Commercial Aircraft Avionics Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

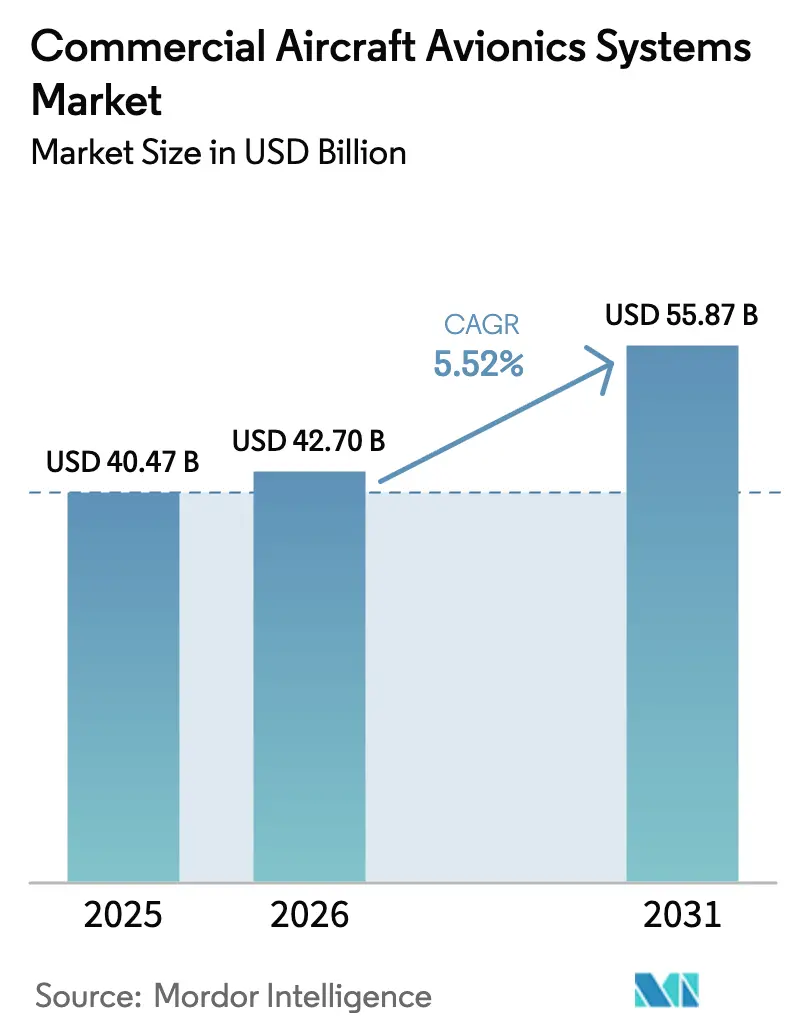

| Market Size (2026) | USD 42.70 Billion |

| Market Size (2031) | USD 55.87 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

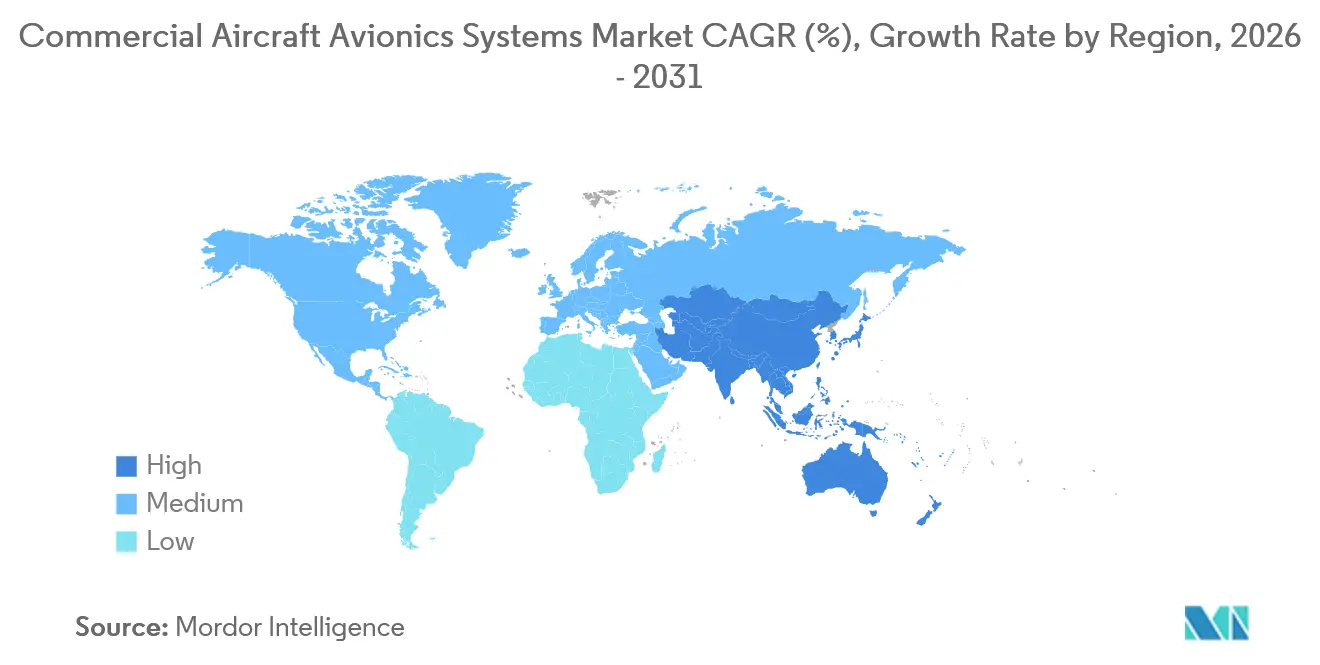

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Avionics Systems Market Analysis by Mordor Intelligence

The commercial aircraft avionics systems market size is expected to grow from USD 40.47 billion in 2025 to USD 42.70 billion in 2026. It is forecast to reach USD 55.87 billion by 2031, with a 5.52% CAGR over 2026-2031. Tighter equipage rules are already pulling forward cockpit upgrades, with the United States mandating ADS-B In by December 2031 for aircraft currently fitted with ADS-B Out and Europe requiring Performance-Based Navigation that limits ILS Category I use to contingencies after June 2030. Narrow body fleet expansion continues to anchor line-fit demand, reinforcing OEM integration pathways as airlines seek fuel and reliability improvements from advanced flight management systems. Predictive maintenance is another tailwind as Boeing’sAirplane Health Management 2.0 scales across large fleets and shifts maintenance toward sensor-driven intervals. Together, these factors keep the commercial aircraft avionics systems market focused on safety, compliance, and operational efficiency gains that improve dispatch reliability and reduce downtime.

Key Report Takeaways

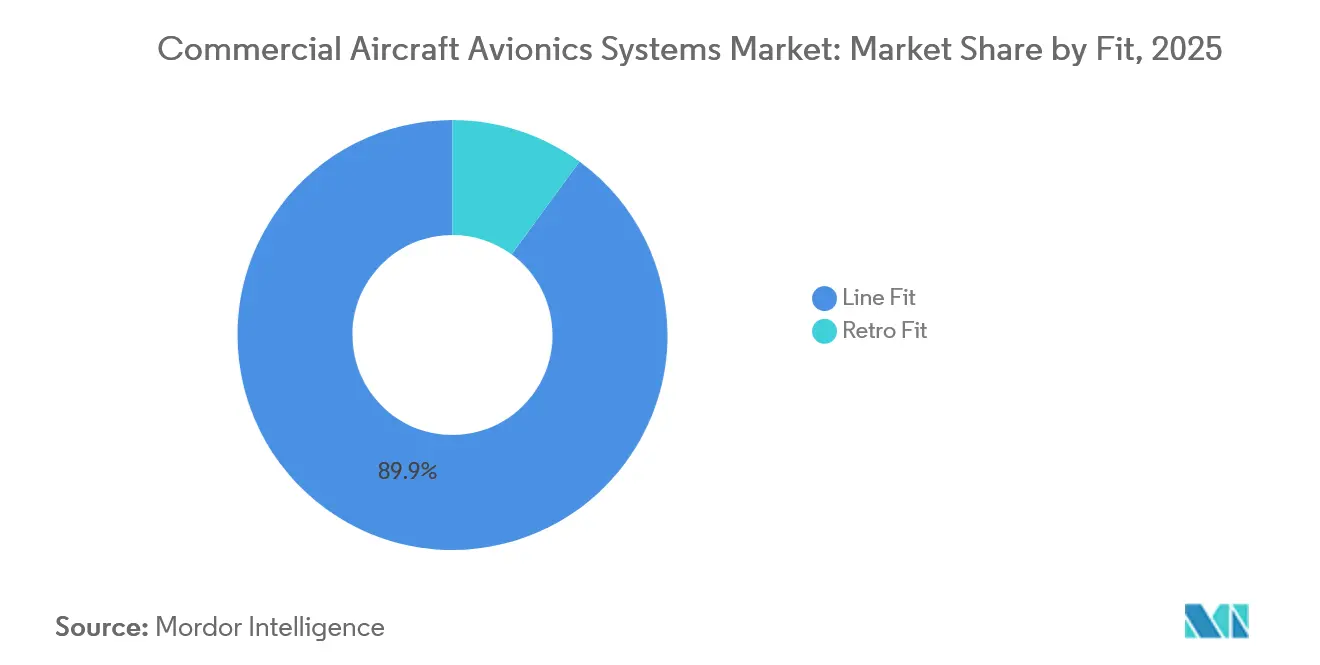

- By fit, line fit led with 89.94% revenue share of the commercial aircraft avionics systems market in 2025, while it is forecast to expand at a 6.04% CAGR through 2031.

- By aircraft type, narrow body jets led the commercial aircraft avionics systems market with a 67.83% revenue share in 2025 and are projected to grow at a 6.78% CAGR through 2031.

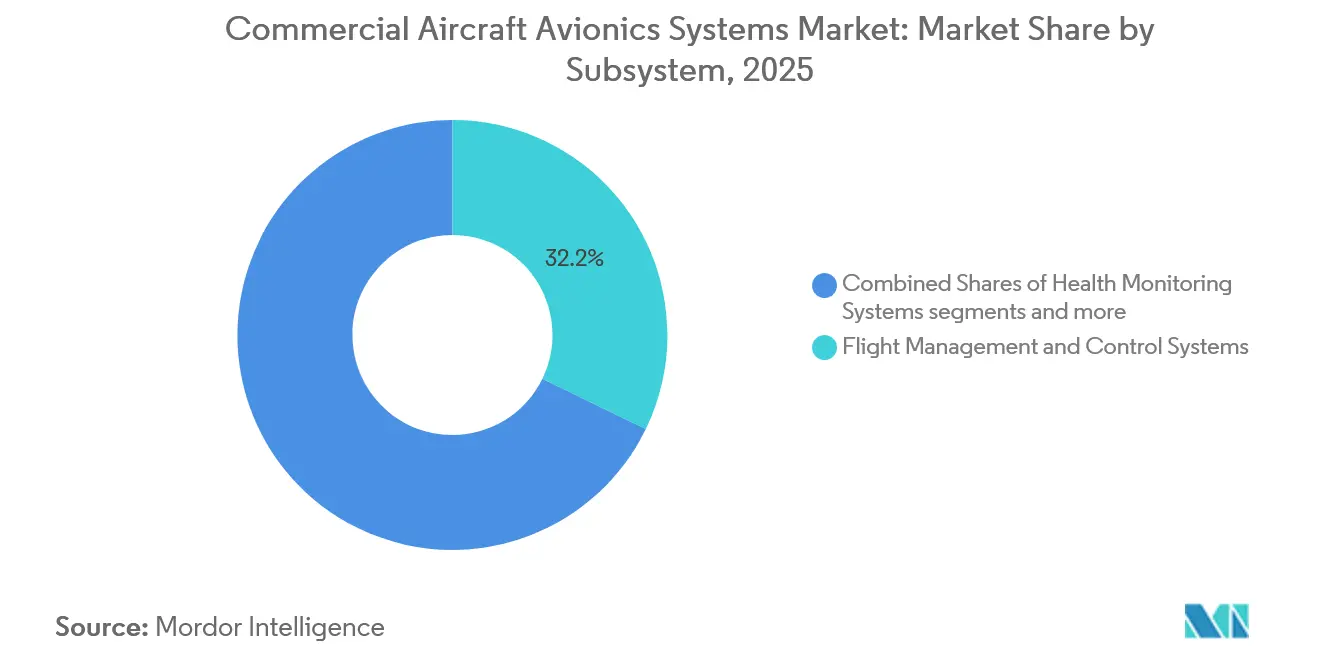

- By subsystem, flight management and control systems captured a 32.21% share in 2025, while visualization and display systems are forecast to expand at a 7.65% CAGR to 2031.

- By geography, Asia-Pacific held a 29.96% share of the commercial aircraft avionics systems market in 2025, and it is projected to record the fastest growth at an 8.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Aircraft Avionics Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet expansion and single-aisle dominance | + 1.8% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Mandated CNS/ATM equipage and surveillance (ADS-B, PBN, CPDLC) | + 1.5% | Global, with early gains in United States and European airspace | Short term (≤ 2 years) |

| Predictive maintenance and aircraft health monitoring adoption | + 0.9% | North America and Europe, with spill-over to Asia-Pacific | Medium term (2-4 years) |

| Cybersecurity regulations (EASA Part‑IS; DO‑326A/ED‑202A) driving upgrades | + 0.6% | Europe and North America, with EASA Part-IS influence spreading to Middle East & Africa | Short term (≤ 2 years) |

| Connected aircraft and cockpit digitalization | + 0.7% | Global, led by North America with rapid growth in Asia-Pacific | Medium term (2-4 years) |

| Fuel and emissions cost pressure accelerating FMS optimization | + 0.5% | Global, with regulatory intensity in Europe and expanding programs in North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fleet Expansion and Single-Aisle Dominance

Single-aisle production and deliveries remain the volume engine for avionics demand as airlines refresh narrow body fleets and accelerate line fit adoption of integrated cockpit suites. Airbus’s long-range forecast underscores sustained aircraft requirements across Asia-Pacific and other growth corridors, which drives multi-year avionics content tied to OEM build rates and service contracts. The commercial aircraft avionics systems market continues to benefit from single-aisle standardization, which supports advanced FMS functions, satellite navigation receivers, and modern displays aligned with required navigation performance. As airlines target fuel savings and higher asset utilization, cockpit upgrades become part of a broader efficiency program that hinges on precise routing and more dependable system health data. Supply tension around airframes and engines still shapes timelines, yet demand visibility remains strong for narrow body platforms where avionics value scales with delivery volume.

Mandated CNS/ATM Equipage and Surveillance (ADS-B, PBN, CPDLC)

Regulatory deadlines are compressing retrofit windows and pushing multi-system upgrades onto operator roadmaps in the United States and Europe. The US Senate’s October 2025 bipartisan agreement requires ADS-B In by December 31, 2031, for operators already equipped with ADS-B Out, which drives demand for traffic awareness and collision alerting in busy terminal areas and en route airspace.[1]U.S. Senate Committee Staff, “Cantwell, Cruz Bipartisan Aviation Safety Agreement Requires Full Implementation of ADS-B Technology,” U.S. Senate Committee on Commerce, Science, & Transportation, commerce.senate.gov Europe’s PBN rule set restricts ILS Category I operations to contingencies after June 6, 2030, and requires RNP APCH with LPV minima at all instrument runway ends, which accelerates SBAS-capable receivers, data-link upgrades, and display changes across fleets. Controller-Pilot Data Link Communications continue to expand, with European protected-mode requirements in the upper airspace already in effect and US domestic towers offering CPDLC departure clearances across major hubs. Certification queues shape project phasing as operators balance compliance with resource availability for aircraft downtime and engineering support. These mandates concentrate spending on navigation, data-link, and surveillance enhancements that enable access to key airspace and procedural efficiencies.

Predictive Maintenance and Aircraft Health Monitoring Adoption

Airlines are scaling predictive maintenance to convert unscheduled events into planned work and to protect on-time performance. Boeing’s Airplane Health Management 2.0 supports condition-based scheduled maintenance under FAA approval and aggregates high-rate data from large fleets to detect component degradations earlier.[2]Boeing Services Team, “Airplane Health Management & Monitoring (AHM),” Boeing, boeing.com Documented results include significant savings and sustained 100% technical dispatch in long-haul operations, which support broader adoption across additional fleet types. Aircraft health platforms also influence avionics architectures, since robust data buses, onboard processing, and secure connectivity are needed to deliver actionable analytics to maintenance control centers. This shift embeds digital services into avionics content, extending the commercial aircraft avionics systems market toward lifecycle value anchored in reliability and turnaround-time gains.

Fuel and Emissions Cost Pressure Accelerating FMS Optimization

Fuel remains one of the largest operating costs for carriers, so cockpit technologies that deliver measurable reductions draw sustained capital even during supply-chain headwinds. Honeywell’s upgraded FMS software suite, introduced in 2024, targets better vertical profiles and wind-optimal cruise levels, with reported fuel-efficiency improvements that strengthen the business case for rapid deployment. Navigation infrastructure programs also create downstream demand for compatible avionics, including receivers and procedures that enable more efficient trajectories. In aggregate, FMS-centric upgrades support compliance with evolving emissions frameworks while delivering direct fuel-cost savings that improve the payback for cockpit modernization. The commercial aircraft avionics systems market, therefore, benefits whenever carriers lock in multi-year efficiency targets tied to procedural improvements and advanced FMS functions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain and semiconductor constraints delaying deliveries and retrofits | - 1.2% | Global, acute in North America and Europe manufacturing hubs | Medium term (2-4 years) |

| Certification and airworthiness approval backlogs elongating STC/TC timelines | - 0.8% | North America and Europe, with ripple effects in Asia-Pacific | Medium term (2-4 years) |

| Air traffic controller staffing constraints limiting capacity and ROI timing | - 0.4% | North America and Europe, with spill-over impacts in Asia-Pacific | Medium term (2-4 years) |

| Cybersecurity compliance burden and talent gaps | - 0.3% | Europe and North America, spreading globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply-Chain and Semiconductor Constraints Delaying Deliveries and Retrofits

Persistent supply-chain stress has imposed high costs and operational burdens on airlines and their maintenance plans, thereby deferring certain retrofit projects. Delivery shortfalls and elevated backlogs continue to put pressure on schedules and resource allocation, affecting when operators can induct aircraft for avionics modifications. Component availability for complex flight-deck systems remains uneven, and that uncertainty leads airlines to prioritize mandatory equipage upgrades first. The net effect is a slower installation cadence for non-critical enhancements, even as regulatory deadlines pull forward must-have capabilities. This dynamic shapes project timing in the near term for the commercial aircraft avionics systems market.

Certification and Airworthiness Approval Backlogs Elongating STC/TC Timelines

Certification and surveillance workloads have risen, while some inspector functions face staffing gaps, stretching timelines for new approvals and modifications. Reported vacancies for FAA operations and avionics inspectors limit throughput for certificate management and surveillance, which constrains Supplemental Type Certificate pipelines that many avionics retrofits rely on. Past airworthiness directives and software fixes for complex avionics illustrate how investigations and corrective actions can take extended periods, reinforcing the need for robust safety assessments and design assurance. Cybersecurity compliance expectations have also moved into certification baselines on both sides of the Atlantic, further expanding documentation and review requirements for protections against intentional unauthorized electronic interactions. These realities extend program schedules and create sequencing challenges that airlines must factor into compliance roadmaps. In the commercial aircraft avionics systems market, that means project phasing must account for certification resource availability and hangar slots.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fit: Line-Fit Installations Anchor OEM Economics

Line Fit commanded 89.94% of the commercial aircraft avionics systems market share in 2025, and the segment is projected at a 6.04% CAGR through 2031 as OEM programs integrate full-suite cockpits at the factory. This scale advantage tightens supplier collaboration on certification artifacts that flow into Part 25 compliance and streamlines the software and hardware baselines that airlines inherit with new deliveries. As equipage rules converge on ADS-B In, PBN, and expanded data link, OEM-installed avionics deliver a ready compliance path that reduces post-delivery engineering burden for operators. Europe’s PBN transition reinforces this approach by making SBAS-capable navigation and LPV minima standard across instrument runway ends and by encouraging unified cockpit architectures in new builds.[3]European Union Aviation Safety Agency Editors, “Transition to Performance-Based Navigation (PBN) Operations,” EASA, easa.europa.eu

Retrofitting continues to serve aging single-aisle and twin-aisle platforms, with airlines prioritizing navigation, surveillance, and display changes where immediate compliance or fuel savings justify the downtime. Europe’s June 2030 constraint on non-PBN operations and the growing prevalence of LPV minima on instrument approaches push operators to add SBAS and upgrade cockpit displays that present modern guidance. Retrofit shops also plan for cybersecurity updates as EASA Part-IS takes effect for airlines and maintenance organizations in early 2026, which drives the inclusion of secure data loaders and network segmentation designs into modification packages. The commercial aircraft avionics systems market, therefore, balances high-volume line fit standardization with retrofit programs that protect access to regulated airspace and procedures.

By Aircraft Type: Narrow Body Jets Propel Volume, Wide Bodies Command Premiums

Narrow body jets accounted for 67.83% of the commercial aircraft avionics systems market size in 2025 and are projected to grow at a 6.78% CAGR through 2031, reflecting point-to-point network expansion and sustained fleet renewals. Airbus's long-range planning signals strong demand for single-aisle capacity in Asia-Pacific and other fast-growing corridors, which magnifies the avionics content per delivery. Airspace modernization in Europe and equipage mandates in the United States add urgency to line fit and retrofit cycles for navigation, data link, and surveillance upgrades that align to PBN and ADS-B In. These requirements reinforce consistent avionics baselines across narrow body fleets, improving training commonality and lifecycle support for operators. Airlines also target FMS-driven fuel savings in high-cycle single-aisle operations, and those savings scale meaningfully when applied to large narrow body subfleets.

Wide bodies maintain premium avionics content even as annual deliveries remain below historic peaks, with dual FMS channels, head-up and enhanced vision systems, and multi-band satcom architectures common on long-haul fleets. This raises per-aircraft avionics value, while refurbishment cycles cover display suites and communications systems in line with evolving data-link and cybersecurity standards. Predictive maintenance adoption also runs deep in long-haul fleets that target dispatch reliability and coordinated turnarounds across global hubs. Regional jets round out demand with selected upgrades for compliance and operations optimization, often paced by budget cycles and airspace access needs. Across types, the commercial aircraft avionics systems market reflects a mix of volume-driven narrow body programs and feature-rich twin-aisle fleets that reinforce the business case for full-suite integration.

By Subsystem: Flight Management Leads Share, Visualization Systems Sprint Fastest

Flight management and control systems captured 32.21% of the commercial aircraft avionics systems market size in 2025, supported by four-dimensional trajectory optimization, required navigation performance, and tighter coupling between FMS, autopilot, and auto-throttle. Honeywell’s upgraded FMS suite demonstrates how predictive navigation and wind-aware profile management can deliver meaningful fuel savings, which supports operator adoption across large fleets. Airlines implementing fuel programs have confirmed significant annual reductions through routing, procedures, and aircraft performance changes, coordinated with cockpit guidance. Regulatory modernization also sustains demand for multi-mode receivers and data-link capability that integrate with FMS to execute advanced procedures. This stack keeps FMS at the core of operational efficiency and compliance within the commercial aircraft avionics systems market.

Visualization and display systems are projected to grow at a 7.65% CAGR, reflecting the shift from legacy cathode-ray-tube instrumentation toward modern LCD-based glass cockpits that support SBAS approaches and integrated engine and systems awareness. European PBN milestones push for display refresh across fleets that need reliable presentation of guidance, terrain, and procedure data in compact, integrated formats. Airlines also seek digital pathways to accelerate database updates and to align cockpit configurations across subfleets for training and maintenance commonality. Health-monitoring and data services further elevate the role of onboard visualization, directing crews toward predictive alerts and mitigations. As these capabilities converge, the commercial aircraft avionics systems industry increasingly treats display refresh as a platform upgrade that unlocks both efficiency and regulatory compliance benefits.

Geography Analysis

Asia-Pacific accounted for 29.96% of the market size in 2025 and is projected to advance at an 8.11% CAGR through 2031, underpinned by long-term fleet growth and infrastructure investment. Airbus projects robust aircraft demand across the region through the 2040s, reinforcing line-fit avionics volumes for single- and twin-aisle programs. National regulators are updating frameworks for communications, navigation, and surveillance equipment, and China’s civil aviation law, effective July 2026, strengthens certification clarity for onboard systems.[4]CAAC Legal Department, “Civil Aviation Law of the People’s Republic of China (Effective July 1, 2026),” Civil Aviation Administration of China, caac.gov.cn As airlines scale predictive maintenance and digital operations, the region’s large order books translate into growing demand for modern FMS, SBAS navigation, and integrated display suites. These patterns keep the commercial aircraft avionics systems market in Asia-Pacific closely tied to OEM build rate execution, regulatory harmonization, and airport procedure deployment.

Europe and North America together represent the largest market share with mature demand centers anchored by installed fleets, strong OEM presence, and ongoing airspace modernization. Germany’s air navigation service provider recorded 3.071 million flight movements in 2025 and cut average ATC-related delays to around 30 seconds per flight, illustrating how system upgrades and modular architectures support throughput.[5]DFS Communications, “Luftverkehr 2025 in Deutschland: Mehr Flüge, gute Pünktlichkeit,” DFS Deutsche Flugsicherung, dfs.de In the United States, equipage rules and staffing dynamics shape the timing of cockpit projects, while navigation programs that expand DME coverage at busy airports reinforce demand for compatible avionics. European PBN milestones constrain non-compliant operations after June 2030 and concentrate retrofit activity on SBAS avionics and compatible display systems. Taken together, these factors drive multi-year compliance cycles that sustain the commercial aircraft avionics systems market across both regions.

The Middle East, Latin America, and Africa represent smaller but strategic growth footprints where fleet modernization and selected retrofit programs proceed as budgets and access requirements align. Premium long-haul operators in the Middle East continue to refresh cabin and cockpit systems, with major wide body retrofit programs that extend service life and standardize avionics. Across Latin America and Africa, compliance-driven upgrades for ADS-B and PBN remain a focal point, with timelines driven by regulatory scoping and certification resources. Commercial synergies with predictive maintenance platforms also emerge as airlines tie avionics changes to data-driven reliability goals. These dynamics contribute to diversified regional demand that complements the high-volume centers of North America, Europe, and Asia-Pacific, supporting a broad-based commercial aircraft avionics systems market through the forecast horizon.

Competitive Landscape

The commercial aircraft avionics systems market is driven by tier-1 suppliers specializing in flight-deck suites, communications, navigation, surveillance, and digital services. These firms leverage certification expertise, OEM integration programs, and support models aligned with airline maintenance goals. Their roadmaps focus on regulatory compliance, fuel and emissions optimization, and cybersecurity capabilities integrated with certification frameworks. As airlines adopt predictive maintenance and cockpit digitalization, integrated offerings combining FMS, displays, and data services are differentiating in both line-fit and retrofit channels. This market emphasizes lifecycle value, with program wins tied to multi-year support and upgrade paths.

Recent strategic moves underscore investments in autonomy, services, and next-generation avionics. Honeywell secured a multi-year IARPA award for a real-time speech anonymization solution to reduce language barriers for pilots, controllers, and autonomous systems. RTX’s Collins Aerospace and the Royal Netherlands Air and Space Force established a long-term avionics service center targeting 2026. L3Harris partnered with Joby Aviation to explore a hybrid VTOL platform for defense missions, advancing autonomy and mission systems integration. Safran expanded by acquiring Collins Aerospace’s flight control and actuation activities and launched the OSYRYS Clean Aviation project for next-generation regional aircraft energy management. These initiatives align R&D and industrial footprints with autonomy, electrification, and services growth.

Commercial Aircraft Avionics Systems Industry Leaders

Honeywell International Inc.

General Electric Company

Safran

Thales Group

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Panasonic Avionics Corporation announced that its Astrova in-flight entertainment (IFE) solution had been chosen by more than 30 airlines for 100 individual airline programs.

- September 2025: Thales and IndiGo, India’s largest airline, signed a strategic maintenance contract covering IndiGo's existing fleet of 430 Airbus A320 aircraft and a future order of over 800 A32X aircraft. Under this 11-year agreement, Thales will deliver expert repair services for avionics components, supported by its ‘Avionics-By-The-Hour’ (ABTH) program. This program offers a comprehensive spares management solution to ensure the availability of critical components and reduce aircraft downtime.

Global Commercial Aircraft Avionics Systems Market Report Scope

Avionics is an assembly of electronics subsystems integrated onboard an aircraft to carry out several mission and flight management tasks. These systems include engine controls, flight control systems, navigation, communications, flight recorders, lighting systems, fuel systems, electro-optic (EO/IR) systems, weather radar, and performance monitoring systems. The scope of the study excludes freighter aircraft, military aircraft, business jets, and other privately owned, chartered, and unscheduled aircraft.

The commercial aircraft avionics systems market is segmented by subsystem, aircraft type, fit, and geography. By subsystem, the market is segmented into health monitoring systems, flight management and control systems, communication and navigation, cockpit systems, visualizations and display systems, and other subsystems. The different subsystems include emergency systems, fire safety systems, electronic flight bags (EFBs), and weather systems. By aircraft type, the market is segmented into narrow body, wide body, and regional jet. By fit, the market is segmented into line fit and retrofit. The report also covers the market sizes and forecasts for the commercial aircraft avionics systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Line Fit |

| Retro Fit |

| Narrow Body |

| Wide Body |

| Regional Jet |

| Health Monitoring Systems |

| Flight Management and Control Systems |

| Communication and Navigation |

| Cockpit Systems |

| Visualization and Display Systems |

| Other Subsystems |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Fit | Line Fit | ||

| Retro Fit | |||

| By Aircraft Type | Narrow Body | ||

| Wide Body | |||

| Regional Jet | |||

| By Subsystem | Health Monitoring Systems | ||

| Flight Management and Control Systems | |||

| Communication and Navigation | |||

| Cockpit Systems | |||

| Visualization and Display Systems | |||

| Other Subsystems | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the Commercial Aircraft Avionics Systems market in 2026 and how fast is it growing?

The Commercial Aircraft Avionics Systems market size stands at USD 42.70 billion in 2026 and is projected to reach USD 55.87 billion by 2031 at a 5.52% CAGR.

Which segments lead growth within the Commercial Aircraft Avionics Systems market through 2031?

Narrow body aircraft lead volumes with a 67.83% 2025 share and a 6.78% CAGR, while visualization and display systems are the fastest-growing subsystem at 7.65% CAGR.

How do regulations influence investment in the Commercial Aircraft Avionics Systems market?

US ADS-B In by December 2031 and Europe’s PBN deadlines after June 2030 compress retrofit windows and direct spend toward surveillance, navigation, and data-link upgrades.

Which region is growing fastest in the Commercial Aircraft Avionics Systems market?

Asia-Pacific leads growth with an 8.11% CAGR forecast, supported by large multi-decade aircraft deliveries and modernization programs.

What role does predictive maintenance play in the Commercial Aircraft Avionics Systems market?

Predictive maintenance platforms like Boeing AHM 2.0 enable condition-based intervals and have delivered documented dispatch and cost gains, which strengthens adoption and lifecycle value.

How are suppliers positioning in the Commercial Aircraft Avionics Systems market?

Leading vendors pursue autonomy, services, and compliance-aligned upgrades, highlighted by investments in AI-enabled avionics, depot services, and cybersecurity-ready architectures.

Page last updated on: