Aircraft Autopilot System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

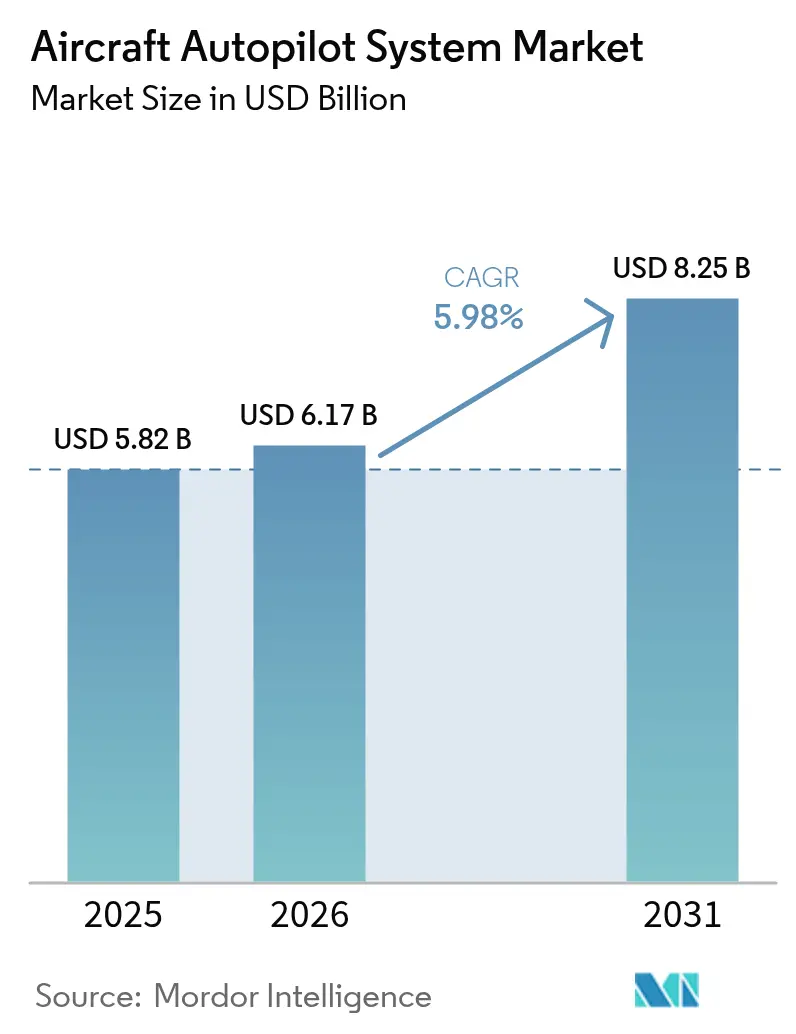

| Market Size (2026) | USD 6.17 Billion |

| Market Size (2031) | USD 8.25 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

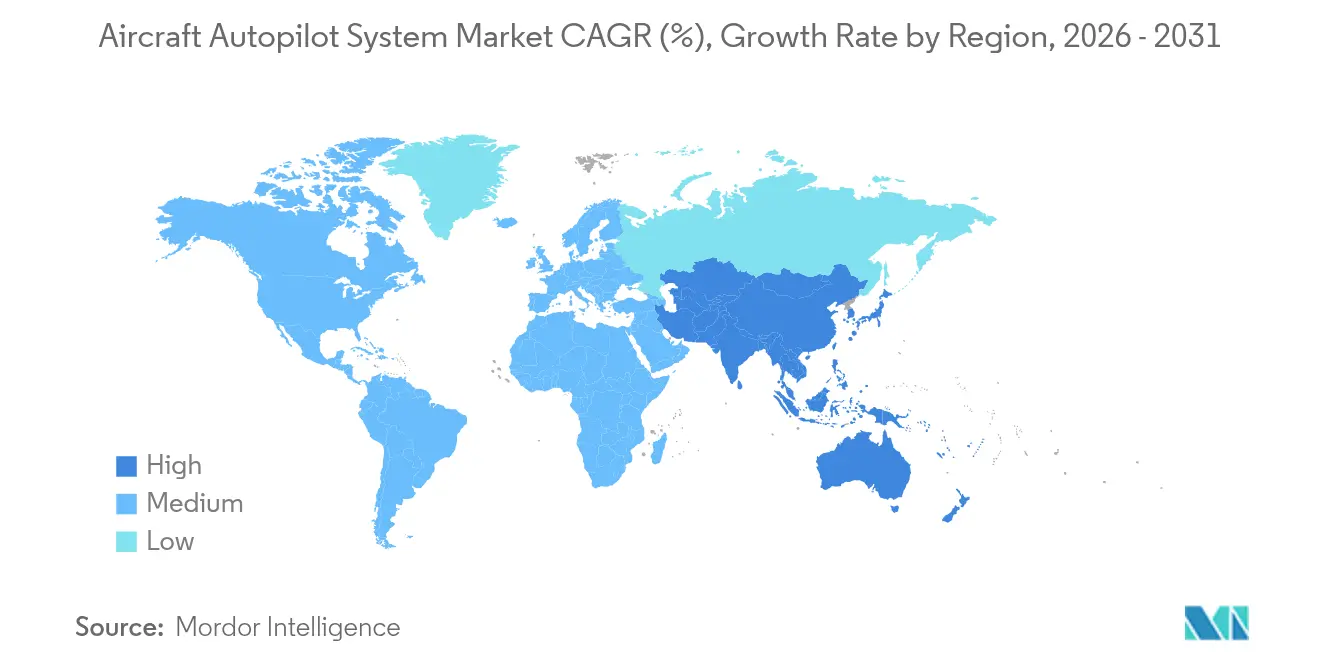

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Autopilot System Market Analysis by Mordor Intelligence

The aircraft autopilot system market size was valued at USD 5.82 billion in 2025 and estimated to grow from USD 6.17 billion in 2026 to reach USD 8.25 billion by 2031, at a CAGR of 5.98% during the forecast period (2026-2031). This trajectory reflects the sector’s pivot toward higher levels of cockpit automation as regulators, airlines, and defense agencies prepare for single-pilot commercial operations and wider unmanned flight adoption. Sustained recovery in commercial aviation, large order backlogs, and avionics modernization programs collectively reinforce demand, while artificial-intelligence-driven contingency management solutions unlock new platform opportunities. Leaders focus on software-defined architectures that extend system life cycles and enable over-the-air feature upgrades. Supply chain constraints in inertial sensors and rising cybersecurity compliance costs remain near-term pressure points. Yet, resilient capital spending by North American and Asia-Pacific operators keeps the aircraft autopilot system market on an expansion path.

Key Report Takeaways

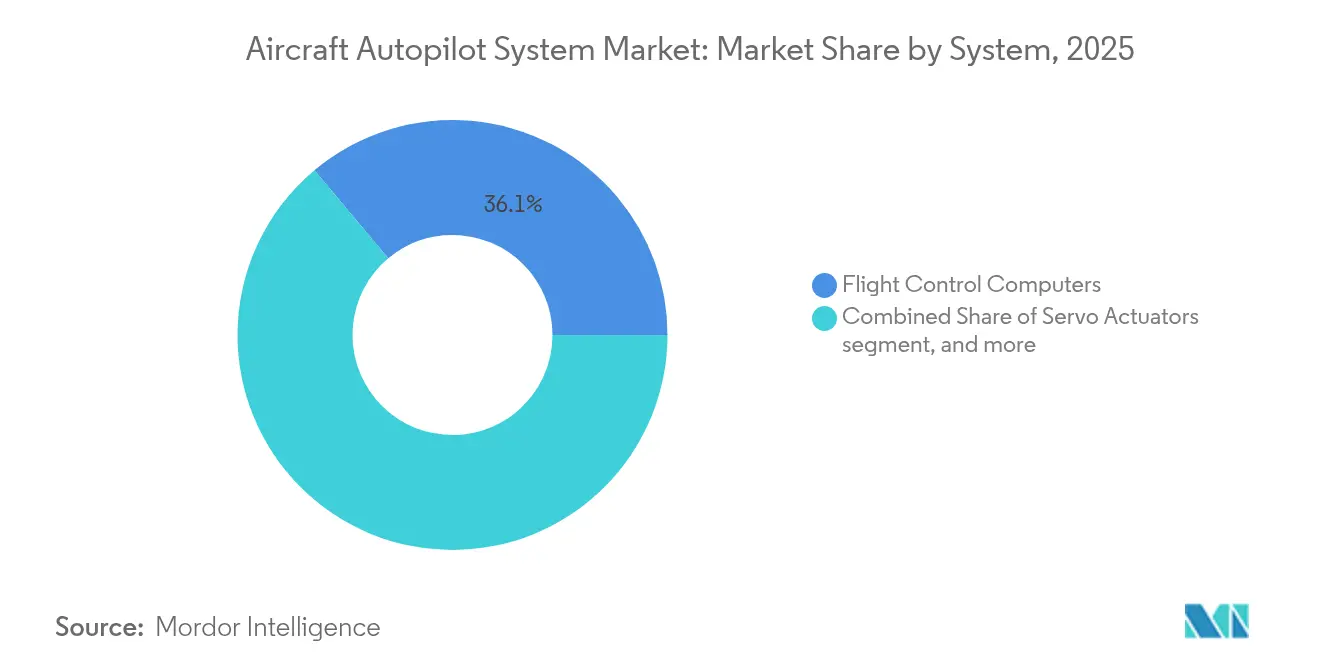

- By system, flight control computers held 36.10% of the aircraft autopilot system market share in 2025, whereas autopilot software suites are advancing at a 9.02% CAGR through 2031.

- By aircraft type, Narrow-body Jets led with 40.35% revenue share in 2025, while unmanned aerial vehicles are projected to expand at a 7.28% CAGR to 2031.

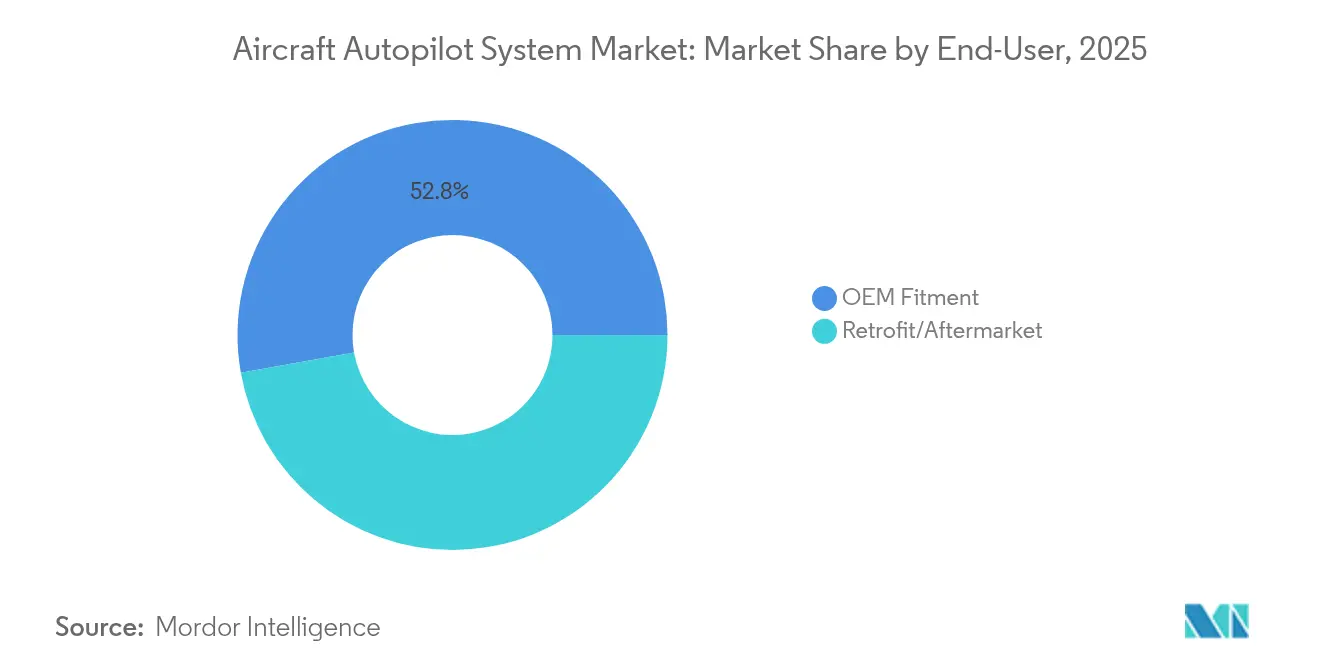

- By end-user, OEM fitment accounted for 52.80% of the aircraft autopilot system market in 2025; retrofit/aftermarket is the fastest-growing channel, with a 6.95% CAGR.

- By geography, North America commanded 42.90% share of the aircraft autopilot system market size in 2025, whereas Asia-Pacific is progressing at an 7.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Autopilot System Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising commercial aircraft deliveries | +1.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing demand for advanced flight automation | +1.5% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Fleet-wide avionics modernization programs | +1.2% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of UAV and UAM operations | +1.0% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| AI-enabled contingency-management autopilots | +0.9% | North America and Europe early adoption, global expansion | Long term (≥ 4 years) |

| Move toward single-pilot commercial ops | +0.8% | North America and Europe regulatory leadership, global follow-on | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Commercial Aircraft Deliveries

Boeing’s plan to raise B737 output toward 42 jets a month and Airbus’s intent to reach 75 A320-family units monthly underpin a steady production ramp that lifts autopilot installations. Asia-Pacific carriers drive a sizable share of these commitments, ensuring that integrated flight management and autopilot suites remain line-fit priorities. Suppliers expand manufacturing capacity for flight control computers and servo actuators to keep pace. The aircraft autopilot system market benefits directly because every forward-fit narrow-body or wide-body requires a certified digital autopilot with growth margins for future software features. The production outlook stabilizes revenue visibility for tier-one avionics vendors through 2030.

Growing Demand for Advanced Flight Automation

The FAA’s More Pilots, More Aircraft, Simplified Certification (MOSAIC) framework paves the way for aircraft that rely on automation layers to guard against loss of control, accelerating the adoption of high-authority autopilots.[1]Federal Aviation Administration, “MOSAIC Draft Rule,” faa.gov Airlines specify weather-linked guidance, satellite-based augmentation, and integrated datalink functions to trim workload on congested routes. Academic research highlights digital flight assistants that contextualize sensor data and present actionable cues, reinforcing the value proposition of enhanced automation. These capabilities expand the aircraft autopilot system market as buyers transition from legacy rate-based systems to attitude-based, AI-supported solutions.

Fleet-wide Avionics Modernization Programs

Carriers extend airframe life by refitting legacy cockpits with touch-screen flight decks and performance-based navigation features. Collins Aerospace’s King Air upgrade package exemplifies how operators migrate to Pro Line Fusion autopilot logic, which cuts pilot workload and meets upcoming airspace mandates. The FAA’s performance-focused certification pathway shortens retrofit lead times, unlocking recurring aftermarket revenue. Mature fleets in Europe and North America sustain the aircraft autopilot system market during soft periods in new aircraft deliveries. Airlines spread capital outlays across multi-year programs, creating predictable demand for modular autopilot LRUs and software licenses.

AI-enabled Contingency-management Autopilots

Partnerships such as Honeywell and NXP Semiconductors integrate high-performance processors that enable real-time machine-learning models to execute weather avoidance, runway overrun prevention, and emergency descent logic. Military projects like Saab’s Centaur demonstrate reinforcement-learning agents maneuvering aircraft without pilot input during complex engagements. Commercial variants focus on autonomous diversion and landing sequences that protect passengers when the crew is incapacitated. These breakthroughs elevate the long-term growth ceiling of the aircraft autopilot system market by opening cargo and air-taxi niches that require limited or zero onboard crew.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High certification and compliance costs | −1.1% | Global, particularly stringent in North America and Europe | Medium term (2-4 years) |

| Cyber-security vulnerabilities in flight-control links | −0.8% | Global, with heightened concerns in defense applications | Short term (≤ 2 years) |

| Shortage of DO-178C qualified engineers | −0.6% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Supply-chain bottlenecks in MEMS/IMUs | −0.5% | Global, with particular impact on Asia-Pacific manufacturing | Short term |

| Source: Mordor Intelligence | |||

High Certification and Compliance Costs

The FAA’s System Safety Assessments rule mandates exhaustive verification to ensure catastrophic failure probabilities remain below 1 × 10-9 per flight hour, driving software validation budgets into the USD 5-15 million range per program.[2]Federal Register, “System Safety Assessments for Transport Category Airplanes,” federalregister.gov DO-178C Level-A compliance requires multiple independent reviews and full code coverage, extending schedules by up to two years. Smaller innovators in the aircraft autopilot system industry often partner with primes to navigate these hurdles, which keeps market entry barriers high and consolidates share among incumbents.

Cyber-security Vulnerabilities in Flight-control Links

A 131% year-on-year rise in aviation cyber incidents heightened scrutiny on autopilot databus integrity. Proposed Equipment, Systems, and Network Information Security mandates force manufacturers to embed encryption, intrusion detection, and secure boot protocols that add hardware cost and verification cycles. Airlines confronted by the 2024 CrowdStrike incident faced network outages that exposed latent risk in connected cockpits, reinforcing procurement criteria that favor hardened solutions. The additional compliance load tempers near-term adoption speed in segments such as unmanned cargo aircraft, yet also encourages sales of upgraded secure flight control computers, indirectly supporting the aircraft autopilot system market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Software-Defined Architecture Gains Momentum

Flight Control Computers retained 36.10% of the aircraft autopilot system market share in 2025 because every commercial transport class aircraft mandates triple-redundant processing for pitch, roll, yaw, and speed commands. Conversely, Autopilot Software Suites are expanding at a 9.02% CAGR as operators shift toward cloud-updateable logic bundles that overlay predictive algorithms on existing hardware. Thales’s PureFlyt platform illustrates this pivot by optimizing real-time trajectories for fuel and noise benefits. The aircraft autopilot system market size for software-centric solutions is projected to reach USD 2.28 billion by 2031, mirroring broader aerospace digitalization. Hardware components like servo actuators and attitude sensors remain essential, yet margins migrate to proprietary code, differentiating approach, go-around, and emergency modes. Vendors invest in DevSecOps pipelines that shorten certification cycles and permit rapid deployment of AI functions, reinforcing the competitive importance of software road maps.

Airlines prefer line-replaceable units that isolate processing from I/O boards, allowing capability upgrades without deep mechanical changes. Open-architecture standards such as FACE in defense aviation and ARINC 653 in civil transport encourage cross-vendor interoperability, expanding addressable volume for niche software developers. As a result, new entrants leverage subscription-based licensing models, while established integrators bundle software warranties with extended service agreements. These shifts foster a layered ecosystem where the aircraft autopilot system market accommodates both tier-one primes and agile code specialists.

By Aircraft Type: UAVs Disrupt Traditional Hierarchies

Narrowbody Jets captured 40.35% of the aircraft autopilot system market size in 2025 on the strength of the A320neo and B737-8 production ramps that each embed autopilots as part of an integrated flight deck. Wide-bodies are recovering in tandem with long-haul traffic but remain below pre-2020 delivery levels. The disruptive force comes from UAVs, whose 7.28% CAGR through 2031 reflects procurement of MALE drones and burgeoning urban air mobility prototypes. UAV autopilots differ in weight, power, and certification path, yet they still rely on tightly coupled inertial and GNSS sensors. Sky-Drones Technologies has adopted 5G links and AI classifiers to navigate contested airspace, broadening its appeal among logistics operators.

Rotorcraft autopilot integration gains momentum following Garmin’s three-axis system for the Airbus H130, which stabilizes hover and cruise modes. Business jet buyers specify auto-throttle and auto-brake functions once reserved for airliners, compressing feature differentiation across aircraft classes. Overall, the aircraft autopilot system market finds new growth lanes as unmanned cargo and passenger concepts mature, challenging legacy suppliers to design lighter, standards-agnostic controllers that still meet transport-category reliability metrics.

By End-User: Retrofit Market Accelerates

OEM Fitment continues to dominate with a 52.80% share in 2025 because every airframe leaves the factory with a baseline autopilot certified for that type certificate. However, airlines and fractional owners are ramping retrofit campaigns that drive a 6.95% CAGR in aftermarket demand. The FAA’s Non-Required Safety Enhancing Equipment (NORSEE) pathway streamlines approvals for digital autopilots, enabling Garmin’s GFC 600 installations across piston and turboprop fleets. This policy shift elevates the aircraft autopilot system market size for retrofits to USD 2.55 billion by 2031. The aging A320ceo and B737-NG aircraft are prime targets for flight director and auto-throttle updates that align with the required navigation performance-authorization required (RNP-AR) routes.

MRO providers partner with avionics OEMs on power-by-the-hour contracts that bundle spares, software updates, and predictive diagnostics. Such models appeal to operators seeking fixed-cost predictability. Emerging leasing pools for autopilot line-replaceable units further reduce downtime during heavy checks. Consequently, the aircraft autopilot system market benefits from a virtuous cycle where retrofit activity extends airframe service life, and extended service life, in turn, demands incremental capability updates.

Geography Analysis

North America led the aircraft autopilot system market with 42.90% revenue share in 2025, supported by robust defense budgets and a quick rebound in domestic air travel. The FAA’s automation and cybersecurity regulation leadership makes the United States an early adopter of advanced autopilot features, reinforcing domestic procurement. Canada’s regional-jet fleet modernization and Mexico’s narrow-body expansion contribute incrementally. High utilization rates accelerate replacement cycles for flight control computers, locking in baseline demand. Honeywell, Collins Aerospace, and Garmin all maintain substantial production and engineering centers in the region, ensuring close alignment with customer requirements.

Asia-Pacific is the fastest-growing territory, advancing at an 7.75% CAGR through 2031. Middle-class air-travel adoption and defense modernization programs centrally drive China and India. Airbus forecasts the global fleet will double to 50,000 aircraft by 2044, with Asia-Pacific supplying most of that increment. Domestic OEMs such as COMAC integrate locally developed autopilot subsystems, while regional airlines launch large retrofit contracts to meet performance-based navigation mandates. Japan and South Korea invest in autonomous UAM ecosystems, exemplified by Thales’s unmanned traffic management testbed in Thailand. Varied certification regimes create customization overhead and foster partnerships between global primes and local system houses, widening the aircraft autopilot system market footprint.

Europe remains a mature yet innovation-centric market. EASA’s acceptance of Garmin Autoland on King Air platforms underscores regulatory openness to high-authority automation. Thales, Safran, and BAE Systems supply integrated autopilot and flight management packages across Airbus and Eurofighter programs. The European Defense Fund channels resources into AI-enhanced resilience features, such as the AIDA project that shields avionics buses from cyber intrusions. Middle East and Africa, while smaller in volume, register steady procurement from Gulf carriers and defense agencies upgrading transport and rotary fleets. Barrier factors include uneven economic conditions and regulatory capacity, yet the region still adds incremental value to the aircraft autopilot system market as wide-body utilization rebounds.

Competitive Landscape

The market remains moderately consolidated, with the top five vendors holding roughly 65% collective revenue, anchored by Honeywell, Collins Aerospace, Safran, Thales, and Garmin. These leaders bundle hardware, software, and lifecycle support into end-to-end offerings that lock in long contracts. Honeywell’s strategic agreement with Bombardier, valued up to USD 17 billion across its term, exemplifies the scale of integrated avionics capture. Collins Aerospace leverages its Pro Line Fusion architecture across business and regional jets, while Safran capitalizes on dual-use capabilities that span commercial liners and combat aircraft.

Second-tier competitors differentiate via niche technologies. Moog supplies high-lift and primary actuation packages for the V-280 Valor Future Long-Range Assault Aircraft, accentuating its strength in electromechanical controls. Avidyne and Dynon Avionics target general aviation with affordable IFR-capable autopilots, using modularity to grow into light-turbine classes. Start-ups like Sky-Drones Technologies and UAV Navigation pursue the UAV and eVTOL segment where weight, cost, and algorithmic sophistication rank higher than traditional certification pedigree. Software-only disruptors license stabilized code that overlays existing flight control computers, broadening competitive intensity within the aircraft autopilot system market.

Strategic alliances and acquisitions accelerate the closure of capability gaps. Honeywell’s planned spin-off of Honeywell Aerospace intends to sharpen focus on autonomy and electrified propulsion by 2026. Regal Rexnord’s collaboration with Honeywell in eVTOL actuation and Curtiss-Wright’s joint cockpit voice recorder line demonstrate convergent interest in urban air mobility systems. These maneuvers aim to secure early mover status in new-generation platforms, thereby amplifying long-run share positions.

Aircraft Autopilot System Industry Leaders

Honeywell International Inc.

Collins Aerospace (RTX Corporation)

Garmin Ltd.

Thales Group

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vertical Aerospace and Honeywell expanded their VX4 eVTOL partnership, targeting certification of flight-critical systems to 1 × 10⁻⁹ catastrophic failure probabilities.

- March 2025: Garmin received EASA approval for Autoland and Autothrottle retrofits on Beechcraft King Air aircraft.

- October 2024: Airbus is developing a new 3-axis autopilot system for the H130 helicopter in collaboration with Garmin. The system will be available in the market in 2025.

- September 2024: Boeing awarded MicroPilot a contract to develop software enhancements for small, unmanned aircraft systems. The contract, signed under the Industrial and Technological Benefits (ITB) Policy, establishes an Investment Framework Agreement between Boeing and MicroPilot, a leading developer of UAV autopilots.

Global Aircraft Autopilot System Market Report Scope

An autopilot system is used to automate guiding and controlling the aircraft. A typical autopilot system can automate multiple tasks, such as attitude and altitude maintenance, rate of climb and descent, and course interception and guidance. To provide a comprehensive outlook, the aircraft autopilot system market encompasses companies offering autopilot and flight director software and hardware components. Market estimates are based on line-fit installations of autopilot systems in the cockpit of new-generation aircraft being procured by airline operators worldwide and do not include retrofitting old-generation aircraft. Furthermore, the report does not consider unmanned aerial vehicles (UAVs) but considers rotorcraft and experimental demonstrators, such as NASA X-57.

The aircraft autopilot system market is segmented by system, application, and geography. The aircraft autopilot system market is segmented by the system into attitude and heading reference systems, flight director systems, flight control systems, and avionics systems. By application, the market is segmented into civil, commercial, and military. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

The market sizing and forecasts for all the segments have been provided in value (USD).

| Attitude and Heading Reference Systems |

| Flight Director Systems |

| Flight Control Computers |

| Autothrottle and Thrust Management |

| Air-data and Inertial Reference Units |

| Servo Actuators |

| Autopilot Software Suites |

| Narrowbody Jets |

| Widebody Jets |

| Regional and Commuter Aircraft |

| Business Jets |

| Helicopters |

| Unmanned Aerial Vehicles (UAVs) |

| Urban Air Mobility/eVTOL |

| OEM Fitment |

| Retrofit/Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System | Attitude and Heading Reference Systems | ||

| Flight Director Systems | |||

| Flight Control Computers | |||

| Autothrottle and Thrust Management | |||

| Air-data and Inertial Reference Units | |||

| Servo Actuators | |||

| Autopilot Software Suites | |||

| By Aircraft Type | Narrowbody Jets | ||

| Widebody Jets | |||

| Regional and Commuter Aircraft | |||

| Business Jets | |||

| Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Urban Air Mobility/eVTOL | |||

| By End-User | OEM Fitment | ||

| Retrofit/Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aircraft autopilot system market?

The aircraft autopilot system market stands at USD 6.17 billion in 2026, with a projected value of USD 8.25 billion by 2031.

Which region holds the largest aircraft autopilot system market share?

North America leads with 42.90% share in 2025, driven by strong defense spending and an early adoption climate for advanced automation.

Which system segment is growing the fastest?

Autopilot Software Suites are expanding at a 9.02% CAGR through 2031 as airlines transition to software-defined avionics architectures.

How quickly is the retrofit market growing?

Retrofit and aftermarket applications are increasing at a 6.95% CAGR as operators modernize in-service fleets with digital autopilots.

What is the biggest restraint to market growth?

High certification and compliance costs reduce speed to market for new entrants and add USD 5 to 15 million to program budgets.

Why are unmanned aerial vehicles important to this market?

UAVs post a 7.28% CAGR because defense and emerging urban air mobility operators require lightweight, AI-ready autopilot solutions.

Page last updated on: