Aircraft Health Monitoring Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

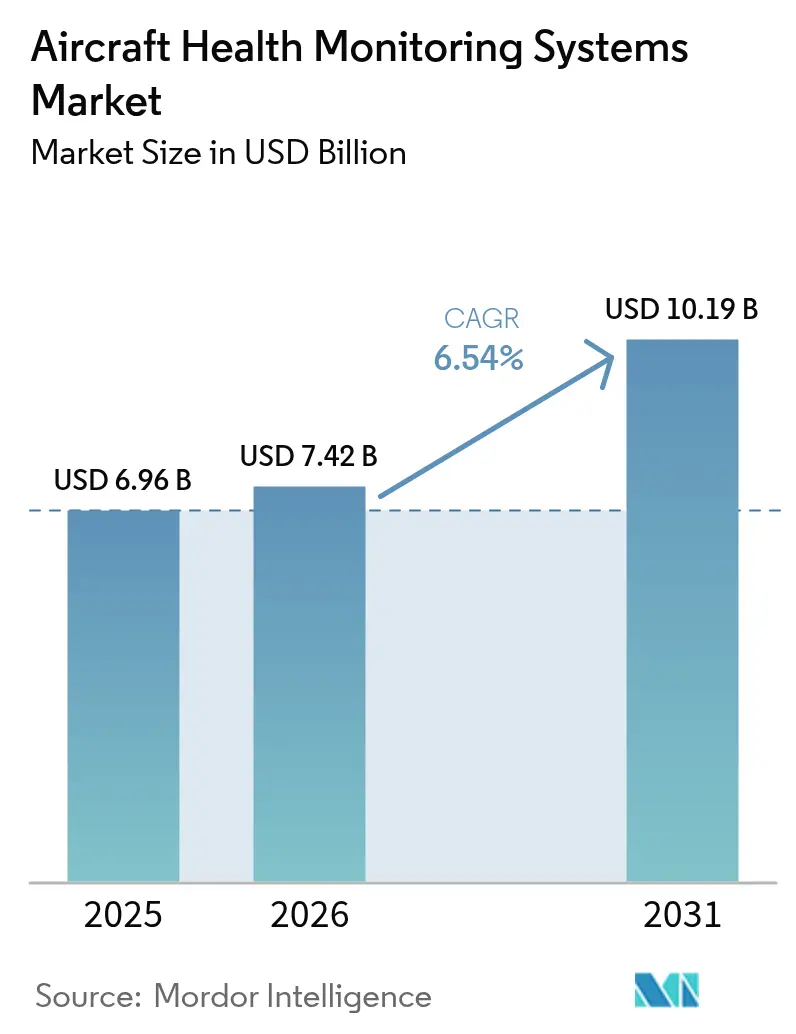

| Market Size (2026) | USD 7.42 Billion |

| Market Size (2031) | USD 10.19 Billion |

| Growth Rate (2026 - 2031) | 6.54% CAGR |

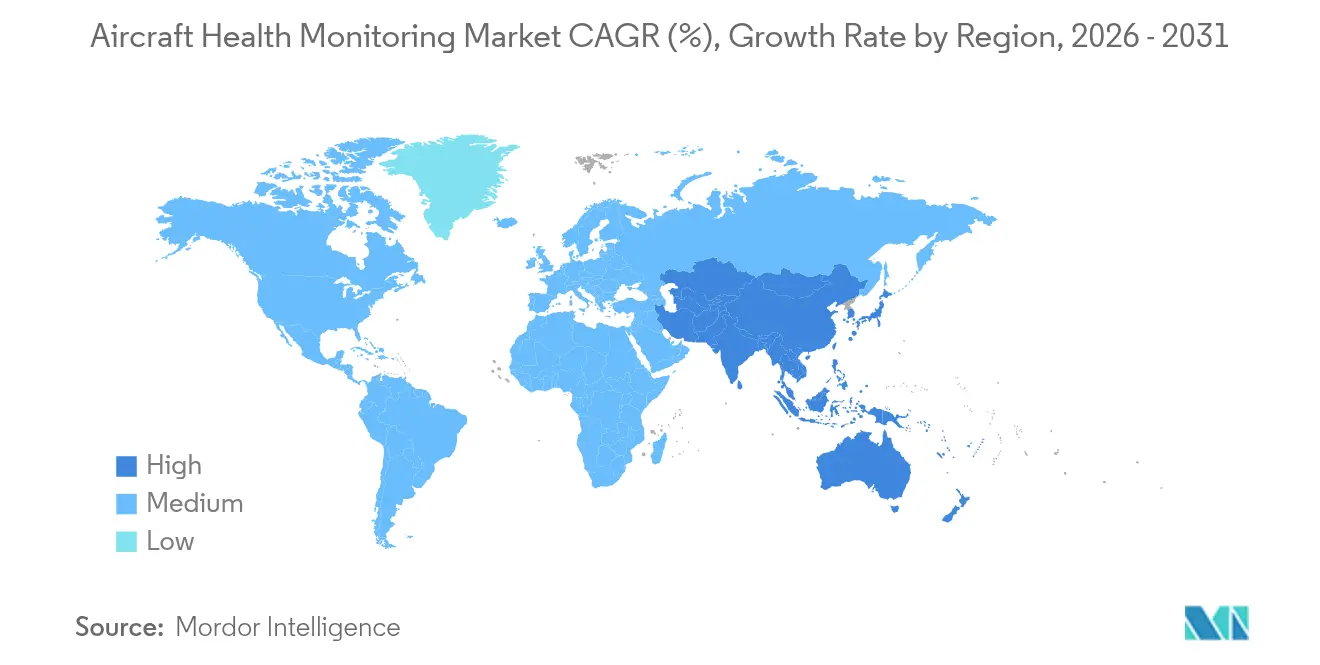

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Health Monitoring Systems Market Analysis by Mordor Intelligence

The aircraft health monitoring systems market size was valued at USD 6.96 billion in 2025 and estimated to grow from USD 7.42 billion in 2026 to reach USD 10.19 billion by 2031, at a CAGR of 6.54% during the forecast period (2026-2031). The upward trajectory reflects airline, MRO, and OEM investments in data-driven maintenance that cut unscheduled ground time and improve fleet availability. Regulatory bodies have tightened flight-data and structural-integrity rules, accelerating the installation of onboard analytics and secure connectivity systems.[1]Source: Federal Aviation Administration, “Advisory Circular AC 120-82,” faa.gov OEM digital platforms such as Airbus Skywise and Boeing Airplane Health Management scaled rapidly, providing real-time diagnostics across mixed fleets. Asia-Pacific fleet growth and urban-air-mobility prototypes further widened the application scope, while cybersecurity gaps and retrofit costs tempered near-term adoption.

Key Report Takeaways

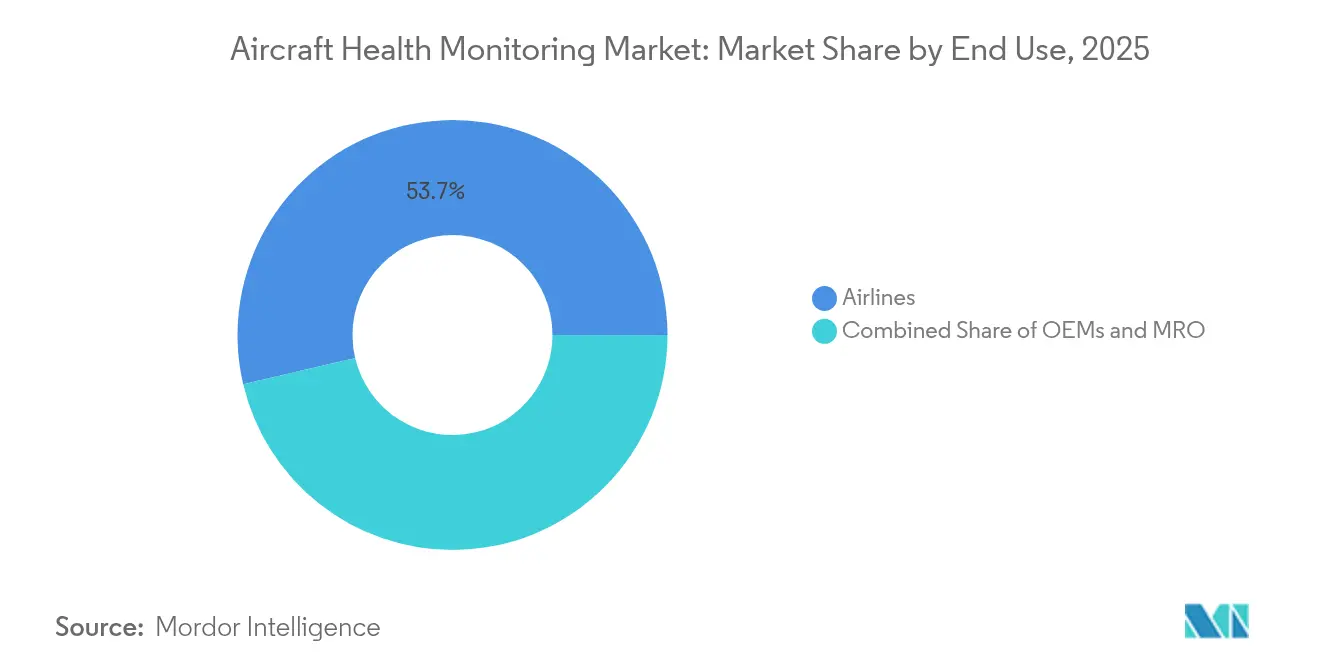

- By end user, airlines held 53.68% of the aircraft health monitoring systems market share in 2025, while the MRO segment is forecasted to expand at a 7.31% CAGR to 2031.

- By subsystem, aero-propulsion led with a 41.85% revenue share in 2025; aircraft structures are projected to grow at a 6.92% CAGR through 2031.

- By component, hardware accounted for 47.95% of the aircraft health monitoring systems market size in 2025, but software is set to post the fastest 8.18% CAGR between 2026 and 2031.

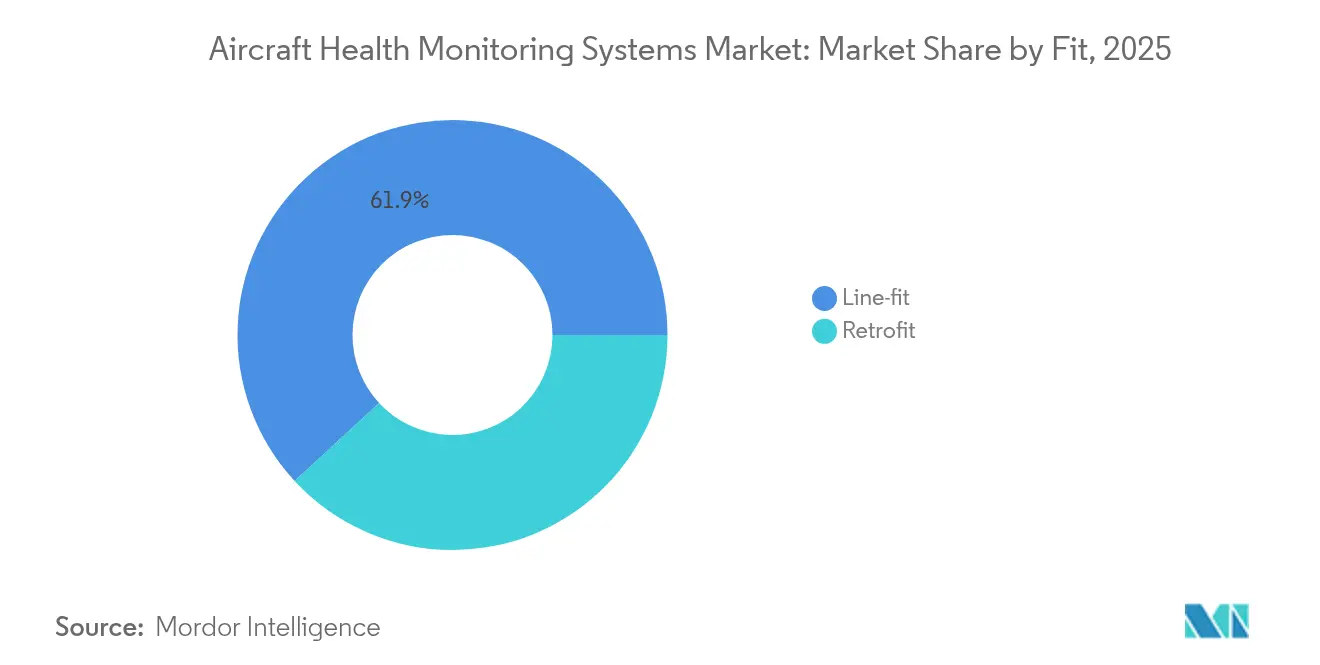

- By fit, line-fit represented 61.88% of the aircraft health monitoring systems market size in 2025, whereas retrofit installations will rise at a 7.63% CAGR to 2031.

- By transmission mode, on-board systems captured 55.25% market revenue in 2025, and ground-based transmission is anticipated to grow at an 8.09% CAGR through 2031.

- By aircraft type, fixed-wing platforms held a 56.65% share in 2025; advanced air mobility is forecasted to witness a 10.12% CAGR up to 2031.

- By geography, North America dominated with a 40.12% share in 2025, while Asia-Pacific will likely register a 7.02% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Health Monitoring Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Predictive maintenance imperative | +1.8% | Global | Medium term (2-4 years) |

| Regulatory mandates for flight and FOQA data | +1.2% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Rapid commercial fleet expansion | +1.5% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Connected-aircraft and IoT ecosystem maturity | +1.0% | Global, led by North America and EU | Medium term (2-4 years) |

| Digital-twin-driven virtual sensor modelling | +0.8% | Global, concentrated in advanced markets | Long term (≥ 4 years) |

| On-board edge-AI avionics processors | +0.6% | Global, early adoption in premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Predictive Maintenance Imperative

Airlines reported notable cuts in unscheduled maintenance events after adopting data-driven prognostics, with Honeywell indicating 99% prediction accuracy that avoided premature part removals.[2]Source: Honeywell Aerospace, “Moving Beyond the Hype of Predictive Maintenance,” aerospace.honeywell.com Rising labor costs and higher engine shop-visit rates made predictive maintenance a strategic hedge against budget pressure, especially as new-generation jets produce terabytes of sensor data per flight. Therefore, the aircraft health monitoring systems market transitioned from optional analytics to core operational infrastructure, embedding algorithms that flag anomalies during scheduled turnarounds. Wider adoption also improved asset-utilization metrics valuable to lessors and financiers. Collectively, these factors underpin a strong, multi-year stimulus for investment across the aircraft health monitoring systems market.

Regulatory Mandates for Flight and FOQA Data

The FAA’s revised Flight Operational Quality Assurance circular compelled US operators to institute continuous data-monitoring programs. ICAO and EASA rules mirrored this stance, extending requirements to structural components and aging-aircraft safety. Operators above 20,000 kg MTOW must now archive and analyze large data sets, turning compliance into a guaranteed buyer pool for monitoring software and secure recorders. Protection measures that shield airlines from punitive misuse of FOQA findings fostered voluntary uptake, further enlarging the aircraft health monitoring systems market.

Rapid Commercial Fleet Expansion

Airbus forecasted that passenger demand in Asia-Pacific will climb 3.8% annually through 2043, necessitating thousands of new deliveries. Each new narrowbody or widebody enters service with embedded diagnostics, instantly enlarging the installed base for aftermarket analytics contracts. Simultaneously, carriers launched retrofit programs on legacy aircraft to harmonize fleet-wide maintenance standards, pushing incremental growth in the aircraft health monitoring systems market size. High-cycle regional jets and low-cost-carrier operations magnified the value of predictive insights, boosting uptake across both mature and emerging routes.

Connected-Aircraft and IoT Ecosystem Maturity

More than 12,000 commercial jets had been linked to the Skywise data backbone by early 2025, transmitting secure streams that enable continuous surveillance. Satellite bandwidth improvements and low-latency links allowed data offloading even on polar or oceanic sectors. Edge processors executed first-line anomaly detection on board, while cloud engines refined models using fleet-wide comparisons. This bidirectional data flow strengthened OEM, airline, and MRO collaboration, anchoring an integrated aircraft health monitoring systems market in which insights translate directly into dispatch-reliability gains and optimized parts inventory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and data-integrity risks | -1.4% | Global, acute in connected aircraft | Short term (≤ 2 years) |

| High capex/retrofit integration cost | -1.1% | Global, pronounced in emerging markets | Medium term (2-4 years) |

| Operator-lessor-OEM data-ownership disputes | -0.8% | Global, concentrated in commercial aviation | Medium term (2-4 years) |

| Sensor ruggedization limits on ageing fleets | -0.6% | Global, acute in cost-sensitive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-security and Data-Integrity Risks

A 2024 GAO review pinpointed unpatched avionics software and supply-chain weaknesses that could permit data manipulation.[3]Source: US Government Accountability Office, “Aviation Cybersecurity: FAA Should Fully Implement Key Practices,” gao.gov IBM recorded a 74% jump in aviation-sector cyber incidents since 2020. A compromised sensor may feed spurious parameters to ground crews, undermining trust in predictive dashboards and potentially grounding aircraft until verification. Regulators drafted cohesive rules, yet operators still face integration costs for encryption, network segmentation, and continuous-monitoring tools. These uncertainties have postponed some retrofit programs and curbed near-term expansion of the aircraft health monitoring systems market.

High Capex/Retrofit Integration Cost

Cranfield University research showed that a full monitoring suite can exceed USD 1 million per legacy aircraft once installation downtime and certification testing are included. Added weight from sensor wiring also raises fuel burn, eroding cost-saving claims on older fleets. Smaller airlines, therefore, stagger adoption or limit deployments to engines only. In price-sensitive regions, such financial hurdles limit penetration, slowing overall CAGR for the aircraft health monitoring systems market despite proven long-term benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Airlines Maintain Scale, MROs Gain Momentum

Airlines held 53.68% of the aircraft health monitoring systems market in 2025, reflecting their direct accountability for dispatch reliability and passenger safety. Many flag carriers embedded OEM dashboards that flag anomalies hours before landing, allowing part pre-positioning and faster turnarounds. The aircraft health monitoring systems market size for airlines is expected to progress steadily as digital-first start-ups enter service with fully connected fleets. Independent maintenance, repair, and overhaul providers posted a brisk 7.31% CAGR outlook, using analytics dashboards to deliver value-added contracts that rival OEM packages. Their growth has been propelled by deals such as Lufthansa Technik’s AI-based inspection platform that cuts hangar time by 75%. Data-sharing protocols remain a sticking point because airlines aim to preserve proprietary flight-profile insights while MROs need access to refine predictive models. Consequently, partnerships that guarantee reciprocal access reshape procurement norms across the Aircraft Health Monitoring market.

In parallel, leasing companies demanded standardized data formats that support residual-value tracking, nudging airlines toward common interfaces. Low-cost carriers embraced non-proprietary software to sidestep vendor lock-in, stimulating open-architecture competition. The scale advantages of major network airlines continue to underpin bulk sensor-procurement agreements. Yet, regional players now tap cloud analytics on a subscription basis, widening entry pathways into the aircraft health monitoring systems market.

By Sub-system: Engines Lead, Structures Accelerate

Aero-propulsion systems generated 41.85% of global revenue in 2025, underscoring the centrality of engine condition monitoring to flight safety and cost. High-bypass turbofan maintenance bills justify sophisticated vibration and performance analytics, making engine OEMs early movers in the aircraft health monitoring systems industry. Aircraft structures, however, are projected to advance at a 6.92% CAGR as fiber-optic strain sensors and embedded Bragg gratings become lighter and cheaper. Airlines that operate composite-fuselage wide-bodies seek real-time insight into hidden delamination, elevating demand for structural-health dashboards.

The aircraft health monitoring systems market share of structural applications could widen further once regulators accept virtual inspection records in lieu of some manual checks. Digital twin platforms that overlay live strain data onto simulated load maps have shortened engineering-change cycles, opening new service revenues for OEMs. Meanwhile, avionics, environmental control, and auxiliary power units expanded monitoring to satisfy airframers’ performance-guarantee clauses. Market participants that blend multi-system analytics into a single cockpit view stand to capture incremental share within the aircraft health monitoring systems market.

By Component: Hardware Dominates, Software Captures Value

Hardware occupied 47.95% of revenue in 2025 through sensor packages, data gateways, and rugged recorders. Yet software is forecast to clock an 8.18% CAGR, becoming the principal margin driver as algorithms convert raw streams into actionable alerts. Line-fit installations increasingly ship with common-standard sensors, tilting incremental spending toward machine-learning licenses, cloud storage, and cross-fleet benchmarking dashboards. Two global carriers jointly piloted a neural-network tool that aggregated engine and airframe data, delivering 14% deeper fault-isolation accuracy and showcasing the monetization potential of software layers within the aircraft health monitoring systems market.

Services such as systems integration and regulatory documentation retained steady demand because operators require end-to-end solutions rather than standalone apps. Cyber-secure APIs, training modules, and data-quality audits grew in tandem, reinforcing a holistic value stack. Consequently, hardware vendors accelerated moves into analytics through acquisitions and joint ventures, illustrating how the competitive frontier of the aircraft health monitoring systems market is inexorably shifting toward software dominance.

By Fit: Line-fit Integrated, Retrofit Rising

Line-fit configurations accounted for 61.88% of the aircraft health monitoring systems market size in 2025, thanks to factory-level design synergies that minimize wiring and certification hurdles. OEMs embed monitoring nodes during assembly, allowing weight-neutral placement and enabling broader parameter capture. Airlines prefer such integrated kits because they avoid future service-bulletin costs. Though burdened by higher capex, retrofit programs are slated for a 7.63% CAGR as operators extend the life of 15-year-plus aircraft, especially freighters. Wireless sensors trimmed installation time by up to 40%, making partial retrofits economically viable.

Third-party providers developed portable ground receivers that tap standard quick-access recorder ports, which lowers engineering-order complexity. Leasing houses sponsor retrofit bundles tied to power-by-the-hour contracts, offsetting initial cost via predictable maintenance savings. This hybrid innovation cycle keeps the dynamic aircraft health monitoring systems market, drawing new players into approval and modification services while OEMs maintain an edge on future production orders.

By Transmission Mode: On-board Real Time, Ground-based Deep Analysis

On-board processing delivered 55.25% of revenue in 2025, reflecting airline preference for immediate crew alerts and dispatch decisions. Rudimentary diagnostic computers evolved into AI-enabled edge devices that could classify anomalies during climbs. Ground-based transmission, however, should expand at 8.09% CAGR because enhanced satellite links and 5G corridors allow full-flight data streaming. Cloud clusters can then execute computation-heavy digital-twin models without bandwidth constraints, adding depth to prognostic reports.

Hybrid architectures dominate bids, with non-critical data landing post-flight while safety-critical triggers remain on board. Regulators endorse this split approach as long as reliability analyses disclose latency risks. Vendors that bundle airtime, cybersecurity, and analytics under a single service level agreement capture sizeable contracts, reinforcing the structural sophistication of the aircraft health monitoring systems market.

By Aircraft Type: Fixed-Wing Core, Advanced Air Mobility Emergent

Fixed-wing fleets generated 56.65% of sales in 2025 across commercial, business, and defense niches. Each wide-body or single-aisle program integrates standardized engine, avionics, and structural sensors, sustaining the baseline scale of the aircraft health monitoring systems market. Rotary-wing platforms employed vibration-specific solutions to address gearbox fatigue, yet market share remained lower due to fleet size. Advanced air mobility vehicles are forecast to rise at a 10.12% CAGR as eVTOL developers bake in battery, propulsion, and structural monitoring from day one.

Certification roadmaps for urban air taxis demand 10-9 failure probabilities, effectively mandating continuous health data capture. Developers collaborate with semiconductor partners such as NXP to embed high-performance processors that safeguard latency budgets. Lessons learned in this environment could trickle back into conventional airframes, reinforcing innovation links across the aircraft health monitoring systems market.

Geography Analysis

North America remained the principal revenue center with 40.12% of the aircraft health monitoring systems market in 2025 as FAA mandates, mature MRO infrastructure, and early digital-service adoption converged. US carriers began replacing legacy quick-access recorders with 25-hour versions that align with new safety mandates, driving a steady upgrade cycle. Canadian operators similarly adopted engine-health kits for winter reliability, keeping regional demand resilient. The aircraft health monitoring systems market size within the region is forecast to retain mid-single-digit growth amid strict cyber-compliance requirements.

Asia-Pacific is projected to post the fastest 7.02% CAGR through 2031. Domestic networks in China, India, Indonesia, and Thailand moved from schedule recovery to optimization, relying on predictive dashboards to manage high-utilization narrow-body fleets. Airlines deploying new A320neo and B737-8 aircraft obtained factory-installed diagnostics, expanding the Aircraft Health Monitoring market. Governments promoted indigenous MRO capability, which leveraged cloud analytics to win third-party business, reinforcing regional self-sufficiency.

Europe delivered steady replacement demand amid EASA-driven safety-management-system reforms that compel structural-health assessments on aging airframes. Lufthansa Technik, Air France-KLM, and multiple low-cost carriers used monitoring data to refine parts pooling, improving profit resilience under carbon-pricing pressure. The region’s digital-twin research consortia attracted EU funding, enhancing analytic sophistication and ensuring that the aircraft health monitoring systems market remains a strategic component of broader aerospace innovation goals.

Regulatory Landscape

Aircraft Health Monitoring (AHM) / Aircraft Health Monitoring Systems (AHMS) deployments are governed mainly through existing airworthiness and continuing-airworthiness frameworks, rather than a single dedicated global standard. In the United States, FAA guidance such as AC 43-218 (operational authorization of integrated aircraft health monitoring systems) and flight-operations oversight practices tied to Part 121 programs shape how operators apply monitoring outputs within approved maintenance and reliability processes. Separately, FAA programs such as Continuing Analysis and Surveillance System (CASS) expectations emphasize continuous data collection and analysis as part of operator maintenance control, which increases the compliance value of secure flight and maintenance data capture.

In Europe, EASA certification and continuing-airworthiness requirements (including CS-25 for large aeroplanes) set technical expectations for monitoring, failure indication, and integration with aircraft systems. EASA has also addressed AHM integration with MSG-3 maintenance logic through certification material, reflecting efforts to align condition-based maintenance claims with standardized maintenance task development and acceptable means of compliance. Across jurisdictions, certification-credit use cases typically require verification and validation evidence for fault detection performance. Industry standards, including SAE guidance referenced by manufacturers, are then used to support consistent design and substantiation approaches.

Value Chain Analysis

The AHMS value chain begins with sensor, avionics, and data-acquisition hardware suppliers, including vibration, strain, temperature, and other condition sensors, data gateways, and recorders. Aircraft OEMs and engine OEMs then integrate these components for line-fit architectures, with supplemental type certificate pathways also used for retrofits. Connectivity providers (satellite and ground links) and cybersecurity and encryption tool vendors support data transmission, while software layers such as diagnostics, prognostics, and fleet benchmarking aggregate inputs from flight data, maintenance logs, and manufacturer databases into actionable maintenance recommendations. OEM platforms and large Tier-1 suppliers often package sensors, analytics, and connectivity into subscription offerings, while MROs and integrators provide installation, certification documentation, and ongoing condition-monitoring services.

On the downstream side, airlines, lessors, and defense operators act as primary buyers and data owners and users, translating alerts into work orders, parts provisioning, and scheduled maintenance planning. Regulatory and standardization bodies, including the FAA via AC 43-218 and EASA pathways for MSG-3 integration (as well as SAE/ISO guidance such as ARP-series references used in maintenance process definitions), influence how health monitoring outputs can be used for approved maintenance credit. A persistent bottleneck is demonstrating performance and governance sufficient for condition-based maintenance substitution in a manner regulators accept, which raises the role of verification, validation, and data integrity controls across the chain.

Competitive Landscape

The aircraft health monitoring systems market registered moderate consolidation, dominated by The Boeing Company, Airbus SE, Honeywell International Inc., GE Aerospace, and RTX Corporation. These five firms blended manufacturing scale with proprietary analytic ecosystems, capturing a large services backlog and shaping data standards. Boeing sought USD 50 billion in annual services by 2028, hinging on the market's growth. Airbus capitalized on Skywise alliances, while Honeywell packaged sensors, edge processors, and AI software into subscription bundles.

Specialist entrants focused on narrow niches such as embedded fiber sensors, edge-certificate cybersecurity, and battery prognostics. Lockheed Martin’s autonomous inspection drones demonstrated 99.59% defect recognition accuracy and won military trials. MTU’s acquisition of 3D.aero added machine-vision expertise that cuts borescope times.

Customer bargaining power increased as airlines demanded interoperable APIs and open data rights. Some carriers negotiated joint-intellectual-property clauses, aiming to in-source analytics portions over time. Suppliers responded by offering tiered licensing and white-label dashboards. The resulting competitive chessboard keeps pricing rational yet innovation brisk, positioning the aircraft health monitoring systems market for sustained evolution through strategic alliances and spin-offs such as Honeywell’s aerospace restructuring.

Aircraft Health Monitoring Systems Industry Leaders

The Boeing Company

Honeywell International Inc.

RTX Corporation

Safran SA

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Airline and OEM digital ecosystems create a clear whitespace for scalable, software-led monitoring that connects mixed fleets and multiple subsystems, particularly where operators want a single operational view across engines, structures, and auxiliary systems. Visible proof points support this demand. Airbus Skywise surpassed 12,000 connected aircraft by early 2025, and airlines continue signing for Skywise Fleet Performance+ to operationalize predictive maintenance workflows across active fleets. These programs increase requirements for interoperable data pipelines, cyber-secure APIs, and analytics that can extend beyond new-build line-fit aircraft, including retrofit-friendly approaches designed to reduce downtime and certification burden.

Condition-based maintenance enablement is another opportunity area, supported by ongoing regulatory and industry work to formalize acceptable pathways for AHM integration into MSG-3 logic and approved maintenance programs. As OEMs and Tier-1 suppliers bundle prognostics with long-term lifecycle support, the market is also shifting toward predictive maintenance contracts as a service layer rather than a standalone hardware sale. Recent commercial actions reinforce this direction: Collins Aerospace expanded FlightSense agreements with major airlines in 2026, and Bombardier and Rolls-Royce introduced an enhanced monitoring program for in-service and new Global 5500 and 6500 aircraft that combines aircraft connectivity with engine vibration and health monitoring units, showing continued productization of end-to-end monitoring stacks.

Recent Industry Developments

- June 2026: Bombardier and Rolls-Royce introduced an enhanced health monitoring program for Global 5500 and 6500 aircraft, combining Bombardier Smart Link Plus with Rolls-Royce engine vibration and health monitoring units (EVHMU). The upgrade being available across Bombardier's service center network broadens access for in-service fleets, strengthening OEM-led recurring digital services alongside traditional support.

- April 2026: Airbus announced an agreement with JetBlue to deploy the Skywise Fleet Performance+ (S.FP+) solution across its A320 and A220 fleets. The move deepens airline adoption of OEM analytics for predictive maintenance and fleet health monitoring, reinforcing platform-scale advantages tied to connected-aircraft data backbones.

- July 2024: HRL Laboratories announced a project to develop embedded sensors for wireless structural health monitoring. Work on embedded and hard-to-access sensing supports the structural-monitoring segment by improving data capture feasibility and reducing wiring and installation complexity that can constrain retrofits.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers aircraft health monitoring systems that collect aircraft condition and usage data, transmit it, and convert it into maintenance actions through analytics, alerts, and decision support across commercial and defense fleets.

Scope exclusions: This sizing excludes airport ground infrastructure monitoring tools and broad airline ERP platforms that are not directly used for aircraft condition monitoring.

Segmentation Overview

- By End User

- OEMS

- Airlines

- MRO

- By Sub-system

- Engines

- Avionics

- Aircraft Structures

- Environmental Control and Ancillary Systems

- By Component

- Hardware

- Sensors

- Avionics

- Flight Data Management Systems

- Connected Aircraft Solutions

- Ground Services

- Software

- Onboard Software

- Diagnostics Analytics

- Prognostics Analytics

- Services

- Integration and Customisation

- MRO/Condition-Monitoring Services

- Hardware

- By Fit

- Line-fit

- Retrofit

- By Transmission Mode

- Onboard

- Ground-based

- By Aircraft Type

- Fixed-Wing

- Commercial Aviation

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Transport Aircraft

- Military Aviation

- Fighter Aircraft

- Transport Aircraft

- Special Mission Aircraft

- Business and General Aviation

- Business Jets

- Light Aircraft

- Commercial Aviation

- Rotary Wing

- Commercial Helicopters

- Military Helicopters

- Military Unmmaned Aerial Vehicles

- Advanced Air Mobility

- Fixed-Wing

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Israel

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the aircraft activity baseline and to anchor technical scope so the model stays close to what is actually installed and used on aircraft. We relied on public sources such as FAA and EASA airworthiness and safety publications, ICAO air transport indicators, aircraft delivery and fleet in-service statistics from official registries, and selected peer-reviewed papers on HUMS and condition-based maintenance.

To translate activity into dollars, we also reviewed company filings and investor presentations for revenue cues around avionics and digital maintenance offerings, along with association content and reputable aerospace trade press for adoption themes. Where needed, paid subscriptions for company financials and patent databases were used to cross-check product focus, release timing, and broad pricing direction. These examples are illustrative only, and many other public sources were referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets counted as an aircraft health monitoring system sale versus adjacent digital tools, and on confirming how installs differ by aircraft type and fitment (line-fit versus retrofit). We spoke with a mix of OEM-side experts, operators, MRO-focused roles, and engineering specialists across major aviation regions so assumptions on penetration, typical package mix, and service attach rates could be corrected where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 43% |

| Mid tier: 46% | Functional/Unit leaders: 31% | EMEA: 35% |

| Smaller Players: 21% | Managers: 56% | Americas: 22% |

Market-Sizing & Forecasting

Sizing started with a top-down build where global and regional aircraft fleet, utilization, and delivery outlooks were translated into an addressable install base, and then filtered by expected adoption of health monitoring on engines, airframe, and key components. Only after the demand pool was set were price and mix assumptions applied, using typical system content (hardware, software, and services) and how it changes between line-fit and retrofit programs.

Selective bottom-up approximations were then used to pressure-test the totals, including supplier revenue sense-checks, sampled package value ranges by aircraft category, and channel checks on service and analytics attach rates. Key inputs that moved the model included in-service fleet by aircraft type, annual flight hours and cycles (which drive maintenance intensity), retrofit penetration by age cohort, connectivity and data transmission readiness, and the share of maintenance shifting toward predictive or condition-based practices.

Forecasting used scenario analysis supported by simple regression-style relationships between fleet growth, utilization recovery, and digital maintenance adoption, then adjusted using expert views on certification timelines and airline spending cycles. When bottom-up inputs were patchy in smaller regions or niche rotorcraft fleets, gaps were handled through adoption proxies tied to fleet size and MRO intensity, and then rechecked during validation calls.

Data Validation & Update Cycle

Model outputs were triangulated against independent signals such as aircraft deliveries, active fleet counts, and maintenance activity indicators, and then reviewed for unusual jumps in penetration, pricing, or service share. Where variances appeared, assumptions were re-opened, and follow-up outreach was triggered to confirm whether the change was real or caused by scope overlap.

Before sign-off, the dataset and calculations go through multi-step analyst review so unit logic and regional splits remain consistent with the market definition. The report is refreshed annually, with interim updates when major events materially change fleet utilization, retrofit cycles, or regulation-driven maintenance behavior. Right before delivery, a fresh analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Aircraft Health Monitoring Systems Market Size Compared Against Other Published Estimates

Published market values for aircraft health monitoring systems do not always line up, and the main reasons usually come from what each study counts as a system, how service revenue is treated, and the year used as the sizing anchor. Differences also show up when aircraft categories are grouped differently, or when assumptions on retrofit timing and analytics attach rates are not checked with real operator behavior.

The biggest gap driver is whether broader airline IT platforms and airport-side monitoring are included, and in Mordor Intelligence's model only onboard and aircraft-linked hardware, software, and connected services that directly support condition monitoring and maintenance actions are counted. Estimates can also move when aggressive utilization recovery or faster penetration is assumed without aligning it to delivery schedules, certification timing, and typical upgrade intervals. For that reason, we anchor adoption to fleet age cohorts and then validate pricing progression with interview feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.42 B (2026) | |

| Global Consultancy A | USD 7.25 B (2025) | Uses an earlier anchor year and applies a higher long-run growth path, and the scope appears to be broader around digital maintenance bundles, which can pull adjacent software into the total. |

| Industry Publisher B | USD 6.14 B (2025) | Leans more heavily on a conservative adoption curve for retrofit and service attach, and it can understate near-term value if line-fit uptake and analytics subscriptions are not fully reflected. |

The comparison shows that most of the spread comes from scope edges and from how quickly adoption and pricing are allowed to move year to year. By keeping the counted revenue tied to aircraft-linked monitoring functions, and by using fleet, utilization, and fitment checks to keep assumptions realistic, the final number stays traceable to repeatable steps instead of broad digital spending totals.

Key Questions Answered in the Report

What is the current size of the Aircraft Health Monitoring Systems market?

The market stood at USD 7.42 billion in 2026 and is projected to reach USD 10.19 billion by 2031 on a 6.54% CAGR trajectory.

Which segment leads the Aircraft Health Monitoring Systems market?

Airlines held the top position with 53.68% market share in 2025, driven by direct operational-reliability pressures and embedded monitoring in new aircraft.

Which is the fastest growing region in Aircraft Health Monitoring Systems Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period.

Why is Asia-Pacific the fastest-growing region?

Rapid fleet expansion, new-aircraft deliveries, and digitalization programs are expected to push Asia-Pacific to a 7.02% CAGR through 2031.

What role does software play in market growth?

Software analytics are forecasted to post an 8.18% CAGR as machine-learning tools transform sensor data into actionable maintenance insights, shifting value capture from hardware to algorithms.

How will advanced air mobility influence future demand?

EVTOL programs are integrating health monitoring from design inception, creating a high-growth sub-segment that is projected to expand at 10.12% CAGR and drive innovation for traditional aviation.

Page last updated on: