Aircraft Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

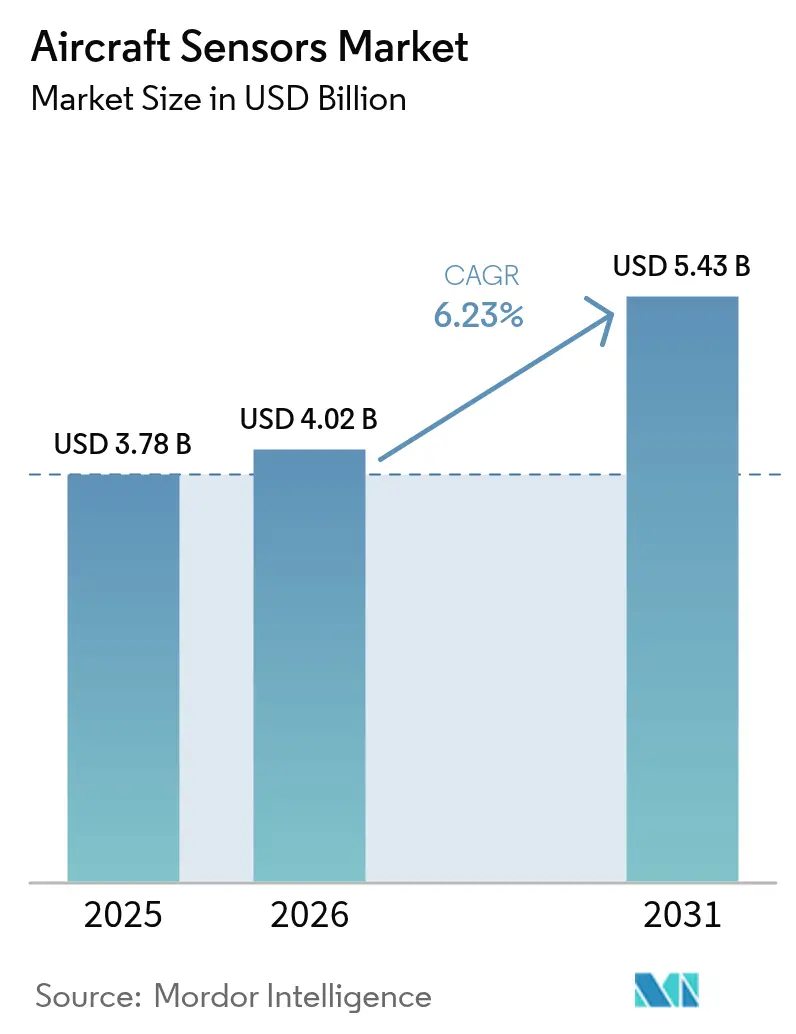

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

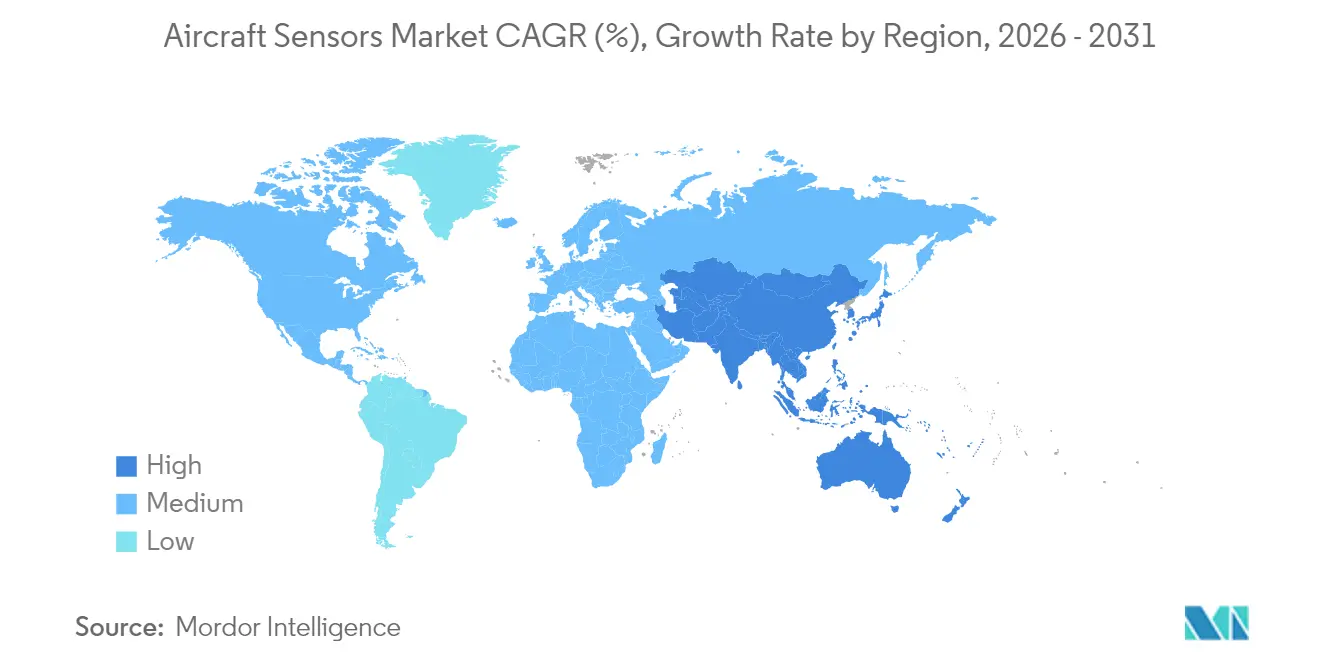

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Sensors Market Analysis by Mordor Intelligence

Aircraft sensors market size in 2026 is estimated at USD 4.02 billion, growing from 2025 value of USD 3.78 billion with 2031 projections showing USD 5.43 billion, growing at 6.23% CAGR over 2026-2031. This trajectory reflects sustained fleet expansion, the migration to fly-by-wire control systems, and rising adoption of predictive maintenance services. Operators are compelled to upgrade sensing suites after the Federal Aviation Administration (FAA) tightened airborne collision-avoidance rules in 2024, while engine makers introduced higher-temperature sensors that support sustainable aviation fuel (SAF) combustion. Radar-based weather and hazard-avoidance products gained momentum as carriers sought to mitigate climate-driven turbulence risk. Military buyers accelerated modernization, funding a USD 270 million infrared upgrade for the F-22 Raptor and expanding orders for autonomous platforms that depend on dense, rugged sensor networks.[1]Source: Federal Aviation Administration, “Equipment, Systems, and Network Information Security Protection,” federalregister.gov Suppliers that combined sensor hardware with cloud analytics captured premium contracts, yet global shortages of aerospace-grade semiconductors stretched lead times and intensified qualification hurdles.

Key Report Takeaways

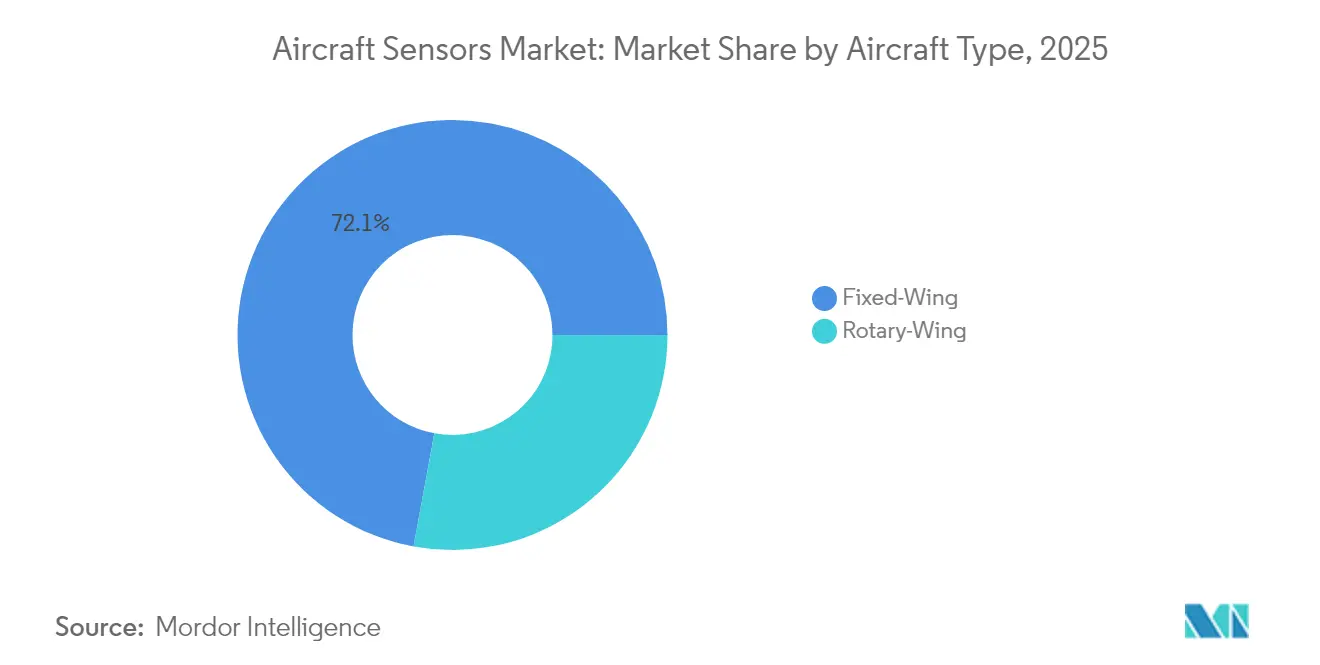

- By aircraft type, fixed-wing platforms held 72.10% of the aircraft sensors market share in 2025, while the military aviation sub-segment is projected to record an 8.18% CAGR through 2031.

- By sensor type, pressure sensors led with 29.20% revenue share in 2025; radar sensors are forecasted to expand at a 9.61% CAGR to 2031.

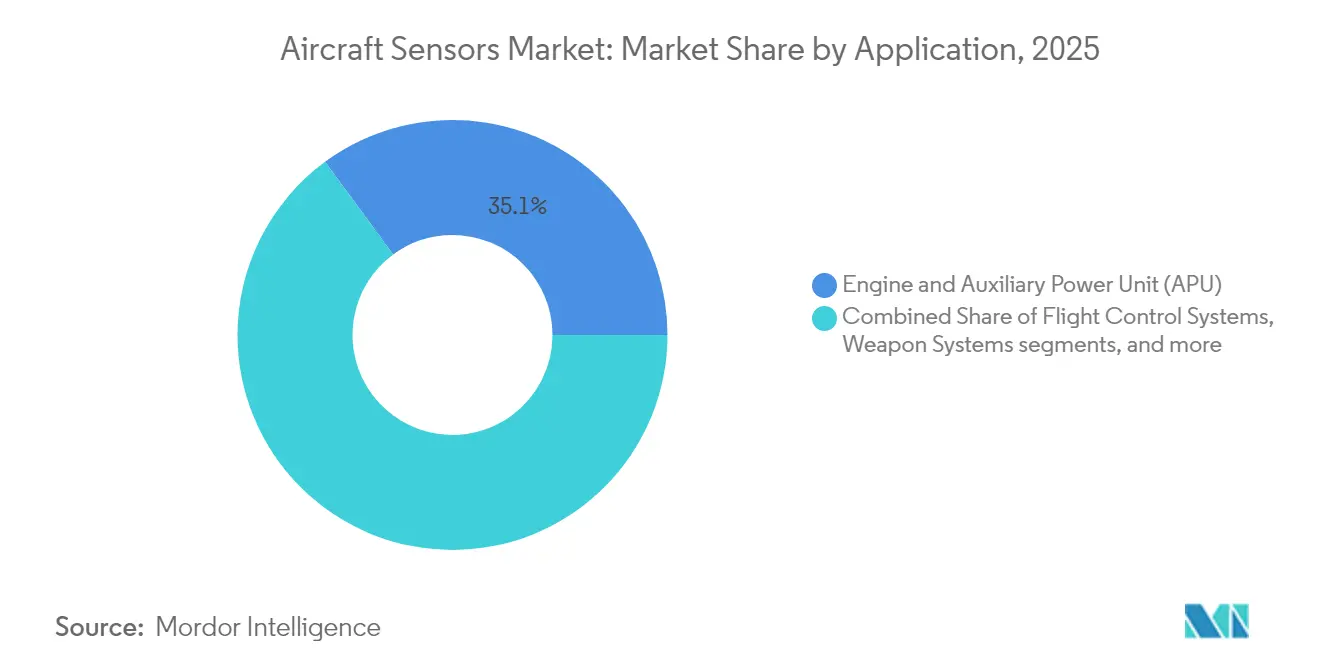

- By application, engine and APU systems accounted for a 35.10% share of the aircraft sensors market size in 2025, whereas flight-control systems are set to grow at a 7.42% CAGR over the same horizon.

- By end user, OEM installations represented 74.65% of total demand in 2025; the aftermarket/MRO segment is advancing at a 7.54% CAGR on predictive-maintenance uptake.

- By geography, North America retained 42.10% of the aircraft sensors market in 2025, but Asia–Pacific is poised for the fastest expansion, with a 7.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated adoption of fly-by-wire and health-monitoring architectures | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Shift to SAF-ready engines driving high-accuracy thermal sensing | +0.8% | Global, led by North America and EU regulatory zones | Long term (≥ 4 years) |

| FAA mandate on airborne collision-avoidance upgrades | +0.9% | North America primary, spillover to international operators | Short term (≤ 2 years) |

| Mainstream drivers-as-a-service platforms for connected fleets | +0.7% | Global, early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Additive-manufactured sensor housings reducing unit cost | +0.5% | Global manufacturing hubs, focused in North America and Europe | Long term (≥ 4 years) |

| Edge-AI-enabled self-calibrating sensors lowering MRO spend | +0.6% | Global, faster uptake in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Fly-by-Wire and Health-Monitoring Architectures

Aircraft programs shifted from mechanical linkages to electronic flight-control systems that rely on triple-redundant sensors for every critical parameter. Collins Aerospace demonstrated its Enhanced Power and Cooling System on the F-35, doubling thermal capacity to support energy-intensive sensor loads.[2]Source: RTX, “Collins Aerospace EPACS Power and Thermal Management System Ready for Aircraft Integration,” rtx.com Airlines integrated structural-health-monitoring suites that cut downtime by 30% when combined with predictive analytics from real-time sensor streams. Sensor fusion software stitched pressure, inertial, and radar feeds into a unified flight picture, improving autopilot responsiveness and enabling single-pilot operations.

Shift to SAF-Ready Engines Driving High-Accuracy Thermal Sensing

SAF blends alter combustor temperature profiles, prompting engine makers to specify thermocouples capable of surviving 1,400°F environments—nearly triple the limit of erstwhile transducers. The US Department of Energy’s SAF Grand Challenge targeted 3 billion gallons of annual output by 2030, stimulating demand for fuel-quality and emissions sensors across supply chains. Airlines are deploying SAF-equipped digital fuel-flow meters and exhaust-gas sensors to verify carbon-reduction claims required for tax credits.

FAA Mandate on Airborne Collision-Avoidance Upgrades

In 2024, the FAA moved from TCAS II to ACAS Xa protocols, obliging carriers to retrofit transponder-linked radar and optical sensors that simultaneously process multilateration, ADS-B, and satellite inputs. EUROCONTROL projected a fivefold decline in mid-air collision risk once ACAS penetrated the fleet. Military adoption surged as the US Army selected Northrop Grumman’s ATHENA sensor to enhance low-altitude threat recognition.

Mainstream Drivers-as-a-Service Platforms for Connected Fleets

Sensor-enabled subscription services accelerated, led by Honeywell’s Ensemble platform, which streamed engine and environmental data to cloud dashboards, slashing unscheduled events by 35%. The Airbus-Delta-GE Skywise alliance added thousands of aircraft, illustrating the economics of outcome-based maintenance contracts. Vendors monetized data through predictive algorithms while guaranteeing dispatch reliability, creating recurring revenue that insulated them from aircraft production cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent supply-chain crunch of aerospace-grade ASICs | -1.1% | Global, acute impact in North America and Europe | Short term (≤ 2 years) |

| Certification backlog slowing new sensor design-ins | -0.8% | Global, concentrated in major certification authorities | Medium term (2-4 years) |

| Cyber-hardening requirements inflating BOM cost | -0.6% | Global, stricter rules in developed markets | Long term (≥ 4 years) |

| Export-control tightening on MEMS IMUs | -0.4% | Global, notably Asia-Pacific supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Supply-Chain Crunch of Aerospace-Grade ASICs

Lead times for radiation-tolerant processors and mixed-signal ASICs lengthened to 40 weeks, overshadowing pre-pandemic norms of 12 weeks. Aviation represented less than 2% of global chip demand, leaving it low on foundry priority lists. Consultancies reported that 66% of aerospace Tier-1s struggled with allocation shortfalls in 2025. Airframers stocked safety-critical devices, yet inventory buffers raised working-capital needs and delayed retrofit schedules.

Certification Backlog Slowing New Sensor Design-ins

New DO-178C and DO-254 rules expanded software and hardware assurance artifacts, pushing average avionics approval cycles to three years. EASA’s revision of Technical Standard Orders aimed to streamline reviews but still demanded extensive documentation for AI-enabled sensors, where algorithms evolve during service. Smaller suppliers struggled to fund test campaigns, delaying the entry of innovative MEMS devices and curbing competitive pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Military Aviation Drives Modernization

Fixed-wing programs dominated demand, capturing 72.10% of the aircraft sensors market share in 2025 on the strength of commercial jet deliveries. The aircraft sensors market size for fixed-wing applications is projected to exceed USD 3.6 billion by 2031 at a 5.69% CAGR. Within that total, military aviation sensors are advancing 8.18% annually as defense ministries retrofit legacy fighters with wide-area infrared, radar, and electronic-warfare suites. Lockheed Martin’s F-22 upgrade illustrated the premium paid for 360-degree passive surveillance.

Rotorcraft and tilt-rotor fleets embraced multispectral cameras and lidar for obstacle avoidance during low-altitude operations. Collins Aerospace’s perception-sensing system enabled automated landing in degraded visual conditions. Cross-pollination of software-defined sensor processors between rotorcraft and fighter jets cut non-recurring engineering costs, compressing time-to-market for export variants. As autonomous cargo drones scale, demand for lightweight inertial and barometric modules will reinforce the expansion of the aircraft sensors market across all airframe classes.

By Sensor Type: Radar Systems Lead Innovation

Pressure devices remained foundational underlying pitot-static, environmental-control, and engine-oil systems with stable, high-volume shipments. Still, radar units registered the steepest growth at 9.61% CAGR as airlines sought advanced turbulence prediction and de-icing advisory features. The aircraft sensors market size for radar is forecast to reach USD 1.34 billion by 2031, reflecting both retrofit and line-fit programs. ACAS Xa requirements further boosted airborne surveillance radars for regional jets.

Edge-AI packages integrated radar, lidar, and optical inputs on a single board, reducing wiring by 20% and enabling condition-based antenna calibration. MEMS accelerometers and proximity detectors benefited from automotive cost curves yet continued to undergo supplemental screening to meet RTCA DO-160 vibration profiles. Temperature and flow sensor designers added cybersecurity wrappers to satisfy imminent FAA network-security mandates, raising bill-of-materials cost but cementing long-term service revenue prospects.

By Application: Flight Control Systems Accelerate Growth

Propulsion-related installations generated the largest revenue pool, accounting for 35.10% of the aircraft sensors market size in 2025 as turbofan makers embedded hundreds of sensors to monitor combustion dynamics and bearing loads. The shift toward geared turbofan and open-rotor architectures introduced higher thermal and vibratory stresses, which required next-generation fiber-optic strain gauges. Meanwhile, fly-by-wire expansion drove a 7.42% CAGR in flight-control-system sensors, a pace that outperformed all other domains.

Digital control-surface actuators demanded position and torque feedback with 10-bit resolution, spurring volume orders for contactless Hall-effect devices. Cabin-environment applications gained from increased humidity-control requirements on long-haul jets, integrating air-quality and particulate sensors derived from industrial cleanroom technology. Landing-gear load sensors migrated to wireless formats to trim wiring weight, while weapons-bay pressure devices incorporated fail-safe redundancy to achieve two-fault tolerance demanded by defense customers.

By End User: Aftermarket Gains Momentum

OEM fitment accounted for 74.65% of 2025 unit shipments as airframes left factories with full sensor suites. However, predictive maintenance platforms triggered a 7.54% CAGR in the aftermarket, pushing operators to retrofit wireless gateway modules that stream health data once aircraft land. The aircraft sensor industry witnessed airlines allocate capital for sensor-as-a-service arrangements that transfer ownership to vendors in exchange for guaranteed availability.

Component pooling widened, and MROs stocked standard-fit MEMS inertial units that cater to multiple fleets, cutting turnaround times. Asia–Pacific’s maintenance spending is projected to reach USD 109 billion by 2043, implying sustained demand for replacement sensors that meet regional Civil Aviation Administration of China guidelines. Independent repair stations invested in automated calibration benches to reduce cycle times from weeks to days.

Geography Analysis

North America retained 42.10% of global demand in 2025, benefiting from major airlines' elevated Pentagon outlays and fleet-modernization campaigns. Domestic sensor suppliers leveraged early engagement with the FAA to shape standards, enhancing export prospects once rules were adopted abroad. Yet the reliance on offshore chip fabrication prompted Washington to allocate USD 52 billion under the CHIPS Act to bolster local microelectronics capacity.

Asia–Pacific recorded the highest growth rate at 7.71% CAGR as carriers expanded narrowbody fleets and governments funded Indigenous sensor programs to mitigate export-control risks. China's aviation services value was forecast to hit USD 61 billion by 2043, eclipsing every single country market. Japanese and Korean manufacturers collaborated on MEMS inertial modules for urban-air-mobility vehicles, while India advanced roadmaps for domestically produced air-data sensors to support regional jet projects.

Europe remained a technology bellwether, enforcing stringent sustainability and cybersecurity rules that fostered sensor innovation. Thales completed the Cobham Aerospace Communications acquisition, reinforcing avionics portfolios that blend sensors and secure datalinks. EASA's harmonization with the FAA facilitated reciprocal acceptance of approvals, but suppliers still navigated separate documentation streams. The region emphasized SAF validation instrumentation and non-CO₂ emissions monitoring as part of its Fit-for-55 climate package.

Regulatory Landscape

Aircraft sensor design-ins and retrofit demand are being shaped by tighter avionics performance and certification specifications across major authorities. In January 2026, the Federal Aviation Administration (FAA) issued an NPRM (26-02) that sets minimum interference-tolerance requirements for aircraft radio altimeters operating in the 3.98-4.2 GHz (Upper C-band) spectrum. This reinforces the need for compliant altimeter sensor hardware and associated avionics integration across affected fleets.

In Europe, the regulatory focus is expanding beyond traditional air transport into new architectures and integrated functions. EASA updated certification and airworthiness building blocks through CS-ACNS Issue 5 (April 2024) for airborne communications, navigation, and surveillance systems, and it closed a March 2026 consultation on a Proposed Special Condition for a Sensor Consolidation Function (M-TS-000577). The updates reflect scrutiny of integrated, software-driven sensing functions. EASA also published CS-MCSD Issue 2 in February 2026 for continuing airworthiness of electric and hybrid propulsion aircraft, which increases requirements for sensor reliability, diagnostics, and documentation across emerging platforms.

Value Chain Analysis

The aircraft sensors value chain begins with upstream materials and electronics (MEMS wafers, ASICs, RF components, connectors, and specialty packaging). It then moves through sensor design, calibration, and environmental qualification (DO-160 vibration/EMI and related test regimes) before integration into LRUs and avionics suites by Tier-1s and airframers. OEM line-fit demand remains dominant, but a growing share of sensor shipments and configuration changes is pulled by heavy checks and retrofit events tied to collision-avoidance, navigation resilience, and health-monitoring architectures.

Qualification-heavy electronics and test capacity remain key constraint points. Lead times for aerospace-grade semiconductors and availability of specialized combined environmental and EMI/EMC test facilities slow ramp-ups, while certification backlogs extend time-to-market for new integrated sensing concepts. Industry consolidation and vertical moves also affect sourcing routes: Woodward signed a definitive agreement in December 2024 to acquire Safran Electronics & Defense’s electromechanical actuation business in the US, Mexico, and Canada. Defense-led integration work, including the USD 270 million F-22 infrared defensive sensor contract (January 2025), further shows how prime contractors and Tier-1s pull sensors through tightly controlled, program-specific supply chains.

Competitive Landscape

The aircraft sensors market displayed moderate concentration. Honeywell, Collins Aerospace, and Thales remained entrenched through extensive certification credentials and vertically integrated offerings that stretch from MEMS fabrication to analytics dashboards. Their scale allowed multi-year fixed-price bids that newcomers could not match. Strategic plays focused on digital services: Honeywell acquired Civitanavi Systems to deepen inertial navigation know-how, while Collins Aerospace launched subscription-based health-monitoring modules for the A320 and B737 families.

Supply-chain resilience became a differentiator. GE Aerospace applied 3D printing to bleed-air valves, yielding 35% cost savings and freeing capacity for chip allocations. Mid-tier firms pursued specialization; Curtiss-Wright secured a USD 80 million IDIQ contract for high-speed data-acquisition recorders supporting the US Air Force flight-test programs. Cybersecurity standards such as the FAA Aircraft Network Security Program favored incumbents able to embed encryption and intrusion detection directly in sensor firmware, erecting entry barriers for low-cost competitors.

White-space opportunities persisted in AI-enabled sensor fusion, additive-manufactured housings, and condition-based lubrication sensors for electric-propulsion architectures. Venture-backed start-ups targeted these niches, yet long certification queues and capital intensity limited their near-term influence. Overall, price competition centered on mature pressure and temperature devices, while high-performance radar and infrared modules commanded double-digit operating margins.

Aircraft Sensors Industry Leaders

Honeywell International Inc.

Safran SA

TE Connectivity Corporation

AMETEK Aerospace, Inc.

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Multi-modal and software-defined sensing is creating whitespace where suppliers can bundle certified hardware with onboard processing and data fusion for mission and safety-critical use cases. Defense modernization is a visible pull: in April 2026, RTX (Raytheon) completed the first flight test of its RAIVEN Staring system on a UH-60 Black Hawk, demonstrating an air-cooled EO/IR sensing package designed for wide-angle situational awareness. In parallel, in July 2026 the U.S. Air Force awarded Northrop Grumman a USD 60.4 million contract to develop the ODIN sensor for LAIRCM, underscoring funded demand for advanced threat detection functions that depend on ruggedized optical and infrared sensing.

Navigation resilience and integrated sensing functions are also moving from concept into demonstrators and certification pathways, supporting opportunities in inertial sensing, sensor consolidation, and GNSS-denied operation. Airbus disclosed testing of radar, LiDAR, and quantum sensing under its Optimate demonstrator work in June 2026, which points to a pathway for obstacle detection and GPS-independent navigation sensor stacks. On the regulatory side, EASA’s March 2026 consultation closure on a Proposed Special Condition for a Sensor Consolidation Function indicates an active framework for certifying consolidated sensing functions. That creates room for suppliers to meet assurance evidence requirements (hardware, software, and cybersecurity) while reducing size, weight, and wiring in next-generation aircraft architectures.

Recent Industry Developments

- June 2026: Safran announced a 120 million euro investment at its Montlucon site to triple production capacity of hemispherical resonator gyroscopes (HRG) by 2032. The capacity expansion supports higher volumes of inertial sensing hardware used in aircraft navigation and stabilization, while strengthening supply assurance for defense and aerospace programs that face long qualification cycles.

- May 2026: AMETEK completed the acquisition of First Aviation Services, adding MRO capabilities and proprietary aerospace components to its portfolio. The move expands AMETEK’s aftermarket reach and creates tighter linkages between component supply, repair throughput, and life-cycle support for sensor-adjacent aircraft subsystems.

- December 2024: Woodward signed a definitive agreement to acquire Safran Electronics & Defense’s electromechanical actuation business in the United States, Mexico, and Canada. The transaction strengthens Woodward’s position in aircraft control architectures where actuation and sensing are engineered together, and it can reshape Tier-1 sourcing and integration pathways for sensor-rich flight control applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the aircraft sensors market covers the revenues earned from sensors installed on aircraft to measure, monitor, and transmit operating parameters for flight safety, control, and maintenance, with values captured in USD across civil and defense aviation.

Scope exclusions: this sizing does not count sensors used only for ground test rigs, space launch vehicles, or airport and runway infrastructure.

Segmentation Overview

- By Aircraft Type

- Fixed-Wing

- Commercial Aviation

- Narrowbody Aircraft

- Widebody Aircraft

- Regional TJets

- Business and General Aviation

- Business Jets

- Light Aircraft

- Military Aviation

- Fighter Aircraft

- Transport Aircraft

- Special Mission Aircraft

- Commercial Aviation

- Rotary-Wing

- Commercial Helicopters

- Military Helicopters

- Fixed-Wing

- By Sensor Type

- Pressure

- Temperature

- Position

- Flow

- Torque

- Radar

- Accelerometers

- Proximity

- Other Sensors

- By Application

- Fuel,Hydraulic and Pneumatic Systems

- Engine and Auxiliary Power Unit (APU)

- Cabin and Cargo Environmental Controls

- Flight Control Systems

- Flight Decks

- Landing Gear Systems

- Weapon Systems

- Others

- By End User

- OEM

- Aftermarket/MRO

- Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Mexico

- Rest of South America

- Europe

- United Kingdom

- France

- Germany

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arbaia

- Israel

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start by setting a clear fact base using public aviation and industrial sources, so later assumptions can be checked and explained on a client call. Common inputs include air transport and traffic indicators from the International Civil Aviation Organization (ICAO) and the World Bank, plus fleet and airworthiness context from the US Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA).

To align demand with real aircraft activity, we also review aircraft delivery and backlog disclosures from airframe makers, defense procurement releases from government budget documents, and maintenance reliability discussions from peer reviewed aerospace journals. For trade flows and localized manufacturing signals, we reference customs and shipment statistics from UN Comtrade and national statistics offices, followed by company annual reports, investor presentations, association websites, and reputed press coverage of avionics and MRO programs. Where needed, paid subscriptions that compile aircraft and engine fleet records, plus patent databases, are used to verify platform timing and technology direction. This list is not exhaustive, and many other sources were referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Next, we validate assumptions through expert interviews and structured surveys across the value chain, including component suppliers, aircraft and subsystem integrators, MRO stakeholders, and aviation program specialists. Since this is a global market, we balance discussions across APAC, EMEA, and the Americas so differences in fleet growth, retrofit intensity, and certification timelines are reflected before final values are signed off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 18% | APAC: 49% |

| Mid tier: 49% | Functional/Unit leaders: 26% | EMEA: 33% |

| Smaller Players: 21% | Managers: 56% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is first reconstructed using a top-down and bottom-up combination, starting from top-down logic that translates aircraft deliveries, in-service fleet by platform, and maintenance activity into a practical sensor demand pool. Since not every aircraft event triggers the same sensor needs, we apply adjustments for new-build fitment rates, retrofit penetration during heavy checks, and typical sensor count ranges tied to airframe and engine monitoring.

To keep totals realistic, outputs are corroborated with selective bottom-up approximations such as sampled supplier revenue splits, channel checks around replacement cycles, and price range checks by sensor class using sampled ASP times volume. Key inputs used in the model include fleet growth by aircraft type, utilization and flight hours, heavy maintenance visit cadence, sensor replacement intervals, and ASP movement (including mix shifts toward smart sensing used for predictive maintenance). For forecasting, scenario analysis is used with primary feedback on aircraft delivery outlook, defense procurement pacing, and certification driven adoption, which helps avoid overstating short-term surges when programs slip.

Data Validation & Update Cycle

We run multi-step checks so the final market values remain consistent with independent aviation signals, and any sharp jump is questioned before sign-off. Outputs are compared against fleet and delivery trajectories, MRO activity indicators, and the implied sensor spend per aircraft so unit, mix, or price mismatches can be spotted.

When variances appear, assumptions are revisited and respondents are re-contacted to confirm whether the change is real or caused by data timing. Reports are refreshed annually, and interim updates are made when material events occur in aircraft programs, supply chains, or regulation. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Aircraft Sensors Market Size Compared With Other Published Estimates

Published market sizes for aircraft sensors can look far apart, even when the topic sounds similar at first glance. Differences typically come from what is treated as sensor value versus broader avionics content, which aircraft types are included, the base year chosen, and how prices and currency conversions are handled.

Airport and runway infrastructure sensing sits outside Mordor Intelligence's scope, and that exclusion can move totals when other sources group ground systems together with onboard aircraft sensing. Gaps also show up when a model relies mainly on a single growth rate, instead of linking demand to fleet-active indicators like aircraft deliveries, in-service utilization, heavy-maintenance cadence, and replacement intervals, which are then cross-checked by region.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.02 B (2026) | |

| Global Consultancy A | USD 3.68 B (2024) | Uses an earlier base year and may smooth retrofit and heavy-check replacement effects, which can reduce the starting value when demand is not normalized to maintenance cadence. |

| Industry Research Group B | USD 7.36 B (2025) | Likely uses a wider definition that bundles adjacent avionics or electronics content with sensors, and it may apply different ASP escalation assumptions that lift the total. |

The table shows that the spread is mainly explained by scope edges, base-year timing, and how replacement and retrofit waves are translated into annual demand. By keeping the inputs tied to fleet size, utilization, and maintenance rhythms, and then checking the implied spend per aircraft, the final number stays transparent and repeatable for planning.

Key Questions Answered in the Report

What is the current aircraft sensors market size and expected growth?

The aircraft sensors market size reached USD 4.02 billion in 2026 and is projected to rise to USD 5.43 billion by 2031, reflecting a 6.23% CAGR.

Which aircraft segment is expanding the fastest for sensor demand?

Military fixed-wing aviation leads, with sensor revenue forecast to climb at an 8.18% CAGR through 2031 as modernization and autonomous-systems procurement accelerate.

Why are radar sensors growing more quickly than other sensor types?

Regulatory shifts toward ACAS Xa collision-avoidance and heightened weather-hazard awareness are driving a 9.61% CAGR for radar sensors, the highest among all categories.

How will supply-chain constraints influence sensor availability?

Extended lead times for aerospace-grade semiconductors are expected to dampen near-term growth by about 1.1 percentage points, pushing suppliers to localize or redesign electronics.

What regions present the largest growth opportunities?

Asia–Pacific is set to expand at 7.71% CAGR, propelled by fleet additions and domestic sensor-manufacturing initiatives aimed at reducing reliance on imported technology.

How are service-based business models changing market dynamics?

Platforms that bundle sensors with predictive-maintenance analytics let airlines shift capital spending to operating expenses, fostering aftermarket growth and recurring revenue for suppliers.

Page last updated on: