Helicopter Engines Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 19.64 Billion |

| Market Size (2031) | USD 25.68 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

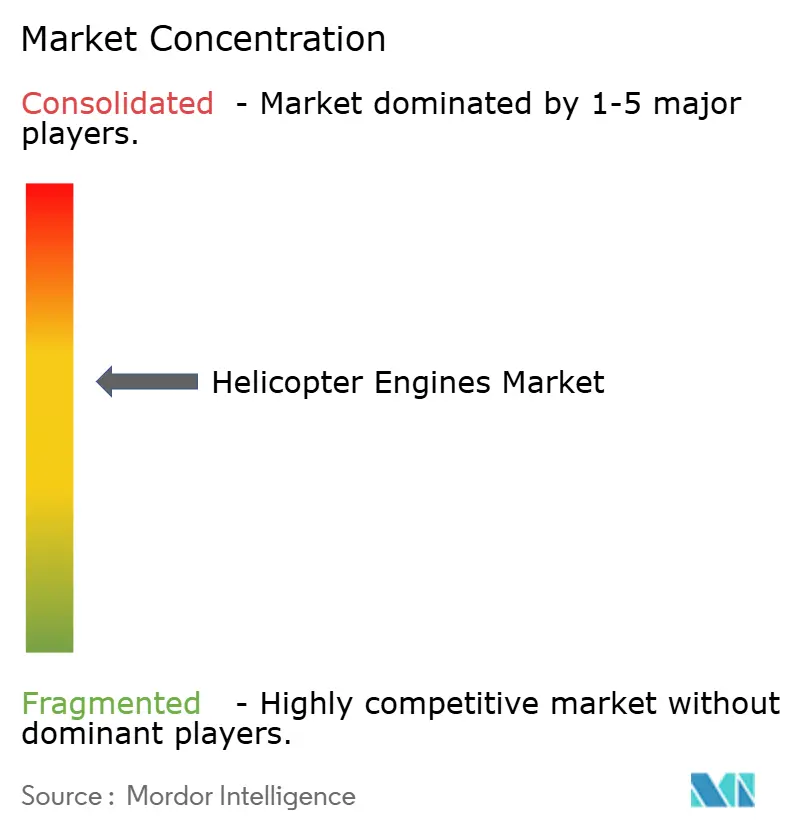

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Helicopter Engines Market Analysis by Mordor Intelligence

The helicopter engines market size is expected to grow from USD 18.58 billion in 2025 to USD 19.64 billion in 2026 and is forecasted to reach USD 25.68 billion by 2031 at a 5.54% CAGR over 2026-2031. This expansion reflects a structural pivot toward predictable, multi-year military modernization programs that dampen the cyclical swings once driven by commercial procurement. Momentum also derives from a synchronized recovery in offshore oil and gas activity, the rapid expansion of helicopter emergency medical services (HEMS) across emerging Asia-Pacific economies, and the increasing adoption of digital health-monitoring systems that extend on-wing time and enhance aftermarket value.[1]Source: Jamie Freed, “US Army Cancels FARA Program, Reallocates $2 Billion,” Reuters, reuters.com Heavy-lift mission profiles that require engines above 2,000 shp are intensifying, while local-content mandates in India, China, and Turkey are fragmenting regional supply bases and nudging indigenous designs into service. Supply-chain resilience remains a key industry watchpoint, with tight forging capacity, escalating nickel-alloy prices, and a global shortage of certified maintenance technicians stretching overhaul turnarounds and elevating lifecycle costs.

Key Report Takeaways

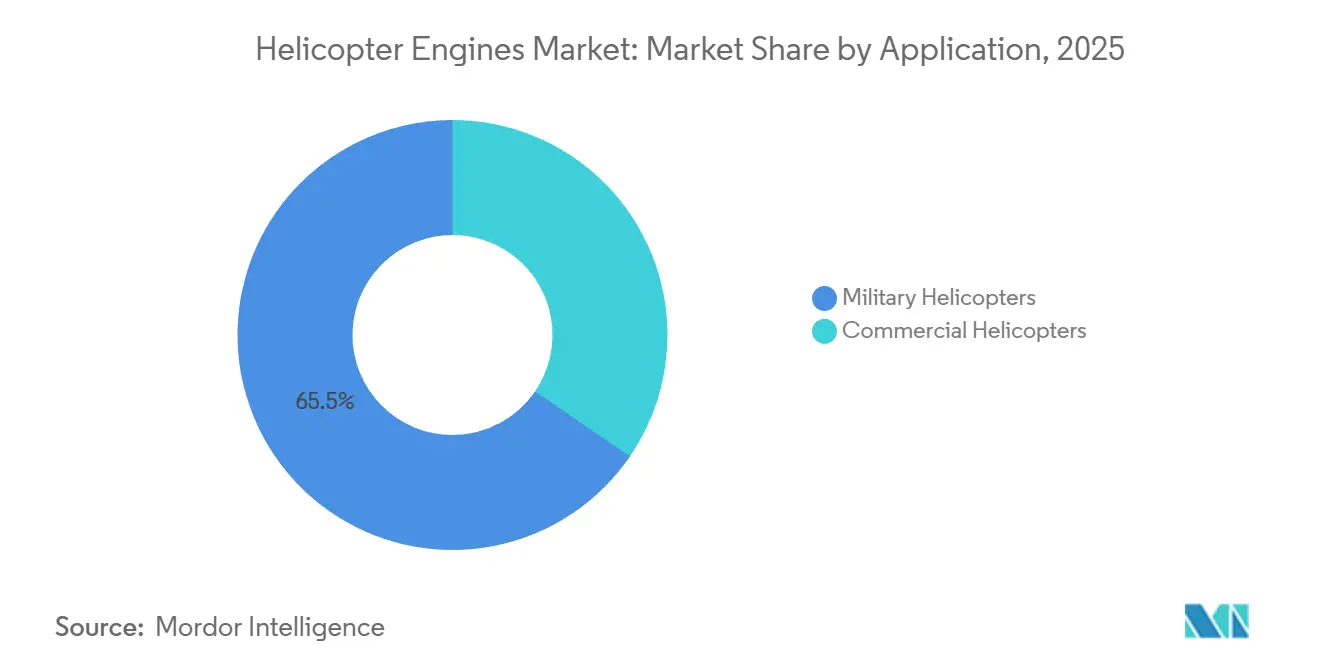

- By application, military helicopters held 65.45% of the 2025 demand. In contrast, commercial platforms are forecast to grow at a 8.25% CAGR through 2031, driven by offshore logistics and the expansion of HEMS fleets in the Asia-Pacific.

- By engine type, turbine units captured 86.71% of the helicopter engines market share in 2025, while turbine demand is forecast to grow at a 7.98% CAGR through 2031 on the back of power-to-weight advantages that have almost eliminated piston alternatives.

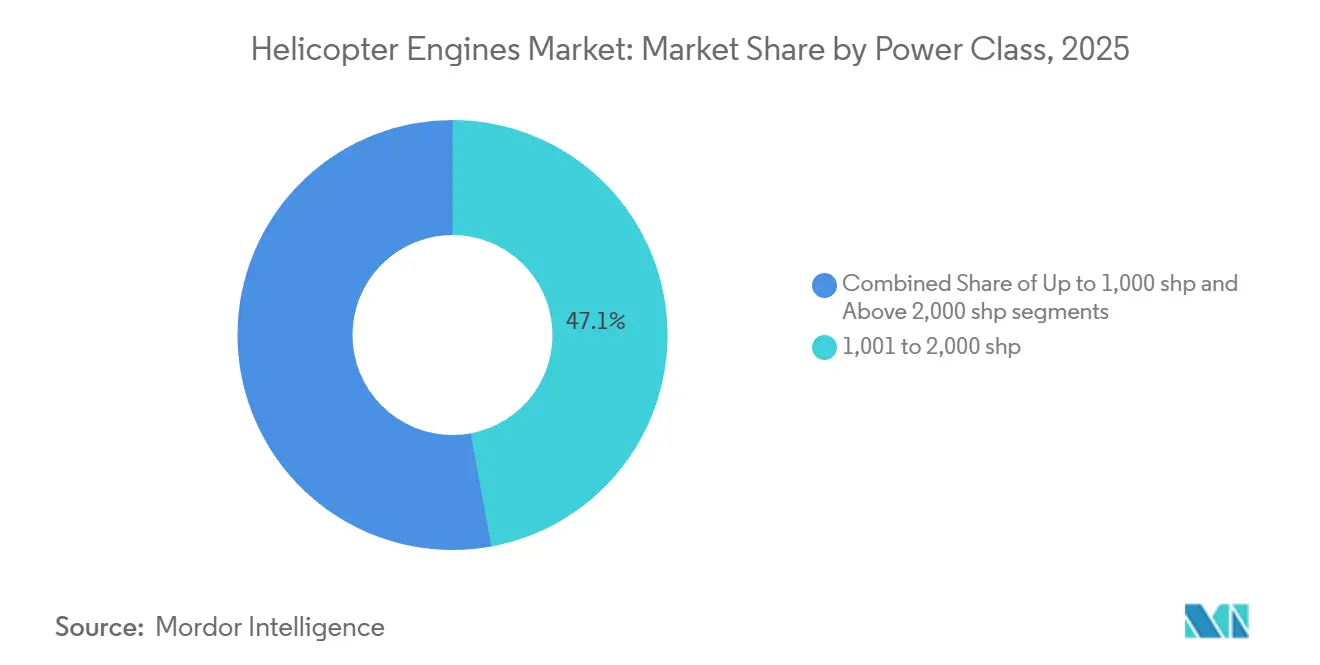

- By power class, engines rated in the 1,001-2,000 shp band held 47.10% of the 2025 market, and engines rated above 2,000 shp are projected to grow at an 8.10% CAGR through 2031.

- By helicopter type, medium helicopters are expected to remain the largest segment, accounting for 43.65% in 2025, due to their multi-role versatility. Heavy platforms are forecast to grow at an 8.36% CAGR through 2031.

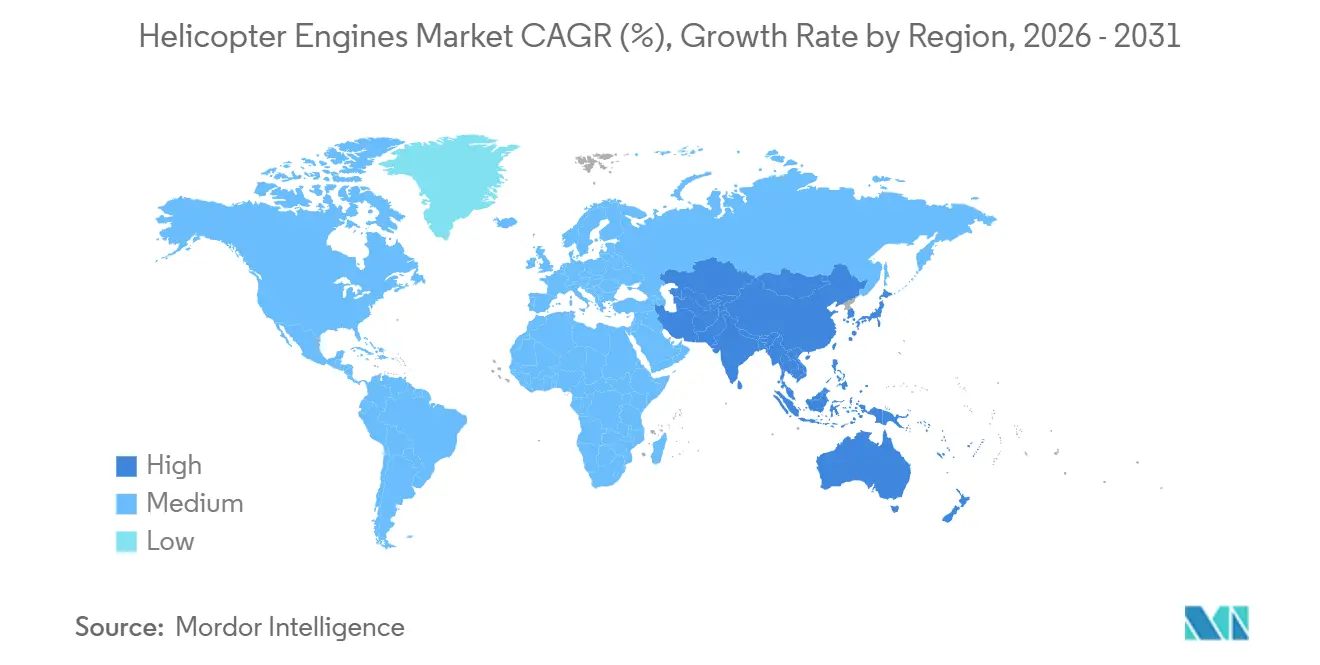

- By geography, North America accounted for 34.50% of the helicopter engines market in 2025; the Asia-Pacific is forecast to grow at a 7.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Helicopter Engines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet expansion and military modernization momentum | +1.8% | North America, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Oil-and-gas offshore recovery lifting heavy-lift engine demand | +1.2% | Gulf of Mexico, Brazil, Middle East, Africa | Short term (≤ 2 years) |

| EMS/SAR helicopter proliferation in emerging economies | +0.9% | India, China, Southeast Asia, Middle East, Africa | Medium term (2-4 years) |

| Predictive maintenance adoption boosting engine-aftermarket value | +0.7% | Global, early uptake in North America and Europe | Long term (≥ 4 years) |

| Hybrid-electric turboshaft R&D linked to Future Vertical Lift (FVL) | +0.5% | United States, Europe | Long term (≥ 4 years) |

| Local content mandates spurring indigenous engine programs | +0.6% | India, China, Turkey | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fleet Expansion and Military-Modernization Momentum

Fleet expansion and military modernization momentum rest on predictable multi-year defense budgets that replace sporadic buys with programmatic procurements covering entire fleets. The June 2024 USD 4.7 billion Apache award and September 2024 USD 433 million Black Hawk order guarantee GE T700 and future T901 production lines, sustaining skilled labor, tooling, and supplier networks for another decade. Australia's USD 2.80 billion Black Hawk acquisition, Japan's UH-2 induction, and South Korea's KUH-1 Surion production illustrate the Asia-Pacific region's preference for proven powerplants over experimental architectures. India's Light Utility Helicopter (LUH) and Light Combat Helicopter (LCH), powered by HAL's Shakti derivative, are expected to deepen the region's turbine demand.

Oil-and-Gas Offshore Recovery Lifting Heavy-Lift Engine Demand

Reviving offshore exploration in the Gulf of Mexico, Brazil’s pre-salt cluster, and Middle Eastern waters has reignited demand for super-medium and heavy-lift helicopters that can haul crews and cargo over 200-nautical-mile sectors. When gearbox shortages grounded 27 Sikorsky S-92s in 2024, operators scrambled for substitutes equipped with 2,000 shp Safran Aneto engines, such as the Leonardo AW189 and Airbus H175, thereby tightening availability and boosting lease rates. BOEM reports indicate that operators are now favoring larger cabins to reduce seat-mile costs, while Saudi Aramco and ADNOC have expanded their AW189 fleets for platform shuttle missions. Higher utilization squeezes maintenance capacity, raising aftermarket revenue per engine visit.

EMS/SAR Helicopter Proliferation in Emerging Economies

Government-funded emergency medical services and search-and-rescue (SAR) initiatives are proliferating across the Asia-Pacific region, reshaping demand toward light and medium turboshaft helicopters with quick-start capabilities and high hover performance. India’s 2024 pilot HEMS project at AIIMS Rishikesh employed Bell 407s and could scale to 600-700 aircraft once insurers, regulators, and state health budgets align. Chinese planners identify a 700-unit civil fleet gap to meet regional response benchmarks, spurring municipal subsidies for Airbus H125 and AC352 acquisitions. South Korea’s expanded doctor-helicopter program and Hong Kong’s Government Flying Service fleet extend the trend. ICAO Annex 16 noise caps steer buyers toward quieter FADEC-equipped engines.

Predictive-Maintenance Adoption Boosting Engine-Aftermarket Value

Digitally enabled predictive maintenance is transforming helicopter engine economics by shifting overhaul decisions from rigid calendars to real-time condition data. Pratt & Whitney’s eFAST suite, introduced in February 2024, processes gigabytes of flight telemetry, cutting troubleshooting labor by 30% and identifying anomalies before components fail. Rolls-Royce’s IntelligentEngine platform builds digital twins that forecast wear patterns, while GE’s T901 FADEC streams vibration and combustion metrics continuously. Offshore transporters and HEMS operators, where every grounded hour erodes revenue, lead uptake and pay subscription fees that lift OEM lifetime margins. Analytics also inform inventory stocking, thereby reducing costly expedited shipments of parts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating R&D and certification costs for new engines | -0.8% | North America, Europe | Long term (≥ 4 years) |

| Procurement volatility from defense and oil-price cycles | -0.9% | Middle East, South America | Short term (≤ 2 years) |

| Global MRO-talent shortage extending shop-visit TAT | -0.6% | North America, Europe | Medium term (2-4 years) |

| Urban noise limits accelerating shift to eVTOL platforms | -0.4% | North America, Europe, Asia-Pacific urban hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating R&D and Certification Costs for New Engines

The financial barrier to entry for modern turboshaft programs has soared, deterring challengers and concentrating innovation among established conglomerates. GE’s T901 required more than USD 1 billion over ten years, including dozens of endurance rigs and high-altitude icing campaigns, before its first production delivery in July 2024. FAA and EASA Part 33 protocols require thousands of hours of cyclic abuse, and any design tweak restarts the certification process, adding quarters to schedules.[2]Source: Federal Aviation Administration, “Part 33 Certification Standards,” faa.gov Material inflation for nickel-based superalloys and single-crystal turbine blades magnifies budgets, steering OEMs toward incremental block upgrades rather than riskier clean-sheet designs that may never clear regulatory hurdles.

Procurement Volatility from Defense and Oil-Price Cycles

Helicopter engine producers navigate an order landscape that oscillates with geopolitical tensions and crude oil benchmarks, complicating capacity planning. The US Army’s May 2024 cancellation of the Future Attack Reconnaissance Aircraft (FARA) stripped suppliers of USD 2 billion in expected turboshaft volume, forcing redeployment of engineers toward upgrade kits and uncrewed propulsion. Petrobras budget tightening the same year postponed heavy-lift renewals for Brazilian pre-salt operations, while Gulf monarchies routinely defer procurement when barrel prices soften. Commercial offshore fleets mirror volatility; rig counts can swing 30% annually, creating feast-or-famine shop-visit cycles that squeeze working capital and destabilize staffing rosters across global MRO networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Military Dominance Anchors Near-Term Growth

Military helicopter programs delivered 65.45% of the 2025 engine demand, shielding overall revenue from the more cyclical commercial cycle. Multi-year US Army production contracts for Apaches, Black Hawks, and Chinooks anchor GE’s T700 and forthcoming T901 lines through the 2030s, guaranteeing stable pull for critical castings, forgings, and digital-control components. Australia’s 40-unit Black Hawk order, together with steady procurement of Japan’s UH-2 and South Korea’s KUH-1 Surion, keeps derivative T700 variants in continuous flow. Asia-Pacific momentum is reinforced by India’s LCH and LUH programs, as well as China’s serial production of the Z-20, establishing a robust, regionally diversified military backlog.

Although defense budgets underwrite today’s volumes, commercial demand is projected to compound at an annual rate of 8.25%, gradually increasing its contribution to the helicopter engines market size by USD 3.5 billion between 2026 and 2031. Certification paths differ sharply: military engines undergo ballistic-tolerance, sand-ingestion, and extreme-climate tests that exceed the FAA and EASA Part 33 civil baselines. Fleet managers, therefore, tend to gravitate toward standard engine families that span troop transport, attack, and training aircraft, thereby reducing parts inventories and simplifying field-level maintenance. In parallel, commercial operators returning to offshore logistics and HEMS missions are unlocking deferred purchases; however, military fleets will still dominate the installed-base value through mid-decade.

By Engine Type: Turbines Cement Market Dominance

Turbines controlled 86.71% of 2025 shipments and will grow 7.98% per year, propelled by superior power-to-weight ratios, FADEC-enabled reliability, and hot-and-high performance. GE’s T700 family, the backbone of global utility fleets, surpasses 20,000 deliveries, while Safran’s Arriel and Arrius series exceed 35,000 installed units across light civil missions. Rolls-Royce’s M250 and RTX’s PT6C/PT6T span mid-power classes, offering modular hot-section upgrades that extend time-on-wing. OEMs embed predictive-maintenance gateways into new models, enabling real-time surveillance of vibration and turbine gas temperature, which lengthens inspection cycles and strengthens aftermarket lock-in across both civil and military operators.

Piston engines now persist mainly in Robinson R22/R44 trainers, kit helicopters, and specialized experimental craft, which face lighter regulatory scrutiny. Rising avgas prices, higher scheduled-maintenance labor, and tightening emissions mandates reduce their economic appeal versus turboshaft alternatives that burn widely available jet-A and require fewer top-end overhauls. As regulators press carbon intensity targets, piston market share is forecast to contract below 10% by 2031. GE’s next-generation 3,000 shp T901, promising 25% fuel savings and 50% added power over legacy T700 cores, typifies turbine innovation that further widens the performance gap and cements long-run turbine primacy.

By Power Class: Heavy-Lift Segment Accelerates

Engines in the 1,001–2,000 shp band accounted for 47.10% of 2025 deliveries, powering stalwarts such as the UH-60 Black Hawk, AW139, and H225. These units strike the optimal balance between payload, range, and acquisition cost for multi-role military and commercial tasks. Core designs such as GE's 1,900 shp T700-701D and Safran's 2,100 shp Makila 2A dominate this tier, leveraging mature supply chains and ubiquitous overhaul capacity. Their entrenched status ensures steady overhaul volumes, making the segment a dependable profit center for both independent MRO providers and OEM in-house service divisions.

Demand is now pivoting toward engines exceeding 2,000 shp, which will log an 8.10% CAGR through 2031 as offshore and defense operators seek fewer sorties and longer unrefueled legs. Safran's dual-Aneto-powered AW189 and GE's 7,500 shp GE38 on the CH-53K King Stallion exemplify this migration, delivering an extended range and a 27,000-pound external load capacity. Super-medium commercial users report double-digit seat-mile cost reductions when upgrading from legacy medium types, accelerating retirements of older airframes. The US Marine Corps' commitment to 200 CH-53Ks alone secures multi-decade visibility in heavy-engine production, adding USD 2.1 billion to the above 2,000 shp helicopter engines market size by 2031.

By Helicopter Type: Medium Platforms Lead, Heavy Units Gain

Medium helicopters captured 43.65% of 2025 demand because their 10-ton gross weight envelopes and 600–800 km ranges straddle utility, offshore, and HEMS missions. Platforms such as the AW139, H175, and UH-60 achieve favorable dispatch reliability, cabin flexibility, and acquisition economics, sustaining their popularity across both civil and defense portfolios. OEMs continually enhance these airframes with glass cockpits, advanced autopilots, and incremental engine upgrades that reduce specific fuel consumption. Consequently, medium-class overhaul and spare-parts ecosystems remain the broadest, enabling pooling arrangements that lower operator inventory requirements and reinforce fleet-planning preference for this category.

Heavy helicopters, including the CH-47 Chinook and CH-53K, are expected to grow at an annual rate of 8.36% as militaries and offshore majors pursue single-lift solutions for transporting outsized cargo, inserting troops, and conducting deep-water missions of up to 300 kilometers. These airframes accommodate three-engine or high-output twin-engine configurations, mitigating the risk of one-engine inoperability while carrying 7-ton payloads. Nations facing disaster-relief and expeditionary logistics scenarios increasingly justify their higher unit costs by counting avoided refueling stops and reduced sortie numbers. Conversely, light helicopters remain vital for ab-initio training and law enforcement, but now confront eVTOL entrants that match short-range tasks with lower acoustic footprints and simplified electric power architectures.

Geography Analysis

North America maintained a 34.50% share in 2025, anchored by the US Army's multibillion-dollar remanufacture and new-build programs for Apaches, Black Hawks, and Chinooks, which guarantee T700 and upcoming T901 production through at least 2035. Gulf of Mexico offshore recovery further lifts super-medium demand, with operators adopting Aneto-powered AW189 and H175 models to optimize 200-nautical-mile crew transfers. North American fleets are also early adopters of predictive maintenance; the widespread installation of eFAST and IntelligentEngine portals reduces unscheduled removals and expands high-margin OEM service contracts, reinforcing the region's role as a bellwether for digital aftermarket monetization.

Posting a 7.80% CAGR, the Asia-Pacific region combines large-scale indigenous programs with rapidly growing civil applications. China's WZ-16-powered Z-20 utility line is ramping up its monthly outputs, while India's HAL Shakti engine underpins the LUH and LCH series, with plans to reach several hundred deliveries by 2030. Australia's adoption of Black Hawks and Japan's UH-2 procurement sustain Western engine penetration, balancing regional self-reliance drives. Nascent HEMS fleets in Southeast Asia, along with growing offshore activity in Indonesia and Malaysia, widen civil opportunities. Converging ICAO-aligned noise and emissions rules compel local OEMs to enhance efficiency, placing an additional spotlight on digitally controlled, lower-specific-fuel turbines.

Europe tracks the global average growth rate, propelled by Airbus Helicopters' 361 deliveries in 2024 and expanded NATO budgets that prioritize multi-role capability.[3]Source: Airbus Helicopters, “2024 Annual Report,” airbus.com North Sea energy firms are switching from legacy mediums to H175 and AW189 super-mediums to contain seat-mile costs in harsher, longer-distance environments. EASA continues to tighten acoustic and emissions limits, accelerating the uptake of FADEC-equipped, quieter engines. Indigenous propulsion development remains modest; most European nations rely on Safran Makila, Rolls-Royce M250, or GE joint-venture units. However, collaborative R&D under Clean Sky is examining hybrid-electric demonstrators that could inform longer-term fleet refresh strategies.

Regulatory Landscape

Helicopter engines are certified and maintained in continued airworthiness primarily under FAA 14 CFR Part 33 and EASA CS-E, with type-certification and post-certification changes managed through EASA Part 21 processes (and equivalent FAA oversight). These frameworks cover core safety and performance demonstrations for turboshafts, including endurance, vibration, ingestion tolerance, fuel and control-system integrity, and documentation for instructions for continued airworthiness, which in turn affects both development cost and the cadence of block upgrades for in-service fleets.

Environmental compliance is tightening alongside airworthiness requirements through ICAO Annex 16-aligned rules. In March 2026, EASA published NPA 2026-02 (A) proposing updates to environmental protection requirements to align with ICAO Annex 16 amendments, with new SARPs referenced as becoming applicable from 1 January 2027. This is increasing compliance focus on engine emissions and non-volatile particulate matter measurement and reporting, which reinforces OEM investment in FADEC optimization, combustor refinements, and test capability to meet evolving certification and in-service conformity expectations.

Value Chain Analysis

The helicopter engine value chain begins with raw materials and precision manufacturing inputs (nickel-based superalloys, forgings/castings, blades/vanes, bearings, and electronic engine controls), then moves through core module production, final assembly, and certification, before flowing into aftermarket-heavy sustainment (spares, repair development, overhauls, field support, and digital health monitoring). OEMs such as Safran, GE Aerospace, Rolls-Royce, and Pratt & Whitney Canada set design authority, while tier suppliers provide compressor and turbine hardware, accessory gearboxes, and FADEC and sensor ecosystems; aircraft OEM integration and operator acceptance testing complete the path into service.

Recent activity points to modular industrial partnering and regionalized service capacity as value-chain levers. The June 2025 ENGHE development accord among Safran Helicopter Engines, MTU Aero Engines, and Avio Aero reflects a modular workshare approach for next-generation military propulsion. Downstream support also expanded in April 2026: Safran inaugurated a 3,000-square-meter MRO facility in Norderstedt, Germany (covering Arrius, Arriel, and RTM322), and Pratt & Whitney Canada launched PT6C-67C MRO services in Singapore with a modular test cell to support Asia-Pacific operators. The chain remains sensitive to airworthiness actions that change shop loads and parts flows, including Transport Canada issuing an emergency directive in June 2026 requiring repetitive inspections on PW210A and PW201S turboshaft turbine exhaust frames due to crack-risk concerns.

Competitive Landscape

The helicopter engines market is semi-consolidated, marked by the presence of prominent players such as Safran, GE Aerospace, Rolls-Royce, and RTX, which hold a majority share of certified helicopter turbines. This reflects decades of accumulated flight hours, established overhaul networks, and proprietary digital health ecosystems. Safran’s portfolio spans 650-2,500 shp classes, GE’s T700/T901 lines lock in US military annuities, Rolls-Royce’s M250 dominates civil light segments, and Pratt & Whitney Canada’s PT6C/PT6T fills the medium gap. High entry costs and rigorous FAA/EASA compliance perpetuate barriers, maintaining elevated market concentration. Nevertheless, local-content mandates in Asia and policy-backed innovation grants create beachheads for regional aspirants seeking to dilute incumbent dominance.

The competitive battleground is shifting from pure thrust metrics to lifecycle-service economics. Pratt & Whitney’s eFAST and Rolls-Royce’s IntelligentEngine platforms stream aircraft-generated data into cloud analytics that predict part-life consumption and schedule maintenance windows, reducing avoidable groundings by up to 30%. GE embeds similar telematics in the T901’s FADEC, promising tighter parameter monitoring and faster root-cause analysis. Subscription-based dashboards, parts-availability algorithms, and pay-by-the-hour coverage deepen customer stickiness and reroute profit pools from initial hardware margins to recurring digital services, altering the way OEMs structure long-term performance-based logistics agreements with civil and military operators.

Emerging rivals HAL, AECC, and TEI leverage sovereign procurement rules, technology-transfer clauses, and soft financing to win home-market tenders; however, their export credibility is constrained by limited FAA or EASA reciprocity and perceived performance deltas. Venture-backed disruptors such as Joby and Archer concentrate on eVTOL niches, where battery energy density and certification pathways still postpone mass adoption beyond short-range urban corridors. Consequently, mergers among incumbents remain scarce; antitrust regulators view additional consolidation as a threat to already high market concentration. Most strategic investments, therefore, target hybrid-electric R&D, additive-manufactured spares, and supply-chain resilience rather than outright acquisitions.

Helicopter Engines Industry Leaders

Safran SA

RTX Corporation

Honeywell International Inc.

General Electric Company

Rolls-Royce Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Aftermarket capacity and turnaround commitments create a visible opportunity as utilization rises across offshore, HEMS, and military training fleets and as talent constraints extend shop-visit cycles. The March 2026 selection of StandardAero by Robinson Helicopter Company as the preferred MRO provider for Rolls-Royce RR300 engines powering the R66, with commitments around capacity and turnaround across North America and the UK, indicates operator demand for service-level certainty. It also opens room for expanded test-cell throughput, parts pooling, and digital troubleshooting services that reduce time-on-ground.

Defense-funded propulsion technology programs and engine-health connectivity upgrades are also broadening addressable spend beyond traditional hardware sales. In June 2026, the European Defence Fund awarded EUR 25 million to the SHARP project led by Safran, MTU, and Avio Aero to mature scalable technologies for the European Next Generation Helicopter Engine (ENGHE), strengthening the pipeline for European sovereign military turboshaft architectures and associated industrialization. At the same time, OEM efforts such as Safran Helicopter Engines collaboration with SKYTRAC (March 2026) to integrate flight-data connectivity for helicopter engines support wider use of predictive maintenance subscriptions and condition-based maintenance, supporting analytics-enabled services and retrofit kits across mixed civil-military fleets.

Recent Industry Developments

- July 2026: GE Aerospace announced the selection of CT7-2E1 engines for Leonardo AW149 helicopters under the UK New Medium Helicopter program. The platform selection reinforces the CT7/T700-derived engine family footprint in European defense fleets and supports multi-year demand for production spares and long-term sustainment services.

- June 2026: Safran Helicopter Engines, MTU Aero Engines, and Avio Aero welcomed EU backing for the SHARP project under the European Defence Fund, with EUR 25 million allocated to develop technologies for the European Next Generation Helicopter Engine (ENGHE). The funding advances a European sovereign engine technology base and pulls forward R&D work on scalable architectures tied to future military rotorcraft requirements.

- April 2024: The UK Ministry of Defence signed a GBP 122 million contract for six Airbus H145M helicopters powered by dual Arriel 2E turboshaft engines with FADEC. The procurement adds near-term engine deliveries and establishes a downstream stream of spares and overhaul demand tied to operational deployments and training cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue generated from helicopter propulsion engines sold for rotary wing aircraft across civil, commercial, and military use, including piston and turbine (turboshaft) engine categories. All values are expressed in USD and reflect the engine market linked to helicopter production and active fleet replacement needs.

Scope exclusions: We exclude complete helicopter airframes, standalone avionics and rotor systems, and general MRO services that are not directly tied to an engine sale, upgrade, or an engine-specific overhaul event.

Segmentation Overview

- By Application

- Commercial Helicopters

- Military Helicopters

- By Engine Type

- Piston Engines

- Turbine Engines

- By Power Class

- Up to 1,000 shp

- 1,001 to 2,000 shp

- Above 2,000 shp

- By Helicopter Type

- Light Helicopters

- Medium Helicopters

- Heavy Helicopters

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand pool and the supply capacity, so the market is not built only from a single data series. We rely on public sources such as civil aviation authorities and registries, defense budget documents, customs and trade statistics, and trade associations that track rotorcraft deliveries and fleet activity. We also use technical publications and peer reviewed papers to understand engine power classes, typical replacement cycles, and technology shifts that influence pricing.

To convert activity signals into dollars, we review company annual reports, investor presentations, and press releases for references to engine programs, production ramps, and aftermarket commentary. Where coverage is fragmented, we use paid subscription datasets for company financials and a patent database to cross-check ownership of key engine families and the pace of platform upgrades. These desk sources are illustrative only, and additional public and paid references are used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to validate what desk sources cannot fully show, mainly the split between OEM deliveries and aftermarket demand, and the practical price movement by power class. We interview engine OEM and supplier side experts, helicopter operators, and maintenance stakeholders across APAC, EMEA, and the Americas to make sure timing assumptions for procurement and overhaul reflect real operations.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | APAC: 44% |

| Mid tier: 43% | Functional/Unit leaders: 27% | EMEA: 37% |

| Smaller Players: 19% | Managers: 57% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built from a top-down structure where helicopter production, the active fleet by class, and engine fit rates are used to reconstruct the yearly engine demand pool by region. Once the demand pool is created, it is translated into value using typical engine counts per aircraft, the power-class mix, and an average selling price curve that reflects configuration differences, for example light versus heavy helicopters and the share of turbine engines.

We then corroborate totals with selective bottom-up checks, such as sampled program level volumes, channel discussions on overhaul cadence, and a sanity check on revenue intensity versus known engine family footprints. When public data is uneven, gaps are handled using conservative penetration ranges from primary inputs, then retested against fleet utilization and delivery patterns.

Forecasting uses scenario analysis supported by trend lines in defense modernization schedules, civil fleet replacement timing, and expected delivery backlogs. The highest impact inputs include helicopter deliveries, average engine price movement by power band, overhaul intervals linked to flight hours, and region level procurement timing. These are refreshed during analyst reviews before finalizing the curve.

Data Validation & Update Cycle

Outputs are validated through cross-checks against independent signals such as delivery counts, fleet additions, and visible procurement events, and then variances are investigated before sign-off. If a segment moves outside expected bounds, the assumptions are revised and experts are re-contacted to confirm whether the shift is real or driven by timing, currency, or scope treatment.

A multi-step review is followed to keep calculation logic, unit conversions, and year mapping consistent across regions and categories. Reports are refreshed annually, with interim updates when material events occur, followed by a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Helicopter Engines Market Size Measured Against Other Published Estimates

Published market numbers for helicopter engines can differ widely because publishers may choose different base years, treat OEM and aftermarket revenue differently, and apply different pricing assumptions across power classes. Currency timing also matters since exchange rate updates and inflation adjustments can change the USD value even when unit volumes are stable.

The spread usually comes from repeat drivers, including whether overhauls are counted as full engine revenue, how fast average selling prices step up, and whether military retrofit programs are recognized at contract award or at delivery. By refreshing exchange rates and ASP logic in the same update window used for the 2026 value, and rechecking it against delivery and fleet signals, Mordor Intelligence reduces timing noise that can inflate or compress the market in a given year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.64 B (2026) | |

| Industry Publisher A | USD 20.04 B (2024) | Uses an earlier base year and presents a longer-range outlook, and the scope can bundle OEM and aftermarket differently, which shifts the market value even before forecasting assumptions are applied. |

| Global Publisher B | USD 24.14 B (2023) | The base year and forecast window do not fully align with other publications, and the model appears to apply broader segment labels, which can pull in adjacent revenue items and raise the stated total. |

Looking at the three figures together, most of the gap is explained by year selection and how aftermarket and pricing are treated, not by a sudden change in real engine demand. Our approach keeps the number traceable to visible volume drivers and a clear price logic, which makes the estimate easier to reproduce and update as new delivery and fleet data becomes available.

Key Questions Answered in the Report

What is the projected value of the helicopter engine market in 2031?

The helicopter engine market is forecast to reach USD 25.68 billion by 2031.

Which region is expanding fastest for helicopter engines?

Asia-Pacific leads growth with a 7.80% CAGR through 2031, driven by indigenous programs and expanding HEMS fleets.

How dominant are turbine engines compared with piston types?

Turbines controlled 86.71% of 2025 demand and will expand further as power-to-weight and digital-control advantages widen.

Why are heavy-lift engines gaining share?

Offshore logistics and military lift missions demand higher payload and range, driving an 8.10% CAGR for engines above 2,000 shaft horsepower.

How are OEMs increasing aftermarket revenue?

Predictive-maintenance platforms such as eFAST and IntelligentEngine extend on-wing time and enable subscription analytics, boosting service income.

What factors threaten sub-1,000 shaft horsepower demand?

Urban noise limits and the rise of eVTOL aircraft are diverting some short-haul missions away from traditional light helicopters.

Page last updated on: