Aircraft Engine Blades Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

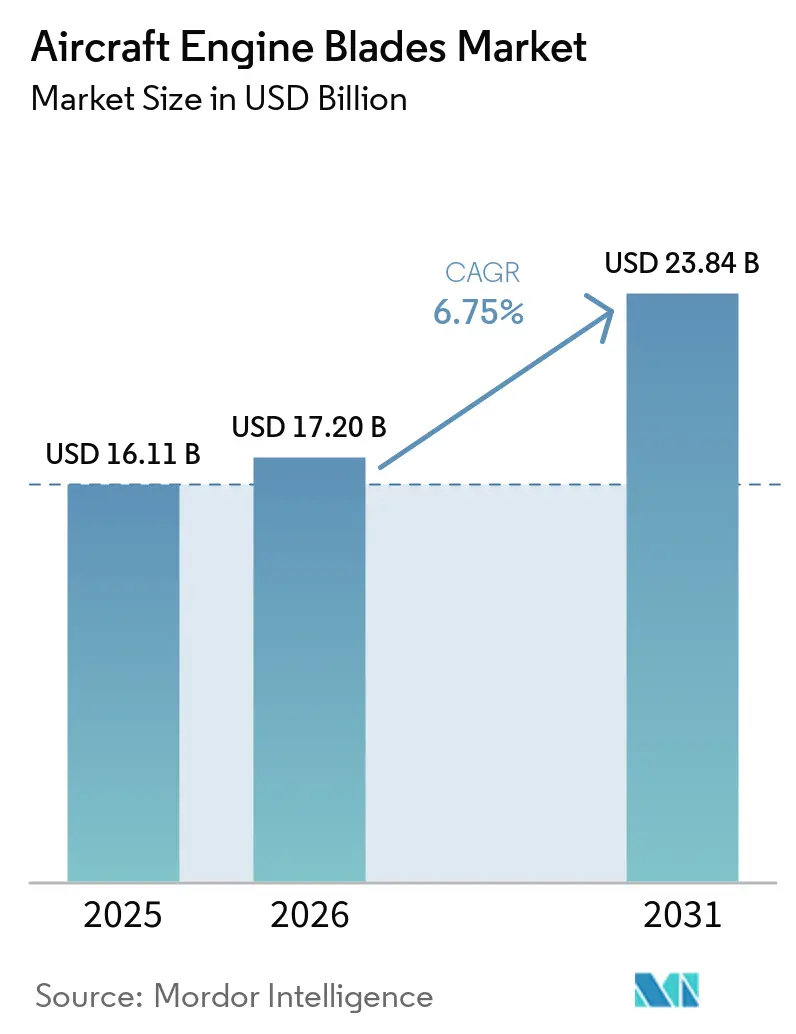

| Market Size (2026) | USD 17.20 Billion |

| Market Size (2031) | USD 23.84 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Engine Blades Market Analysis by Mordor Intelligence

The aircraft engine blades market size is expected to grow from USD 16.11 billion in 2025 to USD 17.20 billion in 2026 and is forecast to reach USD 23.84 billion by 2031 at a 6.75% CAGR over 2026-2031. Rising aircraft deliveries are anchoring near-term demand, with Airbus reporting 793 deliveries in 2025 and Boeing delivering 600 aircraft, and both production systems preparing for further ramp-up in 2026. Engines that power the core of narrowbody growth are scaling too, with LEAP output targeted for sustained high-rate production and a deep backlog that ties blade orders to aircraft delivery slots through the decade. Defense procurement strengthened turbine blade volumes in 2025 as modernization programs accelerated and contract awards advanced into 2026 production schedules. Shorter shop visit intervals for newer engines are adding another layer of aftermarket pull-through, concentrating demand for high-pressure turbine and compressor airfoils in the MRO channel.

Key Report Takeaways

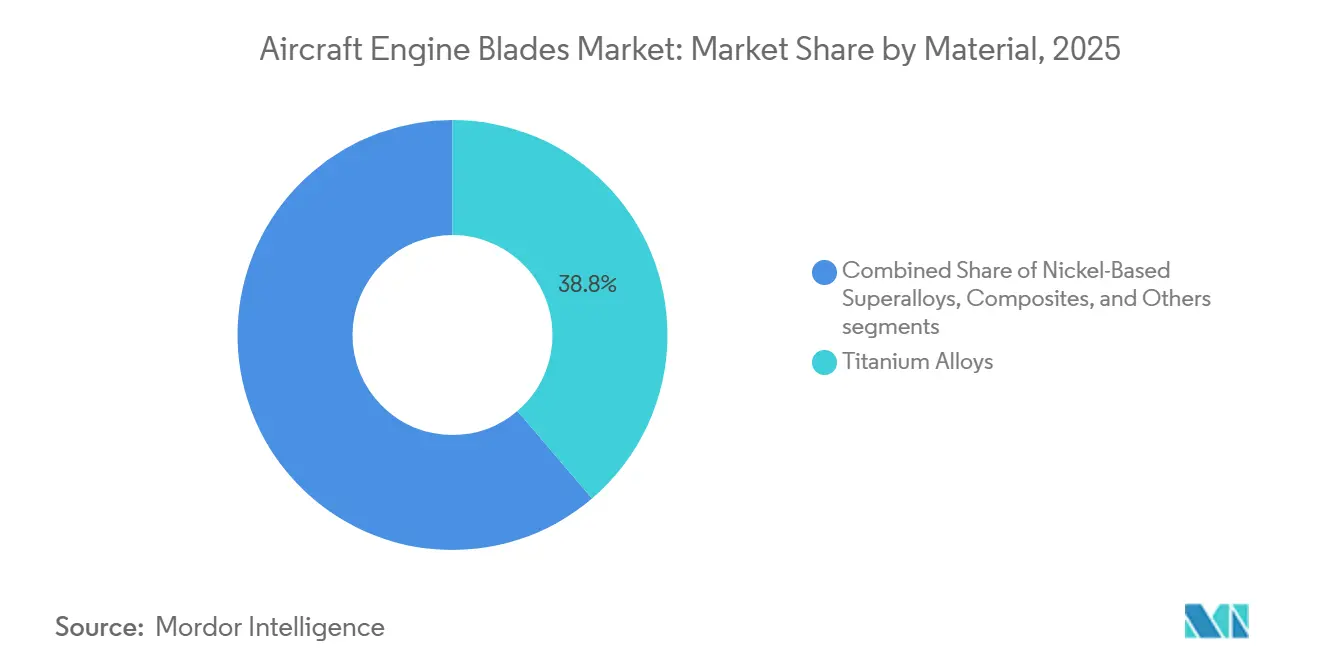

- By material, titanium alloys led with 38.76% of the aircraft engine blades market share in 2025, while composites are projected to expand at a 9.43% CAGR through 2031.

- By blade type, compressor blades held a 42.32% share in 2025, while turbine blades are set to grow at a 7.21% CAGR through 2031.

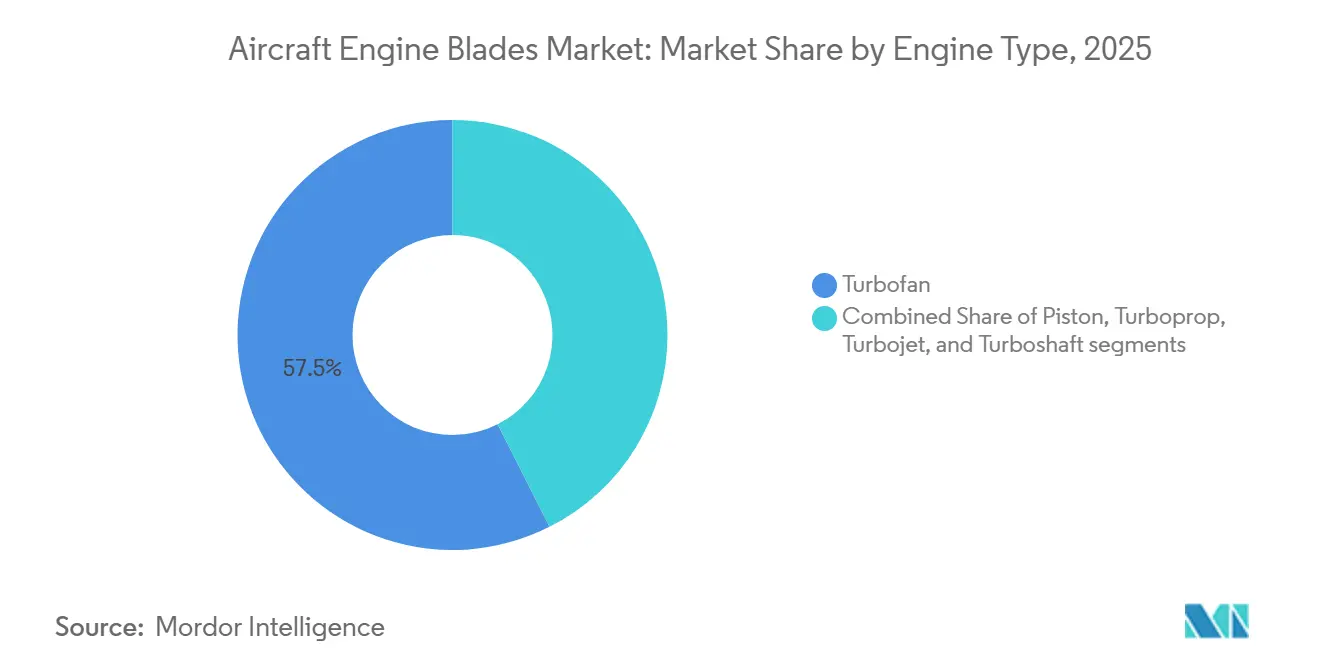

- By engine type, turbofan engines captured a 57.45% share in 2025 and are forecasted to grow at the fastest 7.87% CAGR through 2031.

- By aircraft type, commercial aviation led with a 65.21% share in 2025, while military aviation is projected to post the highest 7.65% CAGR through 2031.

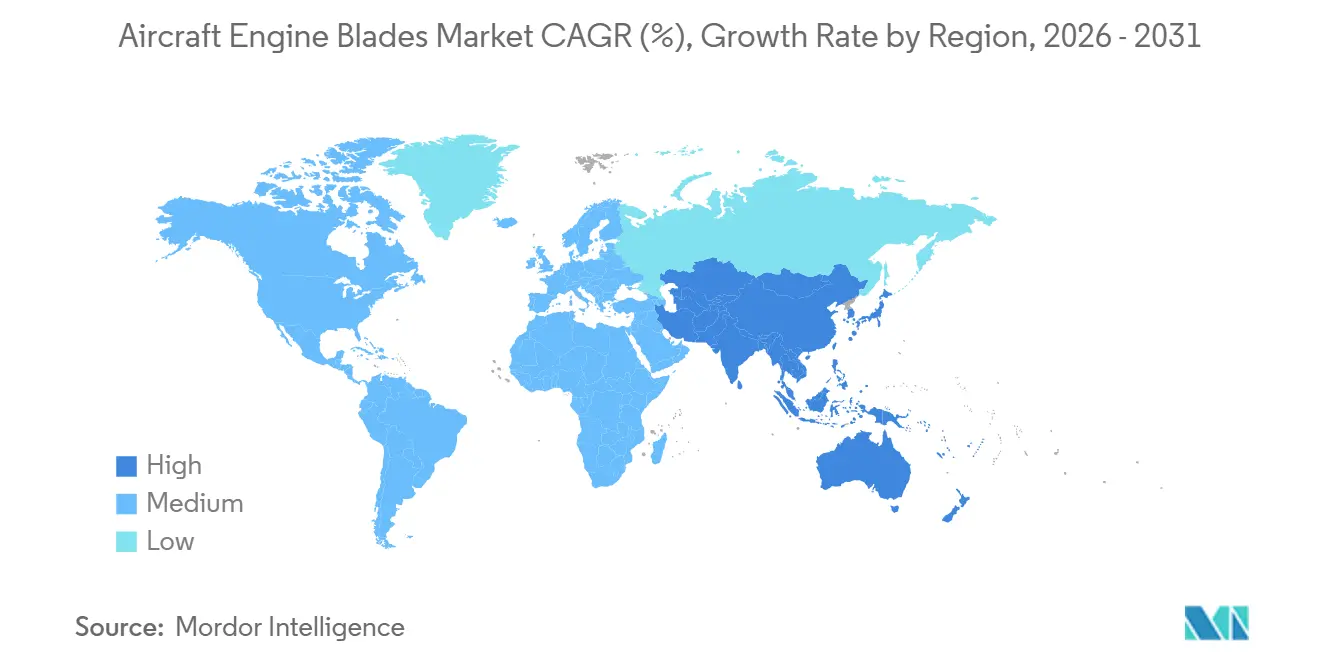

- By geography, North America held a 33.24% share in 2025, while Asia-Pacific is expected to be the fastest-expanding region at an 8.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Engine Blades Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global aircraft deliveries and fleet expansion driving engine blade demand | +1.8% | Global, highest intensity in Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing demand for fuel-efficient next-generation turbofan engines | +1.5% | Global, core uptake in Europe and North America | Medium term (2-4 years) |

| Military modernization programs accelerating turbine blade procurement | +1.2% | North America, Middle East, Asia-Pacific | Short term (≤ 2 years) |

| Shorter aftermarket MRO cycles increasing blade replacement demand | +0.9% | Global, early gains in North America, Europe | Short term (≤ 2 years) |

| Integration of smart sensor-enabled blades supporting predictive maintenance | +0.7% | North America, Europe | Medium term (2-4 years) |

| Additive manufacturing-enabled circular titanium feedstock improving material sustainability | +0.6% | Global, pilots in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Aircraft Deliveries And Fleet Expansion Driving Engine Blade Demand

Airbus reported 793 commercial aircraft deliveries in 2025 and guided higher output in 2026, while Boeing delivered 600 aircraft in 2025, suggesting blade demand will track the upward slope of assembly lines as slots are filled amid strong order backlogs. Narrowbody concentration amplifies this demand signal because each high-rate engine line draws substantial volumes of compressor and turbine airfoils throughout the build process. The LEAP family’s shipset, with numerous blades across stages, translates minor monthly changes in engine production into significant variations in airfoil demand, impacting supplier operations and planning in the aerospace supply chain. Regional dynamics are shifting load toward Asia, as the A321 has become the dominant variant in Airbus’s single-aisle backlog and India’s multi-year order flow demands engine and blade capacity that must be localized or supported via resilient transnational logistics. FAA and EASA airworthiness directives also frame replacement cycles for in-service fleets, with proposed FAA AD 2025-0341 addressing high-pressure turbine blades produced with non-compliant porosity and defining specific replacement actions within cycle limits.

Increasing Demand For Fuel-Efficient Next-Generation Turbofan Engines

Commitments to the newest engine platforms are locking in multi-decade blade demand as airlines move to reduce fuel burn by double digits on narrowbody and widebody missions. Recent selections by American Airlines and Pegasus highlight sustained LEAP engine adoption across Airbus and Boeing narrowbody fleets, driving consistent demand for compressor and turbine blades throughout production cycles and maintenance operations.[1]Safran Group Press Office, “Pegasus Airlines Finalizes Agreement for CFM LEAP-1B Engines,” Safran, safran-group.com In-service experience on harsh routes has prompted targeted blade design and durability improvements, with CFM advancing upgraded high-pressure turbine airfoils and associated systems to stabilize time-on-wing profiles for LEAP variants. Advanced materials are also moving from test cells to fleets, with 3D-printed ceramic-matrix composite components validated for the GE9X, poised for entry into service alongside new-generation widebodies. These technological shifts support lower fuel consumption and emissions targets. Still, they also increase blade complexity in repair and overhaul, which influences scrap rates, parts availability, and cost structures at MROs.

Military Modernization Programs Accelerating Turbine Blade Procurement

Defense demand strengthened in 2025 as major programs advanced, driving increased procurement of both new-production blades and spares to support intensive operating tempos. F-35 deliveries reached a record in 2025, and fresh multi-lot agreements secured output into the next planning window, locking in turbine blade requirements from core suppliers and sustainment ecosystems. Increased funding for adaptive propulsion expands technology risk budgets for next-generation programs, driving demand for airfoils capable of handling high thermal cycles and supporting variable-bypass architectures. Helicopter upgrades and regional defense aircraft orders contributed incremental pull for turboshaft and turboprop blades, adding breadth to the mix even as fighter programs dominate volume narratives.

Shorter Aftermarket MRO Cycles Increasing Blade Replacement Demand

Shop visits accelerated faster than initially expected, with industry tracking a sharp rise in events through the middle of the decade that directly increased blade replacement volumes. Fleet age normalization, along with earlier-than-planned removals for newer engines, is creating a tight scheduling environment and a greater emphasis on parts pooling to avoid extended ground time. OEM durability kits for high-pressure turbine stages are now being deployed in fleets, reducing premature wear in harsh environments while still front-loading demand for replacement blades as updated parts are installed. MRO networks report increased variability in workscope and turnaround, reflecting both maturing reliability fixes and transitional engine cohorts entering their first full restorations. Material costs remain the largest share of overhaul expense, and operators are actively managing life-limited parts and used serviceable material strategies to balance availability, lead time, and capital exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and manufacturing complexity of superalloys and ceramic matrix composites | -1.1% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Lengthy certification and quality assurance timelines for advanced blade technologies | -0.9% | Global, strict FAA/EASA regimes | Medium term (2-4 years) |

| Supply chain fragility for argon and helium used in single-crystal casting | -0.7% | Global, highest risk in Asia-Pacific | Short term (≤ 2 years) |

| Limited non-destructive inspection standards for large composite fan blades | -0.5% | Global, regulatory focus in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost And Manufacturing Complexity Of Superalloys And Ceramic Matrix Composites

Advanced alloys and composites carry high embedded energy and process costs, which keep blade pricing elevated and constrain yield during production ramp-ups. Overhaul economics are highly sensitive to material costs, and research shows that the majority of shop visit expense is tied to replacement parts, including life-limited turbine components, which intensifies budget pressure during heavy maintenance cycles. Nickel alloy markets face intersecting policy and demand effects, including tariff actions and sector-specific needs, which translate into variable cost trajectories for aerospace-grade material. Airlines also faced broader cost headwinds in 2025 due to supply chain constraints, with maintenance, leasing, and inventory burdens adding billions to sector expenses, thereby indirectly reinforcing conservative procurement and stocking stances for critical parts like blades. OEM investments in capacity and advanced factories are designed to counter these pressures, as seen with European titanium compressor blade lines that apply high-throughput digital production techniques to stabilize supply for high-volume narrowbody engines.

Lengthy Certification And Quality Assurance Timelines For Advanced Blade Technologies

Certification pipelines for new blade materials and processes have lengthened as aviation authorities scrutinize complex manufacturing routes and field performance over extended timelines. Regulatory actions underscore this dynamic, with a 2025 FAA notice of proposed rulemaking targeting specific high-pressure turbine blade lots and requiring defined replacements. This process can pause or slow deliveries during evaluation. Qualification of additively manufactured hot-section components required new non-destructive evaluation methods and supplemental material controls, and while breakthroughs have been certified on the GE9X program, the effort demonstrates the rigor needed before broad-scale deployment. Supply chain diversification efforts in emerging aerospace hubs are advancing the production of advanced blades. Yet, the first-time qualification of single-crystal and coated parts still involves steep learning curves and extensive process verification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Titanium Alloys Dominate Despite Composites Gaining Momentum

Titanium alloys accounted for 38.76% of the aircraft engine blades market in 2025, as the material’s strength-to-weight ratio, corrosion resistance, and temperature capability supported both compressor stages and selected turbine locations across major engine families. The aircraft engine blades market for composites is projected to expand at a 9.43% CAGR to 2031, driven by the shift toward higher turbine inlet temperatures and the adoption of ceramic-matrix composite designs that improve engine efficiency and reduce cooling air requirements in approved applications. Titanium supply security remains a central theme for blade producers due to concentration in upstream sponge capacity and national policy actions that influence availability, leading OEMs and Tier 1s to secure long-term agreements and, where practical, diversify sources within certification constraints- on the technology front, additive processes for hot-section components reached significant milestones, with certified 3D-printed CMC structures on the GE9X demonstrating the viability of advanced designs that would be difficult to achieve through conventional routes.[2]GE Aerospace, “A Flying Start: GE9X Durability Technologies,” GE Aerospace, geaerospace.com These shifts are shaping a balanced portfolio in which titanium continues to anchor high-volume compressor blade production. At the same time, composites expand into defined roles where thermal and environmental barrier requirements justify higher initial costs.

OEM investments in high-rate titanium compressor blade facilities are designed to de-risk near-term capacity for LEAP and similar programs. At the same time, composite content growth depends on continued progress in inspection standardization and lifecycle validation in harsh operating environments. The aircraft engine blades industry is also driving digital inspection and repair planning to manage heterogeneity in composite structures, which tightens feedback loops between field performance and design updates. Taken together, the material mix will likely remain anchored by titanium for volume compressor applications, with composites growing fastest where temperature, mass, and cooling tradeoffs favor higher-value airfoils supported by approved non-destructive evaluation and robust repair schemes.

By Blade Type: Compressor Blades Lead, But Turbine Blades Accelerate Due To Thermal Demands

Compressor blades held 42.32% of the aircraft engine blades market in 2025, reflecting their high unit volumes across multi-stage cores and the emphasis on weight and efficiency in modern axial designs. Turbine blades are projected to grow at the fastest 7.21% CAGR through 2031 as temperature margins rise and fleets incorporate durability upgrades to address early-life wear in challenging operating conditions. Narrowbody scale drives large, recurring orders for compressor airfoils. At the same time, high-pressure turbine blades command a higher value per unit due to their single-crystal or advanced-alloy content and the repair complexity they entail during MRO cycles. First restoration visits for new-generation engines are clustering in the middle of the decade, intensifying the need for turbine blade replacements and updated designs that improve time-on-wing without compromising performance. OEM upgrade kits already in the field confirm this trend and have been scaled to bring improved high-pressure turbine parts into service as fleets move through planned and unplanned removals.

Fan blades remain a visible area of innovation due to structural size and aerodynamic loading. Yet, their growth trajectory is steadier because inspection and certification maturity for large composite designs still shape replacement policies and service intervals. Engine programs have demonstrated that early-life durability improvements for high-pressure turbine stages are achievable, with some cases showing more than a doubling of time-on-wing, thereby reducing replacement frequency after retrofit cycles are complete. As a result, compressor blades anchor the base of the volume pyramid, turbine blades lead in growth and value intensity, and fan blades advance more gradually as NDE, repair, and certification frameworks for large composite structures continue to train toward broader standardization.

By Engine Type: Turbofan Dominance Reflects Narrowbody Surge And Next-Gen Efficiency

Turbofan engines captured 57.45% of the aircraft engine blades market in 2025 and are expected to grow at a 7.87% CAGR through 2031, reflecting the scale of single-aisle fleets and the entry into service of higher-efficiency widebody platforms. Airline selections in 2025 and 2026 reinforce this path, with recent commitments that keep turbofans at the center of fleet strategies for the rest of the decade. The GE9X adds another layer of demand for advanced materials and inspection schemes, as its architecture incorporates additive CMC elements and enhanced coatings that influence the downstream MRO model and blade repair standards. Turboprop and turboshaft engines continue to meet stable replacement needs for defense and civil rotorcraft fleets, which rounds out the airfoil mix with different repair profiles and lifing methodologies.

Blade demand by engine type is also shaped by accelerated first shop visits on new platforms, which pull forward portions of the replacement curve into 2025-2028 and then redistribute maintenance exposures as fleets stabilize with updated parts. The aircraft engine blades market is therefore set to track turbofan scale most closely. In contrast, niche engines support a broad base of steady activity, which can buffer volatility when one engine family experiences a field issue or an inspection wave. As widebody activity increases with next-generation entries, hot-section airfoils for large turbofans will add to value intensity even as single-aisle fleets continue to dominate volumes.

By Aircraft Type: Commercial Aviation Leads, Military Surges On Defense Spending

Commercial aviation accounted for 65.21% of the aircraft engine blades market in 2025, consistent with passenger traffic recovery and the long order books for single-aisle fleets that require high-throughput blade production to match delivery plans. Military aviation is forecasted to grow at the fastest 7.65% CAGR through 2031, driven by fighter, transport, and rotorcraft programs that prioritize readiness and life extension, which increases both new-production blades and in-service replacements. Within commercial fleets, the A321’s dominance in the A320 family backlog concentrates fan and core blade requirements in thrust classes aligned to that airframe, which pressures suppliers to balance precision manufacturing with scaled capacity. Regional manufacturing remains uneven, with emerging programs showing modest delivery counts in 2025 due to component availability, signaling where upstream constraints still limit throughput. Defense programs added strong momentum in 2025 through record F-35 deliveries, which lifted new production and sustainment pull for high-value turbine airfoils.[3]Lockheed Martin News, “F-35 Breaks Delivery Record in 2025,” Lockheed Martin, lockheedmartin.com

The maintenance profile is also diverging by aircraft type, as commercial operators adopt predictive analytics to extend blade life. In contrast, defense operators face different lifing curves shaped by high-tempo operations, which can shorten replacement cycles. Helicopter and special mission fleets generate steady, program-led demand for turboshaft blades and related hot-section parts, which follow separate certification and sustainment pathways compared to those for civil transport engines. The aircraft engine blades market will remain anchored by commercial volumes. At the same time, defense accounts for a growing share of value due to the material and process intensities in single-crystal and advanced alloy airfoils.

Geography Analysis

North America held the largest share at 33.24% of the aircraft engine blades market in 2025, reflecting the concentration of engine OEMs, deep MRO infrastructure, and strong defense procurement that sustain blade demand across new-production and aftermarket channels. US investments announced in 2025 targeted additional manufacturing capacity and durability technologies to support programs that will require advanced airfoils over long service lives. Strategic metals supply agreements also underpinned the region’s readiness to meet narrowbody and widebody blade needs through the decade. Upstream and midsize suppliers continue to develop capabilities in machining, coating, and inspecting rotating parts, thereby enhancing regional resilience for high-integrity blade production and repair. From a maintenance perspective, predictive analytics are spreading among US operators and MROs, helping extend blade life when data quality and inspection maturity align with engine health-monitoring goals.

Asia-Pacific is the fastest-growing region, with an 8.09% CAGR through 2031, for the aircraft engine blades market, driven by rising fleet counts and long-dated narrowbody order pipelines that pull on both compressor and turbine airfoil capacity. China’s manufacturing ecosystem is expanding but still faces periodic component constraints, underscoring the importance of multi-country supply strategies for scaling blade availability for emergent programs. India’s long-term growth in aircraft count and maintenance capabilities supports multi-year demand for new blades and MRO spares, with partner-driven localization expected to gain momentum as certifications and tooling mature. The region’s path to higher output depends on securing specialty gases and alloy inputs, qualifying inspection technologies, and scaling trained labor to ensure reliable yields on demanding blade geometries. As fleets grow, Asia-Pacific maintenance activity will also shift from interval-based methods to condition-based decisions for high-value airfoils, as data infrastructure and certified inspection tools become more widely available.

Europe continues to advance next-generation blade manufacturing and materials research in support of sustainability and efficiency targets, with new high-rate compressor blade facilities inaugurated in 2025 to support LEAP production. The region’s engine and airframe OEMs are investing in thermal management, coatings, and composite structures for hot sections, which will influence blade mix as programs mature. The Middle East and Africa add a stable stream of high-value widebody and narrowbody engine requirements, and durability technologies developed with regional feedback loops are feeding into design refinements for dust- and sand-ingestion environments. South America maintains a smaller but steady profile in blade demand centered on commercial operations and regional MRO growth, which benefits from global supplier partnerships and standardized maintenance protocols.

Competitive Landscape

The aircraft engine blades market is moderately consolidated, with long-standing engine OEMs determining platform specifications and lifecycle economics that concentrate blade sourcing through qualified suppliers and repair channels. CFM International’s LEAP program remains a central driver of compressor and turbine blade volumes, supported by an extensive in-service base and a significant backlog that extends procurement visibility. Pratt & Whitney’s geared turbofan family and Rolls-Royce’s widebody engines each have distinct blade requirements, lifing models, and inspection demands, which together form a multi-speed aftermarket shaped by varying time-on-wing and upgrade paths. Regulatory directives from the FAA and EASA continue to shape blade replacement intervals and compliance procedures, influencing aftermarket timing and inventory plans across fleets.

Strategic moves in 2025 and 2026 center on engine selections and facility expansions that lock in long-run blade demand and stabilize throughput. American Airlines’ selection of LEAP-1A engines for A321neo orders reinforces the outlook for LEAP blades in the single-aisle market across production and MRO cycles. European blade capacity is being scaled up with high-throughput titanium compressor blade lines inaugurated in Belgium, a response to sustained LEAP production growth that requires consistent, certifiable volumes from European sources. On the widebody side, GE9X advanced durability technologies and additive elements underpin the readiness of airfoils suited to extreme operating parameters and long service intervals on the next generation of twin-aisle platforms.

Specialist blade manufacturers remain critical to the value chain as they scale single-crystal casting, precision machining, coating, and repair capabilities to meet OEM and MRO specifications. Large producers highlighted output gains in 2025 while signaling that process discipline and workforce skills remain core constraints on yield and lead time improvements for high-pressure turbine blades. Digital inspection, AI-enabled borescope tools, and standardized workscopes are spreading across maintenance facilities, raising the bar for blade triage and lifecycle planning. The regulatory environment continues to evolve with specific blade-related directives, and 2025 rulemaking activity affirmed that inspection criteria and replacement limits can change as additional testing refines the risk picture for particular lots or processes.

Aircraft Engine Blades Industry Leaders

Safran SA

General Electric Company

RTX Corporation

MTU Aero Engines AG

Rolls-Royce Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: After receiving a GBP 2 million (USD 2.70 million) grant from the South Yorkshire Mayoral Combined Authority (SYMCA), Rolls-Royce unveiled a GBP 19.3 million (USD 26.10 million) investment in its Advanced Blade Casting Facility (ABCF) located in Rotherham.

- October 2025: Rolls-Royce renewed its agreement with Bharat Forge Ltd. for the manufacturing and supply of fan blades, supporting the production of the Pearl 700 and Pearl 10X engines under precise technical specifications.

- April 2025: GKN Aerospace secured a three-year contract with Boeing to provide specialized fan blade repair services for dual-use C-17 Globemaster engines (PW F117-100 / PW2000).

- March 2025: AAR CORP. signed an exclusive multi-year distribution and license agreement with BELAC LLC, a Chromalloy subsidiary, for PMA high-pressure turbine blades, ensuring guaranteed stock levels of the T1 blade for PW4000 engine platforms.

Global Aircraft Engine Blades Market Report Scope

Aircraft engine blades consist of vanes and valves. These vanes and valves may produce a smooth gas flow by directing and compressing the air inside the engine. A turbine blade, an aerodynamic blade positioned on the rim of a turbine disc with multiple blades, generates a tangential force that rotates a turbine rotor. Both steam turbines and gas turbine engines use these blades. The gas produced by the combustor, at elevated temperature and pressure, is used by the blades to generate energy. The engine's blades are typically its limiting element.

The aircraft engine blades market is segmented by material, blade type, engine type, aircraft type, and geography. By material, the market is segmented into titanium alloys, nickel-based superalloys, composites, and others. By blade type, the market is segmented into compressor blades, turbine blades, and fan blades. By engine type, the market is segmented into piston, turbofan, turboprop, turbojet, and turboshaft. By aircraft type, the market is segmented into commercial aviation, military aviation, and general aviation. The report also covers the market sizes and forecasts for major countries across the regions. For each segment, the market size is provided in terms of value (USD).

| Titanium Alloys |

| Nickel-Based Superalloys |

| Composites |

| Others |

| Compressor Blades |

| Turbine Blades |

| Fan Blades |

| Piston |

| Turbofan |

| Turboprop |

| Turbojet |

| Turboshaft |

| Commercial Aviation | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| Military Aviation | Combat Aircraft |

| Non-combat Aircraft | |

| General Aviation | Business Jets |

| Helicopters | |

| Turboprop Aircraft | |

| Piston Engine Aircraft |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Material | Titanium Alloys | ||

| Nickel-Based Superalloys | |||

| Composites | |||

| Others | |||

| By Blade Type | Compressor Blades | ||

| Turbine Blades | |||

| Fan Blades | |||

| By Engine Type | Piston | ||

| Turbofan | |||

| Turboprop | |||

| Turbojet | |||

| Turboshaft | |||

| By Aircraft Type | Commercial Aviation | Narrowbody Aircraft | |

| Widebody Aircraft | |||

| Regional Jets | |||

| Military Aviation | Combat Aircraft | ||

| Non-combat Aircraft | |||

| General Aviation | Business Jets | ||

| Helicopters | |||

| Turboprop Aircraft | |||

| Piston Engine Aircraft | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the aircraft engine blades market size and expected growth through 2031?

The aircraft engine blades market size was valued at USD 16.11 billion in 2025 and is projected to reach USD 23.84 billion by 2031 at a 6.75% CAGR over 2026-2031.

Which engine type will drive the most blade demand to 2031?

Turbofan platforms lead, with 57.45% share in 2025 and the fastest growth at a 7.87% CAGR as single-aisle fleets expand and widebody entries add higher-value hot-section airfoils.

Which region will grow fastest for aircraft engine blades by 2031?

Asia-Pacific is the fastest-growing region at an 8.09% CAGR as fleet additions and long-dated orders scale blade needs across production and MRO.

What operational factors are increasing aftermarket blade demand in 2026?

Shorter shop visit intervals, early-life durability upgrades, and clustered first restorations are lifting blade replacements and tightening MRO capacity in 2026.

Which material trends are most relevant for hot-section blades?

Composites are gaining where high temperatures drive benefits, supported by certified 3D-printed CMC elements on programs like GE9X, while titanium remains the high-rate choice for compressor blades.

How are regulations shaping blade replacement cycles?

The FAA and EASA directives define inspections and replacement actions for specific blade lots and processes, which can pause deliveries and adjust service intervals during compliance.

Page last updated on: