EVTOL Aircraft Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

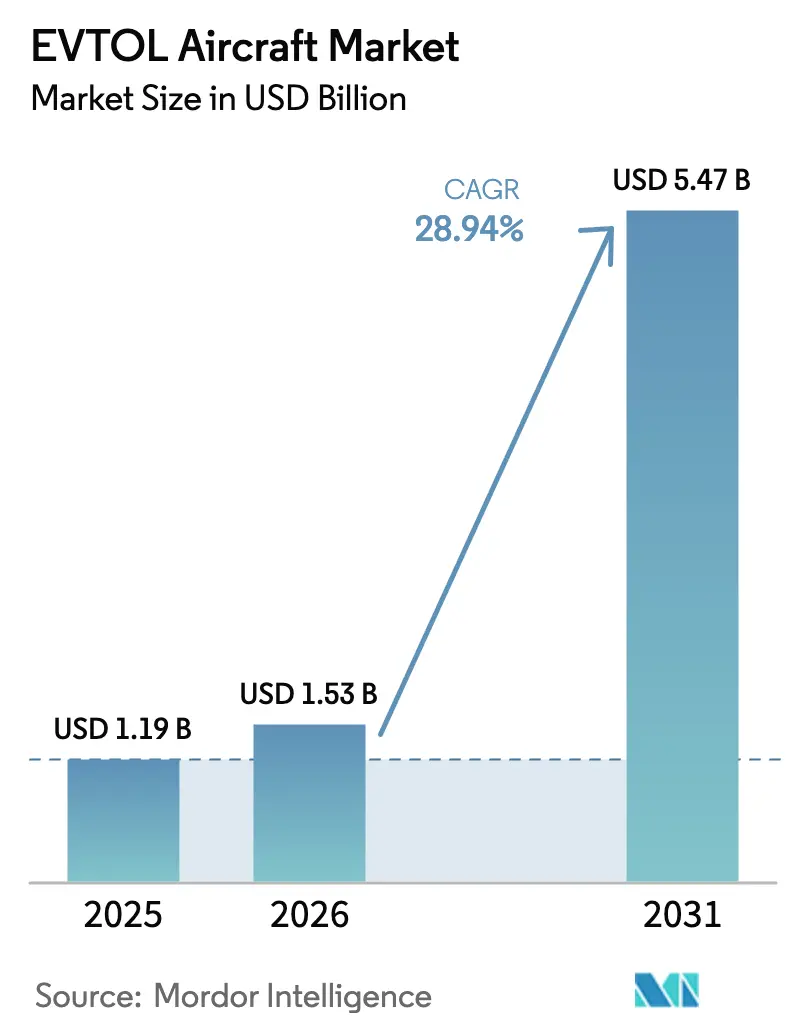

| Market Size (2026) | USD 1.53 Billion |

| Market Size (2031) | USD 5.47 Billion |

| Growth Rate (2026 - 2031) | 28.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EVTOL Aircraft Market Analysis by Mordor Intelligence

The eVTOL aircraft market size is expected to grow from USD 1.19 billion in 2025 to USD 1.53 billion in 2026 and is forecast to reach USD 5.47 billion by 2031 at 28.94% CAGR over 2026-2031. This expansion is propelled by clear certification pathways, rapidly improving battery energy density, and the economic cost of airport congestion pushing cities to adopt advanced air-mobility solutions. Manufacturers now have predictable rules under the FAA’s powered-lift framework and EASA’s Special Condition for VTOL aircraft, allowing parallel certification programs and faster commercialization. Meanwhile, battery prototypes surpassing 500 Wh/kg have removed one of the last technical barriers to longer-range operations. Operators in North America, the Middle East, and parts of Asia have responded by committing to fleet purchases and vertiport construction, while corporate net-zero mandates are creating a ready customer base. Nonetheless, supply-chain resilience for lithium and the high capital cost of vertiports remain material headwinds.

Key Report Takeaways

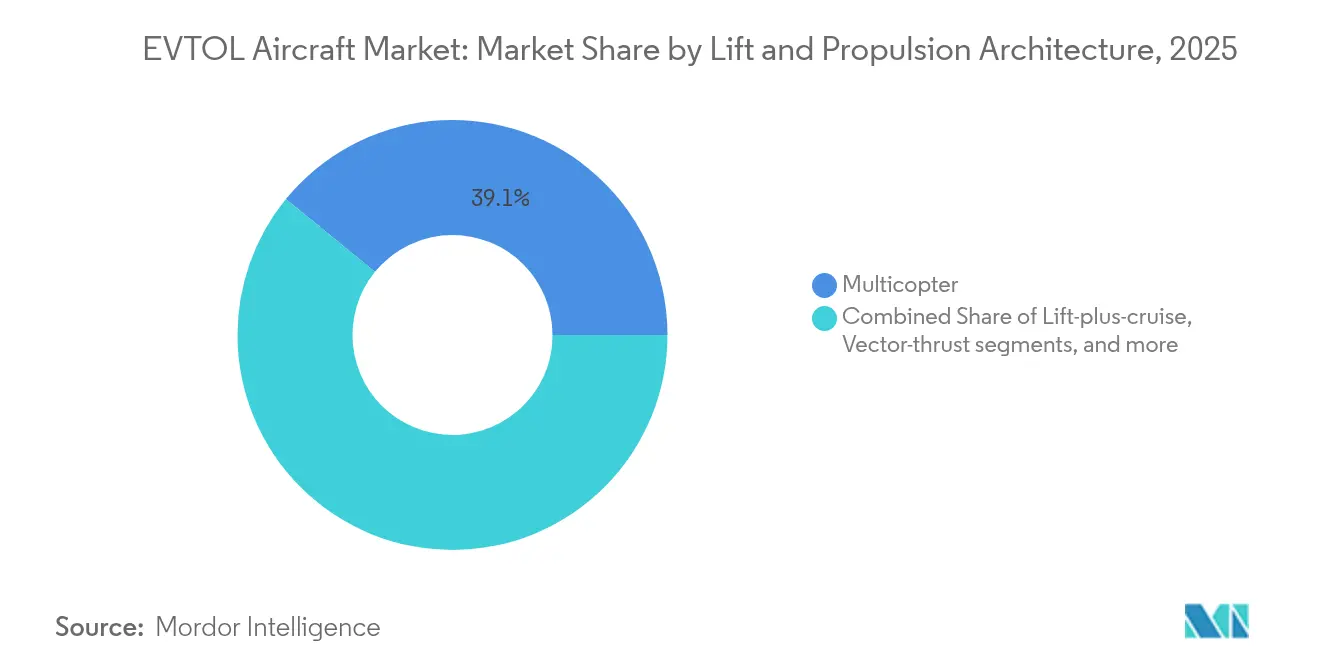

- By lift and propulsion architecture, multicopter designs led with 39.11% of the eVTOL aircraft market share in 2025, while lift-plus-cruise systems are projected to grow at a 34.10% CAGR to 2031.

- By range, aircraft certified for less than 50 km captured 48.62% of the eVTOL aircraft market size in 2025; greater than 150 km platforms are forecasted to expand at a 29.95% CAGR through 2031.

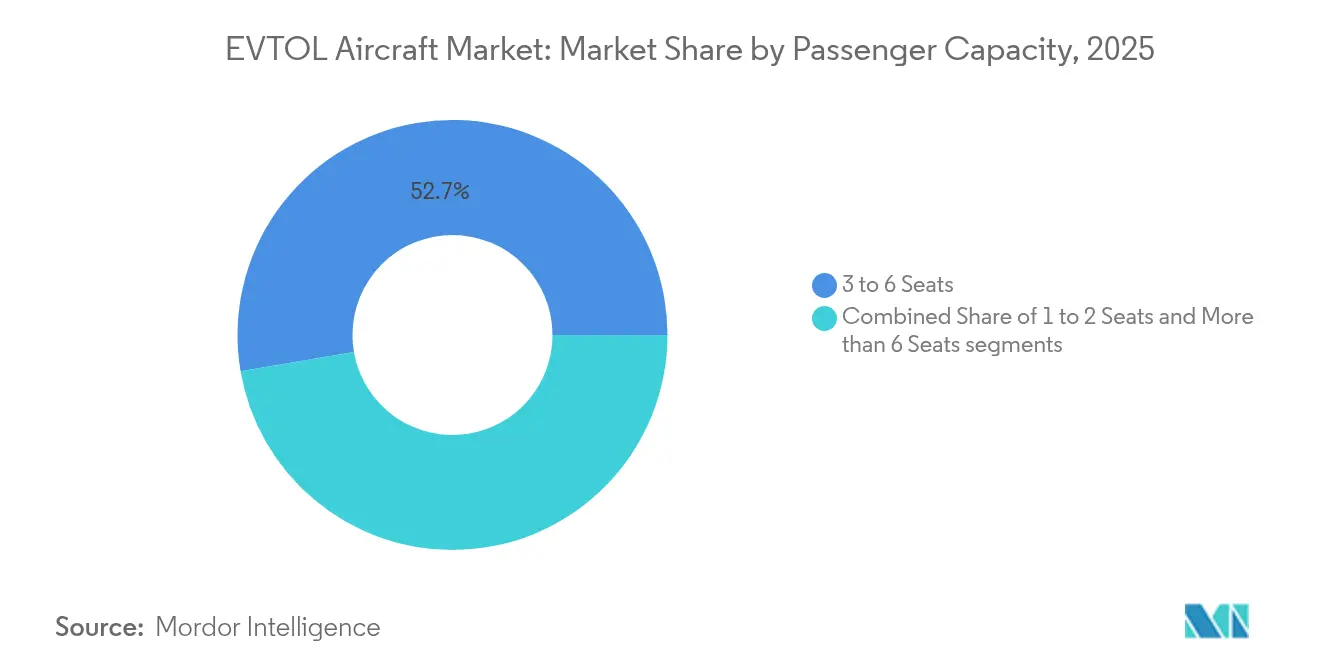

- By passenger capacity, 3- to 6-seat models accounted for a 52.70% share of the eVTOL aircraft market in 2025 and will remain the most commercially attractive segment.

- By application, urban air taxi services held 63.60% revenue share in 2025; medical evacuation is advancing at a 33.70% CAGR to 2031.

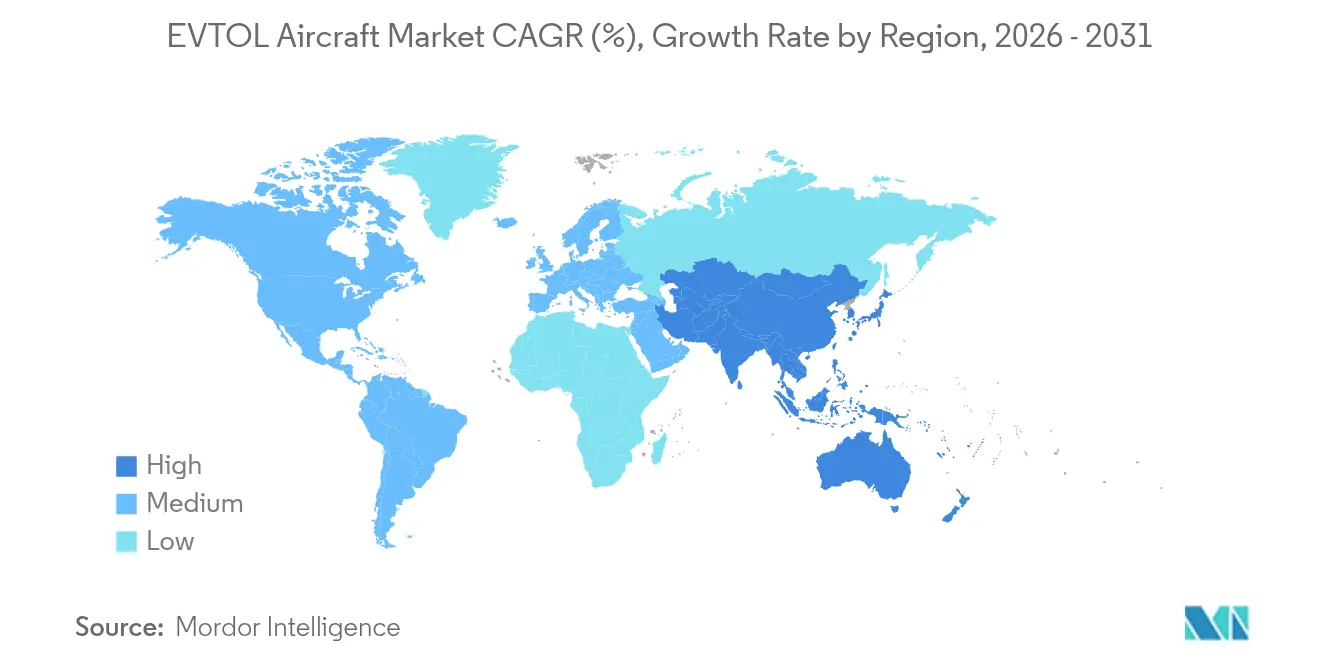

- By geography, North America commanded 41.20% of 2025 revenue, whereas Asia-Pacific was the fastest-growing region, with a 28.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global EVTOL Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory certification pathways becoming clearer (FAA, EASA) | +8.5% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Battery‐energy density breakthroughs hitting 450 Wh/kg lab level | +7.2% | Global, manufacturing center in APAC | Long term (≥ 4 years) |

| Airport congestion driving urban air-mobility demand | +6.8% | North America and EU core, spill-over to APAC megacities | Short term (≤ 2 years) |

| Corporate net-zero mandates pushing zero-emission air travel | +4.1% | Global, emphasis in Europe and North America | Medium term (2-4 years) |

| Rise of vertiport infrastructure PPPs in Asia | +2.9% | APAC core, expansion to MEA | Long term (≥ 4 years) |

| Defense interest in silent VTOL ISR platforms | +2.3% | North America, Europe, selective APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory certification pathways becoming clearer (FAA, EASA)

A decade of uncertainty has ended with the FAA’s Special Federal Aviation Regulation No. 120 and EASA’s expanded Special Condition for VTOL aircraft published in 2024. The documents outline airworthiness criteria, crew licensing, and operational limitations, allowing companies to synchronize flight-test programs and avoid serial redesign.[1]Federal Aviation Administration, “Special Federal Aviation Regulation No. 120,” faa.gov Both texts detail airworthiness, crew-licence, and operations rules, enabling manufacturers to run flight-test programs in parallel instead of redesigning for each region. Airworthiness criteria already issued for Joby’s JAS4-1 and Archer’s M001 indicate that regulators are moving from concepts to type-specific approvals, compressing certification timelines. Streamlined bilateral validation lets builders file once and leverage the ruling in multiple jurisdictions, lowering capital at risk before service launch. These milestones have pushed investors to front-load funding, confident that commercial air-taxi services could start as early as 2026 in the Middle East and by 2028 in the United States.further strengthening the outlook for the eVTOL aircraft market.

Battery energy density breakthroughs hitting 450 Wh/kg lab level

Cell developers have demonstrated 500 Wh/kg packs suitable for flight and more than 700 Wh/kg in controlled laboratory settings, enough to double today’s usable range while cutting structural weight by a third. Aviation-grade batteries must also deliver 10C–60C discharge during take-off; condensed batteries announced in 2025 meet this bar and exceed 1,000 cycles, offering lifecycle parity with turbine engines.[2]magniX, “Samson Aviation-Grade Battery Launch,” magnix.aero The technology jump allows regional routes up to 300 km in temperate climates with reserve margins intact. Higher density translates into lighter structures, larger cabins, or longer ranges, all of which improve ticket economics. With most OEM business plans anchored on reaching 500 Wh/kg by 2027, battery progress is now the pivotal technology driver shaping the electric vertical take-off and landing aircraft market.

Airport congestion driving urban air-mobility demand

Peak-hour commutes from major hubs such as LAX or Dubai International can exceed 90 minutes by road. Route modelling shows an eVTOL hop can slash that to 15–20 minutes, drive 40% higher effective passenger throughput per airport gate, and lower indirect CO₂ emissions for feeder traffic.[3]Dubai Roads and Transport Authority, “AAM Time-Savings Study,” rta.ae Airlines are teaming with eVTOL operators to keep premium passengers inside their networks, creating a captive customer base and predictable load factors. Modelling by state transport planners shows that an eVOL ride becomes cost-competitive once prices fall below USD 90 per seat, a threshold reachable when autonomy occurs. The congestion driver, therefore, intersects squarely with fleet-scale economics and environmental policy, providing another catalyst for the eVTOL aircraft market.

Corporate net-zero mandates pushing zero-emission air travel

The EU Corporate Sustainability Reporting Directive obliges large firms to publish Scope 3 travel emissions, making zero-emission aviation a compliance tool rathe r than a luxury. eVOL aircraft generate no direct exhaust and register 65% lower exterior noise during cruise than helicopters, two attributes that score well in ESG filters. Firms with heavy executive-travel footprints are already signing letters of intent for dedicated, branded air-taxi fleets to showcase carbon leadership. Joby’s 523-mile hydrogen-electric sortie in July 2025 widened the sustainability narrative by proving that regional flights can also be emission-free. The pull from corporate travel budgets gives operators predictable early demand at premium yields, ensuring steady revenue inflow for the electric vertical take-off and landing aircraft market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited lithium supply chain resilience | -6.3% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Public noise-safety perception gap | -4.7% | Global, higher resistance in Europe and North America | Short term (≤ 2 years) |

| High capex of vertiport network build-out | -3.9% | Global, financing challenges in emerging markets | Long term (≥ 4 years) |

| Air-traffic-management software immaturity | -2.8% | Global, complex in dense airspace regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited lithium supply chain resilience

Global lithium demand is projected to rise 700% by 2030, yet refining capacity remains concentrated in a handful of countries that command price and export policy levers. Aviation-grade cells require tighter impurity thresholds and specialised heat-resistant separators, shrinking the pool of suitable suppliers to a few gigafactories. Rapid EV uptake means battery-grade lithium carbonate is already trading twice its 2023 average, eroding cost models for eVTOL operators that expected steady price declines. The US Inflation Reduction Act offers tax credits for domestic content, but mining permits and refinery build-outs take four to six years, leaving a supply gap in the medium term.Any prolonged spike could delay fleet deliveries or force OEMs to redesign around lower-density chemistries, posing a critical challenge to the eVTOL aircraft market.

Public noise-safety perception gap

EASA’s 2021 survey showed that 71% of respondents cited noise and crash risk as major barriers to accepting urban air taxis, even though distributed-propulsion aircraft measure 15 dB quieter than conventional helicopters at 500 ft. NASA studies warn that tonal peaks unique to electric rotors can raise perceived loudness despite lower decibel levels, demanding revised psychoacoustic metrics.[4]NASA Langley Research Center, “Noise Profiles of Distributed-Propulsion Aircraft,” nasa.gov Consumer drone incidents have already primed public scepticism about low-altitude traffic, forcing cities like Paris and Los Angeles to pledge extensive community consultations before issuing route permits. Operators must therefore budget for public-outreach campaigns and dynamic-noise-mapping tools, costs not always factored into early business plans. Delays in local approvals could push route launches beyond published timelines, slowing growth momentum in the electric vertical take-off and landing aircraft market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lift and Propulsion Architecture: balancing simplicity and range

Multicopters held the largest slice of the eVTOL aircraft market in 2025 with a 39.11% share. Still, their forward-flight inefficiency steers commercial focus toward lift-plus-cruise systems growing at a 34.10% CAGR. Lift-plus-cruise aircraft transition to efficient wing-borne flight after take-off, extending range without sacrificing vertical landing capability. Manufacturers such as Joby Aviation have validated 150-mile prototypes, challenging the multicopter's incumbency. For operators, the economics hinge on energy burn per kilometre; as battery density rises, the performance gap will widen further in favour of hybrid architectures, shifting future eVTOL aircraft market share toward range-optimised layouts.

The manufacturer's strategy reflects this pivot. Integrated players are redirecting R&D investment from pure multicopter prototypes to modular tilt-wing or vectored-thrust platforms able to service both short urban hops and longer regional legs. Concurrently, propulsion suppliers are tailoring motor-inverter packages to lighter airframes, creating an incremental upgrade path rather than a wholesale fleet replacement. Over the forecast horizon, a multi-architecture marketplace is expected, but the lift-plus-cruise segment will account for the bulk of incremental eVTOL aircraft market size gains.

By Range: from sub-50 km dominance to cross-regional adoption

Aircraft designed for less than 50 km captured the majority of early orders because initial service models focused on airport transfers. That segment owned 48.62% of the eVTOL aircraft market size in 2025. Yet operators eyeing higher revenue yield are moving to the greater than 150 km class, which is projected to expand at 29.95% CAGR. Route economics show that energy consumed during two vertical cycles can exceed cruise burn on flights shorter than 20 km, eroding profit margin. With commercially available 500 Wh/kg batteries, the break-even distance migrates outward, supporting wider catchment areas and higher seat-kilometre returns.

Longer ranges also unlock medical, tourism, and intercity cargo missions, broadening the eVTOL aircraft market outlook. Demonstrations of hydrogen-electric powertrains have extended achievable range beyond 500 miles without direct emissions, signalling that the next leap in the eVTOL aircraft market will come from regional connectivity rather than purely urban shuttles. Infrastructure planners respond by designing dual-use vertiports adjacent to rail stations and highway hubs.

By Passenger Capacity: the rise of mid-size cabins

Three- to six-seat airframes generated 52.70% of 2025 revenue because they match vertiport pad constraints and deliver a favourable load-factor breakeven. These cabins also optimise pilot wage amortization across multiple passengers. Larger, greater than 6-seat models are now the fastest-growing capacity class at a 33.05% CAGR. They appeal to business aviation customers seeking per-seat parity with regional jets while avoiding slot congestion. Regulatory updates lifting the certified take-off weight cap to 12,500 lbs have opened the door for nine- to twelve-seat platforms, which can spread operating-cost overhead across more seats and drive down ticket prices.

On the other hand, single-seat and dual-seat ultralights will persist in pilot-training and recreational niches but will not materially affect the overall eVTOL aircraft market share. Manufacturers that can derive family platforms—sharing subsystems between 4-seat and 8-seat models—will enjoy scale benefits and stronger bargaining power in supply negotiations.

By Application: urban air taxi still leads but diversification is accelerating

Urban air taxis delivered 63.60% of 2025 sales, concentrated in megacities where a willingness to pay for time savings overlaps with regulatory readiness. However, medical evacuation is rising at a 33.70% CAGR as emergency services recognise that eVTOL aircraft can halve response times during peak traffic. Cargo logistics, tourism, and defense surveillance add incremental demand pools that lower reliance on commuter traffic cycles. Such diversified adoption provides resilience for the eVTOL aircraft market against economic fluctuations. Diversification matters because ticket-price elasticity varies widely across use cases. For example, sightseeing flights can tolerate premium fares, while parcel delivery requires a low cost per kilogram. Operators hedging across multiple verticals are better positioned against macroeconomic downturns that may dampen discretionary travel spending.

Geography Analysis

North America retained the largest regional position in 2025 with 41.20% revenue. Early FAA rule-making, a deep venture-capital base, and defense procurement programs underpin civil and military adoption. The FAA’s Innovate28 roadmap further cements the regulatory runway for scaled services by 2028. Canada is aligning its remotely piloted aircraft regulations to accept eVTOL approvals, while Mexico is negotiating bilateral validation of US type certificates to accelerate market entry. Collectively, these moves reinforce North America’s leadership role in the electric vertical take-off and landing aircraft market.

Europe is next in line. The EASA VTOL regulatory package approved in 2024 sets unified rules across the EU for air operations, licensing, and U-space air-traffic management. Germany and France anchor funding for Olympic-related eVTOL showcases, whereas the UK executes separate but harmonised pathways through the Civil Aviation Authority post-Brexit. State-backed infrastructure grants and zero-emission aviation mandates create a favourable policy stack, explaining why European airlines have already placed triple-digit conditional orders.

Asia-Pacific is the growth engine at a 28.05% CAGR through 2031. China’s low-altitude economy policy targets CNY 1.5 trillion (USD 2.1 trillion) of GDP contribution by 2025, and domestic OEMs have achieved the first mass-production type certificate for an eVTOL passenger aircraft. Japan and South Korea view eVTOL technology as a pillar of national carbon-reduction goals, knitting vertiport networks into existing rail hubs. India’s urban density offers a long-term opportunity; draft rules under the Digital Sky initiative hint at future green corridors linking airports and central business districts.

The Middle East rounds out the high-growth regions. Government financing and streamlined aviation authorities have made Dubai and Abu Dhabi preferred launch markets for US OEMs, accelerating first-mover advantage in commercial operations. In contrast, home markets work through more complex noise-consultation cycles.

Competitive Landscape

The eVTOL aircraft market remains highly fragmented, with more than 800 active programs at end-2024, yet few possess the USD 1-2 billion required for full certification and industrialization. Top players—Joby Aviation, Archer Aviation, Lilium, and Vertical Aerospace—collectively control well under 30% of global firm orders, underscoring low concentration. Competitive strategies fall into three clusters:

- Vertically integrated operators combining aircraft design, ride-sharing platforms, and vertiport management.

- Pure-play manufacturers are partnering for infrastructure while retaining airframe IP.

- Component specialists supplying batteries, flight-control software, or composite structures to multiple OEMs.

Strategic moves in 2025 illustrate consolidation pressure. Joby completed piloted transition flights in Dubai and executed a record 523-mile hydrogen-electric sortie, strengthening its technological moat. Archer secured USD 430 million in equity for a hybrid-propulsion defense variant and co-signed a regulatory alliance spanning five aviation authorities. Lilium won a 100-unit contract from Saudia Group, extending its backlog into the 2030s.Traditional aerospace giants are also circling; Airbus has established a dedicated eVTOL aircraft market division to leverage its composite supply chain. Boeing is investing in autonomous flight software that applies to its rotorcraft portfolio.

Supply-chain leverage is emerging as a decisive advantage. Firms that pre-secured high-purity lithium allocations and proprietary battery chemistries can shield themselves from material price shocks. Conversely, smaller aspirants reliant on spot procurement face escalating cost of capital and may become acquisition targets as the market converges ahead of commercial entry.

EVTOL Aircraft Industry Leaders

Joby Aviation, Inc.

Guangzhou EHang Intelligent Technology Co. Ltd

Archer Aviation Inc.

Vertical Aerospace Ltd.

Volocopter Technologies GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Archer Aviation flew the Midnight in Abu Dhabi, collecting hot-weather performance data for Gulf deployments.

- July 2025: Eve Air Mobility has established a binding framework agreement with Brazilian urban air mobility operator Revo and its parent company, Omni Helicopters International (OHI). The agreement includes the purchase of up to 50 electric vertical takeoff and landing (eVTOL) aircraft, along with entry into service and aftermarket services, valued at USD 250 million.

- July 2025: Joby Aviation logged a 523-mile hydrogen-electric flight, setting a new distance record for zero-emission VTOL, boosting credibility across the eVTOL aircraft market.

- June 2025: Joby Aviation completed piloted full-transition test flights in Dubai, validating operations for a 2026 commercial start.

- January 2025: Skyports Infrastructure received design approval for Dubai’s first commercial vertiport.

- December 2024: Anduril and Archer launched a hybrid-propulsion defense program funded with USD 430 million in equity.

Global EVTOL Aircraft Market Report Scope

| Vector-thrust |

| Multicopter |

| Lift-plus-cruise |

| Tilt-wing/Tilt-rotor |

| Less than 50 km |

| 51 to 150 km |

| Greater than 150 km |

| 1 to 2 Seats |

| 3 to 6 Seats |

| More than 6 Seats |

| Urban Air Taxi |

| Air Cargo/Logistics |

| Military and Government |

| Medical Evacuation |

| Tourism and Recreational |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| Turkey | |

| UAE | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Lift and Propulsion Architecture | Vector-thrust | |

| Multicopter | ||

| Lift-plus-cruise | ||

| Tilt-wing/Tilt-rotor | ||

| By Range | Less than 50 km | |

| 51 to 150 km | ||

| Greater than 150 km | ||

| By Passenger Capacity | 1 to 2 Seats | |

| 3 to 6 Seats | ||

| More than 6 Seats | ||

| By Application | Urban Air Taxi | |

| Air Cargo/Logistics | ||

| Military and Government | ||

| Medical Evacuation | ||

| Tourism and Recreational | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| Turkey | ||

| UAE | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the eVTOL aircraft market today and how fast will it grow?

The eVTOL aircraft market was valued at USD 1.53 billion in 2026 and is forecasted to reach USD 5.47 billion by 2031 at a 28.94% CAGR.

Which region leads the adoption of eVOL aircraft?

North America held 41.20% of 2025 revenue owing to clear FAA regulations and strong defence links, while Asia-Pacific is the fastest-growing at a 28.05% CAGR.

What aircraft configuration is likely to dominate over the next decade?

Lift-plus-cruise architectures are projected to outpace multicopters, growing at a 34.10% CAGR due to superior range and energy efficiency.

What battery technology milestones matter most for commercial viability?

Achieving 500 Wh/kg pack-level energy density with 10C–60C discharge rates and 1,000-cycle life is the threshold for profitable, all-electric regional routes.

What are the main obstacles to large-scale deployment?

Key restraints include lithium supply-chain bottlenecks, vertiport capital costs, and a public noise-safety perception gap that can delay urban approvals.

When are commercial air-taxi services expected to begin?

Pilot routes are targeted for 2026–2028 in cities such as Dubai, Los Angeles, and Paris, contingent on final type certification and vertiport readiness.

Page last updated on: