing at a 7.48% CAGR to 2030.

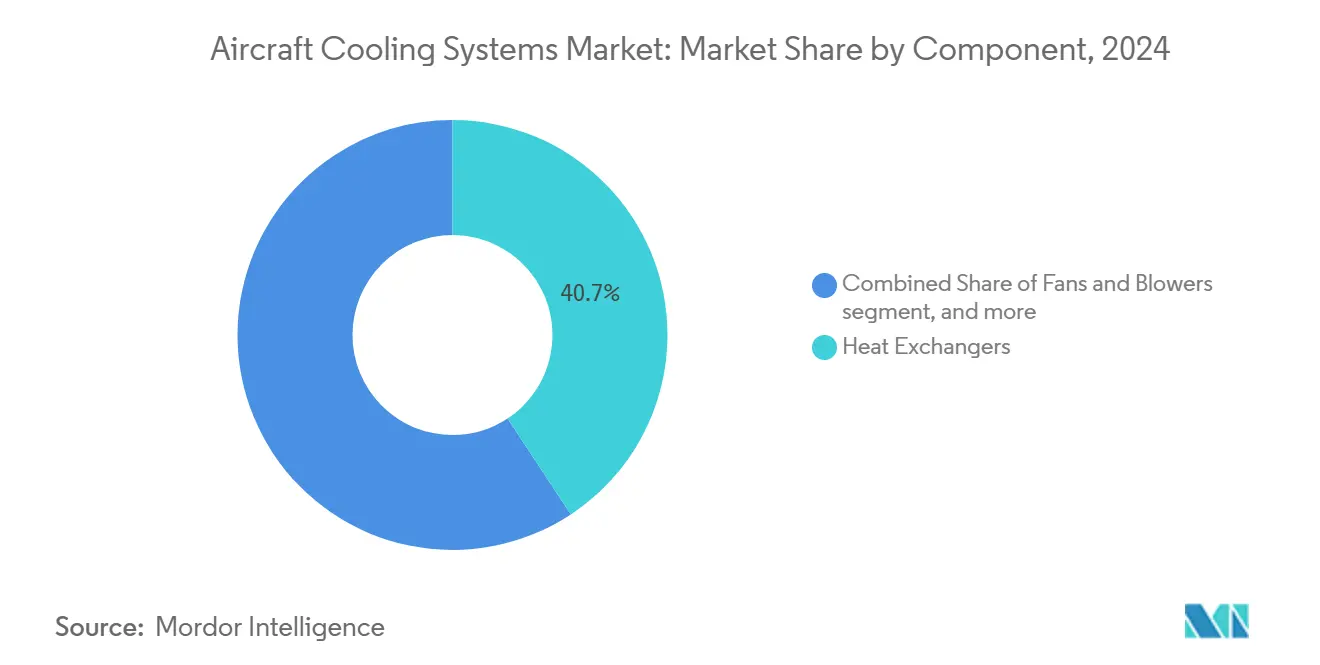

- By component, heat exchangers held a 40.72% share of the aircraft cooling systems market in 2024, and sensors and controllers posted the fastest 6.35% CAGR through 2030.

- By end-use, OEM installations represented 63.17% share of the aircraft cooling systems market size in 2024, and the aftermarket segment is rising at a 5.71% CAGR to 2030.

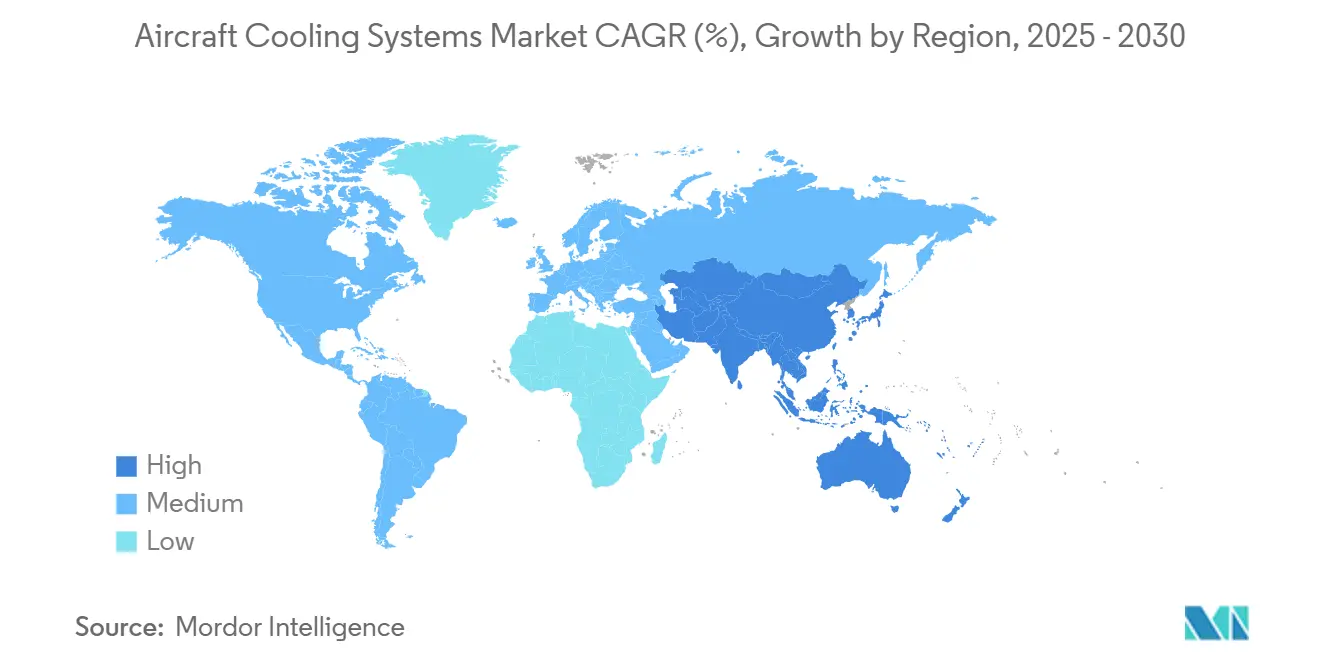

- By geography, North America commanded a 43.29% share of the aircraft cooling systems market in 2024, while Asia-Pacific is forecasted to grow at a 6.39% CAGR through 2030.

Global Aircraft Cooling Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising deliveries of commercial aircraft, esp. narrowbodies | +1.20% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid electrification (MEA/hybrid-electric) raises thermal loads | +1.80% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Surging military and civil UAV fleet needs compact cooling | +0.90% | North America, Europe, Asia-Pacific defense sectors | Medium term (2-4 years) |

| Stringent cabin comfort and environmental regulations | +0.70% | Global, led by EASA and FAA jurisdictions | Long term (≥ 4 years) |

| Additive manufactured micro-channel heat exchangers slash weight and lead-time | +0.60% | North America and Europe advanced manufacturing hubs | Short term (≤ 2 years) |

| Mandated switch to non-flammable hydraulic fluids enlarges heat-exchanger area | +0.40% | Global regulatory compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising deliveries of commercial aircraft enhance thermal system demand

Narrowbody programs such as the A320neo and B737 MAX drive continuous orders. Airbus delivered 735 and Boeing 528 units in 2024; more than 80% were single-aisle models relying on highly integrated environmental-control packs.[1]Honeywell Aerospace Communications Team, “Air Management Systems,” Aerospace.Honeywell.com Higher production volumes translate into predictable line-fit opportunities for heat exchangers, air-cycle machines, and liquid pumps. Airlines’ focus on fuel burn reductions pushes OEMs to specify lighter, more efficient thermal components that reduce bleed-air extraction and optimize cabin pressure ratios. Because aircraft cooling systems must be installed approximately 18-24 months after the initial order, booked backlogs give suppliers clear visibility into revenue streams. Therefore, the aircraft cooling systems market benefits from synchronized build-rate increases planned through 2028, especially at China, France, and the US final assembly lines.

Electrification paradigm reshapes thermal architecture requirements

Transitioning from bleed-air to electric environmental-control architectures elevates heat generation by three to four, forcing designers to incorporate liquid loops, phase-change materials, and vapor-compression subsystems. Demonstration programs on eVTOL prototypes and regional hybrid-electric aircraft illustrate how power electronics, battery packs, and high-resolution displays create localized hotspots that legacy air-cycle systems cannot manage. Honeywell’s liquid-cooled upgrades for the F-35 confirm that even fighter platforms now integrate dedicated loops to stabilize avionics temperatures during high-load missions. Certification timelines remain long, yet early adopters in urban-air-mobility accelerate learning curves, shortening development cycles for commercial transports expected in the next decade. Consequently, electrification exerts the strongest positive pull on the aircraft cooling systems market over the forecast horizon.

UAV proliferation demands miniaturized high-performance cooling

Defense ministries and parcel-delivery operators are fielding larger numbers of long-endurance drones and cargo UAVs, each requiring ultra-compact systems capable of dissipating more than 10 kW/kg within restricted fuselage volumes. Suppliers respond with micro-channel heat exchangers produced via additive manufacturing that cut weight by 30% and shrink lead times from months to weeks. Thermal signature management adds complexity because cooling airflow must not compromise radar or infrared stealth profiles. Rapid block upgrades in UAV programs compress qualification schedules, rewarding modular subsystems that can be reconfigured for new payloads without recertification. Though smaller in absolute dollars, this demand segment lifts the overall aircraft cooling systems market by adding high-margin specialty hardware orders.

Regulatory mandates elevate cabin environmental standards

EASA and the FAA have tightened requirements on temperature uniformity, air quality, and humidity in passenger cabins, cargo holds, and crew compartments. Revised DO-160 environmental tests stipulate narrower permissible temperature bands for avionics bays and lithium battery enclosures.[2]EASA Directorate, “Halon replacement in the aviation industry guide 2025,” Easa.europa.eu Compliance pushes OEMs toward variable-speed compressors, advanced filtration media, and smarter sensors that constantly adjust mass-flow rates. Regulatory scrutiny extends to cargo aircraft carrying pharmaceuticals and live animals, increasing demand for precision-controlled airflow. System designers embed additional redundancy to meet fail-operational expectations, expanding bill-of-materials content per aircraft and raising average system-selling prices in the aircraft cooling systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High certification and reliability costs | -1.10% | Global, particularly stringent in North America and Europe | Long term (≥ 4 years) |

| Volatile defense procurement cycles | -0.80% | North America, Europe, Asia-Pacific defense markets | Medium term (2-4 years) |

| Weight-penalties discourage liquid loops in small aircraft | -0.50% | Global general aviation and regional aircraft segments | Medium term (2-4 years) |

| Tight supply of nickel super-alloy and micro-channel plate stock | -0.70% | Global supply chain, concentrated in specialized metallurgy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High certification and reliability costs constrain technology adoption

Thermal-management upgrades must undergo 18-36 months of qualification tests costing USD 5–15 million per program. Updated AMC-20 guidance obliges applicants to demonstrate fault tolerance for systems that protect flight-critical avionics, lengthening paperwork and ground-test campaigns. Despite promising considerable weight savings, additive-manufactured heat exchangers face extra scrutiny over micro-structure integrity and long-term fatigue. Smaller suppliers often lack the capital to finance multiple concurrent QARs, slowing their entry and consolidating bargaining power with incumbents. The cash burden particularly discourages deployment of liquid loops on regional and general-aviation aircraft, where certification cost relative to aircraft price is high, tempering adoption in those niches of the aircraft cooling systems market.

Volatile defense procurement cycles disrupt planning

Defense budgets oscillate with geopolitical tensions and national election calendars, causing sudden order deferrals or accelerations for fighter, tanker, and UAV programs. Honeywell’s experience on the F-35 showed that cooling upgrades needed to align with block-buy approvals; slippage cascaded across subcontractors and delayed revenue recognition. Suppliers struggle to balance engineering-capacity commitments when multiyear contracts are re-phased. Inventory overhang during downturns leads to margin erosion, while surprise contract wins can strain machining and specialized alloy supply chains. This volatility injects uncertainty into the aircraft cooling systems market outlook, especially for vendors heavily exposed to a single flagship defense platform.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Business jets spearhead advanced thermal adoption

Business jets exhibit the sharpest 8.91% CAGR as owners retrofit cabins with OLED-based entertainment suites and high-bandwidth connectivity that intensify heat generation. Because these aircraft often pioneer avionics now migrating to commercial fleets, vendors secure early feedback loops that refine liquid pumps, micro-processors, and predictive-control algorithms. Commercial passenger models remain the volume anchor, commanding 48.67% of the 2024 aircraft cooling systems market revenue. Their standardized line-fit requirements give tier-one suppliers economies of scale and decades-long maintenance contracts. Regional jets and turboprops, hampered by slimmer margins, adopt innovations later but still require compliance-driven upgrades. Military fixed-wing and rotorcraft platforms grow steadily on the back of avionics modernization and mission-system cooling, yet budget cycles temper their ordering cadence. UAVs, though representing a smaller slice of the aircraft cooling systems market size, post double-digit expansion as civil applications—pipeline inspection, logistics, and urban air mobility (UAM) multiply.

Rising electrification blurs the lines among categories. Large cabin business jets already integrate liquid loops similar to narrow-bodies, while upcoming hybrid-electric commuter designs converge with sophisticated UAV thermal solutions. Suppliers capable of cross-leveraging designs across multiple aircraft types optimize R&D spend and accelerate certification. Consequently, business-jet learnings increasingly shape commercial transport specifications, reinforcing their strategic importance within the aircraft cooling systems market.

By Cooling Technology: Liquid loops outpace legacy pneumatic systems

Air-cycle machines retained a 56.23% share in 2024 due to proven reliability, a broad certification pedigree, and existing tooling across Airbus, Boeing, and Embraer production lines. Nevertheless, liquid subsystems deliver a 7.48% CAGR as power-electronics cooling, battery thermal conditioning, and directed-energy systems on military aircraft require heat-flux densities unreachable by compressed-air packs. Vapor-cycle units occupy a middle ground, offering higher coefficients of performance than air cycles with less weight and certification burden than liquid circuits. Thermoelectric modules and hybrid architectures remain niche today but serve as testbeds for future solid-state cooling in hydrogen or fuel-cell aircraft.

Transition costs are non-trivial. Liquid loops introduce pumps, reservoirs, and leak-detection sensors that weigh against their superior performance. In small rotocraft, designers still favor air-cycle simplicity to avoid mass penalties and a restraint on segment uptake. Yet FAA-approved demonstrations showing 25% energy savings and 15 °C lower component temperatures ease operator hesitancy. As certification data matures, liquid loops are expected to seize incremental wins, especially in eVTOL fleets where battery thermal envelopes are critical. Suppliers with proprietary additively-manufactured micro-channels and corrosion-resistant alloys sit at the forefront of this shift, reinforcing growth momentum for the aircraft cooling systems market.

By Component: Sensors enable predictive thermal management

Heat exchangers accounted for 40.72% of component revenue in 2024, underscoring their ubiquitous role across all architectures. Yet rising digitalization propels sensors and electronic controllers to the fastest 6.35% CAGR. Operators now demand real-time temperature mapping, self-diagnostics, and cloud-based prognostics that slash unscheduled maintenance events. Air-cycle compressors, blowers, and expansion turbines represent a mature install base but continue to see incremental efficiency tweaks. Pumps, valves, and manifolds expand alongside liquid-loop proliferation, while fans gain subtle improvements from advanced composite shrouds that boost pressure ratios without weight penalties.

Predictive maintenance is moving from optional to mandatory in high-utilization fleets. Honeywell’s acquisition of CAES brought radiation-hardened processors that power onboard analytics capable of anticipating heat exchanger fouling before system performance degrades.[3]Ahjay Rai, “Honeywell and NXP expand partnership to accelerate next-generation aviation technology,” Honeywell.com Integrated control modules now dynamically orchestrate mass flow, pump speed, and pressure ratios, delivering up to 3% fuel-burn savings over static schedules. Though small in dollar terms, such electronics content differentiates suppliers and lifts recurring software-license revenues within the aircraft cooling systems market.

By End-Use: Aftermarket upgrades capitalize on fleet modernization

OEM linefit sales drove 63.17% of 2024 revenue as single-aisle assembly lines scaled to satisfy record order backlogs. Line-fit dominance guarantees volume contracts and positions suppliers for multi-decade spares demand. Nonetheless, the aftermarket grows 5.71% annually as airlines retrofit Wi-Fi, cabin LEDs, and next-gen flight decks that all raise thermal loads beyond the capability of earlier-generation packs. Airlines treat cooling system enhancements as low-hanging fruit to unlock additional dispatch reliability and cabin-comfort scores.

Fleet life extensions also spur upgrades. Narrowbodies approaching 15-year service intervals require overhaul of heat exchangers suffering core fouling and corrosion. Drop-in replacement kits that improve heat rejection by 20% without structural changes attract operators seeking minimal downtime. As e-enablement spreads, supplemental-type certificates covering smart controllers and liquid-cooling add-ons broaden the addressable aftermarket scope. This dual-revenue architecture—linefit plus retrofit—creates a resilient earnings profile for top aircraft cooling systems market suppliers.

Geography Analysis

North America’s 43.29% revenue share flows from consolidated OEM production, extensive MRO networks, and the world’s largest defense budget. Boeing’s Everett and Charleston lines integrate heat exchangers, valves, and air-cycle machines supplied predominantly by local primes, while F-35 block upgrades secure multiyear funding that stabilizes defense volumes. The region also leads in additive-manufacturing capacity and electrified-propulsion testbeds, accelerating qualification of micro-channel components. US regulatory agencies collaborate with industry to pilot digital certification tools, potentially trimming development cycles for new cooling architectures.

Asia-Pacific delivers the fastest 6.39% CAGR through 2030 as China and India boost indigenous aircraft programs. COMAC’s C919 and CRAIC CR929 require localized supply chains, prompting joint ventures between Western component specialists and regional tier-twos. Rising middle-class travel drives fleet expansion, compelling carriers to prioritize dispatch reliability and cabin-comfort upgrades. Defense modernization across Australia, South Korea, and Japan adds new fighter and UAV procurements, each demanding advanced thermal control. Consequently, Asia-Pacific’s aircraft cooling systems market share is widening as local expertise and production scale mature.

Europe leverages Airbus assembly hubs in France, Germany, and Spain, together with stringent EASA mandates that push the adoption of energy-efficient cooling solutions. Suppliers such as Liebherr-Aerospace partner with OEMs early in aircraft programs to embed hybrid vapor-cycle packs meeting low-global-warming-potential refrigerant targets. Environmental sustainability drives R&D into lightweight alloys and closed-loop recycling for heat-exchanger cores. Meanwhile, the Middle East and Africa pursue fleet expansion in harsh climates, necessitating high-capacity air-cycle machines capable of ambient temperatures above 50 °C. South America remains an aftermarket opportunity, anchored by Embraer’s installed base and regional defense programs.

Collectively, geographic diversification cushions suppliers against localized downturns and spreads certification investment across multiple regulators, sustaining long-term momentum in the aircraft cooling systems market.

Competitive Landscape

Aircraft cooling remains moderately consolidated, with Honeywell International Inc., Collins Aerospace (RTX Corporation), and Liebherr Group collectively controlling a majority of OEM linefit awards. Decades of certification data and entrenched design-in positions create high switching costs for airframers. These incumbents extend competitive advantages through global support centers offering AOG parts within 24 hours, aligning with airlines’ tight operational windows. Yet market entry barriers are eroding as additive manufacturing democratizes complex-geometry heat-exchanger production. Start-ups employ lattice infills and generative design to achieve weight reductions unattainable with traditional brazing.

Technology differentiation is shifting toward intelligent system-of-systems offerings. Honeywell’s partnership with NXP integrates AI-based anomaly detection, enabling controllers to predict coolant-pump wear and trigger maintenance during scheduled layovers. Rheinmetall collaboration adds battery-augmented power and cooling packages for tactical vehicles, signaling convergence between aerospace and defense ground platforms.[4]Juliet Collins-Achong, “Rheinmetall and Honeywell sign memorandum of understanding to develop new technology,” Aerospace.Honeywell.com Collins continues investing in electromechanical actuation paired with variable-frequency vapor-cycle packs that modulate capacity to match dynamic mission profiles.

White-space opportunities appear in eVTOL, hydrogen propulsion, and lunar-lander thermal management. Certification pathways remain uncertain, but forward-leaning suppliers build prototypes to lock in early design wins. Those capable of bundling hardware, software, and data analytics command premium pricing and long-tail digital-service revenues, reinforcing scale advantages in the aircraft cooling systems market.

Aircraft Cooling Systems Industry Leaders

Honeywell International Inc.

Collins Aerospace (RTX Corporation)

Liebherr Group

Safran SA

Mitsubishi Heavy Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Conflux Technology partnered with a Honeywell-led consortium to develop thermal management systems for next-generation hybrid-electric aircraft.

- March 2025: Conflux partnered with AMSL Aero to develop hydrogen fuel cell cooling systems for long-range, zero-emission electric Vertical Take Off and Landing (VTOL) aircraft.

- March 2024: Honeywell unveiled an upgraded F-35 thermal fix addressing overheating concerns flagged by the Pentagon.

- June 2023: Safran Aero Boosters introduced HIPEX, a new range of heat exchangers at the Paris Air Show. The heat exchangers feature an aerodynamic design with curved or adjustable shapes, reducing aerodynamic drag by 50% compared to existing models while maintaining equivalent thermal performance.

Global Aircraft Cooling Systems Market Report Scope

| Commercial Passenger Aircraft |

| Regional and Commuter Aircraft |

| Business Jets |

| Military Fixed-Wing and Rotorcraft |

| Unmanned Aerial Vehicles (UAVs) |

| Air Cycle Systems |

| Vapor Cycle Systems |

| Liquid Cooling Systems |

| Hybrid and Solid-state/Thermoelectric |

| Heat Exchangers |

| Air-Cycle Machines and Compressors |

| Pumps, Valves, and Manifolds |

| Fans and Blowers |

| Sensors and Controllers |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Commercial Passenger Aircraft | ||

| Regional and Commuter Aircraft | |||

| Business Jets | |||

| Military Fixed-Wing and Rotorcraft | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Cooling Technology | Air Cycle Systems | ||

| Vapor Cycle Systems | |||

| Liquid Cooling Systems | |||

| Hybrid and Solid-state/Thermoelectric | |||

| By Component | Heat Exchangers | ||

| Air-Cycle Machines and Compressors | |||

| Pumps, Valves, and Manifolds | |||

| Fans and Blowers | |||

| Sensors and Controllers | |||

| By End-Use | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast growth rate for aircraft cooling solutions through 2030?

The aircraft cooling systems market is projected to rise at a 5.59% CAGR from USD 6.34 billion in 2025 to USD 8.32 billion by 2030, translating into a 5.59% CAGR over the period.

Which platform segment is expanding quickest?

Business jets lead with an 8.91% CAGR as early adopters of advanced avionics and liquid cooling technologies.

Why are liquid loops gaining traction over air-cycle packs?

Electrification raises heat densities beyond pneumatic capacity, and liquid systems dissipate heat up to four times more efficiently while enabling battery and power-electronics cooling.

Which region offers the strongest demand upside?

Asia-Pacific shows the fastest 6.39% CAGR driven by China and India’s fleet expansions and indigenous aircraft programs.

How do regulations influence cooling-system design?

Stricter EASA and FAA cabin-comfort and environmental rules force adoption of higher-efficiency heat exchangers, smarter controls, and low-GWP refrigerants.

What role does additive manufacturing play?

3D printed micro-channel heat exchangers cut weight by 30% and shorten lead times, improving performance metrics and supply responsiveness for OEMs.

Page last updated on: